Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

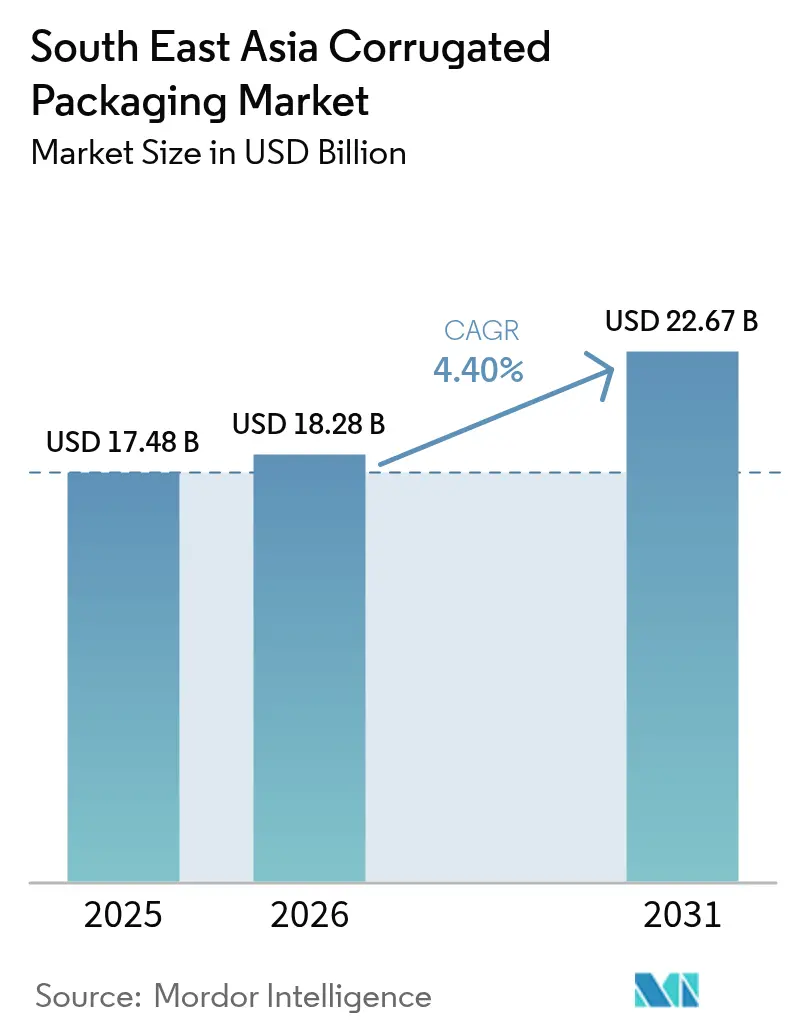

| Base Year Market Size (2025) | USD 17.48 Billion |

| Market Size (2026) | USD 18.28 Billion |

| Market Size (2031) | USD 22.67 Billion |

| Growth Rate (2026 - 2031) | 4.40% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South East Asia Corrugated Packaging Market Analysis by Mordor Intelligence

The South East Asia corrugated packaging market size was valued at USD 17.48 billion in 2025 and estimated to grow from USD 18.28 billion in 2026 to reach USD 22.672 billion by 2031, at a CAGR of 4.4% during the forecast period (2026-2031). Explosive e-commerce adoption, accelerated by a 65.9% jump in B2C parcel volumes during Q2 2025, is pulling converters toward thinner flute profiles that cut dimensional-weight fees. Parallel regulatory crackdowns on single-use plastics in Indonesia, Vietnam and Thailand are redirecting capital toward corrugated capacity, cementing fiber-based formats as retailers’ default substrate. Technology upgrades digital flexo presses, AI-guided box-design software and automated folder–gluers are compressing lead times, enabling converters to serve high-mix, low-volume runs at premium margins. Margin headwinds persist from kraft-liner and old-corrugated-container (OCC) price swings, yet vertical integration into fiber recovery and plantation forestry is mitigating volatility for well-capitalized players.

Key Report Takeaways

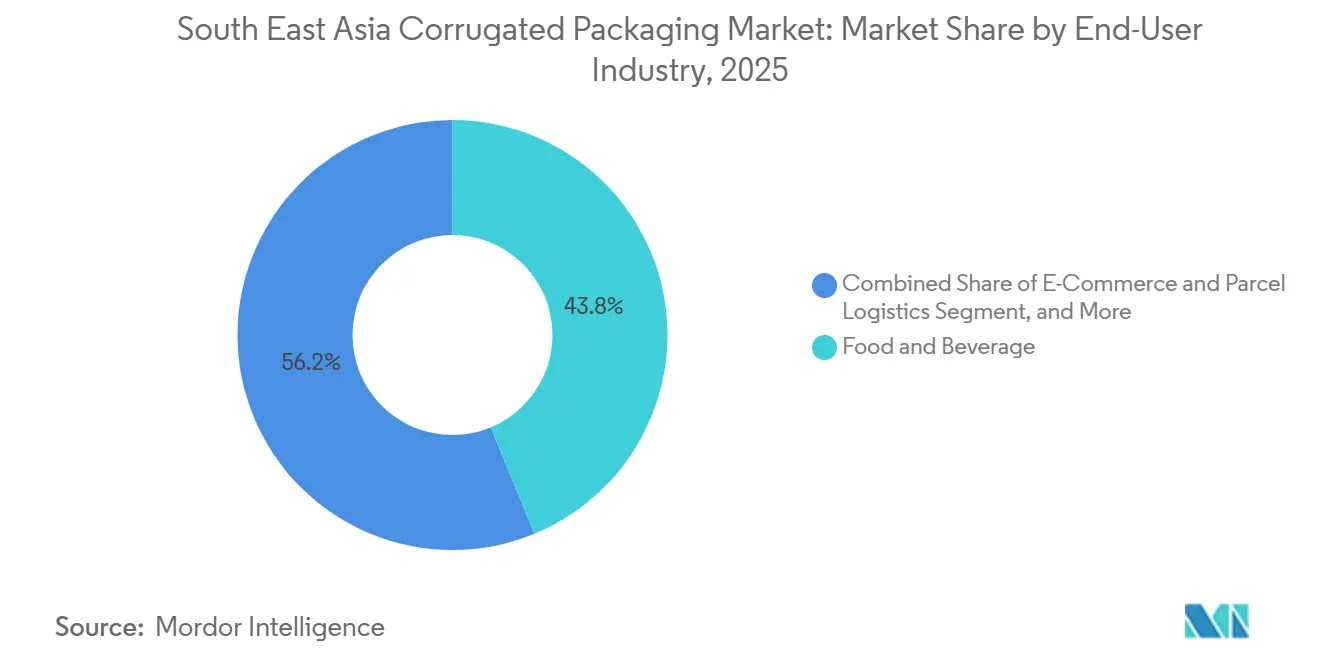

- By end-user industry, Food and Beverage led with a 41.58% share of the South East Asia corrugated packaging market in 2025, while E-Commerce and Parcel Logistics is projected to post the highest 5.11% CAGR between 2026-2031.

- By board type, Single Wall accounted for 57.32% of the South East Asia corrugated packaging market size in 2025, whereas Double Wall is forecast to expand at a 5.25% CAGR through 2031.

- By flute type, C-Flute captured 50.84% revenue share in 2025; E-Flute is set to advance at the fastest 5.29% CAGR to 2031.

- By printing technology, Flexographic printing held 64.59% share in 2025, but Digital Inkjet is expected to register a 5.16% CAGR over 2026-2031.

- By geography, Indonesia dominated with 35.84% market share in 2025, yet Vietnam is poised for the quickest 5.33% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South East Asia Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive B2C E-commerce Parcel Volumes | +1.20% | Indonesia, Vietnam, Thailand, Philippines, Malaysia | Medium term (2-4 years) |

| Food-Delivery Boom Accelerating Demand for Leak-Resistant Meal Boxes | +0.80% | Urban centers across Indonesia, Thailand, Vietnam, Singapore | Short term (≤ 2 years) |

| Mandated Phase-Out of Single-Use Plastics in Indonesia, Vietnam, Thailand | +0.90% | Indonesia, Vietnam, Thailand | Medium term (2-4 years) |

| Installation of High-Speed Digital Flexo Lines Shortening Lead-Times | +0.60% | Vietnam, Indonesia, Thailand | Long term (≥ 4 years) |

| AI-Enabled Box-Design Software Reducing Trim Waste | +0.40% | Global, early adoption in Singapore, Malaysia | Long term (≥ 4 years) |

| Shift to Plantation-Based Fast-Growing Fibre Grades | +0.50% | Indonesia, Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive B2C E-commerce Parcel Volumes

Rapid growth in cross-border and domestic parcels is redrawing corrugated demand curves. J&T Express alone moved 65.9% more parcels year-on-year in Q2 2025, compressing fulfilment lead times below 48 hours in Jakarta, Bangkok and Ho Chi Minh City.[1]J&T Express, “Q2 2025 Parcel Growth,” jt-express.com Marketplaces such as Shopee and Lazada externalize packaging costs onto third-party merchants, creating steady pull for low-print, auto-erect cartons. Courier dimensional-weight pricing rewards E- and micro-flute formats that shave 15%–20% off billable weight yet keep stacking strength. Converters are integrating inline folder–gluers with warehouse-management systems, enabling real-time carton call-offs that slash picking errors and labour. As rural smartphone penetration tops 75% in the Philippines, micro-entrepreneurs are onboarding parcel-hungry business models, widening the addressable pool for corrugated shippers.

Food-Delivery Boom Accelerating Demand for Leak-Resistant Meal Boxes

Meal-delivery platforms delivered more than 2 billion orders region-wide in 2024, with average journeys surpassing 5 kilometres.[2]Grab Holdings, “Food-Delivery Volumes 2024,” grab.com Hot, greasy contents require moisture barriers that uncoated linerboard cannot satisfy. Converters respond with aqueous-dispersion and micro-wax coatings compliant with EU Regulation 10/2011 and FDA 21 CFR 176.170, allowing export of pre-formed clamshells into Singapore and Malaysia. Thailand’s National Food Institute certified 14 corrugated meal-box designs in 2024, fast-tracking institutional catering uptake.[3]National Food Institute Thailand, “Eco-Label Meal Boxes 2024,” nfi.or.th Refrigerated last-mile pilots in Jakarta and Manila pair corrugated inserts with phase-change gel packs, edging polystyrene coolers out of seafood and dairy chains. Subscription-based cloud kitchens amplify frequency, anchoring a recurrent revenue stream for specialty board grades.

Mandated Phase-Out of Single-Use Plastics

Vietnam banned non-biodegradable plastic bags under 50 cm × 50 cm from 1 January 2026, eliminating an estimated 8 billion units a year.[4]Vietnam Furniture Association, “Furniture Export 2024,” vietnamfurniture.org.vnIndonesia’s EPR rules require brands to recover 30% of packaging volumes by 2025, making certified recycled content corrugated a compliance shortcut. Thailand’s roadmap stipulates 30% recycled content in rigid formats by 2026. Enforcement varies tourist hubs see tight policing while rural districts lag yet multinational FMCG companies apply the strictest national rule across ASEAN, tilting procurement toward fiber. ISO 14001 certification has turned quasi-mandatory; 62% of regional mills now hold valid accreditation, up from 48% in 2023.

Installation of High-Speed Digital Flexo Lines

Digital flexo presses cut setup to 15 minutes versus 45 minutes on analog units, unlocking profitable runs below 5,000 linear meters. Canon’s ProStream deployment in Malaysia achieved 1,200 × 1,200 dpi on uncoated linerboard, attracting luxury brands that demand photo-grade graphics. HP’s PageWide T1190 in Thailand matches mid-tier flexo throughput at 75 m/min, eliminating plate costs that can exceed USD 800 per colour. Ink prices remain double analog equivalents, but brand owners pay 15%–20% premiums for 72-hour turnarounds, validating a two-tier service model where speed commands higher margins. Early adopters secure capacity reservations, creating barriers for lagging rivals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Kraft Liner and OCC Price Volatility Squeezing Margins | -0.70% | Indonesia, Vietnam, Thailand, Malaysia, Philippines | Short term (≤ 2 years) |

| Inferior Humidity Resistance During Monsoon Logistics Cycles | -0.50% | Indonesia, Malaysia, Thailand, Vietnam, Philippines | Medium term (2-4 years) |

| Fragmented Panel-Board Logistics Inflating Empty-Run Costs | -0.30% | Indonesia, Philippines | Medium term (2-4 years) |

| Skilled-Operator Shortage for Industry-4.0 Corrugators | -0.20% | Vietnam, Indonesia, Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Kraft Liner and OCC Price Volatility Squeezing Margins

United States OCC export prices into Southeast Asia oscillated between USD 165 and USD 190 per tonne across 2024-2025, a 15% swing that compresses converters’ gross margin by as much as 8 percentage points under fixed-price retailer contracts. Indonesia’s fragmented scrap-collection network leaves contamination rates above 12%, lowering pulp yield and inflating clean-up costs. Rupiah weakness 7% depreciation versus the dollar in 2024-2025 further amplifies imported liner prices. Vietnam, sourcing 70% of virgin pulp externally, felt the pinch when a Canadian mill strike delayed kraft shipments six weeks, forcing emergency spot purchases at 12% premiums. Large players hedge exposure via long-term take-or-pay agreements and backward integration into collection, but small converters struggle to finance such buffers.

Inferior Humidity Resistance During Monsoon Cycles

Relative humidity above 85% can slash edge-crush strength by up to 45%, a condition common from May to October. Wax-coated liners add 8%-12% to material cost and complicate recycling because wax obstructs re-pulping. Alkyl-ketene-dimer hydrophobic sizing pilots in Thailand preserve recyclability, yet adoption lingers below 15% due to a 5% premium. Export-oriented furniture makers in Indonesia report 3%-5% carton rejections for moisture damage, nudging some consignments back to plywood crates that inflate freight. Dehumidified cross-docks in Singapore and Malaysia serve pharmaceuticals and perishables, but broader industrial freight remains exposed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: E-Commerce Rewrites Demand Hierarchies

E-Commerce and Parcel Logistics is projected to grow at a 5.11% CAGR, eclipsing the South East Asia corrugated packaging market average as rapid online retail lifts carton demand. Food and Beverage, with 41.58% 2025 share, still anchors baseline volumes through supermarket and quick-service restaurant channels. Electrical and Electronics shippers specify anti-static liners, expanding secondary-packaging value per unit. Cosmetics brands leverage digital printing for limited-edition “unboxing,” paying up to 25% premiums. Healthcare applications mandate ISO 11135-validated shippers able to withstand ethylene-oxide sterilization, a capability confined to 12% of regional converters. Automotive and Industrial users favour triple-wall cartons rated above 10 kN/m edge strength. Rest-of-industry segments, including chemicals and building materials, log steady but slower uptake as closed-loop plastic totes compete for repeat lanes.

Corrugated converters chasing e-commerce volumes standardize on single-wall C-flute to maximize machine speed, while omnichannel grocers test shelf-ready E-flute trays that eliminate secondary corrugate, thereby reclaiming backroom space. Subscription-box direct-to-consumer models in beauty and snacks deepen order frequency, improving asset utilization. Yet platform subsidization of shipping fees distorts true cost signals, creating vulnerability should incentives fade. On the food-service front, aqueous-coated clamshells win city tenders in Bangkok and Ho Chi Minh City as municipal bans on foamed polystyrene enter force.

By Board Type: Double Wall Gains on Cross-Border Freight Intensity

Single Wall maintained a 57.32% share of the South East Asia corrugated packaging market in 2025 on the back of domestic e-commerce and FMCG throughput. Double-wall boards, however, are forecast to compound at 5.25% annually as cross-border freight from Thai auto suppliers to Indonesian plants demands higher compression strength. Converters invest in dual-backer corrugators capable of format swaps within 20 minutes, juggling low-margin, high-volume local runs with higher-margin export orders. Triple Wall remains niche for bulk chemicals and heavy machinery exceeding 800 kg pallet loads. Single Face is losing ground to on-demand paper-cushion systems integrated into fulfillment centers.

Weight-optimized Double Wall designs enable European damage-rate thresholds below 0.5% for Vietnam’s USD 14.3 billion furniture exports. Imported recycled fluting from China competes on price but faces scrutiny over fiber-origin certification, nudging buyers toward ASEAN-made grades that clear due diligence audits faster. Continuous-shift corrugators in Indonesia clock 92% overall equipment effectiveness after IoT retrofits, trimming unit costs enough to offset liner inflation.

By Flute Type: E-Flute Captures Retail-Ready and Subscription Boxes

C-Flute captured 50.84% share in 2025, yet E-Flute is predicted to log the fastest 5.29% CAGR as retailers push shelf-ready guidelines that demand sub-2 mm calipers. A-Flute’s cushioning keeps it relevant for ceramics, while B-Flute handles intricate die-cuts for point-of-purchase displays. F- and micro-flutes (<1 mm) enter luxury cosmetics and smartphone cases, but scarcity of precision corrugators limits supply. Eight ASEAN plants currently run sub-1-mm tooling, leading to 4-week lead times on custom orders.

E-Flute’s printable facings rival folding carton graphics, supporting direct-to-shelf merchandising in Singaporean hypermarkets that cut labour-intensive shelf-stocking. Dimensional-weight savings of 15% versus C-Flute lower courier charges, a pivotal differentiator for marketplace sellers operating on single-digit margins. Micro-flute’s rigid feel aligns with premium unboxing; however, a 20%-30% price premium restrains penetration beyond luxury segments until economies of scale emerge.

By Printing Technology: Digital Inkjet Disrupts Short-Run Economics

Flexography owned 64.59% share in 2025 thanks to cost efficiency on runs beyond 10,000 m. Digital Inkjet volumes will accelerate at a 5.16% CAGR, enabling profitable micro-lots vital to seasonal SKUs and regional language variants. Litho-lamination clings to ultra-premium packaging where metallic inks and mirror finishes earn 40%-50% premiums. Screen and offset methods continue to recede.

Canon’s ProStream and HP’s PageWide T1190 presses close the quality gap with litho-lam, while slashing pre-press delays. Variable data opens hyper-localized campaigns; a beverage major printed 18 language variants in 2025, each under 4,000 units, impossible under plate-based economics. Ink costs, double analog norms, confine uptake to high-margin SKUs, although larger converters negotiate volume rebates that narrow the gap.

Geography Analysis

Indonesia retained 35.84% share in 2025, reflecting its 280-million population and diversified manufacturing FMCG, cocoa, palm oil and automotive components. Pura Barutama operates integrated mills exceeding 600,000 t capacity, supplying domestic converters and exporters into Australia and the Middle East. Vietnam is projected to grow fastest at 5.33% CAGR as foreign direct investment in electronics and apparel accelerates corrugated demand; Samsung and Canon collectively ship over 200 million units a year from northern complexes, each unit needing at least one corrugated carton. Thailand’s mature sector posts slower gains: per-capita usage hit 35 kg in 2024, plateauing alongside stagnant vehicle output.

Malaysia’s bifurcated market sees high-spec converters in Peninsular states serving electronics while East Malaysia specializes in plantation crop exports. The Philippines, with only 12 kg per-capita consumption, holds latent upside but must resolve port congestion and inter-island logistics. Singapore focuses on high-value aerospace and pharma cold-chain secondary packaging, where strict validation limits supplier pool to a handful of ISO-certified plants. Rest of South-East Asia (Cambodia, Laos, Myanmar) remains under-penetrated, consuming one-fifth of Thailand’s per-capita corrugate due to lower industrialization and the dominance of woven sacks.

Policy convergence favours fiber, yet enforcement differs. Vietnam’s plastic-bag ban fines non-compliant retailers VND 40 million (USD 1,600). Indonesia’s EPR mandates a 30% collection target, spawning recycled-content credits tradable on a nascent exchange. Thailand’s 30% recycled-content stipulation is policed mainly in Phuket and Chiang Mai tourist zones. Malaysia and Singapore rely on voluntary pacts, progressing slower but avoiding supply shocks.

Plantation pulp supply skews regionally. Indonesia produced 11.3 million t in 2024, 96% from plantation-grown Acacia and Eucalyptus. APRIL’s BoardOne grades carry PEFC chain-of-custody, easing exports to Europe. Vietnam covers only 30% of pulp needs domestically; Hawkins Wright forecasts chip shortages by 2027 without new plantations. Thailand benefits from Siam Cement’s vertically integrated loop, while the Philippines and Malaysia remain import-dependent, exposing converters to FX and freight swings.

Competitive Landscape

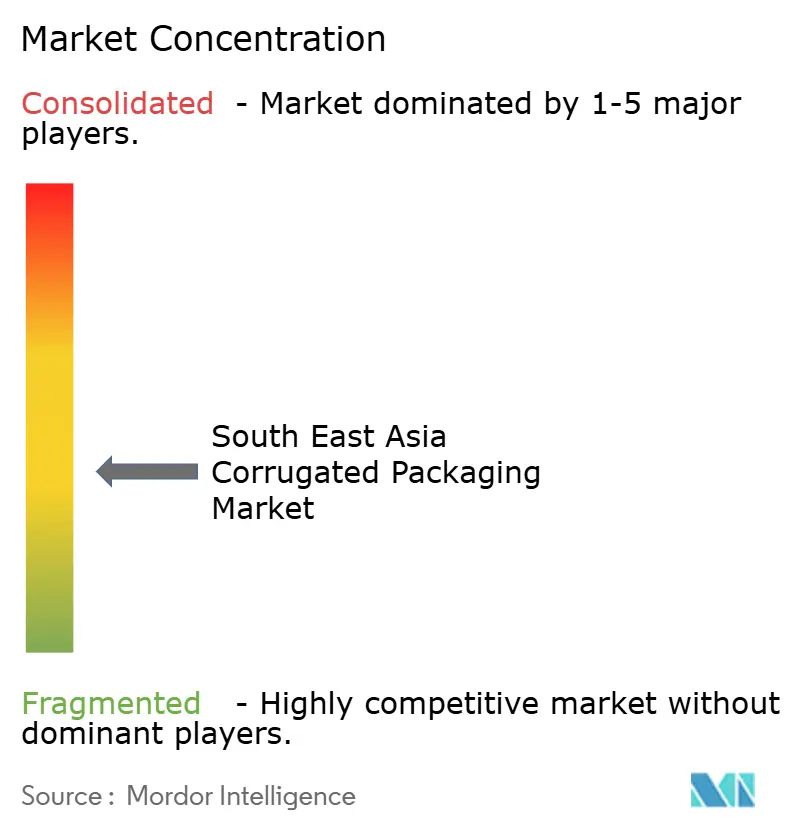

The South East Asia corrugated packaging market hosts a moderate concentration: the top five players command roughly 38% combined revenue. International Paper closed its USD 28.2 billion acquisition of DS Smith in January 2025, positioning the enlarged group for bolt-on ASEAN deals and leveraging integrated fiber reserves to undercut spot liner costs. Smurfit WestRock, born from a USD 32 billion merger in July 2024, earmarks at least USD 500 million for Asia-Pacific expansion and already enjoys 5%-8% procurement discounts versus independents.

Regional champion SCG Packaging recorded THB 21.8 billion (USD 624 million) Q3-2024 revenue and a 14% EBITDA margin, with funds earmarked for digital printing upgrades across Thai and Vietnamese plants. Nine Dragons Paper added a 300,000-t recycled-containerboard mill in Vietnam, part of a broader 15.9 million-t global network that anchors supply security and cost control. Smaller converters differentiate via rapid-turn custom die-cuts and online configurators, promising 72-hour delivery, winning SME business that larger mills find uneconomical.

Technology adoption is decisive. Plants deploying AI-powered box-design engines cut trim waste by up to 24%, lifting margins two-plus points. Bobst’s MASTERCUT 1.6 die-cutter at CPI Flexible Packaging trims setup to under 10 minutes, making 3,000-sheet orders viable. Vertical integration into scrap-collection insulates against OCC spikes; SCG’s closed-loop network collects 1.3 million t annually, equivalent to 70% of its regional requirements.

South East Asia Corrugated Packaging Industry Leaders

SCG Packaging Public Company Limited

Oji Holdings Corporation

Rengo Co., Ltd.

Toppan Inc.

Smurfit WestRock

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: International Paper completed its USD 28.2 billion acquisition of DS Smith, creating a USD 30 billion revenue packaging giant targeting Southeast Asian bolt-ons.

- November 2024: Sarnti Packaging Co., Ltd. deployed machine learning algorithms for corrugated box design optimization, resulting in 11% average material usage reduction and THB 45 million (USD 1.25 million) annual cost savings.

- October 2024: Harta Packaging Industries installed digital printing capabilities at Selangor facility with MYR 15 million (USD 3.4 million) investment, enabling minimum run sizes of 500 units and capturing 28% more SME customer orders.

- September 2024: Vina Kraft Paper Co., Ltd. expanded containerboard capacity by 400,000 tonnes through USD 180 million investment at Dong Nai facility, including advanced water treatment systems and energy recovery capabilities.

South East Asia Corrugated Packaging Market Report Scope

The South East Asia Corrugated Packaging Market Report is Segmented by End-User Industry (Food and Beverage, Electrical and Electronics, Cosmetics and Personal Care, Healthcare and Pharmaceutical, Automotive and Industrial, Rest of End-User Industries), Board Type (Single Face, Single Wall, Double Wall, Triple Wall), Flute Type (A-Flute, B-Flute, C-Flute, E-Flute, F- and Micro-Flutes), Printing Technology (Flexographic, Digital Inkjet, Litho-Lamination, Other Printing Technologies), and Geography (Indonesia, Thailand, Malaysia, Vietnam, Philippines, Singapore, Rest of South-East Asia). The Market Forecasts are Provided in Terms of Value (USD).

By End-User Industry

| Food and Beverage |

| Electrical and Electronics |

| Cosmetics and Personal Care |

| Healthcare and Pharmaceutical |

| Automotive and Industrial |

| Rest of End-User Industries |

By Board Type

| Single Face |

| Single Wall |

| Double Wall |

| Triple Wall |

By Flute Type

| A-Flute |

| B-Flute |

| C-Flute |

| E-Flute |

| F- & Micro-Flutes |

By Printing Technology

| Flexographic |

| Digital (Inkjet) |

| Litho-Lamination |

| Other Printing Technologies |

By Country

| Indonesia |

| Thailand |

| Malaysia |

| Vietnam |

| Philippines |

| Singapore |

| Rest of South-East Asia |

| By End-User Industry | Food and Beverage |

| Electrical and Electronics | |

| Cosmetics and Personal Care | |

| Healthcare and Pharmaceutical | |

| Automotive and Industrial | |

| Rest of End-User Industries | |

| By Board Type | Single Face |

| Single Wall | |

| Double Wall | |

| Triple Wall | |

| By Flute Type | A-Flute |

| B-Flute | |

| C-Flute | |

| E-Flute | |

| F- & Micro-Flutes | |

| By Printing Technology | Flexographic |

| Digital (Inkjet) | |

| Litho-Lamination | |

| Other Printing Technologies | |

| By Country | Indonesia |

| Thailand | |

| Malaysia | |

| Vietnam | |

| Philippines | |

| Singapore | |

| Rest of South-East Asia |

Key Questions Answered in the Report

How big is the South East Asia corrugated packaging market today?

It was valued at USD 17.48 billion in 2025 and is projected to reach USD 22.672 billion by 2031.

Which segment is growing fastest within regional corrugated demand?

E-Commerce and Parcel Logistics is forecast to post a 5.11% CAGR between 2026-2031 as online retail expands.

Why is Vietnam attracting so much new corrugated capacity?

Foreign direct investment in electronics, apparel and furniture drives carton demand, pushing Vietnam toward a 5.33% CAGR through 2031.

What technologies are reshaping converter economics?

High-speed digital flexo and AI-powered box-design software cut setup times and reduce trim waste, enabling profitable short runs.

How are raw-material cost swings managed by leading players?

Major converters hedge OCC and kraft-liner volatility via vertical integration into scrap collection and long-term take-or-pay fiber contracts.

What is the outlook for Double Wall board?

Rising cross-border freight and heavier industrial loads are expected to lift Double Wall demand at a 5.25% CAGR to 2031.

Page last updated on: