IoT Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

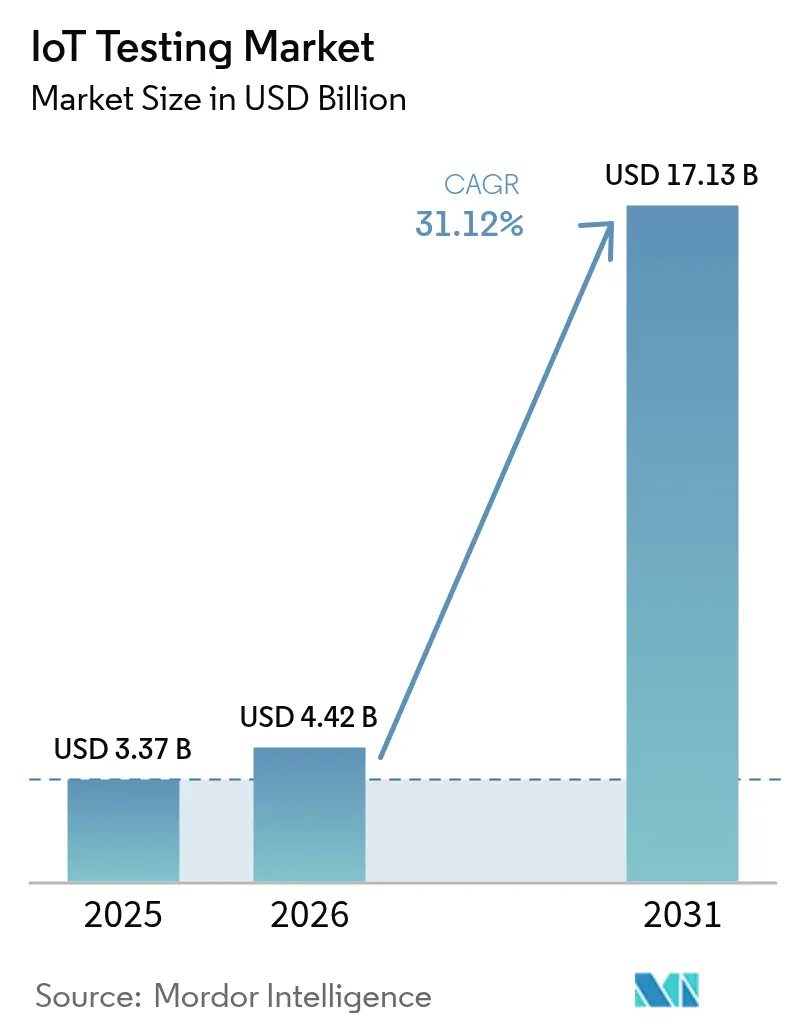

| Market Size (2026) | USD 4.42 Billion |

| Market Size (2031) | USD 17.13 Billion |

| Growth Rate (2026 - 2031) | 31.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IoT Testing Market Analysis by Mordor Intelligence

IoT Testing Market size in 2026 is estimated at USD 4.42 billion, growing from 2025 value of USD 3.37 billion with 2031 projections showing USD 17.13 billion, growing at 31.12% CAGR over 2026-2031.

This rapid expansion mirrors rising digital-transformation targets, stricter cybersecurity mandates, and the swelling universe of connected endpoints that now permeate industrial and consumer settings. Enterprises are migrating from reactive to predictive validation models because a single device failure can stall production lines, trigger safety incidents, and invite regulatory penalties running into millions. Low-latency requirements born of 5G and edge computing are intensifying demand for testbeds that can capture millisecond-level performance variations in mission-critical workloads. At the same time, digital-twin environments are cutting hardware costs by letting developers model full device lifecycles in software while maintaining traceability to real-world conditions.

Key Report Takeaways

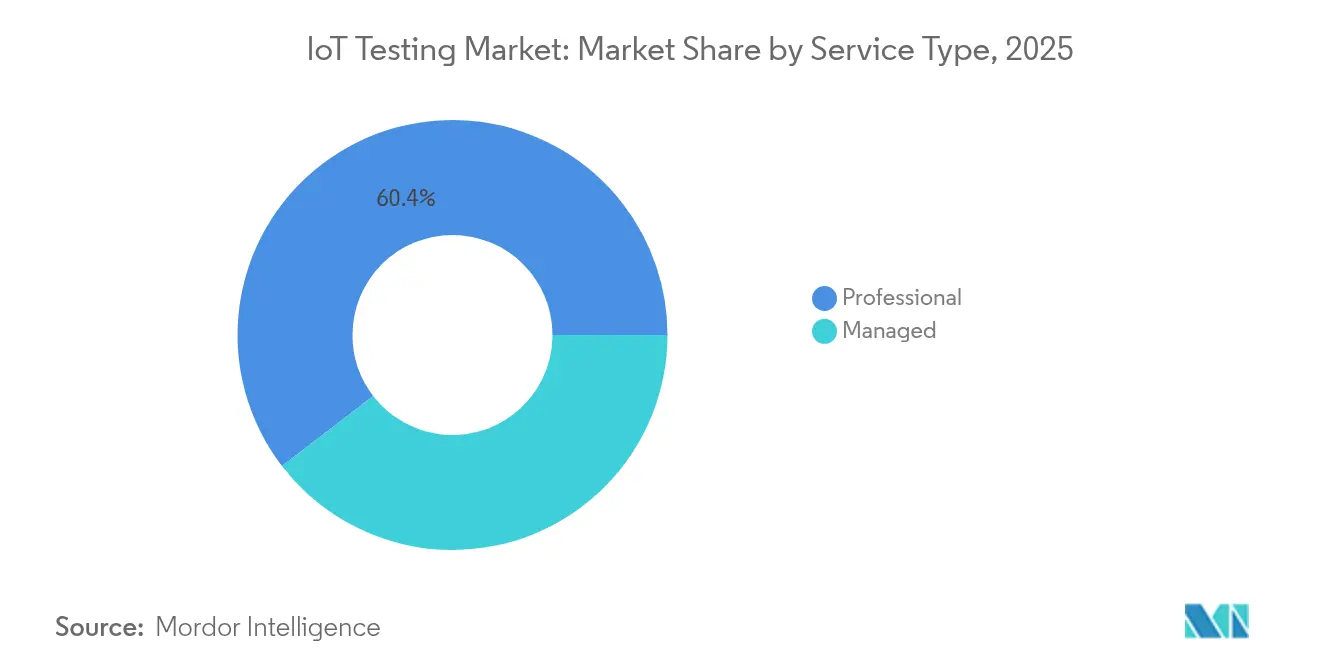

- By service type, professional services held 60.42% of the IoT testing market share in 2025, whereas managed services are projected to expand at an 18.15% CAGR to 2031.

- By testing type, functional testing led with 26.85% revenue share in 2025; security testing is forecast to grow at a 21.95% CAGR through 2031.

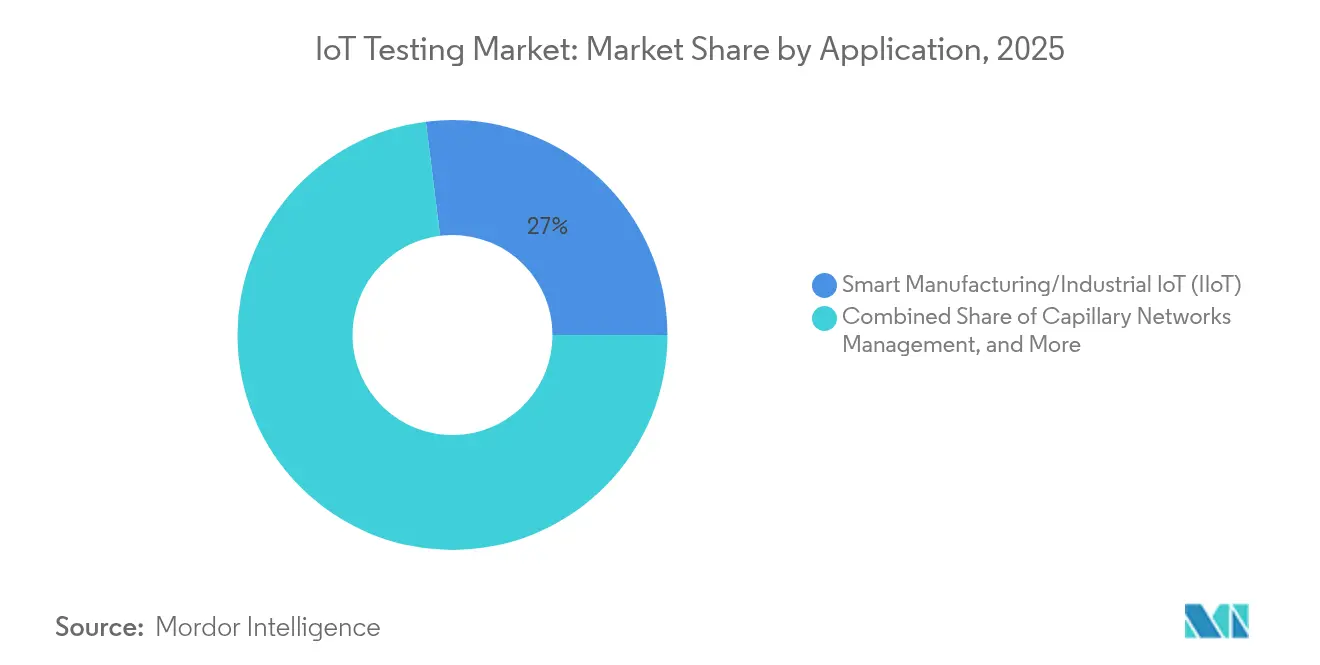

- By application, smart manufacturing/industrial IoT captured 26.98% of the IoT testing market size in 2025, while vehicle telematics is advancing at a 22.35% CAGR to 2031.

- By end-user industry, manufacturing accounted for 27.55% revenue share in 2025; healthcare is expected to post the fastest 18.95% CAGR up to 2031.

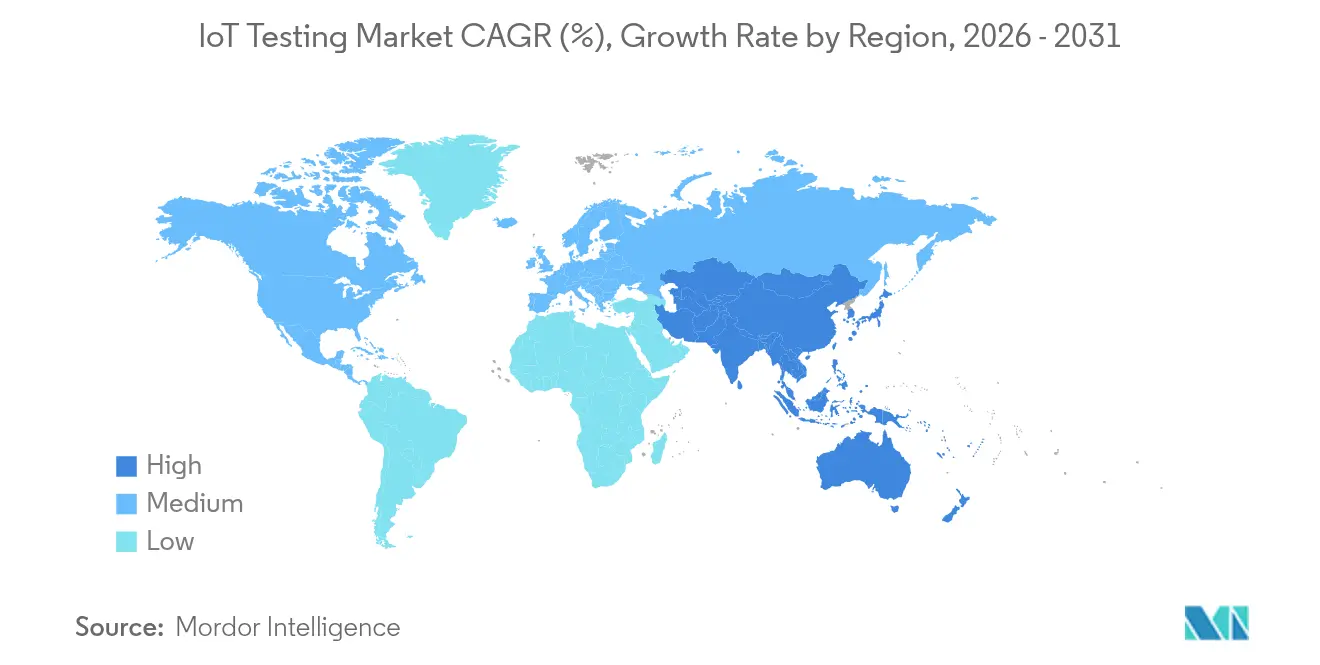

- By region, North America commanded 38.12% of revenue in 2025, and Asia Pacific is set to grow at a 15.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global IoT Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion in connected IoT endpoints | +8.20% | Global, with Asia Pacific leading deployment density | Medium term (2-4 years) |

| Escalating security and privacy regulations | +6.80% | Europe & North America, expanding to Asia Pacific | Short term (≤ 2 years) |

| Shift toward DevOps and continuous testing pipelines | +5.40% | North America & Europe, enterprise-focused | Medium term (2-4 years) |

| 5G/edge-computing driven low-latency use-cases | +4.90% | Global, concentrated in urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosion in Connected IoT Endpoints

China reported 2.57 billion active IoT terminals by August 2024, underscoring the scale shift that now drives exponentially larger test matrices[1]China Daily, “China’s IoT Terminals Exceed 2.5 Billion,” chinadaily.com.cn. A single smart factory can blend Zigbee sensors, LoRaWAN gateways, and 5G RedCap robots, forcing validation teams to assure seamless interoperability across every protocol permutation. Hyundai and Samsung have already proven private 5G RedCap production lines that demand sub-10 millisecond latency verification. As mixed-generation fleets proliferate, each new device SKU multiplies the combinations that must be certified, compelling enterprises to invest in unified test-automation frameworks able to scale without sacrificing coverage. The IoT testing market must therefore support legacy 4G modules and future 5G endpoints in one configurable environment.

Escalating Security and Privacy Regulations

From August 2025, the European Union’s Radio Equipment Directive obliges every internet-connected product to pass cybersecurity conformance testing before sale. The harmonized EN 18031 series now prescribes network protection, data privacy, and fraud-prevention test cases, expanding compliance workloads well beyond functional checks. In the Gulf region, mandatory biometric SIM registration in Saudi Arabia and the UAE is reshaping connectivity-test protocols. Enterprises unable to field in-house security expertise are increasingly outsourcing validation, steering demand toward managed-service providers inside the IoT testing market.

Shift Toward DevOps and Continuous Testing Pipelines

DevOps adoption is relocating IoT validation from discrete project phases to ongoing pipelines aligned with every code commit. Ford integrates digital-twin models of building-management assets at its Dearborn campus, generating real-time sensor replicas for automated regression runs[2]Ford Motor Company, “Digital Twins Drive Energy Optimization,” corporate.ford.com. “Testing-as-code” applies infrastructure-as-code principles so engineers can spin up identical cloud testbeds on demand, drive parallel scenario execution, and receive pass-fail metrics within hours. These efficiencies curb time-to-market and help the IoT testing market align with agile product roadmaps across the automotive, healthcare, and utilities sectors.

5G/Edge-Computing Driven Low-Latency Use-Cases

Researchers in Munich measured standalone 5G New Radio latency below 7 milliseconds, but production deployments must validate performance under congestion, handover, and edge-node failure scenarios. Azure Private 5G Core now offers industrial clients a containerized network slice plus a companion test suite that mirrors real-time traffic loads before rollout. This fusion of telecom and IT disciplines places fresh emphasis on synchronized radio, transport, and application-layer tests extending the IoT testing market beyond traditional device metrics into holistic system validation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising device/protocol complexity | -4.60% | Global, acute in multi-vendor environments | Short term (≤ 2 years) |

| Lack of global interoperability standards | -3.80% | Fragmented across regions and industries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Device/Protocol Complexity

Contemporary deployments mix Wi-Fi 6E sensors, Bluetooth 5.4 beacons, LoRaWAN meters, NB-IoT trackers, and 5G RedCap modems, each demanding distinct tooling. Automotive semiconductor content is projected to hit USD 1,200 per car by 2030, doubling validation points across control units and telematics gateways. Every new protocol stacks onto the existing matrix, lengthening test cycles and challenging resource-constrained labs. Unless automation, virtualization, and AI-enabled prioritization shrink cycle times, this complexity could slow spend within the IoT testing market.

Lack of Global Interoperability Standards

ETSI EN 303 645, US NIST 8259A guidelines, and emerging Chinese smart-city benchmarks all diverge, forcing multinational vendors to certify identical devices three separate times. Redundant testing inflates costs, extends release dates, and limits SMEs’ ability to scale internationally. Harmonization initiatives are underway, yet near-term fragmentation continues to dampen economies of scale for the IoT testing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Professional Services Drive Complex Validations

Professional services dominated 2025 revenue with a 60.42% stake as enterprises leaned on external specialists for multifaceted protocol, security, and compliance needs. Their strength stems from deep benches versed in 5G, RedCap and EU cyber-conformance testing. Managed services, however, are forecast to rise 18.15% annually because manufacturers and fleet operators prefer subscription contracts that guarantee 24/7 lab capacity. HCL Technologies reported USD 13.3 billion FY24 revenue, attributing strong growth to its managed testing portfolios. This transition is redefining delivery models across the IoT testing market and widening demand for fully outsourced validation centers.

The IoT testing market size for managed services is projected to jump from USD 1.33 billion in 2025 to USD 3.63 billion by 2031, mirroring the steep complexity curve that favors dedicated external labs. Global system integrators are investing in remote-accessible device farms so clients can queue tests around the clock without shipping hardware.

By Testing Type: Security Testing Emerges as Growth Leader

Functional validation retained the largest 26.85% revenue slice in 2025 because projects still begin with connectivity and data-flow checks. Nevertheless, security testing is expected to post a 21.95% CAGR through 2031. The IoT testing market must now execute penetration simulations, firmware-integrity scans, and encrypted-channel evaluations aligned with EN 18031 and US FDA pre-market submissions. Applus+ opened a new European cyber-lab in 2024 to fast-track ETSI 303 645 certification demand.

Security services alone could capture 30.20% IoT testing market share by 2031 as regulatory fines push device makers to bake validation into every build. In parallel, performance-stress and network-handover tests stay critical for 5G URLLC scenarios, keeping them relevant, though not as fast-growing.

By Application: Vehicle Telematics Accelerates Past Manufacturing

Smart manufacturing/industrial IoT applications owned 26.98% of 2025 revenue thanks to proven ROI in downtime reduction and predictive maintenance. Thyssenkrupp Materials documented a 52% fall in unplanned stoppages once connected-equipment monitoring went live, underscoring why factories prioritize exhaustive test coverage. Yet vehicle telematics is tracking a blistering 22.35% CAGR, fueled by eSIM rollouts and over-the-air update mandates in Europe and North America. Geotab’s integration program with Volkswagen Group is one illustration of the data volumes and security layers now requiring validation.

Consequently, the IoT testing market size allocated to automotive applications could surpass USD 4.38 billion by 2031, bringing strict ISO 21434 and UNECE R155 cybersecurity clauses into mainstream lab routines.

By End-User Industry: Healthcare Disrupts Manufacturing Leadership

Manufacturing held 27.55% of the 2025 demand as Industry 4.0 programs matured, integrating sensors across conveyors, robots, and warehouse systems. However, remote-patient monitoring and connected therapeutics mean healthcare is set to expand at 18.95% CAGR. The Monit4Healthy project combines multi-sensor fusion with edge analytics for continuous vital tracking and exemplifies the depth of validation now essential for medical devices.

This shift signals rising regulatory oversight from the US FDA’s cybersecurity guidance to the EU MDR, compelling healthcare OEMs to contract specialized partners inside the IoT testing industry for lifecycle-long compliance support.

Geography Analysis

North America led with 38.12% revenue in 2025 as enterprises adopted DevOps pipelines that embed testing from design through production. San Antonio’s SmartSA initiative demonstrates municipal-grade pilots where every lamp-post sensor must clear interoperability and security gates before field deployment. The IoT testing market benefits from established certification ecosystems and well-funded aerospace, automotive, and industrial-automation clients.

Asia Pacific is predicted to post the fastest 15.32% CAGR. China’s Xiong’an 10 Gbps backbone and Beijing’s vehicle-road-cloud pilots elevate demand for massive-scale conformance labs. Japan’s Society 5.0 and South Korea’s USD 101 million national smart-city fund are adding thousands of devices that must be profiled under region-specific telecom and privacy rules. The IoT testing market size in Asia Pacific could cross USD 5.23 billion by 2031 as local vendors integrate cloud-native automation.

Europe maintains solid growth anchored in its rule-first posture. Radio Equipment Directive cybersecurity clauses require third-party labs to run penetration tests before CE marking. Smart-meter rollouts hit 60% for electricity and 45% for gas in 2023, driving sustained validation work for utility suppliers. Nordic telcos are opening shared 5G IoT labs, exemplified by Telenor’s Karlskrona facility that grants global device makers plug-and-play access to Swedish networks. These frameworks ensure the IoT testing market in Europe remains compliance-centric and resilient.

Regulatory Landscape

Cybersecurity and privacy compliance is emerging as a primary market-access gate for connected products, expanding mandatory test scope beyond RF and basic functional checks into software assurance, vulnerability handling, and system-level conformance. In Europe, the Radio Equipment Directive cybersecurity provisions referenced in the report take effect from August 2025 for internet-connected radio equipment, anchored by the EN 18031 series that prescribes network protection, privacy, and fraud-prevention test cases. The EU Cyber Resilience Act (Regulation 2024/2847) also introduces horizontal cybersecurity requirements for products with digital elements, with incident and vulnerability reporting obligations becoming active from September 11, 2026. This increases the need for evidence-ready security testing and documentation across device, app, and cloud components.

In the United States, federal cybersecurity baselines for IoT devices continue to formalize through NIST guidance that procurement and assurance programs reference. In June 2026, NIST released the initial public draft of SP 800-213r1 (comment period open through August 24, 2026), updating how IoT product cybersecurity requirements are framed for federal agencies and their suppliers. It also reinforces demand for repeatable security test methods and artifacts. The UK tightened its posture via the Radio Equipment (Amendment) (Northern Ireland) Regulations 2025 (in force December 16, 2025), aligning essential cybersecurity requirements for radio equipment with EN 18031-1/-2/-3, which increases the role of accredited test labs and harmonized test suites in go-to-market workflows.

Value Chain Analysis

The IoT testing value chain covers device and module OEMs, connectivity chipset and protocol-stack suppliers, test equipment manufacturers (RF, OTA, network emulation, and security), cloud and DevOps toolchain providers, and independent test labs and certification bodies. Standards bodies and certification ecosystems shape test plans and acceptance criteria, including ITU-T and ISO/IEC frameworks and evaluation indicators, as well as industry programs such as GCF that formalize end-product certification steps. In January 2026, ITU-T approved Recommendation Q.4080, a framework for testing and monitoring IoT devices and networks, and ISO/IEC published ISO/IEC 30187:2026 (May 2026), defining evaluation indicators for IoT systems and helping buyers and labs align performance, reliability, and security validation.

Midstream, solution design and integration increasingly combine digital-twin testbeds, CI/CD automation, and device farms with specialized wireless and OTA capabilities for new connectivity. Partnerships among instrumentation vendors and ecosystem specialists accelerate test readiness for emerging standards, including Anritsu and Bluetest (July 2025) on OTA measurement for 5G RedCap IoT devices, and Anritsu with Microwave Vision Group (August 2025) on OTA testing for Non-Terrestrial Network IoT and mobile devices. Downstream, compliance and certification drive recurring demand through managed services and recognized test organizations, with labs translating standards (for example, ETSI EN 303 645 and associated IoT security specifications) into repeatable conformance, interoperability, and penetration-test workflows needed by OEM release cycles across industrial, automotive, and smart-building deployments.

Competitive Landscape

The IoT testing market is moderately fragmented. IBM, Keysight Technologies, HCL Technologies, and Accenture head the global tier, holding diversified device, network, and application test portfolios. Keysight shifted the landscape in March 2025 by acquiring Spirent Communications for USD 1.46 billion, then divesting Ethernet and security assets to VIAVI Solutions for USD 410 million to clear regulators. This maneuver consolidates 5G, cloud, and automotive test assets under one umbrella, accelerating integrated-platform demand.

Vendors now compete on AI-driven automation that slashes scenario-generation time. Rohde & Schwarz patented a context-aware engine that auto-selects required test suites based on detected traffic patterns, pointing toward self-optimizing labs. Edge-computing validation and 5G RedCap conformance are current white-space arenas where niche specialists attract premium valuations. Cloud-native upstarts offer containerized, pay-as-you-go environments appealing to start-ups and SMEs who cannot finance dedicated hardware labs. Continued acquisitions are likely as buyers seek one-stop partners able to traverse device, network, cloud, and application layers within the IoT testing industry.

IoT Testing Industry Leaders

Novacoast, Inc.

Keysight Technologies, Inc.

Praetorian Security, Inc.

Apica Systems

AFour Technologies Pvt. Ltd. (ACL Digital)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Security labeling and compliance programs are creating whitespace for managed, repeatable security-testing services that bundle evidence, documentation, and continuous re-testing across the product lifecycle. In April 2026, ioXt Alliance was selected as Lead Administrator for the US Cyber Trust Mark program, bringing more consumer IoT devices into structured security evaluation. This also creates demand for standardized test artifacts that manufacturers can reuse across models and firmware releases. ISO/IEC 27404:2025 further supports a labeling-oriented approach by defining a cybersecurity labeling framework for consumer IoT products, which can increase the need for lab readiness, vulnerability-test coverage, and conformity documentation across regions.

Interoperability at scale is also shifting into procurement and deployment requirements, particularly in smart buildings and commercial environments where multi-vendor ecosystems are common. In June 2026, the Connectivity Standards Alliance released Product Security Certification 1.1, expanding certification scope from devices to full IoT systems (including apps, gateways, and remote processes) with two assurance levels. That broadens the addressable test scope for vendors able to validate end-to-end behavior and security. The same month, Silicon Labs demonstrated a 200-node Matter-over-Thread validation network in a real-world environment, highlighting the operational need for large-scale, environment-realistic testbeds that stress multicast, multi-hop, and fleet-level updates rather than single-device functional checks. These developments favor providers that can combine protocol interoperability testing, system security assurance, and automated regression in DevOps pipelines for mixed fleets across industrial IoT, smart building, and vehicle telematics deployments.

Recent Industry Developments

- March 2026: Keysight Technologies joined the NSS Labs AI Protection Systems (AIPS) security testing initiative as a lead partner. The move expands third-party evaluation capacity for AI-related security controls used in connected and edge systems, aligning with rising demand for security testing alongside functional and network validation.

- November 2025: Keysight Technologies reported its Device Security Lab in Delft, Netherlands, was accredited as an IT Security Evaluation Facility (ITSEF) under the EU Cybersecurity Certification Scheme on Common Criteria (EUCC). The accreditation strengthens Keysight's role in higher-assurance device evaluations and supports customers building conformity evidence for European cybersecurity requirements.

- April 2024: Keysight Technologies added post-quantum cryptography testing capabilities to the Keysight Inspector platform, including testing for the Dilithium algorithm. This broadened security validation coverage for long-lifecycle connected devices where cryptographic agility is becoming part of product risk management and compliance planning.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The IoT testing market is defined as the revenue earned from services that validate and verify connected devices, gateways, networks, and the supporting software, so IoT solutions work as intended in real-world conditions.

Scope exclusions: This sizing excludes in-house QA costs that are not billed as testing revenue and also excludes general IT outsourcing that is not specific to IoT test work.

Segmentation Overview

- By Service Type

- Professional

- Managed

- By Testing Type

- Functional Testing

- Performance Testing

- Network Testing

- Compatibility Testing

- Security Testing

- Usability Testing

- By Application

- Smart Building and Home Automation

- Capillary Networks Management

- Smart Utilities (Energy / Water)

- Vehicle Telematics and Connected Vehicles

- Smart Manufacturing / Industrial IoT (IIoT)

- By End-user Industry

- Retail

- Manufacturing

- Healthcare

- Energy and Utilities

- IT and Telecom

- Government and Smart Cities

- Transportation and Logistics

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the model and to align on common terms used in IoT quality and assurance work. We referenced public sources such as NIST guidance on IoT security, FCC and ETSI material tied to device communications, ISO and IEC standards summaries, and indicators from ITU and OECD on connectivity and digital adoption.

To keep the model grounded, we also reviewed company annual reports, investor decks, and trusted press releases to understand how testing is packaged (managed versus professional) and where demand is strongest by industry. A paid subscription covering company financials, along with a separate patent database, was used selectively to validate growth themes and to avoid missing key service lines. These sources are illustrative, and many other public documents were also reviewed to support collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with testing service providers, system integrators, IoT platform teams, and end users who procure testing for connected products. We covered demand signals across APAC, EMEA, and the Americas so assumptions on adoption, pricing, and test intensity could be checked against what teams are actually budgeting for and delivering.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 13% | APAC: 42% |

| Mid tier: 46% | Functional/Unit leaders: 43% | EMEA: 31% |

| Smaller Players: 20% | Managers: 44% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where overall software and digital assurance spend was filtered down to IoT-specific testing through adoption and intensity ratios by industry and region, and then split into managed and professional service revenue. To keep the totals realistic, we corroborated outputs with selective bottom-up checks like sampled price-per-engagement ranges, delivery capacity signals, and rollups from a limited set of supplier revenue disclosures.

Key inputs included IoT device and connection growth, enterprise rollout pace for connected products, the share of projects requiring security and interoperability testing, typical test cycle frequency after firmware updates, and regional wage and billing-rate differences that shift service pricing. Forecasts leaned on scenario analysis, where device growth, compliance pressure, and security incident trends were varied, then validated against expert expectations before finalizing the forward curve. Where direct vendor splits were missing, gaps were handled by using peer benchmarks within the same service type and adjusting for regional and industry mix so the implied pricing stayed consistent.

Data Validation & Update Cycle

Outputs were triangulated across multiple signals, including implied testing spend per active IoT deployment, service type mix checks, and region-level comparisons against digital transformation budgets. When a number moved outside expected ranges, we re-checked the assumptions behind adoption, pricing, or service scope, and, when needed, re-contacted respondents to confirm whether a real market shift had occurred.

Before sign-off, the model goes through a multi-step review where another analyst checks formulas, unit consistency, and year-over-year logic so errors are caught early. The report is refreshed annually, and material events such as major regulation changes or step changes in IoT security requirements trigger interim updates. Right before delivery, a final pass is completed so the numbers reflect the latest available inputs.

Mordor Intelligence's IOT Testing Market Size Measured Against Other Published Estimates

Published IoT testing numbers can look far apart because firms do not always count the same services, time periods, or buyer spend categories, even when the topic label is identical. Differences also come from how each model treats pricing progression and how often assumptions are refreshed when device volumes and security needs change.

The biggest gap driver is whether testing tools and broader software QA revenue are blended into the total, where Mordor Intelligence counts only IoT testing service revenue tied to defined test activities (for example, functional, performance, network, compatibility, usability, and security testing) and then validates pricing and mix through primary checks before locking the 2026 base.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.42 B (2026) | |

| Global Market Tracker A | USD 2.15 B (2025) | Uses an earlier base year and often reports factory-gate style totals that can understate service-only revenue when managed testing is bundled under broader IT services, which shifts the counted spend away from dedicated IoT testing lines. |

| Industry Research Desk B | USD 2.18 B (2025) | Starts from a different base year and may apply aggressive expansion assumptions over a longer horizon, while service scope and regional mix differences can keep near-term totals lower than a model that is anchored on current engagement pricing and test intensity. |

The table shows that year selection and what gets counted as IoT testing are doing most of the work behind the spread. By keeping the scope tied to billed IoT testing services and checking the output against adoption, pricing, and service-mix signals, the final number stays traceable to inputs that can be reviewed and repeated.

Key Questions Answered in the Report

What is the current size of the IoT testing market?

The IoT testing market size is USD 4.42 billion in 2026.

How fast is the IoT testing market expected to grow?

It is projected to register a 31.12% CAGR, reaching USD 17.13 billion by 2031.

Which service model is expanding fastest?

Managed services are forecast to grow at an 18.15% CAGR as enterprises outsource complex validation work.

Why is security testing gaining momentum?

Cybersecurity mandates such as the EU Radio Equipment Directive require mandatory conformance, driving a 21.95% CAGR for security testing.

Which region offers the strongest growth outlook?

Asia Pacific is expected to advance at a 15.32% CAGR, supported by large-scale smart-city programs in China, Japan and South Korea.

How will 5G influence IoT testing demand?

5G and edge computing introduce sub-10 millisecond latency targets, compelling investments in advanced testbeds that simulate real-world network dynamics.

Page last updated on: