Enterprise IoT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

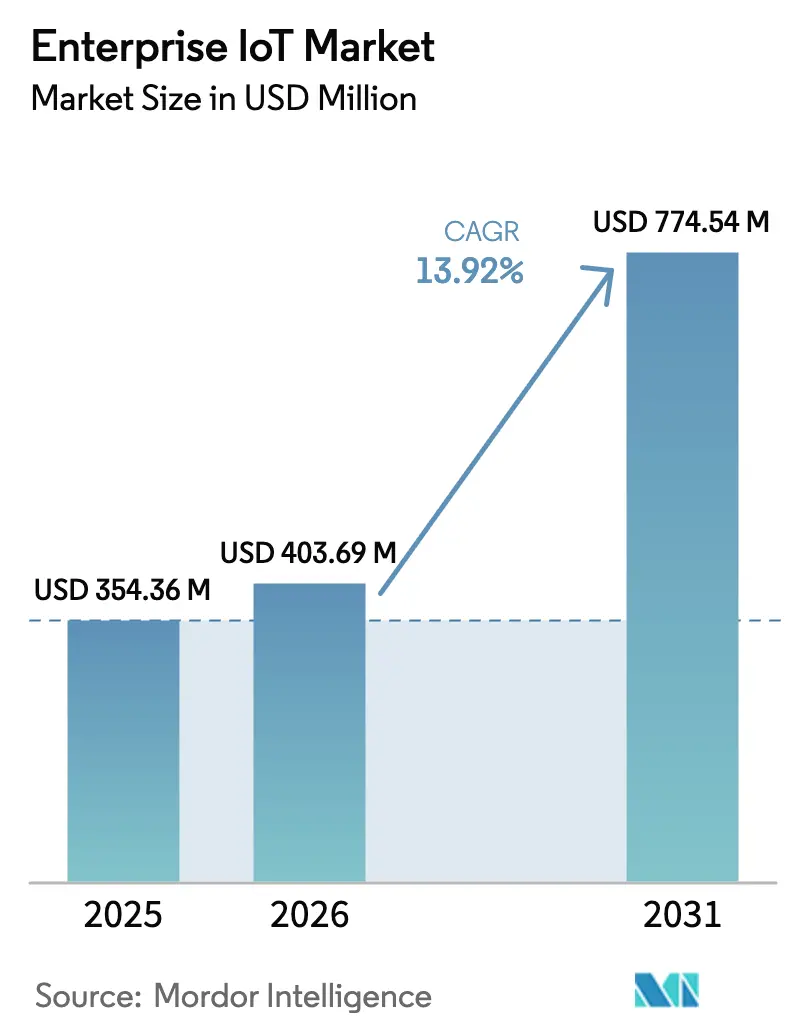

| Market Size (2026) | USD 403.69 Million |

| Market Size (2031) | USD 774.54 Million |

| Growth Rate (2026 - 2031) | 13.92% CAGR |

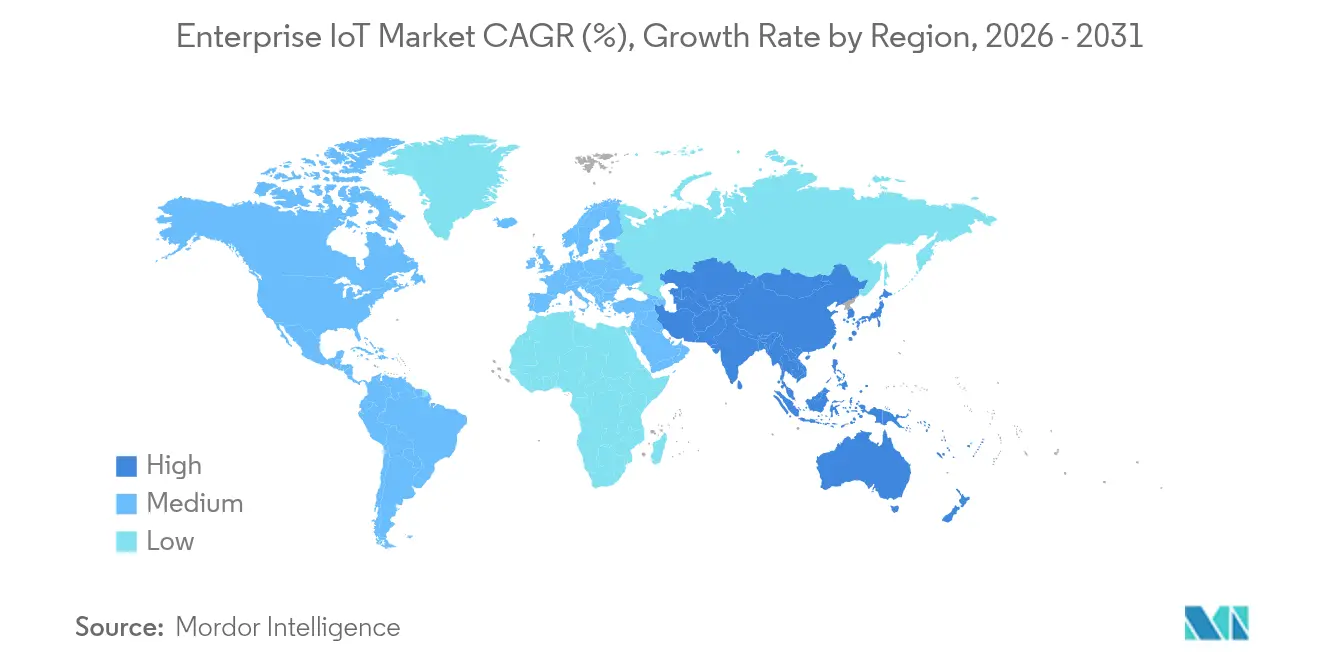

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise IoT Market Analysis by Mordor Intelligence

The Enterprise IoT market size was valued at USD 354.36 million in 2025 and estimated to grow from USD 403.69 million in 2026 to reach USD 774.54 million by 2031, at a CAGR of 13.92% during the forecast period (2026-2031). Accelerated digital-transformation programs, the spread of private 5G networks, and wider access to edge-AI analytics collectively underpin this double-digit growth trajectory. Predictive-maintenance deployments in heavy industry compress unplanned-downtime costs, while smart-energy platforms help enterprises meet tightening sustainability mandates. Device-to-cloud standardization, expanding low-power wide-area (LPWA) coverage, and falling sensor prices lower total cost of ownership and widen the addressable pool of use cases. Competitive intensity remains moderate as technology conglomerates, specialist platform vendors, and telecom operators race to assemble full-stack offerings and secure long-term contracts.

Key Report Takeaways

- By industry vertical, manufacturing led with 26.82% of Enterprise IoT market share in 2025, while energy and utilities is forecast to expand at a 14.52% CAGR to 2031.

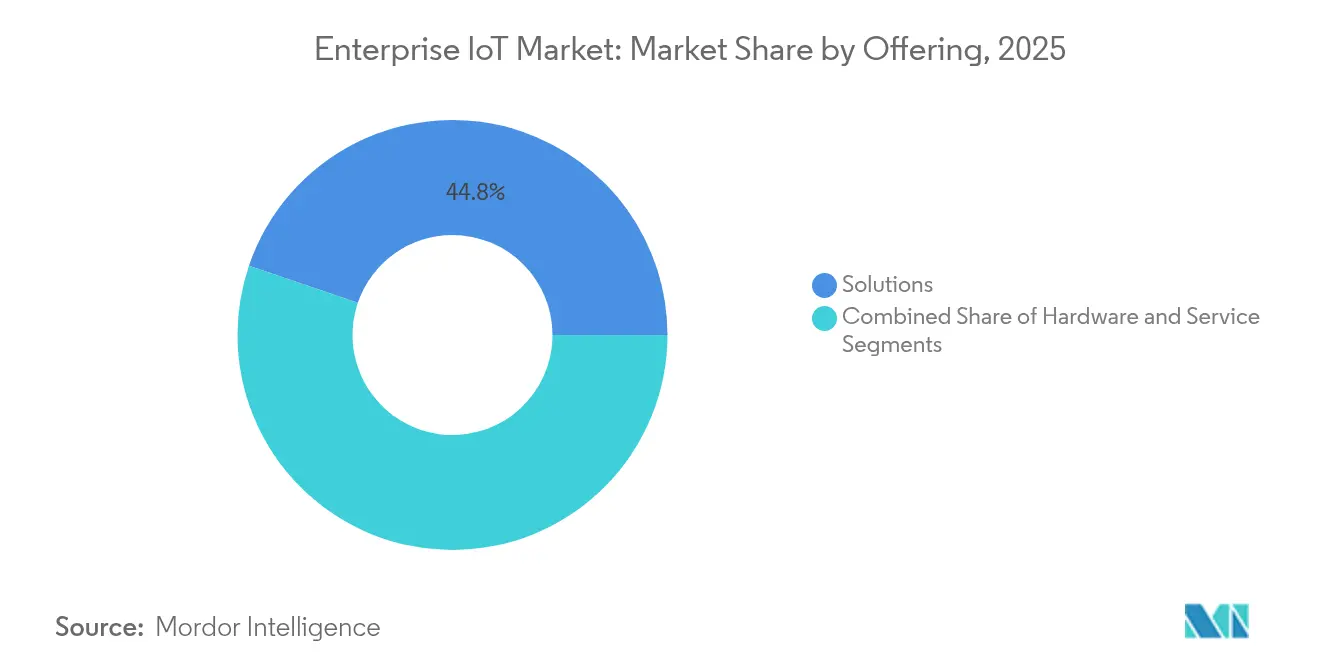

- By offering, the solutions segment accounted for 44.78% revenue share in 2025, whereas services is advancing at a 14.05% CAGR through 2031.

- By enterprise size, large enterprises held 64.12% of the Enterprise IoT market in 2025; small and medium enterprises (SMEs) are growing faster at a 14.88% CAGR.

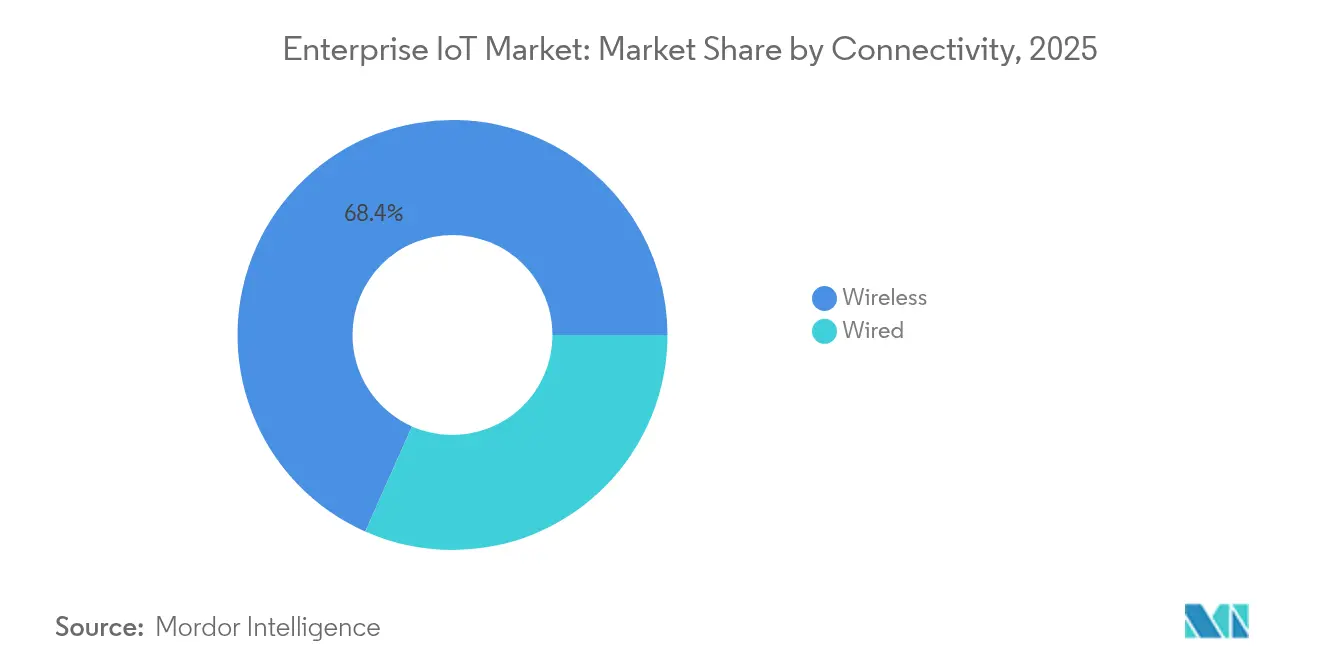

- By connectivity, wireless technologies commanded 68.35% share of the Enterprise IoT market size in 2025 and are set to grow at a 15.96% CAGR through 2031 Mobile .

- By geography, North America led with 31.88% revenue share in 2025, while Asia-Pacific is projected to record the fastest 15.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enterprise IoT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of predictive maintenance in industrial sectors | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growing demand for smart-energy solutions to cut OPEX | +1.8% | Global, led by Asia-Pacific and Europe | Long term (≥ 4 years) |

| Increasing investments in smart-city infrastructure worldwide | +1.5% | Asia-Pacific core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Rapid 5G and LPWA roll-outs enabling massive device density | +2.3% | North America and Asia-Pacific, expanding to Europe | Short term (≤ 2 years) |

| Edge-AI analytics unlocking real-time autonomous operations | +1.9% | Global, with early adoption in manufacturing hubs | Medium term (2-4 years) |

| Enterprise build-out of private LTE/5G networks for secure, low-latency IoT | +2.0% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Predictive Maintenance in Industrial Sectors

Predictive maintenance is shifting factory economics by converting unplanned downtime into pre-scheduled service intervals, thereby maximizing overall equipment effectiveness. General Motors saved USD 20 million annually after deploying an Enterprise IoT market solution that monitors vibration and temperature data across production assets. [1]IoT World Today, “General Motors Saves USD 20 M With Predictive Maintenance,” iotworldtoday.com Machine-learning models identify failure signatures weeks ahead, allowing procurement teams to stage spare parts and technicians to align interventions with production calendars. These improvements raise asset availability while trimming inventory carrying costs for consumables. As more brownfield plants retrofit sensors, the Enterprise IoT market gains resilient recurring revenue streams from analytics subscriptions and edge-AI inference engines.

Growing Demand for Smart-Energy Solutions to Cut OPEX

Enterprises integrating granular consumption metering with automated demand-response orchestration achieve measurable energy-cost reductions and stronger compliance with carbon-reporting mandates.[2]RCR Wireless News, “Nokia Adds 55 Private-Wireless Customers in Q4 2024,” rcrwireless.com Telia’s rollout of 2 million smart meters lowered Nordic utility operating expenses by 25% and enhanced grid reliability, underscoring the financial rationale for energy digitalization. IoT-enabled energy management converts buildings into dynamic assets that can participate in flexibility markets, creating fresh revenue channels. Corporate net-zero pledges accelerate solution adoption, reinforcing the Enterprise IoT market growth narrative across facilities management, data centers, and distribution warehouses.

Rapid 5G and LPWA Roll-outs Enabling Massive Device Density

Private 5G networks provide deterministic latency below 10 milliseconds and prioritized quality-of-service that wired Ethernet historically delivered.[3]StockTitan, “Qualcomm and Honeywell to Integrate AI at the Edge for Energy,” stocktitan.net Nokia added 55 new private-wireless customers in Q4 2024, bringing its installed base to roughly 850 deployments and proving enterprise appetite for licensed-spectrum autonomy. LPWAN alternatives such as NB-IoT and LoRaWAN support battery-operated sensors that communicate small payloads over multi-year lifetimes. Together, these technologies unlock unified campus coverage for robotics, augmented-reality work instructions, and hazardous-asset monitoring—fueling sustained Enterprise IoT market expansion.

Edge-AI Analytics Unlocking Real-Time Autonomous Operations

Edge inference moves decision-making closer to machine tools, slashing backhaul latency and mitigating bandwidth bottlenecks. Qualcomm and Honeywell linked AI-powered chipsets with process-control platforms to identify anomalies in milliseconds, enhancing worker safety in upstream energy fields. Localized learning safeguards sensitive intellectual property by avoiding unnecessary cloud egress, a key selling point for pharma and defense manufacturers. As edge hardware matures, enterprises can tailor proprietary algorithms, embedding competitive differentiation directly into physical operations and stimulating additional Enterprise IoT market demand for developer tools and lifecycle-management services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability and integration complexity across multi-vendor stacks | -1.2% | Global, particularly acute in Europe due to regulatory fragmentation | Medium term (2-4 years) |

| Escalating data-privacy and cybersecurity threats | -1.5% | Global, with heightened impact in North America and Europe | Short term (≤ 2 years) |

| eSIM lifecycle-management and roaming-compliance hurdles | -0.8% | Global, with particular challenges in emerging markets | Long term (≥ 4 years) |

| Sustainability rules raising total lifecycle carbon-cost of connected assets | -0.9% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interoperability and Integration Complexity Across Multi-Vendor Stacks

Enterprises often operate decades-old supervisory-control systems that cannot natively communicate with modern IoT platforms. Custom middleware bridges impose engineering overhead and introduce single points of failure that erode projected return on investment. Fragmented European privacy regulations add further integration friction because data residency and encryption requirements vary by country. Such complexity extends sales cycles and inflates project budgets, tempering Enterprise IoT market acceleration until open standards, including the GSMA’s new eSIM specification, gain wider traction.

Escalating Data-Privacy and Cybersecurity Threats

Every additional sensor becomes a potential attack vector, and many low-cost devices lack secure boot or patch mechanisms. High-profile ransomware incidents have already forced multi-day shutdowns at automotive assembly plants, highlighting the business-critical nature of IoT security. Enterprises must now invest in zero-trust architectures, device-centric encryption, and continuous threat monitoring, adding 7%–10% to total deployment budgets according to vendor disclosures. These extra costs slightly dampen Enterprise IoT market growth but simultaneously spawn ancillary opportunities for specialist cybersecurity suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Accelerate Time-to-Value

The services sub-segment of the Enterprise IoT market is forecast to advance at a 14.05% CAGR, eclipsing hardware revenue growth because many enterprises prefer outcome-based managed contracts over internal builds. System-integration partners bundle cloud orchestration, cybersecurity, and lifecycle governance, compressing pilot-to-production timelines. Concurrently, the solutions category retains the largest 44.78% share of Enterprise IoT market size, covering sensor nodes, gateways, and middleware that anchor every deployment.

Hardware demand is shifting toward edge-AI-capable gateways that preprocess voluminous data streams and filter only actionable insights to cloud dashboards. Software revenue grows from license renewals and developer-platform subscriptions that embed analytics micro-services into bespoke manufacturing execution systems. Qualcomm and STMicroelectronics plan to ship AI-enhanced STM32 reference designs in 2025, promising stronger compute at lower power budgets.

By Enterprise Size: SMEs Embrace Cloud Platforms

Large organizations still dominate spending, controlling 64.12% of 2025 revenue thanks to complex brownfield estates and deep capital reserves. They deploy multi-site architectures with federated data-lakes, driving significant consulting and customization sales. However, SMEs inject dynamism into the Enterprise IoT market with a 14.88% CAGR through 2031 as hyperscale clouds abstract gateway management and embed low-code orchestration templates.

Subscription pricing aligns operating expenditure with usage, letting mid-market manufacturers digitize a single production line before scaling across plants. Intel and Arm’s Emerging Business Initiative further democratizes access by supplying start-ups with foundry-backed system-on-chip design resources that shrink prototyping cycles. As barriers fall, SMEs’ collective spending power becomes a material contributor to overall Enterprise IoT industry momentum.

By Connectivity: Wireless Consolidates Leadership

Wireless standards, spanning private 5G, Wi-Fi 6E, Zigbee, Bluetooth LE, NB-IoT, and LoRaWAN, captured 68.35% of Enterprise IoT market share in 2025 and will grow fastest at 15.96% CAGR. Private 5G ensures deterministic latency for autonomous mobile robots and augmented-reality workflows on factory floors. LPWA protocols extend asset-tracking coverage to remote agricultural plots, offshore rigs, and rolling stock.

Hybrid networking strategies are emerging where time-sensitive workloads ride licensed-spectrum slices, and non-critical telemetry flows through unlicensed LoRaWAN gateways, optimizing both performance and cost. Verizon and Nokia’s UK private-5G agreement illustrates the growing export of early-adopter know-how beyond North America, reinforcing global Enterprise IoT market expansion.

By Industry Vertical: Manufacturing Holds Pole Position

Manufacturing contributed 26.82% of 2025 revenue, cementing its role as the largest adopter segment within the Enterprise IoT market. Predictive maintenance, closed-loop quality control, and digital-twin simulations improve overall equipment effectiveness and shorten design-to-production cycles.

Energy and utilities posts the highest 14.52% CAGR through 2031 as smart-grid modernization integrates renewables, distributed storage assets, and bidirectional electric-vehicle charging nodes. Transportation, healthcare, and agriculture also scale deployments: condition-based rail maintenance reduces freight-line delays, tele-ICU platforms extend specialist care into rural clinics, and precision-irrigation sensors conserve water in arid regions—each reinforcing diversified Enterprise IoT market expansion.

Geography Analysis

North America, with 31.88% of 2025 revenue, leverages mature cloud ecosystems, abundant venture capital, and early regulatory clarity to sustain leadership in the Enterprise IoT market. Manufacturers deploy private 5G alongside autonomous vehicles that shuttle work-in-progress components, while utilities capitalize on advanced metering infrastructure to balance renewable generation inputs. Cybersecurity frameworks such as NIST 800-213 steer procurement toward certified chipsets and hardened operating systems, elevating trust among risk-averse boards.

Asia-Pacific delivers the fastest 15.21% CAGR as governments earmark billions for smart-city pilots, next-generation 5G build-outs, and industrial-automation subsidies. China, Japan, and South Korea anchor regional scale, yet Southeast Asian nations follow rapidly by adopting virtual cellular networks that bypass legacy Wi-Fi limitations. Malaysia’s 5G-first headquarters demonstrator showcases low-latency benefits for immersive collaboration suites, reinforcing policy momentum toward nationwide Enterprise IoT market adoption.

Competitive Landscape

Competition is moderate, with the top 10 suppliers controlling 45% of revenue, leaving ample whitespace for niche specialists to thrive. Integrated players such as Cisco, Siemens, and Microsoft package cloud-edge orchestration, security, and analytics under unified license agreements, simplifying vendor management for multinational buyers. Telecommunications operators, including AT&T, Vodafone, and Telefónica, strengthen value propositions by bundling connectivity, SIM lifecycle management, and managed services for one monthly fee.

Vertical-specific disruptors differentiate through domain expertise: Uptake codes ML models that predict locomotive bearing failures, while Wiliot pioneers battery-free ambient-IoT tags for fast-moving consumer goods. M&A activity intensifies as chip vendors expand into software; Qualcomm’s USD 200 million acquisition of Sequans’ 4G IoT portfolio deepens cellular-IoT IP holdings and shortens go-to-market for integrated modem-AI chipsets. Strategic alliances bloom: Ericsson partners Google Cloud to launch on-demand core-network SaaS, enabling telcos to spin up services in hours rather than months. These moves collectively accelerate Enterprise IoT market innovation while raising barriers for new entrants lacking ecosystem breadth.

Enterprise IoT Industry Leaders

Microsoft Corporation

Samsung Electronics Co., Ltd.

Siemens AG

Cisco Systems, Inc.

Qualcomm Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Ericsson and Google Cloud unveiled “Ericsson On-Demand,” a SaaS core-network platform that shortens deployment cycles for operator enterprise services.

- June 2025: Intel, Qualcomm, PepsiCo, Infineon, and Wiliot created the Ambient IoT Alliance to advance battery-free, object-powered sensing.

- May 2024: Nokia became the first provider to deliver cloud-native 5G voice core on a public cloud with Boost Mobile, boosting flexible IoT connectivity infrastructure.

- March 2025: Digital Nasional Berhad and Ericsson activated the world’s first 5G-first office at DNB headquarters, eliminating Wi-Fi in favor of enterprise virtual cellular networking.

Global Enterprise IoT Market Report Scope

The enterprise IoT market refers to the deployment of Internet of Things (IoT) technologies within businesses to connect devices, systems, and processes. It enables real-time data collection, analysis, and automation, improving operational efficiency and decision-making. This market spans various industries, including manufacturing, logistics, healthcare, and retail, fostering innovation and digital transformation.

The Enterprise IoT Market is segmented by offering (hardware (sensors, actuators, edge devices/gateways, networking equipment (routers, switches), and other hardware devices), software, services (professional services, managed services)), by enterprise size (large enterprises, small and medium enterprises), by connectivity (wired, wireless (cellular (3g, 4g LTE, 5g), wi-fi, Bluetooth/BLE, Zigbee, LoRaWAN, NB-IoT satellite communication), by industry vertical (manufacturing, energy & utilities, transportation & logistics, retail, healthcare, agriculture, hospitality, government and other industry verticals), and geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). the market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware | Sensors |

| Actuators | |

| Edge Devices/Gateways | |

| Networking Equipment (Routers, Switches) | |

| Other Hardware Devices | |

| Solutions | |

| Services | Professional Services |

| Managed Services |

| Large Enterprises |

| Small and Medium Enterprises |

| Wired | |

| Wireless | Cellular (3G, 4G LTE, 5G) |

| Wi-Fi | |

| Bluetooth/BLE | |

| Zigbee | |

| LoRaWAN | |

| NB-IoT | |

| Satellite Communication |

| Manufacturing |

| Energy and Utilities |

| Transportation and Logistics |

| Retail |

| Healthcare |

| Agriculture |

| Hospitality |

| Government |

| Other Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Offering | Hardware | Sensors | |

| Actuators | |||

| Edge Devices/Gateways | |||

| Networking Equipment (Routers, Switches) | |||

| Other Hardware Devices | |||

| Solutions | |||

| Services | Professional Services | ||

| Managed Services | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Connectivity | Wired | ||

| Wireless | Cellular (3G, 4G LTE, 5G) | ||

| Wi-Fi | |||

| Bluetooth/BLE | |||

| Zigbee | |||

| LoRaWAN | |||

| NB-IoT | |||

| Satellite Communication | |||

| By Industry Vertical | Manufacturing | ||

| Energy and Utilities | |||

| Transportation and Logistics | |||

| Retail | |||

| Healthcare | |||

| Agriculture | |||

| Hospitality | |||

| Government | |||

| Other Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Enterprise IoT market?

The Enterprise IoT market stands at USD 403.69 million in 2026 and is projected to reach USD 774.54 million by 2031 at a 13.92% CAGR

Which industry vertical spends the most on Enterprise IoT solutions?

Manufacturing leads with 26.82% of 2025 revenue due to large-scale predictive-maintenance and quality-control deployments.

Why are services growing faster than hardware in Enterprise IoT deployments?

Enterprises favor managed-service contracts that shorten pilot cycles and reduce in-house skill gaps, driving a 14.05% CAGR for the services segment

How critical is wireless connectivity to future Enterprise IoT growth?

Wireless technologies, especially private 5G and LPWA, hold 68.35% market share and are expanding at 15.96% CAGR, enabling ultra-reliable low-latency links for mission-critical workloads.

Page last updated on: