Kenya Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

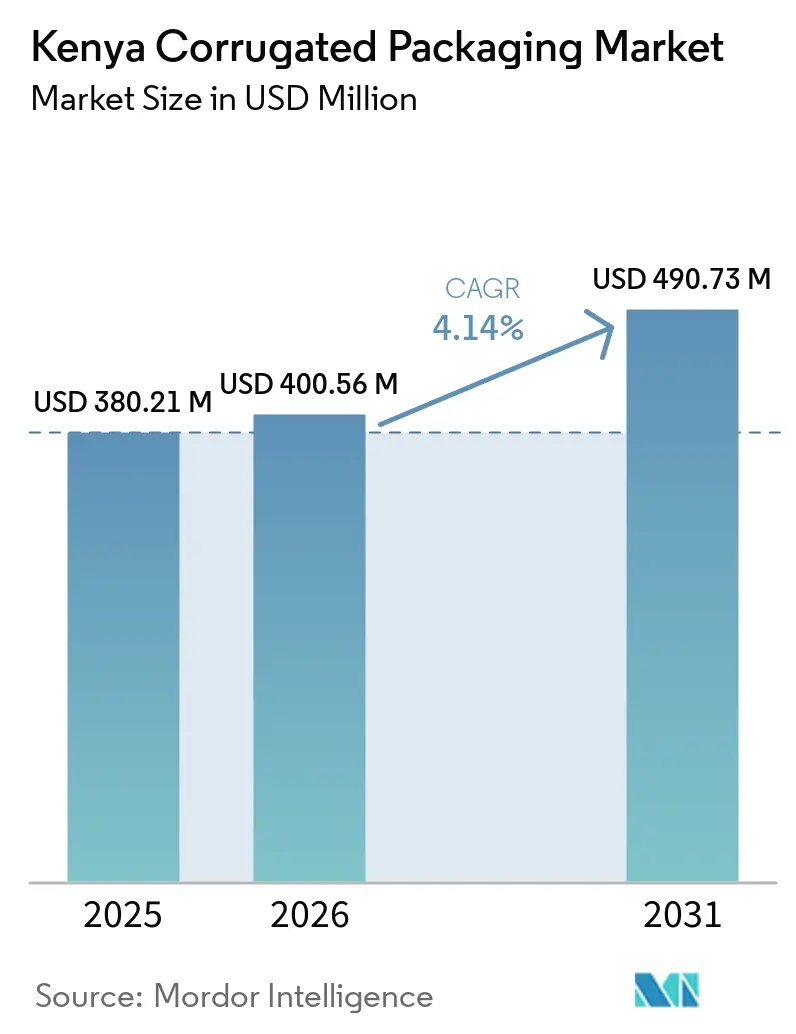

| Base Year Market Size (2025) | USD 380.21 Million |

| Market Size (2026) | USD 400.56 Million |

| Market Size (2031) | USD 490.73 Million |

| Growth Rate (2026 - 2031) | 4.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kenya Corrugated Packaging Market Analysis by Mordor Intelligence

The Kenya Corrugated Packaging Market size was valued at USD 380.21 million in 2025 and is estimated to grow from USD 400.56 million in 2026 to reach USD 490.73 million by 2031, at a CAGR of 4.14% during the forecast period (2026-2031). E-commerce expansion, supermarket proliferation, and government restrictions on single-use plastics are lifting demand even as volatile kraft pulp costs and elevated electricity tariffs narrow converters’ margins. Brand owners are shifting toward lighter flute profiles and high-graphics shelf-ready formats to reduce freight charges and win visibility on modern retail shelves. Meanwhile, food-export certification requirements are channeling spend into moisture-resistant, high-compression board grades, especially among horticulture exporters shipping through Mombasa.

Key Report Takeaways

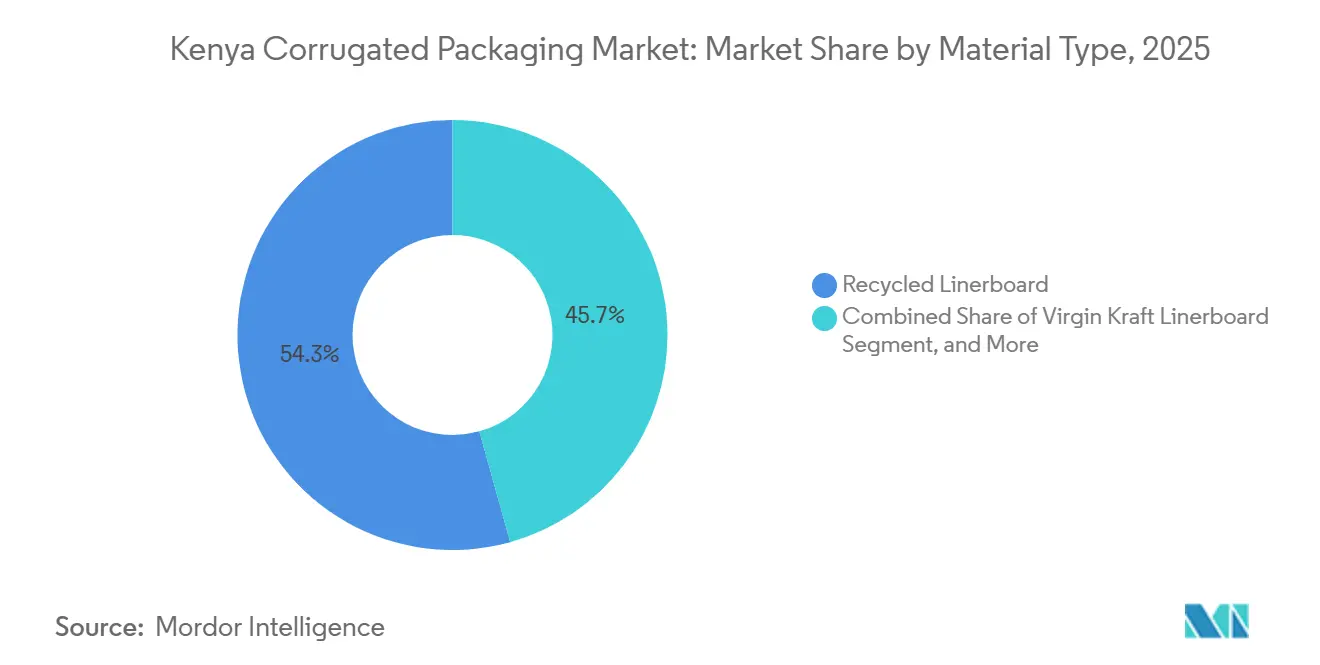

- By material type, the recycled linerboard segment captured 54.32% of the Kenya corrugated packaging market share in 2025.

- By flute type, the Kenya corrugated packaging market size for e flute is projected to grow at an 5.13% CAGR through 2031.

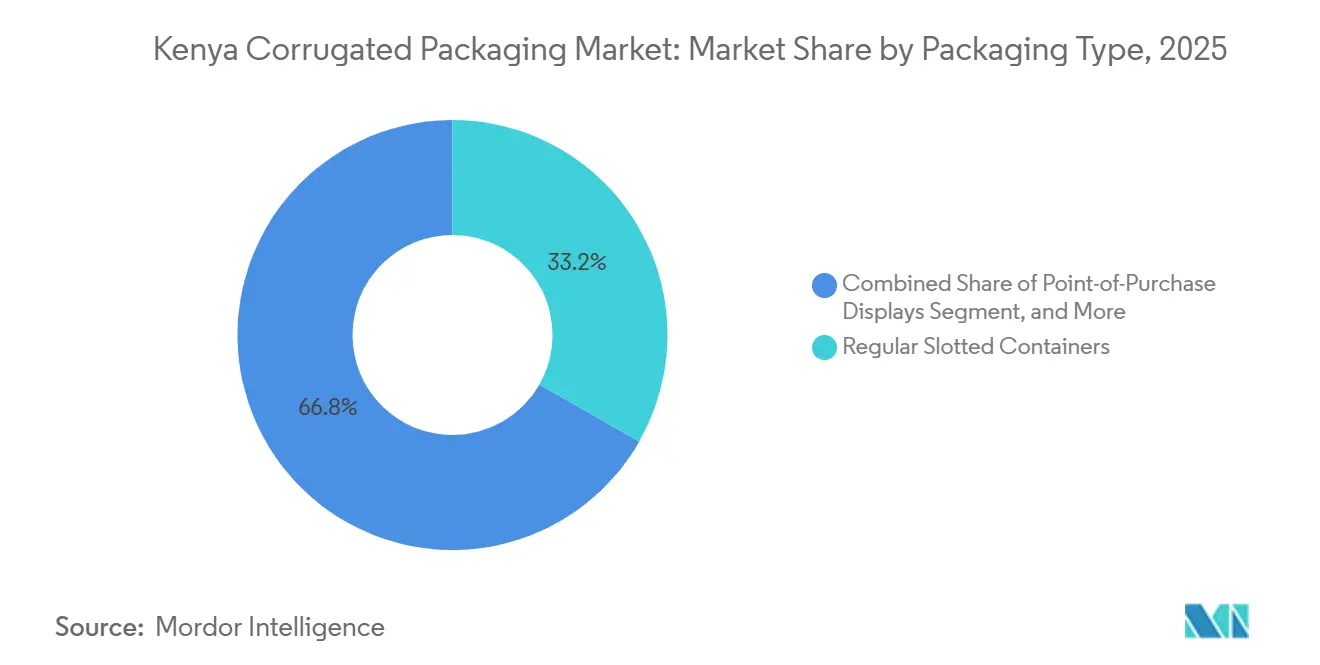

- By packaging type, the regular slotted containers segment captured 33.24% of the Kenya corrugated packaging market share in 2025.

- By wall type, the Kenya corrugated packaging market size for triple-wall is projected to grow at an 5.44% CAGR through 2031.

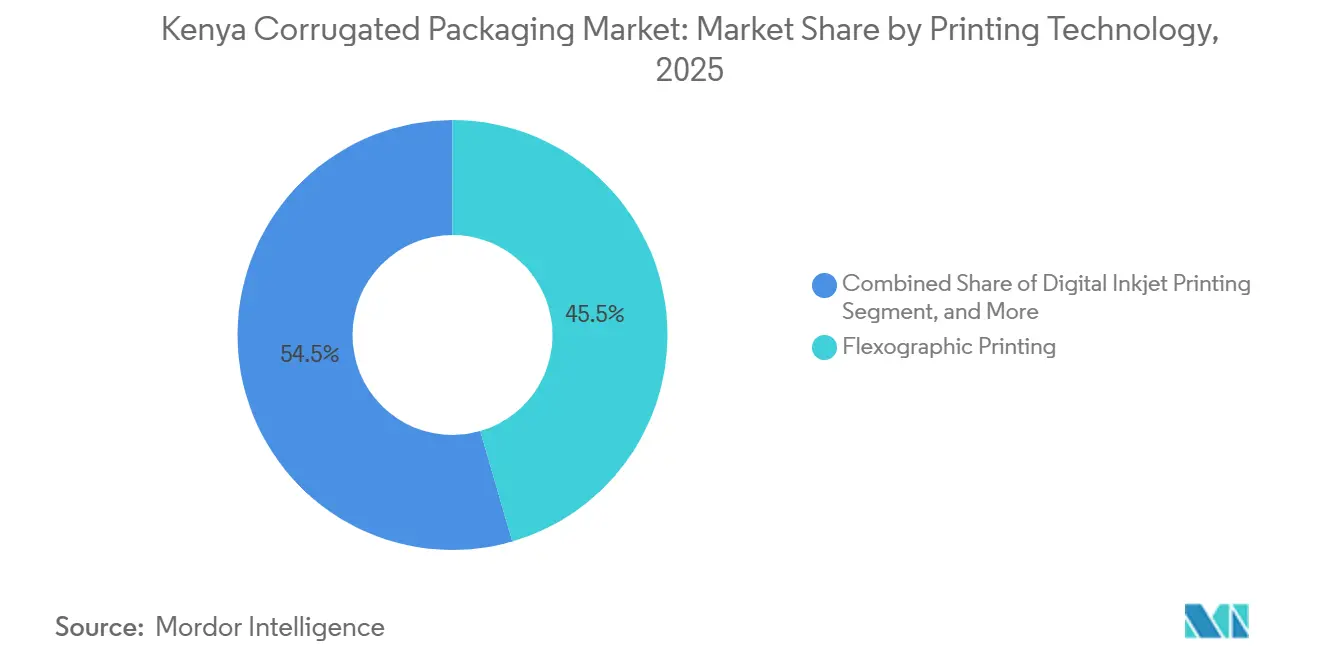

- By printing technology, the flexographic printing segment captured 45.52% of the Kenya corrugated packaging market share in 2025.

- By end-user industry, the Kenya corrugated packaging market size for e-commerce fulfillment centers is projected to grow at an 5.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Kenya Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding E-commerce Logistics Footprint | +0.9% | National, Nairobi and Mombasa corridors | Medium term (2-4 years) |

| Rising Demand for Shelf-Ready Retail Packaging | +0.7% | National, Nairobi-Nakuru-Eldoret supermarket clusters | Short term (≤ 2 years) |

| Government Ban on Single-Use Plastics | +0.6% | National, enforced by NEMA across all counties | Long term (≥ 4 years) |

| Entry of Regional Food Exporters | +0.5% | Export-oriented zones, Mombasa and Nairobi EPZ | Medium term (2-4 years) |

| Technological Upgrades in Flexo Presses | +0.4% | Nairobi and Mombasa converter hubs | Medium term (2-4 years) |

| Mainstream Brands’ Sustainability Commitments | +0.3% | National FMCG and beverage supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding E-Commerce Logistics Footprint

Jumia Kenya’s integrated 11,000 m² warehouse has consolidated inventory, reduced first-mile mileage, and expanded next-day delivery coverage across Nairobi, thereby increasing the number of inner cartons, outer shippers, and void-fill items packed per order.[1]Jumia Group, “Jumia Opens Integrated Warehouse Facility To Reduce Delivery Time,” group.jumia.com E-commerce parcel counts are further amplified by the ubiquity of mobile money and 80% smartphone penetration, both highlighted in Maersk’s 2026 regional supply-chain review. Fulfillment centers increasingly specify smaller die-cut boxes compatible with automated sorters to reduce cubic-weight charges. Green-certified warehouses now exceed 80% occupancy, and many tenants require documentation of recycled-fiber content, forcing converters to enhance the traceability of recovered paper inputs. Combined, faster order cycles, higher shipment fragmentation, and ESG screening are accelerating demand for value-added corrugated formats within the Kenya corrugated packaging market.

Rising Demand for Shelf-Ready Retail Packaging

Supermarket leaders Naivas and Quick Mart opened more than 100 outlets in 2024, intensifying shelf competition and nudging suppliers toward perforated tear-strip cartons that double as display trays. Packaged-food retail sales are forecast to jump 32.2% between 2023 and 2028, heightening the need for high-graphics cases that minimize shelf-restocking labor. Nestlé’s 2025 rulebook now requires 95% area utilization and 90% pallet cube efficiency, penalizing suppliers with oversized cases. Local converter Carton Manufacturers Ltd offers short-run die-cut products with 500-unit minimums, lowering entry barriers for smaller brands. These dynamics channel growth toward shelf-ready solutions within the Kenya corrugated packaging market.

Government Ban on Single-Use Plastics Boosting Paper-Based Alternatives

Legal Notice 181 of 2024 obliges plastic-bag producers to obtain NEMA licenses, include 30% recycled content, and finance take-back schemes, with fines of up to KES 4 million (USD 27,000) or a four-year jail term for violators. NEMA’s 2025 nationwide raids led to multiple arrests, reinforcing compliance pressure. Retailers are therefore migrating toward corrugated trays and kraft wraps that avoid licensing fees altogether. Although porous borders still enable some illegal plastic inflows, the regulatory direction keeps corrugated demand on an upward trajectory across Kenya’s counties.

Entry of Regional Food Exporters Seeking Certified Corrugated Solutions

Kenya’s flower exports exceeded USD 800 million in 2023 and rely on telescopic boxes that maintain dimensional integrity under cold-chain humidity conditions. Buyers increasingly mandate FSSC 22000 or BRCGS certification, steering business to converters such as Allpack Industries that maintain audit-ready quality systems. A similar certification pull is emerging from fish, sugar, and meat processors, whose 2024 output grew between 6% and 16% year on year. Compliance premiums lift ASPs and deepen semi-chemical fluting penetration in the Kenya corrugated packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Global Kraft Pulp Prices | -0.5% | Import-dependent converters in Nairobi and Mombasa | Short term (≤ 2 years) |

| Chronic Electricity Outages | -0.7% | National, severe in peri-urban industrial zones | Medium term (2-4 years) |

| Limited Local Recovery of High-Quality OCC | -0.3% | Counties lacking organized waste collection | Long term (≥ 4 years) |

| Competition From Lightweight Plastic Crates | -0.2% | Horticulture and fresh-produce value chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Global Kraft Pulp Prices Impacting Margins

Kenyan converters import most virgin linerboard, leaving them exposed to currency swings and international pulp cycles that can move spot costs by double digits within one quarter. East African Packaging Industries sources 75% of its raw material offshore, magnifying forex risk. Without hedging tools, manufacturers hold larger working-capital buffers that raise financing costs, especially when informal retailers resist price increases. The mismatch compresses margins across the Kenya corrugated packaging market.

Chronic Electricity Outages Elevating Operating Costs

Industrial power in Kenya averaged USD 0.185 per kWh in 2025, far above peers such as Ethiopia at USD 0.01 per kWh, eroding competitiveness for energy-intensive corrugators. Transmission upgrades are behind schedule, and peri-urban plants frequently switch to diesel generators that add KES 5-8 per kWh (USD 0.03-0.05 per kWh) to effective tariffs. Each outage disrupts adhesive curing and flexo drying, causing spoilage and overtime costs. High energy overheads, therefore, temper investment in new capacity within the Kenya corrugated packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Fiber Dominates Cost-Sensitive Supply Chains

Recycled linerboard controlled 54.32% of Kenya's corrugated packaging market share in 2025, reflecting converters’ push to offset imported kraft exposure and comply with extended producer responsibility rules. Waste-paper aggregators such as Kamongo process over 100 tons daily, anchoring a domestic feedstock network that keeps unit costs predictable. Virgin Kraft linerboard remains essential for export-grade food-contact cases, but its landed cost above USD 130 per ton restricts its application to niche segments. Semi-chemical fluting is predicted to grow at 5.21% CAGR, buoyed by horticulture exporters seeking moisture-resistant, high-compression board grades.

The Kenya corrugated packaging market size for semi-chemical fluting is poised to expand as converters trial powerflute and aquaflute grades that meet cold-chain requirements without wax coatings. Chandaria Industries’ USD 38.5 million tissue mill will absorb more local OCC, potentially tightening supply for independent box plants. While wax-coated and specialty grades serve as flower wraps and furniture protectants, they remain niche. Overall, material choice is diverging between low-cost recycled inputs for domestic distribution and premium virgin or semi-chemical options for export markets, where export specifications command higher margins.

By Flute Type: Lightweight Profiles Capture Logistics Efficiencies

B flute led 2025 shipments with 43.71% market share in Kenya's corrugated packaging market, balancing stacking strength and print quality for processed-food multipacks and beverage trays. E flute, however, is forecast to clock a 5.13% CAGR through 2031 as electronics assemblers, cosmetics brands, and e-commerce retailers specify thinner profiles to cut dimensional weight. A flute sustains demand in industrial chemicals and cement, but its bulk limits use where freight costs are critical. C flute sits between these extremes yet lacks a clear performance edge, restraining its growth.

The Kenya corrugated packaging market size advantage of E flute lies in its ability to deliver high-resolution graphics on a leaner substrate, something retailers prize for shelf-ready packs. Converters upgrading corrugators to finer-tip knives and tighter tension controls can transition to micro-flutes without major line overhauls. Still, capital scarcity slows equipment refresh outside Nairobi. Until wider access to precision corrugators materializes, B flute will retain dominance, while E flute captures incremental high-value volumes.

By Packaging Type: Custom Die-Cut Formats Accelerate Retail Differentiation

Regular slotted containers accounted for 33.24% of 2025 volume, due to their low unit cost and compatibility with automated case erectors, yet die-cut custom boxes are forecast to rise 5.57% per year, driven by modern trade expansion and brand needs for point-of-purchase impact. Shelf-ready trays with tear-away fronts reduce in-store handling and elevate visibility, prompting FMCG firms to re-allocate budgets toward premium converting features.

The Kenya corrugated packaging market for die-cut boxes benefits from minimum order quantities as low as 500 units, enabling smaller bakeries and snack makers to test retail-ready concepts without incurring heavy tooling costs. Folding cartons serve the pharmaceutical and cosmetic industries, buoyed by sustainability rules that require recyclability and ban PFAS coatings. Pallet boxes hold a share of the cement and sugar markets, yet face plastic-crate competition in fresh produce. Packaging-type selection is cleaving between economy RSCs for bulk flows and premium die-cuts for brand-led retail channels.

By Wall Type: Triple-Wall Formats Secure Heavy-Duty Export Loads

Single-wall cases accounted for 61.97% of 2025 shipments, reflecting their cost advantage for light- and medium-duty products moving through domestic retail and e-commerce. Triple-wall boxes, however, are projected to log a 5.44% CAGR as cement, industrial-chemical, and machinery exporters demand containers that survive rough road and sea transits to key AfCFTA partners. Double-wall grades sit between the two extremes, protecting bulk food ingredients and consumer durables where higher edge-crush values justify the modest material premium. Single-face wraps remain niche, serving primarily for furniture and flower protection, but demonstrate the breadth of corrugated options in the Kenya corrugated packaging market.

Second paragraph. The Kenya corrugated packaging market growth in triple-wall packaging stems from the adoption of heavier pallet loads exceeding 1,000 kg, which require burst strengths well above 1,300 kPa. East African Packaging Industries has redesigned its Athi River line to run triple-wall board at 250 m min-¹, cutting changeover time and enabling smaller batch runs for cement clients that mix pallet box and paper sack orders on the same truck. Independent converters weigh similar upgrades yet face financing constraints because high industrial power tariffs lengthen payback cycles. Until grid reliability lifts, single-wall will stay volume leader, while triple-wall captures premium export lanes.

By Printing Technology: Digital Inkjet Unlocks Short-Run Agility

Flexographic presses held a 45.52% share in 2025, favored for medium- and long-run jobs on B and C flute formats that dominate staple foods and beverages. Digital inkjet units, though, are forecast to rise 5.58% per year as online sellers request variable-data graphics, QR codes for traceability, and rapid color changes that sidestep plate fees. Litho-lamination keeps a foothold in luxury cosmetics and spirits, yet is hampered by limited local laminators. Screen printing fills specialty tactile-effect orders, but its slow throughput restricts scale.

The Kenya corrugated packaging market size for digital inkjet remains small, yet Platinum Packaging’s 2024 commissioning of two BOBST MASTER M6 lines with one ECG automation slashed setup waste below 30 m and cut job switchover to under five minutes, proving the model’s economics. Flexoworld Ltd now supplies flat-top-dot plates and Esko HD files, enabling converters to run hybrid flexo-digital workflows without full equipment replacements.[2]Flexoworld Ltd, “Our Products,” flexoworld.co.ke Adoption is fastest in Nairobi, where brand owners demand same-day mock-ups, while plants in Eldoret and Kisumu await cheaper printheads and lower power bills before signing lease-purchase agreements.

By End-User Industry: Fulfillment Centers Drive Incremental Volume Growth

Processed foods retained the largest 38.13% share of 2025 sales, underpinned by USD 5.1 billion in packaged-food turnover, which is tracking toward USD 7.3 billion by 2028. E-commerce fulfillment centers are expected to post the strongest CAGR of 5.49%, buoyed by Jumia Kenya’s warehouse consolidation and the spread of mobile-money checkout, which lifts order frequency. Fresh-produce exporters continue specifying telescopic cases with water-resistant semi-chemical fluting, while domestic growers test reusable plastic totes to trim per-trip costs.

The Kenya corrugated packaging market for beverages is growing on the back of multipack promotions from soda and bottled-water brands that value B flute’s stacking strength. Personal care and cosmetics lines favor E flute die-cuts with litho-laminated sleeves to project premium shelf appeal. Electronics assemblers choose thin flutes and engineered inserts to combat vibration during inland transport between Mombasa port and Nairobi’s industrial parks. Pharmaceutical orders remain modest but attract converters with FSSC 22000 certification, unlocking higher unit margins.

Geography Analysis

Nairobi and the Mombasa corridor account for the bulk of Kenya's corrugated packaging market demand, due to their dense clusters of FMCG plants, converter workshops, and logistics hubs such as Athi River and Tatu Industrial Park. The Standard Gauge Railway shortens linerboard hauls from port to inland mills, trimming dwell time and reducing moisture pickup that can weaken edge-crush values en route. Green-certified warehouse space in greater Nairobi topped 80% occupancy in Q1 2026, a marker of multinational buyers that favor traceable recycled content in secondary packaging. High urban consumption and modern retail penetration sustain a steady pull for single-wall RSCs and an emerging appetite for shelf-ready die-cuts.

Coastal Mombasa anchors import flows of virgin kraft pulp and semi-chemical fluting, and also houses East African Packaging Industries’ sack plant, which feeds cement and tea exporters. Landing costs for imported OCC exceed, so box makers located near the port gain a thin freight edge over up-country rivals.[3]PaperIndex, “OCC 11 Waste Paper Dealers,” paperindex.com Nonetheless, grid instability in Mombasa’s peripheral industrial parks prompts frequent diesel-generator use, inflating unit costs and pressuring margins. Converters offset some of this burden by backhauling finished cartons on trucks returning to the inland route, thereby maximizing payload efficiency.

Third paragraph. Secondary hubs including Nakuru, Eldoret, Kisumu and Thika are rising on supermarket build-outs, agro-processing zones and dairy clusters. Limited recovery of high-grade OCC in these counties curbs recycled linerboard quality, driving periodic imports from Uganda and Tanzania. Electricity supply outside Nairobi central remains erratic, lengthening ROI on new corrugators and stunting technology upgrades that would widen product choice. Even so, AfCFTA tariff reductions promise fresh export routes for Kenyan converters to Uganda, Rwanda and Burundi, provided that electricity tariffs can be trimmed below the current USD 0.185 kWh⁻¹ level that undercuts regional price competitiveness.

Competitive Landscape

The market exhibits moderate concentration, with East African Packaging Industries holding roughly 25% share after Canadian Overseas Packaging Industries clinched a full buyout in 2024, positioning the group to seed capacity in Ethiopia and hedge against Kenyan power costs. Chandaria Industries, East and Central Africa’s largest tissue maker, is injecting KES 5 billion (USD 38.5 million) into a new waste-paper-fed tissue mill at Tatu City that may later house corrugating assets, tightening OCC availability for independents.[4]Tatu City, “Chandaria Industries to Build Tissue Facility,” tatucity.com Allpack Industries competes on FSSC 22000 and ISO 22000 certifications, aiming at food export accounts that require rigorous traceability.

Technology adoption creates a two-speed field: Platinum Packaging’s DigiFlexo lines handle five-color jobs with sub-30 m setup waste, while older plants still run three-color stack flexos that need 300 m of startup board per shift. Converters able to finance servo-driven corrugators and laser-ruled rotary die-cutters win shelf-ready contracts from multinational brand owners enforcing 95% area-utilization rules. Smaller firms lean on rapid quoting, localized service, and low overheads to keep informal retailers supplied with economy RSCs.

Upstream, waste-paper aggregators such as Kamongo and Nopaltech exert growing influence by controlling rural OCC flows and floating build-own-operate proposals for micro-mills that would secure fiber and forward-integrate into box making. Downstream, supermarket chains standardize pallet footprints and shelf facings, encouraging suppliers to converge on die-cut case formats that optimize cube efficiency. Competitive intensity is therefore shaped by vertical integration moves, access to certified recycled fiber, and the ability to finance energy-efficient machinery that blunts Kenya’s high tariff environment.

Kenya Corrugated Packaging Industry Leaders

East African Packaging Industries Ltd.

Dodhia Packaging Ltd.

Tetra Pak East Africa Ltd

ASL Packaging Limited

Shri Krishana Overseas plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Propak East Africa 2026 drew more than 5,000 attendees and spotlighted sustainable packaging, with the trade ministry urging exporters to adopt world-class corrugated systems.

- March 2026: Chandaria Industries confirmed a KES 5 billion (USD 38.5 million) tissue plant at Tatu City that will recycle over 100 tons day⁻¹ of wastepaper and employ 1,000 workers.

- February 2026: ROTOCON announced turnkey label and flexible-packaging lines for East African converters, featuring Pantec RHINO embellishment for premium corrugated graphics.

- January 2025: Nestlé issued updated Rules of Packaging Sustainability that require 95% area utilization and ban PFAS coatings in corrugated secondary cases.

Kenya Corrugated Packaging Market Report Scope

The Kenya Corrugated Packaging Market report provides a comprehensive analysis of the market, focusing on trends, growth drivers, challenges, and opportunities. Corrugated packaging refers to packaging solutions made from corrugated fiberboard, which is widely used for shipping, storage, and product protection across various industries. The study covers market dynamics, competitive landscape, and key developments, offering insights into the current market scenario and future growth prospects.

The Kenya Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material Type | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Kenya corrugated packaging market?

The market is valued at USD 400.56 million in 2026 and is forecast to reach USD 490.73 million by 2031, reflecting a 4.14% CAGR.

Which material dominates corrugated production in Kenya?

Recycled linerboard holds 54.32% share, helped by abundant local waste-paper recovery and extended producer responsibility rules.

Why are digital inkjet presses gaining popularity among Kenyan converters?

E-commerce sellers request short runs with variable data and brand personalization, and inkjet eliminates plate costs while cutting setup waste below 30 m.

How are high electricity tariffs affecting box makers?

Average industrial power costs of USD 0.185 kWh⁻¹ narrow margins and delay investment in new corrugators, especially outside Nairobi.

What certifications are exporters demanding for corrugated packaging?

Buyers increasingly insist on FSSC 22000 or BRCGS Packaging Materials audits to ensure food-contact safety and supply-chain traceability.

Which corrugated segment is growing fastest?

E-commerce fulfillment centers are projected to expand at a 5.49% CAGR through 2031 as order volumes and packaging intensity rise.

Page last updated on: