IoT Data Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

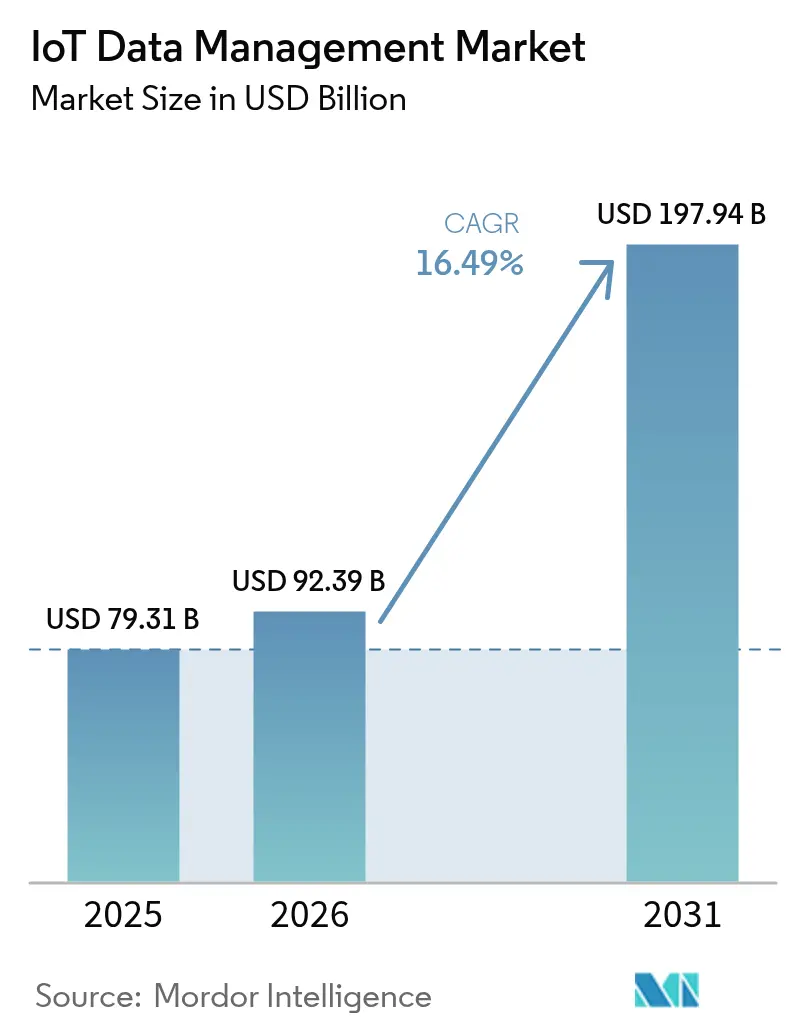

| Market Size (2026) | USD 92.39 Billion |

| Market Size (2031) | USD 197.94 Billion |

| Growth Rate (2026 - 2031) | 16.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IoT Data Management Market Analysis by Mordor Intelligence

IoT Data Management Market size in 2026 is estimated at USD 92.39 billion, growing from 2025 value of USD 79.31 billion with 2031 projections showing USD 197.94 billion, growing at 16.49% CAGR over 2026-2031.

Strong demand stems from swelling connected-device volumes, the move toward edge-enabled architectures, and the rise of cloud-native analytics that turn raw telemetry into high-value insights. Predictive maintenance, asset-health optimization, and cross-enterprise data-sharing are accelerating vendor revenues as enterprises modernize legacy stacks and monetize sensor data. Intensifying merger activity, such as Cisco’s USD 28 billion Splunk purchase, is sharpening competitive differentiation around unified ingestion, governance, and AI-ready analytics. [1]Cisco, “Cisco Completes Acquisition of Splunk,” splunk.com Meanwhile, hybrid deployment models, 5G-powered low-latency networks, and regulatory pressure for airtight data governance are shaping investment priorities across industries and regions.

Key Report Takeaways

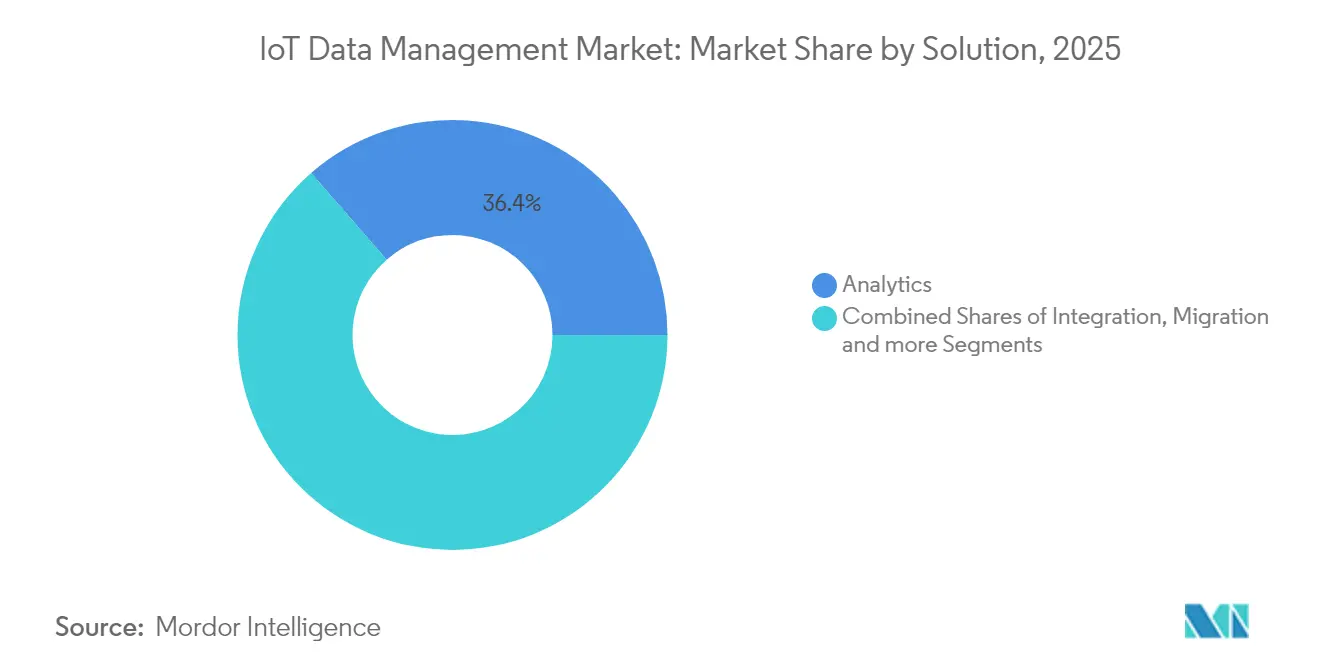

- By solution, analytics led with a 36.42% revenue share in 2025, while stream processing is projected to expand at a 16.86% CAGR through 2031.

- By deployment model, cloud held a dominant 70.35% share in 2025; hybrid architectures are the fastest-growing at 17.12% CAGR to 2031.

- By data type, time-series workloads accounted for 48.20% of processing demand in 2025, whereas unstructured data management is set to rise at a 16.88% CAGR.

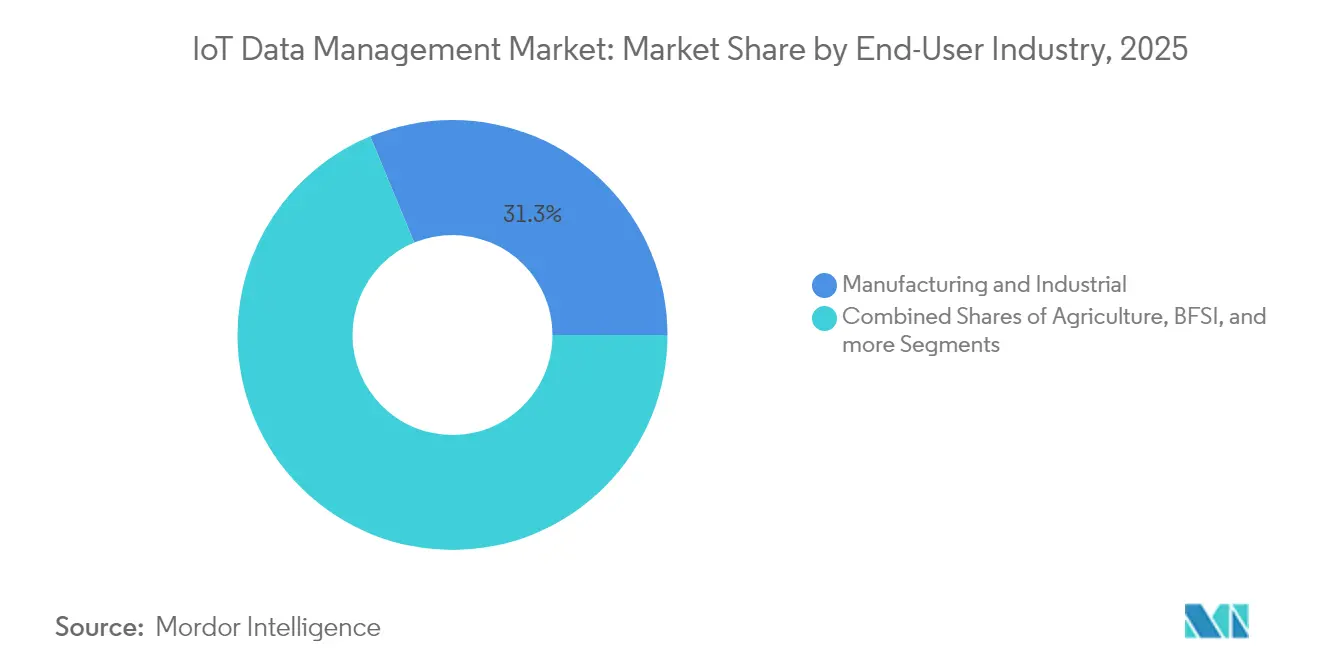

- By end-user industry, manufacturing & industrial captured 31.25% of the IoT data management market share in 2025; healthcare & life sciences is forecast to lead growth at 17.19% CAGR.

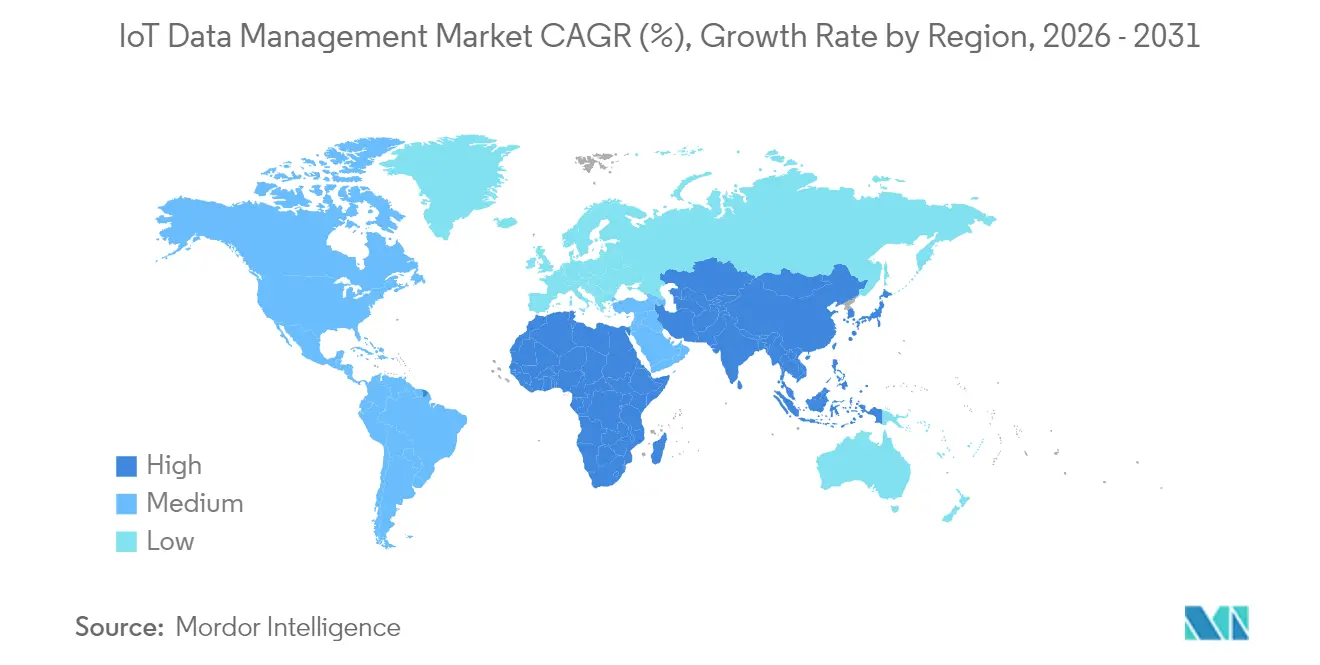

- By geography, North America commanded 40.55% of the IoT data management market size in 2025, but Asia Pacific is poised for the highest 17.56% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of IoT Data Management Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of connected devices spurring data volumes | +4.2% | Global; APAC leads deployments | Medium term (2-4 years) |

| Cloud-native data lakes and analytics maturity | +3.4% | North America & EU core; APAC rising | Long term (≥4 years) |

| Regulatory push for data governance and security | +3.0% | EU leads; global adoption | Medium term (2-4 years) |

| Real-time edge analytics for operational efficiency | +2.5% | Manufacturing hubs in Germany, US, China | Short term (≤2 years) |

| 5G network-slicing enabling prioritised IoT data streams | +2.0% | Urban centers in developed markets | Long term (≥4 years) |

| Emergence of data-marketplaces monetising sensor data | +1.3% | North America & EU early adopters | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Connected Devices Spurring Data Volumes

Industrial plants now deploy thousands of sensors per line, generating terabytes of telemetry that traditional data stores cannot absorb. Bosch shortened AI rollout cycles from months to weeks by automating data-pipeline orchestration, underscoring the scale challenges of sensor growth. Healthcare sees a similar surge as remote patient monitors stream continuous biometrics, needing HIPAA-compliant, low-latency storage. Velocity and variety pressures are pushing enterprises toward stream-first, time-series-native architectures that synchronize edge and cloud data in sub-second windows.

Cloud-Native Data Lakes and Analytics Maturity

Containerized and serverless data-lake patterns auto-scale with ingestion peaks, dissolving prior capacity-planning bottlenecks. Snowflake’s Openflow release in June 2025 illustrates friction-free cross-cloud data mobility that accelerates AI prototyping. Built-in ML pipelines now run directly inside lake environments, avoiding costly ETL steps and strengthening governance via lineage, encryption, and granular permissions.

Regulatory Push for Data Governance and Security

The EU Digital Services Act sets a precedent for enforceable algorithmic transparency, pushing vendors to embed data-classification, provenance, and privacy controls by design. Similar compliance requirements in healthcare and financial services reward platforms that automate audit trails across the entire IoT data lifecycle. Cross-border deployments must juggle overlapping rulesets while keeping architectures unified, making native governance a competitive differentiator.

Real-Time Edge Analytics for Operational Efficiency

Factories apply edge-resident vision analytics for instant quality checks, trimming bandwidth use and preventing production delays. The COGNIFOG framework shows how Kubernetes-orchestrated micro-services span edge and core for seamless DevOps. Utilities echo this approach by performing grid load-balancing at millisecond speeds, cutting latency costs and strengthening resilience.

Restraints Impact Analysis of IoT Data Management Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented standards and interoperability gaps | -2.5% | Global, multi-vendor projects | Medium term (2-4 years) |

| High total cost of ownership for end-to-end stacks | -2.0% | SMEs in developing regions | Short term (≤2 years) |

| Sustainability concerns over energy footprint | -1.3% | EU & North America regulatory focus | Long term (≥4 years) |

| Data-sovereignty regulations restricting cross-border flows | -1.0% | EU, China, Russia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Standards and Interoperability Gaps

Divergent protocols force businesses to build custom middleware that inflates maintenance costs and slows rollouts. Legacy industrial gear exacerbates complexity by requiring translation layers to talk to modern IoT platforms. Proprietary data models heighten vendor lock-in, burdening teams with parallel catalogs and lineage trackers that sap productivity and elevate risk.

High Total Cost of Ownership for End-to-End Stacks

Budget overruns often arise when integration, data-engineering, and security expenses triple initial license fees. Specialized skill shortages in edge orchestration and cyber-resilience lengthen deployment timelines, while hidden cloud egress charges widen cost gaps for SMEs. These dynamics fuel demand for managed, pay-as-you-grow IoT data services that mask infrastructure intricacies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

IoT Data Management Market Segment Analysis

By Solution:

Analytics Drives InnovationAnalytics held a 36.42% revenue lead in 2025 as enterprises pivoted from raw-data capture to actionable insight generation within the IoT data management market. The need to visualize anomalies, optimize asset utilization, and feed predictive algorithms propelled analytics adoption alongside integrated dashboards that democratize insights for frontline staff.

Stream processing is slated for a 16.86% CAGR, reflecting a decisive transition to continuous decision loops in manufacturing, healthcare, and mobility. Teradata’s integrated enterprise vector store debuted in March 2025 to power AI-ready workloads that unify traditional analytics and generative models. Security, metadata management, and time-series-optimized storage deepen platform stickiness, positioning full-stack suites as default enterprise choices.

By Deployment Model:

Hybrid Architectures AccelerateCloud retained a commanding 70.35% share in 2025 thanks to limitless scalability and opex-friendly pricing, delivering elastic compute for AI-intensive workloads across the IoT data management market. Yet hybrid configurations will post a 17.12% CAGR as data-sovereignty rules and latency-sensitive use cases keep select workloads on-premises.

Organizations increasingly process high-frequency data at the edge, forwarding aggregated analytics to cloud lakes for enterprise reporting. Hitachi Vantara’s EverFlex with Cisco Powered Hybrid Cloud showcases on-demand infrastructure ranging from IaaS to Containers-as-a-Service, bundled under flexible subscriptions. The convergence of edge orchestration and centralized governance unlocks new deployment patterns that align cost, compliance, and performance goals.

By Data Type:

Unstructured Growth AcceleratesTime-series telemetry made up 48.20% of workloads in 2025, reflecting its legacy position within SCADA systems and asset-health monitoring across the IoT data management market size. However, unstructured inputs will rise fastest at a 16.88% CAGR as computer-vision, audio, and NLP sensors proliferate in smart manufacturing and telehealth.

Manufacturers now blend machine-vision feeds with vibration and temperature streams to anticipate faults, while voice-activated hospital wards generate dialog data for clinical insights. Blockchain-enabled frameworks capable of managing 1 million devices illustrate the push for unified platforms that simultaneously support structured SQL queries and unstructured vector search.

By End-User Industry:

Healthcare Transformation LeadsManufacturing & industrial users captured 31.25% of the 2025 IoT data management market share through predictive-maintenance returns that directly cut downtime and scrap. Conversely, healthcare & life sciences will log a 17.19% CAGR on the back of remote-patient monitoring, clinical-trial digitization, and rising regulatory compliance for connected devices.

Government and smart-city projects are scaling sensor grids for traffic, air-quality, and safety oversight. Energy providers deploy distributed analytics to balance dynamic loads and integrate renewables, while BFSI firms embrace IoT-enabled fraud analytics. Cisco and TELUS plan to onboard 1.5 million 5G cars to the Cisco IoT Control Center from 2024, highlighting automotive traction.

By Application:

Asset Tracking InnovationPredictive maintenance dominated with 28.02% share in 2025, providing tangible ROI across heavy industry through reduced unplanned downtime. Asset-tracking and fleet management will expand at a 16.97% CAGR as supply-chain visibility and cold-chain integrity become board-level priorities in the IoT data management market.

Utilities advance smart-metering rollouts for demand-response programs, while remote-patient monitoring scales value-based care. PTC’s Servigistics upgrade on Cisco UCS X-Series cites 6-35% uptime boosts and 10-35% inventory cuts, validating broader business-case appeal. Multi-application convergence reduces platform sprawl and operational overheads.

Geography Analysis

North America IoT Data Management Market

North America generated 40.55% of 2025 revenue, anchored by hyperscaler ecosystems, abundant data-science talent, and regulatory clarity that speeds enterprise adoption. Ongoing 5G and edge rollouts support sub-second processing needs in smart-factory and telehealth programs. AWS signaled healthy momentum with robust Q1 2025 cloud revenue.

APAC IoT Data Management Market

Asia Pacific will pace global growth at an 17.56% CAGR to 2031 as China’s industrial-IoT drive and India’s smart-city spend enlarge addressable volumes. Huawei’s AI Data Lake and 5.5G network solutions reveal regional commitment to low-latency, AI-centric infrastructure. Rising Southeast-Asian deployments in logistics and agriculture further broaden demand.

EMEA and LATAM IoT Data Management Market

Europe sustains measured expansion through Industry 4.0 and stringent privacy rules that necessitate localized processing. Germany’s automotive lines, the UK’s digital-health pilots, and Nordic smart-grid projects exemplify high-value, compliance-first engagements within the IoT data management market. Meanwhile, Latin America and Middle East & Africa remain early-stage, yet infrastructure programs and urbanization create long-run upside for vendors offering turnkey, cost-efficient solutions.

Competitive Landscape

The vendor field remains moderately fragmented, though consolidation is quickening as buyers favor all-in-one suites over stitched point tools. Cisco’s USD 28 billion Splunk acquisition and Databricks’ USD 1 billion Neon deal underline the race to unify observability, security, and AI-ready data pipelines.

Three strategic archetypes are emerging: cloud-first hyperscalers with integrated AI services; edge-native specialists optimizing latency and sovereignty; and hybrid orchestrators bridging both realms. Patent US12143425B1 describes distributed graph analytics that adapt in real time, offering disruptive performance advantages for complex sensor streams.[3]Google Patents, “US12143425B1 Distributed Graph Analytics,” patents.google.com Differentiation now hinges on built-in governance, cross-format querying, and seamless AI model deployment across the edge-to-cloud continuum.

Partnership ecosystems are just as pivotal. Hitachi Vantara teams with Cisco for hybrid IaaS; PTC aligns with Cisco hardware for AI-powered service-life extensions; Snowflake collaborates with Microsoft Azure OpenAI to embed LLM capabilities within data lakes. Vendors that combine robust marketplaces, low-code tooling, and managed services are best positioned to capture share as enterprises pursue faster time-to-value.

IoT Data Management Industry Leaders

SAP SE

IBM

PTC Inc.

Cisco Systems, Inc.

Teradata Corporation

- *Disclaimer: Major Players sorted in no particular order

IoT Data Management Market Companies Covered in this Report

- Amazon Web Services (AWS)

- Microsoft Corp. (Azure)

- IBM Corp.

- SAP SE

- Cisco Systems Inc.

- Oracle Corp.

- Google Cloud Platform

- PTC Inc.

- Teradata Corp.

- Hewlett Packard Enterprise

- SAS Institute Inc.

- Fujitsu Ltd.

- Cloudera Inc.

- Snowflake Inc.

- Databricks Inc.

- Hitachi Vantara LLC

- Huawei Technologies Co. Ltd.

- Bosch.IO GmbH

- MongoDB Inc.

- Software AG

Recent Industry Developments in IoT Data Management Market

- June 2025: Snowflake unveiled Cortex AISQL and SnowConvert AI to streamline AI-driven analytics workflows.

- June 2025: Databricks reported USD 3.7 billion annualized revenue and previewed Lakebase, built on Neon technology.

- June 2025: Snowflake launched Openflow to enhance multi-cloud data interoperability.

- May 2025: Huawei introduced its full-stack AI Data Lake platform integrating ransomware-resistant backup.

Global IoT Data Management Market Report Scope

IoT Data Management is a comprehensive management framework that includes architectures, practices, and procedures developed for proper management of data generated and stored by the objects within an IoT.

Segmentation Overview

| Integration |

| Migration |

| Analytics |

| Storage |

| Security |

| Visualization and Dashboards |

| Metadata Management |

| Stream Processing |

| Cloud |

| On-Premise |

| Hybrid |

| Structured |

| Semi-Structured |

| Unstructured |

| Time-Series |

| Automotive and Transportation |

| Healthcare and Life Sciences |

| Government and Smart Cities |

| Manufacturing and Industrial |

| Energy and Utilities |

| Retail and E-commerce |

| Agriculture |

| BFSI |

| Others |

| Predictive Maintenance |

| Asset Tracking and Fleet Management |

| Smart Metering |

| Supply-Chain Visibility |

| Remote Patient Monitoring |

| Smart Grid Analytics |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Solution | Integration | ||

| Migration | |||

| Analytics | |||

| Storage | |||

| Security | |||

| Visualization and Dashboards | |||

| Metadata Management | |||

| Stream Processing | |||

| By Deployment Model | Cloud | ||

| On-Premise | |||

| Hybrid | |||

| By Data Type | Structured | ||

| Semi-Structured | |||

| Unstructured | |||

| Time-Series | |||

| By End-User Industry | Automotive and Transportation | ||

| Healthcare and Life Sciences | |||

| Government and Smart Cities | |||

| Manufacturing and Industrial | |||

| Energy and Utilities | |||

| Retail and E-commerce | |||

| Agriculture | |||

| BFSI | |||

| Others | |||

| By Application | Predictive Maintenance | ||

| Asset Tracking and Fleet Management | |||

| Smart Metering | |||

| Supply-Chain Visibility | |||

| Remote Patient Monitoring | |||

| Smart Grid Analytics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the IoT Data Management Market?

The market is valued at USD 92.39 billion in 2026.

How fast will the IoT Data Management Market grow by 2031?

It is projected to reach USD 197.94 billion, registering a 16.49% CAGR over 2026-2031.

Which deployment model is expanding quickest?

Hybrid architectures lead growth with a 17.12% CAGR as organizations balance sovereignty and scalability.

Which region offers the highest growth opportunity?

Asia Pacific shows the fastest regional trajectory at an 17.56% CAGR due to smart-city and manufacturing digitization.

What is the leading end-user segment today?

Manufacturing & industrial applications hold the largest 31.25% share in 2025, driven by predictive-maintenance returns.

Why are analytics solutions dominant in IoT data management?

They commanded 36.42% revenue in 2025 because enterprises derive the greatest business value by converting raw device data into actionable, real-time insights.

Page last updated on: