Indonesia Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

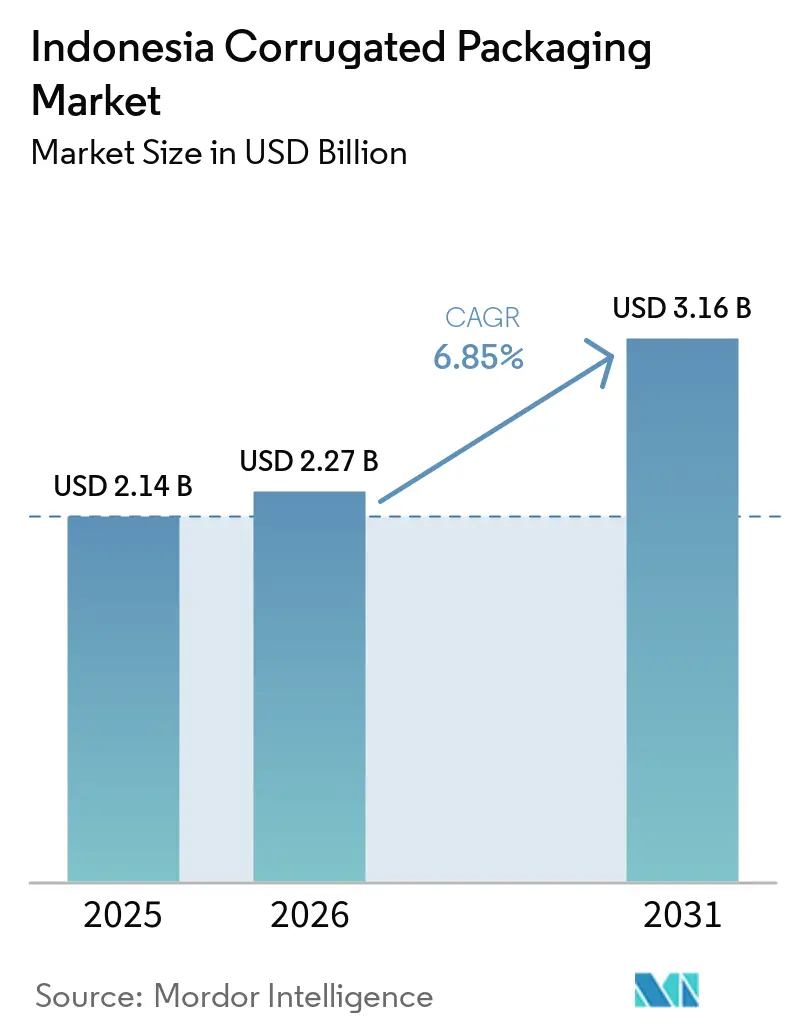

| Base Year Market Size (2025) | USD 2.14 Billion |

| Market Size (2026) | USD 2.27 Billion |

| Market Size (2031) | USD 3.16 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

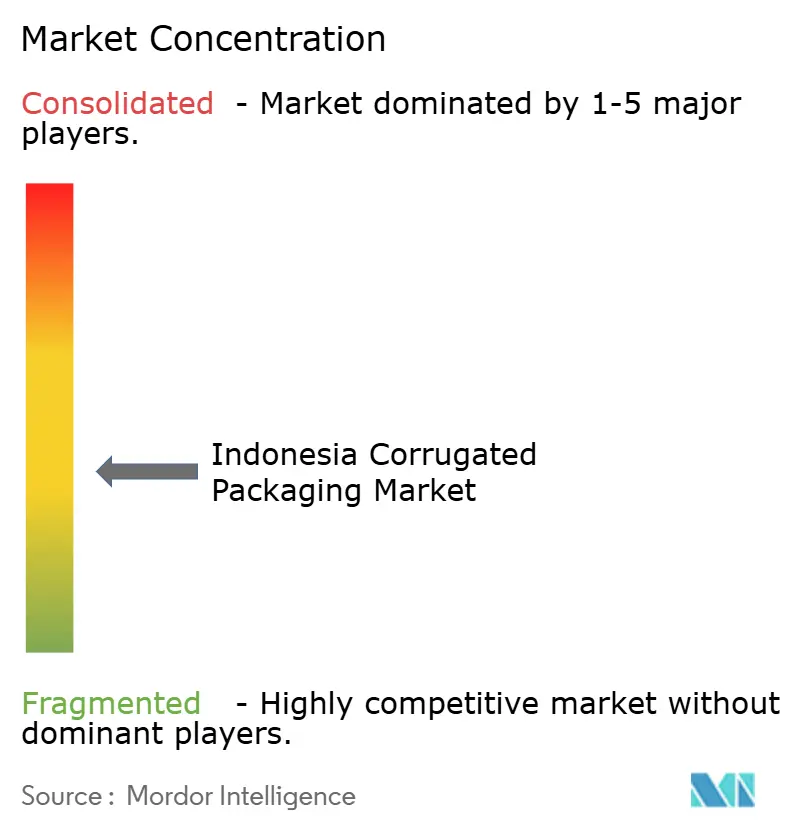

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Corrugated Packaging Market Analysis by Mordor Intelligence

The Indonesia corrugated packaging market size is expected to increase from USD 2.14 billion in 2025 to USD 2.27 billion in 2026 and reach USD 3.16 billion by 2031, growing at a CAGR of 6.85% over 2026-2031. A trio of structural shifts is propelling this advance in rapid retail digitization, national mandates substituting plastic for fiber, and new domestic pulp and paper capacity that cushions converters against volatility in imported feedstock. Brand owners now view the box as an extension of digital storefronts, prompting accelerated adoption of thinner flutes, custom die-cut styles, and high-graphic surfaces that elevate the unboxing moment. Converters capable of pairing recycled linerboard with water-based flexographic or digital inkjet workflows are capturing wallet share as small and medium enterprises scale direct-to-consumer channels. Simultaneously, the integration of old corrugated containers, biomass energy, and right-sizing automation is shifting the industry playbook toward cost leadership with measurable sustainability credentials. Competitive intensity remains elevated because roughly three-quarters of national capacity still sits idle, rewarding vertically integrated players that can hedge fiber prices and undercut spot-market rivals.

Key Report Takeaways

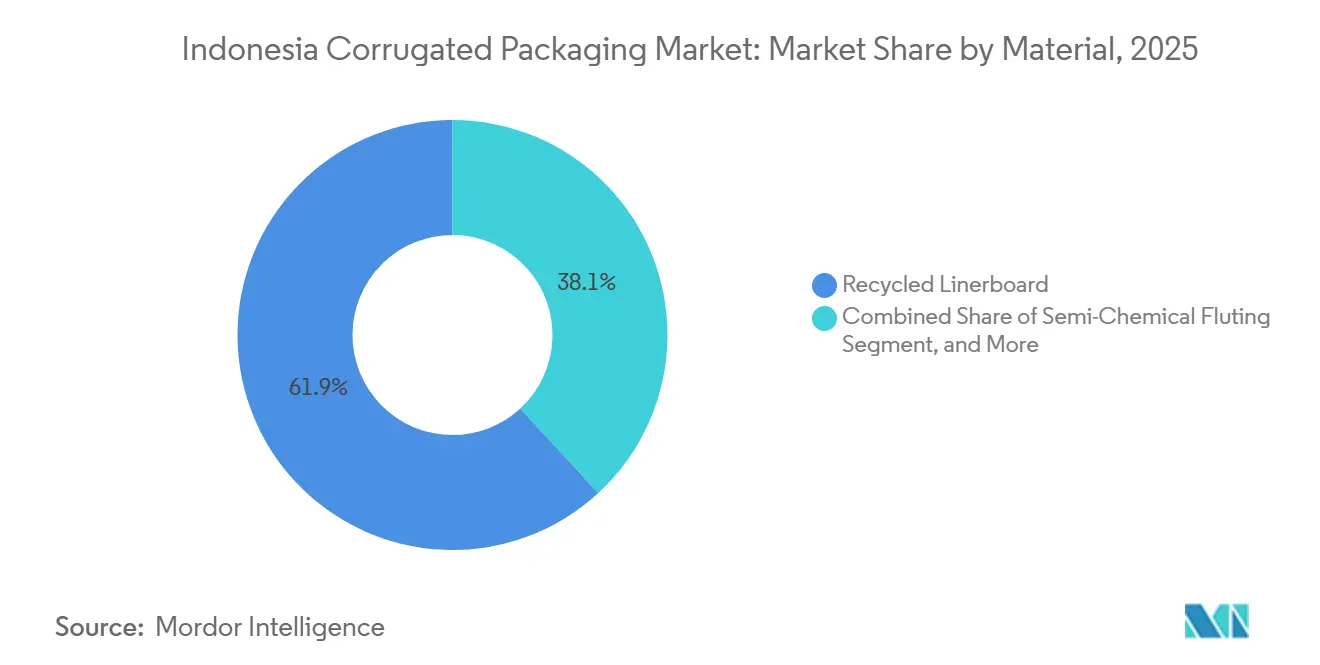

- By material, recycled linerboard captured 61.86% of the Indonesia corrugated packaging market share in 2025.

- By flute type, the Indonesia corrugated packaging market size for the E flute segment is forecast to advance at an 8.08% CAGR through 2031.

- By packaging type, regular slotted containers captured 51.60% of the Indonesia corrugated packaging market share in 2025.

- By wall type, the Indonesia corrugated packaging market size for the double-wall segment is forecast to advance at an 8.28% CAGR through 2031.

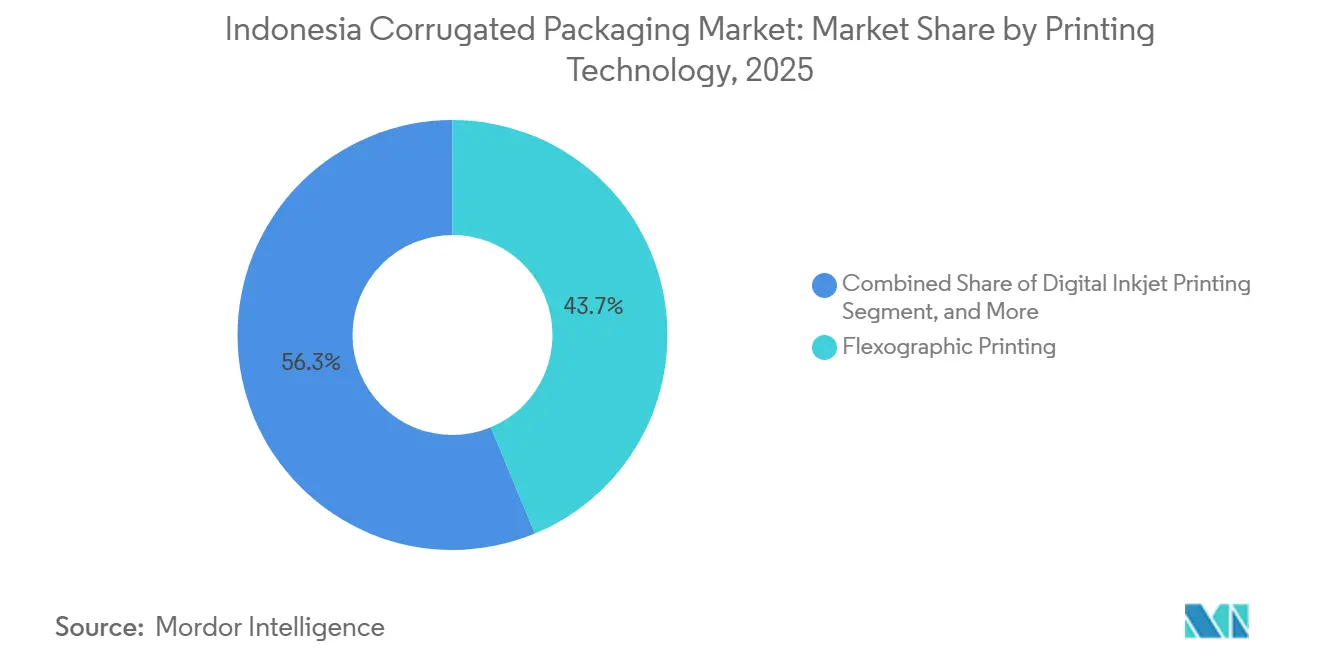

- By printing technology, flexographic printing captured 43.74% of the Indonesia corrugated packaging market share in 2025.

- By end user, the Indonesia corrugated packaging market size for the e-commerce fulfillment centers segment is forecast to advance at an 8.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in E-Commerce Shipments | +1.80% | National, focused on Greater Jakarta, Surabaya, Medan | Short term (≤ 2 years) |

| Plastic-Reduction Policies Accelerating Fiber Adoption | +1.50% | National, stricter in Jakarta, Bali, tourist zones | Medium term (2-4 years) |

| Expansion of Indonesia's Processed Food Industry | +1.20% | West Java, East Java, North Sumatra clusters | Medium term (2-4 years) |

| Growth of Domestic Pulp and Paper Capacity | +1.00% | West Java, South Sumatra mills | Long term (≥ 4 years) |

| Advances in Digital and Flexographic Printing for Short Runs | +0.80% | Jakarta, Surabaya, Semarang converters | Medium term (2-4 years) |

| Investment in Automated Fulfilment Boosting Right-Sized Boxes | +0.60% | Greater Jakarta, Surabaya hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in E-Commerce Shipments

Indonesia’s booming parcel economy is redefining box design as platforms optimize packaging to avoid dimensional-weight tariffs and improve last-mile efficiency. Daily sales on major social-commerce channels now spawn millions of micro-orders that favor thinner E and F flutes, right-sized die-cuts, and rapid art changes. Fulfillment centers are installing automated cutters that reduce void space by up to 20 percent, compelling converters to provide on-demand blanks rather than pre-made regular slotted containers. The absence of a unified national recyclability standard adds compliance complexity for cross-border sellers, so outsized parcels often revert to heavier gauges to guarantee intact returns. As the internet economy expands beyond Java, converters that synchronize just-in-time deliveries with regional hubs are best placed to ride the e-commerce wave.[1]DHL, “Indonesia Internet Economy Overview,” dhl.com

Plastic-Reduction Policies Accelerating Fiber Adoption

Extended Producer Responsibility rules and localized plastic bans are nudging brands toward fiber-based secondary packaging. The government’s circular roadmap aims to achieve complete waste management by 2029, prompting retailers in Jakarta and Bali to switch from shrink wrap to corrugated trays and folding cartons.[2]Indonesia Ministry of Environment and Forestry, “National Waste Management Progress,” menlhk.go.id Multinationals now require ISO 14001 certification from suppliers, lifting entry barriers for smaller box plants. Adoption, however, is uneven, as only 60 percent of urban residents have access to formal waste collection, limiting effective recycling in secondary cities.[3]World Wildlife Fund Indonesia, “Indonesia Plastic Action Partnership,” wwf.id This regulatory mosaic creates openings for converters that pair green credentials with region-specific supply chains.

Expansion of Indonesia's Processed Food Industry

USD 22 billion in agricultural-processing investment is expanding demand for shipping containers that can withstand humid transit and multi-modal routes.[4]Reuters, “Indonesia Agricultural Processing Investment,” reuters.com Liquid food processors are shifting toward triple-wall cases that pass International Safe Transit Association testing for export consignments. Instant-noodle makers are ditching shrink-wrapped trays in favor of litho-laminated corrugated for shelf appeal, though higher ink coverage squeezes converter margins. Government food-safety modernization, requiring tamper-evident seals and traceability labels, further tilts the balance toward rigid fiber packaging over flexible plastic.

Growth of Domestic Pulp and Paper Capacity

Large-scale mill expansions in West Java and South Sumatra are trimming Indonesia’s import dependence and stabilizing linerboard pricing. A newly commissioned 2,000 tonnes-per-day old-corrugated-containers line yields premium testliner while reducing freshwater use. Integrated producers lock in fiber costs, shielding downstream box operations from global pulp swings. Still, a temporary global oversupply in 2024 drove pulp prices to USD 520-540 per tonne, delaying a full margin recovery until capacity utilization climbs past 90 percent.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in OCC / Pulp Prices | -1.20% | Jakarta, Surabaya non-integrated converters | Short term (≤ 2 years) |

| Rising Energy and Logistics Costs | -0.90% | Outer islands Kalimantan, Sulawesi, Maluku | Medium term (2-4 years) |

| Humidity-Driven Strength Loss Requiring Costly Barriers | -0.70% | Coastal and equatorial zones | Long term (≥ 4 years) |

| Fragmented Scrap-Collection and Low Recycling Rates | -0.60% | Secondary cities, rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in OCC / Pulp Prices

In January 2026, old-corrugated-container exports from the United States reached USD 130 per short ton, and Indonesia’s compulsory inspections added extra cost to spot purchases. Bleached hardwood kraft pulp tracked near USD 530 per tonne late in 2025, yet looming Chinese demand weakness threatens another dip. Every USD 50 swing in pulp pricing materially alters the profit trajectories of converters without vertical integration. Such volatility forces many mid-tier players to delay automation or digital-printing upgrades, locking them into low-margin commodity segments.

Rising Energy and Logistics Costs

Grid-tariff uncertainty and transport surcharges erode the lightweighting savings that corrugated aims to deliver. Inter-island freight from Java to Kalimantan or Sulawesi can exceed 20 percent of the delivered cost because converter hubs cluster in Java. Outer-island distributors, therefore, favor thicker, damage-resistant boxes to offset multiple handling nodes. Although new toll roads and port projects are easing congestion in Java and Sumatra, progress remains slow farther east, sustaining regional price gaps that dampen package innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Feedstock Anchors Cost Leadership

The Indonesia corrugated packaging market drew 61.86% of 2025 material revenue from recycled linerboard, validating domestic investments in old-corrugated-containers recovery. Virgin Kraft grades remain mandatory for export-oriented food and pharma shippers wanting moisture resistance, yet rising carbon reporting costs keep their share modest. Corrugating medium, the backbone of flute structure, is on track for a 7.20% CAGR, paced by converters trimming basis weight while protecting box compression. Semi-chemical fluting still secures premium appliance and pallet cases due to its superior stiffness-to-weight, though its larger energy footprint limits mainstream adoption. Mills now mix imported and local scrap to hit burst-strength targets after contamination issues reduced fiber yield in several urban collection streams. The Indonesian corrugated packaging market, therefore, rewards mills that install advanced drum pulpers that achieve higher yields and freshwater savings.

Second-order effects ripple through converter buying. Chain-of-custody-certified linerboard is now featured in bids from multinational customers seeking Scope 3 cuts, increasing documentation requirements for smaller sheet plants. Meanwhile, specialty moisture-barrier coatings, priced 10-15% above uncoated stock, gain ground in tropical export lanes despite budget pushback from domestic food producers. Integrated players leveraging biomass power and solar arrays further widen cost gaps as grid tariffs climb, underscoring why scale plus in-house fiber remains the long-term hedge within the Indonesia corrugated packaging market.

By Flute Type: E Flute Gains as Cube Efficiency Trumps Cushioning

C flute supplied 42.50% of 2025 volume because its 4 mm caliper balances stacking and cushioning for noodles, oils, and beverages. E flute, at roughly 1.6 mm, is sprinting ahead at an 8.08% CAGR as e-commerce hubs chase dimensional-weight savings per parcel. Digital printers praise E and F flutes for smoother surfaces that improve image resolution, enabling brands to print social media graphics directly on shipping cases.

B flute, historically favored for retail displays, is under pressure as marketers migrate to lighter walls and engineered inserts that handle shock separately from the corrugated structure. A flute remains a niche guardrail for fragile glassware, while microflute designs slot into folding carton hybrids that merge graphics with shipping protection. Because converting E flute needs tighter gaps and cleaner liner, integrated producers with on-site testliner enjoy fewer crush rejects, sharpening their edge in the Indonesia corrugated packaging market.

By Packaging Type: Customization Erodes Commodity Box Share

Regular slotted containers still captured 51.60% of revenue, yet die-cut custom boxes are sprinting at 9.10% as direct-to-consumer labels treat packages as billboards. Right-sizing systems within automated fulfillment now demand variable-depth blanks, prompting converters to stock broader die libraries. Folding cartons cling to premium cosmetics and pharmaceuticals where high-definition offset print wins shelf battles, but their limited cushioning curbs broader penetration.

Point-of-purchase displays are resurging as modern grocery chains simplify in-store labor, although fragile assemblies add logistics risk. Triple-wall pallet boxes defend heavy industrial lanes but concede share to reusable plastic totes in domestic automotive flows. The Indonesia corrugated packaging market thus tilts toward converters that bundle graphic design, rapid prototyping, and small-lot scheduling under one roof.

By Wall Type: Export and Heavy-Duty Segments Lift Double-Wall

Single-wall occupied 50.12% of 2025 turnover, as it remains adequate for most intra-Java transport routes with relatively low handling risks. Double-wall is projected to grow at an 8.28% CAGR, supported by battery shipments and ocean freight that require higher edge-crush strength and puncture resistance. Integrated mills capable of producing custom-calendered, higher-basis-weight liners are securing long-term double-wall contracts, reinforcing scale advantages within the Indonesia corrugated packaging market.

Triple-wall remains limited to specialized applications such as export-oriented machinery racks, where maximum strength is essential but high paper consumption restricts widespread adoption. At the same time, single-face wrap continues to decline as alternatives like air pillows and molded-pulp cushioning gain share in void-fill applications. These shifts reflect evolving material preferences and cost-efficiency priorities across the packaging value chain.

By Printing Technology: Digital Gains but Flexo Retains Volume Leadership

Flexography held a 43.74% share due to its ability to run water-based inks efficiently on recycled liner while maintaining high production speeds. Digital inkjet is projected to grow at a 9.31% CAGR, driven by plate-free operations and significantly reduced lead times that appeal to small businesses with frequent product launches. Hybrid workflows are increasingly adopted, splitting solid print areas between flexo and variable data, and separating inkjet for customization.

Litho-lamination continues to deliver superior graphic quality but faces scrutiny due to the adhesive layers that complicate recycling. Converters across Jakarta, Surabaya, and Semarang are investing in inline quality-control cameras and predictive maintenance systems to improve color consistency and machine uptime. Meanwhile, screen printing and UV flexo remain limited to ultra-premium applications requiring specialized textures or metallic finishes.

By End User: E-Commerce Disrupts Food’s Dominance

Processed foods accounted for 32.52% of 2025 sales, driven by categories such as instant noodles, snack chips, and cooking oils, which move through humid supply chains that favor C flute structures. E-commerce fulfillment centers are projected to expand at an 8.52% CAGR through 2031, leading to smaller order sizes and increasing demand for high-quality graphics. Beverage multipacks continue to drive steady tray demand, although intense brand competition is placing pressure on converter margins.

Fresh produce volumes are gradually increasing as cold-chain infrastructure expands, driving demand for ventilated corrugated boxes with moisture-resistant linings. Electronics and lithium-ion battery shipments rely on double-wall packaging with anti-static foam or thermal liners, offering higher average selling prices despite lower volumes. Personal-care and pharmaceutical brands are adopting digital printing with serialized QR codes and tamper-evident designs, reinforcing the importance of agile customization in the Indonesia corrugated packaging market.

Geography Analysis

Greater Jakarta and West Java account for roughly half of the national corrugating capacity because the metro area hosts consumer-goods factories, seaports, and booming e-commerce hubs. Surabaya and East Java contribute nearly 30% as processed-food clusters and electronics assemblers anchor demand, while Central Java’s industrial estates in Semarang, Kendal, and Batang capture close to 10% as investors chase lower land and labor costs. Outer islands such as Sumatra, Kalimantan, and Sulawesi mainly source boxes from Java, adding freight premiums that can reach 30% of the delivered cost and dampening the adoption of lightweight custom formats. The Indonesian corrugated packaging market, therefore, remains heavily Java-centric, exposing supply chains to congestion or natural-disaster risk.

Regional production hubs are emerging. A 60,000-tonnes-per-year plant in Pekanbaru, Riau Province, demonstrates Sumatra’s viability for local sourcing and faster turnaround. Likewise, continuous expansion by multi-site converters across Bekasi, Gresik, and Kendal shows a deliberate build-out along national toll-road corridors, enabling just-in-time drops to food and auto customers while shaving working capital. Yet eastern Indonesia lags due to limited cold-chain infrastructure and port depth, which sustain higher shipping surcharges and constrain package innovation. The Indonesian corrugated packaging industry consequently balances scale efficiencies in Java against rising incentives to de-risk through diversified regional plants.

Government infrastructure upgrades, new toll roads, ramp-ups at Patimban Port, and inter-island Ro-Ro services are chipping away at logistics penalties, especially in Java and Sumatra. Still, recycled-content targets hinge on urban waste-collection networks that remain patchy outside major cities, capping feedstock quality for mills pursuing high-strength testliner. As social-commerce apps expand into tier-two cities, converters able to stage board or convert on-site will secure first-mover status in the Indonesian corrugated packaging market.

Competitive Landscape

Roughly 100 medium-to-large converters belong to formal trade groups, while an estimated 500 small family plants compete on price in local niches, leaving industry-wide utilization below 75% and steering the Indonesia corrugated packaging market toward chronic margin pressure. Cost leadership belongs to integrated giants that own pulp and linerboard, such as PT Indah Kiat and PT Pabrik Kertas Tjiwi Kimia, which weather old corrugated container swings better than sheet-only rivals. Foreign strategics Rengo, Oji Holdings, and SCG Packaging continue to pursue bolt-on acquisitions, exemplified by Rengo’s 60% stake in Mypak, to secure regional redundancy for multinational customers.

Technology bifurcation is stark. Leading groups deploy digital presses, automated die-cutters, and inline inspection that enable profitable runs under 1,000 units, while smaller plants cling to legacy machinery and manual QC. New entrants aim for white spaces in pharmaceutical serialization, moisture-resistant produce boxes, and battery-grade double-wall segments, demanding capex and certifications many independents cannot afford. Geographic spread also differentiates players; PT Satyamitra Kemas Lestari’s Batang plant cuts transit times to East Java clients by over a day compared with its Tangerang base, sharpening its bid competitiveness. Sustainability is the latest competitive axis, with mills showcasing biomass boilers and rooftop solar arrays to meet retailer scorecards and win export accounts in the Indonesia corrugated packaging market.

Indonesia Corrugated Packaging Industry Leaders

PT Indah Kiat Pulp & Paper Tbk

PT Pabrik Kertas Tjiwi Kimia Tbk

PT Pabrik Kertas Indonesia (Pakerin)

PT Fajar Surya Wisesa Tbk

PT Industri Pembungkus Internasional

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: KION Group opened a warehouse-automation facility that supplies robotic picking and right-sizing systems, allowing fulfillment operators to cut corrugated usage by up to 20 percent per order.

- February 2026: ANDRITZ commissioned a 2,000-tonnes-per-day old-corrugated-containers line at PT Indah Kiat Pulp and Paper’s Karawang mill, enabling mixed-waste conversion into premium testliner and supporting national recycled-content targets.

- December 2025: Rengo acquired a 60 percent stake in Mypak, boosting its Indonesian footprint to 12 factories and deepening its regional hub strategy.

- December 2025: PT Indah Kiat’s 3.9-million-tonne Karawang expansion entered ramp-up, positioning the mill to lift 2026 revenue and reinforce cost leadership.

Indonesia Corrugated Packaging Market Report Scope

The Indonesia Corrugated Packaging Market report encompasses a comprehensive analysis of fiber-based and polymer-based (PP) corrugated materials used for the containment, protection, and transport of goods across diverse industrial and retail sectors. The market refers to the industry that produces multi-layered boards, typically consisting of a fluted medium sandwiched between linerboards, designed to provide high strength-to-weight ratios and crush resistance for secondary and tertiary packaging.

The Indonesia Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-Commerce Fulfilment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-Commerce Fulfilment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the Indonesia corrugated packaging market size in 2026?

The Indonesia corrugated packaging market size is estimated at USD 2.27 billion for 2026.

How fast is the market expected to grow between 2026 and 2031?

It is forecast to post a 6.85% CAGR, lifting value to USD 3.16 billion by 2031.

Which factor contributes the most to near-term growth?

A surge in e-commerce shipments adds about 1.8 percentage points to the forecast CAGR, making it the strongest single driver.

Which material holds the largest share today?

Recycled linerboard leads with 61.86% of 2025 revenue, reflecting Indonesia's circular-economy push.

Which segment is growing the fastest?

Die-cut custom boxes are projected to rise at 9.10% annually through 2031.

What is the key restraint converters face?

Volatile old-corrugated-containers and pulp prices, swinging margins for non-integrated plants, represent the most immediate headwind.

Page last updated on: