Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Narrowband IoT Enterprise Application Market Report is Segmented by Enterprise Size (Small and Medium Enterprises and Large Enterprises), Application (Smart Governance, Smart Metering, Smart Asset Tracking, and More), End-User Industry (Energy and Utilities, Retail, Industrial Manufacturing, Transportation and Logistics, and More), and Geography.

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

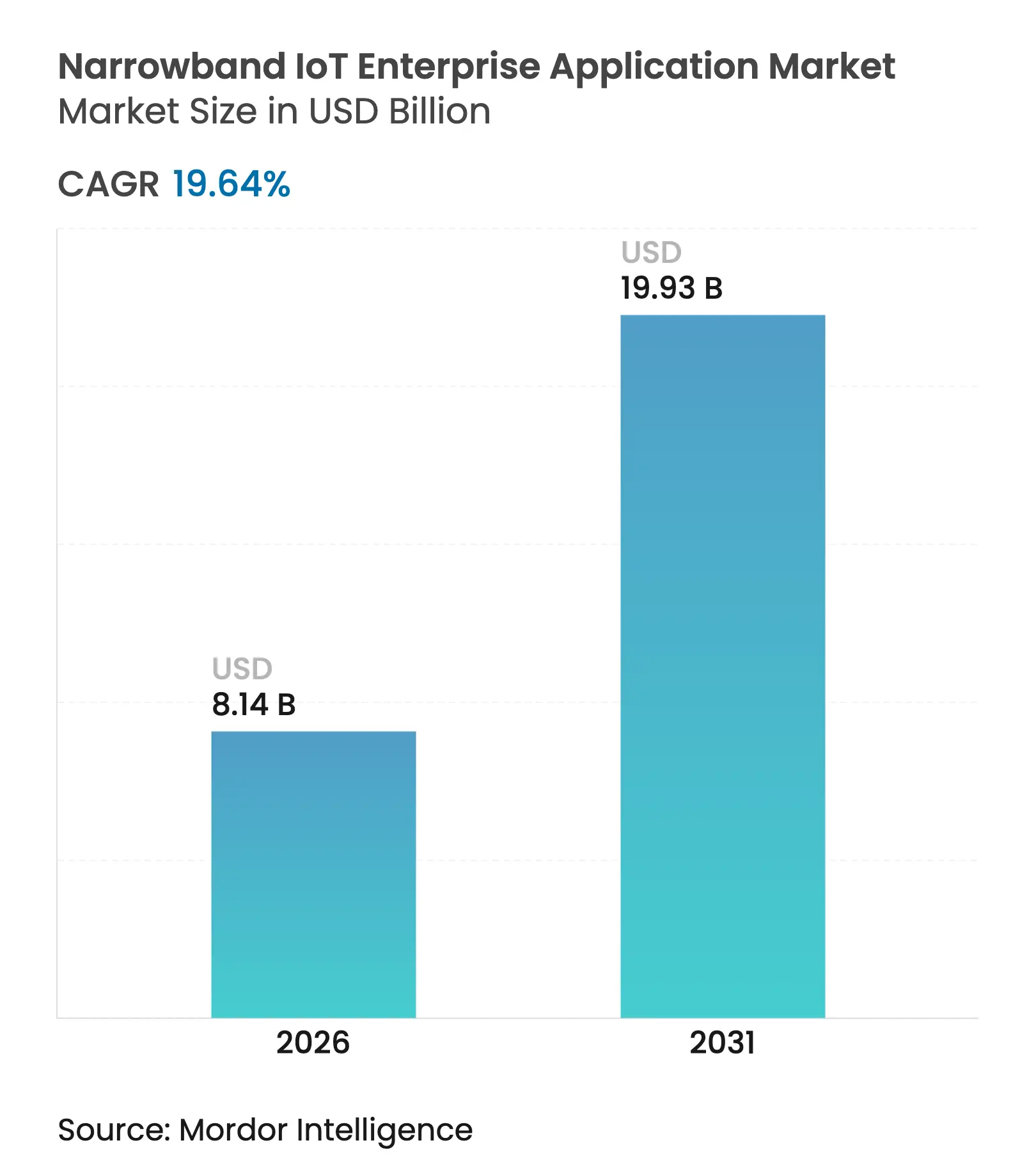

| Market Size (2026) | USD 8.14 Billion |

| Market Size (2031) | USD 19.93 Billion |

| Growth Rate (2026 - 2031) | 19.64 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The current growth phase reflects a shift from pilot projects to full-scale, mission-critical rollouts as governments back nationwide NB-IoT networks, energy-harvesting chipsets cut maintenance costs, and 3GPP Release-17 provides a stable migration path into 5G RedCap. Satellite NB-IoT constellations address the last-mile coverage gap, while falling module prices open the technology to smaller enterprises. Competitive intensity rises as satellite providers, mobile network operators, and LoRaWAN vendors position themselves around cost, coverage, and integration advantages.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Government-backed nationwide NB-IoT rollouts Government-backed nationwide NB-IoT rollouts | + 4.20% | China, EU core markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast :+ 4.20% | Geographic Relevance : China, EU core markets | Impact Timeline : Medium term (2-4 years) |

Rapid smart-meter tenders in water and gas utilities Rapid smart-meter tenders in water and gas utilities | + 3.80% | Global, Europe and APAC focus | Short term (≤ 2 years) | |||

3GPP Release-17 integration with 5G RedCap 3GPP Release-17 integration with 5G RedCap | + 2.90% | Global, led by North America and Europe | Long term (≥ 4 years) | |||

Satellite-enabled NB-IoT for remote assets Satellite-enabled NB-IoT for remote assets | + 2.10% | Global, priority in Africa and remote APAC | Medium term (2-4 years) | |||

Energy-harvesting NB-IoT chipsets Energy-harvesting NB-IoT chipsets | + 1.80% | Global, manufacturing regions | Long term (≥ 4 years) | |||

Declining module costs enabling SME adoption Declining module costs enabling SME adoption | + 1.50% | Global | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Government-backed Nationwide NB-IoT Rollouts

China’s “Signal Upgrade” program targets 80,000 high-priority locations for NB-IoT coverage by 2025, creating network density that industrial users require for always-on sensors.[1]Ministry of Industry and Information Technology, “Signal Upgrade Initiative,” miit.gov.cn Parallel EU directives require 80% household coverage with smart metering, supported by CEN-CENELEC interoperability standards that reduce fragmentation. These mandates accelerate base-station upgrades and spectrum allocations, lower enterprise risk, and drive rapid module demand in utilities, manufacturing, and urban infrastructure.

Rapid Smart-Meter Tenders in Water and Gas Utilities

Global smart-meter installations are projected to double to 3.4 billion by 2033 as utilities modernize networks for leak detection and demand forecasting. In France, Veolia and Birdz have rolled out millions of NB-IoT water meters that deliver near real-time data while avoiding manual reads. Honeywell’s NB-IoT-enabled meters paired with Verizon connectivity illustrate how utility pilots transition into large-volume contracts when lifetime ownership costs fall.

3GPP Release-17 Integration with 5G RedCap

Release-17 defines Reduced Capability devices that bridge 4G LTE and full 5G, letting enterprises deploy dual-mode sensors now and migrate later without truck rolls.[2]Rohde & Schwarz, “5G RedCap Devices Explained,” rohde-schwarz.com Ericsson research shows RedCap devices achieve sub-10 Mbps throughput with markedly lower power draw, ideal for factory sensors and environmental monitors. GSMA’s Mobile IoT framework lists 252 commercial NB-IoT networks, giving enterprises the confidence that devices procured today remain compatible with future 5G rollouts.

Satellite-enabled NB-IoT for Remote Asset Monitoring

Sateliot’s 5G NB-IoT constellation integrates with standard SIM cards, merging terrestrial and non-terrestrial networks for true global reach. Telefónica field tests confirm roaming from space to ground networks, enabling oil, mining and agriculture firms to track equipment beyond cellular footprints. OQ Technology further extends coverage through Deutsche Telekom partnerships that fill maritime and desert gaps.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

LoRaWAN price advantages in private utilities networks LoRaWAN price advantages in private utilities networks | –2.7% | North America and Europe | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast : –2.7% | Geographic Relevance :North America and Europe | Impact Timeline : Short term (≤ 2 years) |

Fragmented roaming SLAs across MNO footprints Fragmented roaming SLAs across MNO footprints | –1.9% | Global | Medium term (2-4 years) | |||

Lengthy and costly module certification processes Lengthy and costly module certification processes | –1.6% | Global | Short term (≤ 2 years) | |||

Limited rural coverage in developing regions Limited rural coverage in developing regions | –1.4% | South America and Middle East | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

LoRaWAN Price Advantages in Private Utilities Networks

LoRaWAN modules remain cheaper than NB-IoT units and operate on unlicensed spectrum, letting utilities bypass recurring cellular fees. Private water utilities in rural zones often favor LoRa due to simple gateway deployments that avoid operator negotiations. The cost gap forces NB-IoT vendors to stress security, QoS and seamless integration with existing cellular assets when pitching to cost-sensitive buyers.

Fragmented Roaming SLAs across MNO Footprints

Permanent-roaming restrictions differ by country, so a device certified on one network may fail elsewhere, slowing multinational rollouts.[3]Telnyx, “IoT Roaming Restrictions Explained,” telnyx.com AT&T’s approval process can cost USD 175,000 and take almost 12 months, hampering time-to-market for global equipment suppliers. Multi-IMSI and eUICC solutions mitigate some pain, yet enterprises still face legal and operational uncertainty every time they cross borders.

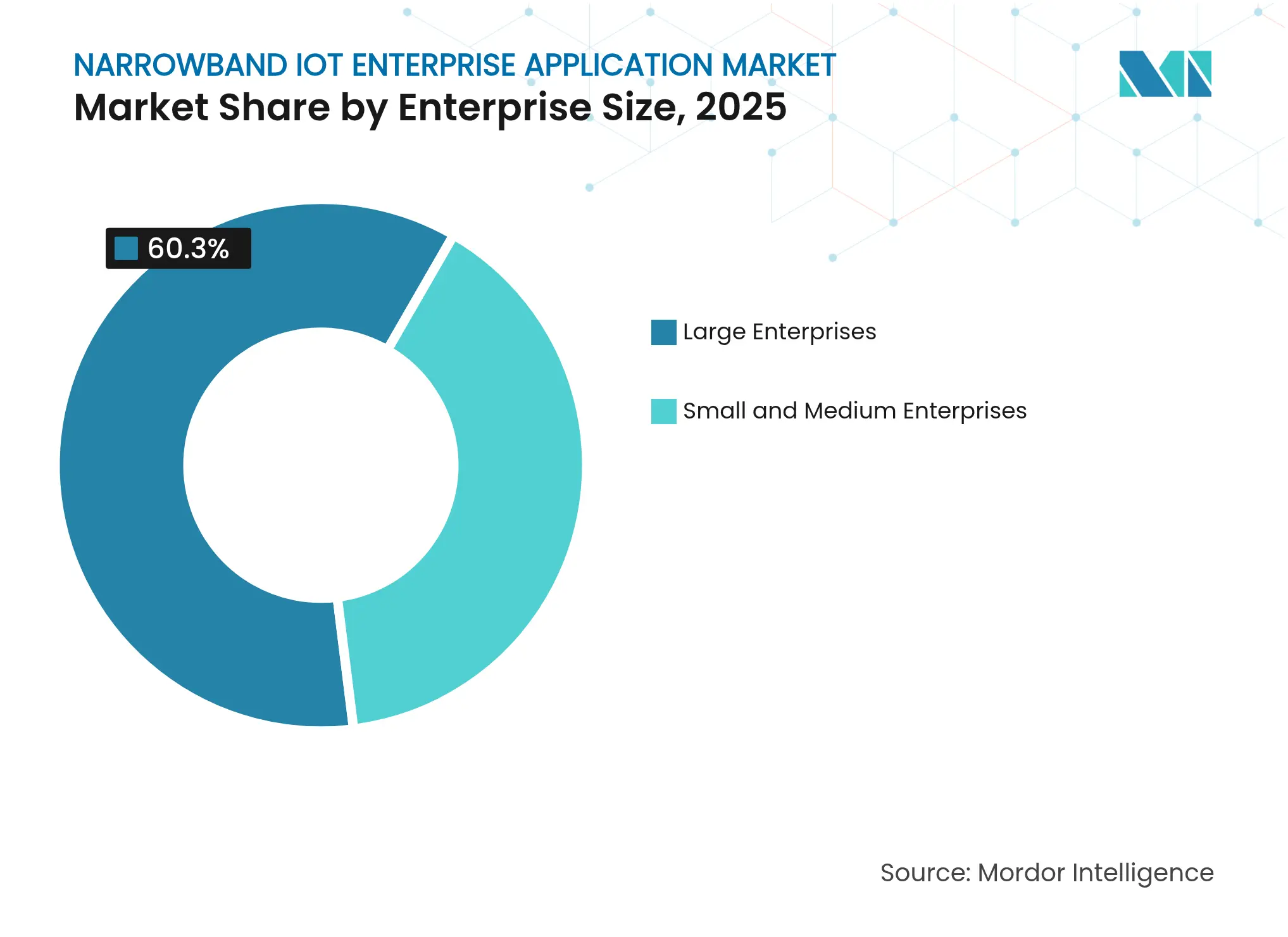

By Enterprise Size: SMEs Drive Adoption through Simplified Deployment Models

SMEs are the fastest-growing customer group, expanding at 22.4% CAGR despite large enterprises retaining 60.30% share of the Narrowband IoT enterprise application market in 2025. The uptick stems from sub-USD 10 modules, cloud-first dashboards, and managed services that shield smaller firms from integration complexity. Industrial case studies show payback periods under 24 months when sensors prevent unplanned downtime. Large enterprises continue to dominate multistate deployments in utilities and automotive plants, leveraging dedicated IT teams and economies of scale for platform licensing.

The total addressable Narrowband IoT enterprise application market size for SMEs is projected to reach USD 5.66 billion by 2031, while large-enterprise spending climbs to USD 14.27 billion. Energy-harvesting reference designs from HiSilicon allow “install-and-forget” sensors in mid-sized factories that lack maintenance staff, making NB-IoT economically viable at smaller scale.

Note: Segment shares of all individual segments available upon report purchase

By Application: Smart Asset Tracking Moves Beyond Traditional Metering

Smart metering accounted for 33.40% of Narrowband IoT enterprise application market share in 2025 on the back of utility mandates, yet smart asset tracking will grow at 24.1% CAGR to 2031 as logistics and industrial firms demand real-time visibility. Container operators that adopt NB-IoT tags report fewer demurrage fees and improved customer SLAs.

Asset-tracking growth pushes the total Narrowband IoT enterprise application market size for tracking solutions to USD 5.95 billion by 2031, overtaking new meter installations after 2028. Combined with AI analytics, NB-IoT tags feed predictive ETAs into transport management systems, improving route planning and reducing emissions.

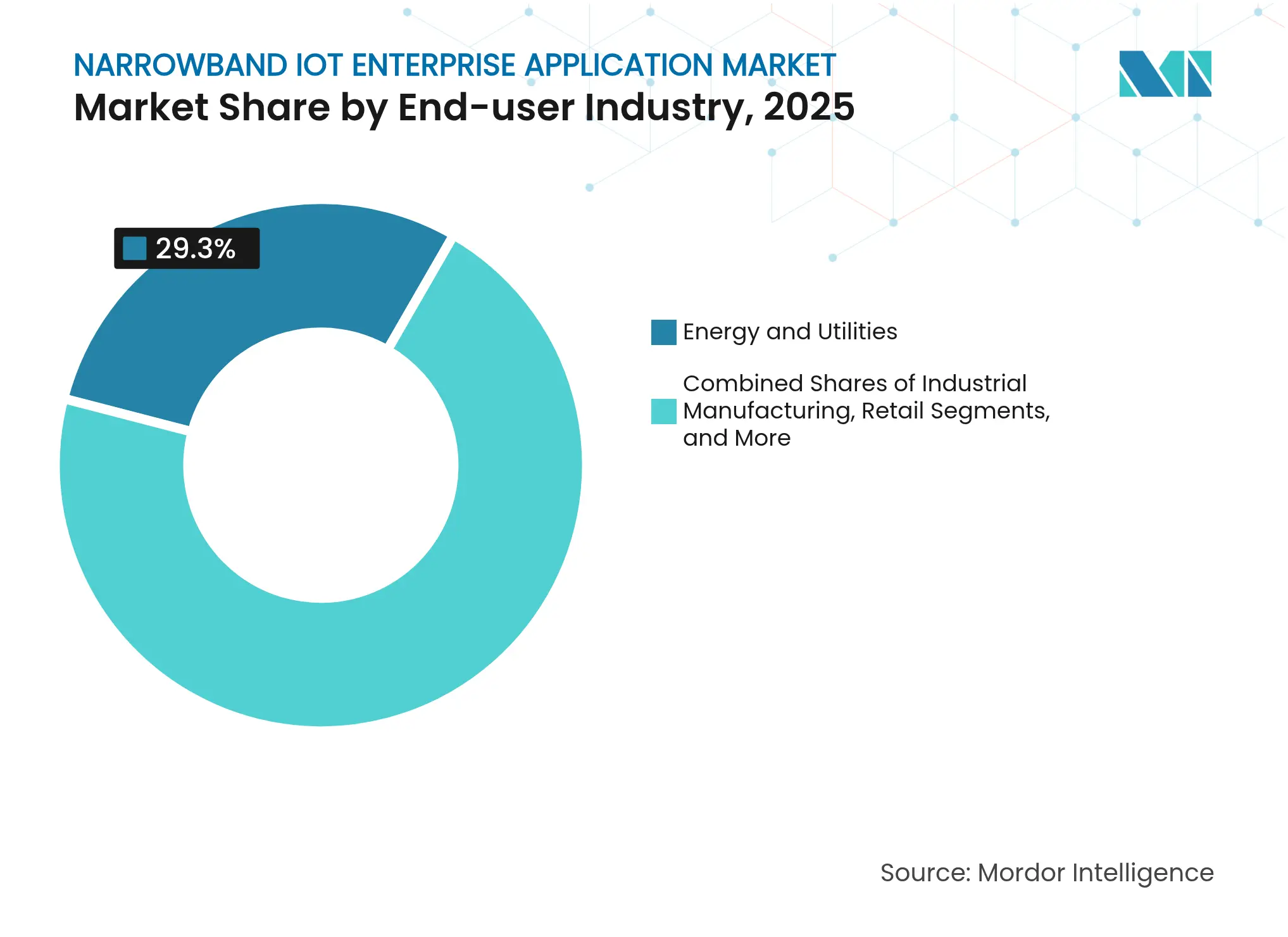

By End-user Industry: Transportation and Logistics Disrupts Utility Dominance

Energy and utilities held a 29.30% share in 2025 as regulators required interval data for gas and water. However, the transportation and logistics segment is projected to expand at 23.2% CAGR through 2031 as supply chain digitalization becomes board-level priority. T-Mobile reports double-digit growth in NB-IoT fleet subscriptions, driven by cold-chain monitoring that must meet pharmaceutical compliance.

Under Industry 4.0, manufacturers adopt private LTE/NB-IoT networks on shop floors to enable condition-based maintenance; productivity gains up to 25% have been recorded in pilot plants. Mining and oil and gas operators use NB-IoT for safety sensors in underground shafts where Wi-Fi is unreliable.

Note: Segment shares of all individual segments available upon report purchase

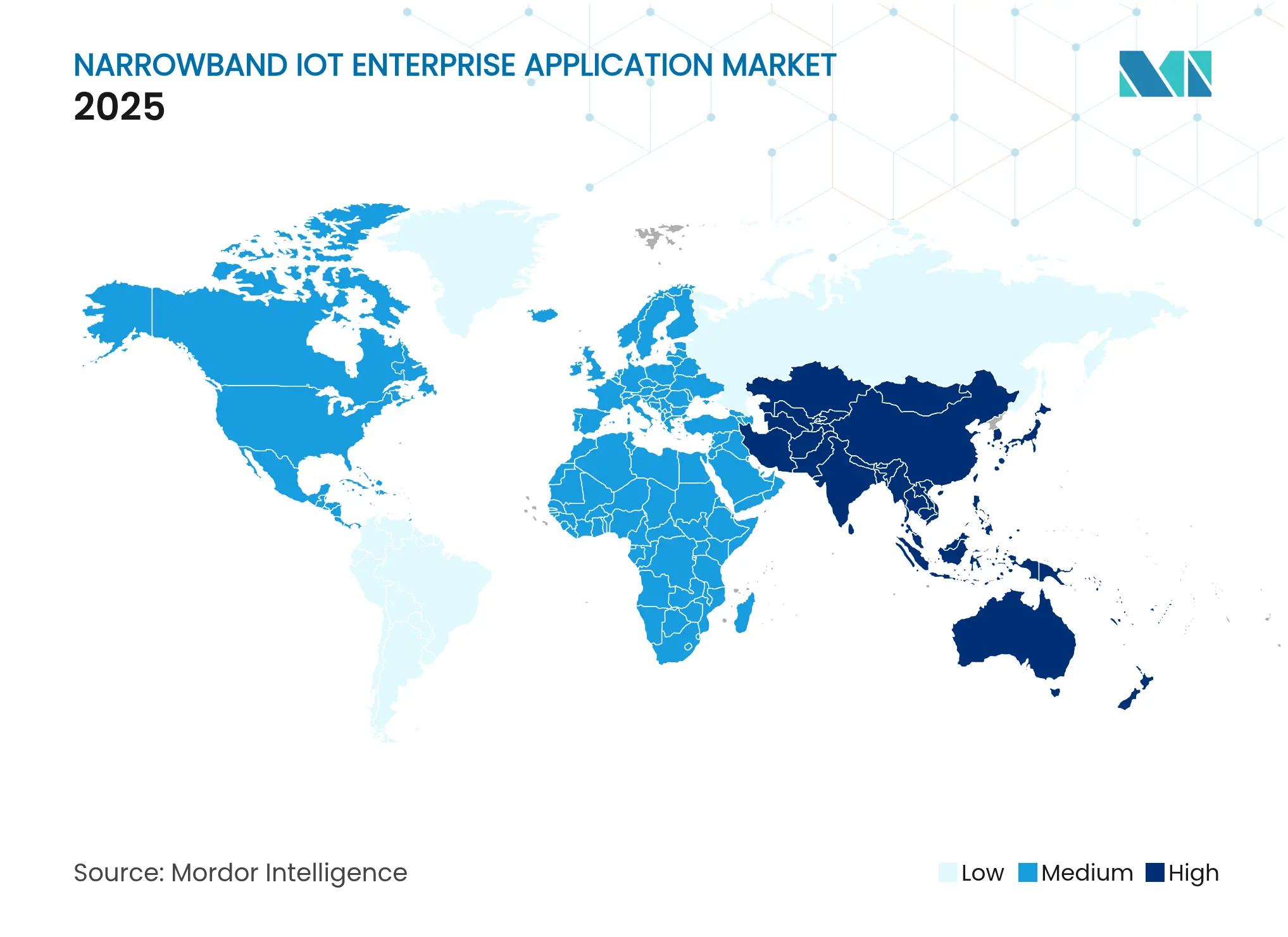

APAC commanded 51.40% of 2025 revenue as China surpassed 2.3 billion cellular IoT connections, outnumbering smartphones. Beijing’s 5.5G build-out covers 70% of the Fourth Ring Road, enabling dense deployments for smart traffic lights and municipal waste bins. Indonesia’s PLN and Huawei fiber program extends backbone capacity that rural NB-IoT base stations rely on. Singapore, Australia, and South Korea top GSMA’s Digital Nations Index, while markets such as Cambodia and Nepal still show double-digit adoption potential.[

Africa is expected to register a 27.1% CAGR outlook as the African Union’s Continental AI Strategy and Broadband Africa Vision 2030 focus on digital inclusion. South Africa’s plan to sunset 2G/3G by 2027 forces utilities and agriculture to shift to LPWA options, and satellite NB-IoT fills extreme coverage gaps. National broadband plans exist in 84% of countries, creating policy frameworks for public–private partnerships.

Europe records steady expansion through legally binding smart-meter targets and CEN-CENELEC standards that ensure cross-border interoperability. North America sees rising industrial private-cellular projects, although roaming fragmentation limits seamless multinational coverage. South America and the Middle East are in early diffusion stages; economic constraints and spotty rural coverage moderate growth until satellite-terrestrial hybrids mature.

Market Concentration

Competition remains fragmented across network, module and application layers. Vodafone manages 205 million IoT connections, offering one-stop device management for multinational clients. China Unicom leverages government contracts to scale NB-IoT in smart cities, while Deutsche Telekom positions itself as an integrator for NTN-IoT through alliances with Skylo and OQ Technology.

Satellite specialists like Sateliot and OQ Technology erode terrestrial exclusivity by extending coverage into maritime, desert, and polar zones. LoRaWAN vendors such as Semtech retain cost leadership in private utilities, causing price pressure on NB-IoT module suppliers. Chipset makers HiSilicon, Nowi, and Sequans focus on energy harvesting to slash maintenance, a persuasive point for SMEs.

Intellectual-property stakes rise as firms patent Release-17 features and Integrated Sensing and Communication (ISAC) capabilities for 6G. The Global Telco AI Alliance, SK Telecom, Deutsche Telekom, e&, Singtel and SoftBank, integrates generative AI into IoT service portals to reduce customer churn. The diversified landscape implies healthy rivalry, yet consolidation is likely among smaller module vendors unable to fund multi-standard R&D.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

NB-IoT is a standards-based low power wide area (LPWA) technology that is developed to enable a wide range of new IoT devices and services. It significantly improves the system capacity, power consumption of user devices, and spectrum efficiency, especially in deep coverage. The technology also provides wide coverage; many connections; low data rates, costs, and power consumption; and optimized architecture. It perfectly satisfies the need for IoT deployment in numerous industries as well as applications.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.