Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

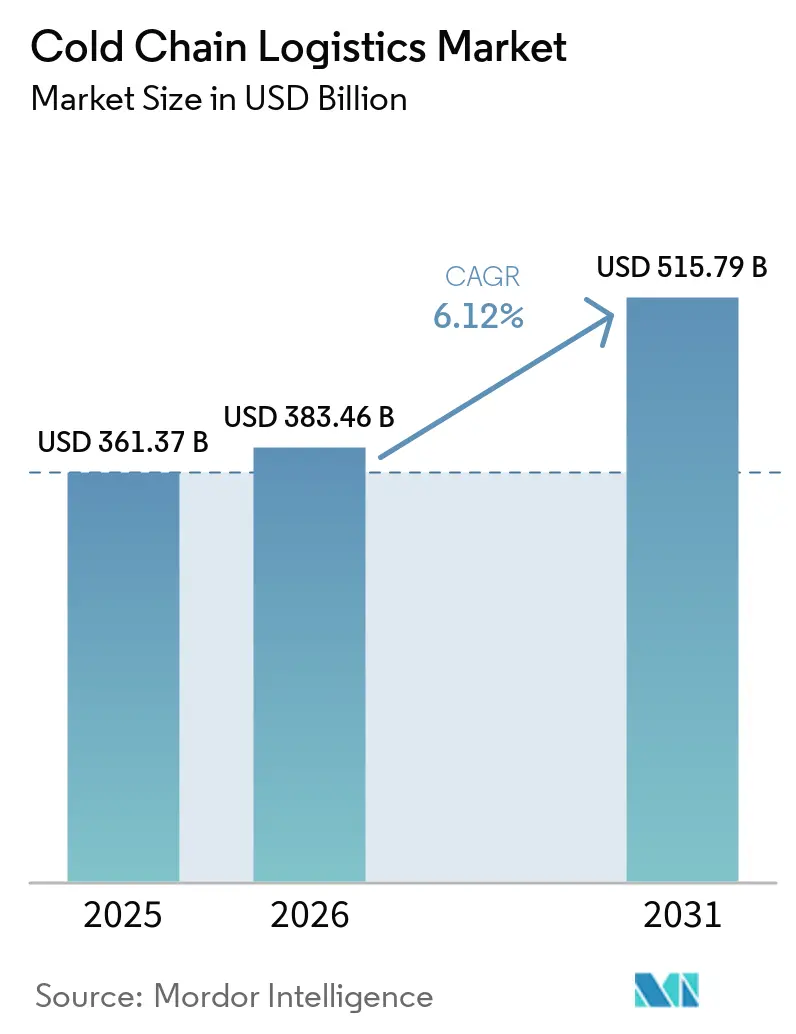

| Market Size (2026) | USD 383.46 Billion |

| Market Size (2031) | USD 515.79 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

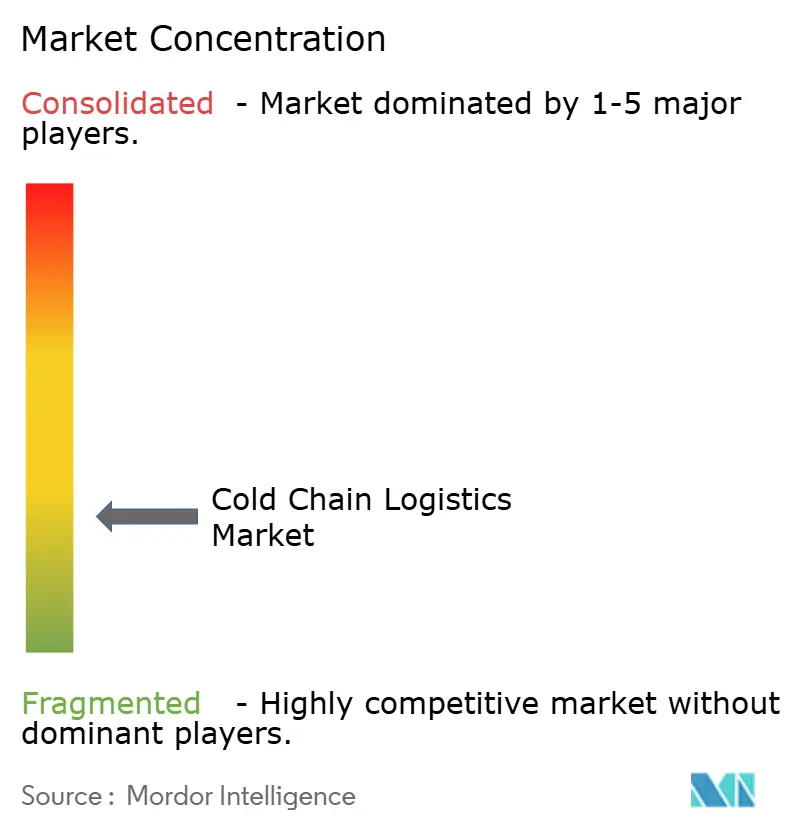

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cold Chain Logistics Market Analysis by Mordor Intelligence

The Cold Chain Logistics market size is expected to grow from USD 361.37 billion in 2025 to USD 383.46 billion in 2026 and is forecast to reach USD 515.79 billion by 2031 at 6.12% CAGR over 2026-2031.

Robust growth is anchored in the expanding global vaccine pipeline, the surge of quick-commerce grocery platforms, and sustained demand for premium frozen foods. Deep-frozen and ultra-low temperature services are growing faster than conventional frozen storage owing to the distribution requirements of mRNA vaccines and advanced biologics. Asia-Pacific is the fastest-growing region, yet North America retains the largest regional share through continued investment in automation and IoT-enabled monitoring. Regulatory mandates such as the United States Food Safety Modernization Act (FSMA) 204 rule are turning real-time temperature tracing into a competitive differentiator rather than a mere compliance box.

Key Report Takeaways

- By service type, refrigerated transportation expanded at a 6.88% CAGR through 2031, overtaking refrigerated storage, which held a 52.37% cold chain logistics market share in 2025.

- By temperature range, the deep-frozen/ultra-low segment grew at an 8.22% CAGR, and the Frozen segment accounted for 61.35% of the cold chain logistics market size in 2025.

- By application, pharmaceuticals and biologics advanced at a 7.56% CAGR, while food and beverages maintained a 74.25% share of the cold chain logistics market size in 2025.

- By geography, Asia-Pacific led growth at an 8.05% CAGR, whereas North America contributed 33.62% of global revenue in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-low temperature demand for mRNA vaccines | +1.2% | North America & Europe | Medium term (2-4 years) |

| Quick-commerce grocery growth | +0.9% | Asia-Pacific & North America | Short term (≤ 2 years) |

| Pharmaceutical outsourcing to GDP-compliant 3PLs | +1.0% | Europe & global pharma hubs | Medium term (2-4 years) |

| IoT telematics adoption under FSMA 204 | +1.1% | North America, expanding to Europe & Asia-Pacific | Short term (≤ 2 years) |

| Government Incentives for Solar-Powered Cold Warehouses in Middle East & Africa to Curb Post-Harvest Food Losses | +0.7 | Middle East & Africa, with expansion to South Asia | Long term (≥ 5 yrs) |

| China's "Ready-to-Cook" Meal Boom Propelling Cold Storage Leasing in Tier-2 Cities | +0.8 | China, with similar trends emerging in Southeast Asia | Medium term (~ 3-4 yrs) |

| Source: Mordor Intelligence | |||

Surging demand for mRNA vaccines requiring ultra-low temperature distribution

mRNA vaccines must be stored between -70 °C and -80 °C, which is far below conventional frozen ranges. Manufacturers now partner with logistics providers that operate specialized ultra-low freezers, dry-ice replenishment stations, and redundant power systems. DHL earmarked USD 2 billion for healthcare logistics through 2030, with USD 860 million reserved for North America. Vaccine spoilage remains a critical cost driver; nearly 50% of global doses still go to waste because of thermal excursions, representing an annual USD 35 billion loss to drug makers. The need to mitigate this waste is accelerating investment in the deep-frozen segment of the cold chain logistics market. Ultra-low projects now command premium yields, which is drawing private equity into purpose-built freezer farms. Collectively, these forces add a 1.2 percentage-point uplift to the market’s long-term CAGR.

Rapid expansion of quick-commerce grocery platforms transforming last-mile logistics

Fifteen-to-thirty-minute grocery delivery promises have triggered a wave of micro-fulfilment centre construction across densely populated Asian cities. Operators install multi-temperature chambers so that produce, dairy, meat, and ice cream depart in perfect condition without cross-contamination. The e-grocery channel is poised to account for one-fifth of all United States grocery revenue by 2025. Similar adoption curves are visible in India, Indonesia, and South Korea, aided by rising smartphone penetration. Every incremental point of e-grocery penetration raises demand for temperature-controlled vans and two-wheelers, which expands the cold chain logistics market. Legacy retailers are responding by outsourcing hyper-local distribution to third-party specialists that guarantee on-time delivery within strict temperature bands.

Pharmaceutical outsourcing drives GDP-compliant 3PL adoption

Drug developers continue to shift manufacturing and distribution to third parties to focus on core R&D. European regulators enforce Good Distribution Practice standards, so 3PLs that can document lane validation, calibrated packaging, and chain-of-custody events attract new contracts. Biopharmaceutical cargo values are often greater than USD 5 million per pallet, which justifies premium pricing for validated cold rooms and passive shippers. Outsourcing lifts utilisation rates in multi-client facilities, which in turn lowers unit costs for shippers and expands the cold chain logistics market. Providers that demonstrate end-to-end visibility earn higher renewal rates, reinforcing a flywheel of volume, data, and revenue growth across the cold chain logistics industry.

IoT-enabled telematics under FSMA 204 elevate real-time monitoring investments

The FSMA 204 rule requires detailed traceability records for leafy greens, shell eggs, and other high-risk foods by 2026[1]Food and Drug Administration, “FSMA 204 Traceability Rule Guidance,” Food and Drug Administration, fda.gov. Sensors now transmit location, temperature, and humidity every few minutes, and deviations trigger automated alerts that prevent spoilage. The same data stream feeds optimisation engines that cut empty backhauls and shrink fuel costs. Providers differentiate by offering shipper dashboards that integrate blockchain ledgers, which simplify audits and litigation defence. Early adopters report product-loss reductions of up to 30%, validating the business case for wider roll-out. As compliance deadlines approach, capital outlays for telematics solutions are forecast to exceed USD 5 billion annually, injecting double-digit growth into the cold chain logistics market.

Restraints Impact Analysis*

| Restraints | (~) Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electricity instability in Sub-Saharan Africa | -0.8% | Sub-Saharan Africa | Medium term (2-4 years) |

| Shortage of CDL-certified reefer drivers | -1.2% | United States | Short term (≤ 2 years) |

| High Capital Costs of Ammonia/CO₂ Cascade Retrofits for EU F-Gas Regulation Compliance | -0.7 | Europe, with potential spillover to global operations | Medium term (~ 3-4 yrs) |

| Fragmented Ownership of Small-Scale Cold Rooms in India Hindering Network Optimization | -0.6 | India, with similar patterns in Southeast Asia | Long term (≥ 5 yrs) |

| Source: Mordor Intelligence | |||

Chronic electricity instability inflating operational costs in Sub-Saharan Africa

Cold stores in Nigeria, Kenya, and Ghana face grid outages that exceed 500 hours per year. Operators run diesel generators for backup power, pushing energy costs to 60% of operating expenses versus 35% in developed markets. Solar-hybrid microgrids cut fuel consumption, yet upfront investments remain prohibitive for small owners. Unstable electricity hampers adherence to temperature protocols, exposing exporters to rejection at destination ports. Unless renewable solutions scale, logistics providers may limit capacity expansions, slowing the cold chain logistics market in the region.

Acute shortage of CDL-certified reefer drivers constraining United States capacity

The United States trucking fleet is short more than 80,000 qualified drivers, and refrigerated lanes feel the deficit most acutely. Candidates must master temperature checks, load securement, and additional regulatory paperwork, which extends training time and raises cost. Carriers raise wages to recruit talent, lifting freight rates for temperature-controlled loads by double digits compared with dry van rates. High turnover strains service reliability, forcing shippers to build larger safety stocks or diversify modes. A sustained gap in driver supply could limit the near-term upside of the cold chain logistics market until automation or autonomous technologies mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Segment Accelerating Past Storage

Refrigerated storage accounted for 52.37% of the cold chain logistics market share in 2025, yet refrigerated transportation is climbing faster at a 6.88% CAGR. The uptick mirrors consumer expectations for fast, fresh delivery and the diversification of global sourcing lanes. Longer cross-border e-commerce chains and direct-to-consumer seafood deliveries expand lane-kilometres that must stay within tight temperature ranges. Multi-stop routing software allows carriers to maximise the the utilisation of reefer trucks, offsetting the high capital cost of insulated trailers. Investments in lithium-ion battery systems for trailer refrigeration units lower fuel burn, aligning with strict emissions standards in California and the European Union.

Value-added services are emerging as a margin-rich niche inside the cold chain logistics market. Activities such as relabeling, reverse logistics, and seasonal packaging require skilled labour and high-velocity workflows that produce higher revenue per pallet than basic storage. Pharmaceutical shippers now expect order kitting, clinical return handling, and excursion reporting under one roof to streamline quality audits. Food brands request aroma-guard packaging and end-of-line quality inspection to match retailer specifications. Demand for integrated services entices traditional warehouse operators to expand into transport-plus-value-added bundles to protect share and avoid price-only competition in the cold chain logistics market.

By Temperature Type: Ultra-Low Segment Outpacing Conventional Ranges

The frozen range of -18 °C to 0 °C retained a 61.35% share of cold chain logistics market size in 2025, underpinned by global frozen food consumption. Nonetheless, the deep-frozen and ultra-low band below -20 °C posts the fastest 8.22% CAGR through 2031. Mounting volumes of cell and gene therapies, oncology biologics, and mRNA vaccines propel this segment. The WHO reports a 200% rise in ultra-low storage capacity since 2020. Infrastructure upgrades include vacuum-insulated panels, liquid-nitrogen backup, and redundant power to guarantee hold times of 120 hours during transit. Providers that own modular freezer pods scale capacity in weeks rather than months, enabling rapid response to vaccine roll-outs.

Chilled storage between 0 °C and 5 °C continues steady growth across dairy, fresh produce, and burgeoning ready-to-eat meal categories. Operators bundle chilled and ambient rooms under one roof to optimise space and labour. Integrated facilities balance seasonal peaks, such as ice cream in summer and citrus exports in winter, which stabilises revenue streams. Ambient-controlled rooms for chocolate, wine, and gourmet coffee complement core refrigerated services, expanding share of wallet across diversified customer bases in the cold chain logistics market.

By Application: Pharmaceuticals Outpacing Traditional Food Segments

Food and beverages sustained a 74.25% contribution to cold chain logistics market size in 2025, anchored by meat, poultry, and seafood demand. The USDA records meat and poultry accounting for 34% of United States refrigerated capacity. Ready-to-eat meals now represent the fastest-growing food sub-segment as urban consumers seek convenience. Plant-based protein lines add further complexity, as they often need tighter humidity control than animal proteins.

Pharmaceuticals and biologics, although a smaller volume, post an 7.56% CAGR and increasingly command ultra-low temperature assets. IATA data show temperature-controlled air cargo for medicines rising 18% year over year. High-value cargo motivates investment in GDP-certified cleanrooms, validated packaging, and excursion management software. Clinical trial material moves require aggressive lead times and strict chain-of-custody, pushing 3PLs to develop specialised control towers. As a result, the cold chain logistics market increasingly allocates capacity to healthcare even in traditionally food-dominated facilities.

Geography Analysis

North America generated 33.62% of 2025 revenue and operates 5 billion ft³ of refrigerated space, more than four-fifths of which sits in the United States. Scale advantages permit aggressive automation roll-outs, such as high-bay cranes and shuttle systems that double pallet density. Yet driver scarcity and port congestion pressure end-to-end reliability. The FSMA 204 rule accelerates adoption of IoT telematics, turning compliance spending into service-quality upgrades that sustain the cold chain logistics market.

Asia-Pacific registers the highest 8.05% CAGR as rising incomes increase per-capita consumption of protein and premium frozen desserts. China’s ready-to-cook meal boom fuels demand for regional distribution hubs in tier-2 cities, while India’s fragmented cold room ownership remains a bottleneck. FAO estimates that improving cold chain infrastructure could cut Asia’s post-harvest losses by up to 40%. Governments in Vietnam, Indonesia, and Thailand offer tax breaks on ammonia-CO₂ plants to lure foreign direct investment. These policies make Asia-Pacific the pivotal battleground for market share in the cold chain logistics market.

Europe exhibits slow-but-steady growth while executing stringent environmental upgrades. The EU F-Gas Regulation encourages a shift to natural refrigerants, driving installation of ammonia-CO₂ cascade systems despite capital burdens. Operators retrofit insulation, LED lighting, and variable-speed compressors to earn energy-efficiency certificates that unlock utility rebates. Partnerships with OEMs accelerate deployment of plug-and-play plant rooms, limiting downtime. Pharmaceutical shipments form a sizable share of European volumes, reinforcing the region’s status as a premium service market within the wider cold chain logistics market.

Middle East and Africa remain small in absolute terms but record double-digit gains where solar-powered cold stores mitigate unreliable grids. UNIDO tracks a 25% jump in African cold chain investments since 2020. Incentive schemes in Kenya and South Africa reimburse up to 30% of photovoltaic installation costs, spurring private-sector interest. However, diesel reliance persists, keeping operating costs elevated. In Latin America, Brazil leads regional expansion. Its national warehousing association notes a 15% capacity jump since 2020. Beef exporters demand near-dock freezer complexes to meet Asian quality checks, reinforcing Brazil’s strategic role in the cold chain logistics market.

Mordor Intelligence provides coverage of the cold chain logistics market across other key regional markets, including Africa and South America, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Mexico, Indonesia, Sweden, Netherlands, and Thailand incorporating local coverage and market participation, as required.

Note: Segments share of all individual segments available upon report purchase

Competitive Landscape

The cold chain logistics market shows moderate consolidation. The top five operators command roughly 25% of global cubic-foot capacity, leaving room for regional specialists. Lineage Logistics tops the ranking with 2.98 billion ft³ across more than 480 warehouses after its 2024 IPO raised USD 4.4 billion. Americold follows with 1.45 billion ft³ and 234 sites, focusing on retrofitting facilities with shuttle-based automation and low-GWP refrigerants.

M&A continues at pace. Lineage acquired MTC Logistics in April 2025, adding port-centric capacity along the East and Gulf Coasts. DHL is allocating USD 2 billion to expand healthcare-compliant warehouses and validated transport assets. Vertical Cold Storage vaulted from fifteenth to sixth place by buying smaller operators and launching greenfield sites that rely on fully automated high-bay designs.

Technology is the chief battleground. Providers deploy AI route-planning tools, robotic case picking, and fully electric trailer units from OEMs such as Mitsubishi Heavy Industries. Autonomous driving pilots by Hirschbach Motor Lines and Kodiak Robotics test hands-free reefer lanes between distribution centres. Early movers expect labour savings and safety gains that could offset the driver shortage. Sustainability differentiators—such as solar rooftops, renewable diesel, and trans-critical CO₂ systems—also shape bidding contests for global contracts in the cold chain logistics market.

Cold Chain Logistics Industry Leaders

Lineage Logistics

Americold Logistics

NewCold Advanced Cold Logistics

Nichirei Logistics Group Inc.

Constellation Cold Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Lineage Logistics completed its acquisition of MTC Logistics, enlarging its port-centric footprint on the East and Gulf Coasts.

- April 2025: DHL Group committed USD 2 billion to life-sciences and healthcare logistics through 2030, with USD 860 million earmarked for North America.

- February 2025: Maersk announced a fourth United States cold-storage warehouse near the Port of New York and New Jersey to meet rising refrigerated cargo demand.

- January 2025: Americold invested USD 127 million in a new automated cold store in Houston, Texas, prioritising energy-efficient technologies.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the cold chain logistics market as the end-to-end revenue generated from temperature-controlled storage, transportation, and value-added handling of perishable food, biopharmaceutical, and specialty chemical cargo that must remain within chilled, frozen, or ultra-low ranges from origin through final delivery. According to Mordor Intelligence, this includes public and private refrigerated warehouses, dedicated reefer fleets across road, rail, sea, and air, plus ancillary services such as blast-freezing and GDP compliance audits.

Scope exclusion: we exclude domestic ice-cream street vending, HVAC equipment sales, and one-time dry-ice packaging rentals.

Segmentation Overview

- By Service Type

- Refrigerated Storage

- Public Warehousing

- Private Warehousing

- Refrigerated Transportation

- Road

- Rail

- Sea

- Air

- Value-Added Services

- Refrigerated Storage

- By Temperature Type

- Chilled (0–5 °C)

- Frozen (-18–0 °C)

- Ambient

- Deep-Frozen / Ultra-Low (more than -20 °C)

- By Application

- Fruits & Vegetables

- Meat & Poultry

- Fish & Seafood

- Dairy & Frozen Desserts

- Bakery & Confectionery

- Ready-to-Eat Meals

- Pharmaceuticals & Biologics

- Vaccines & Clinical Trial Materials

- Chemicals & Specialty Materials

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews and surveys with warehouse operators, pharma quality managers, quick-commerce grocery platforms, and reefer-OEM specialists across North America, Europe, and Asia Pacific. Insights on pallet-turn velocity, lane pricing, and regulatory pain points filled data gaps and calibrated scenario assumptions.

Desk Research

We first screen open-access tier-1 sources such as UN Comtrade shipment codes, USDA cold-store capacity reports, Eurostat road-freight datasets, and WHO GDP guidelines to map product flows and regulatory triggers. Trade bodies like the Global Cold Chain Alliance, regional customs bulletins, and peer-reviewed journals on refrigeration losses further clarify demand pockets. Company 10-Ks, investor decks, and logistics tender notices feed price and capacity benchmarks. Select paid databases (D&B Hoovers for operator revenues and Dow Jones Factiva for deal pipelines) complement public data. The sources listed illustrate the breadth; many others underpin our cross-checks.

Market-Sizing & Forecasting

A hybrid top-down build starts from production, import, and export tonnage of temperature-sensitive goods, which is then priced using region-specific average logistics spend ratios. Results are corroborated through selective bottom-up checks, sampled warehouse pallet rates, reefer lane tariffs, and 3PL contract values to fine-tune totals. Key model drivers include urban e-grocery penetration, biologics clinical-trial pipeline size, refrigerated warehouse utilization, fuel price indexation, and refrigerant phase-out costs. Forecasts employ multivariate regression with ARIMA overlays to reflect both structural demand and cyclical fuel or commodity swings. Where bottom-up estimates show data voids, proxy ratios from matched corridors are applied and later validated with panel experts.

Data Validation & Update Cycle

Outputs pass variance screens against independent freight indices and customs tonnage, followed by senior analyst peer review. We refresh the model annually, triggering interim updates after material events such as refrigerant regulation changes or mega-mergers, and a final sense check occurs just before report release.

Why Mordor's Cold Chain Logistics Baseline Inspires Greater Confidence

Published estimates often diverge because firms pick different service mixes, currency bases, and refresh cadences. Mordor's disciplined scope alignment, variable vetting, and dual-path modeling temper extremes, giving executives a balanced starting point.

Key gap drivers include whether refrigerated last-mile flows are counted, how aggressively future warehouse capacity is priced, and the cadence at which biologics demand shocks are folded into models.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 361.37 B (2025) | Mordor Intelligence | - |

| USD 316.34 B (2024) | Global Consultancy A | Excludes integrated 3PL value-added fees and applies >20 % CAGR without supply-side stress checks |

| USD 228.30 B (2024) | Industry Association B | Counts warehousing revenue only, omits chilled transport lanes |

| USD 324.85 B (2024) | Trade Journal C | Uses pallet-rate x warehouse stock method, ignores cross-border freight mark-ups |

These contrasts show that our model, anchored to observable tonnage and validated tariffs, delivers a transparent baseline stakeholders can trace, replicate, and confidently use for strategic planning.

Key Questions Answered in the Report

What is the current size of the cold chain logistics market?

The cold chain logistics market stands at USD 383.46 billion in 2026 and is projected to reach USD 515.79 billion by 2031 at a 6.12% CAGR.

Which service type is growing fastest within the cold chain logistics market?

Refrigerated transportation leads growth with an 6.88% CAGR as e-commerce and quick-commerce accelerate demand for time-critical deliveries.

Why is ultra-low temperature capacity expanding so rapidly?

Distribution of mRNA vaccines, cell therapies, and other biologics that require storage below -70 °C is driving a 8.22% CAGR in the deep-frozen segment.

Which region offers the strongest growth outlook?

Asia-Pacific shows the highest 8.05% CAGR due to rising disposable incomes, rapid urbanisation, and government incentives to reduce post-harvest losses.

How are regulations influencing technology investment?

Rules such as the United States FSMA 204 mandate real-time traceability, prompting widespread deployment of IoT sensors and telematics that improve compliance and operational efficiency.

Who are the leading players in the cold chain logistics market?

Lineage Logistics and Americold head the field, jointly controlling about 4.4 billion ft³ of temperature-controlled space and focusing on automation, sustainability, and strategic acquisitions.

Page last updated on: