Palm Sugar Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.85 Billion |

| Market Size (2031) | USD 2.22 Billion |

| Growth Rate (2026 - 2031) | 3.74% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

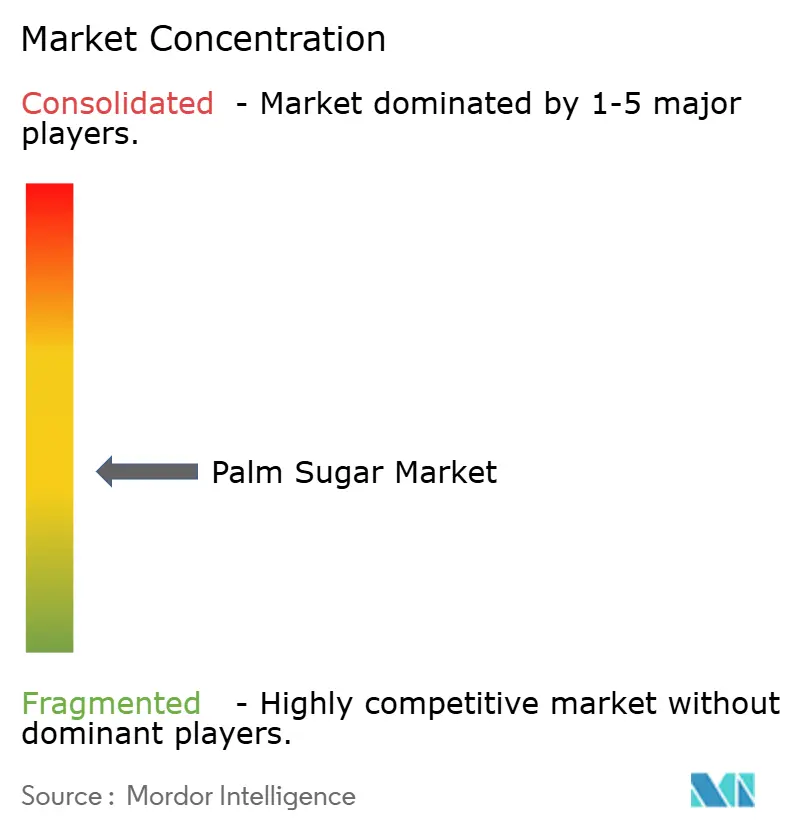

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Palm Sugar Market Analysis by Mordor Intelligence

The palm sugar market size was valued at USD 1.78 billion in 2025 and estimated to grow from USD 1.85 billion in 2026 to reach USD 2.22 billion by 2031, at a CAGR of 3.74% during the forecast period (2026-2031). Demand is rising for Western baked goods, beverages, and functional foods, where low-glycemic and clean-label claims resonate with health-conscious shoppers. Indonesia remains the anchor of global supply, yet value capture is shifting toward North American and European retailers that command higher unit prices for certified organic and single-origin offerings. Formulation advantages such as natural caramelization and trace-mineral content support premium pricing, while modest overall growth reflects a maturing production base and competition from other natural sweeteners. Compliance with the EU Deforestation Regulation and similar traceability mandates is already reshaping sourcing strategies for major importers.

Key Report Takeaways

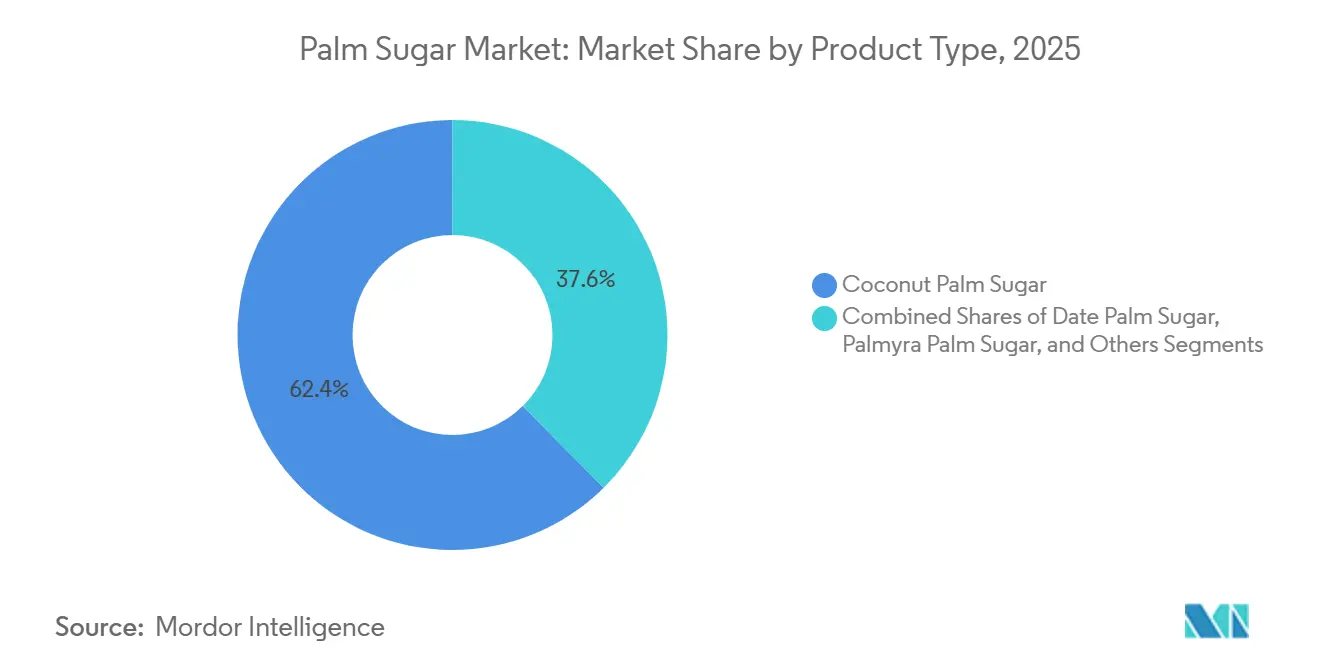

- By product type, coconut palm sugar accounted for a 62.42% share of the palm sugar market in 2025, and palmyra palm sugar will expand at a CAGR of 5.25% through 2031.

- By form, granulated variants led with a 41.18% share of the palm sugar market in 2025, while the same format will record the fastest CAGR of 6.14% through 2031.

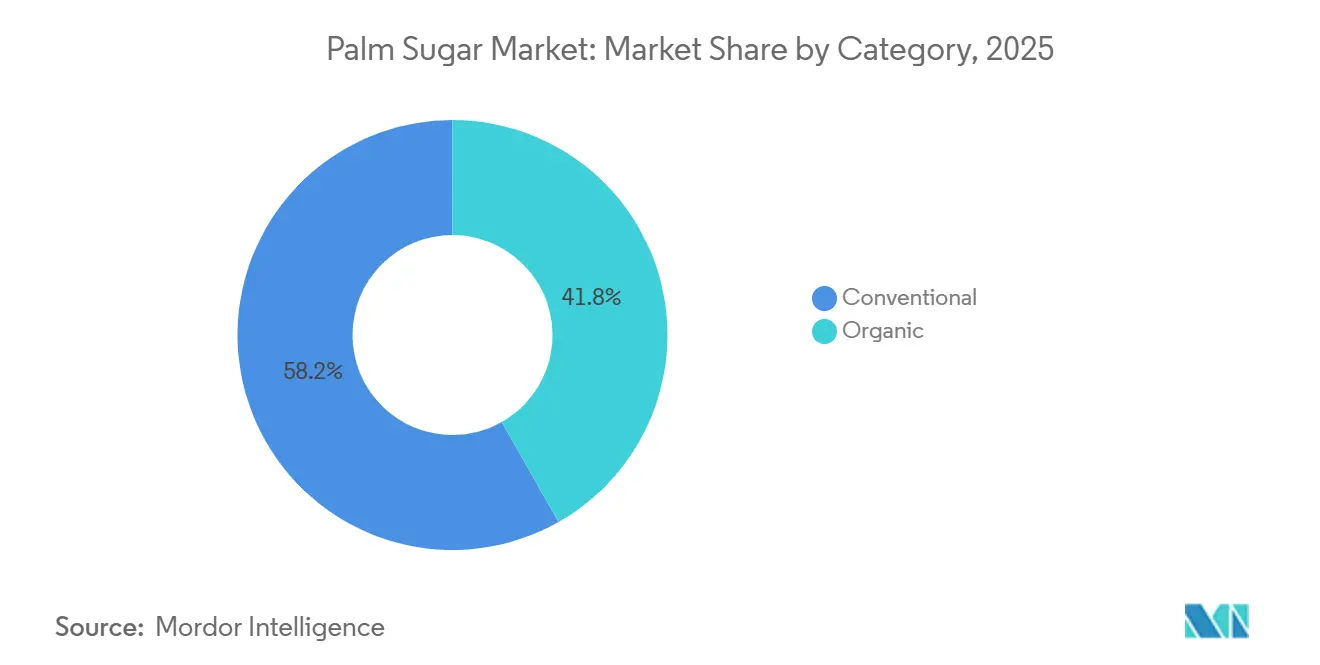

- By category, conventional grades accounted for 58.21% of the palm sugar market in 2025, while organic variants will grow at a CAGR of 5.48% through 2031.

- By application, bakery and confectionery captured 36.44% of the palm sugar market size in 2025; dairy and frozen desserts will post the fastest CAGR of 5.57% through 2031.

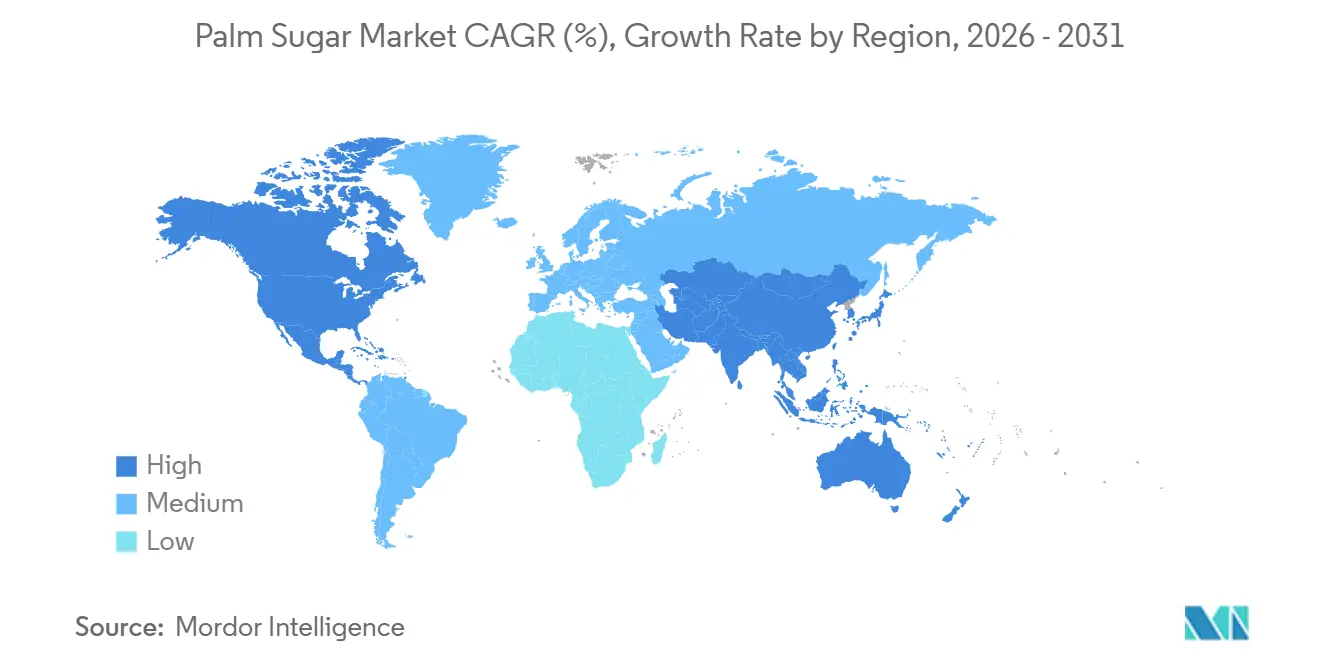

- By geography, Asia-Pacific dominated with a 50.48% market share in 2025, whereas North America will post the highest CAGR of 5.48% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Palm Sugar Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for unrefined sweeteners with trace minerals | +0.8% | Global, with strongest uptake in North America and Europe | Medium term (2-4 years) |

| Expansion of artisanal and ethnic food segments globally | +0.6% | North America, Europe, urban centers in Asia-Pacific | Medium term (2-4 years) |

| Growing demand for natural caramelization agents in food processing | +0.5% | Global, particularly in bakery and confectionery hubs | Short term (≤ 2 years) |

| Application in functional beverages using traditional sweeteners | +0.4% | Asia-Pacific core, spill-over to North America and Middle East | Medium term (2-4 years) |

| Product innovation in granulated and liquid palm sugar formats | +0.5% | Global, led by Southeast Asian processors and North American importers | Short term (≤ 2 years) |

| Popularity in gourmet and specialty coffee sweetening | +0.3% | North America, Europe, urban Asia-Pacific (Melbourne, Los Angeles, Jakarta) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demand for unrefined sweeteners with trace minerals

Palm sugar's mineral profile, potassium, magnesium, zinc, and iron, positions it as a functional ingredient rather than a commodity sweetener, enabling premium pricing in health-food channels. The glycemic index of coconut palm sugar ranges from 35 to 42, significantly below table sugar's 65, making it attractive to the 84 million consumers who adopted low-glycemic diets in 2024. This positioning is particularly effective in North America and Europe, where clean-label regulations and consumer skepticism of artificial additives drive reformulation. However, the mineral content varies by sap source, processing method, and storage conditions, creating quality-control challenges for industrial buyers who require batch-to-batch consistency. Producers are responding by implementing Indonesian National Standard SNI 01-3743-2021, which specifies maximum moisture content below 2% and minimum sucrose levels, but enforcement remains uneven across smallholder cooperatives, according to Tradin Organic.

Expansion of artisanal and ethnic food segments globally

The kopi susu gula aren trend, Indonesian coffee layered with palm sugar syrup, has migrated from Jakarta street stalls to specialty cafes in Melbourne and Los Angeles, demonstrating how ethnic beverages can cross over into mainstream foodservice. Chains such as Kopi Kenangan and Janji Jiwa scaled this format domestically, and their photogenic layered drinks drive social media engagement that helps younger consumers trial. Artisanal bakeries in Europe are incorporating palm sugar into sourdough and pastry formulations to achieve deeper caramelization and extended shelf life, capturing premiums of 15% to 20% over conventional sugar-based products. The challenge lies in educating chefs and product developers on substitution ratios: palm sugar's hygroscopic nature requires minor liquid adjustments in light sponges and meringues, and its lower melting point affects confectionery texture. Tradin Organic's 3-year grant from the Dutch Social Sustainability Fund, announced in 2024, targets 2,275 smallholder farmers in Central Java with training on organic integrity and food safety, aiming to standardize quality for export to artisanal and specialty channels[1]Source: Tradin Organic, “Impact Project Launched for Safe, Organic Coconut Sugar Production,” tradinorganic.com.

Growing demand for natural caramelization agents in food processing

Palm sugar's low reducing sugar content and amino acids accelerate Maillard reactions, delivering deeper browning and richer flavor in baked goods, sauces, and marinades without artificial colorants. This functional advantage is particularly valuable in clean-label formulations where manufacturers seek to eliminate caramel color (E150) and other synthetic additives. Industrial bakeries are adopting granulated palm sugar in cookie and cake batters to achieve consistent browning and moisture retention, which extends shelf life by 10% to 15% compared to sucrose-based formulations. The trade-off is cost: palm sugar typically retails at USD 4.50 to USD 6.50 per kilogram FOB for conventional grades and USD 15 to USD 27 per kilogram at European retail, versus USD 0.50 to USD 1.00 per kilogram for refined cane sugar, according to The Netherlands Ministry of Foreign Affairs, CBI. Processors targeting premium segments can absorb this differential, but mass-market applications remain price-sensitive, limiting penetration in cost-driven categories such as carbonated soft drinks and confectionery.

Application in functional beverages using traditional sweeteners

Functional beverage formulators are incorporating palm sugar into plant-based milks, cold-brew coffee, and ready-to-drink teas to leverage its low glycemic index and trace mineral content. Liquid palm sugar syrups dissolve rapidly in cold liquids, making them suitable for smoothies and protein shakes where granulated sweeteners can settle or clump. Palm Nectar Organics opened a 4,500-metric-ton liquid palm sugar plant in Vietnam in 2024, targeting beverage manufacturers in Southeast Asia and North America. The Southeast Asia ice cream market is adopting palm sugar in non-dairy formulations that score higher in sensory tests for flavor complexity and mouthfeel. However, beverage applications face formulation challenges: palm sugar's hygroscopic nature can cause syrup crystallization during storage, and its caramel notes may clash with delicate fruit or floral flavors, requiring careful flavor balancing.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited industrial-scale processing infrastructure for value-added forms | -0.6% | Asia-Pacific production hubs (Indonesia, Thailand, Philippines) | Medium term (2-4 years) |

| Competition from lower-cost natural sweeteners | -0.5% | Global, particularly in price-sensitive North American and European retail | Short term (≤ 2 years) |

| Challenges in organic certification and traceability compliance | -0.4% | Asia-Pacific smallholder regions, export-oriented producers | Long term (≥ 4 years) |

| Moisture sensitivity leading to clumping and handling issues | -0.2% | Global, affecting granulated formats in humid climates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited industrial-scale processing infrastructure for value-added forms

Palm sugar production remains dominated by smallholder cooperatives and artisanal processors who lack the capital and technical expertise to produce consistent granulated, liquid, and powdered formats at an industrial scale. Approximately 1,400 plantations experienced production disruptions in 2024 due to labor shortages, and only USD 260 million of the USD 420 million in global supply-chain investment targeted Southeast Asia, leaving significant infrastructure gaps. The Indonesian Ministry of Industry partnered with PalmCo and Gerak Nusantara Producers Cooperative in April 2025 to promote palm sugar production from oil palm trunks, estimating that a single tree yields 6.8 liters of sap per day during a 1.5- to 2-month tapping period, with a net profit of IDR 18 million to IDR 25 million (approximately USD 1,150 to USD 1,600) per farmer. However, basic sap-processing equipment requires an estimated IDR 25 million (approximately USD 1,600) per hectare, a prohibitive upfront cost for smallholders without access to credit. The result is a two-tier market: large exporters such as Big Tree Farms and Asia Palm Coco invest in centralized drying and granulation facilities, while smallholders produce block and paste forms that command lower prices and face quality-control issues. This infrastructure gap constrains the supply of premium granulated and liquid formats that foodservice and industrial buyers demand, limiting market growth.

Challenges in organic certification and traceability compliance

USDA Organic certification requires a 36-month transition period, costs USD 500-2,400 in the first year, and mandates 5-year record-keeping with lot-code farm-to-export tracking. EU Organic certification requires a Certificate of Inspection via the TRACES system, and the EU Deforestation Regulation mandates geolocation data and proof of no deforestation after December 31, 2020, according to the European Commission[2]Source: European Commission, “Regulation on Deforestation-free Products,” Environment, environment.ec.europa.eu. Smallholder farmers in Indonesia, Thailand, and the Philippines often lack the literacy, digital tools, and administrative capacity to maintain the documentation required for organic certification, and the 36-month transition period during which they cannot sell product as organic creates cash-flow challenges. Tradin Organic's 3-year grant targets these gaps by providing training on organic integrity, food safety, and traceability, but the program reaches only 2,275 farmers in Central Java, a fraction of the estimated 22,000 palm tappers in Banyumas district alone. The USDA cost-share program covers up to USD 750, or 75% of certification costs, but many smallholders are unaware of this support or lack the documentation required to apply. The result is a bifurcated market: large exporters with centralized quality-control systems can secure organic certification and command premiums, while smallholders remain locked into conventional markets with lower pricing and limited growth prospects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Coconut Palm Dominates, Palmyra Gains Momentum

Coconut palm sugar commanded 62.42% market share in 2025, reflecting its established supply chains, mild flavor profile, and widespread availability across Indonesia, the Philippines, and Thailand. Date palm sugar serves niche Middle Eastern and North African markets where cultural familiarity and halal certification drive demand, while Palmyra palm sugar is expanding at 5.25% CAGR through 2031, the fastest growth among product types. Palmyra palm (Borassus flabellifer) yields up to 20 liters of sap per day per tree, nearly three times the output of coconut palms. However, Palmyra palms require 12 to 20 years to reach maturity, creating a near-term supply bottleneck that limits immediate scale-up. The "Others" category, which includes toddy palm and nipa palm sugars, remains marginal due to limited production volumes and regional supply constraints.

Coconut palm sugar benefits from Indonesia's dominance; the country supplies approximately 90% of global output, with the Greater Banyumas region alone accounting for 80% of Indonesian production, according to ANTARA. This concentration creates supply resilience but also vulnerability: weather disruptions, labor shortages, or policy changes in Indonesia can ripple through global markets. Date palm sugar's growth is constrained by limited sap availability, as date palms are primarily cultivated for fruit rather than sap, and tapping reduces fruit yields. Palmyra palm sugar's expansion is driven by government support in India and Thailand, where ministries of agriculture provide subsidies for seedling distribution and tapping equipment. The product-type segmentation underscores a strategic tension: buyers seeking supply diversification are exploring Palmyra and date palm sugars, but the infrastructure and farmer networks required to scale these alternatives remain underdeveloped. Coconut palm sugar will retain dominance through 2031, but its share will erode as Palmyra and date palm production scales.

By Form: Granulated Leads, Liquid Formats Gain Traction

Granulated palm sugar held 41.18% market share in 2025 and will grow at 6.14% CAGR through 2031, the fastest rate among form types, driven by its versatility, shelf stability, and compatibility with existing bakery and foodservice equipment. Liquid and syrup formats accounted for approximately 22% of the market in 2025 and are expanding rapidly in ready-to-drink beverages, sauces, and quick-service restaurants, where they eliminate the dissolution step and integrate seamlessly into automated dispensing systems. Block-and-paste forms, which represent the traditional artisanal product, are growing more slowly because they require grating or dissolving before use, limiting their appeal to industrial buyers. PT Rumah Seho Nusantara and other Indonesian exporters introduced liquid palm sugar syrups in 2024 to serve beverage manufacturers seeking operational efficiency and consistent Brix levels.

Granulated formats benefit from Royal Pepper Company's enzymatic crystallization process, which extends shelf life by 40% by reducing hygroscopicity and preventing clumping. Powdered palm sugar, milled to fine mesh, is gaining traction in instant beverage mixes and chocolate confectionery, where rapid dissolution is critical. The challenge for liquid formats is logistics: higher water content increases shipping weight and refrigeration requirements, raising landed costs for importers. Producers are responding by concentrating syrups to 75 to 80 Brix and offering aseptic packaging that extends ambient shelf life to 18 months. Block and paste forms retain cultural significance in Southeast Asian cuisines, where they are used in traditional desserts and savory dishes, but their growth is constrained by limited export appeal and the need for consumer education on usage. The form segmentation highlights a bifurcation: granulated formats dominate retail and bakery channels, while liquid formats are capturing growth in foodservice and industrial applications that prioritize operational efficiency over traditional presentation.

By Category: Conventional Leads, Organic Surges

Conventional palm sugar accounted for 58.21% of the market in 2025, reflecting lower production costs, established supply chains, and broader availability across price-sensitive retail channels. Organic palm sugar, though smaller in volume, is expanding at a 5.48% CAGR through 2031, driven by the uptake of USDA Organic and EU Organic certifications among Indonesian and Philippine smallholders. Tradin Organic's 3-year grant from the Dutch Social Sustainability Fund, announced in 2024, targets 2,275 smallholder farmers in Central Java with training on organic integrity, food safety, and productivity, aiming to standardize quality for export to premium channels. USDA Organic certification requires a 36-month transition period, costs USD 500-2,400 in the first year, and mandates 5-year record-keeping with lot-code farm-to-export tracking, creating barriers for smallholders without access to credit or administrative support[3]Source: U.S. Department of Agriculture, “Becoming Certified—Organic Certification,” ams.usda.gov.

Organic palm sugar commands premiums of 30% to 50% over conventional grades, with retail prices ranging from USD 15 to USD 27 per kilogram in Europe versus USD 4.50 to USD 6.50 per kilogram FOB for conventional grades, according to the Center for the Promotion of Imports. The demand for organic sweeteners is expanding as clean-label regulations and consumer preferences drive reformulation. Center and administrative capacity to maintain the documentation required for certification. The USDA cost-share program covers up to USD 750, or 75% of certification costs, but awareness and uptake remain low. Big Tree Farms and other large exporters are investing in farmer support programs that provide training, advance payments, and centralized quality control to facilitate organic certification, but these initiatives reach only a fraction of the smallholder base. The category segmentation underscores a structural challenge: organic palm sugar offers higher margins and growth potential, but scaling organic supply requires sustained investment in farmer education, traceability systems, and certification support that many cooperatives cannot afford.

By Application: Bakery Dominates, Dairy Accelerates

Bakery and confectionery applications accounted for 36.44% of palm sugar demand in 2025, driven by its functional advantages in caramelization, moisture retention, and shelf-life extension. Dairy and frozen desserts represent the fastest-growing application, with a 5.57% CAGR through 2031, as ice-cream formulators substitute refined sugar to meet clean-label mandates and capture premiums in non-dairy segments. An ICAR study demonstrated that coconut sugar effectively substitutes refined sugar in ice cream, contributing to solids-not-fat content while increasing phenolic compounds and minerals, and non-dairy formulations scored higher in sensory tests for flavor complexity and mouthfeel. The Southeast Asia ice cream market is adopting palm sugar in non-dairy formulations that appeal to lactose-intolerant and vegan consumers.

Beverages, including plant-based milks, cold-brew coffee, and ready-to-drink teas, are incorporating palm sugar to leverage its low glycemic index and trace mineral content, and 380 new functional food products featuring palm sugar launched in 2024. Nutraceuticals and functional foods are adopting palm sugar as a clean-label sweetener that aligns with vegan, paleo, and keto diets, and Global Organics positions coconut sugar for diabetic-friendly products targeting the 84 million consumers who adopted low-glycemic diets in 2024. Household use remains significant, particularly in Southeast Asia, where palm sugar is a pantry staple for traditional cooking and baking. Foodservice and B2B channels are expanding as restaurants, cafes, and quick-service restaurants adopt palm sugar to differentiate menus and meet clean-label demands, but adoption is constrained by handling complexity and higher costs compared to refined sugar. The application segmentation highlights a strategic opportunity: dairy and frozen desserts offer the highest growth potential, but capturing this segment requires formulation support, technical documentation, and consistent supply of granulated and powdered formats that meet industrial specifications.

Geography Analysis

Asia-Pacific accounted for 50.48% of the palm sugar market in 2025, led by Indonesia, which accounted for approximately 90% of the global coconut palm sugar supply. The Greater Banyumas region in Central Java alone accounts for 80% of Indonesian production, and district authorities initiated a transition from tall coconut trees to dwarf varieties in 2025, allowing tappers to harvest up to 100 trees per day versus 25 for generic trees, quadrupling productivity and improving worker safety, according to ANTARA. Thailand and the Philippines contribute additional supply, with Thailand's Palmyra palm sector demonstrating a benefit-cost ratio of 11.30 and an internal rate of return of 28%, making it economically attractive for smallholders. However, the region faces infrastructure constraints: approximately 1,400 plantations experienced production disruptions in 2024 due to labor shortages. The Indonesian Ministry of Industry partnered with PalmCo and Gerak Nusantara Producers Cooperative in April 2025 to promote palm sugar production from oil palm trunks, estimating net profit of IDR 18 million to IDR 25 million (approximately USD 1,150 to USD 1,600) per farmer, but basic sap-processing equipment requires an estimated IDR 25 million (approximately USD 1,600) per hectare, a prohibitive upfront cost for smallholders without access to credit, according to the Palm Oil Magazine. China, India, Japan, and Australia represent growing demand centers within Asia-Pacific, driven by rising health consciousness and adoption of plant-based diets.

North America is the fastest-growing region at 5.48% CAGR through 2031, reflecting accelerated import growth and premium positioning in health-food and specialty channels. Canada and Mexico are also expanding, with Mexico serving as a re-export hub for Latin American markets. Europe is growing steadily, with Germany, the United Kingdom, Italy, France, Spain, and the Netherlands leading demand, driven by the EUR 47 billion organic market and stringent clean-label regulations. The EU Deforestation Regulation, effective since 2023, mandates geolocation data and proof of no deforestation after December 31, 2020, adding compliance complexity for exporters targeting European buyers. Big Tree Farms launched a blockchain traceability platform in 2024 to meet these requirements, and 56 exporters adopted blockchain for origin verification.

South America, led by Brazil and Argentina, represents an emerging opportunity, with specialty and gourmet producers adopting palm sugar in artisan bakery and confectionery applications, though volumes remain modest. The Middle East and Africa, including Saudi Arabia, the United Arab Emirates, and South Africa, are expanding as halal certification and health-conscious consumer segments drive demand, but market penetration is constrained by limited distribution infrastructure and consumer awareness. The Philippines exported muscovado (non-centrifugal sugar) at approximately USD 2.25 per kilogram to Europe and Japan, where buyers are willing to pay premium prices, versus PhP 130 per kilogram (approximately USD 2.30) domestically, highlighting the pricing arbitrage available in export markets, according to the Centre for the Promotion of Imports, Europe. The geographic segmentation underscores a structural dynamic: Asia-Pacific will retain production dominance, but value capture is migrating to North American and European retail and foodservice channels that command higher per-kilogram pricing for certified organic and single-origin products.

Competitive Landscape

The palm sugar market exhibits moderate fragmentation, indicating that the top 5 players, Big Tree Farms, Medikonda Nutrients, PMA Organics, Asia Palm Coco, and Betterbody Foods, collectively hold meaningful but not dominant shares, leaving room for regional specialists and private-label entrants. Big Tree Farms secured USD 10 million from Mirova in January 2026 to expand its farmer network from 17,000 to 25,000 and double production capacity, while also launching blockchain traceability to meet EU Deforestation Regulation requirements. The company distributed 42,000 metric tons in 2024 and launched Naughty Bali BBQ sauces in March 2025 at Sprouts and Publix, demonstrating a strategy to capture downstream value through branded consumer products.

Above Food Ingredients signed a Letter of Intent in February 2025 to acquire Palm Global Technologies for approximately USD 180 million, combining Above Food's sustainable food systems with Palm Global's agri-tech, fintech, and carbon-credit securitization platforms to support tens of millions of farmers across Africa, Southeast Asia, and the Americas. Strategy patterns include vertical integration into farmer networks, investment in traceability and certification, and product-format diversification to serve retail, foodservice, and industrial channels. White-space opportunities exist in liquid-syrup formats for quick-service restaurants, powdered formats for instant beverage mixes, and flavored variants for gourmet retail. Emerging disruptors include Palm Nectar Organics, which opened a 4,500-metric-ton liquid palm sugar plant in Vietnam in 2024, and Royal Pepper Company, which developed an enzymatic crystallization process that extends shelf life by 40%.

Technology adoption is accelerating: 56 exporters adopted blockchain for origin verification in 2024, and approximately 35% of producers are integrating advanced processing technology to improve consistency and reduce moisture content. Tradin Organic's 3-year grant from the Dutch Social Sustainability Fund targets 2,275 smallholder farmers in Central Java with training on organic integrity, food safety, and productivity, aiming to standardize quality for export to premium channels. The competitive landscape underscores a bifurcation: large exporters with centralized quality-control systems and farmer support programs are capturing premium segments, while smallholder cooperatives remain locked into conventional markets with lower pricing and limited growth prospects. The challenge for incumbents is to scale organic and value-added production without alienating smallholder suppliers, while new entrants must navigate complex certification requirements and establish farmer networks in a market where relationships and trust are critical.

Palm Sugar Industry Leaders

Big Tree Farms

Medikonda Nutrients

PMA Organics (Lewi's Organics)

Asia Palm Coco

Betterbody Foods & Nutrition LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Big Tree Farms had secured USD 10 million in investment from Mirova, aiming to expand its farmer network from 17,000 to 25,000, double its production capacity, and launch a blockchain traceability platform. This move was to align with the EU Deforestation Regulation, ensuring geolocation data and proof of no deforestation.

- May 2025: The Indonesian government expanded sugar palm plantations as part of its strategy to boost bioethanol production and enhance energy self-sufficiency.

- April 2025: The Indonesian Ministry of Industry partnered with PalmCo/PTPN IV and Gerak Nusantara Producers Cooperative to promote palm sugar production from oil palm trunks, estimating net profit of IDR 18 million to IDR 25 million (approximately USD 1,150 to USD 1,600) per farmer and requiring an estimated IDR 25 million (approximately USD 1,600) per hectare for basic sap-processing equipment

Global Palm Sugar Market Report Scope

Palm sugar is a natural sweetener derived from the sap of various palm trees, known for its rich flavor and minimal processing. The palm sugar market is segmented by product type, form, category, application, and geography. By product type, the market includes coconut palm sugar, date palm sugar, palmyra palm sugar, and others such as toddy and nipa. By form, the market is categorized into granulated, liquid/syrup, and blocks/paste. By category, the market is divided into organic and conventional products. Based on application, the market covers bakery and confectionery, beverages, dairy and frozen desserts, nutraceuticals and functional foods, household consumption, foodservice/B2B, and other applications. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market sizes and forecasts for each region. For each segment, market sizing and forecasts have been conducted on a value basis (USD million).

| Coconut Palm Sugar |

| Date Palm Sugar |

| Palmyra Palm Sugar |

| Others (Toddy, Nipa, etc.) |

| Granulated |

| Liquid/Syrup |

| Blocks/Paste |

| Organic |

| Conventional |

| Bakery and Confectionery |

| Beverages |

| Dairy and Frozen Desserts |

| Nutraceuticals and Functional Foods |

| Household |

| Foodservice/B2B |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Product Type | Coconut Palm Sugar | |

| Date Palm Sugar | ||

| Palmyra Palm Sugar | ||

| Others (Toddy, Nipa, etc.) | ||

| By Form | Granulated | |

| Liquid/Syrup | ||

| Blocks/Paste | ||

| By Category | Organic | |

| Conventional | ||

| By Application | Bakery and Confectionery | |

| Beverages | ||

| Dairy and Frozen Desserts | ||

| Nutraceuticals and Functional Foods | ||

| Household | ||

| Foodservice/B2B | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the palm sugar market and its growth outlook?

The palm sugar market is valued at USD 1.78 billion in 2025 and is set to reach USD 2.22 billion by 2031, indicating a projected CAGR of 3.74% from 2026 to 2031.

Which form is growing fastest within the palm sugar market?

Granulated palm sugar is projected to register a 6.14% CAGR through 2031 thanks to shelf stability and compatibility with industrial bakery equipment, as reported by Mordor Intelligence.

How large is the North American opportunity?

North America records the highest regional CAGR at 5.48%, driven by specialty coffee, functional beverages, and clean-label bakery reformulations.

Who are the leading companies?

Big Tree Farms, Medikonda Nutrients, PMA Organics, Asia Palm Coco, and Betterbody Foods together anchor the competitive landscape but hold only moderate combined share, leaving room for new entrants.

What are the main restraints on palm sugar adoption?

Limited processing infrastructure, competition from cheaper natural sweeteners, certification costs, and moisture-related handling issues jointly temper growth potential, based on Mordor Intelligence findings.

Page last updated on: