Food Premix Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

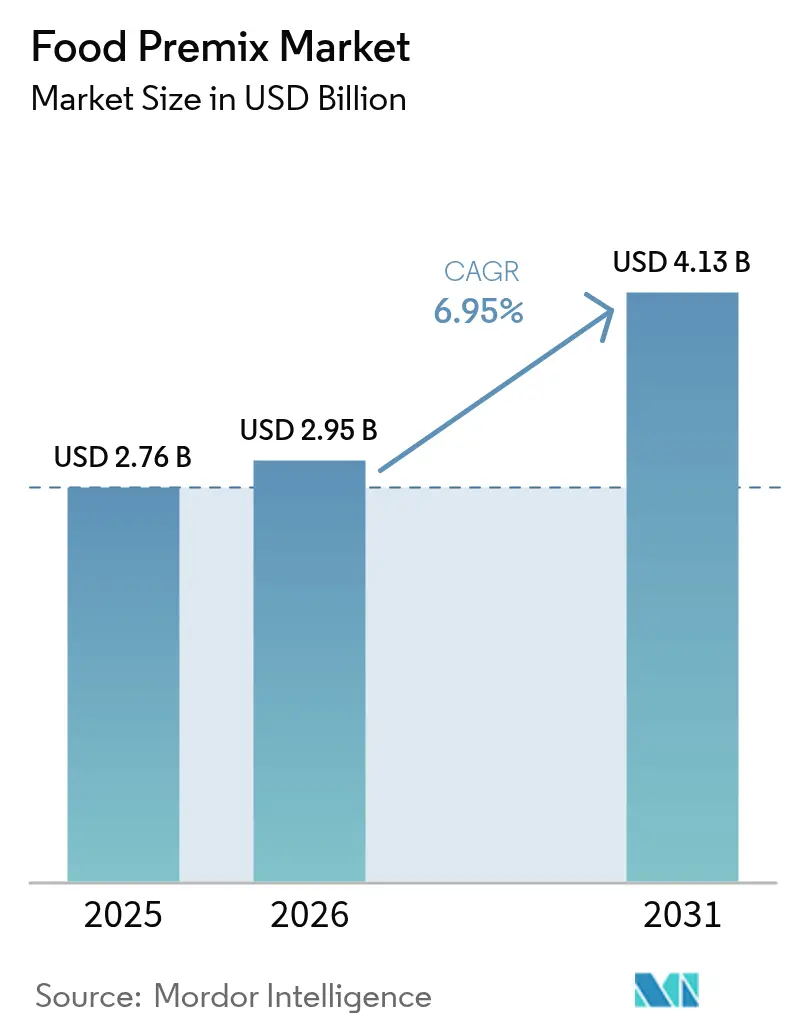

| Market Size (2026) | USD 2.95 Billion |

| Market Size (2031) | USD 4.13 Billion |

| Growth Rate (2026 - 2031) | 6.95% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food Premix Market Analysis by Mordor Intelligence

Food premix market size in 2026 is estimated at USD 2.95 billion, growing from 2025 value of USD 2.76 billion with 2031 projections showing USD 4.13 billion, growing at 6.95% CAGR over 2026-2031. Government-mandated fortification programs, increasing health awareness, and advancements in nutrient-delivery technologies drive the demand for premix solutions. Mandatory wheat flour fortification regulations across various countries and new folic acid requirements in the United Kingdom create stable demand for suppliers. The Asia-Pacific region maintains its position as the primary demand center, while South America experiences the fastest growth, driven by Brazil's expanding feed and food processing industries investing in fortified ingredients. The vitamin premix segment maintains its market leadership across various applications. Vitamin premixes, extensively used in food and beverage formulations and dietary supplements, enable manufacturers to fortify products with essential nutrients, including vitamins A, D, E, and B-complex. The dietary supplements segment has emerged as a significant growth area for premix manufacturers, as consumers across different age groups focus on preventive health measures, driving demand for premix solutions targeting fitness, mental wellness, and healthy aging.

Key Report Takeaways

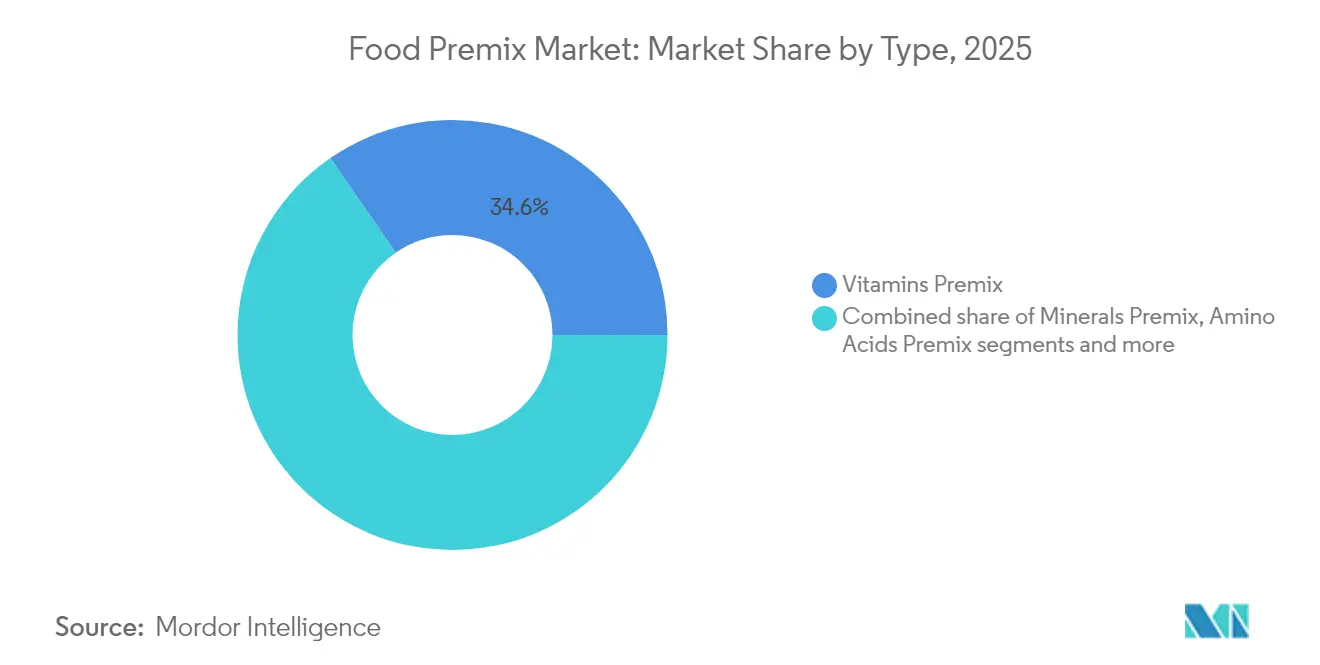

- By type, the vitamins premix segment led with 34.62% food premix market share in 2025, while amino acids are set to grow at a 8.87% CAGR between 2026-2031.

- By form, powder controlled 62.78% of the food premix market in 2025; liquid formulations posted the fastest 10.05% CAGR to 2031.

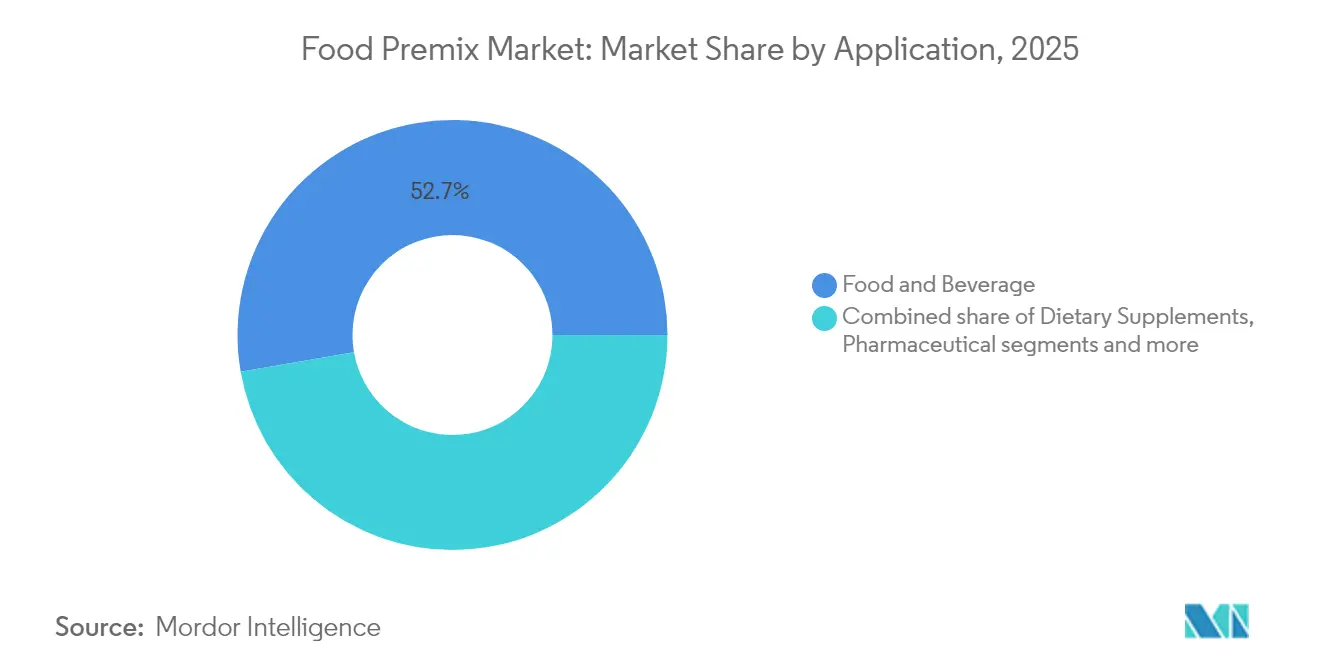

- By application, food and beverage held a 52.74% share of the food premix market size in 2025, whereas dietary supplements are projected to expand at a 9.55% CAGR through 2031.

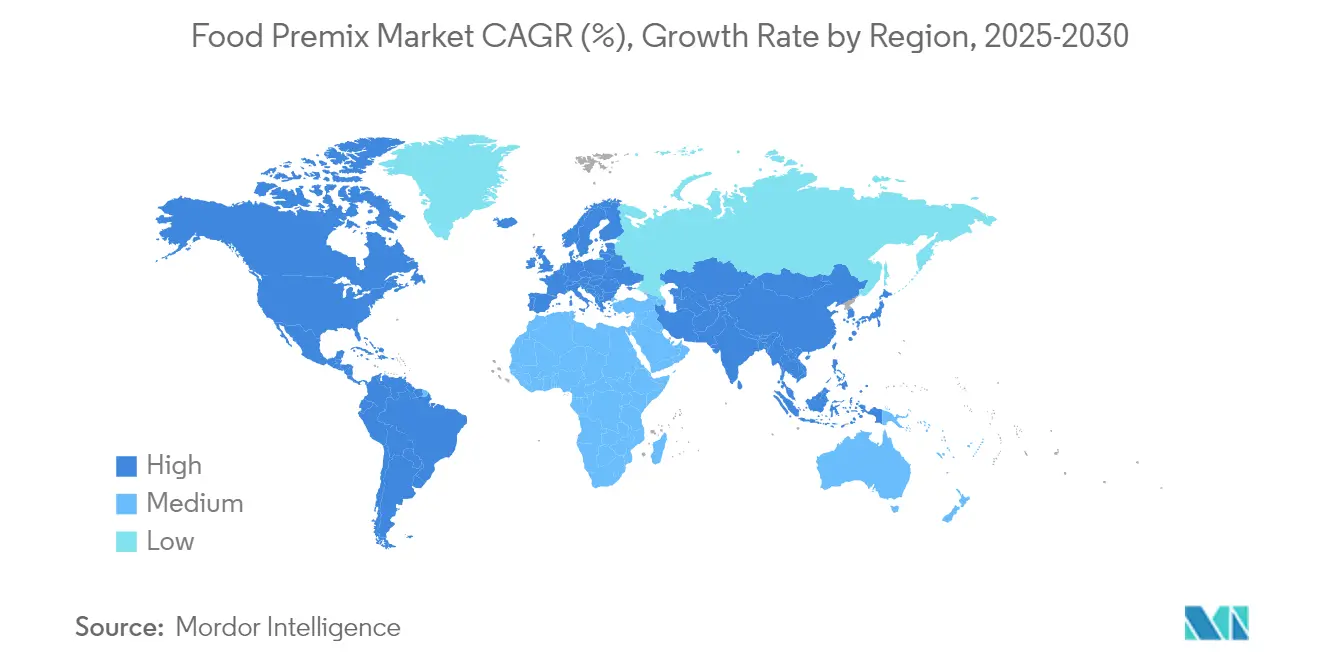

- By geography, Asia-Pacific captured 37.88% share in 2025, and South America is forecast to register a 8.91% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food Premix Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for functional and fortified food products | +1.8% | Global, with strongest uptake in North America and Europe | Medium term (2-4 years) |

| Growing adoption of preventive healthcare practices among consumers | +1.2% | Global, led by developed markets, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rising prevalence of micronutrient deficiencies | +1.5% | Asia-Pacific, Sub-Saharan Africa, with policy spillover to Latin America | Short term (≤ 2 years) |

| Accelerated growth of sports and active-nutrition supplements | +0.9% | North America and Europe core, expanding to Asia-Pacific urban centers | Medium term (2-4 years) |

| Government-led mandatory fortification programs | +2.1% | Global, with accelerated implementation in LMICs (Low- and Middle-Income Countries) | Short term (≤ 2 years) |

| Growth in personalized nutrition | +0.7% | North America and Europe, early adoption in Asia-Pacific metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Functional and Fortified Food Products

The growing inclination toward health and wellness is a key driver fueling the demand for functional and fortified food products in the food premix market. Modern lifestyles characterized by increased automation, reduced physical activity, and various socio-economic pressures have led to a surge in chronic health conditions. As a result, consumers are prioritizing health and nutrition, which is accelerating the shift toward foods enriched with essential nutrients. Functional foods fortified with vitamins, minerals, prebiotics, and amino acids are increasingly viewed as necessary for maintaining optimal bodily functions. Manufacturers are responding by expanding their product portfolios with nutrient-rich premixes to attract health-conscious consumers. According to the International Food Information Council (IFIC), in 2023, 28% of U.S. respondents identified a "good source of nutrients" as a key indicator of healthy food, while 33% associated healthiness with being a "good source of protein/amino acids" [1]Source: International Food Information Council, “2023 Food and Health Survey,” Food Insight, foodinsight.org . These statistics underscore the increasing consumer awareness and demand for fortified products, positioning the functional food segment as a key growth area within the food premix market.

Growing Adoption of Preventive Healthcare Practices Among Consumers

The preventive healthcare approach has transformed consumer behavior, as individuals increasingly view nutrition as a proactive health management tool rather than a response to illness. This transformation creates consistent and sustained demand for nutrient-dense products across all age demographics, generating stable and recurring revenue streams for food premix suppliers. Increasing healthcare costs in developed economies strengthen the demand for nutrition-based preventive measures. According to the OECD, the United States spent USD 13,432 per person on healthcare in 2023, the highest among member countries, significantly exceeding Switzerland, the second-highest spender. Norway, Germany, and Austria also demonstrate consistently high healthcare expenditure, indicating a broader pattern across developed nations [2]Source: Organization for Economic Co-operation and Development, “OECD Statistics,” OECD, stats.oecd.org. The market continues to experience significant growth through personalized nutrition, which provides comprehensive dietary recommendations based on individual genetic data. This approach has gained substantial adoption in developed markets where consumers demonstrate heightened awareness of the connection between diet, genetics, and disease prevention. The personalized nutrition trend enables premium pricing strategies, particularly in the dietary supplements segment, where customized premix formulations command higher price points.

Rising Prevalence of Micronutrient Deficiencies

Global micronutrient deficiency affects a substantial portion of the population, creating both a public health challenge and a market opportunity for food premix solutions. The economic impact of undernutrition, which results in reduced productivity and GDP losses across countries, has increased governmental and regulatory focus on mandatory food fortification programs. These programs generate consistent demand for premix solutions, particularly in staple foods, where fortification provides cost-effective and broad population coverage. In India, research by Tata 1mg Labs in 2023, conducted across 27 cities and involving 2.2 lakh individuals, revealed that 76% of the population had a Vitamin D deficiency. The study found higher prevalence among younger demographics, with 84% of individuals under 25 years and 81% in the 25-40 age group affected. The gender distribution showed a 75% deficiency in females and a 79% deficiency in males. These widespread deficiency rates across population segments demonstrate the need for targeted fortification approaches, driving increased demand for micronutrient premixes in the food industry. The combination of growing public awareness and stricter regulations continues to expand the market for premix solutions.

Accelerated Growth of Sports and Active-Nutrition Supplements

The sports nutrition segment has expanded beyond elite athletes to include mainstream consumers focused on active lifestyles, physical fitness, and overall well-being. This broader consumer base reflects changing lifestyle patterns and demographic shifts, including aging populations seeking to maintain physical function and younger generations incorporating fitness into their daily routines. The growth in the sports and active-nutrition supplements market has created opportunities for food premix suppliers. Consumers now demand products that support endurance, recovery, and general performance enhancement, increasing the need for specialized nutrient blends with proven effectiveness. The sports nutrition segment demonstrates strong price resilience, particularly for products with clinically validated performance claims. This enables premix suppliers to achieve higher margins through evidence-based formulations that align with consumer objectives. According to Sports Destination Management, 242 million Americans participated in at least one sports or fitness activity in 2023, representing nearly 80% of the U.S. population aged 6 and older. This figure shows a 2.2% increase from 2022 and represents the highest recorded participation in a single year [3]Source: Sports Destination Management, “A Record Number of Americans Participated in Sports, Fitness Activities in 2023,” Sports Destination Management, sportsdestinations.com. This increased physical activity highlights the growing importance of sports and active-nutrition supplements in daily wellness routines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating prices of raw materials used in premix formulations | -1.4% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Limited shelf life of certain premix ingredients | -0.8% | Global, particularly affecting liquid formulations | Medium term (2-4 years) |

| Competition from alternative fortification methods | -0.6% | Developed markets with established biofortification programs | Long term (≥ 4 years) |

| Risk of over-fortification | -0.9% | Developed markets with multiple fortified product exposure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fluctuating Prices of Raw Materials Used in Premix Formulations

Raw material prices experienced significant volatility, with vitamin markets facing major disruptions in 2024. According to DSM-Firmenich's Q3 2024 vitamin market update, multiple vitamin categories saw substantial price increases, with vitamin E prices reaching five-year highs due to supply disruptions and production facility incidents. The high concentration of vitamin production in China presents a systemic risk, prompting the American Feed Industry Association to advocate for domestic production investment. The supplement industry faces additional challenges from potential tariffs of 25% on Canadian and Mexican goods and 10% on Chinese imports, affecting ingredient sourcing costs. These market conditions have led premix manufacturers to implement hedging strategies and diversify their supply chains, which may limit their growth investments and margin expansion efforts.

Limited Shelf Life of Certain Premix Ingredients

Ingredient stability constraints create operational complexities that limit market expansion, particularly in emerging markets with extended distribution chains and variable storage conditions. The fundamental trade-off between nutrient potency and stability restricts formulation flexibility, especially for liquid premixes where bioavailability advantages must be balanced against reduced shelf life. The developments, such as Facilitated Self-Assembling Technology (FAST) for nanoparticle preparation, enhance the solubility and bioavailability of hydrophobic molecules without requiring surfactants or stabilizers. While these technological advances indicate potential reduction in stability constraints, current limitations affect product development timelines and market entry strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Vitamins Dominate While Amino Acids Surge

Vitamins premix holds a 34.62% market share in 2025, driven by its essential role in mandatory fortification programs and widespread consumer recognition. The segment's dominance is supported by regulatory requirements in 85 countries that mandate wheat flour fortification, enabling efficient large-scale production and consistent market demand. Amino acids premix is projected to grow at 8.87% CAGR (2026-2031), primarily due to increased demand in sports nutrition and personalized health solutions across global markets.

Minerals premix maintains consistent demand through fortification applications, while the "Others" category includes bioactive compounds and specialized formulations for diverse nutritional needs. The growth in amino acid premix is supported by extensive research validating its effectiveness in muscle recovery and cognitive function, allowing manufacturers to implement premium pricing strategies in various market segments. The market is evolving from basic nutrition supplementation to targeted health solutions, with amino acids emerging as a key segment for performance-focused applications and specialized nutritional requirements.

By Form: Powder Leads but Liquid Innovations Accelerate

Powder formulations hold a dominant 62.78% market share in 2025, due to their stability, cost-effectiveness, and established manufacturing processes. The powder segment benefits from longer shelf life, efficient logistics, and seamless integration with existing food processing equipment, making it the primary choice for large-scale fortification initiatives. The liquid premix segment is projected to grow at 10.05% CAGR (2026-2031), supported by higher bioavailability and versatile applications in beverage and dairy products.

The expansion of liquid premixes reflects manufacturers' focus on product differentiation, offering precise nutrient dosing and enhanced sensory properties. The powder segment continues to advance through liqui-solid technologies that convert liquid nutrients into free-flowing powders while retaining improved dissolution characteristics. This technological advancement indicates that future market development may favor combined approaches that integrate powder stability with liquid bioavailability benefits.

By Application: Food and Beverage Maturity Meets Dietary Supplements Dynamism

Food and beverage applications hold a 52.74% market share in 2025, forming the core of food premix demand through mandatory fortification requirements and established consumer products. This segment grows steadily due to population expansion and urbanization trends, supported by consistent regulatory frameworks and established market dynamics. The segment benefits from long-term stability and predictable volume growth patterns across global markets. Dietary supplements represent the fastest-growing application with a 9.55% CAGR (2026-2031), driven by increasing consumer focus on preventive healthcare and personalized nutrition. Growth in this segment reflects key demographic factors, including aging populations, higher healthcare costs, and increased health awareness among younger consumers, while also benefiting from technological advancements in delivery formats.

The pharmaceutical segment maintains consistent demand for therapeutic formulations that require precise dosing and strict regulatory compliance, with specialized requirements for stability and bioavailability. The food and beverage sector encompasses three main categories: dairy products, bakery and confectionery, and beverages. The beverage category shows significant innovation in functional drinks, while dairy and bakery segments demonstrate sustained demand. The segment's established market position generates reliable revenue streams that fund research and development in new applications, supporting continued innovation across product categories.

Geography Analysis

Asia-Pacific maintains a 37.88% market share in 2025, supported by comprehensive government fortification initiatives, ongoing urbanization trends, and increasing health awareness among the expanding middle-class population. The Asia-Pacific market operates under varied regulatory frameworks, with multiple growth opportunities. India's extensive school-meal programs and Japan's stringent Food for Specified Health Uses regulations maintain consistent market demand. Indonesia, Vietnam, and the Philippines have implemented simplified regulations for vitamin-mineral blends, reducing market entry timelines. Companies with strong regulatory compliance capabilities continue to gain competitive advantages in these dynamic markets.

South America records the highest growth at 8.91% CAGR (2026-2031), with Brazil's strong animal nutrition market and expanding food processing industry driving regional expansion. The region benefits from Feedlatina's regulatory harmonization efforts across Latin American animal feed industries, enabling sustained market growth and standardization that supports premix suppliers' regional operations.

North America and Europe maintain stable market positions with well-defined regulatory frameworks and sustained demand for premium formulations. The United Kingdom's 2024 flour fortification legislation updates, actively supported by Nutrition International, demonstrate ongoing regulatory developments that create substantial market opportunities in developed regions. The varied growth patterns across regions indicate that successful premix manufacturers must implement comprehensive region-specific approaches while effectively balancing global operational efficiency with local compliance requirements and evolving market preferences.

Competitive Landscape

The global food premix market reflects a moderately concentrated structure, with a handful of major players dominating due to their extensive product portfolios, global reach, and strong research and development capabilities. Key players like Glanbia PLC, DSM-Firmenich, Glanbia, Prinova Group LLC, and Corbion N.V. are steering the industry's direction through strategic shifts and innovation-driven growth.

DSM-Firmenich stands out with its significant move to divest its Animal Nutrition and Health division. This decision aims to reduce the earnings fluctuations tied to changing vitamin prices. It underscores a wider industry shift towards human nutrition applications, which promise steadier demand, better profit margins, and opportunities for innovative value addition. By emphasizing segments like sports and medical nutrition, as well as functional foods, these major players are aligning with consumer health trends and the market's push for clean labels and fortified offerings.

On the other hand, smaller and mid-sized companies are finding their niche by honing in on technological expertise rather than sheer size. They're making waves with innovations like patented microencapsulation for enhanced nutrient stability and bioavailability, and advanced nano-milling for optimal ingredient dispersion. Such specialized capabilities empower these niche firms to secure lucrative contracts with manufacturers in functional foods, beverages, and supplements, particularly in areas emphasizing personalized nutrition or adhering to specific regulations.

Food Premix Industry Leaders

Corbion N.V.

DSM-Firmenich

Prinova Group LLC

SternVitamin GmbH and Co. KG

Glanbia PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: At Vitafoods Europe 2025 in Barcelona, SternVitamin showcased its latest micronutrient premixes for women's health. The company presented solutions under the theme "Micronutrients for a healthy life," targeting women's nutritional needs across different life stages. The premixes address common deficiencies in iron, folic acid, and iodine, which women experience during pregnancy, menstruation, and menopause due to hormonal changes.

- June 2024: Sanku, part of the Millers for Nutrition coalition, launched East Africa's first commercial micronutrient premix blending facility in Dar es Salaam, Tanzania. The facility addresses high costs, poor quality, and import dependence by producing nutrient premixes locally for flour millers. Through local sourcing of ingredients and packaging, the facility improves affordability and logistics while supporting regional economic development.

- September 2023: Prinova launched a new range of premix solutions for the Asia-Pacific market at FiAsia Thailand in Bangkok. The product line includes three formulations targeting specific consumer needs: a dragon-fruit hydration drink with freeze-dried coconut water (Cococin), electrolytes, BCAAs, B vitamins, and antioxidants for lifestyle and replenishment; a matcha and white chocolate vegan beverage with pea and fava bean proteins for active lifestyle consumers; and a ginger and yuzu blend featuring EAAlpha essential amino acids, Aquamin, Curcumin C3 Reduct, and BioPerine to support muscle and bone health in aging consumers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the food premix market as the value of customized blends of vitamins, minerals, amino acids, and allied micronutrients that are supplied to food, beverage, and dietary-supplement makers to fortify or enrich finished products. According to Mordor Intelligence, only premixes sold for human nutrition and invoiced at the blender's factory gate are counted, whether delivered in powder or liquid form.

Scope exclusion: Animal-feed and veterinary premixes, stand-alone single-nutrient additives, and pharmaceutical active ingredients are not included.

Segmentation Overview

- By Type

- Vitamins Premix

- Minerals Premix

- Amino Acids Premix

- Others

- By Form

- Powder

- Liquid

- By Application

- Food and Beverage

- Dairy Products

- Bakery and Confectionery

- Beverages

- Others

- Dietary Supplements

- Pharmaceutical

- Others

- Food and Beverage

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- South Africa

- Saudi Arabia

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

To ground the desk findings, we interviewed premix formulation chemists, procurement heads at dairy, bakery, and beverage firms, contract blenders in North America, Europe, and Asia Pacific, and regional food-safety officials. The conversations tested usage ratios, average selling prices, and near-term demand signals, giving us firsthand checks on fortification volumes and pricing assumptions.

Desk Research

Our analysts began with publicly available material such as World Health Organization micronutrient deficiency dashboards, FAO fortification standards, Codex Alimentarius notifications, UN Comtrade trade codes for HS 2106 micronutrient blends, and USDA nutrient databases. Regulatory circulars from FSSAI, EFSA, and the US FDA clarified mandate timelines that influence demand. Company filings, investor decks, reputable press coverage, and paid assets like D&B Hoovers and Dow Jones Factiva helped to map producer capacity and recent price shifts. The sources named here illustrate the breadth of secondary inputs and are not an exhaustive list.

Market-Sizing & Forecasting

The core model starts with a top-down rebuild of global processed food and supplement output and applies premix penetration rates that vary by category and by geography. Results are then cross-checked through selective bottom-up supplier roll-ups and average price-per-kilogram sampling to refine totals. Key variables include fortified cereal production, liquid dairy output, mandated staple fortification coverage, vitamin spot prices, and the count of functional beverage launches. A multivariate regression links these drivers to historical premix sales, generating the base forecast, while scenario analysis stress-tests high and low adoption cases. Where bottom-up inputs are thin, proxy ratios from comparable countries or categories are used and later adjusted once new data arrive.

Data Validation & Update Cycle

Every model pass undergoes variance and reasonableness checks, followed by peer review and a senior analyst sign-off. Mordor refreshes the data annually and triggers interim updates when material policy or pricing events occur, ensuring clients receive the latest vetted view each time the study is delivered.

Why Mordor's Food Premix Baseline Commands Confidence

Published estimates often differ because firms pick dissimilar ingredient baskets, customer sets, and pricing levels. We acknowledge those gaps upfront so decision-makers understand why numbers vary.

Key gap drivers include whether infant-formula or animal-feed premixes are folded in, how aggressively retail mark-ups are layered on top of ex-factory prices, and the cadence at which models are refreshed. Mordor reports the ex-factory value of human-nutrition premixes only, applies validated average selling prices rather than retail tags, and updates the forecast every twelve months.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.76 B (2025) | Mordor Intelligence | - |

| USD 7.62 B (2024) | Global Consultancy A | Combines animal-feed and infant-formula premixes, inflating scope |

| USD 2.20 B (2024) | Industry Journal B | Limits coverage to eight major countries and excludes amino-acid blends |

| USD 7.65 B (2024) | Trade Insights C | Uses retail value of functional ingredients, not ex-factory premix pricing |

The comparison shows that once scope, geography, and pricing bases are aligned, Mordor's disciplined, variable-led approach supplies a balanced midpoint that clients can trace back to transparent inputs and repeatable steps, making it the dependable baseline for strategic planning.

Key Questions Answered in the Report

What is the current size of the food premix market?

The food premix market size reached USD 2.95 billion in 2026 and is projected to hit USD 4.13 billion by 2031 at a 6.95% CAGR.

Which region accounts for the largest food premix market share?

Asia-Pacific leads with 37.88% of global revenue in 2025, supported by extensive fortification mandates and strong food-processing growth.

Which application segment is growing fastest?

Dietary supplements are expected to expand at a 9.55% CAGR from 2026-2031 as consumers adopt proactive health and personalized nutrition regimes.

How are raw-material price swings affecting premix suppliers?

Vitamin price volatility and tariff risks increase input costs, prompting suppliers to diversify sourcing and hedge purchases, which can moderate profit expansion.

Page last updated on: