Saccharin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

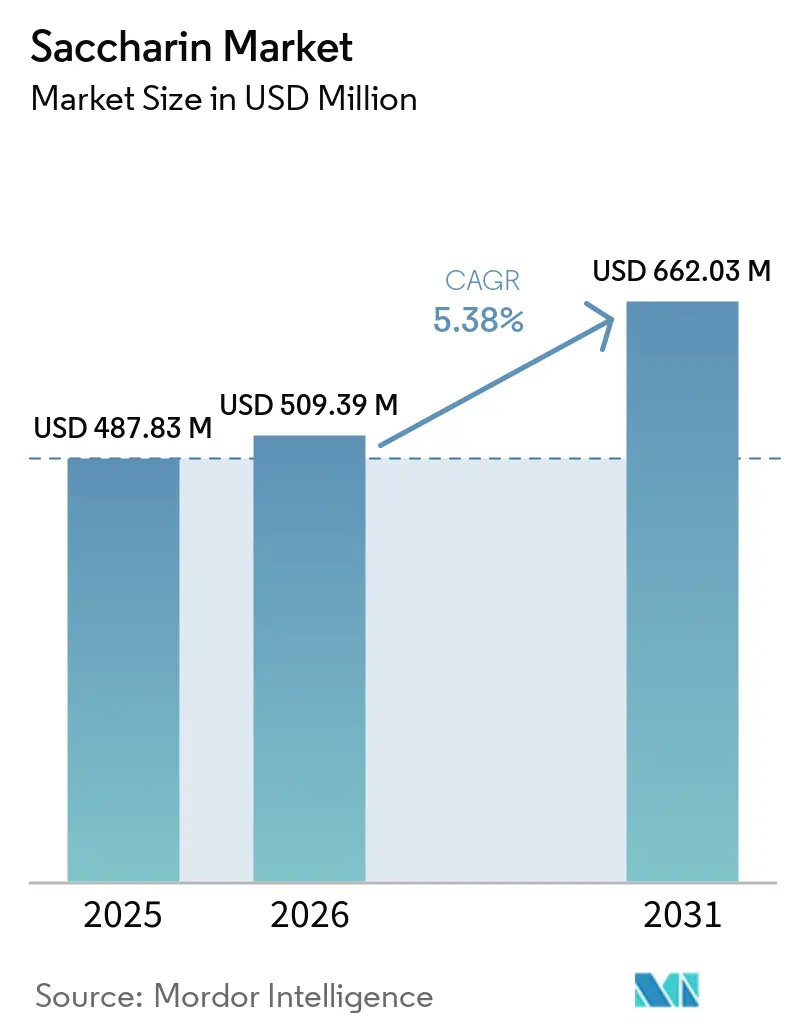

| Market Size (2026) | USD 509.39 Million |

| Market Size (2031) | USD 662.03 Million |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saccharin Market Analysis by Mordor Intelligence

The global saccharin market size is expected to grow from USD 487.83 million in 2025 to USD 509.39 million in 2026 and is forecast to reach USD 662.03 million by 2031, at a 5.38% CAGR over 2026-2031. Regulatory clarity and evolving market dynamics are driving renewed growth in the global saccharin market. In November 2024, the European Food Safety Authority (EFSA) completed its re-evaluation of saccharin (E 954), increasing the Acceptable Daily Intake (ADI) from 5 milligrams per kilogram (mg/kg) of body weight to 9 mg/kg of body weight[1]Source: European Food Safety Authority, "Saccharin: safety threshold increased," efsa.europa.eu/. The EFSA determined that the sweetener does not pose genotoxicity risks at current exposure levels. This regulatory approval has eased long-standing concerns among investors, opening up new opportunities for saccharin in key industries such as food, beverages, and pharmaceuticals. Saccharin remains a cost-effective and technically stable ingredient, making it a reliable choice for large-scale formulations. Additionally, its growing use as a pharmaceutical excipient strengthens its market resilience. While natural sweeteners like stevia and monk fruit, along with clean-label trends, present challenges, saccharin’s affordability and proven performance ensure its continued relevance in global supply chains over the forecast period.

Key Report Takeaways

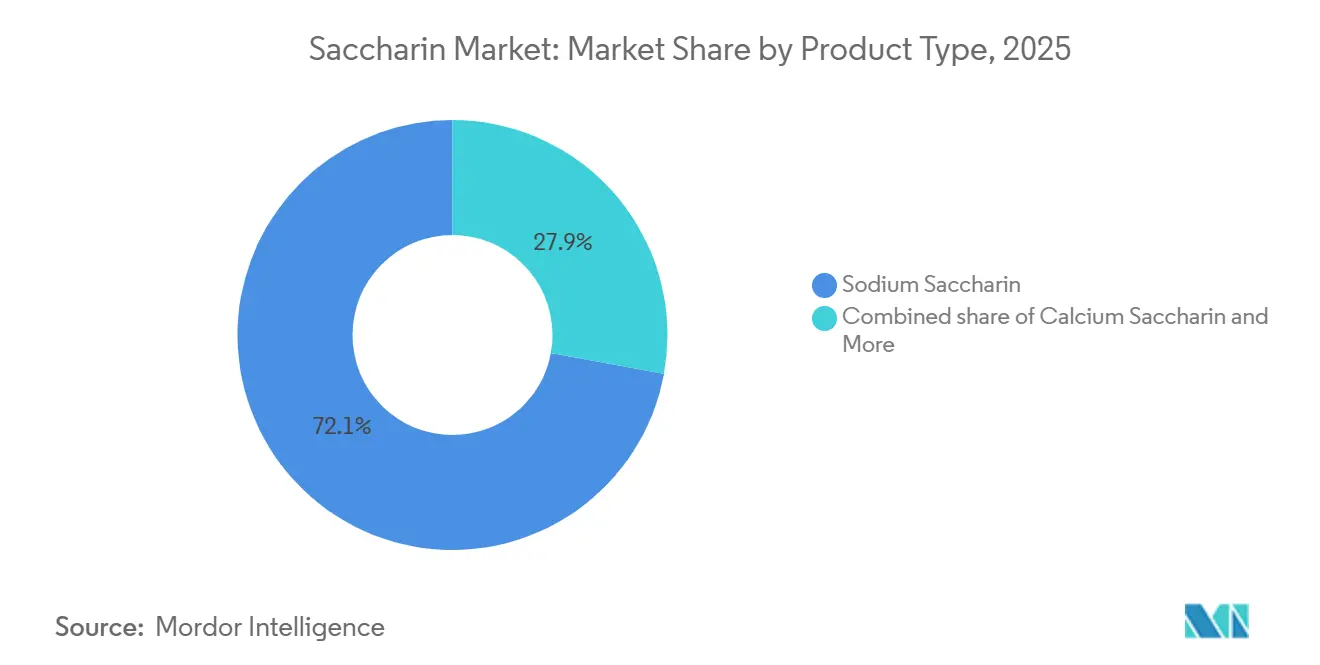

- By product type, sodium saccharin led the global preservatives market with a share of 72.12% in 2025, while calcium saccharin is anticipated to register the fastest CAGR of 5.98% during 2026-2031.

- By form, powder retained 87.35% share in 2025 and is forecast to expand at a 6.43% CAGR through 2031.

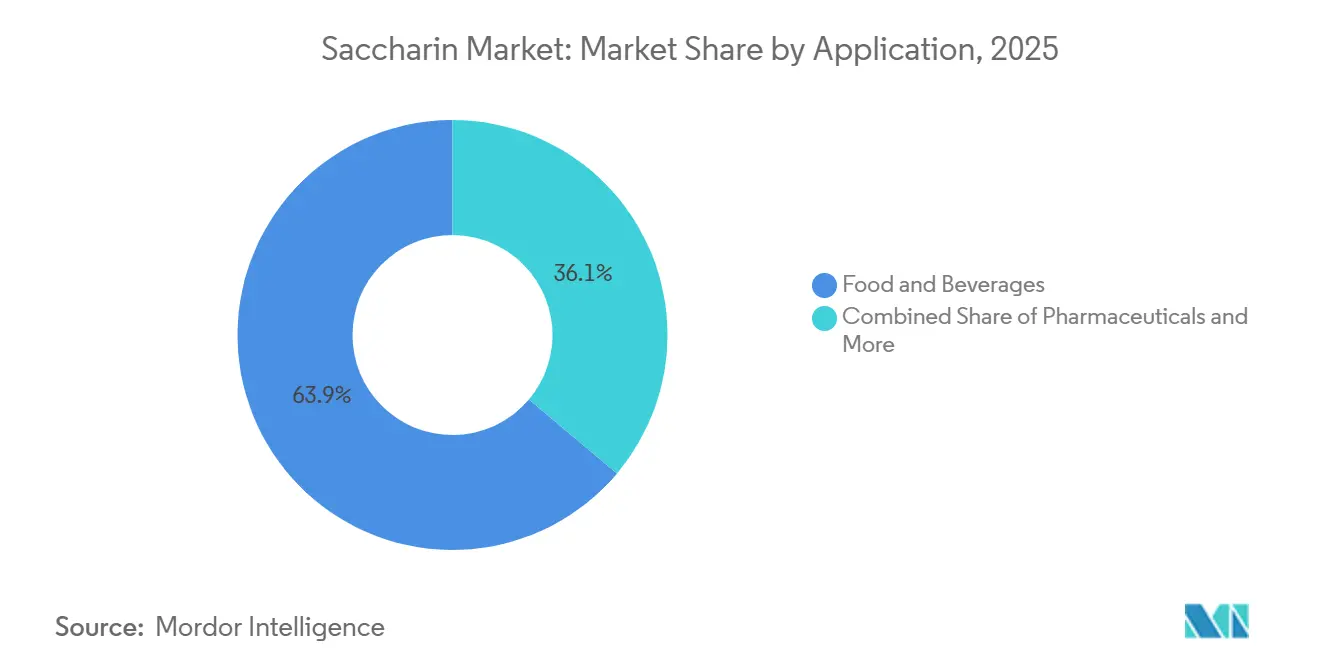

- By application, food and beverages accounted for 63.86% of 2025 revenue, but personal care and oral care are expected to grow fastest at 6.66% through 2031.

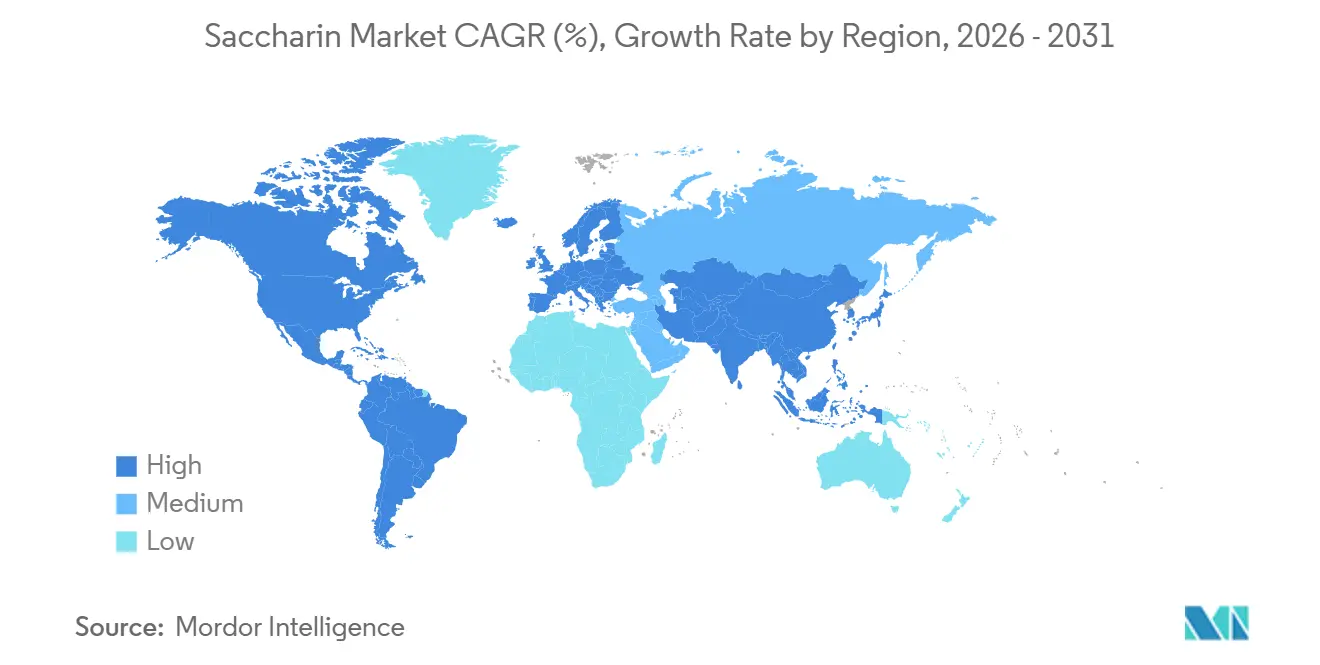

- By geography, Asia-Pacific led the global preservatives market with a share of 46.10% in 2025, and is anticipated to register the fastest CAGR of 5.90% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Saccharin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global sugar reduction initiatives supporting saccharin market growth | +1.5% | Global | Medium term (2–4 years) |

| Zero-sugar beverage boom accelerating sweetener consumption | +1.0% | North America and Europe, with spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Diabetes epidemic driving demand for sugar alternatives | +0.8% | Asia-Pacific core, South Asia, Middle East and Africa | Long term (≥ 4 years) |

| Pharmaceutical industry's shift toward sugar-free formulations | +0.6% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| High-intensity sweeteners becoming essential for calorie reduction targets | +0.5% | North America and Europe | Short term (≤ 2 years) |

| Oral care manufacturers prioritizing non-cariogenic sweetening systems | +0.4% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Global sugar reduction initiatives supporting saccharin market growth

Global efforts to reduce sugar consumption are significantly driving the growth of the saccharin market. Governments are implementing fiscal policies, such as taxes on sugar-sweetened beverages, which are accelerating the reformulation of products across processed food and beverage categories. Saccharin, with its zero-calorie composition and heat stability, has become a cost-effective solution for manufacturers targeting budget-conscious consumers. Additionally, companies reformulating their products are entering into long-term supply agreements, ensuring consistent demand and reducing exposure to short-term market fluctuations. In China, a nationwide health initiative has been introduced to combat the rising prevalence of obesity[2]Source: World Health Organization, "Beyond Weight Management: WHO and China Advance System-Based Approaches to Obesity Prevention and Care," who.int. This initiative emphasizes the need for comprehensive strategies to address obesity and its associated metabolic health risks. Alongside this, the introduction of front-of-pack sugar labeling standards is expected to drive extensive product reformulation in China, which is the largest food and beverage manufacturing market globally. These developments further solidify saccharin’s strategic importance in supporting global sugar reduction objectives.

Zero-sugar beverage boom accelerating sweetener consumption

The global saccharin market is experiencing significant growth, driven by the rapid rise of zero-sugar beverages, which have become one of the fastest-growing segments in the food industry. Leading cola companies and private-label manufacturers are increasingly adopting blend-based sweetening systems. These systems combine saccharin with acesulfame potassium (acesulfame K) or sucralose to achieve a balanced sweetness profile and extend flavor longevity, making saccharin a critical ingredient in cost-effective product formulations. Saccharin has shifted from being a standalone sweetener to a vital component in blends, enhancing flavor while reducing the overall quantity required. Regulatory stability further supports this trend. The United States Food and Drug Administration (FDA) continues to approve saccharin for use in beverages and processed foods, while Codex Alimentarius standards guide international trade specifications. These factors collectively ensure saccharin remains a key ingredient in the expanding global zero-sugar beverage market, reinforcing its importance in long-term product innovation and cross-border supply chain operations.

Diabetes epidemic driving demand for sugar alternatives

With the rising prevalence of diabetes, the demand for saccharin is experiencing significant growth, driven by the increasing need for sugar alternatives in both healthcare and consumer markets. According to the International Diabetes Federation (IDF) Diabetes Atlas (2025), 11.1% of the global adult population aged 20-79, approximately 1 in 9 individuals, are living with diabetes, and over 40% of them remain undiagnosed[3]Source: International Diabetes Federation, "Diabetes Facts & figures," idf.org. This growing health challenge is compelling healthcare systems to enhance diabetes management programs. These programs are increasingly incorporating sugar-free medications, syrups, and chewable tablets, while “diabetic-friendly” food products are gaining popularity in retail markets. Saccharin’s affordability compared to alternatives like stevia and sucralose makes it particularly attractive in lower-income markets, enabling its adoption across various product categories. Supporting this momentum, initiatives such as China’s nationwide health campaign to combat obesity and metabolic disorders, along with the World Health Organization’s (WHO) Global Diabetes Compact aimed at improving diagnosis and glycemic control, are embedding sugar-reduction measures into public health strategies. Together, these factors position saccharin as a critical ingredient in the long-term reformulation of health-focused products.

Pharmaceutical industry's shift toward sugar-free formulations

The pharmaceutical industry is rapidly transitioning toward sugar-free formulations, driving a significant increase in the demand for saccharin. This shift has elevated saccharin from being a secondary additive to a critical excipient in drug formulations. Sodium saccharin, known for its intense sweetness, stability across a wide range of pH levels, and compatibility with complex formulation systems, has become the leading choice for taste-masking in oral liquid medications and chewable tablets. Regulatory guidelines, which emphasize improving the palatability of pediatric medications and creating diabetic-friendly drug options, have further strengthened the need for sugar-free excipients. This trend has established saccharin as a long-term necessity in global pharmaceutical supply chains. Additionally, compliance with stringent requirements under leading pharmacopoeial standards, such as the United States Pharmacopeia (USP) and the European Pharmacopoeia (EP), limits the possibility of substitution. Consequently, certified suppliers benefit from strong customer retention and face minimal price competition. These factors ensure saccharin’s continued importance in pharmaceutical applications, where its functional reliability and regulatory approval make it indispensable in the industry’s move toward healthier, sugar-free drug delivery systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural sweetener revolution challenging artificial alternatives | -0.7% | North America and Europe | Medium term (2–4 years) |

| Regulatory scrutiny on artificial additives intensifying globally | -0.5% | Europe, North America | Medium term (2–4 years) |

| Stevia and monk fruit eroding saccharin's market position | -0.6% | North America and Europe | Long term (≥ 4 years) |

| Taste profile limitations restricting standalone applications | -0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Natural sweetener revolution challenging artificial alternatives

The global saccharin market is encountering significant challenges due to the growing popularity of natural sweeteners, which are reshaping consumer preferences, particularly in premium food and beverage sectors. In regions like North America and Europe, the increasing demand for clean-label products has created a ceiling for artificial sweeteners. Advancements such as enzyme-enhanced stevia, which reduces bitterness and improves the taste profile, are closing the gap that previously gave saccharin a competitive edge. As a result, saccharin manufacturers are shifting their focus to industries where cost efficiency and regulatory compliance are more critical than clean-label requirements. These industries include pharmaceuticals, animal feed, and institutional food services. This market shift has led to a clear division: premium segments are increasingly dominated by natural sweeteners, while saccharin remains competitive in bulk, cost-sensitive applications. In response, companies are prioritizing investments in high-purity pharmaceutical-grade production while scaling back on standard food-grade production. This strategic realignment underscores how evolving consumer expectations are reshaping the long-term growth strategies of saccharin manufacturers.

Regulatory scrutiny on artificial additives intensifying globally

Regulatory scrutiny is becoming a significant challenge for the global saccharin market, increasing the complexity of compliance requirements across both international and domestic regulations. The European Food Safety Authority (EFSA), while confirming the safety of saccharin, emphasized the need for stricter standards. These include more rigorous impurity limits and restrictions on specific manufacturing methods, which pose challenges for producers still using older production processes. Simultaneously, regulatory authorities in China are implementing updates that enforce tighter controls on residuals and contaminants. These changes are placing a heavier burden on smaller domestic manufacturers, prompting consolidation among larger, more established players. The combined impact of stricter export market requirements and evolving local standards is driving up compliance costs throughout the supply chain. This is slowing down capacity expansion and reshaping the competitive landscape, even as the underlying demand for saccharin remains strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pharmaceutical Pull Reshapes the Salt Hierarchy

In 2025, sodium saccharin, with a significant 72.12% share, continues to dominate the global saccharin market. Its leadership is driven by its excellent water solubility, comprehensive certifications from various pharmacopoeias, and proven reliability in applications such as beverages, pharmaceutical syrups, and oral care products. These characteristics make it the preferred choice for manufacturers who prioritize consistent performance and strict regulatory compliance, reinforcing its critical role in large-scale applications where reliability and adherence to standards are essential.

On the other hand, calcium saccharin is emerging as the fastest-growing segment, projected to achieve a CAGR of 5.98% between 2026 and 2031. Its growing appeal stems from its superior taste profile, particularly its reduced metallic aftertaste, which makes it ideal for premium oral care products, pediatric pharmaceutical formulations, and specific beverage blends. This trend highlights a strategic shift toward formulations that emphasize taste and palatability. Leading manufacturers are scaling up production capacity to meet the increasing demand from multinational fast-moving consumer goods (FMCG) companies and healthcare organizations. As a result, while sodium saccharin maintains its strong market position, calcium saccharin is steadily redefining the product landscape, establishing a distinct growth trajectory alongside the established dominance of sodium-based variants.

By Form: Powder Retains Structural Dominance Across Applications

Powder saccharin, which is projected to account for 87.35% of the global market in 2025, is not only the largest category but also the fastest-growing, with a CAGR of 6.43% expected from 2026 to 2031. This rare combination of market leadership and rapid growth highlights its exceptional versatility. Powder saccharin integrates seamlessly into various applications, including tablet compression, dry-mix beverages, pharmaceutical excipients (inactive substances used in drug formulations), and spray-dried preparations. Its low moisture content ensures a longer shelf life and compatibility with sensitive co-ingredients, making it a dependable choice for manufacturers. Additionally, its broad regulatory acceptance enhances operational efficiency, reinforcing its critical role as the backbone of the saccharin supply chain.

This dual leadership emphasizes powder saccharin's adaptability across both the food and pharmaceutical markets, enabling it to meet increasing demand while maintaining its dominant position. Unlike liquid saccharin, which is primarily used in ready-to-drink beverages and a limited range of pharmaceutical formulations, powder saccharin offers a broader manufacturing scope from a single inventory. Its ability to consistently deliver quality, meet regulatory requirements, and optimize costs ensures it remains the preferred format, driving the next phase of market growth.

By Application: Oral Care Emerges as Saccharin's Highest-Value Growth Vector

In 2025, the food and beverages segment dominated the global saccharin market, holding 63.86% of the total market share. This dominance is driven by saccharin’s cost-effectiveness, heat stability, and adherence to regulatory standards, making it a go-to ingredient for sugar-free products such as confectionery, baked goods, and beverages. Within this segment, the beverages category, especially zero-sugar carbonated soft drinks and flavored waters, accounts for a significant portion of the demand. Global brands are reformulating their products to align with sugar taxation policies and health regulations, further reinforcing saccharin’s essential role in mainstream food production.

At the same time, the personal care and oral care segment is projected to be the fastest-growing application, with a CAGR of 6.66% during the forecast period from 2026 to 2031. Saccharin’s non-cariogenic properties and its ability to mask the bitterness of fluoride and antibacterial agents make it a critical ingredient in products such as toothpaste, mouthwash, and denture adhesives. Unlike food applications, this segment faces minimal competition from natural sweeteners. Alternatives like stevia and monk fruit lack the pH stability and compatibility with abrasive silica systems required in dental care formulations. This competitive edge protects the oral care segment from the risks of clean-label substitutions, positioning it as the most promising growth area for saccharin and expanding its applications beyond the traditional food and beverage sectors.

Geography Analysis

In 2025, the Asia-Pacific region dominated the global saccharin market with a significant 46.10% market share and is expected to grow at a CAGR of 5.90% during the forecast period of 2026 to 2031. Asia-Pacific is driven by its dual role as a global production hub and a rapidly growing consumer base. China plays a central role in this dominance with its extensive manufacturing capabilities, which significantly influence international pricing and supply chains. At the same time, India is emerging as a key demand center, fueled by the expansion of its pharmaceutical industry and the high prevalence of diabetes. Additionally, regional health initiatives and stricter labeling regulations are driving domestic consumption, ensuring that Asia-Pacific maintains its leadership position in terms of both market size and influence.

North America and Europe, while considered mature markets, continue to hold strategic importance. Growth in these regions is shaped by regulatory frameworks and changing consumer preferences. In North America, domestic manufacturing provides a reliable supply, particularly for the pharmaceutical sector and institutional food service channels. However, the increasing demand for clean-label products has limited saccharin's use in premium consumer food products. In Europe, steady growth is supported by pharmaceutical production and reformulations driven by sugar taxes. Regulatory clarity from the European Food Safety Authority (EFSA) reinforces saccharin's relevance, even as consumer preferences shift toward natural alternatives.

South America and the Middle East and Africa, although smaller in market size, are emerging as regions with significant growth potential. Factors such as increasing urbanization, the expansion of processed food industries, and a growing diabetic population are driving demand for cost-effective sweeteners. Saccharin is often chosen over more expensive natural alternatives in these regions. In South America, Brazil and Argentina lead consumption, while South Africa and the United Arab Emirates (UAE) act as key import hubs in the Middle East and Africa. These regions are expected to grow at a rate faster than the global average, presenting promising opportunities for specialty pharmaceutical-grade saccharin as well as broader food applications.

Competitive Landscape

The global saccharin market is characterized by a fragmented competitive landscape, with Chinese commodity producers prioritizing cost efficiency and large-scale exports, while specialty manufacturers from India, Japan, and the United States focus on regulatory certifications, product quality, and reliable supply chains. Chinese companies dominate in terms of production volume and international distribution. On the other hand, Indian firms, such as Blue Jet Healthcare, have established themselves in high-purity, certified segments, catering to multinational fast-moving consumer goods (FMCG) and oral care brands. This dual structure creates an opportunity for mid-sized producers who can strike a balance between cost competitiveness and meeting pharmacopoeial certification standards, positioning themselves to capitalize on growth in emerging pharmaceutical excipient markets.

Competitive strategies are increasingly shifting towards backward integration and premium-grade product development as Chinese capacity consolidation puts pressure on commodity margins. Developments in trade policies, such as anti-dumping measures in related sweetener categories, are being closely monitored as they could set a precedent for saccharin. This highlights the critical importance of regulatory resilience. Producers with Good Manufacturing Practice (GMP)-compliant facilities, U.S. Food and Drug Administration (FDA) inspection clearances, and multi-standard certifications are better positioned to withstand trade disruptions. Meanwhile, Indian companies expanding into higher-margin pharmaceutical intermediates and contrast media are expected to drive significant competitive changes by using profits from these segments to support their saccharin investments.

Patent activity indicates that technical differentiation, particularly in impurity control and the adoption of environmentally friendly (green) chemistry processes, is becoming a key competitive advantage. In a market where pricing power alone is no longer sufficient, innovation in production methods and a focus on compliance-driven quality assurance are shaping the long-term strategic direction. This trend suggests that while cost leadership remains important, the future of saccharin competition will increasingly depend on technical expertise, regulatory trust, and alignment with evolving global health and sustainability standards.

Saccharin Industry Leaders

-

Kaifeng Xinghua Fine Chemical Ltd.

-

Blue Jet Healthcare Ltd.

-

PMC Specialties Group

-

Merck Group

-

JMC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Blue Jet Healthcare Limited commenced the construction of a greenfield pharmaceutical manufacturing facility at Rambilli Industrial Park, located in Anakapalli District, Andhra Pradesh, with an investment of INR 2,300 crore. Spanning 102 acres, the facility was planned to produce contrast media intermediates, high-intensity sweeteners (such as saccharin), and multipurpose chemistry products. The project followed a phased development approach, with initial commercial operations expected by the financial year 2028–2029. Once operational, the facility was projected to create approximately 1,750 direct jobs.

- December 2025: Henan Kaifeng Pingmei Shenma Xinghua Fine Chemical Company Limited participated in Food Ingredients Europe 2025, which took place in Paris from December 2 to December 4, 2025. The company showcased its sodium saccharin and spray-dried sodium saccharin product lines, drawing interest from global food and beverage buyers.

- July 2025: Blue Jet Healthcare Limited’s Board approved the acquisition of a 102.48-acre industrial land parcel in Rambilli Cluster Phase II, Anakapalli District, Andhra Pradesh. This land had been allocated by the Andhra Pradesh Industrial Infrastructure Corporation Limited (APIIC).

Global Saccharin Market Report Scope

Saccharin is a non-nutritive, artificial sweetener that is several hundred times sweeter than sugar and is widely used as a calorie-free substitute in foods, beverages, and pharmaceuticals. It is valued for its stability, versatility, and ability to mask bitterness in formulations.

The saccharin market is segmented based on product type, form, application, and geography. By product type, the market is segmented into sodium saccharin, calcium saccharin, and insoluble saccharin. By form, the market is segmented into liquid and powder. By application, the market is segmented into food and beverages, pharmaceuticals, personal care and oral care, animal feed, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The market forecasts are provided in terms of value (USD) and volume (in Tons).

| Sodium Saccharin |

| Calcium Saccharin |

| Insoluble Saccharin |

| Powder |

| Liquid |

| Food and Beverages | Bakery and Confectionery |

| Beverages | |

| Dairy Products | |

| Processed Foods | |

| Other Food Applications | |

| Pharmaceuticals | |

| Personal Care and Oral Care | |

| Animal Feed | |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Sodium Saccharin | |

| Calcium Saccharin | ||

| Insoluble Saccharin | ||

| Form | Powder | |

| Liquid | ||

| By Application | Food and Beverages | Bakery and Confectionery |

| Beverages | ||

| Dairy Products | ||

| Processed Foods | ||

| Other Food Applications | ||

| Pharmaceuticals | ||

| Personal Care and Oral Care | ||

| Animal Feed | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global saccharin market?

The market is valued at USD 487.83 million in 2025 and is projected to reach USD 662.03 million by 2031, growing at a CAGR of 5.38% during 2026–2031.

Which product type dominates the market?

Sodium Saccharin is the largest product type, holding 72.12% of the market in 2025, thanks to its solubility and widespread use in beverages, pharmaceuticals, and oral care.

Which form leads the market?

Powder form dominates with 87.35% share in 2025 and is also the fastest-growing form, projected at a CAGR of 6.43% through 2031, due to its versatility and long shelf life.

Which application is the largest?

Food and Beverages is the largest application segment, accounting for 63.86% of the market in 2025, supported by sugar-free confectionery, bakery, and beverage formulations.

Which region leads the global market?

Asia-Pacific is the largest regional market, holding 46.10% share in 2025, driven by China’s production dominance and India’s rising pharmaceutical demand.

Page last updated on: