Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

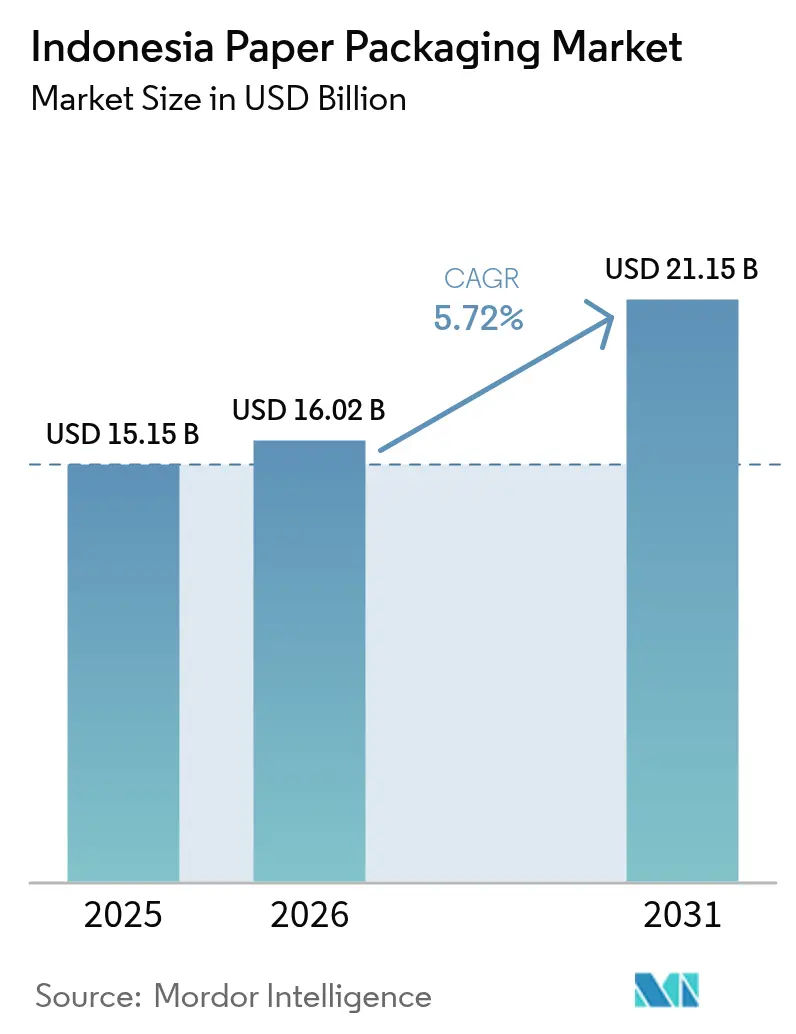

| Base Year Market Size (2025) | USD 15.15 Billion |

| Market Size (2026) | USD 16.02 Billion |

| Market Size (2031) | USD 21.15 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

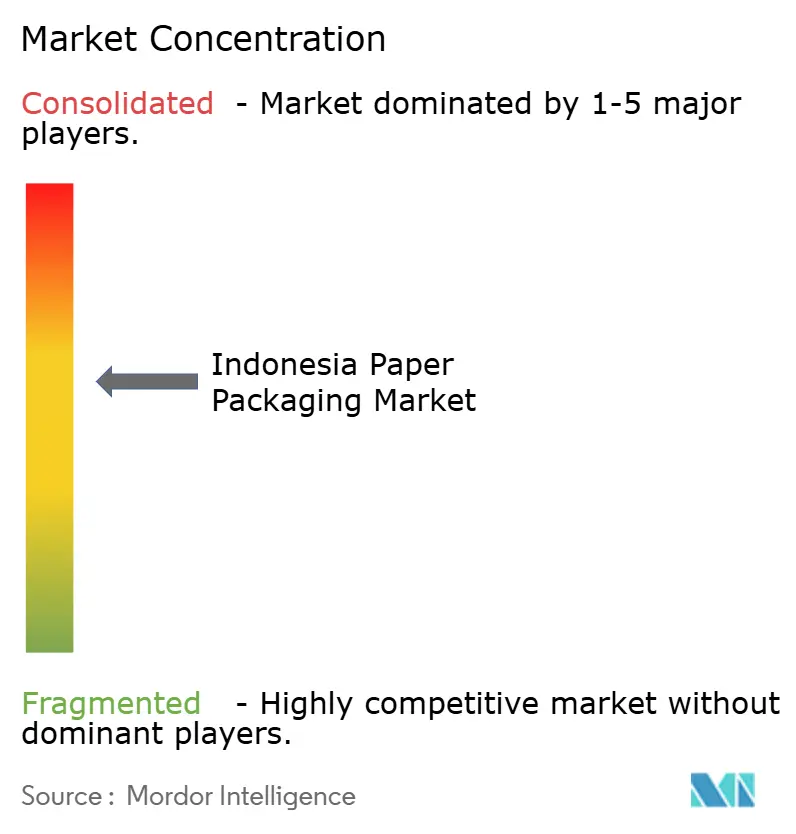

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Paper Packaging Market Analysis by Mordor Intelligence

The Indonesia paper packaging market size in 2026 is estimated at USD 16.02 billion, growing from 2025 value of USD 15.15 billion with 2031 projections showing USD 21.15 billion, growing at 5.72% CAGR over 2026-2031. Strong consumer demand from a population of 275 million, rapid e-commerce expansion outside Java, and sustainability mandates from brand owners are the primary growth engines. Corrugated board retains its leadership position because it protects goods moving across 17,000 humid islands, while paperboard’s faster growth signals a shift towards premiumization in food, beauty, and personal-care categories. Investment in automated corrugators and water-based inks is modernizing production, while Indonesia’s national circular economy roadmap encourages supply chain players to adopt FSC-certified fiber and recyclable coatings. Headwinds stem from volatile recovered-paper rules, fragmented logistics, and electricity tariff hikes; however, government infrastructure spending and supplier diversification are gradually mitigating these risks.

Key Report Takeaways

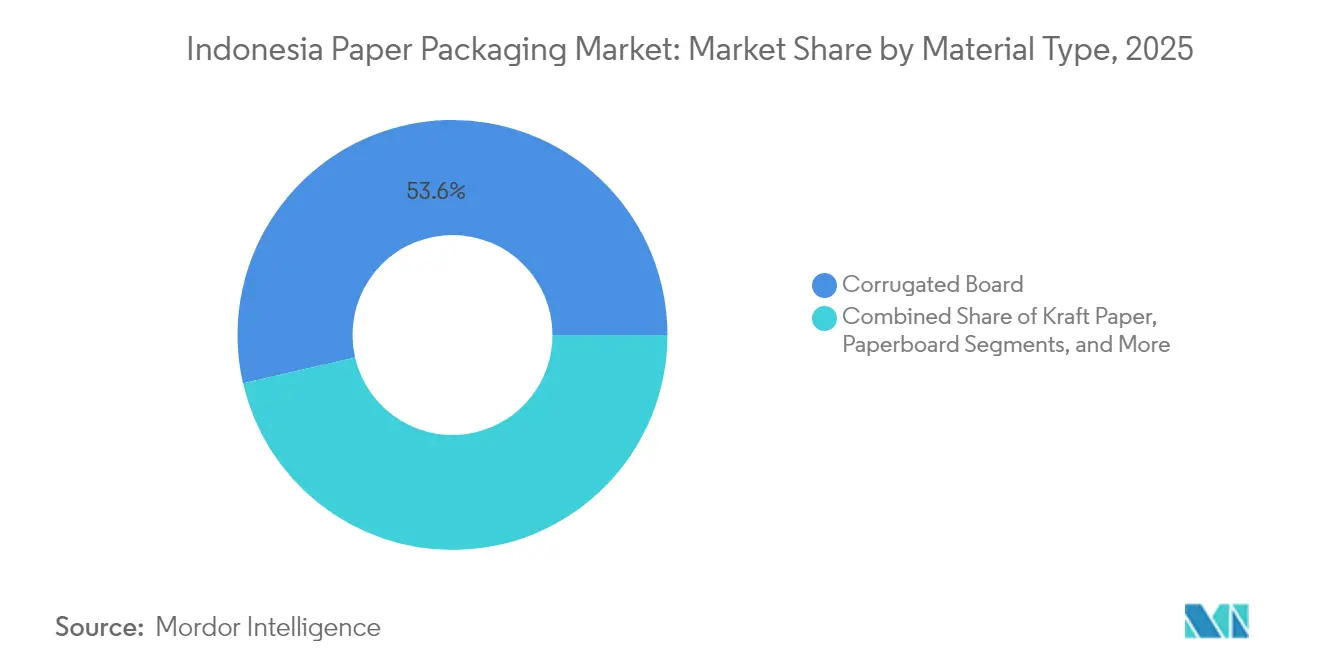

- By material type, corrugated board held 53.61% of Indonesia paper packaging market share in 2025, while paperboard is forecast to expand at a 7.04% CAGR to 2031.

- By product type, corrugated boxes captured 41.78% of the Indonesia paper packaging market size in 2025; folding cartons are advancing at an 7.76% CAGR through 2031.

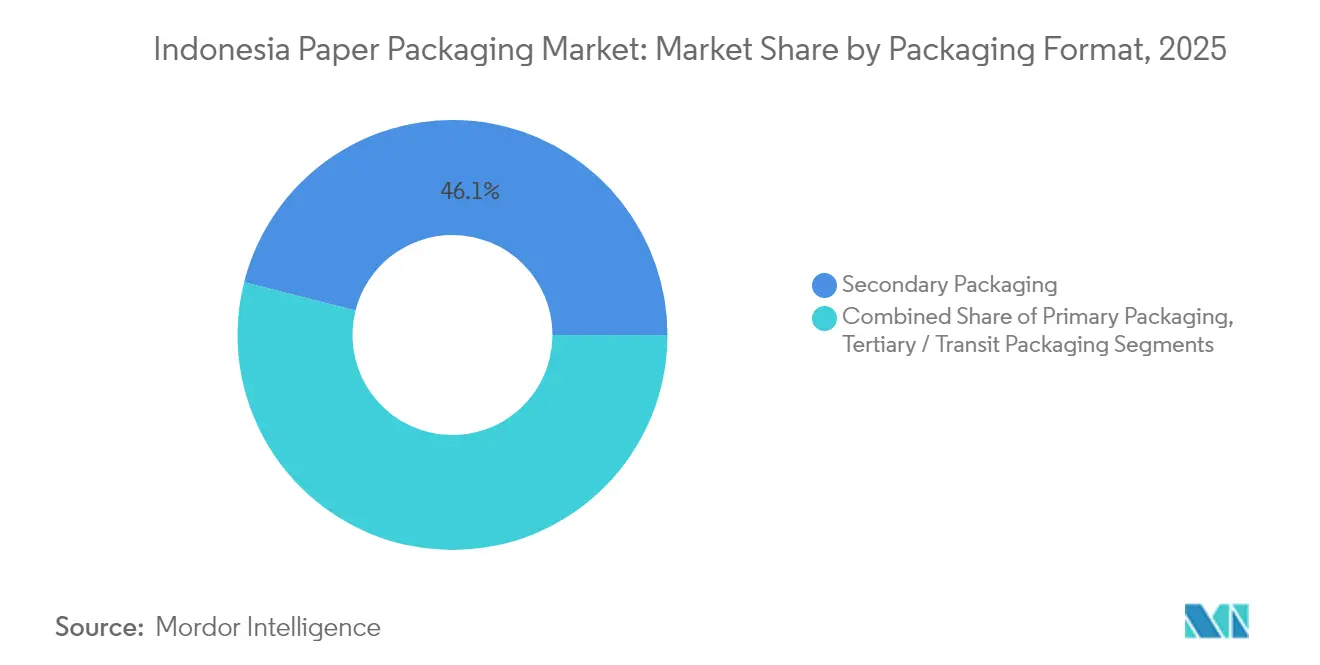

- By packaging format, secondary packaging accounted for 46.05% of Indonesia paper packaging market share in 2025 and is growing at a 6.74% CAGR to 2031.

- By end-use industry, food led with 31.85% revenue share in 2025, whereas personal care and cosmetics posted the highest projected CAGR at 7.53% to 2031.

- SCG Packaging, through its 99.72% stake in PT Fajar Surya Wisesa, controlled the largest single-company share of the Indonesia paper packaging market size in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability mandates from FMCG brand-owners | +1.2% | Java and Sumatra manufacturing hubs | Medium term (2-4 years) |

| E-commerce growth in tier-two and tier-three cities | +0.9% | Nationwide, early gains in Medan, Makassar, Palembang | Short term (≤ 2 years) |

| Rising domestic demand for ready-to-eat meals | +0.7% | Urban centers nationwide | Medium term (2-4 years) |

| Investment inflows into automated corrugators | +0.5% | Java industrial corridor, expanding to Sumatra | Long term (≥ 4 years) |

| Rapid adoption of water-based inks | +0.3% | National, led by Jakarta and Surabaya | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sustainability mandates from multinational FMCG brand-owners

Multinationals require FSC-certified fiber and recyclable barriers, pushing local converters to upgrade materials and secure chain-of-custody credentials. A 2024 survey found 77% of Indonesian food-and-beverage firms willing to absorb higher costs for greener packaging, while 42% of consumers would pay a premium. [1]Digination Editorial Team, “Riset Tetra Pak: Perusahaan Makanan dan Minuman Berkomitmen Meminimalkan Penggunaan Plastik,” digination.idAsia Pulp and Paper’s zero-deforestation milestone across 2.6 million ha of plantation forest signals upstream compliance. Government green-procurement thresholds of IDR 200 million are amplifying demand for low-impact packaging solutions. Investments in water-based inks and halal-certified, bio-based coatings help Indonesian converters win regional export contracts in Southeast Asia and the Middle East.

E-commerce growth in tier-two and tier-three Indonesian cities

Package volumes in Medan, Makassar, and Palembang rose 35% annually, prompting demand for lightweight corrugated boxes optimized for last-mile delivery. Regional manufacturers such as PT Surabaya Mekabox have added digital-print lines for variable data, reducing lead times and supporting personalized branding. New corrugator installations in Sumatra and Kalimantan diversify supply away from Java, lowering freight costs and improving box integrity during multi-modal transit.

Rising domestic demand for ready-to-eat meals

Ready-to-eat consumption is climbing 15% annually in metropolitan areas, spurring grease-resistant and microwave-safe papers. Paperocks Indonesia is supplying hygienic meal-tray packaging for nutrition programs.[2]Paperocks Indonesia, “Inovasi Kemasan Makanan Aman dan Higienis untuk Mendukung Program Makan Bergizi,” paperocks.co.id Revised BPOM migration standards ensure material safety for oily and spicy foods, encouraging converters to adopt specialty barrier coatings. Folding-carton producers gain from portion-control designs that fit Indonesia’s diverse cuisine and limited cold-chain infrastructure.

Investment inflows into automated corrugators

PT Indah Kiat Pulp and Paper’s USD 2.82 billion Karawang expansion will add 3.9 million t of annual board capacity by 2026.[3]Investor Desk, “Grup Sinar Mas Indah Kiat Teken AJB, Punya Proyek Raksasa Puluhan Triliun,” investor.id Chinese suppliers dominate with integrated forming-printing systems that cut energy per unit by 15% and boost throughput 25%. Mid-sized converters such as Teguh Group are adopting modular lines to serve shorter runs for e-commerce brands. Automated quality control improves consistency, satisfying multinational buyers’ stringent standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile recovered-paper import regulations | -0.8% | National, acute for Java-based mills | Short term (≤ 2 years) |

| Fragmented logistics across the archipelago | -0.6% | National, most severe in eastern Indonesia | Long term (≥ 4 years) |

| Electricity tariff hikes for energy-intensive mills | -0.4% | Industrial zones nationwide | Medium term (2-4 years) |

| Shortage of skilled packaging engineers | -0.3% | Sumatra and Kalimantan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile recovered-paper import regulations

Frequent shifts in contamination limits and licensing add 15-20% to raw-material costs each quarter. Mills reliant on recycled fiber face shipment delays from stricter pre-shipment inspections. Integrated producers such as PT Toba Pulp Lestari benefit by supplying virgin alternatives. Manufacturers hedge risk by expanding domestic collection networks, yet outer-island infrastructure limits capture rates.

Fragmented logistics across the archipelago

Logistics costs absorb 23.5% of GDP, with port congestion and multi-modal transfers inflating packaging prices for distant markets. Secondary packaging must be over-engineered to survive humid, long-haul routes, increasing material usage. Government sea-toll subsidies and digital freight platforms are improving visibility, but service gaps persist in eastern islands, slowing penetration of aseptic cartons and pharmaceutical packs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Corrugated Leadership, Paperboard Upswing

Corrugated board contributed 53.61% of Indonesia paper packaging market size in 2025, favored for its strength in humid, multi-modal distribution. PT Fajar Surya Wisesa alone shipped over 1.5 million tons of corrugated medium that year. Paperboard’s 7.04% CAGR outpaces all materials, propelled by premium cosmetics and pharma packs seeking superior graphics.

Corrugated makers are adopting moisture-resistant liners and lightweight fluting, while paperboard suppliers like Alkindo roll out high-bulk grades that cut weight without sacrificing stiffness. Kraft paper and specialty grades remain niche but essential for industrial bags and labels.

By Product Type: Corrugated Boxes Dominate, Folding Cartons Accelerate

Corrugated boxes held 41.78% of Indonesia paper packaging market share in 2025 as e-commerce and FMCG verticals demand sturdy, stackable shipping containers. Folding cartons are forecast to expand at an 7.76% CAGR, mirroring growth in beauty and functional-food segments.

Rigid-box producers leverage digital finishing for short runs, while flexible paper wraps gain acceptance in quick-service restaurants. PT Oki Pulp and Paper Mills’ 2024 green bond financed low-plastic food wraps that extend shelf life

By Packaging Format: Secondary Packaging Prevails

Secondary packaging captured 46.05% of Indonesia paper packaging market size in 2025, owing to the multi-layer protection needs for archipelago shipping. Its 6.74% CAGR is sustained by e-commerce parcels requiring branded mailers and inner cushioning.

Innovations include resealable carry-handles and QR-code-enabled tracking, while Sonoco Asia’s rigid paper containers shield snacks from moisture and oxygen. Primary packaging remains vital for direct food contact, and tertiary wrapping supports bulk export load security.

By End-Use Industry: Food Leads, Personal Care Rises

Food applications commanded 31.85% revenue in 2025 as processed foods, rice, and snacks rely on compliant paper containers. Personal care and cosmetics are projected to climb 7.53% annually as Indonesia’s beauty market matures, seeking premium folding cartons with foil accents and halal adhesives.

Beverage players adopt aseptic cartons supplied by Tetra Pak Indonesia, servicing over 25 local drink brands. Healthcare, industrial, and electronics use niche anti-static or grease-proof grades, rounding out demand diversity.

Geography Analysis

Java accounted for roughly 64.55% of 2025 consumption and capacity, anchored by the Jakarta-Surabaya corridor’s skilled labor, port infrastructure, and proximity to FMCG plants. PT Indah Kiat’s Karawang megaproject will further entrench Java’s dominance once 3.9 million t of board rolls out after 2026.

Sumatra held a near-20.35% share, leveraging rich fiber plantations in Riau and efficient links to Malaysia and Singapore. Asia Pulp and Paper’s Riau mills feed both domestic and export corrugated markets, while local converters service plantation produce requiring moisture-resistant cartons.

Eastern Indonesia - Kalimantan, Sulawesi, Papua - makes up the remaining 15.10% yet offers the fastest 8-10% growth as mining and agriculture boom. High freight costs incentivize on-island box plants; government port upgrades and the National Logistics Ecosystem are expected to narrow regional price gaps.

Competitive Landscape

SCG Packaging’s near-100% control of PT Fajar Surya Wisesa and Asia Pulp and Paper’s integrated model give local champions scale, while global suppliers target premium niches. The top five firms collectively held an estimated 55-60% of Indonesia paper packaging market share in 2024.

Technology is the key battleground. Automated corrugators, digital printing, and AI-driven quality systems enhance output consistency and minimize waste. International players such as Tetra Pak, SIG Group, and Amcor focus on aseptic, high-barrier, and fully recyclable formats that command above-market margins.

White-space opportunities center on halal-compliant beauty packs, pharmaceutical serialization, and ethnically tailored e-commerce mailers. Packindo steers standard harmonization, and patent filings by PT Toba Pulp Lestari on high-purity pulp underscore domestic R&D momentum.

Indonesia Paper Packaging Industry Leaders

PT Industri Pembungkus Internasional

PT Fajar Surya Wisesa Tbk

PT Pabrik Kertas Indonesia (Pakerin)

PT Pura Barutama

PT Surabaya Mekabox

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SIG Group posted 3.2% revenue growth, citing new pack formats in Indonesia.

- April 2025: Rengo acquired 28.6% of Kinki Danboru to extend regional corrugated reach.

- February 2025: SIG opened a EUR 90 million (USD 96.3 million) aseptic-carton plant in India, enhancing regional supply flexibility.

- January 2025: Paperocks Indonesia highlighted hygienic meal-tray innovations for nutrition programs.

Indonesia Paper Packaging Market Report Scope

The Indonesia paper packaging market report tracks demand for the major forms of paper packaging products, including corrugated boxes, folding cartons, and other types of paper packaging. The pricing for raw materials, specifically paper and paperboard for paper products, is taken into consideration along with consumption, import, and export trends, as well as average prices, to determine the market revenue.

The Indonesian paper packaging market is segmented by type (corrugated boxes, folding cartons, and other types) and end-user industry (food and beverage, healthcare, personal care and household care, industrial, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Material Type

| Kraft Paper |

| Paperboard |

| Corrugated Board |

| Other Material Types |

By Product Type

| Flexible Paper Packaging | Pouches and Bags |

| Wraps and Films | |

| Other Flexible Paper Packaging | |

| Rigid Paper Packaging | Folding Carton |

| Corrugated Boxes | |

| Other Rigid Paper Packaging |

By Packaging Format

| Primary Packaging |

| Secondary Packaging |

| Tertiary / Transit Packaging |

By End-Use Industry

| Food |

| Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Cosmetics |

| Industrial and Electronic |

| Other End-Use Industries |

| By Material Type | Kraft Paper | |

| Paperboard | ||

| Corrugated Board | ||

| Other Material Types | ||

| By Product Type | Flexible Paper Packaging | Pouches and Bags |

| Wraps and Films | ||

| Other Flexible Paper Packaging | ||

| Rigid Paper Packaging | Folding Carton | |

| Corrugated Boxes | ||

| Other Rigid Paper Packaging | ||

| By Packaging Format | Primary Packaging | |

| Secondary Packaging | ||

| Tertiary / Transit Packaging | ||

| By End-Use Industry | Food | |

| Beverage | ||

| Healthcare and Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Industrial and Electronic | ||

| Other End-Use Industries | ||

Key Questions Answered in the Report

How large is the Indonesia paper packaging market in 2026?

The market is valued at USD 16.02 billion in 2026 and is forecast to grow at a 5.72% CAGR to 2031.

Which material dominates demand in Indonesian paper packs?

Corrugated board leads with 53.61% share thanks to its ability to protect goods shipped across humid, multi-modal routes.

What segment is growing fastest by product type?

Folding cartons are the fastest, advancing at an 7.76% CAGR through 2031 on rising premium-goods packaging.

Why is secondary packaging so important in Indonesia?

Complex archipelago logistics require multilayer protection, giving secondary formats 46.05% share and a 6.74% CAGR.

Which end-use shows the highest growth outlook?

Personal care and cosmetics are projected to expand at 7.53% annually as Indonesia’s beauty market premiumizes.

What is a key challenge restraining market growth?

Volatile recovered-paper import rules add up to 20% cost swings for mills reliant on recycled fiber.

Page last updated on: