Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

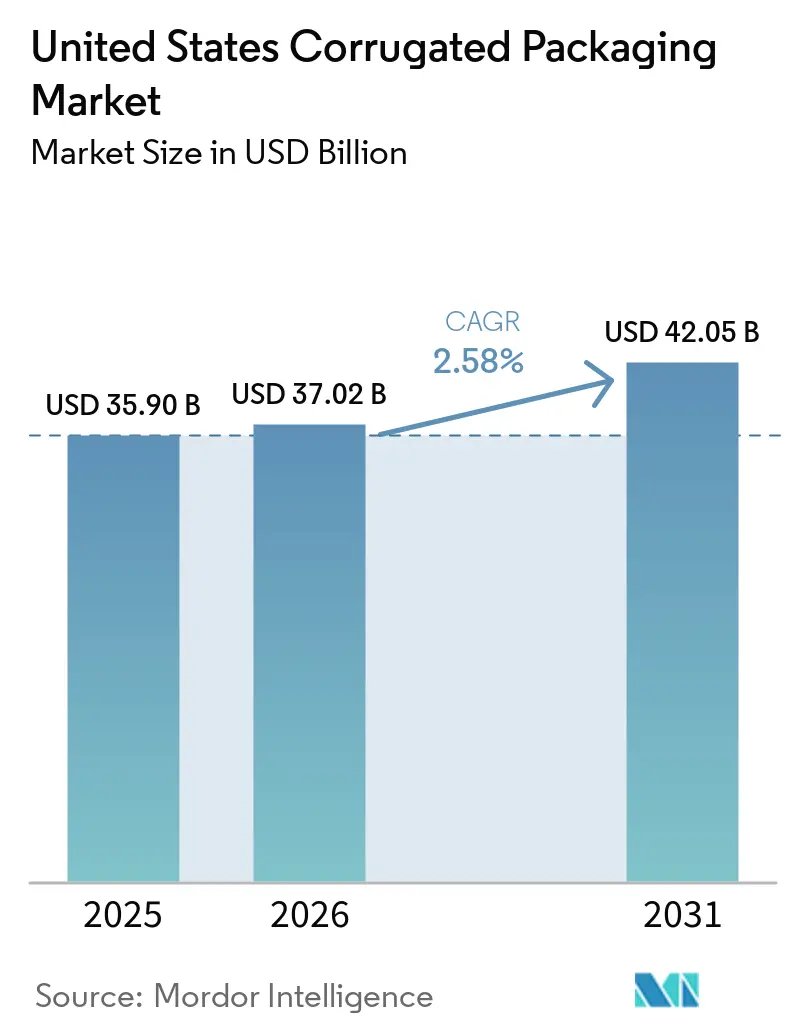

| Base Year Market Size (2025) | USD 35.90 Billion |

| Market Size (2026) | USD 37.02 Billion |

| Market Size (2031) | USD 42.05 Billion |

| Growth Rate (2025 - 2031) | 2.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Corrugated Packaging Market Analysis by Mordor Intelligence

The United States corrugated packaging market size was valued at USD 35.90 billion in 2025 and estimated to grow from USD 37.02 billion in 2026 to reach USD 42.05 billion by 2031, at a CAGR of 2.58% during the forecast period (2026-2031). E-commerce fulfilment centres, extended producer responsibility statutes in seven states, and domestic containerboard capacity closures are reshaping supply faster than baseline demand growth. Operating rates above 93% recorded in the third quarter of 2025 prompted USD 70-per-ton price increases that took effect on 1 March 2026, indicating tighter availability. Brand owners continue to favour premium graphics, which is lifting virgin kraft linerboard demand even as recycled grades dominate the base. Permanent mill shutdowns and energy-price volatility give integrated producers a strategic edge over sheet feeders.

Key Report Takeaways

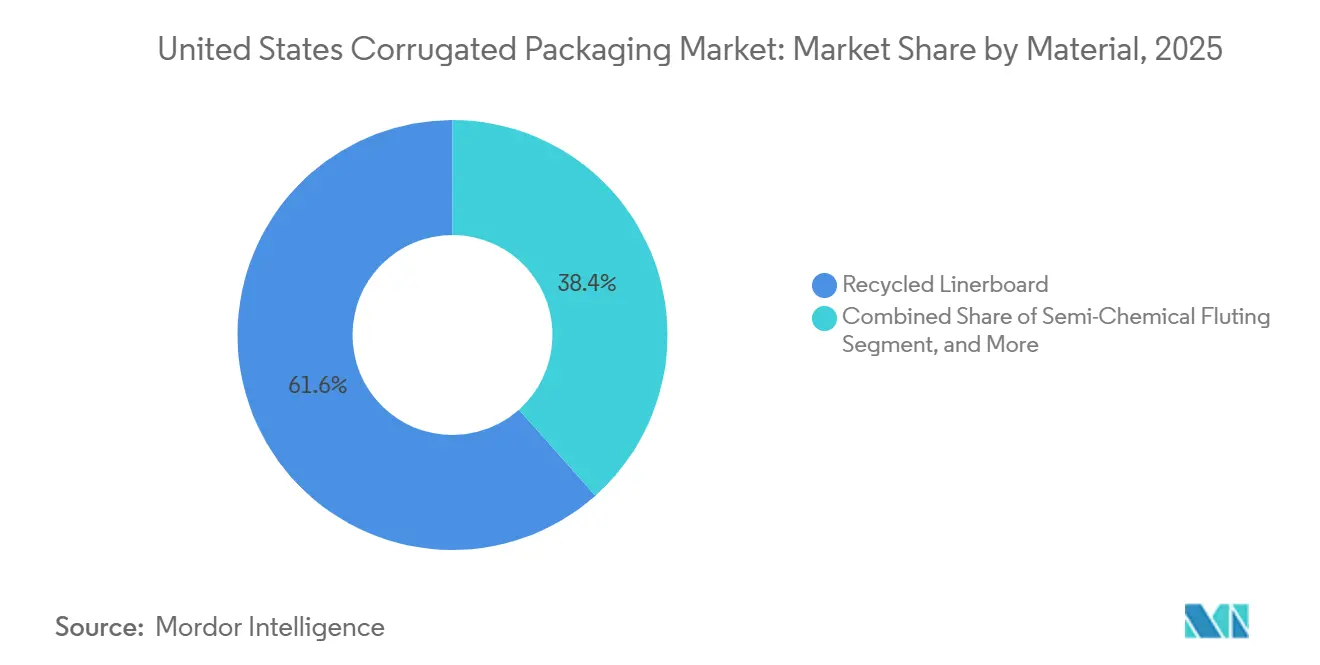

- By material, recycled linerboard captured 61.57% of the corrugated packaging market share in 2025.

- By flute type, the corrugated packaging market size for the E flute segment is forecast to advance at a 4.13% CAGR through 2031.

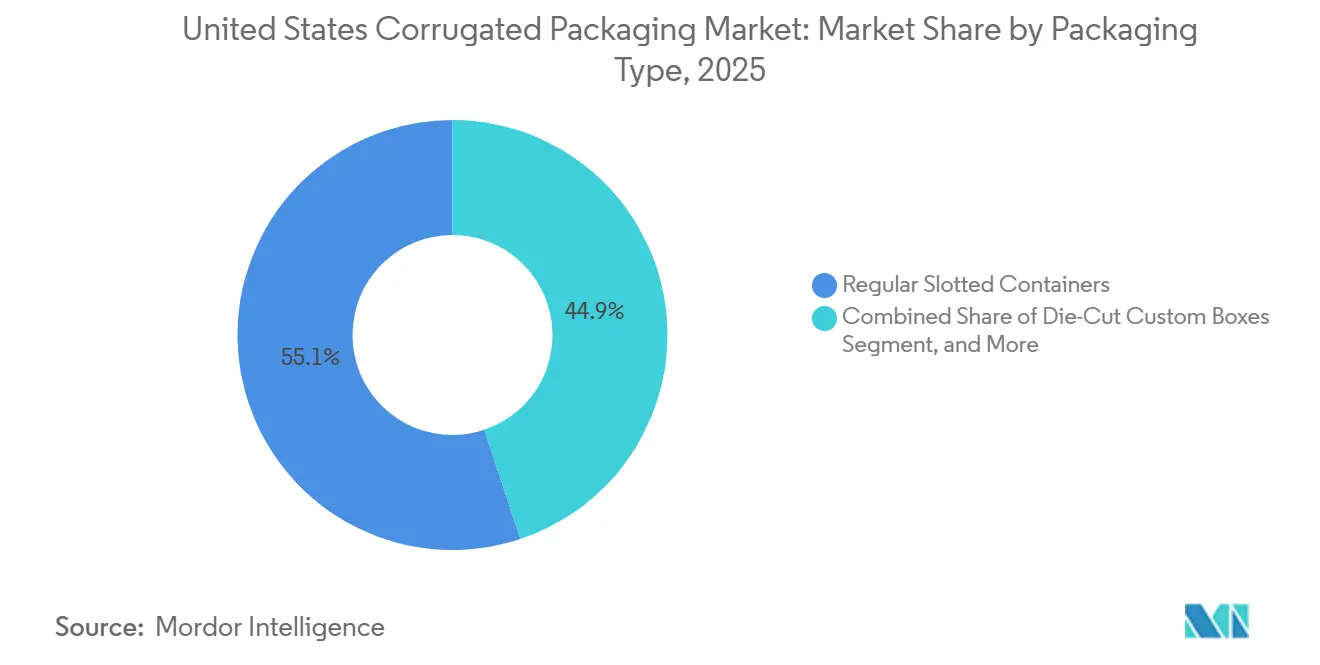

- By packaging type, regular slotted containers captured 55.13% of the corrugated packaging market share in 2025.

- By wall type, the corrugated packaging market size for the double-wall segment is forecast to advance at a 3.64% CAGR through 2031.

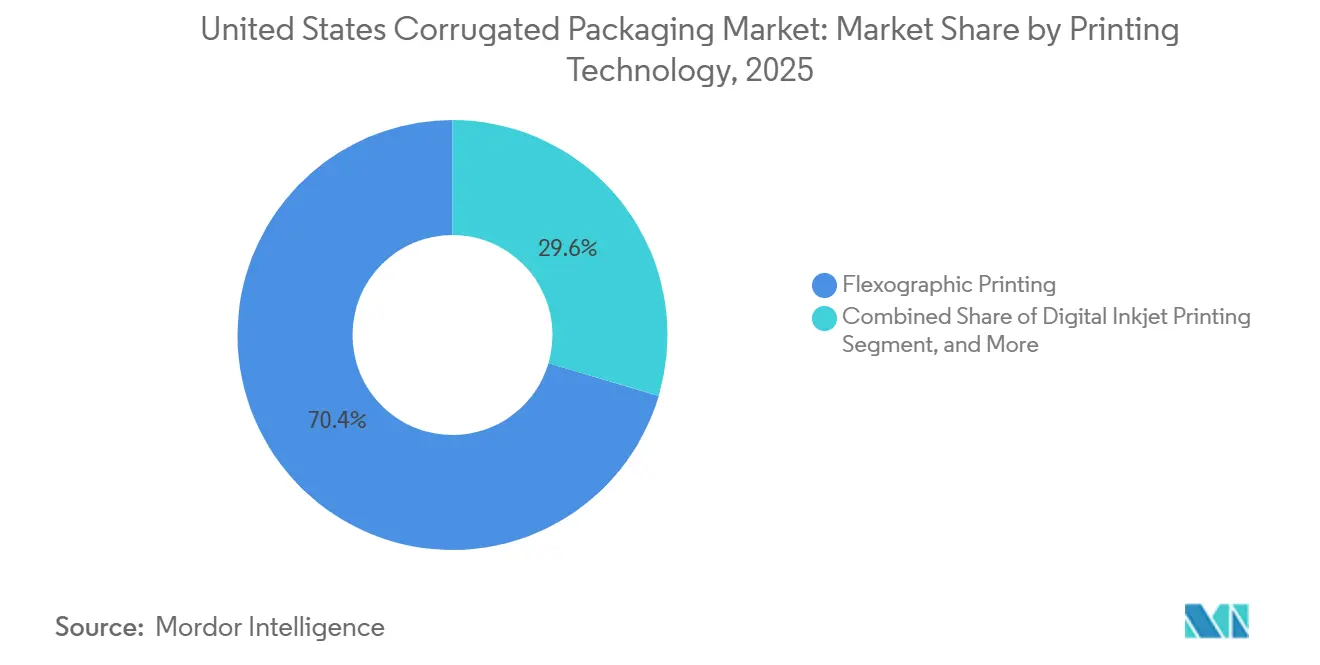

- By printing technology, flexographic presses captured 70.43% of the corrugated packaging market share in 2025.

- By end-user industry, the corrugated packaging market size for the e-commerce fulfilment centres segment is forecast to advance at a 4.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Fulfilment Demand Surge | +0.90% | National, concentrated in metro hubs | Short term (≤ 2 years) |

| Shift Toward Plastic Substitution and Circular Economy Mandates | +0.60% | Seven EPR states | Medium term (2-4 years) |

| Expansion of Same-Day Grocery Delivery Networks | +0.40% | Urban and suburban corridors | Short term (≤ 2 years) |

| Technological Integration of RFID-Embedded Smart Corrugated Boxes | +0.30% | National, early pharmaceutical and electronics use | Medium term (2-4 years) |

| Growth of Direct-to-Consumer Subscription Services | +0.30% | Coastal metros | Medium term (2-4 years) |

| Accelerating Nearshoring of Manufacturing to the United States | +0.20% | Border states and Mexico-adjacent areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Fulfilment Demand Surge

The United States corrugated packaging market is expanding fastest, where parcel networks promise same-day delivery. Amazon, Walmart, and third-party logistics firms added more than 50 million square feet of fulfillment space in 2025, each facility requiring automation-compatible boxes that hold precise caliper tolerances.[1]Bloomberg Newsroom, “Warehouse Expansion Fuels Corrugated Demand,” bloomberg.com Dimensional-weight fees from parcel carriers push shippers toward right-sized packaging, which lifts demand for custom die-cut formats. Smurfit Westrock’s Track Vision platform traced over 1.3 million packages in 2025 and illustrated how digital twins reduce empty-mile trucking.[2]Smurfit Westrock Communications, “Track Vision Package Analytics,” smurfitkappa.com International Paper responded by committing USD 225 million to a greenfield plant in Mississippi, scheduled for late 2027, to stay within a one-day delivery radius of major southeastern metros. Fulfillment density is therefore reinforcing regional capacity clusters and shortening lead times across the United States corrugated packaging market.

Shift Toward Plastic Substitution And Circular Economy Mandates

Extended producer responsibility rules in California, Colorado, Maine, Maryland, Minnesota, Oregon, and Vermont require brand owners to finance collection and sorting systems, creating a policy tailwind for fiber substrates. California Senate Bill 54 alone mandates a 65% recycling rate for single-use packaging by 2032, tilting material selection toward corrugated grades, which already have a 71-76% recovery rate.[3]American Forest and Paper Association, “2025 Recycling Rate Update,” afandpa.org Pratt Industries opened a USD 120 million recycled-content plant in Warner Robins, Georgia, in 2025 to capture demand from these mandates.[4]Pratt Industries Public Relations, “Warner Robins Mill Opens,” prattindustries.com Federal STEWARD Act deliberations in Congress could harmonize rules nationwide and compress compliance costs. As policy momentum accelerates, the United States corrugated packaging market benefits from its closed-loop fibre infrastructure.

Expansion Of Same-Day Grocery Delivery Networks

Instacart, Amazon Fresh, and DoorDash extended refrigerated delivery coverage to more than 5,000 ZIP codes by end-2025, driving demand for moisture-resistant shippers that can survive cold-chain condensation. Wax-alternative coatings improve recyclability and align with municipal compost programs. Georgia-Pacific invested USD 83 million in extra warehouse space at its Palatka, Florida mill to meet Southeast grocery flows. Box complexity is increasing, favouring digital inkjet printing that swaps graphics without plate changeovers. Packaging Corporation of America linked its March 2026 USD 70-per-ton price move partly to the conversion costs of short-run grocery SKUs. These factors collectively amplify growth in the United States corrugated packaging market.

Technological Integration Of RFID-Embedded Smart Corrugated Boxes

In 2025, Smurfit WestRock achieved 97% tag-read rates at material recovery facilities, demonstrating that embedded RFID can automate sorting and support pharmaceutical traceability. Temperature loggers and NFC seals inside shippers help drug distributors comply with federal serialization rules, while Canon’s corrPress iB17 prints variable QR codes linking each unit to a blockchain ledger. Passive RFID costs now range from USD 0.05 to 0.15 per box, offset by reduced manual audits and automatic reorder triggers. Draft GS1 standards due in 2027 should harmonize tag placement, unlocking broader deployment across the United States corrugated packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ongoing Kraft Pulp Supply Chain Volatility | -0.50% | National, reliant on Canadian and South American imports | Short term (≤ 2 years) |

| Rising Energy Costs Impacting Boxboard Production Economics | -0.40% | Natural-gas-dependent regions | Medium term (2-4 years) |

| Increasing Adoption of Reusable Plastic Containers in Produce Supply Chains | -0.20% | California, Florida, Texas | Medium term (2-4 years) |

| Regulatory Pressure on Forest Stewardship Certification | -0.10% | West Coast and Northeast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ongoing Kraft Pulp Supply Chain Volatility

China’s short-fiber pulp benchmark for 2026 rose to roughly USD 570 per ton, while domestic northern bleached softwood kraft held near USD 730 per ton in January 2026. Domtar’s January 2026 closure of its 380,000-ton Crofton mill removed swing capacity and forced U.S. linerboard mills to source higher-cost Scandinavian pulp. Ocean freight from Northern Europe to the Gulf Coast exceeded USD 3,200 per forty-foot container early in 2026, pushing landed costs higher. These dynamics threaten margins for non-integrated converters inside the United States corrugated packaging market and encourage vertical integration or long-term supply contracts.

Rising Energy Costs Impacting Boxboard Production Economics

Energy accounts for 12-18% of box plant costs, and industrial natural-gas prices averaged USD 3.50 per million Btu in the first quarter of 2026, still 40% above 2019 levels. Electricity time-of-use tariffs in California and New England push some converters to overnight shifts, adding labor premiums. Georgia-Pacific installed a combined heat and power system at Palatka to reduce grid dependence, investing over USD 20 million. Smaller independents struggle to finance such upgrades, widening the cost gap in the United States corrugated packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Dominance Meets Virgin Kraft Resurgence

Recycled linerboard maintained 61.57% share in 2025, anchoring cost leadership, yet virgin kraft linerboard is forecast to pace material growth at a 3.03% CAGR. Print-quality requirements in cosmetics and electronics are pulling demand toward the smoother surface that virgin fiber delivers. Domtar’s mill closure tightened virgin supply, nudging spot pulp toward USD 730 per ton, a level that narrows traditional recycled discounts. Many brands now specify Forest Stewardship Council certificates, so mills balancing recycled and virgin fiber can win contracts. Consequently, premium graphics applications are injecting fresh value pools into the United States corrugated packaging market.

Rising circular-economy mandates favor high recycled content, a space where Pratt Industries operates exclusively. Yet blended options such as white-top linerboard are gaining traction in point-of-purchase displays. International Paper already processes 7 million tons of old corrugated containers annually, reducing exposure to imported pulp and reinforcing internal fiber loops. The resulting two-tier material ecosystem ensures that performance and branding demands, rather than price alone, govern fiber choice across the United States corrugated packaging market.

By Flute Type: Thin-Wall Grades Accelerate

C flute commanded 39.10% of 2025 shipments, but E flute is projected to outpace all others at a 4.13% CAGR through 2031 as consumer electronics and cosmetics seek lighter packs that remain protective. Thinner calipers cut dimensional weight and suit robotic packing lines, giving E flute a functional edge. Digital inkjet presses also print more cleanly on micro flutes, aligning with the trend toward personalized packaging. For fragile glassware and ceramics, A flute still offers the highest cushioning, yet its share is declining as converters redesign inserts rather than over-specify board. These mix shifts keep innovation pressure high within the United States corrugated packaging market.

Robot-friendly boxes need tight caliper control, which favors large integrated facilities running advanced process monitors. Smurfit Westrock and BHS Corrugated have tailored corrugators and press lines for micro flutes, helping big players defend their share. Smaller sheet feeders fill niche runs but must absorb higher scrap risk when shifting between flute profiles. The battle for unit economics at thin calipers will therefore shape equipment investment cycles across the United States corrugated packaging market.

By Packaging Type: Custom Die-Cut Boxes Outpace Commodities

Regular slotted containers held a 55.13% share in 2025 due to their low cost and automation-readiness. Yet die-cut custom boxes are forecast to grow 4.23% annually through 2031 as subscription meal kit and apparel brands elevate unboxing experiences. Variable insert designs, interior print, and easy-return tear strips are common upgrades. Folding cartons and litho-laminated displays also gain where shelf appeal dictates purchasing. These customized formats carry a premium that offsets lower run lengths, lifting revenue per thousand square feet for converters inside the United States corrugated packaging market.

Industrial pallet boxes still rely on double-wall and triple-wall builds, serving automotive and machinery shippers that demand puncture resistance. Cross-border nearshoring flows into Mexico reinforce this niche, with International Paper’s Mississippi plant slated to include heavy-duty die-cutting assets. Flexible capacity that toggles between commodity and custom runs is therefore emerging as a strategic requirement across the United States corrugated packaging market.

By Wall Type: Double-Wall Strengthens Industrial Logistics

Single-wall formats accounted for 54.80% of volume in 2025 and will continue to dominate e-commerce and food applications. Double-wall, however, is forecast to expand at a 3.64% CAGR as manufacturing nearshoring intensifies cross-border trucking, where vibration loads are higher. Triple-wall retains specialized duty for bulk chemicals and export crating. Georgia-Pacific added warehouse space for heavier walls at Palatka, confirming that Southeast demand leans toward industrial strength boxes. The ability to switch between wall types in a single shift now defines operational agility in the United States corrugated packaging market.

While double-wall costs 60-100% more per unit than single-wall, reduced damage claims often justify the outlay. Converters with integrated linerboard supply also rebate part of that cost through internal transfer pricing. Such economics explain why Packaging Corporation of America’s recent price hike applied uniformly across wall grades, signaling confidence that the United States corrugated packaging market can absorb broader cost inflation.

By Printing Technology: Digital Inkjet Disrupts Flexo Dominance

Flexographic presses held 70.43% share in 2025 and will stay essential for long runs. Digital inkjet, though, is projected to grow 4.53% per year across 2026-2031 as run lengths fragment. Domino, Canon, and Agfa presses print variable data without plates, enabling same-day promotions. The break-even against flexo now sits near 10,000 linear feet, and many e-commerce SKUs fall below this. Planet Group’s 2025 Domino X630i installation illustrates how mid-tier converters unlock new margins by moving short-run jobs off flexo. Inkjet’s growth, therefore, adds service diversity to the United States corrugated packaging market.

Hybrid presses combining flexo base colors with inkjet variable layers are bridging speed and flexibility gaps. ColorHub’s Kento Hybrid runs at 400 feet per minute in this mode, appealing to beverage marketers who change artwork every season. Equipment suppliers that solve drying and adhesion on recycled liners will likely accelerate market acceptance, further nudging print share inside the United States corrugated packaging market.

By End-User Industry: Fulfilment Centres Take The Lead

Processed foods kept 25.73% share in 2025, reflecting decades-old distribution patterns. Yet fulfillment centers for general merchandise and groceries are forecast to post a 4.73% CAGR, the fastest across end users. Automation-friendly boxes sized to product profiles cut shipping void and save freight. Fresh-produce shippers need moisture resistance, favoring wax-free coatings that are easier to recycle. Cosmetics brands demand high-graphics E flute packs that double as marketing. Pharmaceuticals add RFID and tamper evidence, pushing converters up the value chain. Diversifying end-use mix, therefore, underpins resilient growth in the United States corrugated packaging market.

Subscription services lift order variability, so converters capable of rapid prototyping and just-in-time delivery win share. Pratt Industries’ Georgia facility, opened in 2025, sits within next-day reach of Atlanta fulfillment hubs, demonstrating how proximity shapes capital decisions. This localization trend should sustain balanced growth across the United States corrugated packaging market.

Geography Analysis

Production capacity clusters in the Southeast, Midwest, and West Coast, reflecting access to fibre, energy, and consumer markets. The Southeast houses dense mill networks, with Georgia-Pacific’s Palatka site adding 400,000 square feet of warehouse space to serve export and regional grocery flows. Pratt Industries’ Warner Robins mill feeds Amazon and Walmart hubs in Atlanta, confirming logistics proximity as a planning priority for the United States corrugated packaging market.

Midwest states such as Illinois and Indiana retain legacy mills that serve automotive and appliance manufacturers, yet higher labor and energy costs have encouraged some capacity to move south. Saica Group’s USD 110 million Anderson, Indiana, plant, breaking ground in October 2025, shows that targeted investments still make sense when they plug regional supply gaps. This balance of legacy and new build keeps the Midwest relevant in the United States corrugated packaging market.

The West Coast faces high electricity tariffs and stringent regulations that limit greenfield projects, but demand linked to technology and agriculture remains robust. California’s Senate Bill 54 accelerates the build-out of recycling infrastructure, rewarding vertically integrated producers that can close the loop. Meanwhile, cross-border flows with Mexico, now the nation’s top trading partner, are lifting corrugated movements through Texas and Arizona corridors. International Paper’s forthcoming Mississippi facility is designed to straddle domestic fulfilment and industrial exports, mirroring the geographic reorientation of the United States corrugated packaging market.

Competitive Landscape

Five integrated producers account for an estimated 60-65% of domestic capacity, giving the market a moderate concentration profile. Smurfit Westrock produced more than 200 billion square feet in 2025 and captured the first USD 400 million of merger synergies, while International Paper held roughly one-third of North American volume and is carving its portfolio into regional entities to sharpen capital focus. Packaging Corporation of America bought Greif’s containerboard assets in 2025 to secure 450,000 tons of captive supply and raised prices by USD 70 per ton in March 2026, signalling confidence in demand elasticity.

Pratt Industries positions itself as a 100% recycled player, aligning with state circular-economy mandates. Georgia-Pacific invests in cogeneration and warehouse expansion to offset energy volatility and serve grocery networks. Saica Group is entering the U.S. heartland with a plant geared to automotive components, proving that regional contenders can still penetrate if they target underserved niches. Digital inkjet adoption, RFID-enabled smart boxes, and micro flute capacity are the main competitive battlegrounds, shaping capital spending across the United States corrugated packaging market.

United States Corrugated Packaging Industry Leaders

International Paper Company

Smurfit Westrock plc

Packaging Corporation of America

Georgia-Pacific LLC

Pratt Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sonoco Products Company announced a USD 70-per-ton increase for unbleached recycled board effective 3 April 2026 and an 8% lift on converted items from 15 April 2026.

- March 2026: Cascades completed the sale of its Richmond, British Columbia corrugated plant to Crown Paper Group for CAD 69 million (USD 51 million) and invested CAD 6.9 million (USD 4.93 billion) in Kingsey Falls recycled-content upgrades.

- March 2026: International Paper revealed plans for a USD 225 million greenfield corrugated facility in Mississippi, with operations due in fourth-quarter 2027.

- March 2026: Packaging Corporation of America implemented a USD 70-per-ton containerboard price increase, the first broad rise in 13 months.

United States Corrugated Packaging Market Report Scope

The United States Corrugated Packaging Market report encompasses a comprehensive analysis of fiber-based and polymer-based (PP) corrugated materials used for the containment, protection, and transport of goods across diverse industrial and retail sectors. The market refers to the industry that produces multi-layered boards, typically consisting of a fluted medium sandwiched between linerboards, designed to provide high strength-to-weight ratios and crush resistance for secondary and tertiary packaging.

The United States Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

By Material

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

By Flute Type

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

By Packaging Type

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

By Wall Type

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

By Printing Technology

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

By End-User Industry

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Paper Products |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Paper Products | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current United States corrugated packaging market size and projected value by 2031?

The market stood at USD 35.90 billion in 2025, is set to reach USD 37.02 billion in 2026, and is forecast to climb to USD 42.05 billion by 2031.

Which segment is growing fastest within the United States corrugated packaging market?

E-commerce fulfilment centres are expected to post the highest CAGR at 4.73% from 2026-2031.

How are extended producer responsibility laws affecting corrugated demand?

EPR statutes in seven states reward high-recycled-content packaging, steering brand owners toward corrugated grades that already achieve a 71-76% recycling rate.

Why is digital inkjet printing gaining traction in corrugated packaging?

Rising short-run orders and personalised campaigns make plate-free inkjet economical below about 10,000 linear feet, driving a forecast 4.53% CAGR for digital systems.

What impact do kraft pulp prices have on corrugated box costs?

Volatile pulp, currently near USD 730 per ton, pressures non-integrated converters and reinforces vertical integration strategies to secure fibre supply.

How does nearshoring to Mexico influence corrugated packaging demand?

Relocation of automotive and electronics assembly south of the border raises cross-border shipments, boosting orders for double-wall and heavy-duty corrugated boxes.

Page last updated on: