Japan Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 12.79 Billion |

| Market Size (2026) | USD 13.17 Billion |

| Market Size (2031) | USD 14.86 Billion |

| Growth Rate (2026 - 2031) | 2.44% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Corrugated Packaging Market Analysis by Mordor Intelligence

The Japan corrugated packaging market size is projected to expand from USD 12.79 billion in 2025 and USD 13.17 billion in 2026 to USD 14.86 billion by 2031, registering a CAGR of 2.44% between 2026 and 2031. Beneath the moderate headline growth, the Japan corrugated packaging market is shifting toward lighter substrates, higher recovered-paper content, and digitally printed short-run boxes that support e-commerce personalization. Recycled linerboard already accounts for more than half of board consumption, while semi-chemical fluting is the fastest-growing medium as converters try to cut raw-material weight without sacrificing stacking strength. Demand is buttressed by B2C e-commerce, which reached JPY 26.1 trillion (USD 186.4 billion) in FY 2024, record processed-food exports of JPY 1.7 trillion (USD 12.1 billion) in 2025, and regulatory measures that reward mono-material designs over single-use plastics. At the same time, publishers of the Japanese corrugated packaging market highlight emerging investments in heavy-duty triple-wall formats for semiconductor equipment and seafood exports, signaling new premium niches even as domestic shipment volumes plateau.

Key Report Takeaways

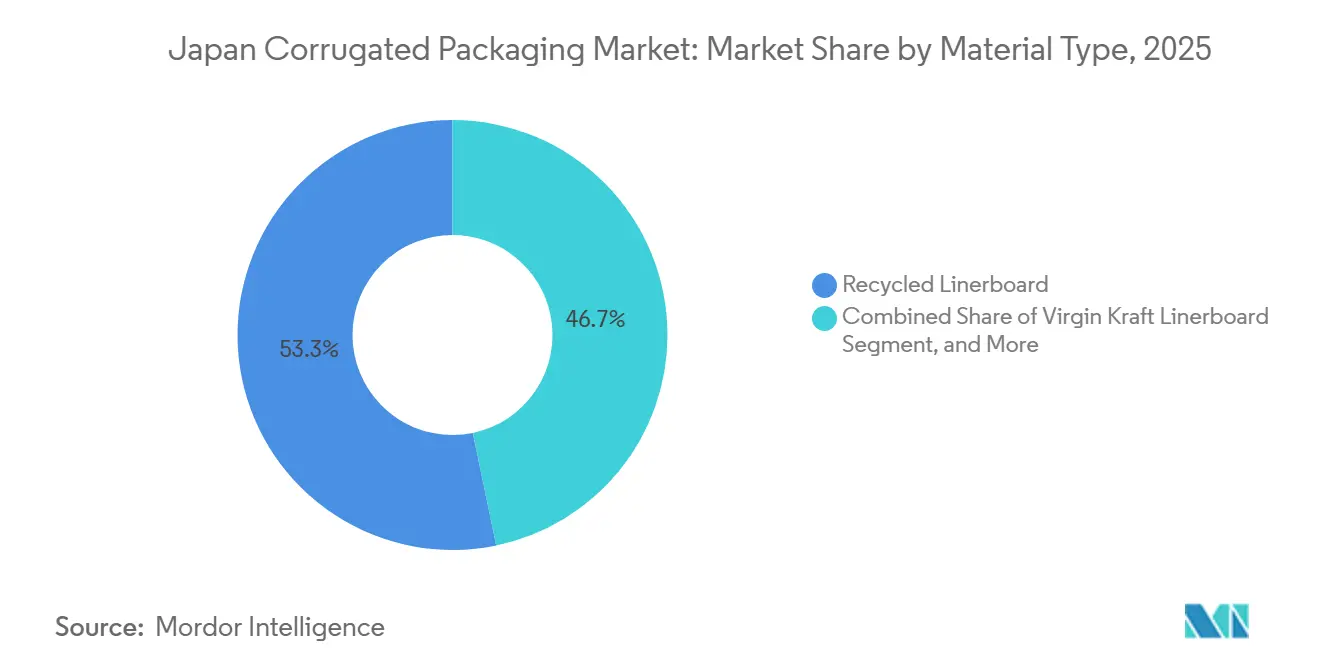

- By material type, the recycled linerboard segment captured 53.26% of the Japan corrugated packaging market share in 2025.

- By flute type, the Japan corrugated packaging market size for e-flute is projected to grow at an 3.73% CAGR through 2031.

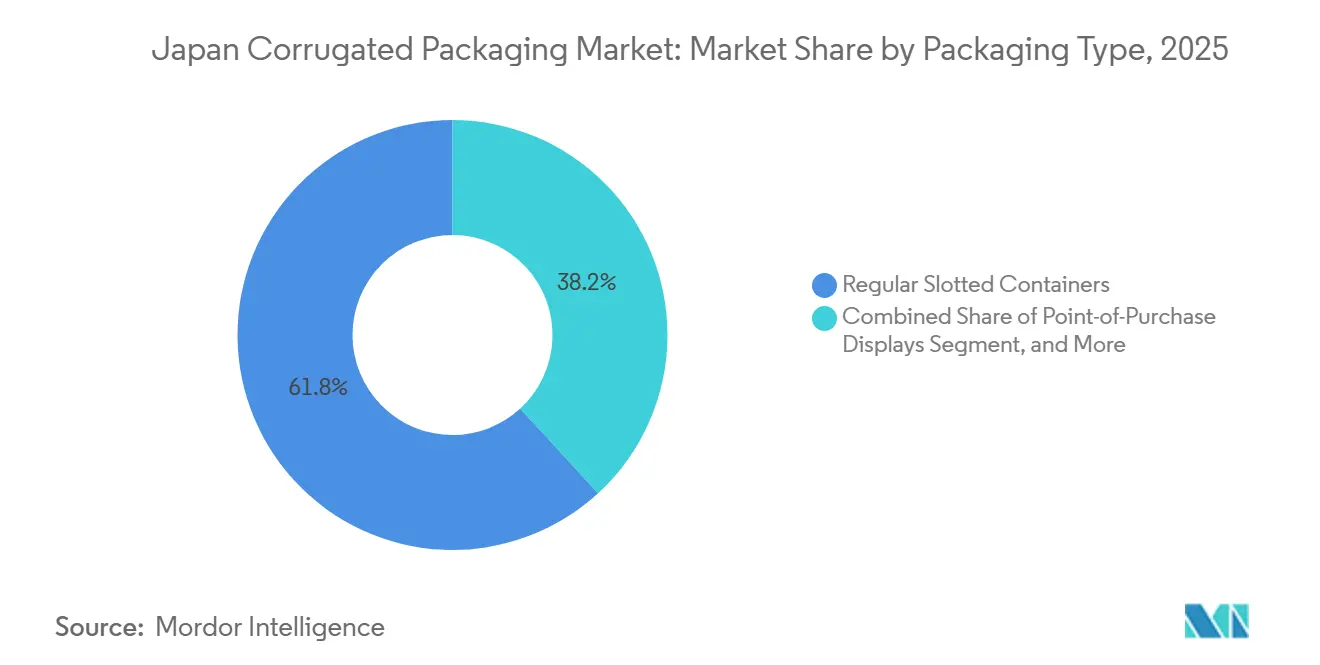

- By packaging type, the regular slotted containers segment captured 61.84% of the Japan corrugated packaging market share in 2025.

- By wall type, the Japan corrugated packaging market size for triple-wall is projected to grow at an 3.76% CAGR through 2031.

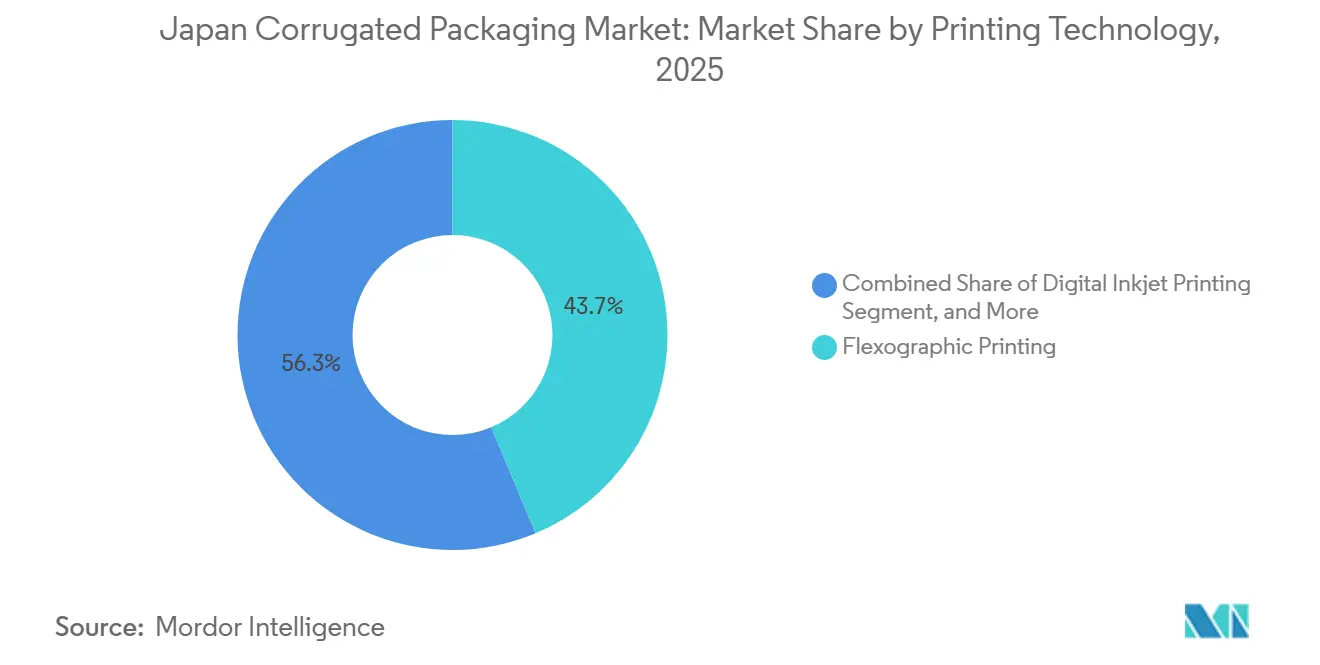

- By printing technology, the flexographic printing segment captured 43.68% of the Japan corrugated packaging market share in 2025.

- By end-user industry, the Japan corrugated packaging market size for pharmaceuticals is projected to grow at an 3.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-Commerce Logistics Acceleration | +0.9% | Tokyo, Osaka, Nagoya corridors | Medium term (2–4 years) |

| Growth in Processed Food and Beverage Exports | +0.6% | Hokkaido and Kyushu supply hubs | Medium term (2–4 years) |

| Regulatory Shift Toward Recyclable Packaging | +0.5% | Nationwide | Long term (≥ 4 years) |

| Nearshoring-Led Electronics Output | +0.3% | Kumamoto, Kyushu, Tohoku | Long term (≥ 4 years) |

| Craft-Brewery Demand for Custom Boxes | +0.1% | Urban craft-beer clusters | Short term (≤ 2 years) |

| Government Subsidies for Bio-Based Barrier Coatings | +0.1% | Pilot sites nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce Logistics Acceleration

Parcel volumes keep rising as Japanese shoppers spend JPY 26.1 trillion (USD 186.4 billion) online, with penetration close to 10% of national retail sales. Online grocery alone accounted for JPY 3.12 trillion (USD 22.3 billion), requiring insulated, leak-resistant corrugated shippers that replace bulky EPS coolers. Cross-border purchases valued at JPY 5.78 trillion (USD 41.3 billion) create export-grade box requirements that meet China and U.S. labeling rules. Subscription cosmetics and D2C health brands increase the frequency of small parcels, favoring digitally printed mailers that can be right-sized on demand.[1]Nippon.com Data Team, “Japan’s Food Exports Rise to JPY 1.7 Trillion in 2025,” nippon.com Logistics companies now optimize truck cube and dimensional-weight fees, so thinner flutes and precise die cuts are preferred.

Growth in Processed Food and Beverage Exports

Japan’s farm and food exports climbed 12.8% in 2025 to a record USD 12.1 billion, boosting demand for export-certified corrugated with moisture barriers and triple-wall stacking strength. Scallops alone contributed JPY 90.6 billion (USD 0.65 billion), requiring refrigerated bulk boxes, while powdered matcha nearly doubled to JPY 72.1 billion (USD 0.52 billion), prompting converters to shift toward lightweight E-flute retail packs. U.S. imports of Japanese foods grew 13.7%, and China rebounded 7.0%, tightening specifications for corrugated barrier coatings that can withstand long sea journeys while remaining recyclable at destination ports.

Regulatory Shift Toward Recyclable Packaging

From January 2026, METI will certify packaging that meets mandated recycled or bio-based plastic thresholds, and the positive list for food-contact synthetics took effect in June 2025. Producers who move to mono-material corrugated avoid costly compliance audits tied to coatings or laminates. Large buyers under Japan’s Green Purchase Act now specify verified low-carbon boxes, so containerboard mills publicize renewable-energy boilers and LNG conversions to win tenders. Retailers also favor boxes that carry GHG reduction logos, accelerating investment in cellulose nanofiber-reinforced grades that deliver equivalent burst strength with 8–10% less fiber.

Nearshoring-Led Electronics Output

Government subsidies attract semiconductor foundries and EV battery plants to Kyushu and Tohoku, increasing shipments of fragile wafers and high-value modules that need triple-wall, anti-static corrugated interiors. Automation on these new lines favors board designs compatible with robotic case erectors and vision-guided palletizers. The elderly workforce shortage magnifies the advantage of lighter, ergonomic boxes that reduce injury risk on assembly floors. As component makers adopt zero-defect logistics, converters must supply corrugated that meets Class III clean-room particle limits, opening premium niches within the Japan corrugated packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycled Paper Price Volatility | -0.4% | Nationwide, export-exposed ports | Short term (≤ 2 years) |

| Competition From Returnable Plastic Crates | -0.2% | Aichi, Kanagawa, Kyushu OEM hubs | Medium term (2–4 years) |

| Water-Scarcity Constraints on Mills | -0.1% | Coastal Shikoku and Kyushu sites | Long term (≥ 4 years) |

| Dependence on Imported Virgin Fiber | -0.1% | Nationwide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Recycled Paper Price Volatility

OCC export prices hovered at USD 170-175 per tonne in early 2025, yet Chinese demand spikes can push quotations up USD 10-15 within weeks. Japanese mills that rely on 98% recovered paper feedstock face profit swings because customer price adjustments lag by one to two quarters. Seasonal Lunar New Year slowdowns momentarily ease pressure, but the underlying upswing limits the margin for converters serving fixed-price retail contracts.

Competition From Returnable Plastic Crates

Automotive and electronics OEMs in Aichi and Kyushu increasingly mandate reusable plastic totes for in-plant loops, citing ergonomic gains and lower waste. Corrugated loses volume on these high-frequency, short-haul routes. Box makers fight back with collapsible paper-based RTIs that fold flat on the return leg, yet lifecycle costing still tilts toward plastic in closed-loop systems. Packaging suppliers are responding by offering hybrid solutions, such as collapsible corrugated containers with reusable corner posts and locking mechanisms, that bridge the cost-performance gap between one-way and fully reusable systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Grades Dominate While Semi-Chemical Fluting Accelerates

Recycled linerboard claimed 53.26% of the Japanese corrugated packaging market in 2025, mirroring the country’s world-leading fiber recovery culture. Domestic majors such as Oji Holdings operate containerboard mills with recycled content approaching 100%, providing brand owners with a low-carbon supply chain at a competitive price. Virgin Kraft retains a small but critical niche for chilled seafood and overseas beef shipments, where humidity can jeopardize board integrity. Semi-chemical fluting is on a 4.21% CAGR trajectory to 2031, as its superior stiffness-to-weight ratio grants an 8.7% material saving versus legacy A flute. On the innovation front, Daio Paper commercialized cellulose nanofiber composites in mid-2025, which enable a thinner medium without flattening under top-load.

These composites also satisfy new regulatory lists that restrict non-approved adhesives and coatings, pushing converters to embrace single-material builds. Semi-chemical products are especially attractive to e-commerce shippers that ship volumetric-weight-priced parcels to urban micro-fulfillment centers. Craft food exporters point to crush resistance gains that cut denting claims by double digits on long hauls. Meanwhile, virgin kraft suppliers hedge volatility in imported North American pulp by increasing domestic softwood procurement, a move signaled by Nippon Paper Lumber’s 1 million m³ target for FY 2026.

By Flute Type: B Flute Leads but E Flute Gains on Dimensional Fees

B-flute continues to command 38.13% of shipments thanks to its 3 mm profile that balances cushioning and cube efficiency for beverage multipacks and convenience-store restocks. Yet E-flute, at a slender 1.5 mm, is growing 3.73% a year as shippers try to dodge dimensional-weight charges on last-mile vans. Digital printers applaud E flute’s smoother surface that reproduces 1200 dpi graphics without liner washboarding, making it the go-to choice for cosmetics and confectionery. Rengo’s proprietary Delta Flute, launched earlier, sits midway at 2 mm, giving retailers a “less weight, less carbon” option that still survives rough sortation.

Premium chocolatiers now specify G flute for gift boxes because its sub-1 mm thickness allows telescoping lids while retaining rigidity. Converters invest in high-precision corrugators and laser embossers to keep micro-flute calipers within ±0.05 mm tolerance. For fragile electronics and glassware, the Japan corrugated packaging market keeps A flute relevant due to its 5 mm cushion, although weight penalties limit widespread comeback. The broadening flute portfolio underscores how SKU proliferation forces box makers to match board geometry to supply-chain economics rather than rely on a one-size-fits-all standard.

By Packaging Type: Regular Slotted Containers Still Rule, Yet Custom Boxes Surge

Regular slotted containers held 61.84% share in 2025, favored for uniform palletization and compatibility with automated case erectors across groceries and pharmaceuticals. However, die-cut custom boxes are outpacing every other format with a 4.05% CAGR, as breweries, D2C apparel, and subscription meal kits seek structural storytelling. Canon’s corrPRESS iB17 enables converters to print multiple seasonal SKUs in runs of less than 20,000 m² without plates, cutting lead times for promotional launches.[2]Canon Production Printing, “Canon Announces the corrPRESS iB17,” cpp.canon

Meanwhile, point-of-purchase displays evolve into lightweight kiosks made entirely of reinforced corrugated material, reducing campaign costs for retailers who no longer need metal fixtures. Folding cartons, occupying the hinge between paperboard and corrugated, thrive in secondary packaging for ramen cups and instant beverages that demand vivid litho graphics. Pallet boxes made with wax-free barrier formulations protect frozen scallops bound for the United States, answering supermarket demands for plastic-free seafood packs.

By Wall Type: Single-Wall Prevails, Triple-Wall Emerges for Export Strength

Single-wall boards dominate everyday shipments with 71.29% share, prized for low material cost and easy recyclability. However, the export boom in seafood and precision machinery boosts triple-wall demand, forecast to rise 3.76% annually through 2031. Heavy-duty triple-wall containers pass 1.8-tonne top-load tests required for refrigerated reefers bound for Los Angeles and Shanghai. Regional fresh-fruit cooperatives in Ehime Province also adopt double-wall cartons lined with bio-based coatings to replace polystyrene crates, helping growers meet plastic-reduction pledges.

At the same time, industrial OEMs exploring closed-loop logistics experiment with reusable quadruple-wall corrugated sleeves that fold flat on the return trip, challenging plastic totes on lifecycle costs. Rengo’s TRICOR plant in Germany showcases automation blueprints that domestic mills intend to replicate, positioning Japanese producers to supply triple-wall packaging as a value-added export rather than a domestic afterthought. These shifts underscore how the Japanese corrugated packaging market adds incremental wall thickness to address rising export compliance requirements and rougher handling conditions.

By Printing Technology: Digital Inkjet Disrupts Flexo’s Reign

Flexographic presses still account for 43.68% of the printed area in 2025, yet digital inkjet volumes climb swiftly at a 3.83% CAGR. Canon’s corrPRESS iB17 operates at 8,000 m² per hour with food-safe, water-based inks, delivering photo-quality CMYK output without the need for cleaning chemicals. Early adopters such as Geopack won the 2025 Japan Packaging Contest for using wide-web inkjet to slash make-ready waste by two-thirds.

Litho-lamination remains the luxury benchmark for high-gloss electronics boxes, but its share is eroding as E flute surfaces approach the smoothness of offset printing. Screen and foil embellishments shrink to souvenir confectionery niches where tactile varnishes justify unit economics. The decisive factor is SKU volatility: Japanese cosmetics lines launch up to eight limited-edition variants per quarter, so the Japanese corrugated packaging market increasingly invests in digital workflows with automated color calibration that one operator can run, softening labor shortages across print floors.

By End-User Industry – E-Commerce Fulfillment Takes Growth Crown

Processed foods capture the largest slice at 38.57%, underpinned by shelf-stable noodles, confectionery, and condiment multipacks, which are heading to 55,000 convenience stores nationwide. Yet e-commerce fulfillment centers are expanding at the fastest pace, with a 3.74% CAGR, driven by the parcelization of groceries and cross-border demand for manga collectibles. Right-sized mailers reduce void fill, and easy-open tear strips improve customer ratings, making corrugated indispensable to last-mile success.

Fresh produce growers of mikan oranges pivot to laser-vented E flute boxes that cool produce within three hours, extending shelf life for export to Hong Kong. Beverage players rely on die-cut partitions inside B flute wraps to stop craft-beer bottle scuffing, while personal-care brands commission stock-colored FINE FLUTE to reinforce brand palettes without lamination. Electronics shippers incorporate static-dissipative liners for PCB modules, underscoring how value-added coatings keep corrugated ahead of foam inserts.

Geography Analysis

Tokyo-Osaka’s industrial corridor accounts for the majority of corrugated demand, driven by dense consumer bases, port access, and clustering of fulfillment warehouses. New investments such as Rengo’s Tokyo Plant renewal enhance local board supply and reduce inbound freight costs. Kansai follows as the second axis; Rengo’s capital tie-up with KINKI DANBORU strengthens business-continuity planning against seismic risk while widening service coverage in Kyoto and Hyogo.

Kyushu emerges as a growth hotspot, leveraging semiconductor projects and proximity to Asian sea lanes. Daio Paper’s Mishima Mill on Shikoku’s coast secures export-grade containerboard for seafood and electronics headed to China, while biomass boilers there cut Scope 1 emissions in line with national 54% reduction targets.[3]U.S. Commercial Service, “Japan Recycled Plastic Materials,” trade.gov Northern Hokkaido and Tohoku specialize in food exports; scallop producers lean on triple-wall chilled cartons to maintain product value on trans-Pacific voyages.

Rural prefectures wrestling with depopulation now tap government digital-transformation subsidies that let micro-brands sell regional delicacies online. These small-lot shipments favor digitally printed E flute boxes with QR codes linking to provenance stories, giving emerging sellers access to premium packaging without big inventories. Over time, such niche adoption balances demographic headwinds and keeps the Japan corrugated packaging market geographically diversified.

Competitive Landscape

The top four producers, Rengo, Oji Holdings, Nippon Paper Industries, and Daio Paper, control roughly 65% of domestic board capacity, yet more than 400 independent converters serve local clients, keeping end-market pricing competitive. Rengo’s Vision 120 blueprint aims to achieve JPY 1.2 trillion (USD 8.1 billion) in revenue by FY 2030 through vertical integration, automation, and overseas expansion, including the heavy-duty TRICOR plant in Germany. Daio Paper’s alliance with Hokuetsu Corp. introduces shared pulp procurement and production worth JPY 5 billion (USD 44.72 million) in operating income by FY 2026.[4]Japan IR, “Daio Paper Corp. Strategic Alliance With Hokuetsu,” japanir.jp

Nippon Paper restructures its Australian arm, Opal, boosting box output from 590 million m² to 660 million m² and trialing high-automation converting lines that could migrate back to Japan. Oji Holdings highlights a 98.3% recovered paper rate, positioning itself to meet the METI procurement lists for buyers seeking low-carbon packaging. Technology disruptors such as Think Laboratory, Uchida Yoko, and TAKEO empower small converters with digital presses and micro-flute cutters, raising the innovation bar across the Japanese corrugated packaging market.

Daio Paper’s 2,000-tonne CNF plant delivers lightweight strength gains, and Mitsubishi Paper Mills’ barricote barrier papers attack plastic-laminate niches. As export pressure rises, containerboard giants pour capital into LNG boilers and solar arrays to lock in Scope 2 emission cuts, converting environmental compliance into a sales differentiator. Overall, rivalry intensifies not on capacity alone but on automation, ESG performance, and the ability to offer turnkey box-design services that integrate digital printing and right-sizing software.

Japan Corrugated Packaging Industry Leaders

Oji Holdings Corporation

Nippon Paper Industries Co., Ltd.

Nine Dragons Paper (Holdings) Limited

Rengo Co., Ltd.

Tri-Wall Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Rengo’s Tri-Wall unit opened a corrugated packaging plant in Shandong Province, China, to reinforce Asian heavy-duty supply.

- December 2025: Rengo’s TRICOR Packaging launched a 54,000 m² heavy-duty plant in Goch, Germany, featuring automated warehouses and photovoltaic power.

- September 2025: Geopack installed Think Laboratory’s wide-web water-based digital inkjet press, winning the 2025 Japan Packaging Contest award for waste reduction.

- July 2025: Daio Paper scaled cellulose nanofiber composite output to 2,000 tonnes per year to supply lightweight, high-strength corrugated board.

Japan Corrugated Packaging Market Report Scope

The Japan corrugated packaging market is defined as the industrial sector focused on the production and conversion of fluted paperboard materials into secondary and tertiary packaging solutions, such as regular slotted containers, die-cut boxes, and structural protective pads. This market is characterized by a sophisticated infrastructure that emphasizes high-quality material grades, including lightweight and moisture-resistant linerboards, designed to support the country's automated logistics networks and precision manufacturing exports.

The Japan Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Japan corrugated packaging market and how fast is it growing?

The market stood at USD 12.79 billion in 2025, is expected to reach USD 13.17 billion in 2026, and is projected to climb to USD 14.86 billion by 2031, reflecting a 2.44% CAGR over 2026-2031.

Which material accounts for the largest share of domestic corrugated board consumption?

Recycled linerboard leads, supplying 53.26% of all board used by Japanese converters in 2025.

Why is E-flute demand accelerating in Japan?

E-flute’s thin 1.5 mm profile lowers dimensional-weight fees for e-commerce parcels and offers a smoother print surface for high-resolution graphics, driving a projected 3.73% CAGR through 2031.

How are Japanese regulations changing packaging specifications?

2026 METI certification rules and the 2025 positive list for food-contact synthetics reward mono-material, fully recyclable corrugated solutions and discourage plastic laminates.

Which printing technology is gaining share most quickly?

Industrial-scale digital inkjet is expanding at 3.83% CAGR, helped by Canon’s corrPRESS iB17 press that eliminates plates and shortens setup times for multi-SKU jobs.

Page last updated on: