India Green Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

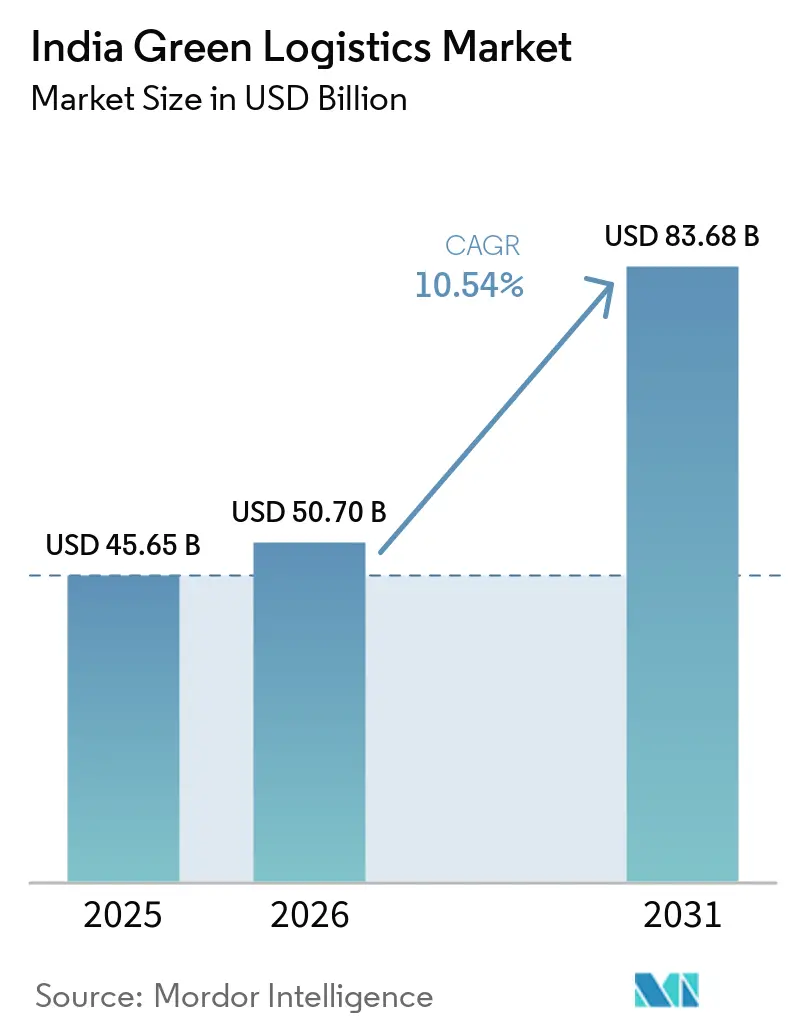

| Base Year Market Size (2025) | USD 45.65 Billion |

| Market Size (2026) | USD 50.70 Billion |

| Market Size (2031) | USD 83.68 Billion |

| Growth Rate (2026 - 2031) | 10.54% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Green Logistics Market Analysis by Mordor Intelligence

The India green logistics market size is expected to increase from USD 45.65 billion in 2025 to USD 50.70 billion in 2026 and reach USD 83.68 billion by 2031, growing at a CAGR of 10.54% over 2026-2031.

The India green logistics market is moving into a more formal operating phase, as freight decarbonization is now tied to compliance, network design, and procurement decisions rather than solely to voluntary sustainability goals. Infrastructure planning is also becoming more supportive, as PM Gati Shakti has integrated transport, utility, and industrial planning on a single geospatial platform, enabling road, rail, port, and waterway investments to work together more efficiently. This has helped the India green logistics market benefit from the same projects that are lowering logistics costs, enabling efficiency and emissions reductions to advance through the same network upgrades. Competition is also tightening as large global and domestic operators invest in cleaner fleets, rail-linked cargo platforms, cold chain assets, and low-emission facilities. At the same time, mid-sized specialists use focused corridor strategies to win contracts. At the same time, the India green logistics market still faces clear constraints in charging density, access to alternative fuels, land approvals, and the capital burden on smaller operators, which keeps expansion uneven across corridors and city tiers.

Key Report Takeaways

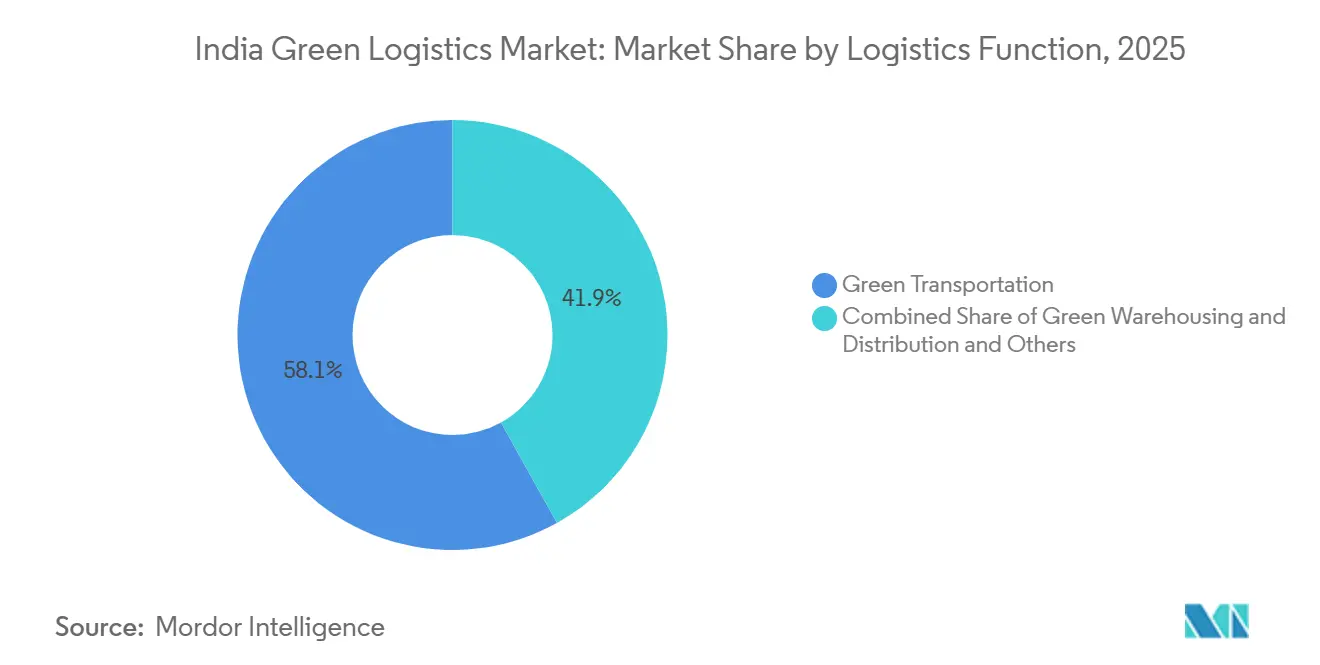

- By logistics function, green transportation led with 58.07% of India green logistics market share in 2025, while green value-added services and others are forecast to expand at a 15.13% CAGR through 2031.

- By fuel and energy type, electric-powered logistics held 54.88% of India green logistics market size in 2025, while hydrogen-powered logistics recorded the highest projected CAGR at 17.49% through 2031.

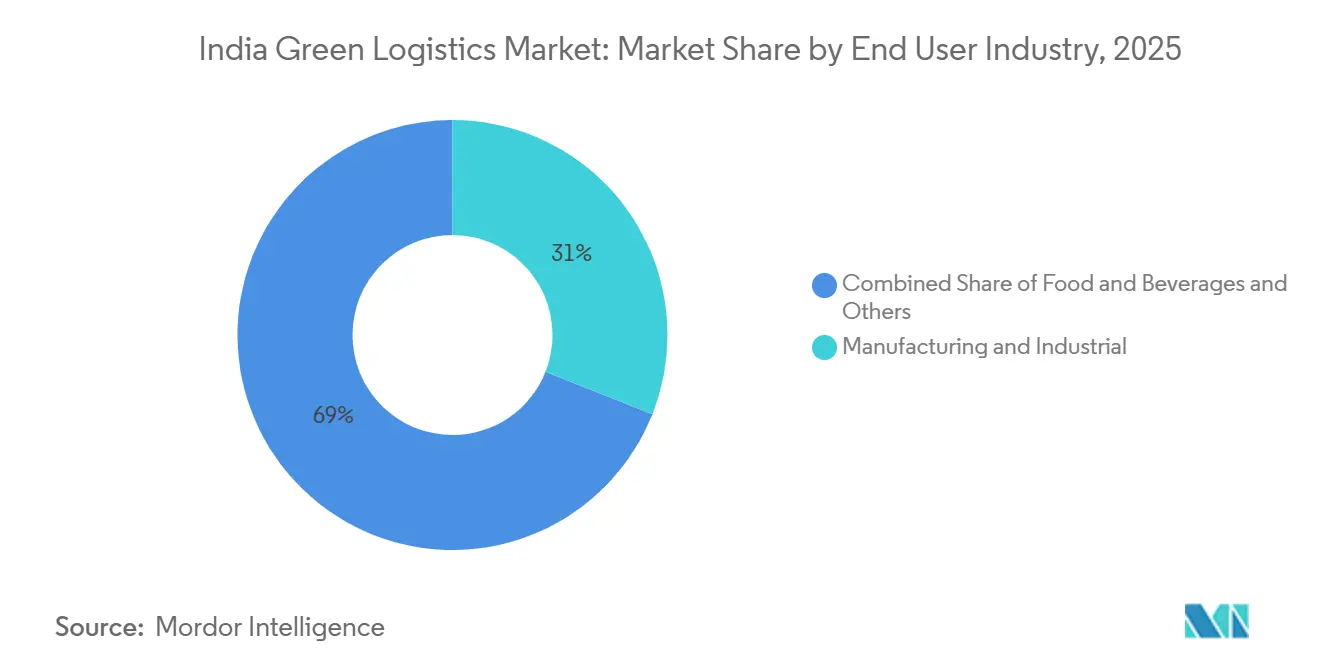

- By end-user industry, manufacturing and industrial accounted for 31% of India green logistics market size in 2025, while healthcare and pharmaceuticals is advancing at a 15.96% CAGR through 2031.

- By region, the West held 28.40% of India green logistics market share in 2025, while the South is projected to grow at a 14.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Green Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising ESG-Led Freight Procurement | +1.8% | National, strongest in export-heavy corridors in the West and South | Medium term (2-4 years) |

| Government-Backed Multimodal Decarbonization Push | +1.9% | National, anchored in the Delhi-Mumbai Industrial Corridor and Eastern DFC zones. | Medium term (2-4 years) |

| Rapid Electrification of Last-Mile and Urban Freight | +2.1% | Urban metros first, Tier-1 cities, spillover to Tier-2 | Short term (≤ 2 years) |

| Solarized and Energy-Efficient Warehousing Adoption | +1.2% | National, institutional-grade parks in the West, South, and NCR | Long term (≥ 4 years) |

| Carbon Reporting Pressure From Export-Oriented Supply Chains | +1.3% | National, the highest impact on export-linked manufacturing and chemical corridors | Medium term (2-4 years) |

| Demand for Low-Emission Cold Chain Logistics | +1.4% | South for pharma, West for food processing, North for agri exports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising ESG-Led Freight Procurement

Large enterprises in the India green logistics market are now treating freight decarbonization as a procurement standard, not as an optional ESG add-on. Under SEBI’s BRSR Core framework, value chain disclosure obligations widened voluntarily for the top 250 listed entities from FY 2025-26, pushing companies to look more closely at supplier-side emission intensity across large parts of their operating base. Once a shipper begins measuring freight-related Scope 3 emissions, transport partners must demonstrate cleaner operations, improved data capture, and credible reporting to retain access to the contract. This is evident in the way major consumer companies have begun using EV fleets, rail transport, and renewable energy-backed operations as practical logistics choices rather than public relations signals. The result is that the India green logistics market is opening up more space for mid-sized green carriers that can document their carbon performance, even when they do not match the national scale of older diesel-led operators.

Government-Backed Multimodal Decarbonization Push

The India green logistics market is benefiting from a policy environment that now links infrastructure efficiency with lower transport emissions. PM Gati Shakti has integrated 57 central ministries and departments onto a single geospatial platform with more than 1,700 data layers, improving the planning of roads, rail lines, ports, utilities, and industrial zones. Budget and corridor measures have extended that approach into freight through new Dedicated Freight Corridors, added national waterway plans, and stronger coastal cargo targets, which together support a cleaner modal mix over time. Gati Shakti Cargo Terminals had already attracted private investment by early 2026. They were associated with large estimated carbon savings from rail-led freight shifts, which shows why operators now see green logistics assets as commercially usable infrastructure rather than experimental platforms[1]"Gati Shakti Multi-Modal Cargo Terminals (GCTs): Driving India's Logistics Transformation." indianindustryplus.com.. This alignment matters because the India green logistics market can expand faster when the same public investment pipeline supports cost reduction and decarbonization.

Rapid Electrification of Last-Mile and Urban Freight

Urban delivery is one of the clearest near-term growth engines for the India green logistics market, as the economics of commercial fleets on short-haul routes are improving. The Ministry of Heavy Industries launched the country’s first dedicated incentive support for electric trucks under PM E-DRIVE in July 2025, within a broader program allocation of INR 10,900 crore (USD 1.3 billion). Large operators are now moving beyond pilots, with Delhivery’s agreement with Zen Mobility supporting a multi-year rollout across Tier-1, Tier-2, and Tier-3 cities, and Amazon India operating more than 12,000 EVs across 500+ cities in 2026. Depot-based charging is one reason adoption is moving faster in logistics than in private mobility because fleet operators can plan overnight charging, route cycles, and maintenance windows in a controlled setting. That operating model is making the India green logistics market more investable in urban freight, especially where uptime and delivery density matter more than long-range flexibility.

Solarized and Energy-Efficient Warehousing Adoption

Warehousing is becoming a more important value pool in the India green logistics market as newer logistics parks are built with energy efficiency and renewable integration from the start. Certified green warehouse stock stood at 65 million ft² in 2024, and this could rise to 270 million ft² by 2030, while Grade A warehouse stock had already expanded 2.5 times between 2019 and 2024 to 238 million ft². This shift matters because new facilities can absorb solar, smart energy management, and higher operating standards at a lower incremental cost than retrofit-heavy legacy sites. Mahindra Logistics’ renewable energy-enabled warehouse for Cummins India in Phaltan shows that industrial clients are now specifying sustainability features as part of contract warehousing requirements rather than treating them as optional upgrades[2]Source: Mahindra Logistics, “Mahindra Logistics Unveils Warehousing Facility in Maharashtra for Cummins,” India Seatrade News, indiaseatradenews.com . As more organized parks move in that direction, the India green logistics market should see stronger demand for green-certified distribution assets in the West, South, and NCR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex for Fleet and Infrastructure Transition | -1.4% | National, disproportionate impact on small fleet operators in North and Central India | Short term (≤ 2 years) |

| Limited Public Charging and Alternate Fuel Refueling Density | -1.2% | Tier-2 and Tier-3 cities, rural and semi-urban freight corridors | Medium term (2-4 years) |

| Fragmented Operator Base and Uneven Technology Adoption | -0.9% | National, most acute in road freight and unorganized warehouse segments | Long term (≥ 4 years) |

| Land, Power, and Permitting Constraints for Green Warehousing | -0.7% | Metro periphery zones, high-density urban areas in the West and South | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex for Fleet and Infrastructure Transition

Capital remains a major brake on the India green logistics market because a large part of the truck base still sits with small operators that do not have easy access to low-cost finance. More than 4 million trucks operate in India, many of them tied to fragmented ownership structures that limit investment capacity for cleaner fleets and supporting infrastructure. Public charging deployment is also behind what will be needed by 2030, meaning operators cannot always count on network availability when evaluating new fleet purchases. These conditions slow the India green logistics market most in corridors where operator fragmentation is high, and asset utilization is not yet strong enough to justify early infrastructure bets.

Limited Public Charging and Alternate Fuel Refueling Density

The India green logistics market also faces a network problem because vehicle adoption is advancing faster than the buildout of charging and refueling infrastructure. PM E-DRIVE aims to reach 72,300 charging points by March 2028, but rollout discipline matters, as previous public charging allocations had not translated into timely execution as of late 2025. The same gap exists in LNG and hydrogen corridors, where commercial viability depends on route coverage rather than fleet purchases alone. Until network density improves, the India green logistics market will scale faster in select urban and industrial corridors than across the full national freight map.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Green Transportation Maintains Operational Core

Green transportation held 58.07% of the India green logistics market share in 2025, making it the dominant mode across road, rail, coastal, and inland freight movements. Its scale reflects the fact that most decarbonization gains still depend on how freight is moved, how routes are designed, and which modal combinations are used for each corridor. Rail-linked cargo handling is becoming increasingly important within the function, as cargo terminals and dedicated freight corridors are diverting industrial traffic toward lower-emission rail networks in sectors such as automotive, chemicals, and steel. The India green logistics market is also seeing modal choice shaped by compliance, since shippers increasingly need freight systems that can support carbon disclosure and lower emissions per ton-kilometer.

Green value-added services and others are projected to grow at a 15.13% CAGR through 2031, indicating rising demand for software, carbon accounting, route optimization, and emissions reporting across the physical freight network. That growth is significant because these services add visibility and auditability, which are becoming more important in contract selection and export compliance. Green warehousing and distribution remains the second major function, supported by the planned expansion of certified warehouse space and by large integrated projects that can serve organized supply chains at scale. Renewable energy equipment manufacturers are also increasing warehouse demand, which gives the India green logistics industry another structurally aligned customer base as clean energy manufacturing expands.

By Fuel / Energy Type: Electric-Powered Logistics Leads Despite Hydrogen’s Rapid Ascent

Electric-powered logistics accounted for 54.88% of the India green logistics market size in 2025, indicating that urban and short-haul use cases continue to lead the current transition. The strongest proof point is not theory but operating scale, with Amazon India running more than 12,000 EVs across 500+ cities in 2026 and extending electric truck deployment into quick-commerce operations[3]LogisticsInsider. "Amazon India to Deploy 1,000 Eicher Electric Trucks for Amazon Now Operations." 2026. . This keeps electric fleets well placed in dense routes where delivery predictability, depot charging, and lower urban operating costs matter most. Biofuel-based logistics and other alternatives continue to serve heavier, longer routes where full electrification still faces cost and charging constraints, and GreenLine’s fleet of more than 1,000 LNG trucks, with over 70 million km logged by 2026, shows that commercially viable alternatives are already in use on selected corridors.

Hydrogen-powered logistics is projected to grow at a 17.49% CAGR through 2031, making it the fastest-expanding fuel pathway in the India green logistics market. The government’s decision to identify 10 highway corridors for hydrogen truck pilots provided the segment with an early deployment framework and brought in large industrial and vehicle partners from the start. Port infrastructure is also beginning to move, with approval for a green hydrogen jetty at Paradip Port Authority and early hydrogen-linked activity at Thoothukudi adding practical nodes to the future freight network. That creates a two-track transition in the India green logistics market, where EVs lead urban freight while hydrogen develops around ports, industrial corridors, and heavy long-haul movement.

By End-user Industry: Manufacturing Anchors Volumes as Healthcare Drives Complexity

Manufacturing and industrial accounted for 31% of the India green logistics market share in 2025, reflecting the scale of freight generated by steel, cement, chemical, and auto component clusters. This base matters because large industrial shippers usually move high volumes across repeat corridors, which makes modal shift, rail use, and carbon tracking easier to operationalize. Listed manufacturers also face stronger disclosure pressure under BRSR-linked reporting, while overseas buyers are paying closer attention to supply chain emissions and transport documentation. The India green logistics industry is also changing within automotive supply chains, where battery movement, EV distribution, and the handling of charging equipment require different warehousing, safety, and transport capabilities than those of legacy internal combustion networks.

Healthcare and pharmaceuticals are forecast to grow at a 15.96% CAGR through 2031, making it the most dynamic demand pocket in the India green logistics market. Growth here is tied to cold-chain precision, regulatory compliance, and the need for reliable low-emission distribution, not just higher cargo volume. That is why reefer rail, energy-efficient refrigeration, live tracking, and GDP-compliant storage are becoming more important across pharma corridors. Maersk’s weekly dedicated reefer rail service from Hyderabad to Nhava Sheva with CONCOR shows how specialized cold-chain networks are being redesigned to reduce emissions while improving service consistency for pharma exporters.

Geography Analysis

The West region accounted for 28.40% of the India green logistics market share in 2025, making it the largest regional base for organized green logistics activity. Maharashtra and Gujarat support that lead through warehousing scale, port connectivity, industrial density, and stronger private investment pipelines. Gujarat’s State Integrated Logistics Master Plan was launched in 2026 with a project shelf of INR 1.80 lakh crore (USD 215 billion), reinforcing the region’s role in the planning of multimodal, green-compliant infrastructure.

The South region is projected to grow at a 14.39% CAGR through 2031, making it the fastest-growing geography in the India green logistics market. Hyderabad and Bengaluru support this momentum through pharmaceutical cold-chain demand, while Tamil Nadu adds port-led energy transition infrastructure. Telangana moved into the High Performer category in LEADS 2025, supported by integrated logistics parks and inland container planning that strengthen the region’s organized freight base. V.O. Chidambaranar Port became the first Indian port to partner with H2Global for green hydrogen export to Europe in June 2026, and the project framework included 2 MW of electrolyzer capacity and 40 Tata Motors hydrogen ICE trucks at the port. Tamil Nadu is also developing urban logistics consolidation centers in Chennai, which are expected to reduce vehicle-kilometers and daily greenhouse gas emissions, indicating that planning in the South is moving down to the city-network level.

The North region remains important to the India green logistics market because Delhi-NCR and Punjab sit on major industrial freight corridors linked to the Eastern Dedicated Freight Corridor. Delhi’s logistics roadmap includes green warehousing zones, digital freight systems, and dedicated green freight corridors, which should improve cleaner freight movement through dense urban territory. Central India is gaining strategic weight through DP World’s Powarkheda Logistics Composite Hub in Madhya Pradesh, while the East is building multimodal reach through waterway expansion and the upcoming Jogighopa logistics park, which widens the addressable freight network beyond the traditional west coast core. This means regional growth in the India green logistics market is no longer tied to a single corridor model, because different regions are advancing through warehousing, cold chain, rail, port, and hydrogen-linked pathways.

Competitive Landscape

The India green logistics market is moderately fragmented, with a few scaled players holding meaningful positions and a long tail of regional operators still shaping corridor-level competition. Large international 3PLs such as DHL Group, Kuehne+Nagel, DP World, and DSV have an advantage with multinational shippers because they bring formal sustainability programs, compliance systems, and wider capital access. DHL Group committed EUR 1 billion (USD 1.16 billion) to India by 2030 for low-emission facilities and battery logistics capabilities, which shows how global operators are using capital depth to secure a long-term presence. Kuehne+Nagel also reported that 99% of the electricity at its logistics sites came from renewable sources in its 2025 sustainability reporting, while planning to double its warehousing capacity in India by 2030[4]Kuehne+Nagel, “Sustainability Report 2025 / Upgraded Science-Based Targets,” Kuehne+Nagel, newsroom.kuehne-nagel.com.

Domestic and corridor-focused operators are responding with asset depth, network specialization, and technology-led operating models. Gateway Distriparks is expanding ICD capacity and train assets along western freight corridors, thereby strengthening its rail-linked position relative to broader 3PL networks. GreenLine Mobility Solutions is one of the clearest green-native challengers in the India green logistics market because it combines fleet deployment, fuel access, and backing for rapid scaling of alternative fuels. Its USD 275 million equity commitment in April 2025, and its plan for 10,000 LNG and EV trucks and 100 alternative-fuel stations, show how specialist models can compete without matching the full-service breadth of legacy players. Delhivery’s AI agent-powered transport management system also shows that digital execution is becoming a competitive differentiator alongside green fuel adoption, especially in high-volume parcel and contract logistics.

CONCOR remains an important national player in the India green logistics market because it couples rail reach with scale, throughput discipline, and new cold-chain formats. The company recorded 5.58 million TEUs in FY 2025-26, its highest ever throughput, while also launching a net-zero rail and land cold-chain platform with IceBattery. DP World’s acquisition of a 49% stake in Reliance Industries’ multimodal park near Chennai is another example of how leading companies are using equity partnerships to lock in strategic locations and future corridor access. Overall, the India green logistics market still leaves room for new entrants in hydrogen fueling, emissions measurement, and corridor-specific low-emission services, even as larger platforms continue to widen their operational moats.

India Green Logistics Industry Leaders

-

DHL Group

-

Delhivery Limited

-

Mahindra Logistics Limited

-

Blue Dart Express Limited

-

Container Corporation of India (CONCOR)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: TVS Supply Chain Solutions formed a 51:49 joint venture with Italy's ALA Group to enter India's aerospace and defense supply chain market, targeting cumulative revenues exceeding INR 2,000 crore (USD 239 million) by 2031, in a logistics vertical requiring higher precision and green compliance standards.

- May 2026: Maersk and CONCOR launched India's first dedicated weekly reefer rail service connecting Hyderabad's pharmaceutical cluster to Nhava Sheva Port, Mumbai, delivering end-to-end cold-chain logistics and cutting an estimated 3,000 tons of GHG emissions annually compared to road freight.

- May 2026: GreenLine Mobility Solutions and Tata Steel expanded their partnership with LNG-powered truck deployment at Tata Steel's Meramandali facility in Odisha, targeting CO₂ reductions of 40% per journey versus diesel on industrial long-haul corridors.

- January 2026: DP World signed an agreement with the Government of Madhya Pradesh at the World Economic Forum in Davos to develop the Powarkheda Logistics Composite Hub, an inland gateway integrating rail connectivity, warehousing, cold chain, and end-to-end cargo management for Central India's export trade.

India Green Logistics Market Report Scope

| Green Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Green Warehousing & Distribution | |

| Green Value-added Services and Others |

| Electric-Powered Logistics |

| Biofuel-Based Logistics |

| Hydrogen-Powered Logistics |

| Others |

| Retail & E-commerce |

| Manufacturing & Industrial |

| Automotive |

| Healthcare & Pharmaceuticals |

| Food & Beverages |

| Chemicals & Hazardous Materials |

| Others |

| North |

| Central |

| West |

| East |

| South |

| By Logistics Function | Green Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Green Warehousing & Distribution | ||

| Green Value-added Services and Others | ||

| By Fuel / Energy Type | Electric-Powered Logistics | |

| Biofuel-Based Logistics | ||

| Hydrogen-Powered Logistics | ||

| Others | ||

| By End-user Industry | Retail & E-commerce | |

| Manufacturing & Industrial | ||

| Automotive | ||

| Healthcare & Pharmaceuticals | ||

| Food & Beverages | ||

| Chemicals & Hazardous Materials | ||

| Others | ||

| By Region | North | |

| Central | ||

| West | ||

| East | ||

| South |

Key Questions Answered in the Report

What is the size outlook for green logistics in India through 2031?

The India green logistics market is valued at USD 50.70 billion in 2026 and is projected to reach USD 83.68 billion by 2031, with a 10.54% CAGR.

Which logistics function currently leads in India?

Green transportation is the largest function, with 58.07% share in 2025, because freight movement remains the main source of both cost savings and emission reduction.

Which fuel pathway is growing the fastest in freight decarbonization?

Hydrogen-powered logistics is projected to grow the fastest at a 17.49% CAGR through 2031, especially in long-haul and port-linked use cases.

Why is healthcare becoming a major demand driver for cleaner freight networks?

Healthcare and pharmaceuticals are forecast to grow at a 15.96% CAGR because they require reliable, low-emission cold-chain distribution, live tracking, and compliant storage.

Which region is leading the transition, and which region is growing the fastest?

The West led with 28.40% share in 2025 due to warehousing and port strength, while the South is growing the fastest at a 14.39% CAGR through 2031.

What is the biggest challenge slowing fleet transition in India?

High upfront capex and weak charging or refueling density remain the main obstacles, especially for small operators and for routes outside major urban or industrial corridors.

Page last updated on: