Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

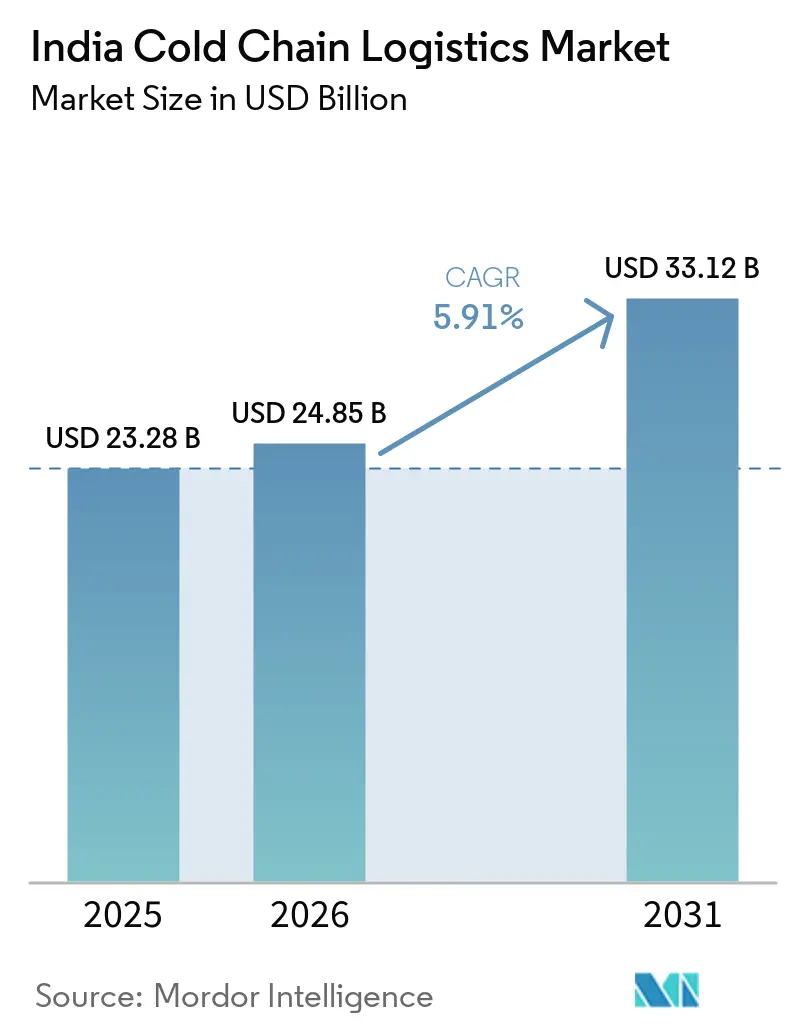

| Base Year Market Size (2025) | USD 23.28 Billion |

| Market Size (2026) | USD 24.85 Billion |

| Market Size (2031) | USD 33.12 Billion |

| Growth Rate (2026 - 2031) | 5.91% CAGR |

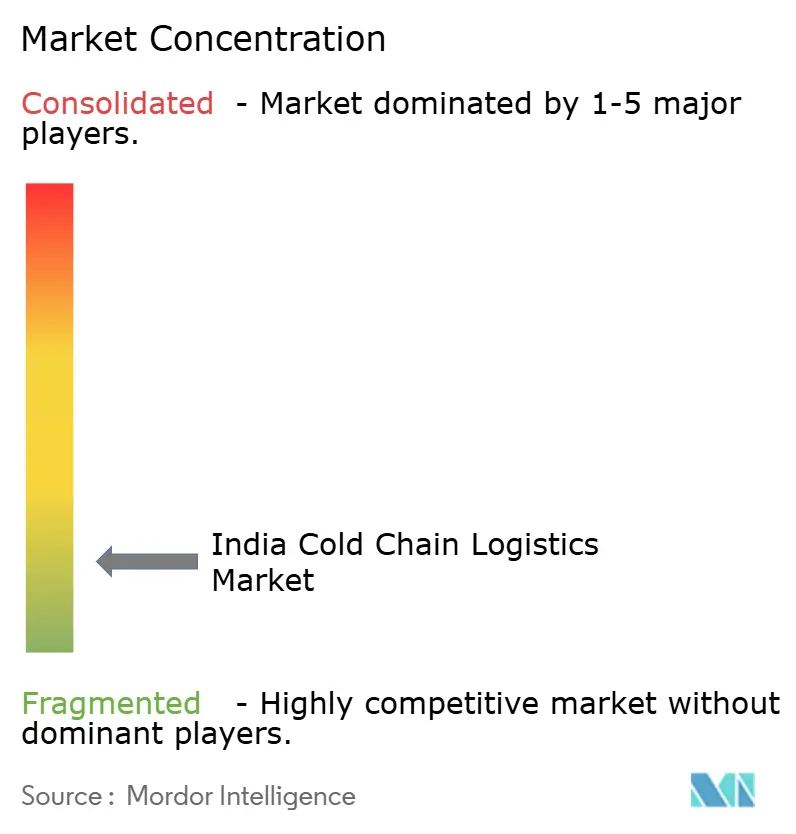

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Cold Chain Logistics Market Analysis by Mordor Intelligence

The India Cold Chain Logistics Market size is projected to expand from USD 23.28 billion in 2025 and USD 24.85 billion in 2026 to USD 33.12 billion by 2031, registering a CAGR of 5.91% between 2026 to 2031.

The India cold chain logistics market is evolving rapidly as demand for temperature-controlled supply chains increases across food processing, pharmaceuticals, and agricultural distribution. With large production volumes of perishable commodities and vaccines, efficient cold storage and refrigerated transportation have become critical to maintaining product quality and reducing supply chain losses. The expansion of organized retail, online grocery platforms, and processed food consumption is further driving investments in integrated cold chain infrastructure across India. Additionally, increasing participation from private logistics providers is supporting the development of modern refrigerated warehouses and reefer fleets. However, regional imbalances in cold storage capacity and high infrastructure costs continue to influence the pace of market development.

Key Report Takeaways

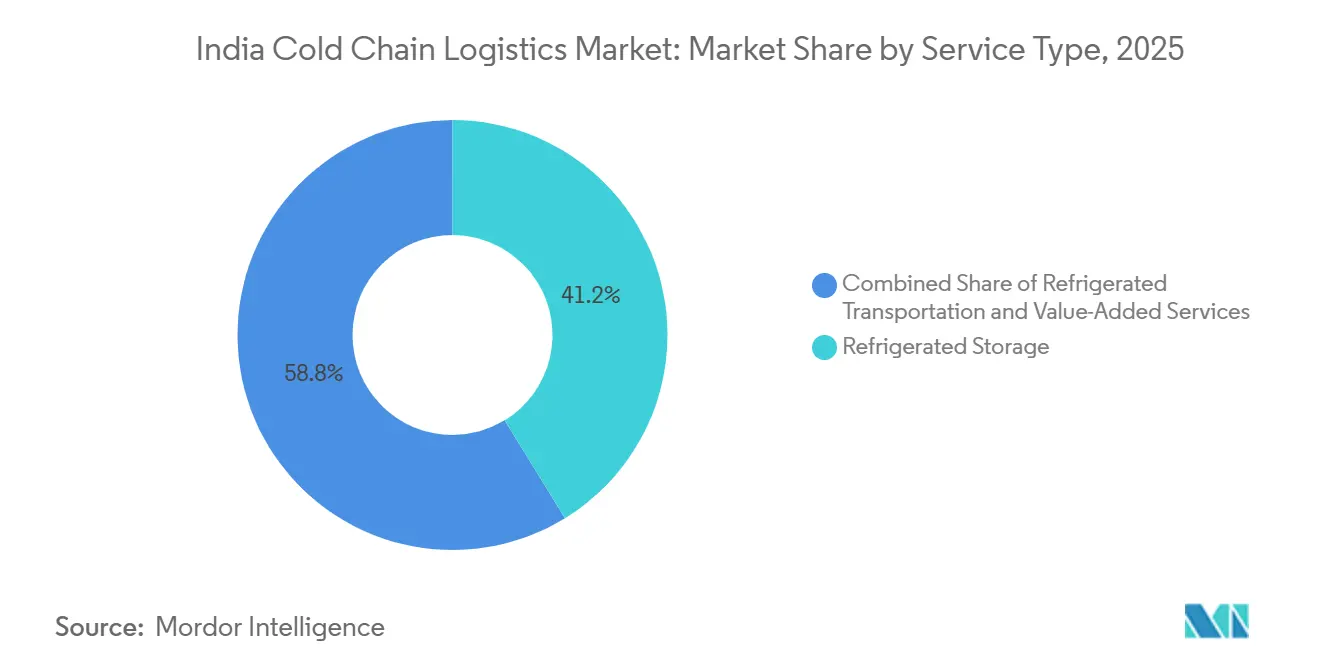

- Refrigerated storage led the India cold-chain logistics market share with 41.24% share in 2025, while value-added services expanded at the fastest 5.34% CAGR through 2031.

- Frozen temperature zones commanded 51.47% of capacity in 2025; chilled facilities recorded the quickest 6.13% CAGR to 2031.

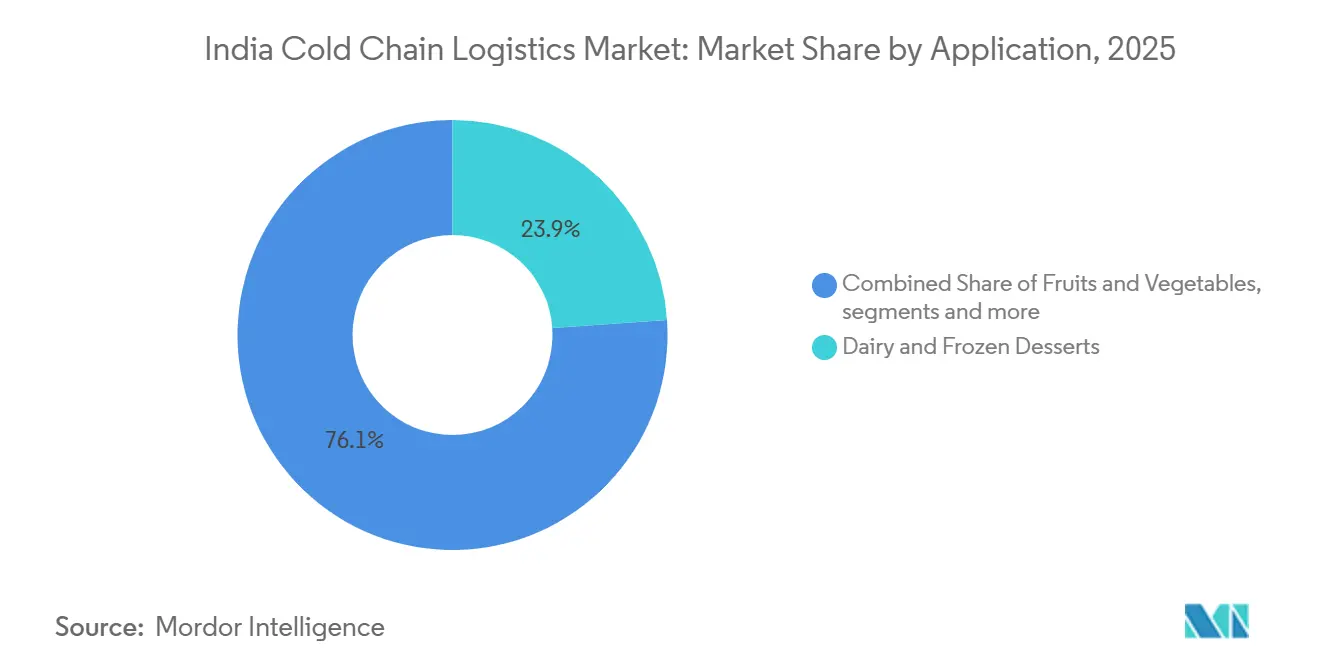

- Dairy and frozen desserts accounted for 23.89% of the India cold-chain logistics market size in 2025, whereas pharmaceuticals and biologics exhibit the highest 6.20% CAGR through 2031.

- West India contributed 22.78% of 2025 revenue; East India is projected to advance at a 6.01% CAGR between 2026-2031.

- Snowman Logistics, DHL Supply Chain India, and TCI Express together controlled the majority of the market share, reflecting a fragmented landscape that still favors regional specialists.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of National Gas Grid enabling LNG-fuelled reefer trucking | +1.2% | National; early uptake in Gujarat, Rajasthan, Maharashtra | Medium term (2-4 years) |

| Government-subsidized bulk-cold-storage schemes | +0.9% | National; concentrated in agricultural states | Long term (≥ 4 years) |

| Pharma biologics & vaccine pipeline expansion | +1.5% | National; hubs in Hyderabad and Pune | Short term (≤ 2 years) |

| E-grocery last-mile refrigerated demand | +1.1% | Urban tier-1 and tier-2 cities | Short term (≤ 2 years) |

| AI-optimized route & load planning adoption | +0.7% | National; metro city pioneers | Medium term (2-4 years) |

| Green-energy-based reefer fleets | +0.4% | National; pilots in Gujarat and Karnataka | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Organized Retail & Frozen FMCG Distribution

Packaged-food sales are projected to climb from USD 122.7 billion in FY 2024 to nearly USD 206.3 billion by FY 2029 as frozen ready-to-eat meals post an 18.1% annual rise. Modern trade formats and quick-commerce operators therefore demand more urban cold rooms, micro-fulfilment hubs, and last-mile reefer vans. HyFun Foods expects quick commerce to account for one-third of its B2C revenue in 2025, underscoring how same-hour delivery compresses supply-chain timelines. Fast-growing products also require stricter compliance with the Food Safety and Standards Authority of India (FSSAI), which shifts preference toward logistics partners holding ISO 22000 or Hazard Analysis and Critical Control Point (HACCP) certifications. As premium frozen SKUs proliferate on shelves, providers able to bundle kitting, blast-freezing, and multi-temperature trucking are likely to capture higher margins.[1]Ministry of Food Processing Industries, “Cold-Chain Projects Under PMKSY,” pib.gov.in

Government Support via PMKSY Cold-Chain Infrastructure Scheme

PMKSY offers 35% capital grants in general regions and 50% in difficult geographies, plus an additional subvention, to shorten the payback period for new plants. While the scheme has sanctioned 25.52 lakh metric tons of capacity, delays in disbursements, land-acquisition bottlenecks, and unreliable rural grids have slowed commissioning. Revised 2025 engineering guidelines now favor rooftop solar, enabling plants to trim electricity costs, which still account for 30-40% of operating costs. The policy also supports 50 irradiation units that extend the shelf life of export-bound produce, such as mangoes and pomegranates. Operators aligning with PMKSY’s multi-product focus and renewable push stand to secure subsidized capex and diversify away from single-crop utilisation.[2]Ministry of Food Processing Industries, “Cold-Chain Engineering Guidelines 2025,” mofpi.gov.in

Rising Pharmaceutical & Vaccine Cold Supply-Chain Demand

India already ships 60% of the world’s vaccines and 20% of generic drugs, and FY 2023-24 pharma exports reached USD 27.85 billion. Good Distribution Practice (GDP) mandates from the Central Drugs Standard Control Organization now require validated transport lanes, continuous data logging, and audit trails, raising the compliance bar. TCI Express answered with a Pharma Cold Chain Express service running GPS-enabled reefers pre-cooled to −18 °C, while Snowman Logistics retrofitted all 45 warehouses with 100% generator back-up. The maturing biologics pipeline further lifts demand for ultra-low (below −20 °C) space, particularly around Hyderabad and Bengaluru CRDMO clusters. Tight audits and export documentation thus create a moat for players that have already digitised their operations.

Growth of E-Commerce Grocery & Frozen Food Delivery

Blinkit, Swiggy Instamart, and Zepto have deployed hundreds of urban dark stores with chilled and frozen aisles to deliver on 10- to 30-minute promises. Their geographic sprawl forces logistics providers to manage a denser mesh of sub-50 km routes, raising the need for smaller 1-3-ton reefer trucks and predictive routing software. Industry associations note that unit economics remain challenging, but the model still stimulates incremental cold-room demand inside residential catchments. Asset-light aggregators are emerging to orchestrate temperature-controlled capacities from multiple small fleet owners through digital marketplaces. As delivery windows shrink, any temperature excursion triggers instant product rejection, making end-to-end IoT monitoring a non-negotiable standard.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Expenditure for Cold-Chain Assets | −0.8% | Tier-3 cities and rural belts | Long term (≥ 4 years) |

| Limited Cold Storage Penetration in Tier-3 and Rural Areas | −0.6% | Central India, Northeast | Long term (≥ 4 years) |

| Seasonal Demand Fluctuations Leading to Under-Utilization | −0.4% | Potato belt in North India | Medium term (2-4 years) |

| Spoilage Risks from Temperature Excursions During Transit | −0.3% | National, rural roads | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure for Cold-Chain Assets

Building a multipurpose store costs USD 42-54 per sq ft, while pharma-grade designs cost USD 60-72 per sq ft, and a single 20-footer refrigerated truck costs USD 36,000-60,000. Together, these numbers stretch payback to seven-plus years in smaller cities where utilization languishes at 40-50%. Banks remain cautious, and interest rates above 11% raise debt-service strain. Though PMKSY subsidies reimburse up to half the project cost, claim processing often takes more than 18 months, unsettling cash flows. Consequently, many entrepreneurs now prefer modular, solar-integrated units that can be expanded into 5,000 sq ft blocks, lowering first-phase risk.

Limited Cold Storage Penetration in Tier-3 and Rural Areas

Around 70-75% of India’s installed capacity is in five states, Uttar Pradesh, Punjab, Gujarat, Maharashtra, and West Bengal, leaving significant white space across Madhya Pradesh, Chhattisgarh, and the Northeast. Weak power grids lead to frequent diesel generator use, which can inflate operating costs by up to 35%. Farmer-producer organizations still view cold stores as potato silos rather than multi-product hubs, limiting off-season revenue. NCCD is pushing digital twin audits and operator training, but land title disputes and road bottlenecks are delaying new builds. Companies adopting hub-and-spoke models, with one medium hub in a tier-2 city feeding small cross-docks in villages, are beginning to improve accessibility despite infrastructure gaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Services Lift Margins

Refrigerated storage accounted for 41.24% of the India cold-chain logistics market share in 2025, supported by potato-centric facilities across Uttar Pradesh and Punjab. Value-added services, though smaller, are forecast to reach the fastest 5.34% CAGR to 2031 as customers increasingly demand ripening chambers, kitting, and export documentation. TCI Express opened a 150,000 sq ft GDP-ready warehouse in Gurugram in December 2025 to anchor its premium pharma lane, while Snowman Logistics now embeds ERP-linked data loggers across 277 reefers for real-time visibility. Service bundling lifts yield because of activities such as blast-freezing command fees up to 40% above plain storage. As NCCD pushes rooftop solar and robotics, the India cold-chain logistics market is poised to see more hybrid facilities marrying storage and high-throughput processing.

Although multipurpose sheds dominate capacity, transport demand is also rising. NCCD projects that truck-related projects will increase from roughly 19,000 in 2024 to over 33,000 by 2031. Mahindra Logistics targets 7 million sq ft of new space in Kolkata, Guwahati, and Agartala, and DHL Supply Chain India has budgeted EUR 500 million for 12 million sq ft with robotic picking systems. These moves underscore a shift from single-commodity stores toward end-to-end, technology-rich solutions that maintain GDP compliance and secure export contracts.

By Temperature Type: Chilled Zones Gain Share

Frozen rooms (−18 °C to 0 °C) controlled 51.47% of 2025 capacity, mirroring the dominance of ice cream, frozen desserts, meat, and seafood. Yet chilled chambers (0 °C to 5 °C) are the fastest sub-segment, expanding at a 6.13% CAGR on the back of fresh produce, ready-to-eat meals, and sensitive drugs. Quick-commerce hubs now dedicate up to 60% of floor space to chilled racks, forcing providers to add flexible racking that can swing between temperature bands. Operators like Snowman already build multi-zone halls so a single dock can ship both −20 °C and +4 °C cargo, improving asset utilization. Deep-frozen rooms below −20 °C, while still niche, are rising in pharma clusters as mRNA vaccines scale.

The India cold-chain logistics market for chilled produce is projected to grow sharply as urban consumers trade up to premium salads, berries, and dairy beverages. Reconfigurable refrigeration, energy-efficient compressors, and solar panels reduce operating costs, which remain the highest barrier to wider chilled coverage in second-tier towns. As fruit exporters shift from air to sea freight to lower costs, controlled atmosphere refers to containers that should see higher import volumes through 2031.

By Application: Pharma Outpaces Dairy

Dairy and frozen desserts represented 23.89% of the India cold-chain logistics market size in 2025, anchored by Amul’s 18 million liters daily milk pool and Mother Dairy’s 3 million liters collection. Pharmaceuticals and biologics, however, are poised to outstrip every other category with a 6.20% CAGR as GDP norms, contract research, and export volumes converge. TCI Express’s express pharma network and Snowman’s GDP-validated rooms cater to vaccine makers who cannot tolerate even ±2 °C swings. Fruits and vegetables remain large by tonnage, yet inadequate cold coverage still causes double-digit wastage, pulling down revenue share.

Meat, poultry, and seafood generated USD 7.37 billion in export value in FY 2023-24, and the Marine Products Export Development Authority enforces strict temperature audits at ports. Ready-to-eat meals and bakery items are riding the wave of urbanization and single-serve demand, prompting FMCG majors to sign multi-year storage leases. Ultimately, the application mix is tilting toward higher-margin pharma and horticulture cargo that rewards tight temperature control and digital proof of compliance.

Geography Analysis

West India delivered 22.78% of 2025 turnover thanks to JNPT’s container heft and the USD 9.18 billion Vadhavan mega-port that will add 23.2 million TEU by 2040[3]Ministry of Ports, Shipping & Waterways, “Vadhavan Port Detailed Project Report,” shipmin.gov.in. Gujarat’s Dholera investment zone and Mundra Port expedite refer boxes for dairy and fruit exporters, while high land and power costs in Mumbai encourage solar rooftop retrofits and automation to defend margins. East India, by contrast, is forecast to clock the fastest 6.01% CAGR to 2031, as Sagarmala funding revamps Kolkata Port and the Act East Policy improves road links to Assam, Meghalaya, and Tripura. Mahindra Logistics is adding 7 million sq ft across Kolkata, Guwahati, and Agartala, and Snowman’s 5,152-pallet Guwahati site marks its first leased asset in the region.

North India still houses nearly three-quarters of national store capacity, mostly potato silos in Uttar Pradesh and Punjab, yet utilization drops below 50% outside the harvest window. TCI Express’s new Gurugram facility seeks to pivot the belt towards premium pharma loads. South India benefits from Hyderabad and Bengaluru biotech clusters plus marine exports through Kochi and Chennai, sustaining multi-temperature demand. Central India remains underserved; PMKSY now offers 50% project grants, plus a transport subsidy, to lure investors into Madhya Pradesh and Chhattisgarh. Operators that knit hub-and-spoke models linking tier-2 cities with farm clusters are therefore best placed to unlock latent produce flows.

Competitive Landscape

India’s cold chain remains fragmented: 8,698 stores across the country provide 395 lakh metric tons of storage, yet the five largest players together control barely 20 lakh metric tons. Snowman Logistics operates 45 warehouses and 277 reefers with full IoT visibility, but its Q2 FY 2025 profit fell 79% amid weaker utilization, underscoring price pressure in commoditized lanes. DHL Supply Chain India has earmarked EUR 500 million for 12 million sq ft that will host robotic picking arms and autonomous tuggers, raising the technology stakes for local incumbents. TCI Express invested USD 42 million in a Gurugram pharma hub and integrated data loggers across its network to drive double-digit growth in clinical-trial traffic.

Second-tier companies such as ColdEx and Cold Star battle on tariffs, often lacking the balance sheet to deploy solar panels or multi-zone chillers. Some are therefore partnering with software start-ups that rent sensor kits and aggregate return loads via digital matching. Consolidation pressure is rising. Mahindra Logistics aims to double cold space by acquiring regional warehouses, and CONCOR Cold Chain leverages 60 rail terminals to roll out multimodal corridors. Despite these moves, potato-heavy capacity and diverse state regulations keep the India cold-chain logistics market's competitive intensity moderate, giving nimble specialists room to carve regional niches.

The most successful strategies now blend asset ownership with technology licensing. Players deploying blockchain-backed traceability and smart-metered compressors win premium contracts from exporters and pharma firms. Those unable to finance upgrades face margin erosion as customers increasingly reject manual logs and paper certificates. Overall, the landscape is tilting toward full-service, energy-efficient networks that can guarantee end-to-end temperature fidelity at scale.

India Cold Chain Logistics Industry Leaders

Snowman Logistics Ltd

ColdEx Logistics Pvt Ltd

TCI Express Ltd

DHL Supply Chain India

Mahindra Logistics Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: TCI Express inaugurated a 150,000 sq ft GDP-compliant warehouse in Gurugram as part of a USD 42 million capex plan to capture 10-15% annual growth in express pharma volumes.

- January 2024: Snowman Logistics opened a 5,152-pallet leased site in Guwahati, its first in the Northeast, raising national capacity above 141,000 pallets.

- October 2024: APEDA launched the i-CAS Halal certification system, cutting export documentation errors for meat cargo by 50.5% versus 2022.

- May 2024: NCCD released engineering guidelines recommending rooftop solar and centralized IoT dashboards projected to save 876 GWh by 2031.

India Cold Chain Logistics Market Report Scope

Cold chain logistics enable the safe transport of temperature-sensitive goods and products throughout the supply chain. It heavily relies on science to evaluate and account for the relationship between temperature and perishability. A comprehensive background analysis of the Indian cold chain logistics market, including an assessment of the economy and the contribution of sectors, a market overview, market size estimates for key segments, emerging trends in the market, and market dynamics, is presented in the report.

The India Cold-Chain Logistics Market Report is Segmented by Service Type (Refrigerated Storage, Refrigerated Transportation, and Value-Added Services), by Temperature Type (Chilled 0-5°C, Frozen -18-0°C, and More), by Application (Fruits & Vegetables, Meat & Poultry, and More), and by Geography (North India, South India, West India, East India, Central India). The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Refrigerated Storage | Public Warehousing |

| Private Warehousing | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0 – 5 °C) |

| Frozen (-18 – 0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than -20 °C) |

By Application

| Fruits & Vegetables |

| Meat & Poultry |

| Fish & Seafood |

| Dairy & Frozen Desserts |

| Bakery & Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals & Biologics |

| Vaccines & Clinical Trial Materials |

| Chemicals & Specialty Materials |

| Other Perishables |

By Region

| North India | Delhi-NCR |

| Punjab | |

| Haryana | |

| Others | |

| South India | Karnataka |

| Tamil Nadu | |

| Telangana | |

| Others | |

| West India | Maharashtra |

| Gujarat | |

| Others | |

| East India | West Bengal |

| Odisha | |

| Others | |

| Central India | Madhya Pradesh |

| Chhattisgarh |

| By Service Type | Refrigerated Storage | Public Warehousing |

| Private Warehousing | ||

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0 – 5 °C) | |

| Frozen (-18 – 0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than -20 °C) | ||

| By Application | Fruits & Vegetables | |

| Meat & Poultry | ||

| Fish & Seafood | ||

| Dairy & Frozen Desserts | ||

| Bakery & Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals & Biologics | ||

| Vaccines & Clinical Trial Materials | ||

| Chemicals & Specialty Materials | ||

| Other Perishables | ||

| By Region | North India | Delhi-NCR |

| Punjab | ||

| Haryana | ||

| Others | ||

| South India | Karnataka | |

| Tamil Nadu | ||

| Telangana | ||

| Others | ||

| West India | Maharashtra | |

| Gujarat | ||

| Others | ||

| East India | West Bengal | |

| Odisha | ||

| Others | ||

| Central India | Madhya Pradesh | |

| Chhattisgarh | ||

Key Questions Answered in the Report

How large is the India cold-chain logistics market in 2026?

The India cold-chain logistics market is projected to reach USD 24.85 billion in 2026, on track to reach USD 33.12 billion by 2031.

Which service type leads the market today?

Refrigerated storage holds the largest 41.24% share, though value-added services are growing fastest at 5.34% CAGR.

What is the fastest-growing temperature segment?

Chilled facilities (0 °C to 5 °C) expand at 6.13% CAGR, propelled by fresh produce, ready-to-eat meals, and pharma cargos.

Which application will add the newest revenue?

Pharmaceuticals and biologics are forecast to advance at a 6.20% CAGR through 2031, outpacing dairy and frozen desserts.

Why are East India investments accelerating?

Port upgrades under Sagarmala and new warehousing by Mahindra Logistics and Snowman are driving a 6.01% regional CAGR.

Page last updated on: