Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

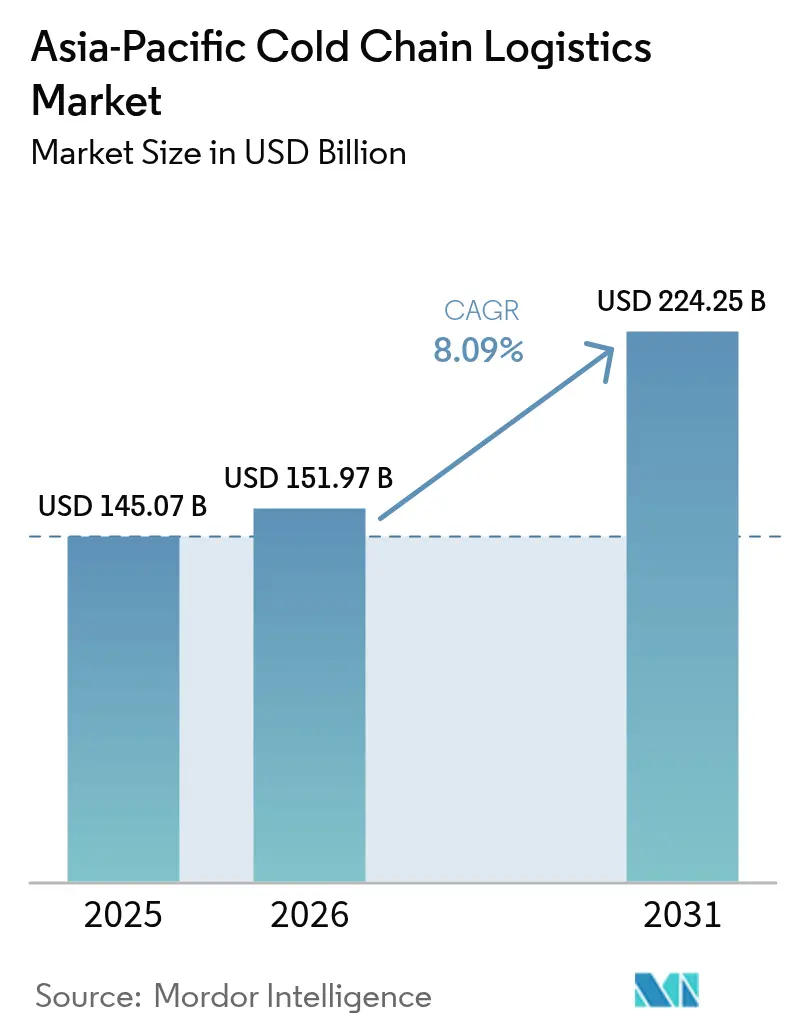

| Base Year Market Size (2025) | USD 145.07 Billion |

| Market Size (2026) | USD 151.97 Billion |

| Market Size (2031) | USD 224.25 Billion |

| Growth Rate (2026 - 2031) | 8.09% CAGR |

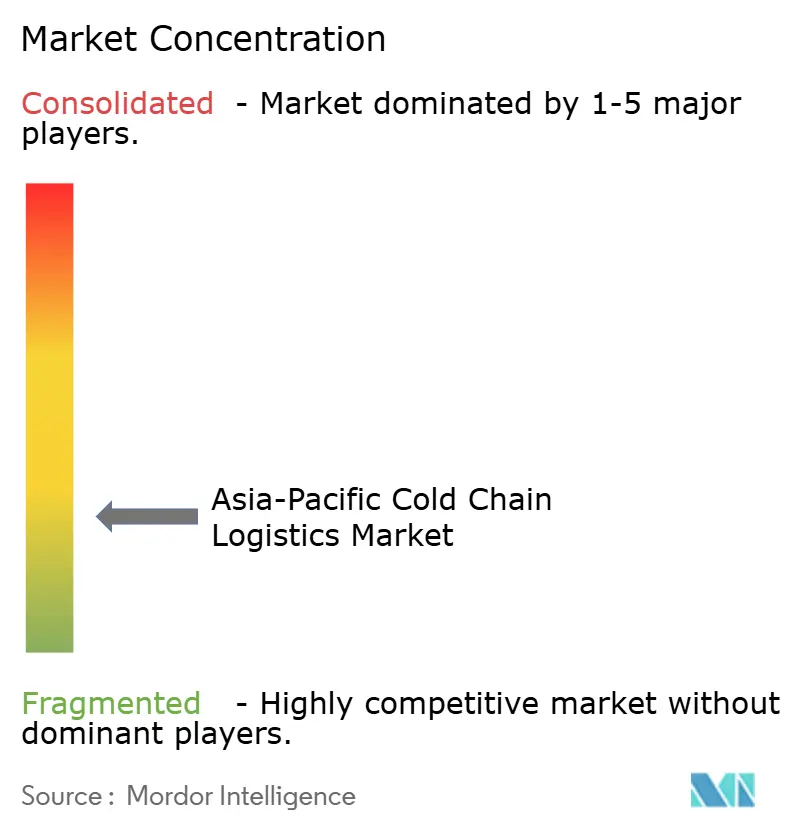

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Cold Chain Logistics Market Analysis by Mordor Intelligence

The Asia-Pacific cold chain logistics market size is projected to be USD 145.07 billion in 2025, USD 151.97 billion in 2026, and reach USD 224.25 billion by 2031, growing at a CAGR of 8.09% from 2026 to 2031.

Biopharmaceutical localization, digital trade protocols, and supermarket-owned distribution hubs are changing infrastructure priorities, steering capital toward automated, sustainability-compliant facilities. China’s entrenched manufacturing scale accounts for 39.79% of the Asia-Pacific cold chain logistics market share in 2025, yet India’s double-digit expansion signals a geographic rebalancing. Air freight capacity dedicated to temperature-sensitive drugs is accelerating as clinical trials proliferate, while development-bank-financed “cold corridors” are knitting rail and port nodes into cost-efficient arteries. Energy-efficient designs, natural refrigerants, and real-time visibility platforms are now universal requirements rather than differentiators, shifting competition toward integrated technology stacks.

Key Report Takeaways

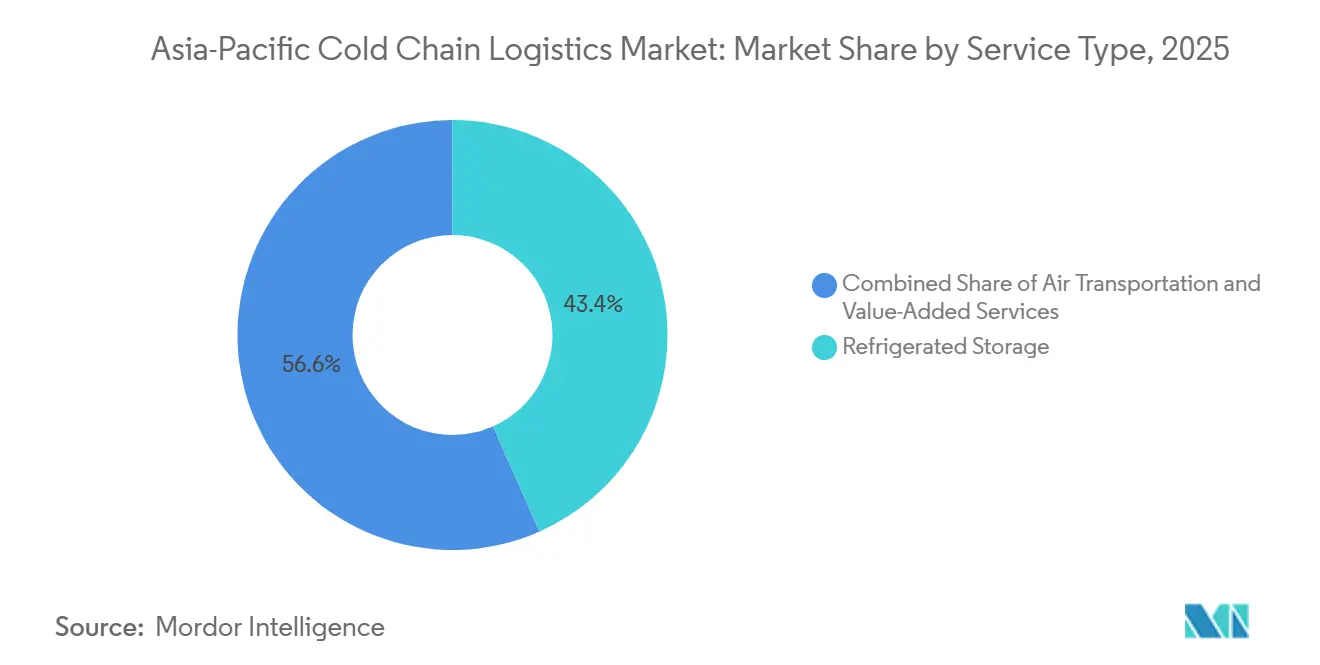

- By service type, Refrigerated Storage led with 43.37% of the Asia-Pacific cold chain logistics market share in 2025, whereas Air Transportation is forecast to expand at a 12.32% CAGR through 2031.

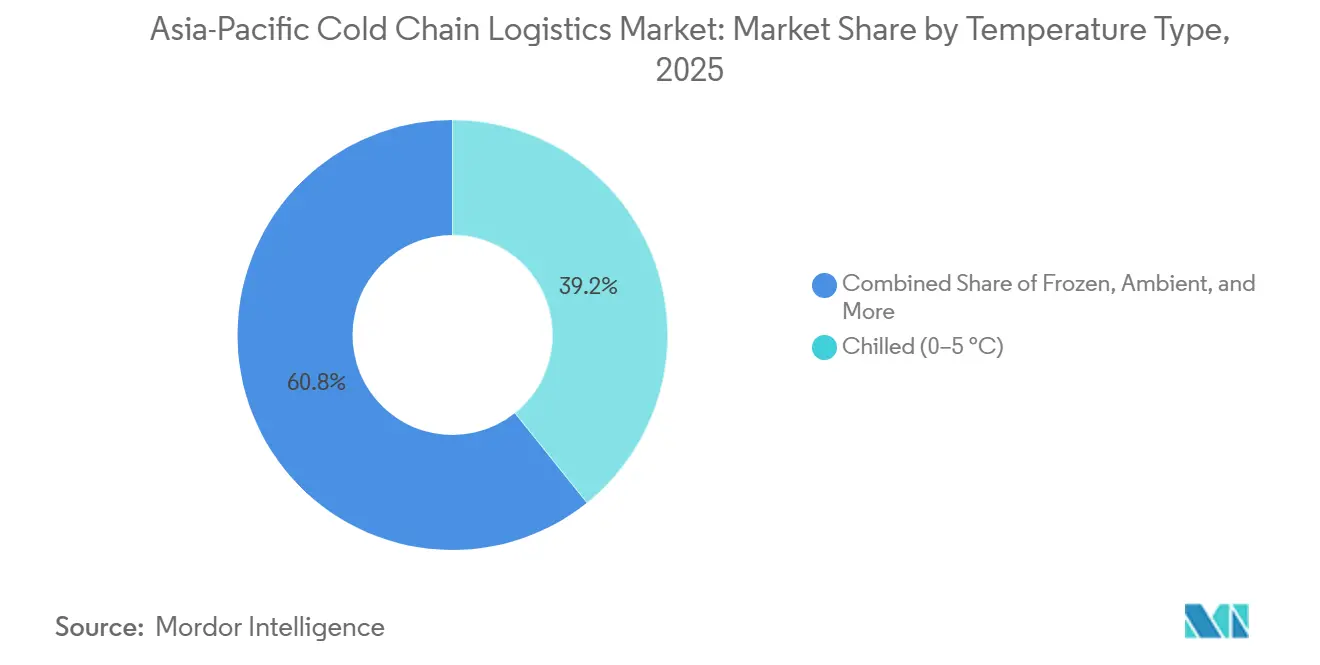

- By temperature type, the Chilled segment commanded 39.24% share of the Asia-Pacific cold chain logistics market size in 2025, while Frozen applications are projected to advance at a 10.28% CAGR through 2031.

- By application, Meat & Poultry accounted for a 24.35% share of the Asia-Pacific cold chain logistics market size in 2025, yet Vaccines & Clinical Trial Materials are registering the fastest 13.1% CAGR to 2031.

- By geography, China retained 39.79% of the Asia-Pacific cold chain logistics market share in 2025; India is on track for the highest 11.02% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating appetite for convenience-oriented chilled & frozen meals | +1.5% | Urban China, Japan, South Korea, and emerging Southeast Asia | Medium term (2-4 years) |

| Proliferation of same-day e-grocery fulfillment models | +1.4% | Metropolitan areas across India, China, Singapore, Thailand | Short term (≤ 2 years) |

| Intensifying the biologic-drug pipeline needs stringent temperature assurance | +1.3% | India, China, Japan, and Singapore are pharmaceutical hubs | Long term (≥ 4 years) |

| Cross-market roll-out of interoperable e-SPS certificates that reduce border latency | +0.9% | ASEAN core, extending to RCEP signatories | Medium term (2-4 years) |

| Supermarket groups investing in proprietary refrigerated distribution hubs | +0.8% | China, India, Australia, Thailand retail markets | Medium term (2-4 years) |

| Development-bank-backed intermodal "cold corridors" expanding reefer rail & port capacity | +0.7% | Belt and Road Initiative countries, ASEAN Economic Corridor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Appetite for Convenience-Oriented Chilled & Frozen Meals

Dual-income urban households now prioritize ready-to-eat formats that require uninterrupted temperature control from the plant to the point of sale. Japan’s convenience sector illustrates the shift, with portion-controlled chilled meals gaining shelf prominence. Clean-label positioning encourages manufacturers to extend shelf life through refrigeration rather than preservatives, deepening reliance on the cold chain. Retailers respond with 24-hour micro-fulfillment centers, expanding demand for multi-temperature warehousing. Operators offering repackaging and quality-inspection services gain favor as regulatory food-safety standards tighten.

Proliferation of Same-Day E-Grocery Fulfillment Models

Quick-commerce platforms promising sub-60-minute delivery are redesigning urban networks around dark stores equipped with high-density cold rooms. Order velocity must triple traditional retail levels to offset premium real-estate and labor costs, making IoT-based energy management indispensable. Active-refrigeration vehicles and phase-change packaging mitigate tropical last-mile heat loads, preserving product integrity and raising consumer repeat-purchase rates.

Intensifying the Biologic-Drug Pipeline Needs Stringent Temperature Assurance

Monoclonal antibodies, mRNA vaccines, and cell therapies require ultra-low-temperature storage environments that few legacy depots can provide. DHL’s USD 3.57 billion commitment to dedicated health-logistics hubs underscores a distinct pharmaceutical sub-market with specialized compliance and chain-of-custody requirements. Decentralized production models shorten shipment distances but multiply shipment frequency, rewarding operators with flexible capacity. Clinical-trial material flows through India’s expanding study base are spurring the development of a cryogenic lane that integrates documentation and real-time temperature analytics.

Cross-Market Roll-Out of Interoperable e-SPS Certificates That Reduce Border Latency

Digital sanitary-and-phytosanitary certificates integrated with customs single windows cut clearance times from days to hours, curbing temperature-excursion risk. ASEAN’s Digital Economy Framework provides the architecture, and blockchain pilots in Singapore and Malaysia already create immutable audit trails for perishable cargo[1]ASEAN Secretariat, “Digital Economy Framework,” asean.org . Sensor data feeds directly into customs systems, allowing expedited processing for shipments that demonstrate compliance in transit. Wider adoption of RCEP is poised to align standards, enabling network rationalization across member economies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile power tariffs & premium industrial land eroding cold-store profitability | -1.4% | Japan, Australia, urban China, Singapore | Short term (≤ 2 years) |

| Fragmented first-mile infrastructure in rural supply zones | -1.0% | India, Indonesia, Philippines, rural China, Vietnam | Long term (≥ 4 years) |

| Limited talent pool certified for natural/low-GWP refrigerant systems | -0.7% | Global, acute in developed APAC markets | Medium term (2-4 years) |

| Disparate carbon-reporting frameworks are inflating compliance overheads | -0.5% | Multinational operators across APAC jurisdictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Power Tariffs & Premium Industrial Land Eroding Cold-Store Profitability

Electricity accounts for nearly 70% of cold-store operating costs in Japan. While rooftop solar with storage can significantly reduce energy costs, high installation expenses make it most feasible for larger buildings or sites. Scarce urban land forces suburban builds, extending last-mile distances and eroding service-level targets. Real estate investment trusts specialising in temperature-controlled assets offer leaseback models that free up operator capital for automation outlays.

Fragmented First-Mile Infrastructure in Rural Supply Zones

Lack of reliable electricity, cold storage, and quality roads causes significant post‑harvest losses, forcing small farmers to sell produce quickly at lower prices; government efforts to build rural cold stores are a step forward, but infrastructure gaps remain a major constraint[2]Philippine News Agency, “Government Eyes Construction of Cold Storage Facilities,” pna.gov.ph . Portable solar chillers piloted in India demonstrate technical viability but require financing structures that pool smallholder demand. Cooperative ownership eases capital burdens but often struggles with professional management and governance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Air Freight Captures Pharmaceutical Urgency

Air Transportation is projected to expand at a 12.32% CAGR, reflecting drug-makers' preference for speed and risk mitigation, whereas Refrigerated Storage maintained a 43.37% share of the Asia-Pacific cold chain logistics market in 2025. The Asia-Pacific cold chain logistics market share is expanding as shippers outsource repackaging, kitting, and quality inspection to single-source providers.

Integrated contracts that guarantee product integrity rather than floor space are reshaping pricing models. Intermodal solutions balance cost and carbon goals by pairing air for clinical trial lots with sea or rail for bulk production, while public warehousing platforms allow rapid scaling during harvest surges. Proprietary technology, including blockchain traceability, is becoming a prerequisite in bid tenders as regulators demand end-to-end visibility.

By Temperature Type: Frozen Applications Gain Share

The Chilled band held 39.24% of the Asia-Pacific cold chain logistics market size in 2025, yet Frozen applications are forecast to grow fastest at a 10.28% CAGR, driven by convenience food and vaccine stockpiling. Ultra-low ranges below -20 °C are expected to expand as cell-therapy supply chains scale, requiring cascade refrigeration and redundant power.

Multi-temperature warehouses deploy zone management and airflow engineering to avoid cross-contamination, lowering utility bills by up to 15% through AI-driven optimization. Regulatory pressure is accelerating the adoption of natural refrigerants, with propane systems already mainstream in China’s retail equipment. IoT sensors feed predictive-maintenance algorithms that reduce downtime and extend compressor life.

By Application: Vaccine Logistics Redefines Growth Hierarchy

Meat & Poultry retained a 24.35% in the Asia-Pacific cold chain logistics market size in 2025, mirroring regional protein demand, but Vaccines & Clinical Trial Materials are growing at a 13.1% CAGR, elevating pharmaceutical lanes from niche to premium mainstream. Fruits & Vegetables benefit from rising export volumes as improved cold chain cuts spoilage, though seasonality challenges warehouse utilization.

Ready-to-eat meal distribution is expected to strengthen demand for mixed-temperature capacity, while fish & seafood shippers pilot ultra-low storage to preserve sashimi-grade quality. Each category imposes distinct documentation and handling procedures, driving specialization among logistics providers.

Geography Analysis

China’s 39.79% share of the Asia-Pacific cold chain logistics market in 2025 stems from integrated manufacturing and consumption clusters concentrated along the eastern seaboard. Next-generation facilities feature autonomous forklifts rated to -30 °C and AI energy-management systems that cut utility spend by 20%[3]Nikkei Asia, “Chinese Startups Race to Upgrade Cold Chain Logistics,” nikkei.com . Interior provinces are now receiving fresh capital as e-commerce penetration spreads inland.

India is projected to post the region’s fastest CAGR of 11.02% between 2026 and 2031, propelled by the PM Gati Shakti infrastructure plan, digital public infrastructure for logistics, and tax incentives for greenfield builds. Innovations such as ice-battery transport and cube packaging improve temperature resilience during power outages[4].Swarajya, “India’s Cold Chain Market to Hit Rs 5 Lakh Crore by 2032,” swarajyamag.com

Japan, South Korea, and Australia focus on asset replacement and automation to offset labor shortages and power costs. Southeast Asian markets, notably Indonesia and Thailand, are bridging rural-urban gaps through ASEAN-backed trade-facilitation platforms that shorten border dwell times, while Singapore and Malaysia leverage strategic port locations to operate as regional redistribution hubs.

Competitive Landscape

The Asia-Pacific cold chain logistics industry is fragmented. Top international 3PLs are extending reach through acquisitions: Kuehne + Nagel’s USD 75 million Thai buyout sharpened its pharmaceutical footprint, and DSV’s USD 120 million Indonesian stake added tropical last-mile reach. Large operators invest in IoT telemetry, warehouse robotics, and carbon-accounting dashboards to lock in multi-year contracts.

Regional specialists leverage regulatory familiarity and real-estate agility to serve retailer-owned networks. Start-ups like Shinsungo secure venture funding to commercialize sensor-rich transport boxes that extend lane options for high-value perishables. Sustainability credentials are decisive in bid evaluations, prompting fleet electrification pilots and renewable-energy procurement deals.

Consolidation is likely as mid-size firms struggle with natural-refrigerant retrofits and ESG reporting overheads. Joint ventures between logistics firms and equipment manufacturers accelerate technology diffusion, while real-estate investment trusts unlock capital for automation retrofits. Operators that can offer unified visibility, compliance, and temperature assurance command premium pricing over commoditized capacity.

Asia-Pacific Cold Chain Logistics Industry Leaders

United Parcel Service (UPS)

Nichirei Logistics Group Inc

SF Express

OOCL Logistics

Lineage Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DHL announced an expansion of its dedicated Airfreight Cold Chain Network as part of a broader investment in its life sciences & healthcare logistics.

- November 2025: Lineage Logistics expanded its import/export cold chain services to help customers navigate tariff changes, including enhanced bonded warehousing and transportation capacities improving flexibility and cross-border cold chain flows.

- June 2025: UPS Healthcare opened a new cold-chain-enabled healthcare logistics facility in Tuas, Singapore (11,500 m²), strengthening its APAC cold chain network with GDP/GMP-compliant temp-controlled storage.

- April 2025: UPS announced an agreement to acquire Andlauer Healthcare Group for US for USD 1.6 billion to boost its cold chain and specialized logistics.

Asia-Pacific Cold Chain Logistics Market Report Scope

By Service Type

| Refrigerated Storage | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0–5 °C) |

| Frozen (-18–0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

By Application

| Fruits & Vegetables |

| Meat & Poultry |

| Fish & Seafood |

| Dairy & Frozen Desserts |

| Bakery & Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals & Biologics |

| Vaccines & Clinical Trial Materials |

| Chemicals & Specialty Materials |

| Other Perishables |

By Country

| China |

| Japan |

| India |

| South Korea |

| Indonesia |

| Thailand |

| Australia |

| Singapore |

| Malaysia |

| Rest of Asia-Pacific |

| By Service Type | Refrigerated Storage | |

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0–5 °C) | |

| Frozen (-18–0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Application | Fruits & Vegetables | |

| Meat & Poultry | ||

| Fish & Seafood | ||

| Dairy & Frozen Desserts | ||

| Bakery & Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals & Biologics | ||

| Vaccines & Clinical Trial Materials | ||

| Chemicals & Specialty Materials | ||

| Other Perishables | ||

| By Country | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the projected value of the Asia-Pacific cold chain logistics market in 2031?

It is forecast to reach USD 224.25 billion, reflecting an 8.09% CAGR between 2026-2031.

Which service type is growing fastest within the region?

Air Transportation leads with a projected 12.32% CAGR, driven by demand for temperature-sensitive pharmaceuticals.

Why is India considered the most attractive growth geography?

India combines an 11.02% CAGR outlook with supportive infrastructure policies, such as the PM Gati Shakti plan and unified logistics digital platforms.

How are energy costs affecting cold-storage profitability?

Electricity can account for 70% of operating expenses, and tariff volatility in markets such as Japan and Australia drives the adoption of on-site renewable generation.

What technology investments are logistics providers prioritizing?

IoT temperature sensors, AI-driven energy management, warehouse robotics, and blockchain traceability systems are becoming standard bid requirements.

Which application segment is expected to grow the fastest?

Vaccines & Clinical Trial Materials are set to grow at a 13.1% CAGR as pharmaceutical supply chains demand ultra-low-temperature compliance.

Page last updated on: