India Healthcare Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

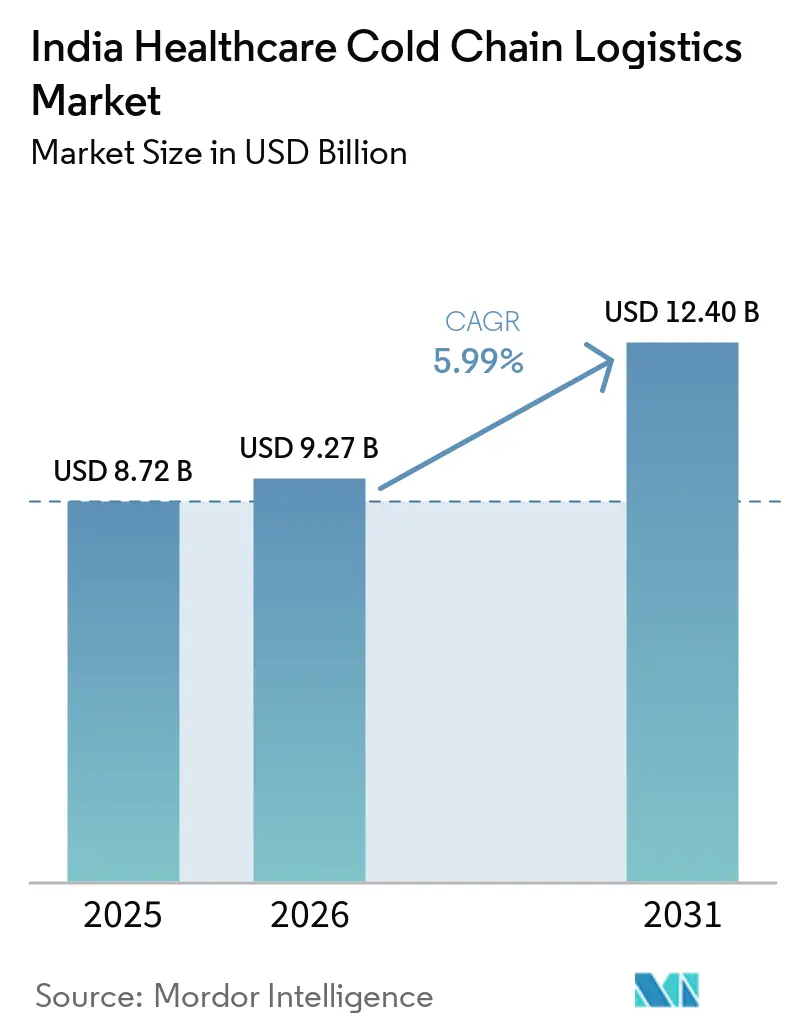

| Base Year Market Size (2025) | USD 8.72 Billion |

| Market Size (2026) | USD 9.27 Billion |

| Market Size (2031) | USD 12.40 Billion |

| Growth Rate (2026 - 2031) | 5.99% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Healthcare Cold Chain Logistics Market Analysis by Mordor Intelligence

The India healthcare cold chain logistics market size is expected to grow from USD 8.72 billion in 2025 to USD 9.27 billion in 2026 and is forecast to reach USD 12.40 billion by 2031 at 5.99% CAGR over 2026-2031.

The market is shifting from bulk, ambient drug movement toward more controlled handling for vaccines, biologics, specialty injectables, and other temperature-sensitive therapies, which is raising the value of validated storage, monitored transport, and documented handoffs. The India healthcare cold chain logistics market is also moving into a more compliance-led phase, where customers increasingly expect traceability, temperature visibility, and deviation management as part of routine service delivery rather than optional add-ons. Global logistics providers are expanding certified infrastructure in Hyderabad, Bengaluru, Mumbai, and other export-linked corridors, which is raising service standards and intensifying competition for high-value healthcare accounts. At the same time, the India healthcare cold chain logistics market still faces structural gaps in reefer availability, rural reach, and backup resilience, which keeps quality uneven outside the major pharmaceutical clusters. These pressures are supporting investment in multimodal lanes, automation, and compliance-linked value-added services, which together define the next growth phase of the India healthcare cold chain logistics market.

Key Report Takeaways

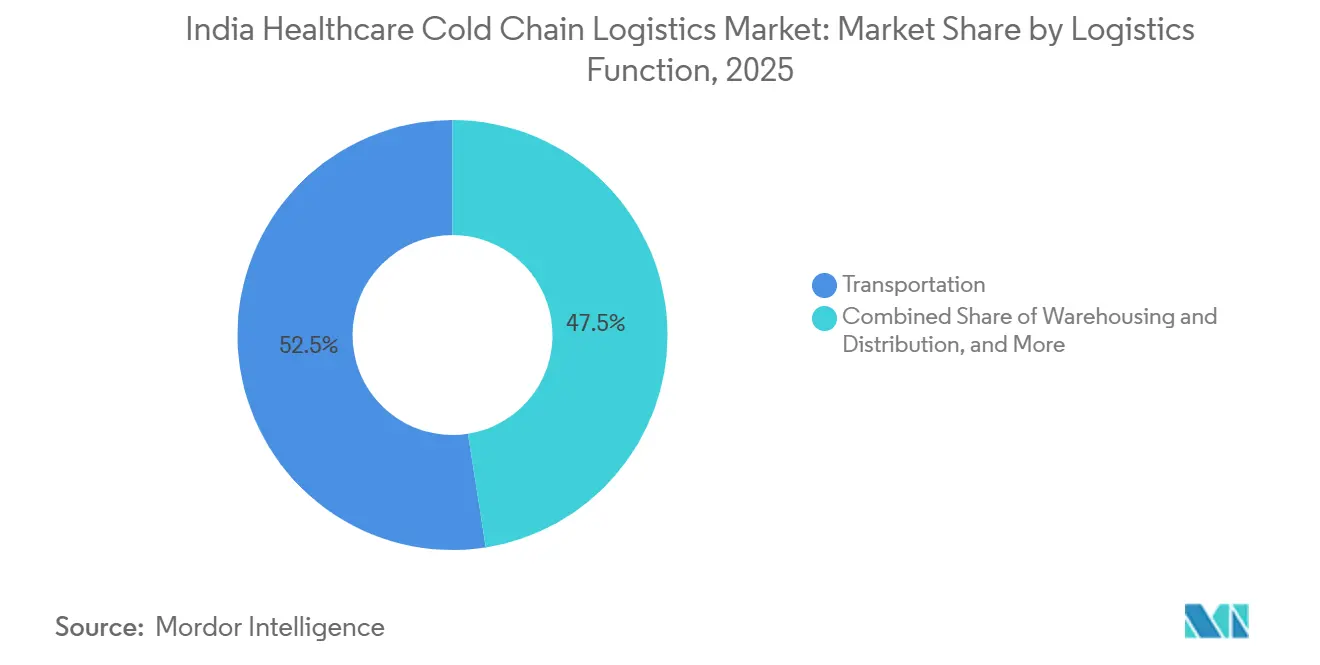

- By logistics function, transportation held 52.47% of the India healthcare cold chain logistics market share in 2025, while value-added services are projected to expand at a 6.74% CAGR through 2031.

- By temperature type, chilled storage accounted for 46.11% of the India healthcare cold chain logistics market size in 2025, while frozen is forecast to grow at a 9.91% CAGR through 2031.

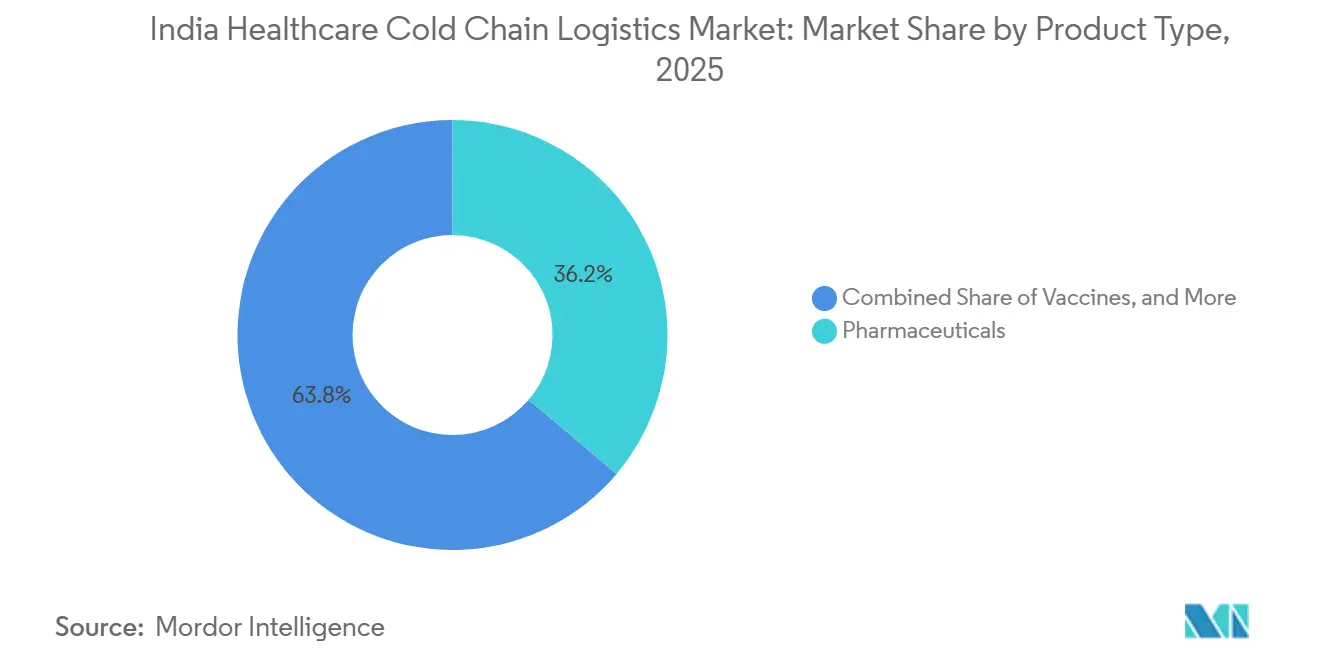

- By product type, pharmaceuticals captured 36.2% of the India healthcare cold chain logistics market share in 2025, while biopharmaceuticals are expected to record the fastest growth at a 12.05% CAGR through 2031.

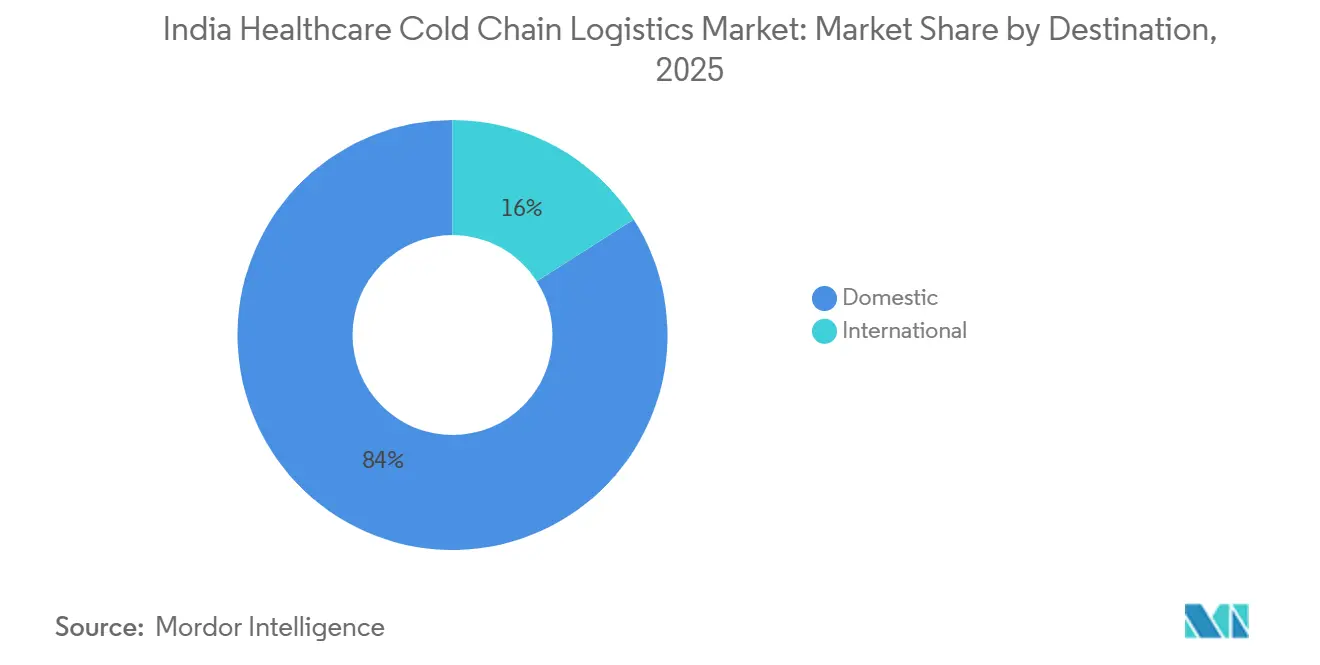

- By destination, domestic retained 84.03% of the India healthcare cold chain logistics market share in 2025, while international is projected to grow faster at a 7.05% CAGR through 2031.

- By end user, pharmaceutical manufacturers held 32.78% of the India healthcare cold chain logistics market share in 2025, while biopharmaceutical manufacturers are forecast to grow at a 6.63% CAGR through 2031.

- By geography, West India led with 29.4% of the India healthcare cold chain logistics market share in 2025, while South India is projected to expand at a 7.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Healthcare Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vaccine and Immunization Throughput Expansion | +1.2% | National, concentrated gains in North, East, and Central India | Short term (≤ 2 years) |

| Biologics and Biosimilars Scale-Up | +1.5% | South and West India predominantly | Medium term (2-4 years) |

| Pharma Export Cold-Chain Compliance Demand | +1.1% | South and West India, with spillover to Central clusters | Medium term (2-4 years) |

| Specialty Injectables and Clinical-Trial Flow Growth | +0.8% | South and West India, urban tertiary care corridors | Medium term (2-4 years) |

| eVIN and U-WIN Demand-Visibility Gains | +0.5% | National, with highest operational impact in East and North India | Medium term (2-4 years) |

| Emerging Cell and Gene Therapy Lanes | +0.3% | South India primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vaccine and Immunization Throughput Expansion

India’s Universal Immunization Program covers 2.9 crore pregnant women and 2.54 crore newborns each year through a cold chain network spanning nearly 30,000 points and using more than 1.06 lakh ice-lined refrigerators and deep freezers. Full immunization coverage reached 98.4% by January 2026, demonstrating that temperature-controlled distribution has extended beyond the main urban corridors into harder-to-serve districts. India also launched a nationwide HPV vaccination campaign on February 28, 2026, adding a new layer of planned volume to the public cold chain at a time when service levels are already under pressure. The expansion of eVIN and U-WIN improves stock visibility, session planning, and distribution control, which supports more predictable movement across the India healthcare cold chain logistics market and reduces avoidable temperature risk in public health delivery[1]“Universal Immunisation Programme, eVIN and U-WIN Platforms,” Ministry of Health and Family Welfare, pib.gov.in. This demand is also important for the private side of the India healthcare cold chain logistics market because vaccine-linked assets often support adjacent pharmaceutical loads when campaigns are not at peak intensity.

Biologics and Biosimilars Scale-Up

The move from small-molecule medicines toward biologics and biosimilars is changing how the India healthcare cold chain logistics market allocates capital, because these therapies need tighter control during storage, handling, and movement. Most biosimilars depend on controlled 2 °C to 8 °C conditions, which means temperature integrity becomes part of product quality rather than a distribution preference. This is pushing more business toward GDP-capable operators that can offer validated lanes, continuous monitoring, and audit-ready documentation, while smaller non-specialized operators face growing exclusion from complex healthcare contracts[2]"The Resilience at Risk: Structural Vulnerabilities and Strategic Pathways in the Indian Pharmaceutical Supply Chain", IJPS Journal, ijpsjournal.com/article/. It is also driving demand in Hyderabad, Bengaluru, Pune, and Ahmedabad, where healthcare logistics providers are building certified capacity near biopharma production and export nodes. As that shift continues, the India healthcare cold chain logistics market is separating into a higher-value compliance tier and a lower-value conventional tier, with pricing power increasingly concentrated in the first group.

Pharma Export Cold-Chain Compliance Demand

Export-linked healthcare cargo now requires much tighter process control, because overseas buyers increasingly expect storage records, lane validation, and documented temperature continuity across every handoff. This is one reason global operators are expanding healthcare-specific infrastructure in India, especially across airfreight corridors connected to Europe and North America. The India healthcare cold chain logistics market is therefore moving from simple refrigerated transport toward integrated compliance service, where digital temperature certificates, exception handling, and traceable chain-of-custody records matter as much as physical movement. Rail-linked reefer services from Hyderabad to western export gateways also show that operators are building new corridor options to strengthen export resilience and reduce dependence on a single mode. For the India healthcare cold chain logistics market, this means export demand is not only adding volume, it is also lifting service intensity and favoring companies that can meet stricter international expectations.

Specialty Injectables and Clinical-Trial Flow Growth

Clinical trial materials and specialty injectables create a different logistics requirement from conventional pharmaceutical distribution, because shipments are smaller, more time-sensitive, and more exposed to product loss if excursions occur. These flows often need documented chain-of-custody, close temperature monitoring, rapid intervention protocols, and controlled delivery into hospitals or research sites rather than broad wholesale distribution networks. That requirement is strengthening the premium end of the India healthcare cold chain logistics market, especially in Bengaluru and Hyderabad, where research activity, CRDMOs, and specialty treatment centers are concentrated. It also supports investment in cross-dock facilities and airport-adjacent handling capacity that can reduce dwell time for sensitive products. As the product mix shifts further toward oncology biologics, autoimmune therapies, and other specialty injectables, the India healthcare cold chain logistics market is likely to see faster growth in high-touch urban last-mile services than in standard refrigerated haulage alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDP-Grade Capex and Energy Cost Burden | -0.8% | National, with highest intensity in Tier-2 and Tier-3 cities and emerging clusters | Medium term (2-4 years) |

| Rural Last-Mile and Multimodal Cold Gaps | -0.7% | East, Central, and North India, plus rural South and West geographies | Long term (≥ 4 years) |

| GDP-Trained Talent and SOP Shortages | -0.5% | National, with acute shortfalls in non-metro hubs | Medium term (2-4 years) |

| Heat Stress and Backup-Power Vulnerability | -0.4% | Central India, North India in peak summer, and East coastal regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GDP-Grade Capex and Energy Cost Burden

GDP-grade pharmaceutical cold infrastructure requires validated mapping, redundant power, continuous logging, documented deviation handling, and system discipline that many smaller operators still struggle to fund. The burden is more severe because only 8% to 10% of India’s 3,500-plus cold chain operators currently meet GDP compliance benchmarks, which shows how uneven the base has remained even as customer requirements tighten. This raises barriers to entry in the India healthcare cold chain logistics market and shifts share toward larger operators that can finance equipment, monitoring systems, and process control at scale. It also limits expansion into smaller cities, because the revenue available in many Tier-2 and Tier-3 locations does not always justify high-cost compliant assets during the early years. The near-term effect is better average quality in major corridors, but the tradeoff is slower geographic spread for the India healthcare cold chain logistics market outside the strongest pharmaceutical and hospital clusters[3]“India, NCCD Reports a 2.2% Compound Annual Growth Rate in Cold Storage Capacity,” International Institute of Refrigeration, iifiir.org.

Rural Last-Mile and Multimodal Cold Gaps

India operates close to 10,000 reefer vehicles against an estimated national requirement of 62,000, which leaves a wide service gap across rural and lower-density healthcare routes. This shortage limits reliable cold penetration in Tier-3 and Tier-4 geographies, where route density is lower, grid conditions are weaker, and delivery windows are harder to control. The India healthcare cold chain logistics market is responding through multimodal pilots, including reefer rail services for pharmaceutical export corridors, but the first-mile and last-mile links around those corridors still depend heavily on road connectivity. The challenge is especially visible in East, Central, and parts of North India, where coverage gaps can offset the gains made by modern warehouse assets in the major metros. Until district-level warehousing, pre-cooling, and reefer movement improve together, the India healthcare cold chain logistics market will continue to show strong urban performance and weaker rural execution[4]“U-WIN, e-VIN and Co-WIN, Harnessing Digital Platforms to Enhance Immunisation Coverage in India,” International Journal of Community Medicine and Public Health, doi.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Road Transportation Anchors Volume as VAS Captures Margin

Transportation held 52.47% of the India healthcare cold chain logistics market share in 2025, which kept it as the largest functional block. Road transport remains the core of that segment because pharmaceutical shipments still require flexible point-to-point delivery across hospitals, distributors, plants, and regional stock points. The strength of road movement reflects India’s geographic spread and the need to reach smaller consumption centers that air and rail cannot directly serve. Reefer trucks equipped with GPS tracking and data loggers remain central to this operating model because they support both route visibility and documented temperature control during transit. This means transport scale still sets the volume base for the India healthcare cold chain logistics market, even as customers become more selective about service quality. Maersk’s dedicated reefer rail service from Hyderabad to Mumbai showed that temperature-controlled pharmaceutical movement can be integrated into multimodal planning when schedules and container standards are reliable. Transportation, therefore, continues to anchor the India healthcare cold chain logistics industry, while modal diversification slowly improves network depth.

Value-added services are the fastest-growing function, expanding at a 6.74% CAGR through 2031, which shows how the service mix is shifting beyond pure movement or storage. Customers increasingly want track-and-trace, digital temperature certificates, risk alerts, repackaging under controlled conditions, and support during deviations, because those features simplify audits and reduce the burden on internal quality teams. Kuehne+Nagel’s HealthChain-certified setup in Bengaluru and Hyderabad reflects this direction, as the company has tied controlled storage and cross-dock capability into a broader healthcare service package. This is improving margin potential for operators that can bundle multiple services around sensitive product flows rather than compete only on line-haul price. In practice, value-added services are becoming one of the clearest differentiators inside the India healthcare cold chain logistics market.

By Temperature Type: Chilled Segment Dominates as Frozen Accelerates on Biosimilar Demand

Chilled storage at 2 °C to 8 °C accounted for 46.11% of the India healthcare cold chain logistics market share in 2025, which made it the leading temperature band. That leadership reflects the daily operating base of vaccines, insulin, and many conventional biologics, all of which move through this range on a recurring basis. The chilled band also benefits from a wider installed base across warehouses, hospitals, and distribution points, which makes it the most practical temperature class for broad healthcare coverage. Because so many essential therapies sit within this temperature requirement, chilled handling remains the revenue foundation of the India healthcare cold chain logistics market. It also shapes how new operators prioritize their initial infrastructure and route design.

Frozen storage from minus 18 °C to 0 °C is projected to grow at a 9.91% CAGR through 2031, which makes it the fastest-moving temperature type. This growth points to a deeper change in pharmaceutical mix, where biosimilar injectables, monoclonal antibodies, and plasma-derived products are taking a larger role in value terms. The frozen segment, therefore, represents a more specialized layer of the India healthcare cold chain logistics market, one that demands stronger process discipline and more selective customer qualification. As frozen products grow, operators will need better insulation, tighter loading practices, and more capable alarm-response systems across both storage and movement. The result is a temperature mix that is steadily shifting toward higher operational intensity across the India healthcare cold chain logistics market.

By Product Type: Pharma Anchors Revenue While Biopharmaceuticals Reshape the Growth Curve

Pharmaceuticals accounted for 36.2% of the India healthcare cold chain logistics size in 2025, which made them the largest product type in the market. This segment includes prescription drugs, specialty medicines, and OTC products, so it remains the broadest source of recurring volume across storage and transport networks. It also spans a wide range of handling profiles, from standard chilled movement for insulin to more controlled distribution for sensitive injectables. Because of that breadth, pharmaceuticals still provide the base utilization that supports route economics, warehouse occupancy, and network continuity across the India healthcare cold chain logistics market. Their importance is not just scale, but also the way they stabilize demand across customer groups.

Biopharmaceuticals are projected to grow at a 12.05% CAGR through 2031, which makes them the strongest growth engine within the India healthcare cold chain logistics market size. This segment grows faster because biologics and biosimilars require tighter handling discipline, attract higher service value, and align more closely with both export demand and specialty care expansion. The growth also reflects how healthcare logistics is moving toward products that cannot tolerate weak temperature control or incomplete documentation. For operators, biopharmaceuticals are attractive because they support premium pricing, longer customer relationships, and more specialized contracts than standard medicine movement often does. That is why biopharmaceuticals are increasingly reshaping the direction of the India healthcare cold chain logistics market.

By Destination: Domestic Scale Anchors the Market as International Drives Premium Revenue

Domestic shipments held 84.03% of the India healthcare cold chain logistics market share in 2025, which made them the clear volume anchor of the market. This dominance reflects the size of India’s internal healthcare demand and the breadth of domestic movement between manufacturing plants, hospital systems, depots, distributors, and pharmacies. Domestic flows also vary widely in quality by corridor, with strong performance in metro-linked routes and weaker control across lower-density regions. That unevenness means the domestic side of the India healthcare cold chain logistics market combines scale with a continuing need for network upgrade. It remains the central base from which most operators build utilization and customer relationships.

International movement is projected to grow at a 7.05% CAGR through 2031, which makes it the faster-growing destination segment. This matters because export-linked healthcare cargo usually demands stronger traceability, more formal documentation, and better-controlled handoffs than domestic movement. The India healthcare cold chain logistics market size for international lanes is, therefore, smaller in absolute terms, but it carries higher service intensity and often supports better pricing for qualified operators. Global network providers are expanding India-linked healthcare capacity partly because these export corridors require integrated handling between origin sites, airfreight or seafreight gateways, and overseas receiving points. As exports deepen, international healthcare logistics will keep raising quality expectations across the broader India healthcare cold chain logistics market.

By End User: Pharma Manufacturers Lead as Biopharma Players Accelerate Fastest

Pharmaceutical manufacturers held 32.78% of the India healthcare cold chain logistics market share in 2025, which made them the leading end-user group. Their position reflects the simple fact that they account for a large share of temperature-controlled product movement across India’s healthcare supply chain. These companies also shape service requirements because they need dependable storage, qualified transport, and documentation that can withstand internal and external quality reviews. As a result, pharmaceutical manufacturers remain the most important customer base for route design, warehouse placement, and service standardization in the India healthcare cold chain logistics market. Their share also gives them strong influence over which providers scale fastest.

Biopharmaceutical manufacturers are projected to grow at a 6.63% CAGR through 2031, making them the fastest-growing end-user segment. Their growth matters because it pulls the India healthcare cold chain logistics market toward tighter process control, better packaging discipline, and more selective vendor qualification. These customers often need specialized handling for monoclonal antibodies, recombinant products, and other sensitive therapies, which leave less room for operating errors. That creates greater demand for providers that can support validated lanes, excursion response, and integrated reporting, rather than just simple refrigerated movement. In commercial terms, biopharma demand is helping raise the technical standard of the India healthcare cold chain logistics market.

Geography Analysis

West India held 29.4% share in 2025, which kept it as the leading regional block in the India healthcare cold chain logistics market. Maharashtra combines pharmaceutical manufacturing, airport-linked cargo handling, and broad distribution density in a way that few other states currently match. Pune and Mumbai give the region a strong mix of formulation output, warehouse presence, and export connectivity. FedEx’s Navi Mumbai cargo hub project strengthens that advantage because it is built for temperature-sensitive products and raises long-term handling capacity in a key western gateway. Gujarat adds further depth through its pharmaceutical manufacturing base and its role in low-temperature infrastructure investment, including automated frozen storage capacity.

South India is projected to grow at a 7.29% CAGR through 2031, which makes it the fastest-growing geography in the India healthcare cold chain logistics market size. Hyderabad is central to this outlook because it combines API, vaccine, and biopharma activity with rising multimodal logistics support. Kuehne+Nagel’s temperature-controlled healthcare facility in Hyderabad adds certified handling capacity close to one of India’s most important pharmaceutical corridors. The company’s earlier Bengaluru Cool Zone also supports the southern growth story because Bengaluru is important for CRDMOs, clinical trial logistics, and specialty care demand. Maersk’s dedicated reefer rail service from Hyderabad to Mumbai further improves corridor depth for pharmaceutical exporters that need more structured and resilient outbound movement.

North India remains a major distribution geography because Delhi NCR supports large-scale warehousing, broad healthcare consumption, and access to surrounding northern states. Its role is more domestic than export-led, but it remains critical for network reach and inventory positioning. East and Central India are still under-served, with weaker reefer density, lower compliant cold storage presence, and greater dependence on uneven local infrastructure. That weakness limits current performance, yet it also creates future room for operators willing to enter earlier and build district-level cold capability. Mahindra Logistics’ expansion in Guwahati and Agartala suggests that parts of the East are beginning to attract planned warehousing investment linked to long-term healthcare demand. Public health programs also matter more in these regions because wider immunization coverage can create a steadier base for cold infrastructure utilization. The regional picture therefore remains uneven, but it supports a market where the strongest near-term value sits in West and South India while the longer runway extends into North, East, and Central corridors.

Competitive Landscape

The India healthcare cold chain logistics market is moderately fragmented overall, but competition is tightening around a smaller group of GDP-capable players serving higher-value healthcare flows. This gives the market a two-layer profile: a long tail of operators remains active, while a narrower set of providers controls the most compliance-intensive contracts. Global companies such as DHL, Kuehne+Nagel, FedEx, and DSV are raising the bar by expanding their certified infrastructure and integrated healthcare service capabilities in India. Their presence matters because healthcare customers increasingly buy compliance depth, network reliability, and documentation quality rather than just refrigerated capacity. This is changing how the Indian healthcare cold chain logistics market rewards scale and specialization.

DHL strengthened its healthcare position through the acquisition of CRYOPDP in March 2025, which added specialized capabilities in life sciences logistics and improved its standing in advanced therapy logistics. Kuehne+Nagel expanded in India with HealthChain-certified facilities in Bengaluru and Hyderabad, which gives it a stronger platform across the main southern biopharma corridor. FedEx broke ground on its Navi Mumbai automated cargo hub in February 2026, which is a direct strategic move to capture more temperature-sensitive air cargo from western India. DSV also expanded its global and Indian reach by completing the acquisition of Schenker, which gives the combined network greater scale for integrated freight and healthcare solutions. These moves show that the India healthcare cold chain logistics market is attracting long-term strategic capital from global integrators rather than short-term opportunistic capacity.

Domestic companies remain important because they bring route familiarity, existing reefer fleets, warehouse presence, and local execution depth in harder operating environments. Snowman Logistics, TCI Cold Chain, Indicold, and CONCOR remain relevant names in the India healthcare cold chain logistics market because they combine local coverage with growing investment in more advanced cold handling models. Indicold’s frozen automation project in Gujarat is one example of a domestic player moving beyond conventional warehousing into higher-precision infrastructure. CONCOR and Maersk’s reefer rail collaboration is another example, showing that domestic and international capabilities can be combined to build new cold corridors for pharmaceuticals. The open space in the India healthcare cold chain logistics market still lies below the top urban centers, where certified service is limited and rural reach remains inconsistent. That means future competition will depend not only on who has the best metro assets, but also on who can extend compliant service into lower-density geographies without losing operating discipline.

India Healthcare Cold Chain Logistics Industry Leaders

-

DHL Group

-

United Parcel Service of America, Inc. (UPS)

-

Kuehne+Nagel

-

Snowman

-

Safexpress Pvt. Ltd,

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: CONCOR, in partnership with Maersk and South Central Railway, launched the Aushadhi Express, India’s first dedicated pharmaceutical reefer rake service, connecting ICD Sanathnagar, Hyderabad, to Jawaharlal Nehru Port Trust (JNPT). The service operates on a fixed weekly schedule using 40-ft refrigerated containers and is projected to reduce GHG emissions by approximately 3,000 tonnes per year, marking a shift toward rail-integrated cold chain for export pharma.

- May 2026: Kuehne+Nagel opened a HealthChain-certified temperature-controlled airfreight cross-dock facility in Hyderabad, 248 sqm, with +2 °C to +8 °C and +15 °C to +25 °C zones, its second GxP-compliant facility in India following the Bengaluru Cool Zone launched in December 2025. The dual-hub model positions the company across both major Southern biopharma clusters.

- February 2026: FedEx broke ground on a fully automated, 300,000 sq ft air cargo hub at Navi Mumbai International Airport, developed in partnership with Adani Airport Holdings Limited at an investment of INR 2,500 crore (USD 278.24 million). The hub is designed to handle temperature-sensitive pharmaceuticals and perishables with initial capacity of 0.5 million metric tonnes annually, scaling to 2.6 million metric tonnes.

- February 2026: DHL Group announced the expansion of its dedicated airfreight cold chain network, with India identified as a priority expansion market, connecting Indian pharmaceutical manufacturers to North American and European life sciences customers through GDP-grade temperature-controlled air corridors.

India Healthcare Cold Chain Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing and Distribution | |

| Value-added Services and Others |

| Chilled (0-5 °C) |

| Frozen (-18-0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

| Pharmaceuticals | Prescription and Speciality Drugs |

| OTC Drugs | |

| Biopharmaceuticals (Biologics and Biosimilars) | |

| Vaccines | |

| Clinical Trail Materials | |

| Cell and Gene Therapies | |

| Medical Devices | |

| Veterinary Medicine | |

| Blood, Plasma and Blood Components | |

| Diagnostic and Laboratory Products | |

| Organs and Human Tissues | |

| Others |

| Domestics |

| International |

| Pharmaceutical Manufacturers |

| Biopharmaceutical Manufacturers |

| Hospitals and Clinics |

| Hospitals and Retail Pharmacies |

| Healthcare Distributors and Wholesalers |

| Others |

| North |

| Central |

| West |

| East |

| South |

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing and Distribution | ||

| Value-added Services and Others | ||

| By Temperature Type | Chilled (0-5 °C) | |

| Frozen (-18-0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Product Type | Pharmaceuticals | Prescription and Speciality Drugs |

| OTC Drugs | ||

| Biopharmaceuticals (Biologics and Biosimilars) | ||

| Vaccines | ||

| Clinical Trail Materials | ||

| Cell and Gene Therapies | ||

| Medical Devices | ||

| Veterinary Medicine | ||

| Blood, Plasma and Blood Components | ||

| Diagnostic and Laboratory Products | ||

| Organs and Human Tissues | ||

| Others | ||

| By Destination | Domestics | |

| International | ||

| By End User | Pharmaceutical Manufacturers | |

| Biopharmaceutical Manufacturers | ||

| Hospitals and Clinics | ||

| Hospitals and Retail Pharmacies | ||

| Healthcare Distributors and Wholesalers | ||

| Others | ||

| By Region | North | |

| Central | ||

| West | ||

| East | ||

| South | ||

Key Questions Answered in the Report

What is the current size of India healthcare cold chain logistics?

The India healthcare cold chain logistics market was valued at USD 8.72 billion in 2025 and is estimated at USD 9.27 billion in 2026, with a forecast of USD 12.40 billion by 2031.

What is driving growth in healthcare cold logistics across India?

Growth is being supported by wider immunization throughput, rising biologics and biosimilars movement, tighter compliance expectations, and more investment in certified healthcare logistics infrastructure.

Which logistics function leads demand in 2025?

Transportation remained the largest function with 52.47% share in 2025, while value-added services is the faster-growing function at a 6.74% CAGR through 2031.

Which temperature segment is growing the fastest?

Chilled handling led in 2025 with 46.11% share, while frozen handling is projected to grow the fastest at a 9.91% CAGR through 2031.

Which region is most important for future expansion?

West India led in 2025 with 29.4% share, but South India is expected to grow faster at a 7.29% CAGR through 2031 because of its stronger biopharma and export-linked ecosystem.

What is the biggest structural challenge for operators?

The largest structural challenge remains weak rural last-mile capability, with India operating close to 10,000 reefer vehicles against an estimated requirement of 62,000.

Page last updated on: