Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

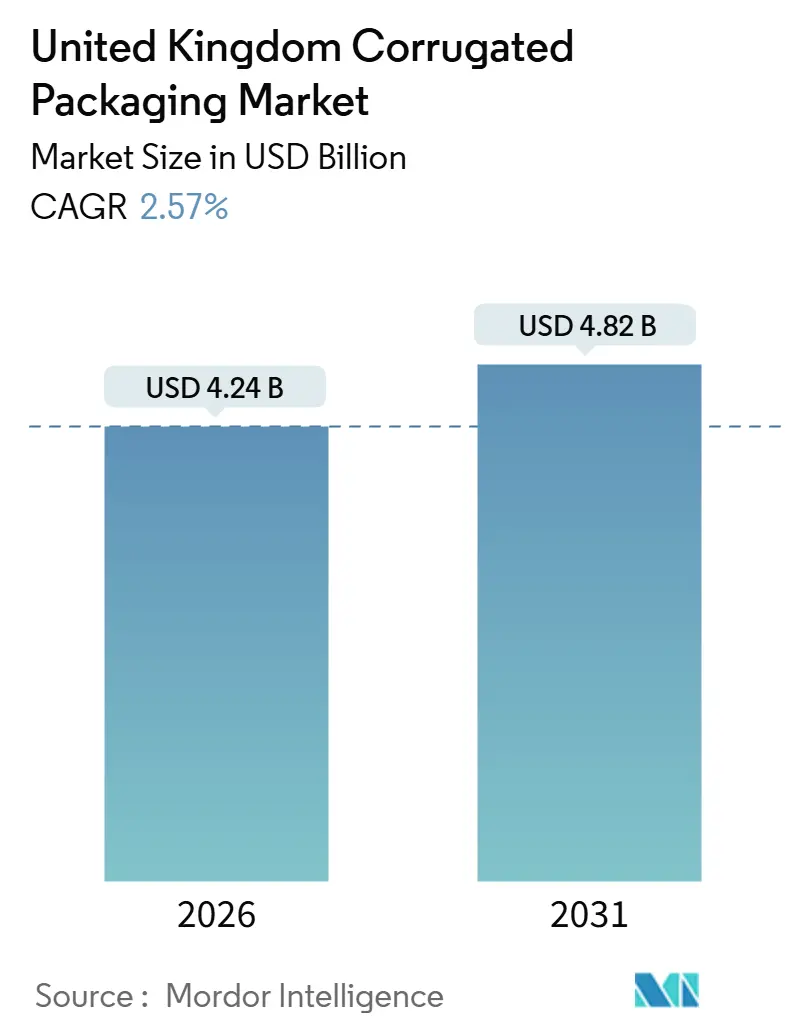

| Market Size (2026) | USD 4.24 Billion |

| Market Size (2031) | USD 4.82 Billion |

| Growth Rate (2026 - 2031) | 2.57% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Corrugated Packaging Market Analysis by Mordor Intelligence

The United Kingdom corrugated packaging market size stands at USD 4.24 billion in 2026 and is expected to reach USD 4.82 billion by 2031, reflecting a 2.57% CAGR over the forecast period. This moderate pace signals a mature landscape where e-commerce parcel growth and plastic-reduction policies outweigh margin pressure from volatile recovered-fiber prices and elevated electricity tariffs. The Plastic Packaging Tax, now GBP 210.82 (USD 267.7) per tonne, continues to redirect capital toward corrugated lines, while Extended Producer Responsibility fees of GBP 196 (USD 248.9) per tonne for paper and card motivate converters to lightweight board grades, curb logistics emissions and stretch pulp yields. Old corrugated container prices remain unpredictable, and fourth-quarter 2024 electricity costs averaged 25.97 pence (USD 0.33) per kilowatt-hour, squeezing corrugator margins. Nevertheless, sustained demand from food, beverage and direct-to-consumer brands supports steady volume gains, and investments in digital inkjet equipment accelerate short-run graphics for personalized packs.

Key Report Takeaways

- By product type, slotted boxes led with 42.43% revenue share in 2025, whereas trays, folders and sheets are forecast to expand at a 3.66% CAGR through 2031.

- By board type, single-wall constructions captured 38.32% of the United Kingdom corrugated packaging market share in 2025, while triple-wall formats are projected to grow at a 4.32% CAGR.

- By flute profile, C-flute retained 32.54% share in 2025 and F-flute is set to climb at a 4.65% CAGR to 2031.

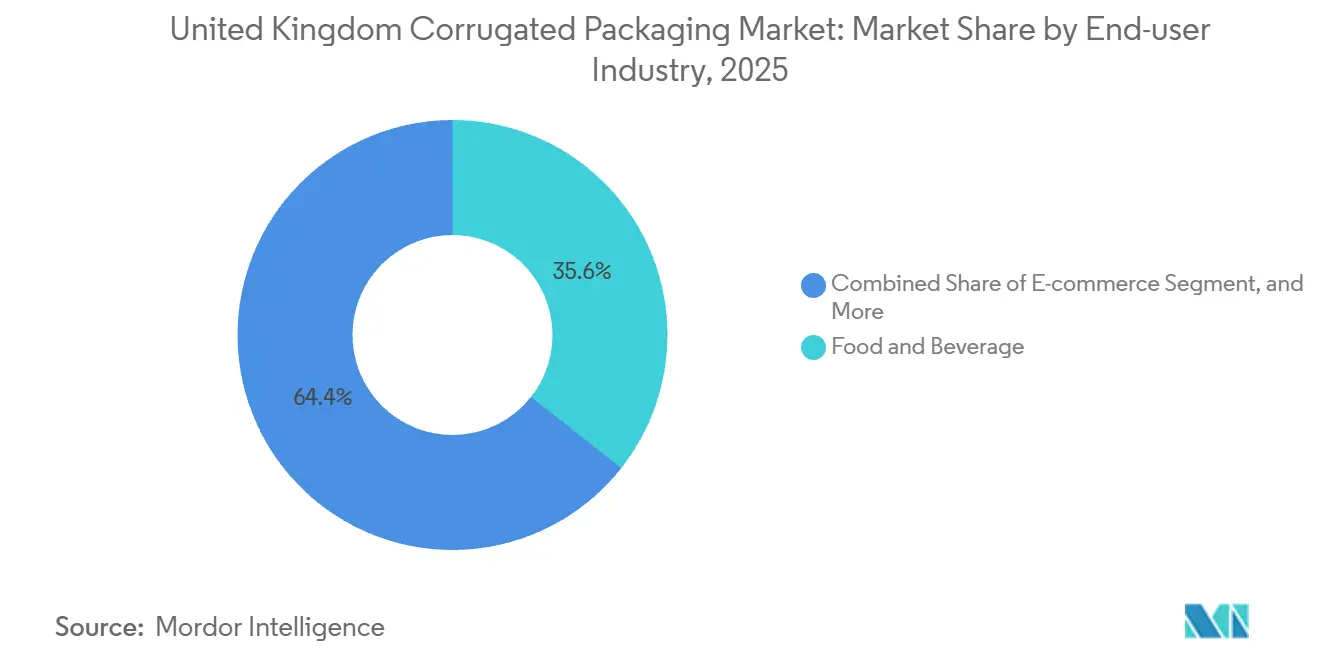

- By end-user industry, food and beverage accounted for 35.63% of the United Kingdom corrugated packaging market size in 2025, whereas e-commerce is advancing at a 4.73% CAGR.

- By print technology, flexography held 28.54% share in 2025, yet digital printing is climbing at a 3.54% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce parcel volumes | +0.6% | National, concentrated in London, Manchester, Birmingham hubs | Short term (≤ 2 years) |

| Preference for recyclable fiber-based packs | +0.5% | National, strongest in England under Simpler Recycling mandates | Medium term (2-4 years) |

| Lightweighting initiatives | +0.3% | National, led by food and beverage chains targeting Scope 3 cuts | Medium term (2-4 years) |

| Rising demand from processed food brands | +0.4% | National, clustered in East Midlands and Yorkshire | Long term (≥ 4 years) |

| Expansion of shelf-ready formats | +0.2% | National, led by leading supermarket groups | Medium term (2-4 years) |

| Plastic Packaging Tax impact | +0.3% | National, affecting producers above 10 tonnes annual throughput | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in E-Commerce Parcel Volumes

Online retail penetration touched 27.8% of total U.K. sales in 2024, stimulating demand for lightweight B- and F-flute mailers that withstand automated sortation forces while minimizing dimensional-weight charges.[1]About Amazon, “Ships in Own Container program,” aboutamazon.com Brand participation in “Ships in Own Container” programs expands the addressable pool for frustration-free slotted boxes, supporting incremental adoption of digital printing for variable data and QR codes.

Preference for Recyclable Fiber-Based Packaging

The Separation of Waste Regulations 2024 mandates dedicated paper and card collection for most businesses by March 2025, lifting bale purity and boosting recovered-fiber prices by roughly 8-12%.[2]UK Statutory Instruments 2024 No. 666, “The Separation of Waste Regulations 2024,” legislation.gov.uk Extended Producer Responsibility fees establish a cost gradient that favors mono-material designs, encouraging brands to substitute plastic trays with corrugated equivalents.

Lightweighting Initiatives

Converters lowered average basis weight by 6-9% from 2021 to 2025 using high-performance liners and micro-flute profiles, cutting shipment carbon footprints by 0.15-0.22 kg of CO₂e while maintaining burst strength above 1,100 kPa.[3]European Federation of Corrugated Board Manufacturers, “Lifecycle Assessment Data,” fefco.org Upgrades at Board24 increased run speed and reduced waste, proving that productivity and sustainability gains can coincide.

Rising Demand from Processed Food Brands

Extended Producer Responsibility costs of GBP 1.1 billion (USD 1.40 billion) in 2025 pushed food manufacturers to rationalize packaging formats and switch to shelf-ready corrugated trays that shorten shelf-stocking time by 15-20%. Major retailers target 100% recyclable own-brand packaging, reinforcing corrugated’s volume base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in recovered paper prices | -0.4% | National, acute where imported fiber is prominent | Short term (≤ 2 years) |

| Substitution threat from flexible plastics | -0.3% | National, notably in cosmetics, electronics and pharma blister packs | Medium term (2-4 years) |

| Urban curbside collection limits | -0.2% | England, especially London, Essex, Cambridgeshire | Medium term (2-4 years) |

| Energy-price fluctuations | -0.2% | National, burdening energy-intensive corrugators | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Recovered Paper Prices and Supply

Household paper collection fell 3.3% year on year to 1.894 million t in 2023, compressing raw-material availability even as recycling rates reached 74.3%. Packaging Recovery Note prices dropped below GBP 5 per tonne in early 2025, undermining the incentive for local authorities to segregate OCC and forcing converters to hedge pulp inputs.

Substitution Threat from Flexible Plastics

Moisture-sensitive cosmetics and electronics accessories still favor polyethylene pouches that meet tight barrier and drop-test demands at a lower weight. A 120-g corrugated mailer costs roughly GBP 0.025 (USD 0.032) in board alone, versus GBP 0.01 (USD 0.013) Plastic Packaging Tax-inclusive outlay for a 50-g flexible pouch, maintaining a cost gap that corrugated cannot yet erase.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Slotted Boxes Anchor Volume, Shelf-Ready Trays Capture Growth

Slotted boxes represented 42.43% of market share in 2025, reflecting their compatibility with high-speed erecting lines and broad use across food, beverage, and industrial shipping. The United Kingdom corrugated packaging market size attached to trays, folders and sheets is projected to expand at a 3.66% CAGR, fueled by retailer mandates for shelf-ready presentation that trims in-store labor and boosts on-shelf visibility. Tesco and Sainsbury’s specifications for perforated tear strips and reinforced corner posts reinforce material upgrades, and Amazon’s ship-in-own-container standard pushes primary packs to double as shipping cases. Additional demand stems from gift and promotional formats that employ litho-laminated graphics to differentiate products in crowded e-commerce storefronts.

Brand owners chasing smaller pack counts for single-person households generate thousands of SKUs, making trays and folders ideal for short-run digital printing. The United Kingdom corrugated packaging market share enjoyed by telescope and multi-piece boxes remains modest, yet heavy-machinery exporters rely on these adjustable depth designs for delicate equipment valued at more than GBP 50,000 (USD 63,500) per shipment. Over the forecast horizon, publishers forecast micro-flute mailers to proliferate, yet slotted boxes retain scale where automated case erectors handle more than 60 cases per minute.

By Board Type: Single-Wall Dominates, Triple-Wall Gains in Heavy-Duty Logistics

Single-wall board captured 38.32% of the United Kingdom corrugated packaging market share in 2025, balancing weight, cost, and stacking performance. In contrast, triple-wall constructions are gaining at a 4.32% CAGR as automotive, aerospace, and machinery shippers shift away from timber crates. CorrBoard and VPK Packaging’s new capacity expands access to BB and BC double-wall flutes that meet edge-crush thresholds above 10 kN per meter. Double-wall variants remain relevant for household appliances, but lightweighting is pushing many applications toward optimized single-wall grades with high-performance liners.

Industrial shippers prefer triple-wall for export cargo that can face vibration, humidity, and puncture hazards during ocean transit. The United Kingdom corrugated packaging market's triple-wall volume remains smaller than single-wall volumes, yet its higher unit revenue and stable margins drive converter interest. Investments in automated palletization at CorrBoard reinforce the medium-term outlook for heavy-duty board.

By Flute Profile: C-Flute Leads, F-Flute Surges on E-Commerce Tailwinds

C-flute retained a 32.54% share in 2025 because upstream packing lines, pallets, and racking in grocery and beverage networks are optimized for its 4 mm thickness. Meanwhile, F-flute, at 1.5 mm, is growing 4.65% annually, allowing retailers to load more parcels per trailer and to cut dimensional-weight fees. The United Kingdom corrugated packaging market for F-flute boards will benefit from integrated digital printing systems that deliver high-resolution graphics without pre-coating.

B-flute will continue in beverage multipacks that require grip strength and edge crush resilience. Hybrid BC and EB combinations fill heavy-duty niches but require longer corrugator changeovers that limit volume share. As carriers enforce cubic efficiency, smaller flutes will gain traction, supported by print-on-demand economics that lower minimum order quantities.

By End-User Industry: Food and Beverage Anchors Demand, E-Commerce Accelerates

Food and beverage brands accounted for 35.63% of the market in 2025, relying on recyclable secondary packs for ambient, chilled, and multichannel distribution. E-commerce shipments are set to rise 4.73% annually as rapid grocery delivery and direct-to-consumer models multiply parcel counts. Pharmaceutical cold-chain logistics now tests fiber-based alternatives, such as DS Smith’s TailorTemp solution, which maintains 2-8 °C for 36 h.

Industrial and electronics segments remain partial to triple-wall and ESD-safe inserts, respectively, reflecting higher performance thresholds. The United Kingdom corrugated packaging industry increasingly serves personal-care products in shelf-ready trays that allow store staff to replenish in under half a minute.

By Print Technology: Flexography Dominates, Digital Gains on Short-Run Economics

Flexography held 28.54% of the revenue share in 2025, excelling at runs above 5,000 linear m, where plate costs amortize efficiently. The United Kingdom corrugated packaging market size linked to digital printing will climb at a 3.54% CAGR, supported by HP PageWide presses integrated with inline die-cutters to deliver variable data at speeds above 150 m min⁻¹.

Lithography remains confined to premium gift packs and point-of-sale displays that require photographic detail, while thermal transfer retains a foothold for compliance coding. As SKU proliferation accelerates, the flexo-to-digital crossover point continues to drop, prompting converters to hybridize workflows.

Geography Analysis

England generated roughly 85% of the market share in 2025, thanks to a dense population, extensive fulfillment hubs, and a strong food-processing base in the East Midlands and Yorkshire. London and the South East accounted for one-third of national parcel traffic, driving adoption of F-flute mailers and digital print for direct-to-consumer brands.

The North West’s automotive and aerospace corridors bolster triple-wall intake to protect high-value engines and assemblies. Scotland, Wales, and Northern Ireland collectively hold 15% of volume; Scotland’s capacity is concentrated in Saica Pack’s network, while Wales benefits from Shotton mill’s linerboard supply, avoiding costly fiber imports. Northern Ireland remains export-oriented but faces Brexit-related customs friction.

Collection quality diverges regionally: Essex and Cambridgeshire send more than 40% of residual waste to landfill, lowering recovered fiber availability, whereas English cities subject to Simpler Recycling mandates improve bale grades, raising gate prices 8-12%. Scotland and Wales lag by a year in adopting parallel collection schemes, delaying uniform EPR enforcement. Rising energy-cost volatility weighs on plants lacking onsite renewables, although installations like Saica Pack’s solar-equipped Hartlepool warehouse signal incremental mitigation.

Competitive Landscape

The market is fragmented, with players including Mondi, Smurfit Kappa, WestRock, International Paper, and others. The 2025 International Paper acquisition of DS Smith created a 6.5 billion m² output platform with mill-to-box integration. Mondi’s April 2025 purchase of Schumacher Packaging enlarged its Central European linerboard footprint, positioning the firm to guarantee supply into the United Kingdom corrugated packaging market.

Eren’s 2024 acquisition of Onboard Corrugated and its GBP 150 million (USD 190.5 million) Shotton mill revamp underscores interest from non-EU investors seeking barrier-free access to U.K. customers. Independents such as Board24, GWP Group, and CorrBoard compete on rapid turnaround, bespoke die-cutting, and renewable-energy attributes, yet remain exposed to OCC price swings.

Digital inkjet adoption serves as a differentiator. Board24’s 19% improvement in run speed and 0.54% reduction in waste in 2025 reduce scope 3 emissions for brand owners. CorrBoard’s GBP 1.7 million (USD 2.16 million) palletization upgrade streamlines the handling of high-girth triple-wall sheets. Kite Packaging and Rigid Containers focus on quick-ship online ordering models that resonate with small and mid-sized enterprises shipping via parcel carriers.

United Kingdom Corrugated Packaging Industry Leaders

Smurfit WestRock

Mondi Group

International Paper Company

Saica Group S.L.

GWP Group Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Board24 completed corrugator upgrades at Preston and Coalville, boosting run speed by 19% and cutting downtime by 254 h year⁻¹.

- May 2025: VPK Packaging Group lifted its CorrBoard UK holding to 50% and approved a GBP 1.7 million automated palletization system.

- April 2025: Mondi closed the Schumacher Packaging acquisition, enhancing Central European containerboard self-sufficiency.

- February 2025: Saica Pack began a GBP 10 million (USD 12.7 million) solar-equipped warehouse in Hartlepool with 9,000-pallet capacity.

United Kingdom Corrugated Packaging Market Report Scope

Corrugated packaging is made up of three or more sheets of corrugated fiberboard, also known as containerboard, and is a durable, cost-effective, and adaptable packaging material. The scope of the UK corrugated market study is structured to track spending across end-user industries, including processed foods, fresh food and produce, beverages, paper products, and electrical products, among others.

The United Kingdom Corrugated Packaging Market Report is Segmented by Product Type (Slotted Box, Telescope/Multi-Piece Boxes, Trays, Folders and Sheets, and Other Product Types), Board Type (Single Wall, Double Wall, and Triple Wall), Flute Profile (A, B, C, E, F, and Other Flute Profiles), End-User Industry (Food, Beverages, Pharmaceuticals, Personal Care and Household, Industrial, E-Commerce, Electrical and Electronics, and Other End-user Industries) and Print Technology (Flexography, Digital, Lithography, and Other Print Technologies). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Slotted Box |

| Telescope/Multi-Piece Boxes |

| Trays, Folder and Sheets |

| Other Product Types |

By Board Type

| Single Wall |

| Double Wall |

| Triple Wall |

By Flute Profile

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Other Flute Profile |

By End-user Industry

| Food |

| Beverages |

| Pharmaceuticals |

| Personal Care and Household |

| Industrial |

| E-commerce |

| Electrical and Electronics |

| Other End-user Industries |

By Print Technology

| Flexography |

| Digital |

| Lithography |

| Other Print Technology |

| By Product Type | Slotted Box |

| Telescope/Multi-Piece Boxes | |

| Trays, Folder and Sheets | |

| Other Product Types | |

| By Board Type | Single Wall |

| Double Wall | |

| Triple Wall | |

| By Flute Profile | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| Other Flute Profile | |

| By End-user Industry | Food |

| Beverages | |

| Pharmaceuticals | |

| Personal Care and Household | |

| Industrial | |

| E-commerce | |

| Electrical and Electronics | |

| Other End-user Industries | |

| By Print Technology | Flexography |

| Digital | |

| Lithography | |

| Other Print Technology |

Key Questions Answered in the Report

How large is United Kingdom corrugated packaging demand in 2026?

Consumption is valued at USD 4.24 billion and is projected to climb to USD 4.82 billion by 2031 at a 2.57% CAGR.

Which product type delivers the most revenue?

Slotted boxes account for 42.43% of 2025 revenue and remain the mainstay for food, beverage and e-commerce shipping.

What drives rapid uptake of F-flute board?

Thinner 1.5 mm caliper cuts dimensional-weight fees, fits automated sortation and supports high-resolution digital graphics.

How are Extended Producer Responsibility fees affecting packaging choices?

Fees of GBP 196 (USD 248.9) per tonne for paper and card push brand owners toward lightweight mono-material corrugated packs to lower compliance costs.

Why is digital printing gaining ground on flexography?

Plate-free HP PageWide and similar presses cut setup waste by 40%, making short runs of 500-1,000 units economical for personalized, multi-SKU campaigns.

Which regions show the fastest e-commerce parcel growth?

London, the South East and major Midlands hubs generate the highest parcel volumes, reinforcing demand for micro-flute mailers and shelf-ready trays.

Page last updated on: