Internet Of Things (IoT) Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

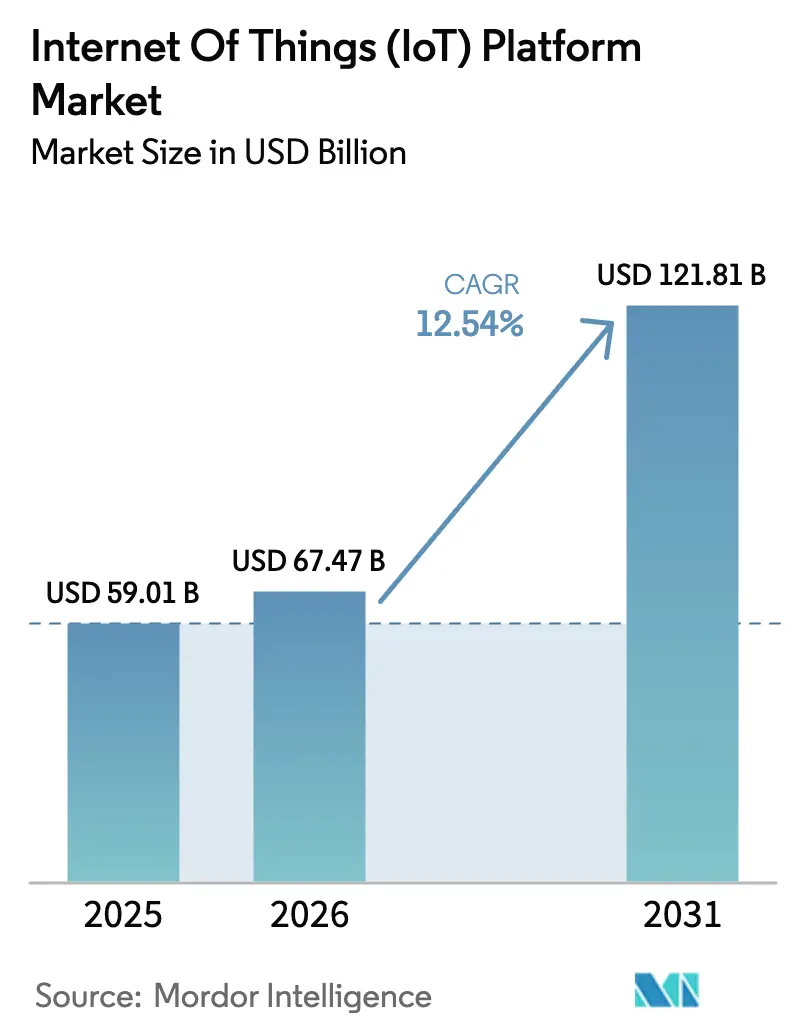

| Market Size (2026) | USD 67.47 Billion |

| Market Size (2031) | USD 121.81 Billion |

| Growth Rate (2026 - 2031) | 12.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Internet Of Things (IoT) Platform Market Analysis by Mordor Intelligence

The Internet Of Things Platform Market size is expected to increase from USD 59.01 billion in 2025 to USD 67.47 billion in 2026 and reach USD 121.81 billion by 2031, growing at a CAGR of 12.54% over 2026-2031.

This market size expansion reflects growing enterprise reliance on platforms that unify device management, data ingestion, and application enablement. Strong cloud infrastructure, falling sensor prices, and government-backed industrial digitalization initiatives are the primary engines of growth. Competitive dynamics are increasingly shaped by bundled edge-to-cloud orchestration, embedded cybersecurity frameworks, and vertical templates that shorten deployment cycles. Meanwhile, hybrid architectures are emerging as the de facto design standard, allowing organizations to satisfy latency-sensitive workloads and data-sovereignty mandates without abandoning cloud scalability. Vendors that can combine advanced analytics, regulatory compliance tooling, and consumption-based pricing are best positioned to capitalize on the widening addressable opportunity in the Internet of Things (IoT) platform market.

Key Report Takeaways

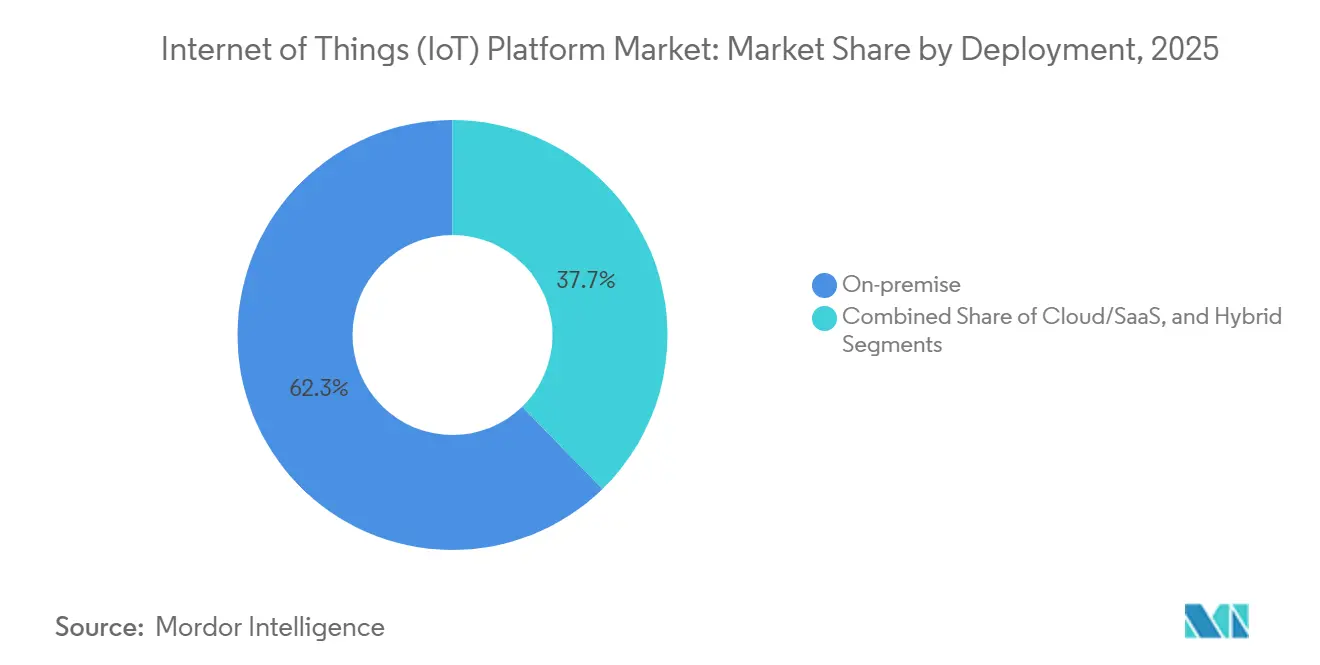

- By deployment, cloud and software-as-a-service held 62.29% of the Internet of Things (IoT) platform market share in 2025, while hybrid configurations are advancing at a 13.22% CAGR through 2031.

- By platform layer, application enablement captured 42.51% of spending in 2025; advanced analytics is set to grow the fastest, at a 12.97% CAGR through 2031.

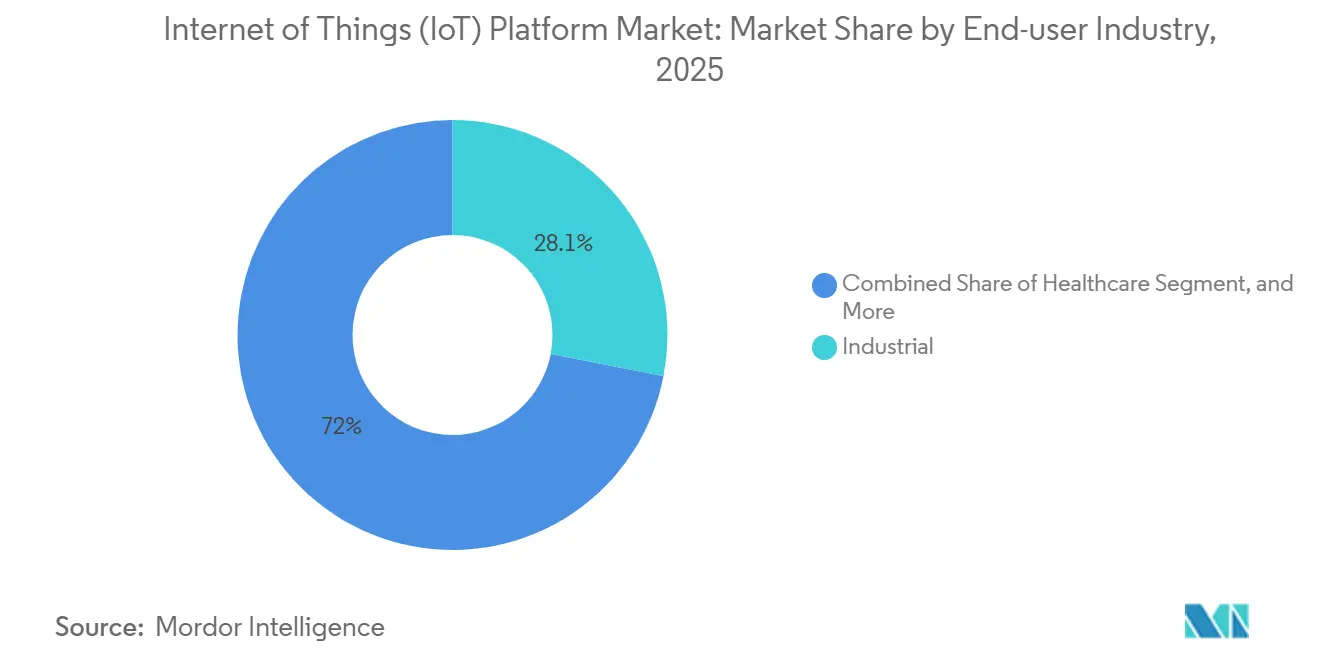

- By end-user industry, industrial applications led with 28.05% of the IoT platform market size in 2025; healthcare is forecast to expand at a 13.30% CAGR to 2031.

- By enterprise size, large enterprises commanded 55.17% share in 2025, whereas small and medium enterprises are projected to grow at a 13.01% CAGR.

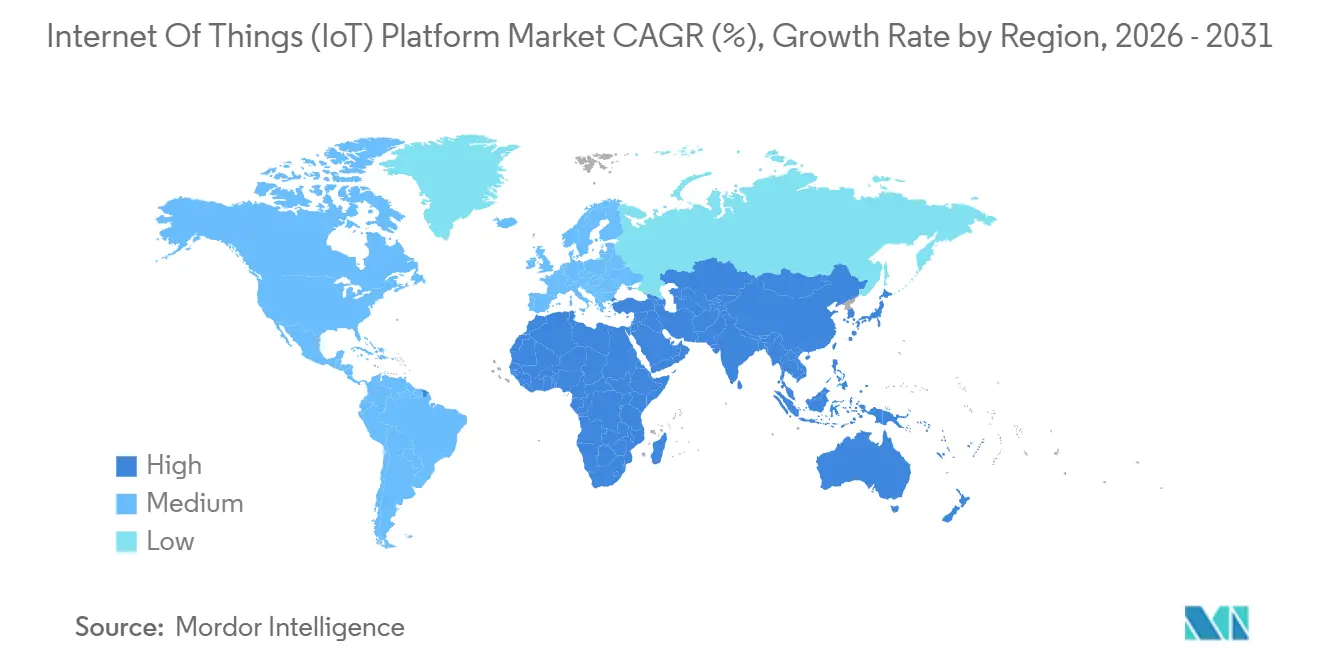

- By geography, North America accounted for 37.59% of global deployments in 2025; Asia Pacific is the fastest-growing region, at a 13.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Internet Of Things (IoT) Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Cloud-Native IoT Platforms | +2.80% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Declining Sensor and Module Costs | +2.10% | Global, strongest impact in Asia Pacific and emerging markets | Short term (≤ 2 years) |

| Growing Automation and Big Data Analytics Becoming a Key Asset | +2.50% | Global, led by industrial sectors in North America, Europe, and Asia Pacific | Medium term (2-4 years) |

| Increasing Regulatory Push for Industrial Digitalization | +1.60% | Europe and North America core, expanding to Asia Pacific | Long term (≥ 4 years) |

| Emergence of TinyML-Enabled On-Device Analytics | +1.30% | Global, early adoption in industrial and healthcare verticals | Long term (≥ 4 years) |

| Expansion of Satellite IoT Connectivity for Remote Assets | +1.10% | Global, highest relevance in maritime, agriculture, and remote infrastructure sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Cloud-Native IoT Platforms

Elastic scalability, pay-per-use billing, and seamless integration with data lake and machine-learning services have made cloud-native architectures the default choice for IoT workloads. Enterprises migrating from on-premises middleware to containerized microservices on Kubernetes are reporting shorter release cycles and lower infrastructure overhead. Managed offerings such as Azure IoT Hub and AWS IoT Core now bundle edge orchestration and real-time stream processing, reducing integration effort by an estimated 40%.[1]Microsoft Corporation, “Azure IoT Solutions,” microsoft.com Nevertheless, dependency on a handful of hyperscale providers raises vendor-lock-in concerns and concentrates operational risk, prompting many adopters to experiment with hybrid deployments.

Declining Sensor and Module Costs

Between 2024 and 2025, average prices for NB-IoT and LTE-M modules fell 15-20%, pushing unit costs below USD 5 in high volumes and expanding deployment feasibility in logistics, agriculture, and utilities. Semiconductor oversupply in mature process nodes continues to depress pricing, enabling high-density sensor networks that were previously cost-prohibitive. Lower hardware costs translate directly into greater recurring revenue for platform vendors that charge per connected device, reinforcing the growth trajectory of the Internet of Things (IoT) platform market. Price declines are most pronounced in Asia Pacific, where local fabrication capacity intensifies competition among module suppliers.

Growing Automation and Big Data Analytics Becoming a Key Asset

Industrial firms are shifting from basic condition monitoring to closed-loop automation that combines predictive algorithms, anomaly detection, and prescriptive optimization. Manufacturers adopting IoT-driven analytics have documented double-digit reductions in unplanned downtime and single-digit gains in overall equipment effectiveness. As petabyte-scale time-series data flows into enterprise data warehouses, demand surges for platforms offering pre-built data models, digital twins, and low-latency in-memory analytics. The emphasis on outcome-driven automation is driving the rapid uptake of advanced analytics modules and reinforcing the IoT platform market’s evolution from connectivity middleware to an intelligence layer.

Increasing Regulatory Push for Industrial Digitalization

Cyber Resilience Act requirements in the European Union and NIST SP 800-213 guidance in the United States compel organizations to incorporate secure-by-design principles, automated updates, and incident-reporting workflows into device fleets.[2]European Commission, “Cyber Resilience Act,” europa.eu Compliance obligations are motivating enterprises to favour mature platforms with embedded governance, thereby accelerating consolidation around providers that can demonstrate certified security capabilities. Beyond cybersecurity, environmental monitoring mandates and worker safety regulations encourage the adoption of real-time sensing and analytics, fortifying the long-term growth outlook for the Internet of Things (IoT) platform market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Market Fragmentation and Interoperability Issues | -1.80% | Global, most acute in brownfield industrial environments | Medium term (2-4 years) |

| Heightened Cyber-Security and Data-Privacy Concerns | -1.50% | Global, regulatory pressure highest in Europe and North America | Short term (≤ 2 years) |

| Edge-Cloud Integration Complexity | -1.20% | Global, particularly challenging in multi-vendor industrial ecosystems | Medium term (2-4 years) |

| Shortage of Full-Stack IoT Developers and Standards | -1.00% | Global, most severe in emerging markets and SME segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened Cyber-Security and Data-Privacy Concerns

High-profile breaches have increased board-level scrutiny of IoT projects, as widely distributed devices create vast, hard-to-defend attack surfaces. Medical device makers must now provide software bills of materials and vulnerability management processes under updated FDA guidance. In Europe, platforms must issue security patches and file incident reports within 24 hours of detection. These requirements inflate compliance costs, especially for smaller vendors. Privacy rules such as GDPR further complicate cross-border data flows, constraining global scalability and adding procedural overhead to deployments in consumer and healthcare segments.

Market Fragmentation and Interoperability Issues

Proprietary protocols and vendor-specific data schemas complicate multi-vendor integrations, particularly on brownfield factory floors where legacy equipment cannot natively communicate with cloud platforms. Although the Connectivity Standards Alliance’s Matter protocol is easing smart-home interoperability, industrial segments remain hamstrung by protocol diversity and lack of universal semantic models. Organizations often default to single-vendor stacks to sidestep integration risk, sacrificing best-of-breed functionality and slowing innovation. The resulting fragmentation subtracts directly from growth potential, putting downward pressure on the IoT platform market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Hybrid Configurations Gain Traction

Hybrid architectures represented the fastest-growing deployment model in 2025, advancing at a 13.22% CAGR through 2031 as organizations balance cloud elasticity with edge-level latency demands. On-demand scalability continues to favour cloud and SaaS arrangements, which collectively retained 62.29% of the Internet of Things (IoT) platform market share in 2025. Even so, regulatory directives in sectors such as defense and critical infrastructure keep on-premises options viable for workloads that require air-gapped networks. Vendors are responding by offering orchestration frameworks that enable seamless container migration across cloud, edge, and on-premises nodes.

The shift underscores a broader re-architecture toward distributed compute, where sub-10-millisecond latency targets in industrial automation and autonomous systems cannot tolerate round-trip delays to centralized data centers. Hybrid designs also satisfy data-sovereignty statutes that obligate local processing within national borders. Consequently, the IoT platform market size attributable to hybrid installations is projected to outpace growth in pure cloud or pure on-premises models. Organizations lacking DevOps personnel, however, cite operational complexity as a lingering obstacle.

By Platform Layer: Advanced Analytics Modules Accelerate

Application enablement layers absorbed 42.51% of spending in 2025, but advanced analytics components are scaling faster, rising at a 12.97% CAGR as firms migrate from descriptive dashboards to prescriptive engines. Device management and connectivity services, now widely commoditized, compete primarily on total cost of ownership and over-the-air update efficiencies. Vendors that deliver domain-specific data models, digital-twin tooling, and AI-powered anomaly detection hold a competitive advantage. For example, SAP’s in-memory analytics integrate directly with streaming sensor inputs, allowing near-real-time optimization of production lines.

Edge-side acceleration chips and GPU-enabled servers amplify the debate over whether analytics should reside locally or in the cloud. While edge inference minimizes latency, high-fidelity model retraining still benefits from centralized compute power. The Internet of Things (IoT) platform market size allocation to analytics is therefore bifurcating between cloud-resident training pipelines and edge-resident inference engines, demanding orchestration capabilities that span this continuum.

By End-User Industry: Healthcare IoT Surges

Industrial organizations commanded 28.05% of demand in 2025, but healthcare exhibits the most robust expansion, charting a 13.30% CAGR as remote patient monitoring and hospital-at-home services scale. FDA cybersecurity mandates tighten device lifecycle controls, pushing providers toward platforms with validated security architectures. The IoT platform market size for healthcare is forecast to eclipse consumer smart-home spending before 2031, propelled by reimbursement models favouring telehealth and by clinical workforce shortages that elevate automation priorities.

In contrast, smart-building deployments emphasize energy optimization, occupant safety, and regulatory compliance with green-building standards. Agriculture gains momentum through precision fertilization and satellite-enabled telemetry in remote fields but remains a smaller slice of total revenue. Each sector’s digital-maturity curve informs distinct platform requirements, reinforcing vendor specialization and the Internet of Things (IoT) platform market’s vertical diversification.

By Enterprise Size: SMEs Embrace Consumption Pricing

Large enterprises retained 55.17% revenue share in 2025 because of their capacity to fund multi-year transformation projects that incorporate thousands of assets and intricate ERP integrations. Nonetheless, the small and medium enterprise cohort is expanding at a 13.01% CAGR, buoyed by pay-as-you-go billing and low-code development environments that mitigate the need for scarce IoT engineers. Consumption-aligned costs enable SMEs to pilot proofs of concept at modest scale before committing capital, thereby democratizing access to the IoT platform market.

Managed service providers further simplify adoption by bundling hardware, connectivity, and lifecycle support under a single invoice. Although SMEs contribute a smaller absolute revenue base, their growth momentum compels vendors to create simplified onboarding workflows and pre-configured vertical solutions. Over time, the shift toward SME-friendly packages broadens the Internet of Things (IoT) platform market’s total addressable footprint.

Geography Analysis

North America led deployments with a 37.59% share in 2025, anchored by the presence of hyperscale cloud infrastructure and federal cybersecurity guidelines that clarify procurement rules. The United States dominates industrial IoT rollouts focused on manufacturing automation and energy grid modernization, while Canada scales IoT-driven resource management in forestry and mining. Mexico’s smart-factory investments benefit from near-shoring trends that re-route supply chains closer to U.S. consumption hubs. Notwithstanding its size, regional growth is moderating as early adopter segments reach saturation, leaving incremental opportunities primarily in brownfield retrofits and compliance-driven upgrades.

Asia Pacific is the fastest-growing territory, slated to expand at a 13.67% CAGR through 2031. China’s sovereign manufacturing directives, India’s Digital India initiative, and Japan’s Society 5.0 program converge to sustain high investment in connected factories, smart cities, and healthcare. Domestic providers such as Huawei and Alibaba Cloud tailor offerings to local regulations and language, thereby intensifying competitive pressure on Western incumbents. Rising 5G penetration and falling sensor prices further enlarge the Internet of Things (IoT) platform market in rural and industrial zones across Southeast Asia and Oceania.

Europe occupies a pivotal role in regulatory shaping, with the Cyber Resilience Act and GDPR embedding cybersecurity and privacy into procurement criteria. Germany leverages Industrie 4.0 funding to digitalize discrete manufacturing, while France and Italy integrate IoT into agriculture and transportation. Regional data-sovereignty provisions foster demand for hybrid or on-premises architectures. Elsewhere, the Middle East and Africa accelerate IoT adoption in oil and gas, utilities, and smart-city megaprojects, whereas South America pilots’ precision agriculture and urban mobility platforms. Although their absolute volumes remain smaller, these regions present greenfield prospects that invite satellite connectivity and low-power network alternatives.[3]Federal Communications Commission, “Cybersecurity Certification Mark for IoT Devices,” fcc.gov

Regulatory Landscape

IoT platform procurement is increasingly shaped by product security and data protection requirements, including secure-by-design controls, vulnerability handling, and audit-ready lifecycle governance. In the European Union, the Cyber Resilience Act (CRA) entered into force on December 10, 2024, establishing a common cybersecurity baseline for connected products and lifting compliance expectations for platforms that manage device identity, patching, and incident workflows across device fleets.

Near-term CRA milestones tighten operational requirements for platform vendors and their customers: conformity assessment body notification procedures apply from June 11, 2026, and reporting obligations for actively exploited vulnerabilities and severe security incidents commence on September 11, 2026. In the United States, NIST guidance for IoT cybersecurity (including NIST SP 800-213 referenced within the market context) and the Federal Communications Commission (FCC) Cyber Trust Mark program reinforce security labeling and assurance expectations for consumer IoT, with the FCC selecting the ioXt Alliance as lead administrator effective April 13, 2026. Overall, these policy moves lift demand for platforms with embedded compliance tooling (SBOM readiness, secure update mechanisms, and incident reporting) that can also support hybrid architectures under data-sovereignty constraints.

Value Chain Analysis

The IoT platform value chain connects device and module suppliers (sensors, MCUs, NB-IoT/LTE-M modules), connectivity providers (cellular, LPWAN, satellite), and cloud and edge infrastructure. These inputs feed platform layers such as device management, connectivity management, application enablement, and advanced analytics. Hyperscalers and industrial software vendors bundle these layers with developer tooling, data pipelines, and security services, while systems integrators and managed service providers (MSPs) operationalize deployments by bundling hardware, connectivity, and lifecycle support for industrial, healthcare, and connected-building use cases.

Upstream connectivity is moving toward greater standardization and multi-operator coverage, which reduces lock-in and changes how platforms manage provisioning and roaming at scale. In July 2026, Thales and Singtel, with operators including Optus, AIS, and Globe Telecom (via Bridge Alliance), launched a multi-operator enterprise IoT eSIM network in Asia Pacific based on GSMA SGP.32, enabling remote device management without single-operator dependency. Downstream, platform differentiation is shifting toward AI-assisted orchestration and workflow integration, where sensor data is translated into actions inside enterprise systems (ERP, PLM, EAM, and FSM), raising the importance of connectors, semantic models, and governance features across hybrid edge-to-cloud deployments.

Competitive Landscape

Vendor dynamics remain fluid, with no firm exceeding a 15% revenue share, underscoring moderate fragmentation. Hyperscale cloud providers bundle IoT functionality with storage, AI training, and analytics services, leveraging economies of scale to undercut pricing and simplify integration. Industrial automation stalwarts such as Siemens and Schneider Electric defend installed bases by embedding IoT modules directly into operational technology stacks, enhancing real-time control and asset visibility. IoT-native specialists, including PTC and Software AG, differentiate through verticalized data models, digital-twin libraries, and low-code application composition.

Edge-native frameworks such as EdgeX Foundry appeal to integrators seeking vendor-agnostic orchestration, fostering a micro-services ecosystem that counters full-stack lock-in. Cybersecurity capabilities aligned with NIST SP 800-213 and the Cyber Resilience Act increasingly determine shortlist success, elevating vendors able to demonstrate certified encryption, device identity, and automated patch workflows. Strategic moves include consumption-based pricing to woo SMEs, satellite-integrated offerings for remote industries, and TinyML toolkits that push inference onto microcontrollers. Consolidation pressures intensify as smaller vendors struggle to fund compliance, yet the entrance of open-source and domain-specific newcomers ensures that the Internet of Things (IoT) platform market retains competitive vigor.

Internet Of Things (IoT) Platform Industry Leaders

IBM Corporation

Microsoft Corporation

PTC Inc.

SAP SE

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Security-by-design compliance is turning into a commercialization lever for IoT platforms, creating room for vendors that package governance, automated patch orchestration, and incident reporting into deployable templates for regulated industries. The EU Cyber Resilience Act (entered into force on December 10, 2024) sets out operational milestones for 2026, including conformity assessment body notification procedures from June 11, 2026 and reporting obligations starting September 11, 2026, pushing manufacturers and operators to favor platforms that can operationalize secure update pathways, device identity, and vulnerability workflows across large fleets.

Interoperability across mixed connectivity and protocol stacks remains a practical gap, especially in brownfield industrial environments where fragmentation persists. Standards activity in 2026 around semantic interoperability, including W3C Web of Things metadata abstraction and OPC-UA industrial information models, supports opportunities for platforms that normalize device data into consistent digital-twin and analytics layers. On connectivity, the July 2026 Asia Pacific multi-operator enterprise IoT eSIM network based on GSMA SGP.32 highlights demand for scalable, multi-country device lifecycle management. In parallel, LoRa Alliance roadmap updates (June 2026) focused on migration procedures and device capability discovery broaden the integration surface for platforms that need to manage LPWAN and satellite extensions alongside cellular and private networks.

Recent Industry Developments

- June 2026: PTC launched PTC Orbit, a cloud-native as-maintained system of intelligence for manufacturers that consolidates data from PLM, ERP, CRM, IoT, EAM, and field service workflows. The release strengthens the application enablement and analytics layers by targeting unified asset intelligence rather than standalone device connectivity. It also raises competitive pressure on horizontal IoT platforms to deliver deeper enterprise-system integration and AI-assisted decision support.

- June 2026: Siemens announced Intelligence Center X, an industrial AI orchestration software offering that integrates Mendix with Graph Studio and AI Studio. The move reinforces Siemens Xcelerator positioning by connecting IT/OT data and operationalizing AI across industrial environments, which shifts buyer evaluation toward orchestration and governed AI enablement on top of IoT data streams. It also supports hybrid deployments where inference and control can be distributed across edge and cloud tiers.

- April 2026: Siemens expanded its Industrial Edge ecosystem at Hannover Messe 2026, including a UL Solutions certification (Smart Systems Verified - Platinum). The update strengthens trust and compliance signaling for edge-to-cloud IoT deployments, particularly where cybersecurity and product assurance are procurement gating factors. It also underscores the market move toward certified edge ecosystems that simplify integration for latency-sensitive industrial applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is measured as the revenue earned from software platforms that help connect IoT devices, manage them, move their data securely, and run applications and analytics on top of that data across industries.

Scope exclusions: We exclude IoT endpoint hardware, connectivity access charges from telecom operators, and stand-alone professional services that are not sold as part of an IoT platform contract.

Segmentation Overview

- By Deployment

- On-premise

- Cloud/SaaS

- Hybrid

- By Platform Layer

- Application Enablement

- Device Management

- Advanced Analytics

- Connectivity

- Cloud Storage/IaaS

- By End-user Industry

- Industrial

- Connected Building

- Smart Home

- Mobility

- Healthcare

- Agriculture

- Rest of End-user Industries

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clear picture of the IoT platform demand pool and the way spending gets reported in public sources. We leaned on non-paywalled sources such as the International Telecommunication Union (ITU) for connectivity and digital indicators, GSMA for mobile and IoT connections context, the US Federal Communications Commission (FCC) and EU policy portals for spectrum and security-related references, NIST publications for IoT cybersecurity guidance, and OECD digital economy materials for adoption signals.

Along with this, we reviewed company annual reports, earnings transcripts, and investor decks to understand how platform revenue is described, how vendors bundle capabilities, and how exposure varies by geography. Patent databases were used selectively to sanity check where platform capabilities are moving (for example, device management, edge orchestration, and analytics). The desk source list is illustrative, and many other public documents were also used for data collection, cross-checks, and clarifying assumptions.

Primary Interviews and Surveys

Primary inputs were collected through expert conversations and structured surveys with platform providers, system integrators, and enterprise buyers that run IoT programs. We covered the main regions and mixed viewpoints across industries like manufacturing, buildings, mobility, and healthcare, so gaps from desk sources could be filled and then checked against the model outputs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 20% | APAC: 44% |

| Mid tier: 46% | Functional/Unit leaders: 36% | EMEA: 31% |

| Smaller Players: 20% | Managers: 44% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using both top-down and bottom-up logic, where an IoT software spend pool is reconstructed by region and then allocated to platform layers and deployment patterns based on adoption and pricing signals. Once the macro totals are shaped, we corroborate them with selective bottom-up approximations like sampled vendor revenue disclosures, channel checks with integrators, and implied ASP times deployed device and application volumes, which helps adjust totals when the first cut looks off.

Key inputs that move the model include enterprise IoT adoption rates by industry, cloud versus on-premise mix, average platform contract values, the share of deployments requiring advanced analytics, and the pace of connected device growth that drives platform seat and message volume needs. Forecasts are produced using scenario analysis, with the base case anchored to expected cloud migration, security and compliance spend, and rollout speed across industrial and smart building projects. We then review the scenario slope with experts so the trajectory stays realistic. Where a bottom-up check has missing coverage for smaller vendors or new offers, we apply a measured uplift based on observed procurement patterns and regional partner feedback.

Data Validation & Update Cycle

Outputs are checked against independent signals, including cloud spending direction, enterprise digital transformation budgets, and reported platform subscription growth patterns. When large variances appear, assumptions are reopened, which can trigger a re-contact with interviewees and a fresh desk pass on the driver series.

Before sign-off, the model goes through multi-step analyst reviews that focus on unit consistency, outlier years, and region to region reasonableness. The report is refreshed annually, and interim updates are made when material events change pricing, regulation, or deployment behavior. Right before delivery, we do a final update sweep so clients receive the most current view available.

Mordor Intelligence's Internet of Things Platform Market Size Versus Other Published Estimates

Published market values for IoT platforms can look far apart because the scope line is not drawn the same way, and because base years and currency timing also shift reported totals. Differences also come from how cloud, hybrid, and on-premise revenues are counted, and whether platform layers are treated as separate or bundled.

The main gap comes from bundling, where Mordor Intelligence counts only platform-layer revenues like device management, application enablement, connectivity management, analytics, and related cloud platform components, instead of folding in IoT hardware, pure connectivity charges, or broad services that sit outside the platform contract.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 67.47 B (2026) | |

| Global Consultancy A | USD 11.10 B (2023) | Uses an earlier base year and a narrower revenue capture that can undercount hybrid and multi-layer platform bundles, especially when analytics and connectivity management are reported under adjacent software lines. |

| Industry Research Group B | USD 16.11 B (2025) | Starts from a 2025 base and often treats the platform as a software-only layer, which can miss IaaS-like platform components and can apply different ASP progression assumptions across regions. |

The spread in the table is mostly explained by what gets counted as platform revenue and how bundled contracts are split across software, cloud components, and services. By keeping the model tied to clear platform layers, deployment mix, and practical pricing and adoption drivers, the estimate stays repeatable and easier to reconcile with real-world purchasing behavior.

Key Questions Answered in the Report

What was the global value of the Internet of Things (IoT) platform market in 2026?

The market reached USD 67.47 billion in 2026 and is forecast to climb to USD 121.81 billion by 2031, reflecting a 12.54% CAGR.

Which deployment model is growing fastest?

Hybrid configurations are advancing at a 13.22% CAGR because they blend cloud scalability with edge-level latency and data-sovereignty benefits.

Why is healthcare seeing rapid platform adoption?

Remote patient monitoring mandates, telehealth reimbursement, and stringent FDA cybersecurity guidance are propelling healthcare IoT at a 13.30% CAGR.

Which region offers the strongest growth prospects?

Asia Pacific is expanding at a 13.67% CAGR, fueled by industrial policies in China, smart-city investments in India, and Japan's Society 5.0 roadmap.

How do falling sensor prices affect adoption?

Module costs below USD 5 make high-density deployments economically viable, enlarging the total addressable opportunity for platform vendors.

What differentiates leading vendors in this space?

Successful providers bundle advanced analytics, certified cybersecurity, hybrid orchestration, and consumption-based pricing to reduce deployment friction and total cost of ownership.

Page last updated on: