Asia-Pacific Healthcare Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

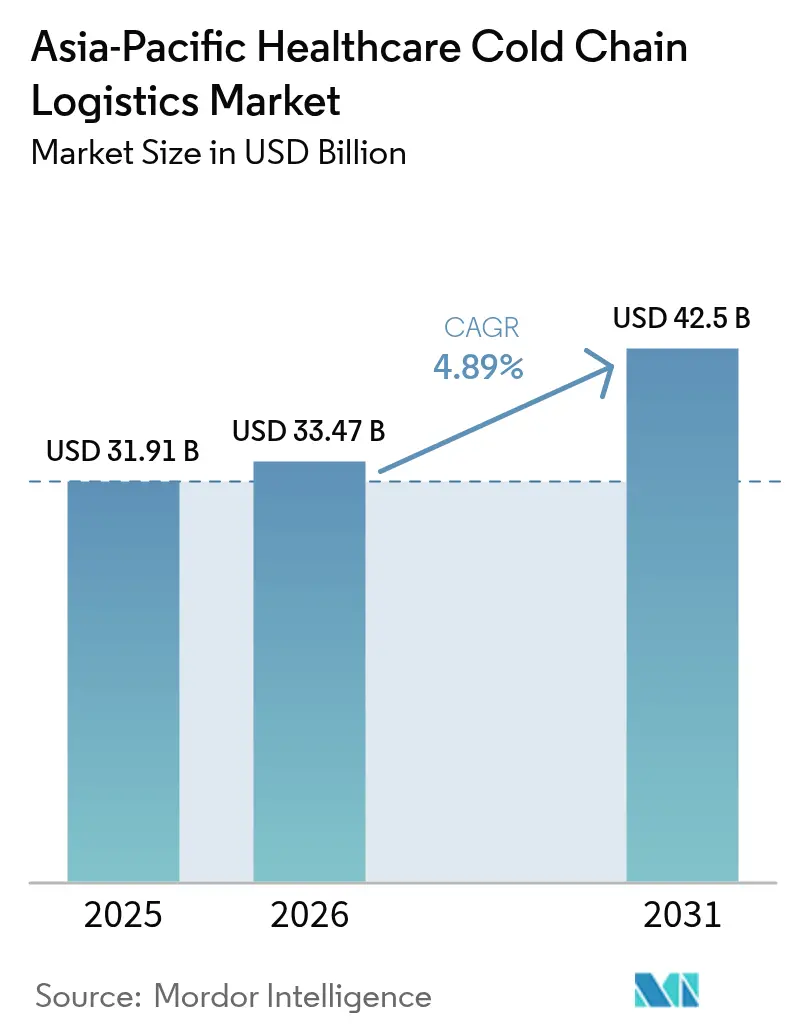

| Base Year Market Size (2025) | USD 31.91 Billion |

| Market Size (2026) | USD 33.47 Billion |

| Market Size (2031) | USD 42.5 Billion |

| Growth Rate (2026 - 2031) | 4.89% CAGR |

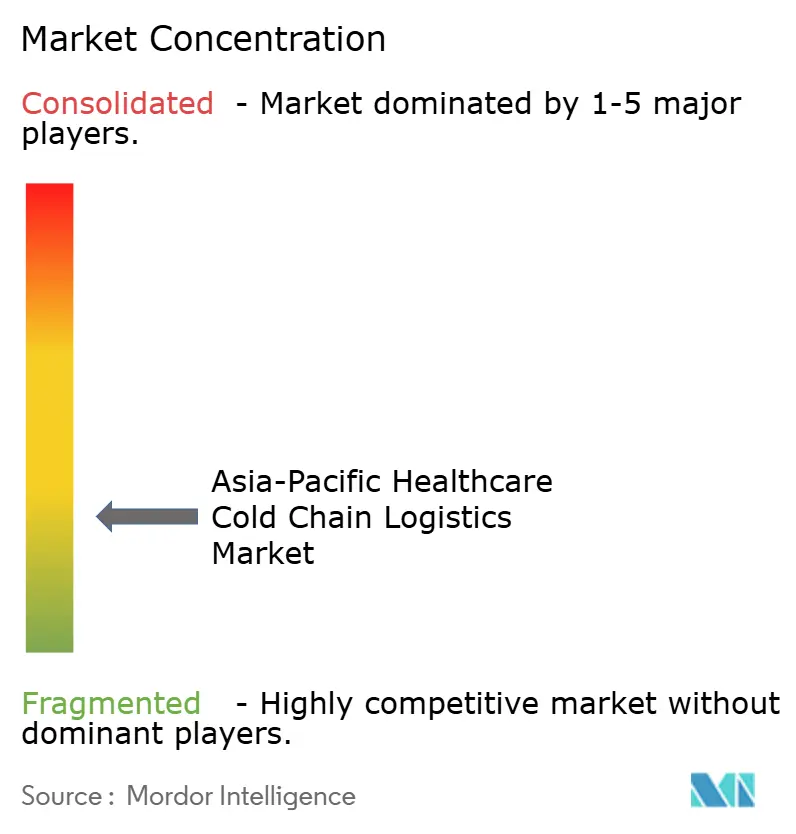

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Healthcare Cold Chain Logistics Market Analysis by Mordor Intelligence

The Asia-Pacific Healthcare Cold Chain Logistics Market size is expected to grow from USD 31.91 billion in 2025 to USD 33.47 billion in 2026 and is forecast to reach USD 42.5 billion by 2031 at 4.89% CAGR over 2026-2031.

Demand gains stem from biologics expansion, post-pandemic vaccine roll-outs, and government-backed supply-chain resilience programs. Rising therapeutic complexity in cell and gene therapy, the ongoing GLP-1 drug boom, and stricter Good Distribution Practice (GDP) rules are set to keep capacity tight and pricing firm across transport modes. Stakeholders also capitalize on AI-enabled lane-risk modeling that trims temperature excursions, while sovereign health-security agendas accelerate infrastructure spending in China, India, and Southeast Asia.

Key Report Takeaways

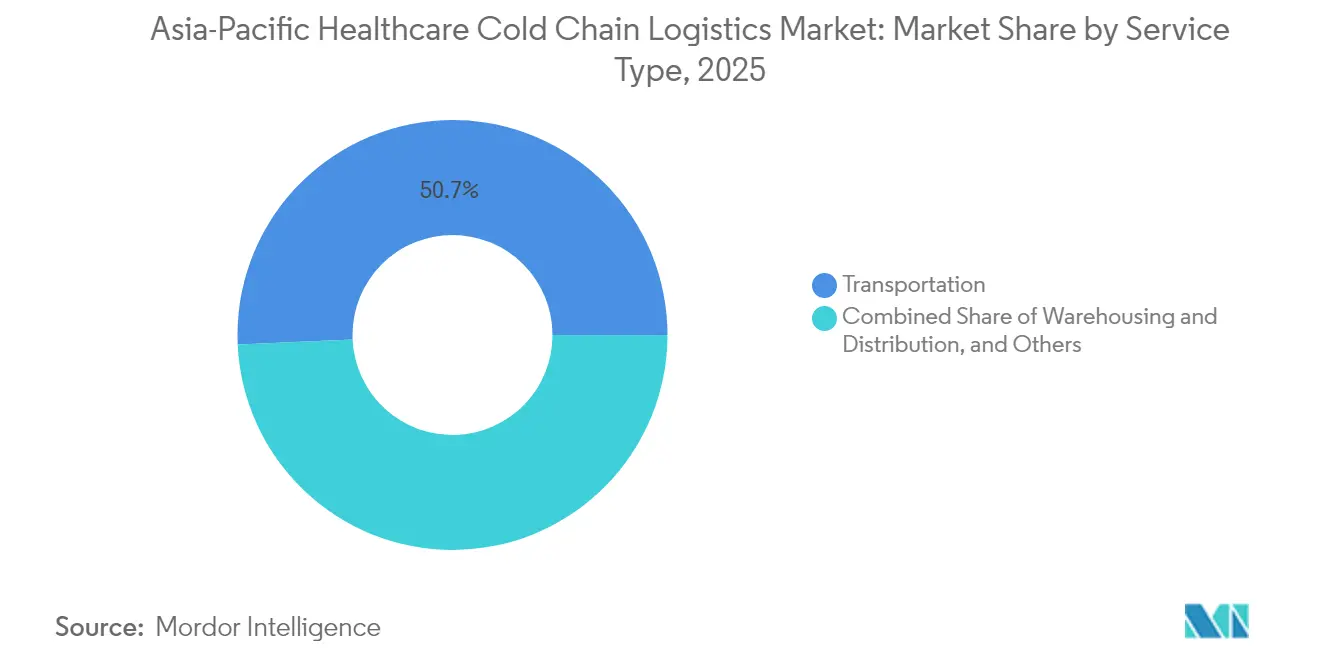

- By services, transportation held 50.70% of Asia Pacific healthcare cold chain logistics market share in 2025, while value-added services are projected to post the fastest 4.95% CAGR to 2031.

- By temperature type, chilled storage controlled 40.60% of Asia Pacific healthcare cold chain logistics market size in 2025; deep-frozen and ultra-low solutions are forecast to expand at a 4.12% CAGR through 2031.

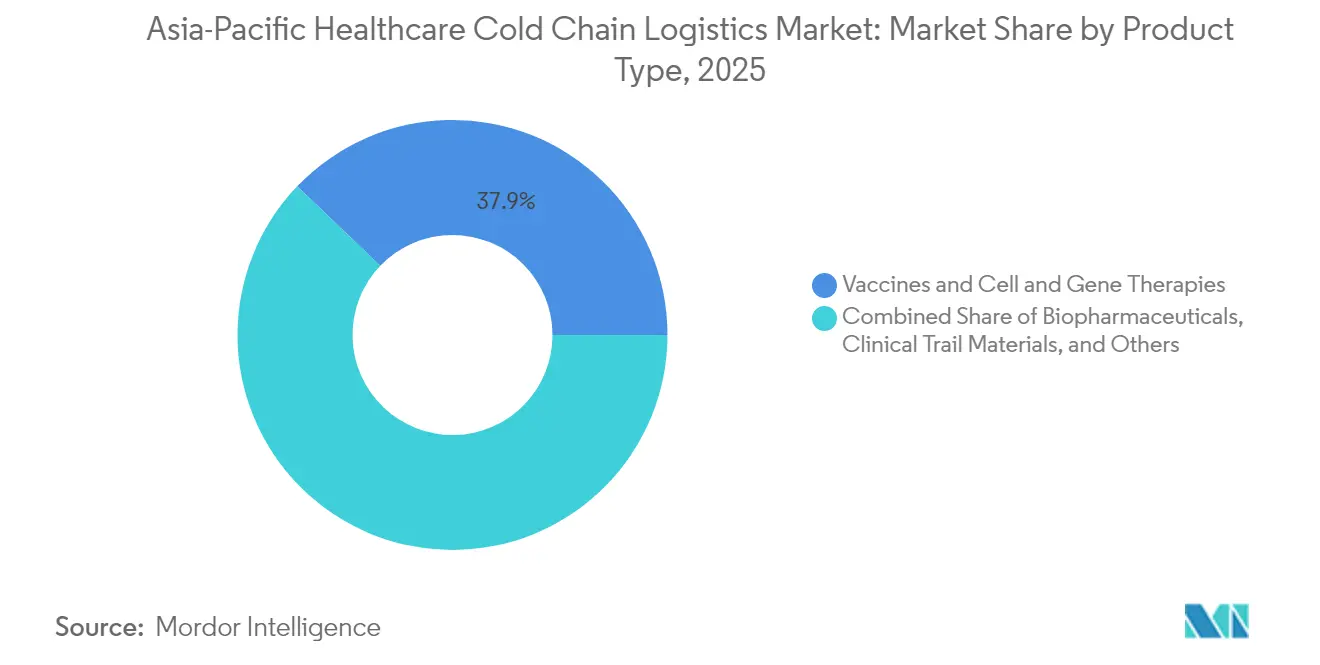

- By product, vaccines plus cell & gene therapies combined for 37.85% of Asia Pacific healthcare cold chain logistics market share in 2025, with cell & gene therapies alone advancing at a 5.62% CAGR between 2026-2031.

- By geography, China accounted for a dominant 38.70% share in 2025, whereas India is slated for the swiftest 5.99% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Asia representing one of the more structurally developed among them. The global report on healthcare cold chain logistics market by Mordor Intelligence reflects how these regional layers combine into a single system.

Asia-Pacific Healthcare Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong vaccine immunization programs post-COVID-19 | +0.8% | Global APAC, with concentration in India, Indonesia, Philippines | Medium term (2-4 years) |

| Accelerated biologics & cell-/gene-therapy pipelines | +0.9% | Japan, South Korea, Singapore, Australia core markets | Long term (≥ 4 years) |

| Government mandates on GDP-compliant distribution | +0.6% | China, India, Thailand regulatory-driven adoption | Medium term (2-4 years) |

| Expansion of GDP-certified pharma hubs | +0.5% | Singapore, Malaysia, Vietnam emerging hubs | Long term (≥ 4 years) |

| AI-enabled lane-risk modelling for shipment integrity | +0.4% | China, Japan, South Korea technology leaders | Short term (≤ 2 years) |

| Rapid GLP-1 drug boom needing 2-8 °C logistics | +0.7% | Global APAC with premium markets first adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Vaccine-Immunization Programs Post-COVID-19

Cold chain infrastructure built for pandemic vaccines is now redeployed for routine pharmaceuticals across the Asia Pacific healthcare cold chain logistics market. India targets USD 17 billion in vaccine revenue for 2025 amid bioeconomy expansion, supported by new vial-handling hubs, GDP-certified cross-docks, and large-scale fill-finish lines[1]“DTI Pushes for More Efficient Logistics, Supply Chain,” Kris Crismundo, pna.gov.ph. The Philippines’ Clark Freeport zone attracts more than USD 1 billion in logistics capital, providing dual-use freezer capacity for routine immunization drives and future outbreak response[2]“Marcos Says New Maersk Mega-Facility to Boost PH Logistics System,” Darryl Esguerra, pna.gov.ph. DHL’s global EUR 2 billion (USD 2.20 billion) healthcare program allocates 25% to Asia Pacific, underscoring corporate confidence in sustained biologics flow. These investments ensure predictive temperature monitoring, lane qualification, and redundancy, anchoring service reliability for vaccines, insulin, and specialty injectables. Governments, meanwhile, lock in long-term procurement contracts that stabilize volume demand and drive network density.

Accelerated Biologics & Cell/Gene-Therapy Pipelines

Japan cleared 43 new drugs in 2025, several being gene therapies that require below--20 °C storage, spurring specialized capacity additions at port-adjacent warehouses and express courier depots. South Korea’s KoBIA supports export-ready biologics clusters near Incheon, pairing GMP manufacturing with GDP-compliant distribution corridors. Singapore’s clinical-trial ecosystem relies on same-day “white-glove” transport for autologous CAR-T cells, pushing providers to integrate cryogenic dewars, data loggers, and chain-of-identity blockchain tags. Australia leverages its proximity to Asian pharma hubs, rerouting long-haul biologics freight through Sydney and Melbourne for time-critical last-mile dispatch. Collectively, these shifts elevate demand for ultra-low pallets, passive PCM packaging, and validated dry-shipper fleets, reinforcing the Asia Pacific healthcare cold chain logistics market.

Government Mandates on GDP-Compliant Distribution

Regulators tighten oversight to curb temperature excursions and counterfeit risk, reshaping competitive dynamics in the Asia Pacific healthcare cold chain logistics market. China’s revised GDP code compels fleet retrofits, warehouse mapping, and digital audit trails, prompting consolidation among smaller 3PLs. Thailand harmonizes with PIC/S standards, catalyzing multinational investment in Bangkok-based pharma hubs. India ties export incentives to documented GDP compliance, nudging logistics partners toward ISO 23412 certification and real-time IoT telemetry. These mandates raise entry barriers but offer margin upside to incumbents able to absorb capital outlays for multi-temperature vehicles, redundant power, and 24/7 control-tower visibility.

AI-Enabled Lane-Risk Modeling for Shipment Integrity

Platform providers harness AI to predict route-specific hazards such as customs delays, tarmac dwell, and micro-climate shifts, reducing spoilage and insurance claims. Chinese integrators deploy digital twins of cross-border lanes, while Japanese forwarders install machine-learning engines in warehouse management systems to refine pick-cycle timing. South Korea outfits reefer trucks with edge-computing gateways that flag compressor anomalies before failure, enabling pre-emptive maintenance. Early adopters report temperature excursion cuts of 15-20%, translating into higher service-level attainment and preference among biotech shippers. The technology trend narrows performance gaps and sets new baselines for evaluations inside tender processes across the Asia Pacific healthcare cold chain logistics market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of GDP-qualified reefer drivers in ASEAN | -0.4% | Indonesia, Thailand, Philippines, Vietnam | Short term (≤ 2 years) |

| High inter-island freight costs in archipelagic nations | -0.3% | Indonesia, Philippines primary impact | Medium term (2-4 years) |

| China's fluorocarbon-phase-out raising CAPEX | -0.3% | China domestic, spillover to regional suppliers | Long term (≥ 4 years) |

| Vial-level e-pedigree compliance inflating costs | -0.2% | Global APAC with premium markets leading adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of GDP-Qualified Reefer Drivers in ASEAN

Indonesia and Thailand expand paved road length yet struggle to staff trailers with GDP-trained personnel, creating a skills gap that constrains capacity during peak vaccine seasons. Certification courses demand mastery of SOPs for temperature mapping, data-logger handling, and deviation reporting, lengthening onboarding cycles compared to dry-van trucking. The Philippine market mirrors the challenge even as Clark Freeport adds modern docks; higher wages lure drivers into e-commerce, leaving fewer for pharma. Logistics firms therefore invest in accelerated training, telematics-enabled driver coaching, and retention bonuses, but near-term tightness persists, shaving throughput and damping the Asia Pacific healthcare cold chain logistics market’s potential.

High Inter-Island Freight Costs in Archipelagic Nations

Moving a 2-8 °C pallet from Jakarta to Manado can be 40% costlier than a similar mainland lane because of feeder vessel hand-offs, scarce reefer plugs, and limited back-haul. The Philippines faces analogous hurdles, with multi-leg barge-truck chains raising landed costs for temperature-controlled medicines. Governments pledge port upgrades and cabotage reforms, yet timelines stretch, leaving pharmaceutical importers reliant on premium airfreight. Elevated logistics spend squeezes smaller generics firms and complicates public-sector tender budgets, muting growth in peripheral provinces of the Asia Pacific healthcare cold chain logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Services: Transportation Dominates Amid Value-Added Growth

Transportation commanded 50.70% of Asia Pacific healthcare cold chain logistics market share in 2025, reflecting the indispensability of road, air, sea, and rail movement across 35,000 kilometers of maritime and land borders. Airfreight retains primacy for time-critical biologics, with Korean Air alone holding 6% of global temperature-sensitive air cargo lift. Sea logistics cater to bulk vaccines and IV solutions moving from Chinese or Indian factories to ASEAN buyers, while China’s burgeoning high-speed rail corridors support 24-hour domestic pharma transits. Warehousing and distribution underpin long-haul nodes, yet value-added services temperature-validated packaging, regulatory paperwork, and control-tower analytics are slated to outpace at a 4.95% CAGR, capturing share as shippers outsource non-core compliance tasks.

Provider differentiation hinges on multimodal orchestration, GDP op-ex discipline, and tech-enabled visibility. UPS expanded cold-chain capacity by 22,000 square meters across Singapore and Australia in 2024, embedding on-site labs for pre-conditioned parcel packs. DHL integrates lane-risk dashboards into its mySupplyChain portal, delivering predictive ETA and excursion alerts. Start-ups supply SaaS overlays that consolidate passive and active tag data, enabling real-time interventions a service tier increasingly demanded across the Asia Pacific healthcare cold chain logistics market.

By Temperature Type: Chilled Storage Leads Ultra-Low Expansion

Chilled solutions between 0 °C and 5 °C represented 40.60% of Asia Pacific healthcare cold chain logistics market size in 2025, driven by the dominance of vaccines, insulin, and GLP-1 agonists that require narrow 2-8 °C ranges. Frozen products at –18 °C to 0 °C continue serving classical biologics, yet the ultra-low sub-segment below –20 °C registers a brisk 4.12% CAGR through 2031, propelled by cell and gene therapy clinical trial volumes. Cryoport’s dry-shipper technology, which maintains –150 °C for 10 days, is in wide adoption among CAR-T sponsors shipping patient-specific doses.

Facility upgrades focus on redundant power, low-GWP refrigerants, and modular blast freezers to handle batch variability. China’s refrigerant phase-out inflates CAPEX, yet accelerates adoption of R32 and CO2 trans-critical systems that offer lower energy intensity, aligning with ESG goals. Across the Asia Pacific healthcare cold chain logistics market, providers balance CAPEX efficiency with stringent mapping, pushing partnerships with OEMs for smart compressor analytics and rapid defrost cycles that preserve shelf life integrity.

By Product: Vaccines Lead While Cell & Gene Therapies Surge

Vaccines and cell-plus-gene therapies together held 37.85% of Asia Pacific healthcare cold chain logistics market share in 2025, reflecting residual immunization runs and the rise of personalized medicine. Within that, cell & gene therapies alone are expected to log a leading 5.62% CAGR, necessitating validated cryo-packaging, GPS sensors, and chain-of-identity protocols. Biopharmaceuticals, including monoclonal antibodies and biosimilars, retain the largest absolute revenue slice, sustained by patent-cliff dynamics that trigger biosimilar launches through 2030.

Clinical trial materials grow on the back of 2,500 ongoing Phase III studies in Asia-Pacific sites, each demanding comparator drugs, placebo returns, and depot management. Diagnostic reagents leverage chilled networks expanded during COVID-19, while blood products require compliance with hemovigilance rules, driving specialized insulated totes. Collectively, product diversification increases lane complexity, fueling demand for integrated 4PL orchestration in the Asia Pacific healthcare cold chain logistics market.

By End User: Hospitals Drive Growth, Biotech Accelerates

Hospitals and retail pharmacies together accounted for 28.60% of Asia Pacific healthcare cold chain logistics market size in 2025 as the primary dispensing points for temperature-sensitive drugs. The group’s cold storage footprints expand as outpatient infusions spread beyond tertiary centers into suburban clinics. Biotech and biosimilar manufacturers, however, are projected to register the fastest 5.03% CAGR on surging outsourcing needs for time-critical export lanes and return-logistics of clinical samples. India now hosts more than 800 biotech firms requiring validated packaging and customs-bonded freezers along the Delhi-Mumbai corridors.

Distributors and wholesalers consolidate to capture volume across fragmented ASEAN channels, adopting RFID-based FIFO picking for GDP compliance. Pharmaceutical manufacturers maintain dedicated captive fleets for high-margin blockbuster biologics, yet even they turn to 3PL partners for end-market last-mile coverage in remote islands. This multiplicity of end-user profiles intensifies service customization in the Asia Pacific healthcare cold chain logistics market.

Geography Analysis

China owned 38.70% of Asia Pacific healthcare cold chain logistics market share in 2025, reflecting unmatched manufacturing scale and GDP-rule enforcement that fosters consolidation among 15,000 licensed pharma carriers. Domestic providers adopt AI-powered route optimization and AGV-enabled warehouses to offset rising labor costs, while R32 refrigerant prices that more than doubled in 2025 incentivize greener cascade systems. Mandatory electronic pedigree serialization extends traceability, setting a benchmark later mirrored by ASEAN states.

India delivers the region’s fastest 5.99% CAGR through 2031, supported by a bioeconomy projected to reach USD 300 billion, of which vaccines alone aim for USD 17 billion in 2025 revenue. Production-linked incentives channel capital into new fill-finish lines and associated GDP warehouses near Hyderabad, Ahmedabad, and Pune. The U.S. Biosecure Act redirects biologics outsourcing from Chinese entities toward Indian CDMOs, requiring export-grade cryo-logistics corridors with redundant last-mile monitoring.

Japan, South Korea, and Australia collectively command a quarter of Asia Pacific healthcare cold chain logistics market size. Japan’s approval of 43 novel drugs in 2025 includes four gene therapies, catalyzing cryogenic build-outs at Narita and Kansai airports. South Korea’s KoBIA maps a national “Bio Cold Chain Belt” linking Seoul, Incheon, and Busan via multi-temperature railcars, readying for CAR-T scale-out. Australia exploits time-zone overlap between U.S. West Coast and Asia supply chains, positioning Sydney as a trans-shipment hub with 24/7 pharma-devoted airside coolers.

Southeast Asian markets add vibrancy yet complexity. Singapore’s Changi pharma corridors achieve CEIV Pharma recertification and attract regional cross-docks, while Vietnam ramps up GDP adoption to underpin vaccine import programs. Archipelagic constraints in Indonesia and the Philippines elevate per-unit cold chain costs by up to 40%, steering logistics strategies toward regional consolidation hubs in Jakarta and Calamba. Government port and road investments gradually narrow the gap but will only partly alleviate cost headwinds through 2030 across the Asia Pacific healthcare cold chain logistics market.

Mordor Intelligence provides coverage of the healthcare cold chain logistics market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Competition remains moderately fragmented as global giants vie with agile regional specialists. DHL, UPS, and FedEx wield vast networks, but local champions such as SF Express, Yusen, and Kerry Logistics leverage domestic customs fluency and short-notice fleet redeployment. DHL earmarked EUR 2 billion (USD 2.20 billion) for healthcare globally by 2030, dedicating a quarter to Asia Pacific for new GDP hubs, multi-modal connectors, and embedded control towers. UPS complements its Singapore and Sydney expansions with Hyderabad’s cross-dock that offers +2 °C to +8 °C and +15 °C to +25 °C zones in one roof, improving lane density toward South Asia[3]“Air Freight News Week 05 2025,” Extrans Global, extransglobal.com.

Acquisitions fast-track vertical integration: UPS bought Andlauer Healthcare for USD 1.6 billion, securing Canadian vaccine expertise now imported into Asia route designs; DHL absorbed CRYOPDP for USD 2.2 billion to access ultra-low know-how. Meanwhile, tech-centric entrants deploy blockchain-time-stamping and drone-assisted last mile, aiming to disrupt high-margin specialty lanes. Yet GDP compliance costs, rising refrigerant CAPEX, and trained-driver scarcity protect scale incumbents and deter pure digital challengers.

Strategic thrusts revolve around ESG compliance, automation, and risk management. Providers retrofit fleets with solar-assisted reefer units, install RFID beacons for 100% pallet visibility, and hedge against fuel volatility through optimized multimodal meshes. Regional white-space remains in archipelagic navigation, AI-based preventive maintenance, and integrated cold-chain-financial insurance offerings. Such innovation pipelines ensure healthy rivalry but no single player exceeds 15% regional share, keeping the Asia Pacific healthcare cold chain logistics market competitively balanced.

Asia-Pacific Healthcare Cold Chain Logistics Industry Leaders

DHL Group

Yusen Logistics

SF Express

JWD Group

Nippon Express

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DHL Group announces EUR 2 billion (USD 2.20 billion) investment by 2030 in healthcare logistics globally, with 25% allocated to Asia Pacific region for GDP-certified pharma hubs, cold chain capacity expansion, and temperature-controlled transport solutions.

- April 2025: Okayama CONNECT Logistics Center, the largest cold storage warehouse in Japan’s Chugoku and Shikoku regions, completes construction featuring advanced energy-efficient technologies and lithium-ion battery emergency power systems.

- March 2025: Probiotec finishes a state-of-the-art distribution center in Sydney’s The YARDS estate, enhancing temperature-sensitive healthcare product distribution capabilities in Australia.

- February 2025: Toll Group announces new healthcare facility in Perth, expanding cold chain logistics infrastructure to support Western Australia’s pharmaceutical distribution requirements.

Asia-Pacific Healthcare Cold Chain Logistics Market Report Scope

Healthcare Cold chain logistics is the technology and process that allows temperature-sensitive goods and products, such as pharmaceutical drugs, to be transported safely throughout the supply chain.It impacts every stage of the supply chain, from purchase to transportation, storage, and last-mile delivery.

The Asia-Pacific healthcare cold chain logistics market is segmented by product (biopharmaceuticals, vaccines, and clinical trial materials), services (transportation, storage, packaging, and labeling), end user (hospitals and clinics, and pharmaceutical, biopharmaceutical, and biotechnology companies), and country (China, Japan, India, and the Rest of Asia-Pacific). The report offers market size and forecast values (in USD billions) for all the above segments.

| Transportation | Road |

| Air | |

| Sea | |

| Rail | |

| Warehousing and Distribution | |

| Value-added Services and Others |

| Chilled (0-5 °C) |

| Frozen (-18-0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

| Biopharmaceuticals |

| Vaccines and Cell and Gene Therapies |

| Clinical Trial Materials |

| Diagnostic and Laboratory Products |

| Blood and Blood Products |

| Others |

| Pharmaceutical Manufacturers |

| Biotech and Biosimilar Manufacturers |

| Hospitals and Retail Pharmacies |

| Healthcare Distributors and Wholesalers |

| Others |

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Thailand |

| Indonesia |

| Singapore |

| Vietnam |

| Rest of ASEAN |

| By Services | Transportation | Road |

| Air | ||

| Sea | ||

| Rail | ||

| Warehousing and Distribution | ||

| Value-added Services and Others | ||

| By Temperature Type | Chilled (0-5 °C) | |

| Frozen (-18-0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Product | Biopharmaceuticals | |

| Vaccines and Cell and Gene Therapies | ||

| Clinical Trial Materials | ||

| Diagnostic and Laboratory Products | ||

| Blood and Blood Products | ||

| Others | ||

| By End User | Pharmaceutical Manufacturers | |

| Biotech and Biosimilar Manufacturers | ||

| Hospitals and Retail Pharmacies | ||

| Healthcare Distributors and Wholesalers | ||

| Others | ||

| By Country (Value) | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Thailand | ||

| Indonesia | ||

| Singapore | ||

| Vietnam | ||

| Rest of ASEAN |

Key Questions Answered in the Report

How large is the Asia Pacific healthcare cold chain logistics market in 2026?

The Asia Pacific healthcare cold chain logistics market size is USD 33.47 billion in 2026 and is projected to reach USD 42.5 billion by 2031.

What CAGR is expected for the sector through 2031?

The market is set to register a 4.89% CAGR between 2026 and 2031.

Which service segment has the greatest share across Asia Pacific?

Transportation services hold 50.70% of regional share owing to essential road, air, sea, and rail movements.

Why is India forecast to grow faster than other countries?

India’s biosimilar manufacturing expansion, vaccine export ambitions, and incentives under national schemes drive a 5.99% CAGR through 2031.

What temperature segment is expanding most rapidly?

Deep-frozen and ultra-low logistics below –20 °C are growing at 4.12% CAGR, propelled by cell and gene therapy pipelines.

Which product category is the most dynamic?

Cell & gene therapies post the highest 5.62% CAGR as personalized medicine adoption accelerates.

Page last updated on: