Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 39.14 Billion |

| Market Size (2026) | USD 40.80 Billion |

| Market Size (2031) | USD 48.96 Billion |

| Growth Rate (2026 - 2031) | 3.71% CAGR |

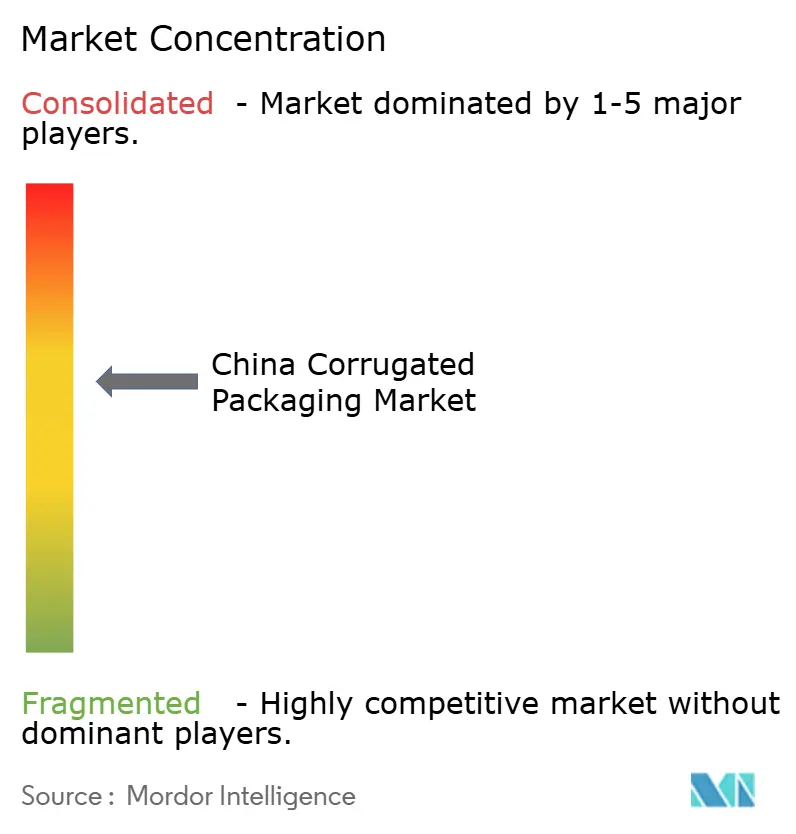

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Corrugated Packaging Market Analysis by Mordor Intelligence

The China corrugated packaging market size is projected to be USD 39.14 billion in 2025, USD 40.80 billion in 2026, and reach USD 48.96 billion by 2031, growing at a CAGR of 3.71% from 2026 to 2031. Demand is propelled by parcel-shipping growth, stringent recycled-content mandates, and premiumization in fresh-produce and luxury e-commerce shipping. Major players are adding integrated pulp capacity to secure fiber while small converters differentiate through digital printing and short-run agility. Environmental rules that tighten recovered-paper imports are raising input costs, yet they also reinforce recycled linerboard’s dominance. Flexible plastics remain a competitive threat, but their limited recyclability and emerging circular-economy penalties temper substitution risk.

Key Report Takeaways

- By end-user, e-commerce fulfillment centers captured 23.24% of the China corrugated packaging market share in 2025.

- By material, the China corrugated packaging market size for the virgin kraft linerboard segment is forecast to advance at a 4.77% CAGR through 2031.

- By flute type, the B flute captured 34.15% of the China corrugated packaging market share in 2025.

- By wall type, the China corrugated packaging market size for the triple-wall segment is forecast to advance at a 4.68% CAGR through 2031.

- By packaging format, regular slotted containers captured 38.23% of the China corrugated packaging market share in 2025.

- By print technology, the China corrugated packaging market size for the digital inkjet segment is forecast to advance at a 4.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding E-Commerce Fulfillment Demand | +1.10% | National, Yangtze River Delta and Pearl River Delta logistics hubs | Medium term (2-4 years) |

| Rising Environmental Regulations Favoring Recyclable Packaging | +0.80% | National, stricter in Tier-1 cities | Long term (≥ 4 years) |

| Growth in Fresh Produce and Food Delivery Services | +0.60% | National, early gains in Guangdong, Sichuan, Yunnan | Medium term (2-4 years) |

| Urbanization Driving Consumer Goods Consumption | +0.50% | National, spillover to Tier-2 and Tier-3 cities | Long term (≥ 4 years) |

| Provincial Incentives for Lightweight Packaging Innovation | +0.30% | Zhejiang, Jiangsu, Guangdong | Short term (≤ 2 years) |

| Adoption of Digital Print-On-Demand Corrugated Boxes by SMEs | +0.20% | National, Yangtze River Delta SME clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding E-Commerce Fulfillment Demand

China processed 175 billion parcels in 2024, and corrugated boxes accounted for roughly 68% of that volume, cementing the channel as the single largest off-taker in the China corrugated packaging market.[1]China Daily, “China’s Parcel Volume Hits 175 Billion,” chinadaily.com.cn Fulfillment centers are shifting from regular slotted containers to right-sized, die-cut boxes that reduce void fill, enabling automated lines to complete a pack cycle in under 30 seconds. JD Logistics eliminated more than 1 billion secondary cartons in 2024, forcing converters to compete on lead time, digital customization, and design precision rather than tonnage.[2]JD Logistics, “Sustainability Report 2024,” jd.com Cross-border sellers in the Hainan Free Trade Port and the Greater Bay Area demand micro flute formats that comply with International Air Transport Association dimensional-weight rules, sustaining unit growth even as average board weight declines.[3]International Air Transport Association, “Dimensional Weight Guidelines for Air Cargo,” iata.org Livestream shopping, a channel that generated CNY 4.9 trillion (USD 0.68 trillion) in gross merchandise value during 2025, has turned packaging into on-screen advertising, prompting brands to pay 40%-60% premiums for litho-laminated, camera-ready shippers.

Rising Environmental Regulations Favoring Recyclable Packaging

The Ministry of Ecology and Environment raised the recycled-content threshold for new corrugated boxes to 85% by 2027, up from a 70% baseline, anchoring recycled linerboard’s 63.21% share in 2025. Import quotas that cut recovered-paper inflows to 4.2 million tonnes in 2025 tightened domestic scrap markets, lifting prices 12% year on year. Provincial extended-producer-responsibility pilots shift collection costs to brand owners, accelerating lightweighting and alternative-fiber trials in Zhejiang and Jiangsu. In pharmaceuticals, the new T/CNPPA 3029-2025 standard specifies low moisture-vapor transmission, carving a regulatory moat for virgin kraft grades in cold-chain cartons. Large mills capitalize on scale to absorb wastewater and VOC-control capex, while regional converters face margin erosion of 8%-12% under the 14th Five-Year Plan.

Growth in Fresh Produce and Food Delivery Services

Cold-chain warehouse capacity reached 200 million m³ in 2025, expanding 15% year on year and boosting demand for triple-wall and wax-alternative moisture-barrier boxes that resist compression at 2-8 °C. Municipal bans on expanded polystyrene in 46 cities pushed food-delivery volumes toward fiber bowls and trays, embedding corrugated as the tertiary pack for 52 billion meal orders last year. The agriculture ministry targets spoilage below 5% for high-value fruits by 2027, spurring ventilated box adoption that balances ethylene off-gassing with stacking strength. Inland pack-houses in Yunnan and Sichuan now install short-run corrugators with 48-hour lead times from harvest to shipment, supporting premium air-freight exports to Southeast Asia.[4]Bloomberg News, “Livestream Shopping Drives Premium Packaging,” bloomberg.com Brand owners pay surcharges for polyethylene-coated barriers that can still be repulped under aqueous processes, linking food safety with recyclability targets.

Urbanization Driving Consumer Goods Consumption

Urbanization hit 67.3% in 2025, adding around 12 million migrants per year and concentrating disposable income in city clusters that favor pre-packed goods housed in secondary corrugated. Tier-2 and Tier-3 cities such as Chengdu and Wuhan are outpacing coastal megacities in per-capita box usage as modern retailers displace wet markets. Fifteen-minute delivery apps fuel micro-fulfillment nodes that rely on pre-erected corrugated kits, compressing replenishment cycles to under 30 minutes. New household formation in interior provinces correlates with first-time appliance purchases that require packaging with an edge-crush strength of 8 kN/m. Consumption vouchers, Guangdong alone issued CNY 2.8 billion (USD 0.39 billion) in 2025, triggering short bursts of volume that reward converters with flexible scheduling systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Recovered Paper Import Policies | -0.40% | National, acute in coastal mills | Short term (≤ 2 years) |

| Competition from Flexible Plastic Packaging | -0.30% | National, dry-food and beverage categories | Medium term (2-4 years) |

| Bottlenecks in Last-Mile Logistics Pallet Standardization | -0.20% | National distribution networks | Medium term (2-4 years) |

| Emerging Bioplastic Corrugated Alternatives from Startups | -0.10% | Zhejiang and Jiangsu innovation zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Recovered Paper Import Policies

Imports slid to 4.2 million tonnes in 2025 under a 0.3% contamination cap, exposing mills to spot-market spikes and lengthening customs clearance from 7 to 18 days. Domestic OCC prices rose 12%, squeezing converters without captive pulping and prompting some buyers to shift to flexible pouches despite recyclability trade-offs. Coastal mills that historically favored long-fiber American scrap are reallocating capital to virgin pulp, illustrated by Nine Dragons’ USD 4.8 billion Beihai complex with 1.1 million tonnes of chemical pulp. Municipal collection remains fragmented, with 35% of urban corrugated waste still co-mingled, adding de-inking costs and weakening small-mill competitiveness.

Competition from Flexible Plastic Packaging

Stand-up pouches gained 8% incremental share in dry foods during 2024-2025 by offering moisture barriers and resealable zippers that corrugated cartons cannot match without expensive coatings. Unit economics favor plastics by 20%-30%, though upcoming EPR levies and poor curbside recyclability raise long-term risk. In beverages, aseptic cartons and PET bottles reduce the need for corrugated secondary packs, a shift accelerated by New Jufeng’s HKD 2.729 billion (USD 0.35 billion) acquisition of Fenmei Packaging, which consolidates aseptic capacity. JD Logistics is piloting 5 million reusable plastic totes for grocery delivery in Beijing and Shanghai, further displacing single-use boxes. Yet plastics face higher tooling costs and slower design cycles, keeping corrugated relevant for rapid promotion turnaround.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Dominates While Virgin Grades Win Premium Niches

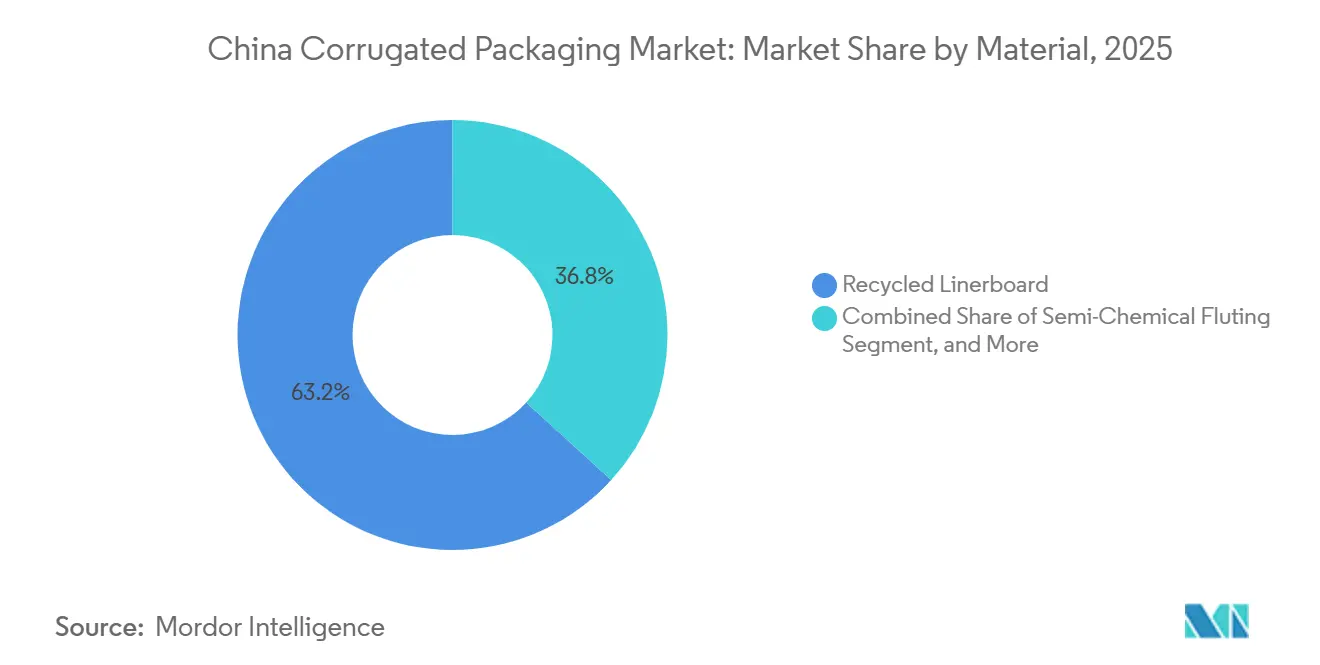

Recycled linerboard accounted for 63.21% of the China corrugated packaging market in 2025, reflecting the mandated 85% recycled content requirement for express parcels by 2027. Integrated mills capture feedstock advantages through nationwide OCC collection networks, anchoring their cost leadership. Virgin Kraft linerboard is forecast to expand at 4.77% CAGR, outperforming overall growth as fresh-produce exporters and luxury e-commerce brands demand higher ring-crush strength, tear resistance, and cleaner print surfaces. Nine Dragons’ Beihai mill and Lee and Man’s specialty-kraft upgrades target this premium. Corrugating medium producers are testing semi-chemical pulps from bamboo and straw to hedge softwood risks, though moisture sensitivity still confines such grades to low-humidity logistics corridors.

Bio-based barrier coatings and starch adhesives are scaling up in pilot runs to achieve recyclability without wax, signaling that the China corrugated packaging market will bifurcate into high-volume recycled-content and smaller, high-margin virgin niches. In parallel, food-contact and pharmaceutical mandates under T/CNPPA 3029-2025 steer critical temperature-controlled applications toward virgin fiber, guaranteeing a price umbrella that offsets higher raw-material costs. The converter strategy, therefore, splits commodity players chase recycled linerboard efficiency, while value-added specialists court brand owners with premium kraft and functional coatings.

By Flute Type: Micro Flutes Capture Lightweight Logistics Opportunities

B flute held 34.15% of the China corrugated packaging market share in 2025 because of its cushioning-to-cost balance in general merchandise. However, the F flute is accelerating at 4.15% CAGR through 2031 as cross-border sellers optimize for dimensional weight and cosmetics brands seek offset-level graphics. The flute’s 0.75-1.0 mm caliper allows direct lithographic printing, eliminating litho-lamination steps and lowering inventory bulk, which is vital in automated warehouses with height constraints.

E flute remains the compromise format for retail-ready displays, offering rigidity with acceptable board economy. A flute persists for fragile ceramics and heavy industrial parts owing to its 5 mm thickness, though its share erodes under lightweighting mandates. Corrugator OEMs now ship quick-change cassette systems that let factories swap flute profiles in under 15 minutes, democratizing micro flute access for small and medium enterprises and enhancing adoption momentum.

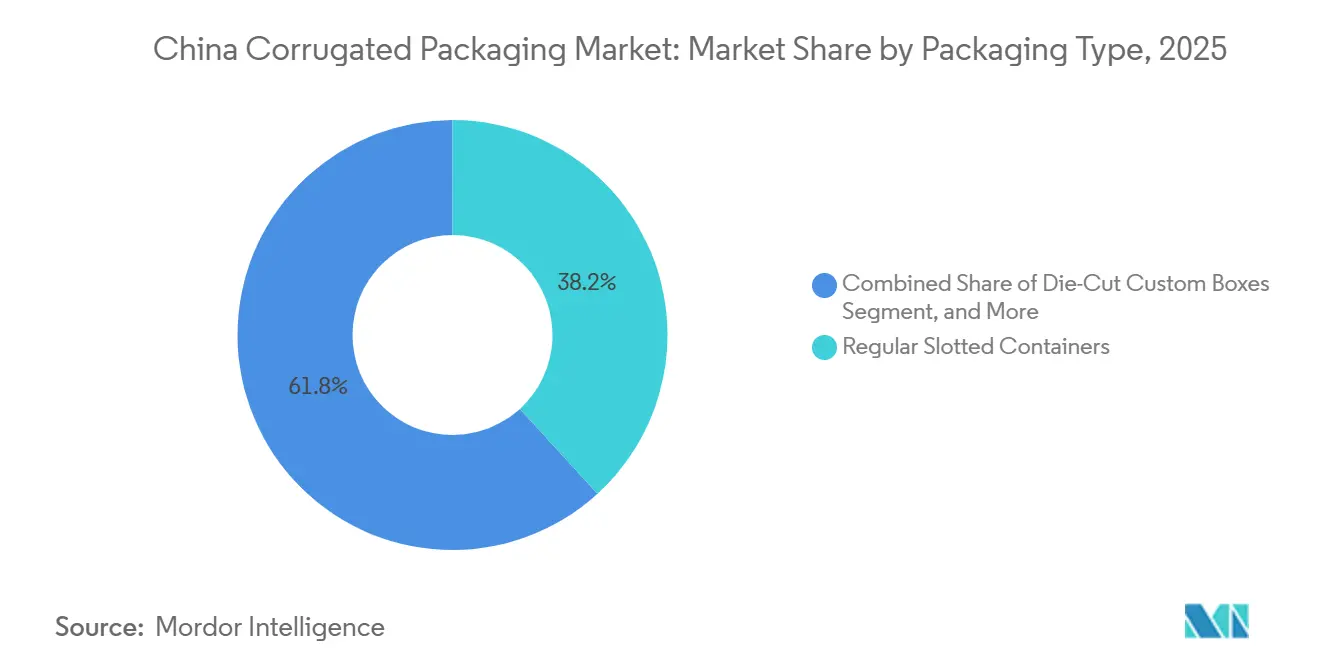

By Packaging Type: Custom Die-Cut Formats Earn Premium Margins

Regular slotted containers (RSCs) accounted for 38.23% of the China corrugated packaging market in 2025, thanks to their ease of automation. Die-cut custom boxes, projected to climb at 4.18% CAGR, monetize the unboxing moment in livestream commerce by embedding pull-tabs, windows, and embossed logos that convert viewers to buyers. These structures command 40%-60% price uplifts and let converters tap marketing budgets rather than procurement lines.

Folding cartons straddle corrugated and paperboard, serving cosmetics and over-the-counter drugs where shelf footprint trumps cushioning. Point-of-purchase displays emerge as an ancillary revenue stream; brands fund them from trade-promotion allocations, insulating converters from linerboard volatility. Pallet boxes address heavy industrial freight with triple-wall sides and reinforced corners, supporting static loads of up to 1,000 kg while remaining recyclable. The result is a two-tier converter landscape, where high-volume RSC specialists maximize uptime, whereas design-led firms chase smaller, higher-margin custom runs.

By Wall Type: Triple-Wall Gains Share in Cold-Chain Pharmaceuticals

Single-wall formats accounted for 51.34% of the China corrugated packaging market in 2025, dominating e-commerce and the light industry, where edge crush strengths of 4-6 kN/m suffice. Triple-wall boxes, though niche, are forecast to rise at 4.68% CAGR through 2031 as biologics and vaccine shippers replace expanded polystyrene with fiber-based insulation compliant with circular-economy penalties on non-recyclables. The new pharmaceutical cartonboard standard stipulates ≤5 g/m²/24 h moisture-vapor transmission, a threshold that triple-wall structures with specialty liners meet without polyethylene layers.

Double-wall remains the midpoint for appliances and furniture, balancing strength against dimensional-weight fees in air freight. Single-face corrugated retains a limited role as protective wrapping and void fill, supporting fragile components inside primary packs. Converter investments reflect divergence commodity plants install ultra-high-speed single-wall corrugators above 300 m/min, while specialty lines adopt wider, slower triple-wall machines with in-line lamination for phase-change material integration.

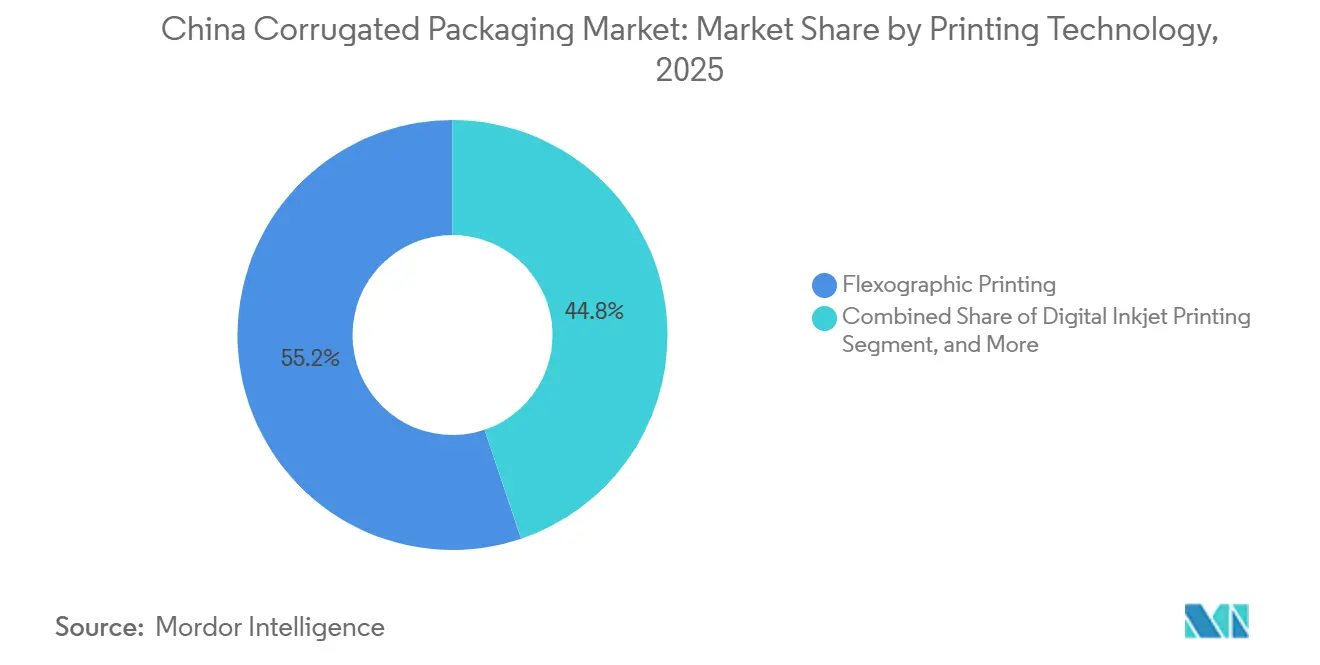

By Printing Technology: Digital Inkjet Accelerates Short-Run Customization

Flexographic presses retained a 55.19% share in 2025, thanks to throughputs approaching 15,000 impressions per hour and compliance with VOC ceilings for water-based inks. Digital inkjet is advancing at a 4.46% CAGR because it slashes setup time from 72 hours to under 4, enabling print-on-demand cartons for seasonal or influencer-driven drops. A 500-unit run that once took 10 days now ships in 48 hours, freeing working capital and slashing obsolescence.

Litho-lamination remains preferred for photo-quality cosmetic packs, yet loses ground to direct-digital as inkjet resolution rises. Screen printing keeps a premium niche for metallic and high-build varnish effects in luxury gift sets. Regulatory serialization in food and pharma also boosts adoption of thermal inkjet and laser coding, embedding traceability at the converter level.

By End-User Industry: Pharmaceuticals Outpace an E-Commerce Core

E-commerce fulfillment retained 23.24% market share in 2025 and remains the anchor of the China corrugated packaging market. Automation in giant hubs near Suzhou and Dongguan standardizes box footprint, reinforcing RSC dominance but increasing demand for micro flute right-sizing inserts. Pharmaceuticals, though smaller today, will expand at 4.56% CAGR because biologics and vaccines require triple-wall insulated shippers certified for 48-hour hold times.

Processed food, beverages, and fresh produce continue to drive volume, each with distinct moisture-barrier and ventilation needs to meet the agriculture ministry spoilage goals. Electrical goods, cosmetics, and personal care continue to use litho-laminated micro flute cartons as point-of-purchase billboards. Industrial machinery, automotive parts, and furniture sustain demand for double- and triple-wall corrugated packaging, showing that the China corrugated packaging market spans commodity to engineered niches.

Geography Analysis

Provincial clustering defines production economics. Guangdong, Zhejiang, and Jiangsu generated an estimated 58% of domestic containerboard capacity in 2025, leveraging export-oriented manufacturing and port access. Guangdong’s Pearl River Delta hosts Nine Dragons’ 3.5 million-tonne Dongguan mill and more than 200 converters supplying cross-border parcels to Southeast Asia and North America. Zhejiang’s Pinghu district achieved 100% recycled-content output under local mandates, while Xiaoshan’s Jinyi Jia invested CNY 600 million (USD 84 million) in plate-less digital presses to serve multinational retailers. Jiangsu’s Kunshan drew Blackstone’s USD 800-900 million purchase of ShyaHsin Packaging in 2025, signaling private-equity faith in premium litho segments.

Inland provinces are catching capacity. Guangxi’s Beihai, backed by Nine Dragons’ USD 4.8 billion megacomplex, will ship 7.95 million tonnes annually by full ramp-up, bridging fiber security through integrated chemical pulp and balancing coastal overconcentration. Sichuan’s Leshan project leverages bamboo fiber and hydropower to supply specialty electrical insulation and fruit-bag grades, reducing logistics drag to western orchard belts. Hubei’s Jingzhou expansion adds 2 million tonnes of packaging paper to serve central auto clusters, reflecting a strategic inland pivot amid rising coastal labor and land costs.

Logistics corridors strengthen regional niches. The Yangtze River Delta aggregates micro flute, digital-print converters aligned with SME export workshops. The Pearl River Delta supports high-speed RSC and international parcel formats. Emerging western hubs focus on fruit export and cold-chain, demanding phase-change-enabled triple-wall boxes. This geographic mosaic underpins supply security, cost optimization, and rapid response to localized policy incentives, anchoring resilience in the China corrugated packaging market.

Competitive Landscape

Market concentration is moderate. Nine Dragons, Lee and Man, and Shanying International run more than 35 million tonnes of containerboard capacity, but roughly 8,000 small-to-mid converters dilute the downstream share. Scale players integrate backward into chemical pulp and forward into box plants, lowering fiber risk and capturing margin from design to delivery. Nine Dragons’ Beihai hub underscores this model by bringing together pulp, containerboard, and converting under one roof. Lee and Man reported FY2025 revenue of HKD 25.8 billion (USD 3.3 billion) and net profit of HKD 2.5 billion (USD 321 million), reflecting disciplined capex and recovered-paper hedging.

Technology divergence is sharpening. Large mills deploy AI-driven trim optimization and IoT moisture sensors that trim waste 3%-5%, whereas agile converters buy digital inkjet presses to win 500-unit, high-mix jobs where speed outranks unit economics. Dreame Technology’s founder invested CNY 2.282 billion (USD 0.32 billion) for a controlling stake in Jia Mei Packaging, importing consumer electronics, precision, and digitization know-how. Foreign majors such as International Paper keep distribution nodes but lack integrated domestic lines, ceding volume to local incumbents protected by land, permitting, and policy familiarity.

Value-added blue oceans are opening. Cold-chain pharma shippers with embedded phase-change packs, RFID tags, and moisture-barrier liners attract margins multiple times RSC pricing. Converters partnering with biotech distributors are winning long-term contracts that insulate against OCC cost swings. Meanwhile, flexible-package challengers force corrugated makers to offer design services, warehouse analytics, and inventory financing to defend share.

China Corrugated Packaging Industry Leaders

Shanying International Holdings Co. Ltd.

Nine Dragons Paper (Holdings) Limited

Lee & Man Paper Manufacturing Ltd.

Hung Hing Printing Group Limited

New Asia Packaging Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Yutong Technology paid CNY 449 million (USD 62.9 million) for 51% of Dongguan Huayan New Materials, diversifying into precision smart-device components and offsetting low packaging margins.

- January 2026: Suzhou Zhuyue Hongzhi spent CNY 2.282 billion (USD 0.32 billion) for 54.90% of Jia Mei Packaging, injecting industrial digitization expertise into beverage cans and corrugated converting.

- January 2025: ORG completed a HKD 2.729 billion (USD 0.35 billion) takeover of COFCO Packaging, forming a CNY 30 billion (USD 3.84 billion) revenue leader across metal and corrugated lines.

- January 2025: New Jufeng launched a HKD 2.729 billion (USD 0.35 billion) bid for Fenmei Packaging to consolidate aseptic-packaging capacity.

China Corrugated Packaging Market Report Scope

The China Corrugated Packaging Market report encompasses a comprehensive analysis of fiber-based and polymer-based (PP) corrugated materials used for the containment, protection, and transport of goods across diverse industrial and retail sectors. The market refers to the industry that produces multi-layered boards, typically consisting of a fluted medium sandwiched between linerboards, designed to provide high strength-to-weight ratios and crush resistance for secondary and tertiary packaging.

The China Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

By Material

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

By Flute Type

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

By Packaging Type

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

By Wall Type

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

By Printing Technology

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

By End-User Industry

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Paper Products |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Paper Products | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current China corrugated packaging market size and its expected growth?

The market is valued at USD 39.14 billion in 2025 and is projected to reach USD 48.96 billion by 2031, registering a 3.71% CAGR from 2026-2031.

Which end-user sector is growing fastest for corrugated boxes in China?

Pharmaceuticals lead growth at a 4.56% CAGR as biologics and vaccines require insulated, triple-wall shippers.

How are environmental policies affecting corrugated packaging materials?

Stricter recycled-content rules and import limits on wastepaper favor recycled linerboard yet raise OCC prices, prompting mills to integrate virgin pulp and develop lightweight designs.

Why is digital inkjet printing gaining share in China's corrugated sector?

It cuts setup to under four hours, enables variable data, and supports small promotional runs that e-commerce and livestream sellers demand.

Which provinces dominate containerboard capacity in China?

Guangdong, Zhejiang, and Jiangsu together account for roughly 58% of national capacity, while Guangxi, Sichuan, and Hubei are emerging inland hubs.

What competitive strategies distinguish leading Chinese corrugated producers?

Market leaders integrate backward into pulp, deploy Industry 4.0 automation for efficiency, and expand into value-added cold-chain and die-cut segments to buffer commodity price swings.

Page last updated on: