Netherlands Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

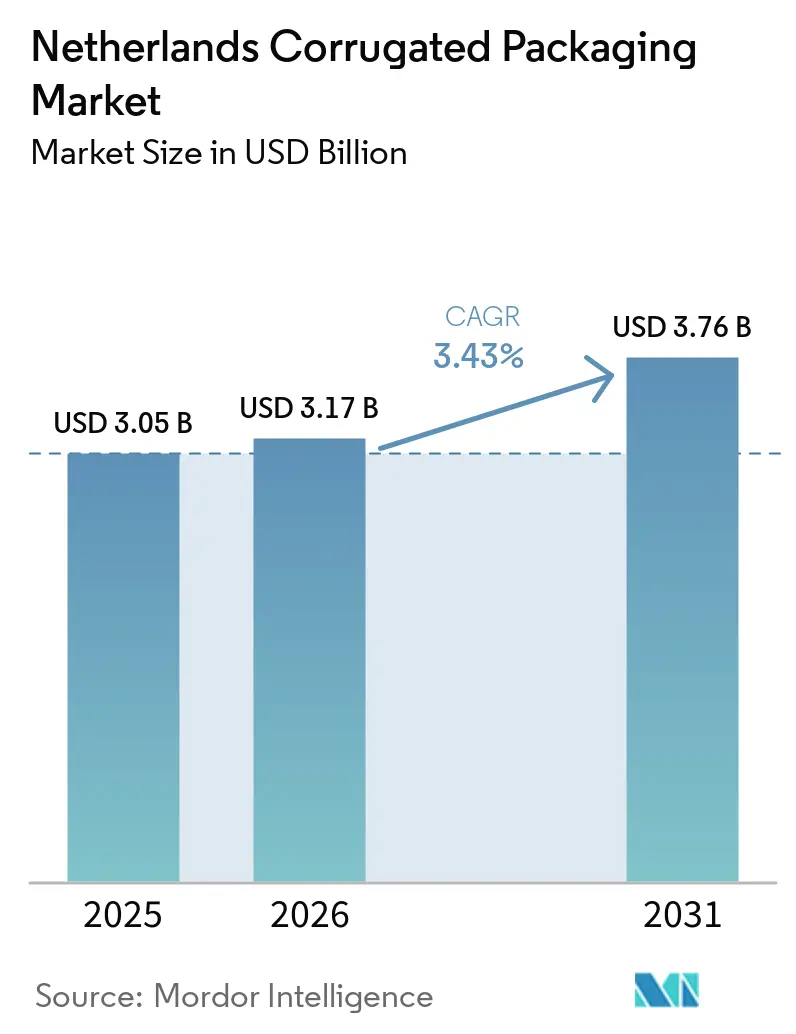

| Base Year Market Size (2025) | USD 3.05 Billion |

| Market Size (2026) | USD 3.17 Billion |

| Market Size (2031) | USD 3.76 Billion |

| Growth Rate (2026 - 2031) | 3.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Corrugated Packaging Market Analysis by Mordor Intelligence

The Netherlands corrugated packaging market size is projected to expand from USD 3.05 billion in 2025 and USD 3.17 billion in 2026 to USD 3.76 billion by 2031, registering a CAGR of 3.43% between 2026 and 2031. Steady parcel-volume gains, stronger circular-economy mandates, and targeted automation programs sustain the overall uptick, yet margin pressure from fiber and power volatility forces converters to look beyond scale toward value-added customization. E-commerce continues to anchor demand, but pharmaceutical, cosmetics, and premium fresh-produce channels are advancing faster due to stricter traceability and humidity-resilience needs. Digital inkjet presses, micro flutes, and semi-chemical mediums enable lightweight, high-graphic packs, allowing converters to capture growing small-batch orders without eroding recyclability. Meanwhile, ongoing mill conversions to recycled linerboard, combined with right-sizing investments at large fulfillment centers, accelerate the shift toward recycled fiber and on-demand box formats.

Key Report Takeaways

- By end-user, e-commerce fulfillment centers captured 26.16% of the Netherlands corrugated packaging market share in 2025.

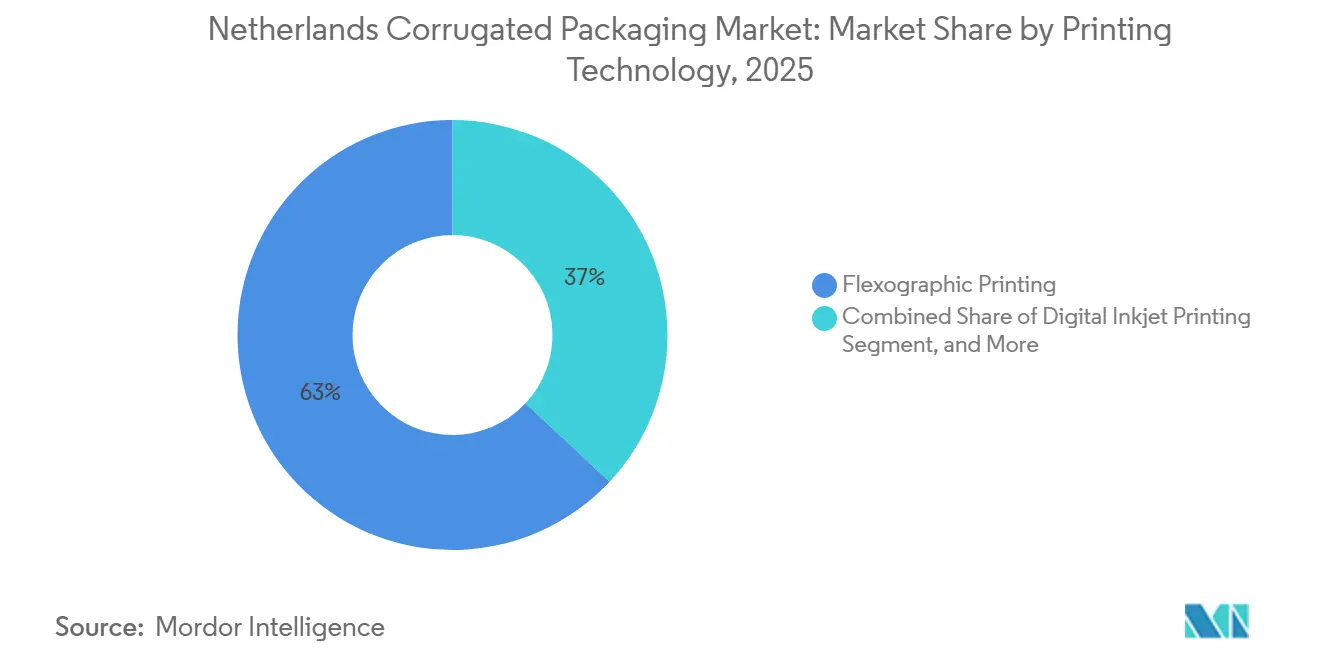

- By printing technology, the Netherlands corrugated packaging market size for the digital inkjet printing segment is forecast to advance at a 5.38% CAGR through 2031.

- By wall type, single-wall boards captured 60.70% of the Netherlands corrugated packaging market share in 2025.

- By flute, the Netherlands corrugated packaging market size for the E flute segment is forecast to advance at a 5.20% CAGR through 2031.

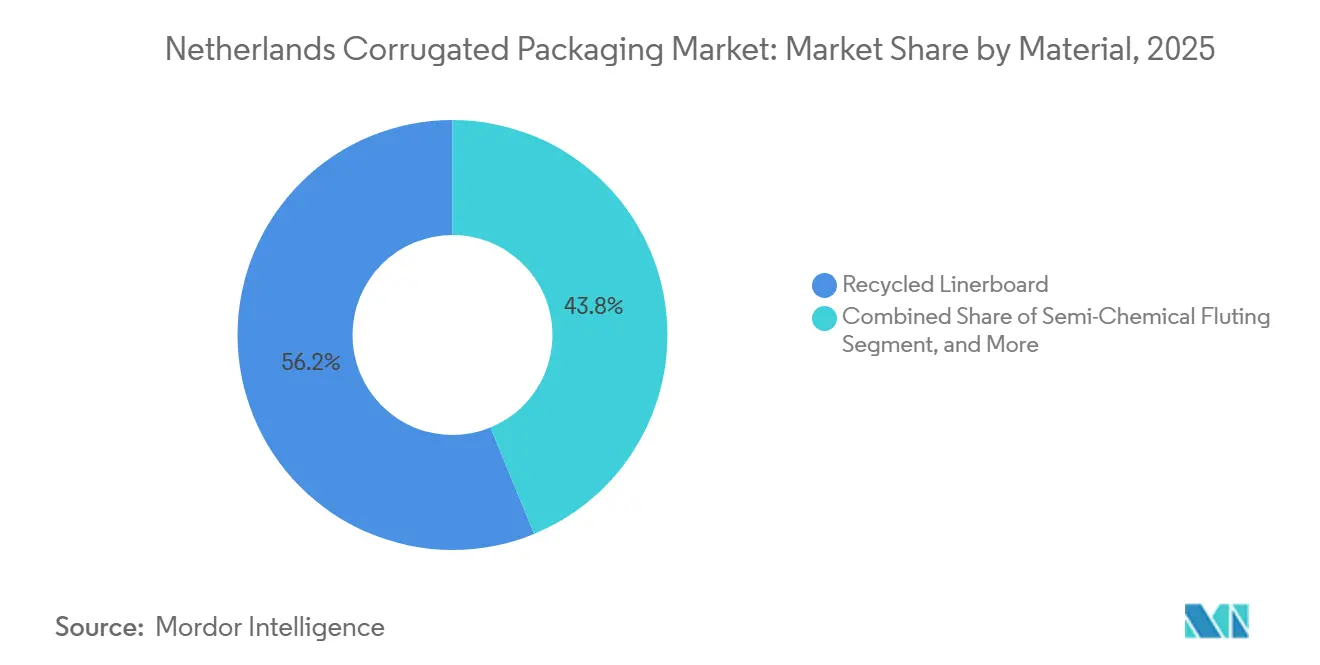

- By material, recycled linerboard captured 56.20% of the Netherlands corrugated packaging market share in 2025.

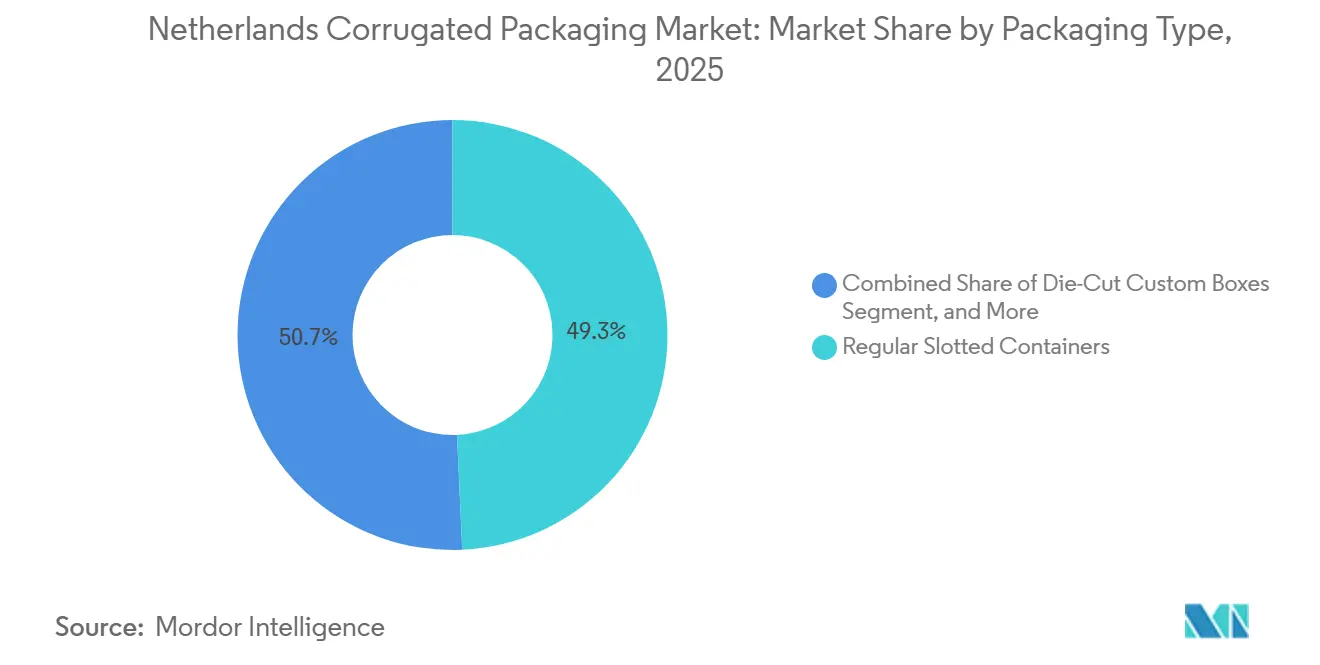

- By packaging type, the Netherlands corrugated packaging market size for the die-cut custom boxes segment is forecast to advance at a 4.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Netherlands Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in E-commerce Parcel Volumes | +1.20% | National, Randstad logistics hubs | Short term (≤ 2 years) |

| Growing Preference for Sustainable Fiber-Based Packaging | +0.90% | National, EU PPWR compliance | Medium term (2-4 years) |

| Automation Investments Among Dutch Box Plants | +0.60% | North Brabant and Gelderland | Medium term (2-4 years) |

| Premium Produce Export Requiring High-Performance Packs | +0.50% | Export corridors to Germany, UK, Scandinavia | Long term (≥ 4 years) |

| Retail Shift to Shelf-Ready Corrugated Solutions | +0.30% | National, large grocery chains | Medium term (2-4 years) |

| Government Incentives for Circular Economy Packaging | +0.20% | National, Verpact EPR | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge In E-Commerce Parcel Volumes

Parcel deliveries rose sharply, yet carriers now deploy algorithmic right-sizing that trims corrugated per parcel, pushing converters to differentiate through rapid custom print runs and low-MOQs.[1]PostNL, “Sustainability Report 2024: Parcel Delivery and Packaging Optimization,” postnl.nl Fulfillment hubs in Amsterdam, Rotterdam, and Utrecht increasingly demand four-hour replenishment windows, favoring plants with real-time scheduling systems and digital presses capable of 1,200-dpi variable graphics. EU recycled-content rules also accelerate the adoption of water-based inks, locking out solvent systems while preserving print vibrancy.

Growing Preference For Sustainable Fiber-Based Packaging

The Packaging and Packaging Waste Regulation bans non-recyclable laminates and enforces 90% collection by 2029, eliminating hybrid grades and boosting demand for FSC-certified, high-recycled boards.[2]European Commission, “Packaging and Packaging Waste Regulation,” environment.ec.europa.eu Floral exporters now require certified corrugated, spurring a double-digit hike in recycled liner orders. Semi-chemical power flute offerings offer lightweight options that meet chilled-food wet-strength metrics while satisfying new mandates.

Automation Investments Among Dutch Box Plants

New BHS corrugators and robotic folder-gluers cut changeovers to under fifteen minutes, enabling profitable 500-unit runs and lifting annual throughput per line by double digits.[3]VPK Group, “VPK Invests in New Corrugator at Erembodegem,” vpkgroup.com Automated high-bay warehouses linked to MES software synchronize reel supply, print schedules, and pallet dispatch, shrinking finished-goods inventories and freeing floor space for value-added services. Capital outlays exceeding EUR 12 million (USD 13 million) per line accelerate consolidation, trimming plant counts even as national capacity climbs. Pharmaceutical customers insist on end-to-end traceability, so ISO 9001 and GDP digital logging now represent the cost of market entry. As a result, the Netherlands corrugated packaging market rewards operators that blend high-speed hardware with data-rich process control, leaving laggard independents vulnerable to acquisition or exit.

Premium Produce Export Requiring High-Performance Packs

Dutch vegetables and cut flowers worth more than EUR 36 billion (USD 40 billion) annually ship under high-humidity, low-temperature conditions that punish conventional fluting. Semi-chemical mediums treated with bio-resins retain edge-crush resistance after extended moisture exposure, ensuring pallets survive trans-Europe and trans-Atlantic routes. Micro flute solutions lower tare weight by over one-fifth, improving air-cargo economics while meeting strict recyclability rules set by Royal FloraHolland’s Sustainable Packaging Initiative. Converters also adopt all-corrugated pallet boxes that bypass ISPM-15 wood-fumigation delays, speeding clearance at Schiphol and regional sea ports.[4]Mondi Group, “ProVantage Corrugated Solutions,” mondigroup.com These technical and regulatory pressures collectively expand the Netherlands corrugated packaging market in premium-produce corridors, creating differentiated revenue streams insulated from commodity price swings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in OCC Prices | -0.80% | National, global fiber markets | Short term (≤ 2 years) |

| Capacity Tightness in Domestic Paper Mills | -0.50% | National, integrated and merchant converters | Medium term (2-4 years) |

| Rising Energy Costs Affecting Conversion Margins | -0.40% | Gas-dependent corrugators | Short term (≤ 2 years) |

| Competition From Reusable Plastic Crates In Produce | -0.30% | Short-haul domestic distribution | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility In OCC Prices

Old corrugated container prices in Rotterdam ranged from EUR 80 (USD 90) to EUR 140 (USD 158) per tonne during 2024-2025, creating a 75% input-cost spread that treasury desks struggled to hedge effectively. Merchant converters without mill integration could not pass surcharges through to 30-day retail contracts, so EBITDA margins fell by more than 2 percentage points when prices peaked. The ripple effect amplified working-capital strains because higher inventory valuations increased credit-line utilization just as lenders tightened sustainability-linked covenants. Integrated groups softened the blow by pooling procurement across Benelux mills, yet independents accelerated consolidation talks or niche pivots toward value-added digital print jobs that consume fewer tonnes.

Capacity Tightness In Domestic Paper Mills

Dutch containerboard mills supply only three-quarters of national demand, forcing converters to import roughly 240,000 tonnes annually at spot premiums that reached EUR 50 (USD 56) per tonne in 2025. Planned Scandinavian conversions to recycled linerboard ease some pressure, but Baltic Sea shipping disruptions periodically choke supply, driving sudden lead-time extensions. The EU Emissions Trading System adds EUR 12 (USD 13) per virgin-fiber tonne, nudging kraft mills toward costly carbon-abatement investments that restrain new-build announcements. Tight capacity also lowers buyers’ leverage during annual price talks, compelling box plants to accept unfavorable indexation clauses tied to energy and freight surcharges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Dominance Masks Specialty-Grade Gains

Recycled linerboard controlled 56.20% of 2025 shipments as Verpact’s 89% collection rate guaranteed plentiful furnish and kept the Netherlands corrugated packaging market size firmly anchored in a circular model. Semi-chemical fluting posts a 5.28% CAGR because bio-resin treatments lift wet-strength metrics, letting exporters down-gauge weight without risking compression failures. Virgin kraft retains a niche for pharmaceutical and electronics packs that demand FDA-level cleanliness, yet customers increasingly specify FSC labels to burnish sustainability credentials. Small but growing micro-corrugated and solid-fiber grades answer cosmetics multipack needs, although combined share still hovers below 3%. Material choices increasingly map to end-market risk tolerance, so converters diversify furnishes to hedge against price spikes and regulation shifts.

Weight-sensitive channels such as air-freighted flowers now favor semi-chemical mediums because every kilogram saved reduces pallet fees on long-haul flights, while e-commerce hubs accept high-recycled blends that hit cost targets. The Netherlands corrugated packaging market share advantage for recycled fiber looks durable, yet specialty blends command price premiums that help offset volatile OCC costs. Integrated mills invest in adaptive furnish dosing systems to swing between recycled and semi-chemical recipes within same-day schedules. That flexibility supports just-in-time box plants supplying both budget shipping cartons and premium fresh-produce trays. Over the forecast horizon, recycled grades stay dominant, but profit pools migrate toward engineered mediums with validated humidity resistance.

By Flute Type: Micro Flutes Disrupt Folding-Carton Territory

B flute captured 44.56% of the market in 2025 because its 2.5 mm profile balances cushioning and pallet-stack density, a sweet spot for processed foods and beverages. E flute is accelerating at a 5.20% CAGR as brand managers replace folding cartons with litho-quality micro-corrugated sleeves that withstand the rigors of parcel networks without outer shippers. High-graphic cosmetics launches illustrate the trend, with converters printing 1,200-dpi imagery directly onto 1.6 mm board, avoiding litho-lam costs. A flute’s thick profile slips to a single-digit share as lighter double-wall combos match its performance at lower freight weight, satisfying retailer decarbonization scorecards. Market momentum, therefore, tilts toward thinner, high-print-fidelity profiles that integrate shelf impact and transit protection in one pass.

The Netherlands corrugated packaging market size allocated to micro flutes also increases because fulfillment centers prefer flatter cube efficiencies that slash void-fill usage and carrier surcharges. Retailers adopting shelf-ready mandates welcome micro flute trays that arrive pre-merchandised, reducing aisle restocking labor. Converters capitalize by adding precision corrugators capable of holding flute-height tolerances within ±0.05 mm to meet stringent die-cut registration windows. Price premia for E flute and F flute run EUR 0.15-0.25 (USD 0.16-0.28) per square meter, a margin that offsets smaller order volumes typical of promotional SKUs. Consequently, micro flute capability has become a strategic differentiator when tendering for personal-care or luxury beverage accounts.

By Packaging Type: Customization Premiums Erode RSC Hegemony

Regular slotted containers still accounted for 49.28% of shipment value in 2025 because automated folder-gluers can chew through standard sizes at unbeatable unit costs. However, die-cut custom boxes enjoy a 4.64% CAGR as unboxing videos shift consumer expectations toward intricate interior fits, pull tabs, and printed storytelling. Shelf-ready packaging for chains like Albert Heijn converts distribution cartons directly into display units, trimming in-store labor by double-digit minutes per pallet. Converters win such business by combining CAD-driven die libraries with fast-set folder gluers that change jobs in under 10 minutes. The pricing gap narrows because brands are willing to pay almost triple the RSC rate for enhanced shelf aesthetics and return-ready peel strips.

In the Netherlands' corrugated packaging market, display units and wraparound cases account for 18% of the market share and are growing steadily as beverage multipacks abandon plastic rings. Fanfold systems let furniture e-tailers cut inventory of long-tail SKUs by producing right-sized packs on demand, further blurring packaging-type boundaries. Pallet boxes remain a small but strategic 6% niche, favored for bulk shipments of liquids and horticulture soil where UN certifications or moisture barriers are mandatory. The diversity of pack formats obliges converters to hold wide board stocks and multi-process finishing, complicating scheduling but raising wallet share per account. Profit leadership hinges on mastering both high-speed RSC economics and premium die-cut craftsmanship.

By Wall Type: Double-Wall Gains As Lightweighting Meets Strength

Single-wall products accounted for 60.70% of volume because they satisfy most parcel weight bands and grocery resupply cycles, with basis weights below 550 gsm. Still, double-wall boards grow at 4.78% CAGR, targeting electrical goods and pharma shippers that need 1,000-newton edge-crush ratings without migrating to costly triple-wall. Semi-chemical mediums enhance ring-crush, letting converters shave 18% mass while meeting ASTM drop tests, a benefit keenly felt on long-distance cold-chain lanes. Single-face wraps for furniture decline as molded pulp end-caps win on curbside recyclability and automated insertion speed. Triple-wall lingers in heavy-machinery exports but faces substitution from engineered honeycomb cores merging with corrugated outers.

The Netherlands corrugated packaging market share evolution toward double-wall is also driven by insurers demanding higher packaging performance to honor damage-in-transit claims, an emerging compliance lever. Converters retrofit lines with dual-web splice systems that switch medium rolls without stopping, preserving throughput even on smaller specialty runs. Retailers oriented to home-delivery groceries choose double-wall cool-chain boxes lined with recyclable dispersion coatings, replacing EPS foam coolers and avoiding landfill surcharges. Although double-wall consumes more paper per square meter, lightweight flutes keep containerboard per parcel almost neutral, preventing a dramatic surge in raw materials. Profit pools, therefore, depend on balancing upgraded performance with grammage reductions that keep cost per unit contained.

By Printing Technology: Digital Inkjet Disrupts Flexo’s Volume Grip

Flexographic presses still dominated 63.04% share in 2025 because eight-color gearless lines churn out 15,000 boards per hour at ink costs below EUR 0.08 (USD 0.09) per square meter. Yet digital inkjet posts a 5.38% CAGR as fulfillment marketers demand SKU-level graphics, QR codes, and one-to-one promotions impossible on flexo without plate swaps. Inkjet reaches 1,200-dpi resolution on coated E flute in a single pass, satisfying luxury cosmetics and seasonal gift programs. Litho-lamination has been in slow retreat since digital now delivers comparable gloss and gamut without the mounting of offset sheets, trimming make-ready waste, or the lead time. UV-curable ink sets have matured to pass fiber-recycling tests, clearing an earlier environmental hurdle.

In the Netherlands, the corrugated packaging market for digital print, converters monetize faster proof-to-press cycles by bundling artwork revisions and late-stage personalization into premium service tiers. Cost curves improve as printhead warranties lengthen and duty cycles climb beyond 10 million linear meters, narrowing the capex per sheet gap with flexo. Screen and pad printing retreat to tiny niches, such as metallic spot colors, because new water-based effects mimic those finishes digitally. The competitive frontier thus becomes software, with automated RIP servers batching hundreds of SKU files into just-in-time production queues. Plants that marry high-speed inkjet with robotic finishing positions themselves for the next wave of on-demand packaging.

By End-User Industry: Pharmaceuticals Outpace E-Commerce On Serialization Mandates

E-commerce fulfillment maintained the largest share at 26.16%, but serialization and GDP rules are pushing pharma to a 4.06% CAGR, making it the standout growth engine. Tamper-evident tapes, humidity sensors, and temperature loggers integrate seamlessly into corrugated inserts, giving box plants an upsell path that offsets the costs of small lot sizes. Processed foods migrate toward shelf-ready display trays, leveraging micro flute print quality to skip outer wraps and shrink floor loading times by 22 minutes per pallet. Fresh-produce growers flirt with reusable crates, but high reverse logistics costs keep corrugated share near 16%, especially for export lanes that require phytosanitary compliance. Beverage firms are replacing plastic ring carriers with corrugated trays to meet EPR targets, boosting tray demand during stadium event seasons.

Electronics and personal-care categories, together accounting for about 16% of the market, rely on anti-static or high-graphic E flute packs that humanize unboxing while protecting against shocks. Automotive parts, textiles, and industrial chemicals make up the final 10%, with the option to use UN-certified triple-wall or coated liners when hazmat regulations require. The Netherlands' corrugated packaging market share split therefore reflects a volume-value dichotomy e-commerce drives tonnage, whereas pharmaceuticals and cosmetics deliver higher gross margins. Converters design portfolio mixes that hedge cyclical softness in parcel flows with steady regulatory-driven pharma orders. Over time, variable-data digital printing cements corrugated’s role as both transport medium and compliance documentation carrier.

Geography Analysis

The Randstad corridor, encompassing Amsterdam, Rotterdam, Utrecht, and The Hague, accounts for roughly 62% of national demand because its dense population and mega-fulfillment hubs compress delivery lead times to hours rather than days. Schiphol Airport moves more than 1.7 million tonnes of air cargo, including 420,000 tonnes of cut flowers packed in ultralight micro flutes that align with airline weight thresholds. Rotterdam’s 14.5 million TEU throughput anchors import flows of deficit testliner, yet Red Sea freight disruptions ratchet up landed costs, exposing the Netherlands' corrugated packaging market to global shipping volatility. High-recovery-rate infrastructure funded by Verpact pushes urban OCC capture above 90%, feeding city-adjacent mills and shortening inward logistics loops.

Southern provinces Noord-Brabant and Limburg host 18 box plants that capitalize on their proximity to Belgium and Germany, integrating cross-border truck lanes into synchronized delivery grids. VPK’s Erembodegem site, only 150 km from Dutch pharmaceutical clusters, ships GDP-compliant fanfold rolls overnight, underscoring how geographic proximity strengthens service-level promises. Eastern border regions Gelderland and Overijssel cater to German automotive part makers, but battle cost headwinds from cheaper Nordrhein-Westfalen corrugators powered by lower industrial gas tariffs. Rural northern provinces contribute high-humidity fresh-produce loads, demanding water-resistant semi-chemical flutes that survive cold storage and ferry crossings to Scandinavia. This regional patchwork forces converters to balance plant footprints across urban parcel density and agrarian export corridors.

Emerging micro-fulfillment nodes in Eindhoven, Groningen, and Maastricht decentralize e-commerce demand, favoring nimble plants outfitted with scheduling AI that manages small-batch cycles. Nearshoring by pharmaceutical firms to tighten GDP chains further heightens logistics sensitivity, rewarding box suppliers within a 2-hour truck radius. Local authorities integrate curbside OCC capture with digital ID tags, enhancing fiber traceability and enabling mills to receive cleaner furnish at stable prices. Over the forecast period, consistent municipal investment and intensified same-day delivery expectations will entrench Randstad’s dominance while scattering satellite bursts of demand into secondary urban rings. Such geography-linked nuances reinforce why plant location choices remain a decisive competitive lever within the Netherlands corrugated packaging market.

Competitive Landscape

The top five groups, Smurfit Westrock, International Paper, Mondi, VPK Packaging Group, and Stora Enso, collectively control about 58% of the market, giving the Netherlands corrugated packaging market a moderate concentration profile. Smurfit Westrock leverages global OCC sourcing contracts and a 500-site scale to flatten recovered-fiber volatility that smaller rivals must absorb. VPK differentiates with 12-minute order changeovers and GDP-ready micro flute lines that secure premium niches among pharmaceutical and personal care customers. Mondi’s acquisition of Schumacher added 13 micro flute plants, one in the Netherlands, enabling cross-selling of water-based barrier coatings alongside micro flute die-cuts. Stora Enso, after buying De Jong Verpakking, now sources 95% recycled fiber and is close to Randstad, amplifying service speed advantages.

International Paper’s plan to split into North American and EMEA entities clouds Benelux capacity allocations, potentially tightening supply if EMEA mills rationalize under new shareholder directives. Patent filings surge as players chase coating chemistries and high-speed digital print workflows, marking a strategic pivot from commodity board toward functional substrates with differentiated IP. Independents remain viable by specializing in fanfold right-sizing or high-graphic short runs, yet face steep automation capex to match big-player efficiencies. Strategic alliances emerge between digital-press vendors and midsize converters, bundling RIP software, service contracts, and variable-ink pricing models to shorten payback periods. Carbon-pricing exposure favors mills with cogeneration or biogas upgrades, giving integrated groups another cost shield that independents struggle to replicate.

Competitive moves increasingly weave sustainability pledges with technology upgrades. Smurfit Westrock publicly targets a 30% cut in energy intensity by 2030, aligning capex for waste-heat recovery with EU taxonomy financing benefits. VPK increases its stake in UK fanfold specialist Ribble to 50%, unlocking patented honeycomb-expansion IP and diversifying beyond conventional RSCs. Klingele installs robotics that trim setup times to 6 minutes, proving that speed and traceability win GDP bids even without integrated mills. Hinojosa’s new Alicante plant showcases a hybrid line blending a 2.5 m corrugator and an inkjet module, signaling Iberian competition on Benelux produce lanes. In sum, strategic success now hinges on blending circular-economy compliance, digital agility, and procurement muscle within a fast-narrowing field of fully compliant suppliers.

Netherlands Corrugated Packaging Industry Leaders

Smurfit Westrock plc

International Paper Company

Mondi plc

Stora Enso Oyj

VPK Packaging Group NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: International Paper committed USD 225 million to a Mississippi plant featuring a double-wall line targeting industrial and e-commerce users, with commissioning set for Q4 2027.

- January 2026: International Paper unveiled plans to separate into independent North American and EMEA companies, a transaction expected to close by Q4 2026.

- December 2025: Klingele installed an EMBA QS Ultima 215 robotic line in Wunsiedel, Germany, reducing setup to six minutes for GDP-compliant pharmaceutical runs.

- December 2025: VPK increased its stake in Ribble Packaging to 50%, securing patented honeycomb-expansion technology for protective applications.

Netherlands Corrugated Packaging Market Report Scope

The Netherlands Corrugated Packaging Market report encompasses a comprehensive analysis of fiber-based and polymer-based (PP) corrugated materials used for the containment, protection, and transport of goods across diverse industrial and retail sectors. The market refers to the industry that produces multi-layered boards, typically consisting of a fluted medium sandwiched between linerboards, designed to provide high strength-to-weight ratios and crush resistance for secondary and tertiary packaging.

The Netherlands Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current Spain corrugated packaging market size and growth outlook?

The market stood at USD 4.46 billion in 2025 and is projected to reach USD 5.59 billion by 2031, growing at a 3.75% CAGR.

Which material segment is expanding fastest within Spain's corrugated sector?

Virgin kraft linerboard is forecast to post the quickest rise at a 4.64% CAGR through 2031, driven by moisture-sensitive fresh-food exports.

How are EU recyclability regulations influencing packaging choices in Spain?

Rules that tax non-recycled plastics and mandate design-for-recycling are steering brand owners toward lightweight, fully recyclable corrugated formats.

Why is digital inkjet printing gaining ground among Spanish converters?

Digital presses eliminate plate costs and allow variable data, enabling economical runs under 5,000 units that private-label and e-commerce customers demand.

Which end-user is set to record the highest growth in corrugated consumption?

E-commerce fulfillment centers are expected to expand at a 5.91% CAGR as online retail penetrates deeper into Spanish consumer spending.

How fragmented is Spain's corrugated packaging competitive landscape?

The top five firms hold 52% of capacity, giving the market a mid-level concentration that still allows numerous regional specialists to thrive.

Page last updated on: