Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

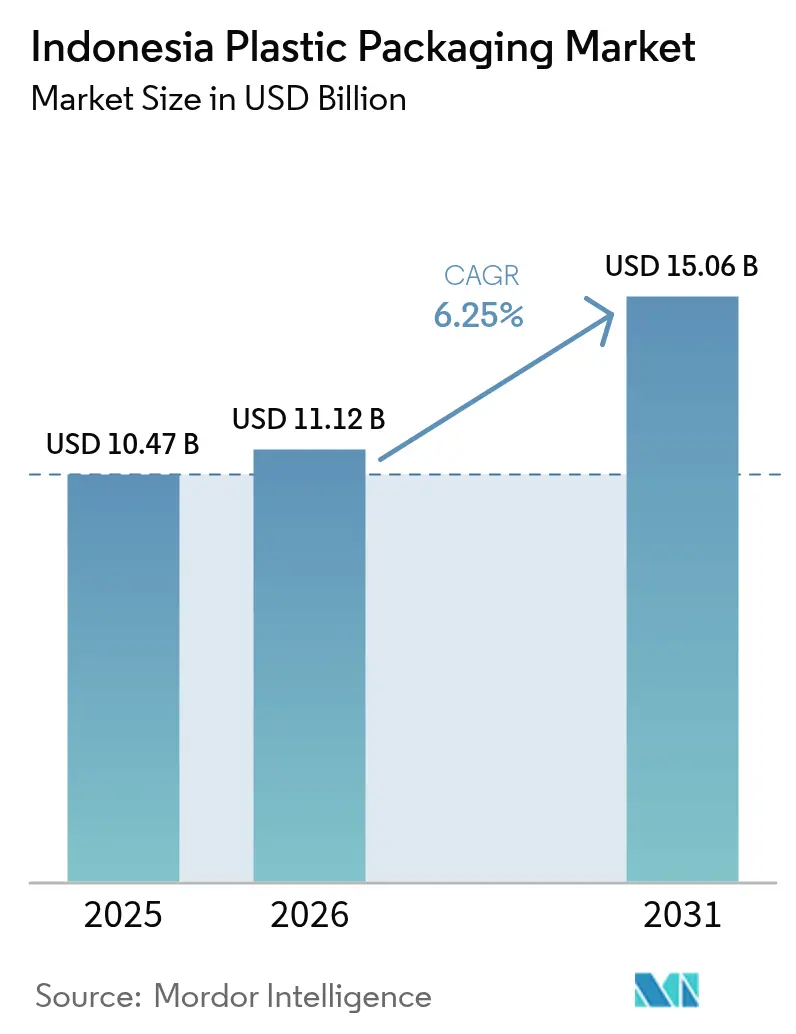

| Base Year Market Size (2025) | USD 10.47 Billion |

| Market Size (2026) | USD 11.12 Billion |

| Market Size (2031) | USD 15.06 Billion |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Plastic Packaging Market Analysis by Mordor Intelligence

The Indonesia plastic packaging market size was valued at USD 10.47 billion in 2025 and estimated to grow from USD 11.12 billion in 2026 to reach USD 15.06 billion by 2031, at a CAGR of 6.25% during the forecast period (2026-2031). Robust urbanization, surging e-commerce traffic, and rising disposable incomes collectively fuel packaging demand for food, cosmetics, pharmaceuticals, and last-mile delivery. Manufacturers favor flexible formats because they reduce shipping weight and cost while satisfying changing consumer preferences for convenience packs. Material substitution accelerates as brands shift toward recycled PET to meet sustainability pledges, even as polyethylene retains volume leadership. Regulatory pushes around Extended Producer Responsibility and single-use bans create simultaneous compliance costs and innovation opportunities across the Indonesia plastic packaging market.

Key Report Takeaways

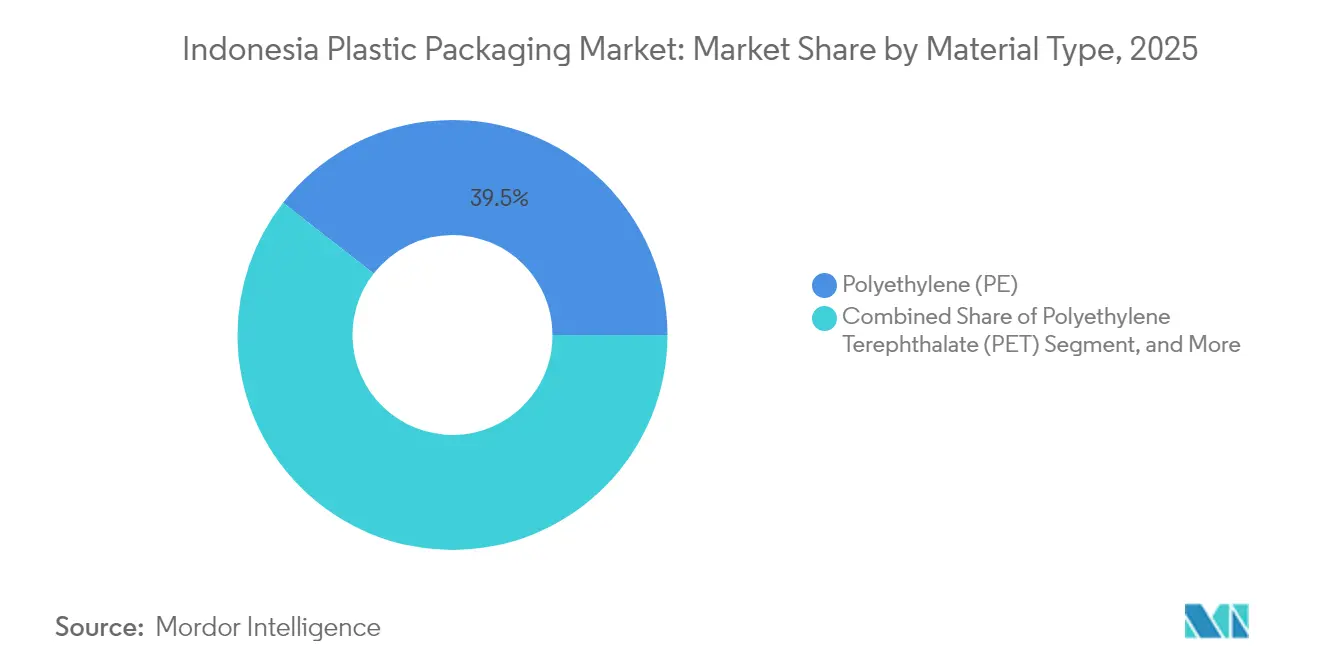

- By material type, polyethylene commanded 39.45% of the Indonesia plastic packaging market share in 2025, while PET recorded the fastest 7.18% CAGR through 2031.

- By packaging type, flexible formats captured 53.61% revenue in 2025; films and wraps are advancing at an 7.75% CAGR to 2031.

- By product form, pouches led with 33.84% share of the Indonesia plastic packaging market size in 2025, whereas films and wraps posted the highest 7.75% CAGR to 2031.

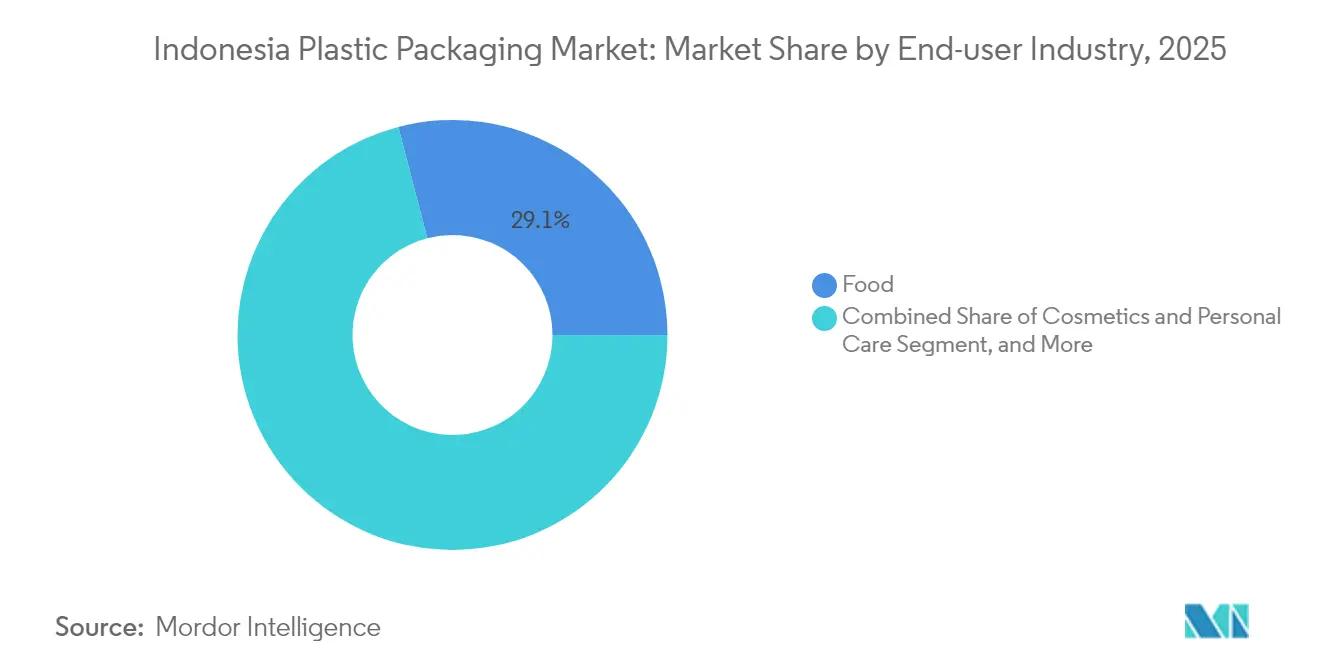

- By end-user, food applications accounted for 29.05% of the Indonesia plastic packaging market size in 2025, but cosmetics and personal care are on track for an 7.73% CAGR to 2031.

- By manufacturing process, extrusion held a 28.12% share in 2025, and thermoforming is the fastest-growing at a 7.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in E-commerce and last-mile delivery demand | +1.8% | Java-Sumatra corridor and major urban centers | Short term (≤ 2 years) |

| Rising consumption of convenience and RTE foods | +1.5% | Nationwide, notably Jakarta, Surabaya, Medan | Medium term (2-4 years) |

| Lightweighting initiatives by FMCG majors | +0.9% | National manufacturing hubs | Medium term (2-4 years) |

| Halal-certification packaging design requirements | +0.7% | Nationwide, Muslim-majority regions | Long term (≥ 4 years) |

| Palm-cooking-oil sector shift to rPET bottles | +0.6% | Sumatra and Kalimantan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in E-commerce and Last-mile Delivery Demand

Indonesia’s digital marketplace recorded unprecedented parcel volumes in 2024, pressuring converters to supply protective films, tamper-evident pouches, and space-efficient mailers that withstand inter-island transit. National Strategic Project upgrades have shortened delivery times and enabled lighter gauges once deemed risky. PT Pos Indonesia’s automated sortation hubs introduced standardized parcel dimensions, rewarding suppliers that meet dimensional accuracy targets. E-commerce platforms now include recycled-content or compostable packaging in vendor scorecards, prompting rapid product development among leading film producers. Early movers gain tender advantages as sustainability clauses become standard in fulfillment contracts.

Rising Consumption of Convenience and RTE Foods

Urban nuclear families increasingly choose single-serve and heat-and-eat products, expanding demand for high-barrier pouches, trays, and portion sachets. BPOM’s 2024 Nutri-Level labeling rule enlarged front-of-pack footprint requirements, spurring investments in digital printing lines that maintain shelf appeal while conveying mandatory data. The government’s nutritious-meal subsidy is raising output from new dairy and protein plants that need aseptic cartons and multilayer bottles. Logistics chains adapt by installing additional cold rooms, reinforcing demand for puncture-resistant overwraps able to handle condensation and temperature swings. As a result, the Indonesia plastic packaging market derives a larger revenue share from high-value food applications.

Lightweighting Initiatives by FMCG Majors

Global and local brand owners target double-digit material elimination to trim freight costs and enhance ESG scores. PT Polytama Propindo’s expanded polypropylene output supplies the narrow molecular-weight distribution resins necessary for down-gauged films. Converter capex now prioritizes multilayer blown-film lines with automatic thickness control to hold tolerance within ±3 microns. Lightweighting also improves pallet density, lowering emissions per shipped unit, a metric highlighted in corporate sustainability reports. As resin prices fluctuate, material savings gained through lighter structures cushion margin volatility and strengthen converter resilience.

Halal-Certification Packaging Design Requirements

From 2024, MUI guidance treats inks, adhesives, and coatings as potential non-halal ingredients, forcing converters to audit every upstream supplier. Enterprises meeting traceability criteria can display the halal logo on primary packs, essential for domestic Muslim consumers and lucrative exports to the Middle East. Certification cycles add months to launch calendars, so multinational pharmaceutical and beauty companies increasingly pre-qualify packaging inventories to mitigate delays. Certified supply chains raise switching costs, solidifying partnerships between compliant converters and large CPG accounts while expanding the Indonesia plastic packaging market reach into Islamic economies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent single-use-plastic bans and EPR rollout | -1.2% | Major cities nationwide | Short term (≤ 2 years) |

| Volatile resin prices and rupiah depreciation | -0.8% | Import-dependent manufacturers | Short term (≤ 2 years) |

| Insufficient recycled-resin supply chain | -0.6% | Java and Sumatra corridors | Medium term (2-4 years) |

| BPA-warning regulation for water bottles | -0.3% | Beverage sector | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Single-Use-Plastic Bans and EPR Rollout

Municipal bans on disposable cutlery, straws, and polystyrene foam have already eliminated legacy SKUs, compelling converters to retool at their own expense. Under Indonesia’s EPR scheme, brand owners must finance post-consumer waste collection that currently lacks scale, transferring cost pressure downstream. Fragmented timelines across provinces create forecasting hurdles and inventory write-off risks as rules tighten unevenly. Small firms with limited liquidity struggle most, potentially driving consolidation within the Indonesia plastic packaging industry.

Volatile Resin Prices and Rupiah Depreciation

Imported feedstock denominated in foreign currency accounts for the bulk of the flexible packaging cost structure. When the rupiah weakened in early 2025, spot polyethylene prices jumped 12% in local terms within one quarter, eroding converter margins. Hedging facilities remain scarce for SMEs, prompting them to adopt shorter supply contracts and dynamic customer pricing. Domestic capacity at PT Lotte Chemical Titan offers partial insulation for polypropylene, but specialty resins used in barrier films still depend on overseas suppliers. Persistent volatility motivates converters to diversify into recycled resin streams, yet supply insufficiency keeps recycled pellet premiums elevated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polyethylene Holds Ground as PET Accelerates

Polyethylene retained 39.45% of the Indonesia plastic packaging market share in 2025 thanks to its versatility across grocery bags, stretch wrap, and multilayer pouches. PET, however, is forecast to grow 7.18% annually as beverage and edible-oil producers embrace food-grade rPET, validated by Coca-Cola Indonesia’s debut of 100% recycled bottles in 2024. PP maintains relevance in hot-fill and microwave-ready trays, while polystyrene’s share erodes under foam bans. Bio-based polymers still occupy niche healthcare and beauty channels where premium positioning offsets higher costs.

Supply security shapes procurement: Java-based film extruders buy ethylene feedstock from the Cilegon complex, whereas PET converters increasingly rely on local bottle-to-bottle recycling to hedge currency swings. The Indonesia plastic packaging market benefits as rPET capacity scales, bridging virgin resin deficits and satisfying EPR collection quotas. Meanwhile, SNI quality standards favor incumbent producers able to document consistent melt-flow indices and heavy-metal compliance.

By Packaging Type: Flexible Formats Dominate, Rigid Adds Value

Flexible solutions commanded 53.61% revenue in 2025, propelled by snack, instant noodle, and detergent refill sachets that thrive in Indonesia’s price-sensitive retail landscape. Films with improved oxygen and moisture barriers permit thinner constructions, reducing resin usage by up to 18% without compromising shelf life. Rigid plastics maintain premium positioning in cosmetics jars and aseptic beverage cartons, where tamper evidence and brand presentation justify a higher unit cost.

The Indonesia plastic packaging market enjoys scale economies as flexibles fulfill e-commerce’s volumetric efficiency challenge. Mono-material PE or PP structures streamline recycling, aligning with forthcoming take-back mandates. In contrast, rigid players differentiate via in-mold labeling, high-gloss finishes, and refillable pack pilots responding to urban zero-waste stores.

By Product Form: Pouches Lead, Films Gain Momentum

Pouches controlled 33.84% of 2025 revenue, favored for condiments, coffee, and infant food that require hermetic seals and consumer-friendly spouts. Continuous-motion forming machinery can output 450 pouches per minute, driving down costs and reinforcing dominance. Yet stretch and shrink films set to expand 7.75% yearly ride the e-commerce boom, protecting goods from abrasion and moisture during cross-archipelago transit.

Bottle innovations concentrate on rPET and tethered caps to satisfy single-use directives, while tray consumption rises alongside chilled ready meals for busy urbanites. As household sizes shrink, demand shifts toward single-portion presentation, strengthening unit velocities across Indonesia plastic packaging industry lines.

By End-User Industry: Food Still Rules, Beauty Surges

Food processors held 29.05% of the Indonesian plastic packaging market size in 2025, as bulk commodities and branded snacks alike require dependable moisture barriers during tropical distribution. Halal certification plus nutrition-label mandates intensify design complexity, encouraging multilayer laminates with advanced printing. Cosmetics and personal care log the briskest 7.73% CAGR as millennials and Gen Z adopt skincare regimens, fueling orders for glossy tubes, airless pumps, and sachet samples that support trial purchasing.

Beverage volume growth moderates, but sustainability drives lightweight preform adoption. Pharma packaging benefits from an expanding national formulary of generics, demanding blister films and HDPE bottles with counterfeit-deterrent QR codes. Industrial exports in automotive and electronics continue to need protective dunnage, anchoring base-load demand for heavy-duty sacks and pallets.

By Manufacturing Process: Extrusion Leads, Thermoforming Climbs

Extrusion generated 28.12% of 2025 turnover by producing sheets, stretch wrap, and blown film used across FMCG categories. Inline corona-treatment and digital defect-inspection systems reduce scrap rates to below 1.5%, safeguarding slim margins. Thermoforming, forecast to grow 7.52% annually, profits from fast-food chains and convenience stores specifying clear hinged containers that showcase ready meals.

Injection molding remains crucial for precision caps and closures, with electric presses lowering energy consumption up to 30%, an advantage in Indonesia’s high-tariff electricity environment. Blow molding serves beverage and personal care bottles, but competes with form-fill-seal pouches encroaching on share. Advances in 3-layer co-ex technology allow local converters to embed PCR layers between virgin skins, meeting EPR quotas without sacrificing aesthetics, thereby lifting the Indonesia plastic packaging market appeal among sustainability-driven brands.

Geography Analysis

Java retained roughly 59.40% of 2025 revenue given its petrochemical base, skilled labor, and consolidated logistics corridors surrounding Jakarta and Surabaya. Sumatra accounted for about 25.30%, leveraging palm-oil refining clusters and new toll-road connectivity that trims haulage costs into Medan and Pekanbaru. Kalimantan and Sulawesi together contributed near 10.20% but posted growth above the national average as resource extraction zones add downstream food and consumer-goods capacity.

Ongoing decentralization initiatives underpin new industrial estates in Batang and Kendal, encouraging converters to co-locate with upstream resin suppliers and downstream FMCG fillers. Government port-automation programs cut container dwell time by 18% at Tanjung Priok, making exports of sachet coffee to the Philippines more competitive.Eastern Indonesia, including Papua, still represents only 5.10% but offers untapped fishery and cacao value-chain opportunities that will require cold-chain packaging investments. Regional expansion of the Indonesia plastic packaging market also depends on power reliability and skilled technician availability. Java’s mature workforce supports advanced printing and multilayer laminates, while outer-island plants focus on mono-material extrusion to minimize technical complexity. As infrastructure equalizes, brand owners may diversify production footprints, balancing earthquake and flood risks across the archipelago.

Regulatory Landscape

Indonesia’s plastic packaging regulations are tightening around food-contact safety and producer responsibility. In June 2026, the Indonesian Food and Drug Authority (BPOM) issued Regulation No. 11 of 2026 on Food Packaging, replacing Regulation No. 20 of 2019 and setting updated requirements for packaging materials and substances, including migration limits and a positive list of permitted substances. Packaging in circulation must comply within 12 months (by June 2027). Separately, label space requirements such as BPOM’s 2024 Nutri-Level labeling rule are shaping pack design and printing choices for food applications.

On waste and circularity, MoEF Regulation No. 75/2019 requires producers to reduce waste from products and packaging by 30% before 2029, while 2026 policy work is moving Indonesia toward a more enforceable EPR model. As of July 2026, the Ministry of Environment is finalizing a ministerial regulation to make Extended Producer Responsibility mandatory for large plastic-packaged goods makers, with Packaging Recovery Organizations (PROs) as the operational mechanism. This approach increases compliance costs while also accelerating shifts toward mono-material designs, recycled content, and traceability across the Indonesia plastic packaging market.

Value Chain Analysis

The Indonesia plastic packaging value chain begins with resin and additive supply (PE, PP, PET and specialty barrier materials) from a concentrated upstream base. Local petrochemical producers such as PT Chandra Asri Petrochemical Tbk, alongside multinational suppliers such as PT Dow Indonesia, influence price and availability, particularly for flexible packaging structures. Converters then compound, extrude, thermoform, injection mold, and blow mold into films, wraps, pouches, bottles, trays, and closures, with printing, lamination, and coating added to meet shelf-life and regulatory labeling requirements. Demand comes from FMCG brand owners in food, beverage, cosmetics, and pharmaceuticals, and from e-commerce fulfillment that specifies protective mailers and films for inter-island distribution.

Downstream, distribution runs through brand owner plants, co-packers, modern trade, and a broad traditional retail network. Logistics performance is affected by port and corridor upgrades. At end-of-life, collection and recycling remain a structural bottleneck, with value recovery relying on the informal sector (waste pickers, aggregators, and waste banks), supported by emerging multi-stakeholder coordination through platforms such as the Indonesia National Plastic Action Partnership (NPAP). With EPR moving toward mandatory execution, Packaging Recovery Organizations (PROs) add a new node that links brand owner funding to collection, sorting, and recycling capacity, increasing the importance of traceable PCR supply and design-for-recycling guidelines in procurement and packaging specifications.

Competitive Landscape

The market shows moderate concentration. Amcor’s merger with Berry Global in April 2025 created a diversified platform spanning films, rigid containers, and healthcare, unlocking synergies in R and D and purchasing scale.[2]Amcor, “Amcor completes combination with Berry Global,” amcor.com Tetra Pak leverages carton expertise to cross-sell filling machinery bundled with service agreements, reinforcing customer lock-in for dairy and coconut processors.

Domestic champions PT Dynapack Asia and PT Berlina exploit cost advantages and deep distribution to defend price-sensitive sachet and tube segments. Both deploy incremental automation vision inspection and robotic case packers to close quality gaps with multinationals while retaining labor flexibility. Sustainability is an emerging battleground: ALPLA’s planned Thailand recycling hub will supply food-grade rPET to Indonesian sites, narrowing resin cost differentials and enhancing ESG credentials.[3]ChemAnalyst, “Alpla targets doubling plastic recycling capacity,” chemanalyst.com

Strategic moves include capacity expansions, vertical integration into recycling, and joint ventures for halal-certified materials. Price wars remain contained as rising compliance costs encourage rational competition rather than volume chasing. Technology adoption, AI-driven predictive maintenance, real-time OEE dashboards, and closed-loop resin reclaim serve as the key differentiators among mid-tier players striving to secure contracts from FMCG giants active in the Indonesian plastic packaging market.

Indonesia Plastic Packaging Industry Leaders

Amcor plc

PT Dynapack Asia

Sonoco Products Company

PT Indo Tirta Abadi

PT Berlina Tbk

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The most immediate commercial whitespace is in compliance-ready food-contact structures and documentation services, following BPOM Regulation No. 11 of 2026 and its June 2027 transition deadline. Converters that can support validated material selections, including migration compliance, while delivering high-quality printing for expanding front-of-pack disclosures have a clearer path to premium food accounts. This is especially relevant for high-barrier pouches, films, and thermoformed trays used in convenience and RTE foods.

Circularity-linked offerings are also becoming more bankable as policy and implementation programs mature. The Ministry of Environment’s July 2026 move to require large plastic-packaged goods manufacturers to fund waste management through PROs formalizes demand for collection and recycling partnerships, creating scope for packaging suppliers that can bundle recycled content, traceability, and take-back execution. Capacity and equipment additions that align with this shift include aseptic packaging output at PT Lami Packaging Indonesia’s Cikande, Serang facility (21 billion packs per year) and new machinery spending tied to bottled drinking water packaging, such as PT Asia Pramulia Tbk’s June 2026 capex allocation for AMDK-focused equipment at its Pasuruan factory. At the program level, the Circular Economy Indonesia 2025-2045 roadmap, launched July 2024, names retail plastic packaging as a priority sector and frames 2025-2029 as an ecosystem-building window for redesign, reuse, and collection, supporting investment cases for mono-material formats, PCR integration, and recycling-aligned conversion capability.

Recent Industry Developments

- July 2026: Indonesia’s Ministry of Environment moved to finalize a ministerial regulation that makes Extended Producer Responsibility mandatory for large plastic-packaged goods manufacturers, using Packaging Recovery Organizations (PROs) to administer producer-funded waste management. The change increases the commercial value of traceable recycled-content packaging and raises the bar for suppliers that can support customers with collection, reporting, and compliant redesign.

- April 2026: Amcor opened an advanced healthcare packaging coating facility in Subang Jaya, Malaysia, with an investment exceeding USD 35 million. The added regional capability expands supply options for high-performance medical and pharmaceutical packaging materials used by Indonesian brand owners and contract packers that require higher barrier performance and tighter quality controls.

- December 2024: Tetra Pak unveiled Direct UHT technology for coconut beverages, extending shelf life to 12 months without preservatives. This supports wider distribution of ambient coconut beverages across Indonesia’s archipelago and reinforces demand for compatible packaging and filling solutions that maintain product integrity over longer logistics cycles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of plastic packaging sold and used in Indonesia across common consumer and industrial packing needs, counted when packaging is supplied into the local market. The sizing is built in USD and aligned to one time period so year-to-year movement stays comparable.

Scope exclusions: We exclude paper, glass, and metal packaging, and we do not count informal reuse of packaging that is not sold as part of the packaging supply chain.

Segmentation Overview

- By Material Type

- Polyethylene (PE)

- Polypropylene (PP)

- Polyethylene Terephthalate (PET)

- Polystyrene and EPS

- Other Material Types

- By Packaging Type

- Flexible Plastic Packaging

- Rigid Plastic Packaging

- By Product Form

- Bottles and Jars

- Trays and Containers

- Pouches and Sachets

- Bags and Sacks

- Films and Wraps

- Other Product Forms

- By End-User Industry

- Food

- Beverage

- Pharmaceuticals and Healthcare

- Cosmetics and Personal Care

- Industrial

- Other End-user Industries

- By Manufacturing Process

- Extrusion

- Injection Molding

- Blow Molding

- Thermoforming

- Other Manufacturing Processes

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with getting the demand backdrop and policy context right, because packaging volumes move with consumption and manufacturing output. We leaned on public sources such as Statistics Indonesia for manufacturing indicators, Indonesia Customs trade statistics for polymer and packaging flows, and Bank Indonesia or Ministry of Trade releases for macro and trade direction. For sustainability and compliance signals that affect mix shifts, we also reviewed government notices and standards updates where available.

To translate that context into a usable sizing sheet, we checked resin and packaging related price movements and trade patterns, then matched them with packaging use signals from association websites, peer reviewed journals, and reputable press coverage of capacity additions. Company annual reports, investor presentations, and public filings were used to sanity check directional growth and product focus. A paid subscription for company financials and a shipment-level import export database were used selectively to avoid missing smaller suppliers and to validate trade-linked demand. These examples are not exhaustive, and many other public references were used for cross-checks, clarification, and final validation.

Primary Interviews and Surveys

Primary work was used to stress test desk assumptions, especially on how fast flexible versus rigid demand is shifting and how pricing is being passed through across end users like food, beverages, home care, and industrial packs. We spoke with a mix of packaging converters, resin-linked stakeholders, distributors, and large packaging buyers, and then compared inputs across Java-heavy demand centers and the rest of Indonesia to reduce a capital-city bias.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 17% | |

| Mid tier: 47% | Functional/Unit leaders: 40% | |

| Smaller Players: 18% | Managers: 43% |

Market-Sizing & Forecasting

The core model is built using top-down and bottom-up checks. On the top-down side, packaging demand is reconstructed from Indonesia-level consumption and production signals, followed by trade flows for relevant polymer inputs and packaging materials, and then filtered through local packaging intensity by major end uses. Once the total was formed, it was corroborated using selective bottom-up approximations, such as sampled converter revenue bands, channel checks on key pack formats, and a volume times average selling price cross-check for common items.

A few practical inputs mattered most in this market, and they were updated year by year so the logic stays repeatable. These include packaged food and beverage output trends, bottled drink consumption direction, manufacturing output proxies, import and export movements for plastics and packaging, and resin price direction that affects realized packaging prices. Where bottom-up signals were thin for smaller informal participants, we handled the gap by using trade and consumption driven indicators, then adjusting the residual based on interview feedback about share held outside the organized base.

For forecasting, scenario analysis was used, because growth can change with regulatory actions, brand sustainability commitments, and shifts in consumer spending. The forward path was built from expected demand in core packaged goods categories, likely substitution between formats, and a pricing progression tied to resin and energy trends, and then it was rechecked with expert consensus from the primary program before finalizing the CAGR path.

Data Validation & Update Cycle

Validation is done in layers so the final number is not dependent on a single data series. We compare the output against independent signals, including trade movements, resin price changes, and end-use growth indicators, and then investigate any variance that falls outside expected ranges. When a conflict shows up, assumptions are revisited and, in some cases, respondents are re-contacted to confirm whether the shift is structural or timing.

Before sign-off, the model and narratives are reviewed by another analyst for logic, arithmetic accuracy, and consistency of the scope. The report is refreshed annually, and interim updates are made when a material event occurs, such as a policy change, a large capacity addition, or a sharp raw material price swing. Right before delivery, we run a fresh data pass so the numbers align with the latest available public releases.

Mordor Intelligence's Indonesia Plastic Packaging Market Size Compared Against Other Published Estimates

It is normal to see different market values for Indonesia plastic packaging, even when the topic name looks identical. The gaps usually come from what is included in the packaging scope, which year is treated as the base, and how pricing is converted and carried forward in the forecast.

By refreshing resin-linked pricing and checking end-use packaging intensity, Mordor Intelligence keeps the total aligned to Indonesia demand across rigid and flexible formats rather than narrowing the count to a single format family or using a fixed price snapshot across years.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.47 B (2025) | |

| Marketplace Publisher A | USD 10.47 B (2025) | The headline matches the 2025 value, but the update cadence and price carry-forward method are not always made clear, which can change the 2030 outcome when resin costs move sharply. |

| Format Specialist B | USD 3.40 B (2025) | This estimate focuses on rigid plastic packaging only, which excludes flexible packs used heavily in food and household categories, so the total is structurally lower even before growth and currency assumptions are applied. |

The table shows that most variance comes from scope boundaries and how prices are progressed across the forecast years. When rigid and flexible packs are counted together and pricing is tied back to observable cost and demand signals, clients can trace the number to clear steps and repeat the logic for internal planning.

Key Questions Answered in the Report

How large is the Indonesia plastic packaging market in 2026?

The Indonesia plastic packaging market size is USD 11.12 billion in 2026.

What is the expected CAGR for Indonesian plastic packaging to 2031?

The market is projected to grow at a 6.25% CAGR from 2026 to 2031.

Which material is growing fastest in Indonesian packaging?

PET is forecast to expand 7.18% annually, aided by recycled-content beverage bottles.

Why are flexible packs dominant in Indonesia?

Flexibles provide cost-effective, lightweight solutions well suited to e-commerce and island logistics.

How do single-use bans impact packaging suppliers?

Converters must invest in recyclable or compostable alternatives and finance take-back systems under EPR rules.

Who are key players in Indonesian plastic packaging?

Major suppliers include Amcor, Tetra Pak, PT Dynapack Asia, PT Berlina, and ALPLA.

Page last updated on: