India Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

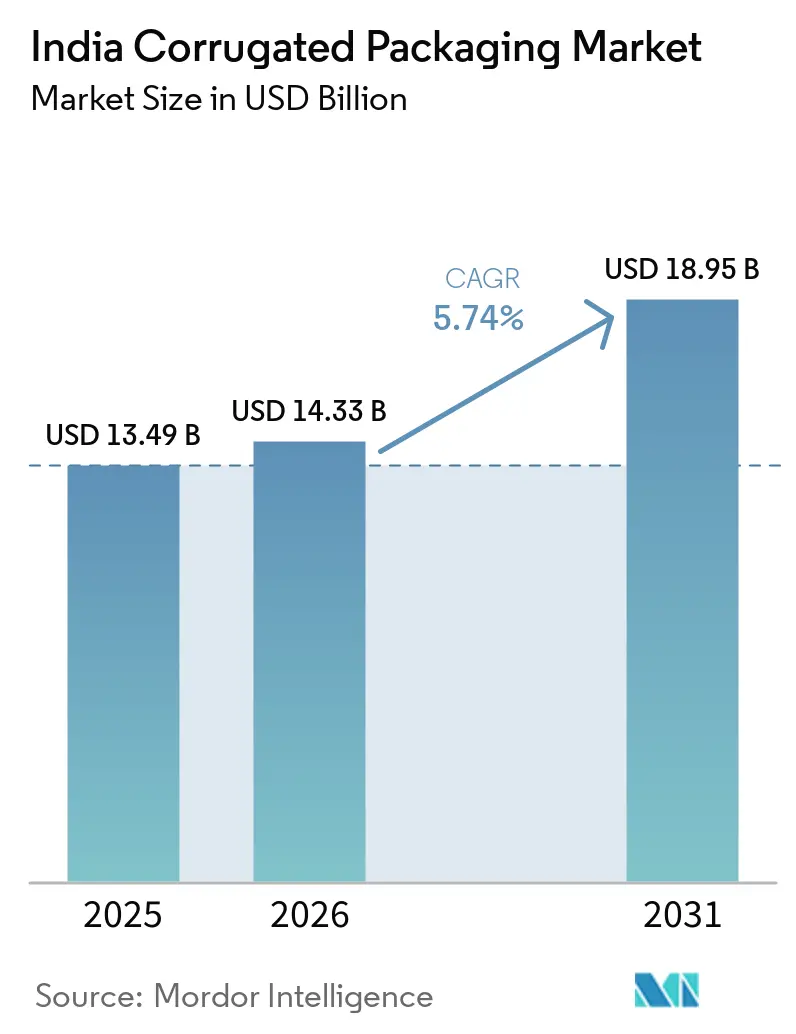

| Base Year Market Size (2025) | USD 13.49 Billion |

| Market Size (2026) | USD 14.33 Billion |

| Market Size (2031) | USD 18.95 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Corrugated Packaging Market Analysis by Mordor Intelligence

The India corrugated packaging market size is expected to increase from USD 13.49 billion in 2025 to USD 14.33 billion in 2026 and reach USD 18.95 billion by 2031, growing at a CAGR of 5.74% over 2026-2031. Demand is shaped by surging e-commerce parcel volumes, export-oriented agri-food corridors, and stricter Extended Producer Responsibility rules that push brands to switch from single-use plastics to recyclable fiber. Recycled linerboard dominates supply because post-consumer collection delivers fiber at a 20-30% cost advantage versus virgin imports, yet premium electronics and export-grade food boxes still rely on FSC-certified kraft to meet burst-strength and humidity-resistance thresholds. Quick-commerce warehouses favor thinner E-flute and die-cut profiles that fit robotic pick systems and reduce dimensional-weight freight charges, while automotive and rice exporters are moving to triple-wall pallet boxes that survive 45-day sea transits without panel crush. Intensifying competition comes from both global majors integrating containerboard mills and hundreds of regional converters adding digital presses for 500-unit personalized runs, setting the stage for margin polarization between scale and specialization.

Key Report Takeaways

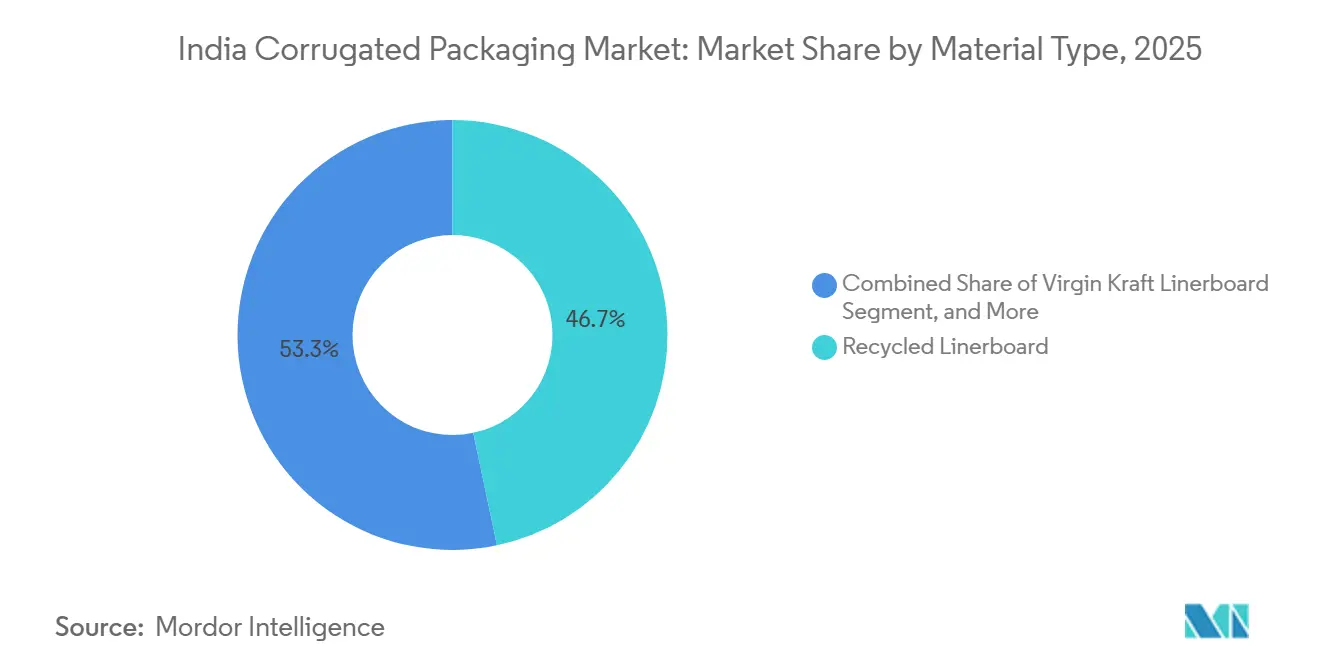

- By material type, the recycled linerboard segment captured 46.68% of the India corrugated packaging market share in 2025.

- By flute type, the India corrugated packaging market size for e flute is projected to grow at an 6.93% CAGR through 2031.

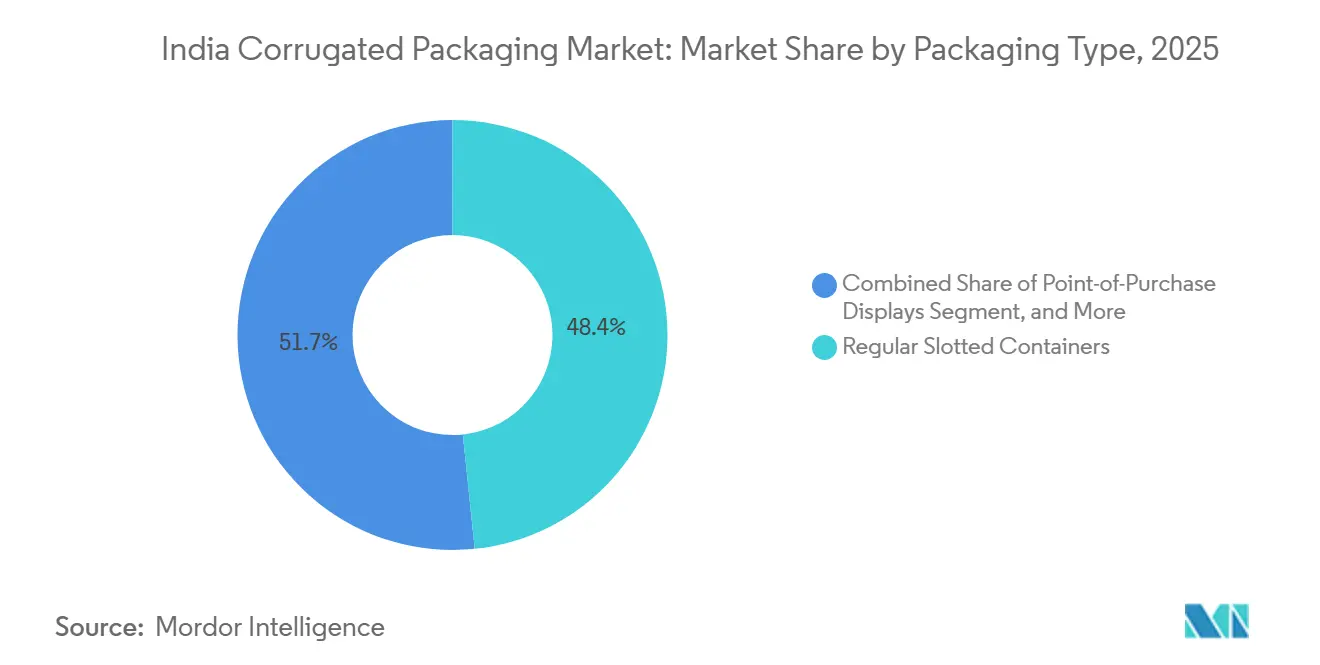

- By packaging type, the regular slotted containers segment captured 48.35% of the India corrugated packaging market share in 2025.

- By wall type, the India corrugated packaging market size for triple-wall is projected to grow at an 7.26% CAGR through 2031.

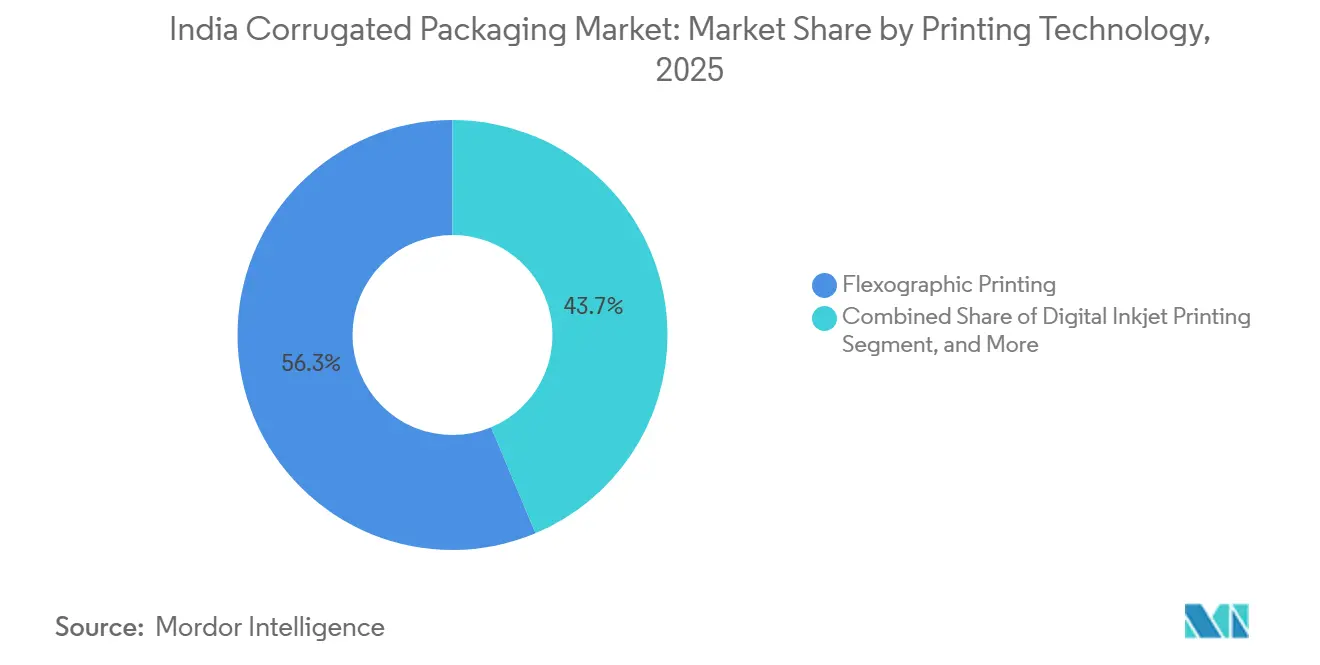

- By printing technology, the flexographic printing segment captured 56.31% of the India corrugated packaging market share in 2025.

- By end-user industry, the India corrugated packaging market size for e-commerce fulfillment centers is projected to grow at an 5.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-commerce Logistics Acceleration | +1.8% | Delhi NCR, Mumbai Metropolitan Region, Bengaluru, Hyderabad | Short term (≤ 2 years) |

| Growth in Processed Food and Beverage Exports | +1.2% | Gujarat, Maharashtra, Tamil Nadu | Medium term (2–4 years) |

| Regulatory Shift Toward Recyclable Packaging | +1.0% | National | Medium term (2–4 years) |

| Nearshoring-Led Electronics Output | +0.9% | Tamil Nadu, Karnataka, Uttar Pradesh | Medium term (2–4 years) |

| Craft-Brewery Demand for Custom Boxes | +0.3% | Maharashtra, Karnataka, Delhi NCR, Goa | Long term (≥ 4 years) |

| Government Subsidies for Bio-Based Barrier Coatings | +0.2% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce Logistics Acceleration

Quick-commerce operators cut delivery windows to 10-15 minutes in 2025, forcing dark-store layouts that rely on shelf-ready corrugated totes doubling as display units. Amazon India surpassed 60 fulfillment centers, each standardizing corrugate footprints to mesh with robotic arms, which raised demand for high-precision die-cuts with ±1 mm tolerances. Flipkart’s augmented-reality storefront initiative triggered a spike in litho-laminated mailers, as photogenic packaging boosts conversion on mobile product pages. Parallel to these design shifts, leading platforms mandated burst strengths 15% above BIS IS 2771 to minimize monsoon-season returns, compelling converters to blend recycled linerboard with imported long-fiber kraft for edge-crush stability. Together, these pressures accelerate upgrade cycles toward high-speed flexo-folder-gluers and single-pass digital presses that can swap artwork in minutes without halting lines.

Growth in Processed Food and Beverage Exports

India’s processed food exports climbed to USD 8.7 billion in FY 2024-25, channeling roughly 40% of packaging spend into corrugated secondary formats. Ventilated mango and grape cartons with moisture-barrier liners now meet 21-day sea-freight shelf-life targets for European grocery chains, amplifying demand for triple-wall boxes coated with biodegradable starch films. Punjab basmati shippers achieved a 12-point reduction in breakage after switching from jute sacks to palletized corrugated bins, unlocking A-grade shelf placement premiums in UK supermarkets. On the beverage side, craft spirit exports surged once Uttar Pradesh relaxed micro-distillery rules; litho-laminated six-packs that conform to U.S. TTB labeling moved from a niche to a baseline SKU.

Regulatory Shift Toward Recyclable Packaging

The 2024 amendment to Plastic Waste Management Rules extended EPR quotas to e-commerce shippers, compelling brands to retrieve and recycle 80% of plastic films by weight.[1]Ministry Officials, “Plastic Waste Management Rules 2024 Amendment,” Ministry of Environment, moef.gov.in Corrugated mailers rich in post-consumer fiber qualify for full EPR credits, triggering a substitution wave that reduced top-tier online sellers’ polybag use by nearly one-third within 18 months. State-level audits in Maharashtra and Tamil Nadu intensified compliance risks, prompting brands to request certificate-backed traceability from bale to box, a capability only vertically integrated converters can document. BIS IS 18000:2024 introduced mandatory recycled-fiber thresholds, effectively shutting the gate on substandard containerboard imports, which in turn buoyed domestic kraft prices and justified investments in new PM-II paper machines.

Nearshoring-Led Electronics Output

Electronics production hit USD 101 billion in FY 2024-25 under the Production-Linked Incentive program. Apple and Samsung subcontractors now specify E-flute cushion inserts pre-scored for robotic pick-and-place, doubling demand for micro-flute corrugators capable of holding ±0.5 mm caliper. Oji India’s Sri City plant added 100 million m² of yearly capacity to serve these clusters, pairing rotary die-cutters with automatic glue application that passes ISTA 3A drops at 1.5 m fall heights. As OEMs shift non-urgent components from air to sea, triple-wall export boxes with desiccant pockets protect high-value PCBs during 40-day voyages, adding up to 8 kg to container weight but saving USD 4-6 per unit in freight costs. FSC-certified virgin linerboard remains mandatory for flagship smartphone packaging, sustaining a parallel import flow of northern bleached softwood kraft alongside India’s recycled-content surge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycled Paper Price Volatility | -0.8% | Uttar Pradesh, Bihar, Rajasthan | Short term (≤ 2 years) |

| Competition from Returnable Plastic Crates | -0.5% | Maharashtra, Gujarat, Haryana | Medium term (2–4 years) |

| Water-Scarcity Constraints on Mills | -0.3% | Tamil Nadu, Andhra Pradesh, Karnataka | Long term (≥ 4 years) |

| Dependence on Imported Virgin Fiber | -0.2% | National | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Recycled Paper Price Volatility

Old Corrugated Containers import prices climbed 18% year-on-year in early 2025 and then eased as Chinese demand softened, creating margin whiplash for converters that carry 45-60 days of feedstock inventory. Domestic collection relies on informal waste-picker networks that lack transparent spot pricing, so converters in Uttar Pradesh and Bihar often pay premiums that erode the recycled-fiber cost advantage. The Directorate General of Trade Remedies’ 2024 minimum-import-price floor on virgin linerboard narrowed the spread between recycled and virgin grades, further squeezing mills that cannot hedge OCC costs through futures contracts. Larger players have responded by signing multi-year supply pacts with municipal aggregators and by co-locating baling stations at major consumption hubs, but small single-corrugator firms lack that bargaining power. Until India formalizes an exchange-traded OCC benchmark, the Indian corrugated packaging market will see periodic pricing shocks that discourage capacity expansion during tight cycles.

Competition from Returnable Plastic Crates

Dairy cooperatives in Gujarat and Maharashtra shifted a share of milk distribution to rigid plastic crates during 2024-25, citing per-trip savings over single-use corrugated trays. FMCG beverage pilots reached 100-cycle reuse targets by leveraging reverse logistics networks, giving crates an attractive amortized cost in short-haul corridors. Yet EPR levies on virgin resin and mandated take-back obligations have started to erode that cost edge, especially for brands without washing depots or end-of-life pathways. Converters counter the threat with hybrid designs, corrugated trays reinforced by plastic corner posts that keep stacking strength while preserving recyclability, an approach pioneered by Horizon Packs for a large soft-drink bottler in late 2025. The tug-of-war is set to continue, but policy incentives tilt marginally toward fiber, limiting crate penetration to specialized cold-chain loops rather than mainstream adoption in the Indian corrugated packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Linerboard Anchors Circular Adoption

Recycled linerboard represented 46.68% of the Indian corrugated packaging market share in 2025, confirming the role of post-consumer fiber in meeting cost targets for e-commerce and FMCG cartons. Semi-chemical fluting, the fastest-rising substrate at 7.48% CAGR, attracts electronics assemblers that need lighter inserts to pass drop tests without breaching air-freight weight bands. Virgin Kraft retains a niche in export-oriented rice, spirits, and smartphone boxes that must carry FSC logos, keeping imports of northern bleached softwood kraft afloat despite domestic price floors. Other specialty grades, such as moisture-resistant liners, serve frozen seafood exporters that face condensation inside reefers, a segment where converters charge 12-15% premiums.

Policy dynamics could reshape the Indian corrugated packaging market for virgin fiber, as the 2024 Forest Conservation Act opened degraded land to farm forestry, a move intended to trim USD 1.2 billion in pulp imports. Astron Packaging’s USD 90 million Pune mill, commissioned in August 2025, bets that recycled linerboard will remain the volume workhorse while premium tiers continue to source imported kraft. Experiments with wheat-straw and bagasse pulps signal an eventual broadening of the feedstock base, though inconsistent fiber quality keeps commercial output limited. As mills upgrade de-inking and water-recycling loops to cut resource intensity, recycled grades are likely to deepen their hold on the India corrugated packaging market.

By Flute Type: E Flute Delivers Thin-Profile Cushioning

B flute held 41.37% of 2025 shipments, prized for its 3.2 mm height that balances cushioning and print real estate for general-purpose shipping cases. E flute posted a 6.93% CAGR and is on track to expand its market share in India's corrugated packaging market as smartphone, pharma, and cosmetics brands embrace thinner profiles that enable pallet density gains without failing ISTA 3A tests. C flute remains entrenched in heavy parts and ceramic tiles where stacking loads exceed 1,000 kg.[2]Technical Team, “E-Flute Demand in Electronics Packaging,” Packaging South Asia, packagingsouthasia.com A flute and F flute fill opposite niches, fragile glassware on the high-cushion side and luxury gift packs on the ultra-thin side.

Oji India installed high-speed corrugators that switch between E-flute and F-flute at its Sri City plant in March 2025 to serve electronics OEMs that demand ±0.5 mm caliper control. E-commerce platforms, meanwhile, impose dimensional caps that penalize bulky C flute boxes, reinforcing the material-reduction tilt of the Indian corrugated packaging market. Quality compliance for thinner flutes drives capital upgrades in adhesive control, board inspection, and automatic slotting, favoring large converters over cottage-scale plants that still rely on manual glue stations.

By Packaging Type: Die-Cut Custom Boxes Monetize Unboxing

Regular slotted containers accounted for 48.35% of 2025 volume thanks to low setup costs, but die-cut custom boxes led growth at 7.75% CAGR because direct-to-consumer labels treat packaging as advertising. Digital die-cutters shrink minimum runs to 500 units, letting microbreweries and boutique cosmetics houses iterate seasonal designs in days rather than weeks. Folding cartons provide a halfway house between rigid boxes and shipper cases, suited to pharma blister packs that need shelf impact and traceability.

Dimensional-weight tariffs introduced by major couriers in 2024 cut average box volume 15-20%, pushing brands to order contour-hugging designs that shave void fill. Converters with CAD labs capture premium margins by offering rapid prototyping and photorealistic 3D renders, thereby shortening approval cycles. Pallet boxes and point-of-purchase displays grow steadily alongside India's corrugated packaging industry modernization of modern-trade retail formats and export bulks, but custom die-cuts remain the headline driver of incremental value.

By Wall Type: Triple-Wall Secures Export Cargo

Single-wall sheets commanded 54.26% of shipments in 2025 because domestic FMCG and e-commerce lanes rarely exceed 1,000 km. Triple-wall boards, however, clocked a 7.26% CAGR as rice exporters, auto-component makers, and white-goods brands adopted seven-layer constructions that withstand 30-45 day sea voyages and high humidity. Double-wall strikes a midpoint for industrial loads stacked 2 m high in rail wagons, while single-face material covers protective wraps for furniture and glass.

Worth Peripherals installed a seven-layer corrugator in 2024 to capture triple-wall demand from OEMs shipping engines and gearboxes to Europe. Pharmaceutical cold-chain distributors also migrated to triple-wall insulated cartons, swapping foam coolers for recyclable fiber and earning EPR credits. These use cases cement Triple-Wall’s position as the fastest-growing player in the Indian corrugated packaging market, even though its absolute tonnage remains lower than that of single-wall.

By Printing Technology: Digital Inkjet Unlocks Short Runs

Flexography dominated 56.31% of 2025 impressions, running at 300 m min⁻¹ for high-volume FMCG orders. Digital inkjet, advancing at 6.52% CAGR, now crosses over financially at 5,000-10,000 linear meters as ink prices drop below USD 0.10 m⁻². Litho-lamination remains relevant for electronics retail cartons that demand photographic graphics, while screen printing is a niche for POP displays that require opaque whites or metallics.

The Indian corrugated packaging market saw its installed base of single-pass digital presses triple between 2023 and 2025, reaching 30 units across metro clusters. Pamex 2026 featured seven new digital models, signaling the vendor's confidence in a broader rollout. Platforms like Amazon now co-brand packages at the press, eliminating pre-printed inventory, a trend regional converters risk missing if they delay digital upgrades.

By End-User Industry: E-Commerce Fulfillment Tops Volume

E-commerce fulfillment centers captured 33.21% of 2025 demand and continue to pace the India corrugated packaging market, with a 5.87% CAGR, as 10-15-minute delivery windows drive micro-fulfillment expansion. Processed food brands pivot to fiber cartons to harvest EPR credits and signal sustainability, while fresh-produce exporters adopt ventilated, moisture-barrier boxes to clear 21-day sea legs to Europe.

Beverage multipacks leverage litho-laminated boards for shelf billboarding, and electronics assemblers specify micro-flute inserts that survive automated pick lines. Pharma cartons demand serialization and temperature mapping, rewarding converters with clean-room spaces and digital printing for variable data. Personal-care labels embrace windowed die-cuts and soft-touch coatings that elevate unboxing aesthetics. Textiles, industrial machinery, and other verticals round out a diverse customer slate that fragments supply and keeps price competition tight.

Geography Analysis

Maharashtra anchors the highest installed capacity because the Mumbai Metropolitan Region hosts dozens of FMCG headquarters and Jawaharlal Nehru Port Trust handles 40% of India’s containerized cargo, giving the state a decisive freight-cost edge for export cartons. Astron Packaging’s new Pune plant, rated at 10,000 tonnes per month, sits near Chakan’s auto cluster and Nagpur’s cross-dock hubs, underscoring why converters chase multi-industry demand pockets that stabilize machine uptime.[3]Company Filing, “Pune Plant Commissioning,” Astron Packaging, astronpackaging.com Tamil Nadu ranks second in capacity; Chennai Port’s roll-on/roll-off terminals support automobile exports, while nearby corrugator parks in Sriperumbudur, Ranipet, and Sri City feed flows of electronics and textiles. Gujarat combines low-cost land with Mundra and Kandla ports to form a chemical, pharma, and fresh-produce export triangle that leans heavily on recycled linerboard sourced through organized collection programs in Ahmedabad and Surat.

Karnataka’s growth rides on Bengaluru’s dominance in e-commerce fulfillment and smartphone assembly, with quick-commerce dark stores absorbing E flute shelf-ready trays that double as picking totes. Andhra Pradesh became a capacity hotspot after Oji India commissioned its fifth factory in March 2025, adding 100 million m² per year to serve nearshored PCB plants, while the state’s Krishnapatnam Port shortens sailing times to East Asia. Uttar Pradesh shows bifurcated demand: Noida and Ghaziabad pull corrugated shipper cases for FMCG and appliances, whereas eastern districts use ventilated produce cartons for mango and litchi flows; water-scarcity worries and fragmented OCC supply, however, deter large new mills. Goa punched above its size once JK Paper bought Borkar Packaging, creating a twin-plant network that supplies coastal cashew in India and spirits exporters along with western Maharashtra buyers.

Regional disparities in water and waste infrastructure shape delivered-cost spreads inside the India corrugated packaging market. States with mandatory zero-liquid-discharge rules Tamil Nadu and Andhra Pradesh add USD 5-10 million to greenfield mill budgets, pushing converters to recycle white-water and harvest rainwater to stay compliant. Maharashtra, Karnataka, and Gujarat benefit from municipal segregation programs that lower OCC procurement outlays by 10-15% versus northern hinterland states, reinforcing a clustering of Grade-A plants near western ports. As capacity footprints widen, the India corrugated packaging industry keeps a hub-and-spoke model: multi-state majors truck pre-printed sheets to satellite box plants, while micro-converters remain local, feeding hyper-regional FMCG distributors at 24-hour lead times.

Competitive Landscape

The India corrugated packaging market balances moderate fragmentation with pockets of scale efficiency because the top five converters together command roughly 25-30% share, leaving hundreds of single-corrugator firms to fight on price in provincial catchments. Global majors Smurfit WestRock, International Paper, and Stora Enso leverage containerboard self-sufficiency to hedge recycled-fiber swings, and Smurfit WestRock’s 2026 road map explicitly flags India as an EMEA and APAC growth pole with plans for recycled-linerboard integration. Domestic leaders B and B Triplewall and Oji India follow a similar playbook: backward-integrated kraft mills plus high-speed FFG lines that deliver sub-48-hour changeovers for national FMCG contracts.[4]Corporate Presentation, “Medium-Term Plan 2026,” Smurfit WestRock, smurfitkappa.com Consolidation quickened when JK Paper purchased a 72% stake in Borkar Packaging in January 2026, injecting USD 28.2 million and signaling that upstream pulp producers view downstream converting as a new profit pillar.

Mid-tier challengers carve niches through technology or vertical specialization. TGI Packaging runs hybrid flexo-digital lines that print serialized pharma codes in-line, winning cold-chain drug cartons that global converters sometimes overlook. Horizon Packs prototypes hybrid fiber-plastic trays for beverage crates, countering rigid-crate substitution and earning design-service retainers that cushion against linerboard volatility. Worth Peripherals’ seven-layer corrugator targets triple-wall export boxes for engine blocks, illustrating how machine choice maps to regional cargo profiles. The competitive map also shows digital-native disrupters: two direct-to-consumer furniture brands installed mini-corrugators in 2025 to insource right-sized boxes, but their volumes remain small relative to the broader India corrugated packaging market.

Technology adoption widens a capability gap. Single-pass inkjet presses that swap artwork in under two minutes concentrate in Delhi NCR, Mumbai, and Bengaluru; rural plants still run two-color flexo lines installed a decade ago. Automated board-inspection and inline glue-monitoring systems reduce waste by 3-4 percentage points at high-volume sites, translating into margin headroom unavailable to manual plants. As brand owners demand traceability to meet EPR audits, converters that document bale-to-box chains of custody are positioned to command premium spreads. Competitive intensity will therefore hinge less on nameplate tonnage and more on digital workflow, sustainability credentials, and access to captive linerboard.

India Corrugated Packaging Industry Leaders

Stora Enso Oyj

Smurfit WestRock plc

TGI Packaging Pvt. Ltd.

Astron Packaging Ltd.

Oji India Packaging Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: EPL Limited and Indovida Holdings merged to form a USD 500 million rigid and flexible PET packaging group that could indirectly boost secondary corrugated demand as beverage clients scale premium lines.

- March 2026: Smurfit WestRock included India in its EMEA and APAC growth cluster, highlighting plans to add recycled-linerboard capacity and serve multinational FMCG expansions.

- January 2026: JK Paper acquired 72% of Borkar Packaging for INR 235 crore (USD 28.2 million), adding 10,000 tonnes per month corrugation capacity across Goa and Maharashtra.

- August 2025: Astron Packaging brought a Pune mill online at 10,000 tonnes per month, targeting INR 750 crore (USD 90 million) revenue from auto and FMCG accounts.

India Corrugated Packaging Market Report Scope

The India corrugated packaging market is defined as the industrial sector engaged in the manufacturing and distribution of multi-layered paper-based shipping containers, primarily comprising a fluted medium sandwiched between flat linerboards. This sector serves as a critical backbone of the Indian manufacturing and logistics ecosystem, facilitating the safe transport of goods across diverse industries, including food and beverage, fast-moving consumer goods (FMCG), and the rapidly expanding automotive and electronics sectors.

The India Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Indian corrugated packaging market, and what is its forecast CAGR?

The market is expected to increase from USD 13.49 billion in 2025 to USD 18.95 billion by 2031, registering a 5.74% CAGR over 2026-2031.

Which end-user segment grows fastest in corrugated demand?

E-commerce fulfillment centers lead growth at a 5.87% CAGR as quick-commerce platforms expand micro-fulfillment hubs.

Why are die-cut custom boxes gaining share?

Digital die-cutters lower minimum order quantities to 500 units, letting direct-to-consumer brands use unique shapes and graphics for unboxing impact.

How does recycled linerboard dominate material choice?

Post-consumer fiber costs 20-30% less than virgin kraft and qualifies for EPR credits, giving recycled linerboard a 46.68% share in 2025.

What technology shift is most disruptive for converters?

Single-pass digital inkjet presses enable on-demand artwork changes and economical short runs, growing at a 6.52% CAGR within printing technologies.

Which regions face the highest water-scarcity risk for paper mills?

Tamil Nadu, Andhra Pradesh, and Karnataka require zero-liquid-discharge systems, raising capital costs for new capacity.

Page last updated on: