Succinic Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

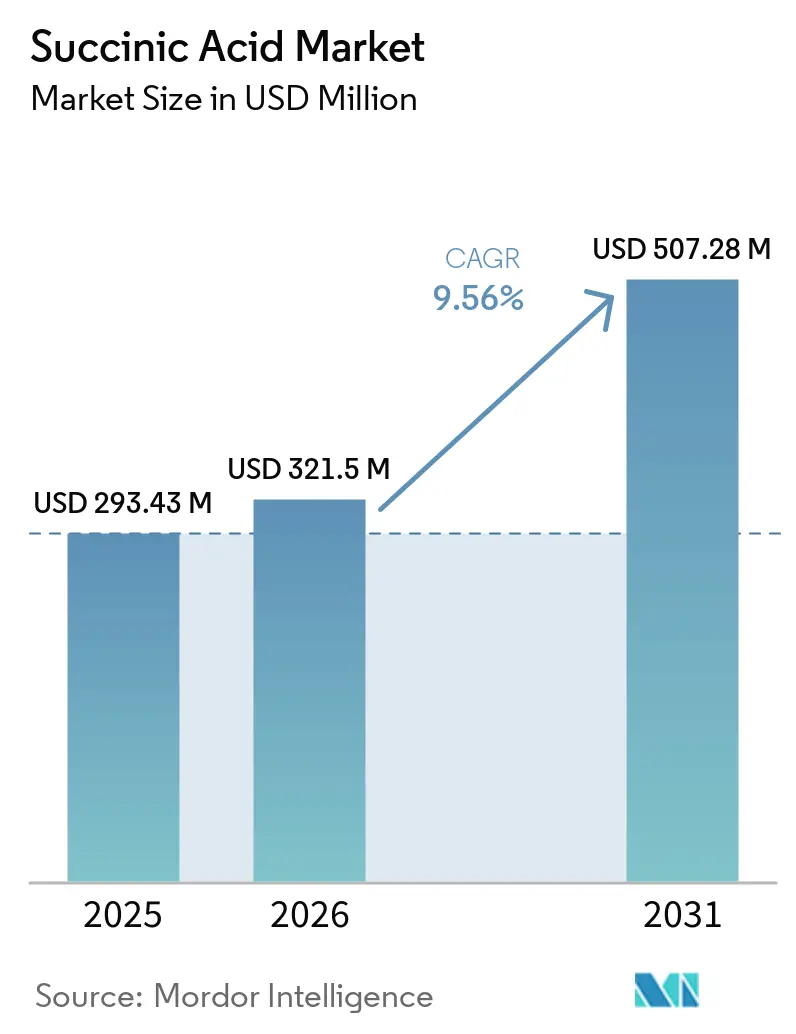

| Market Size (2026) | USD 321.5 Million |

| Market Size (2031) | USD 507.28 Million |

| Growth Rate (2026 - 2031) | 9.56% CAGR |

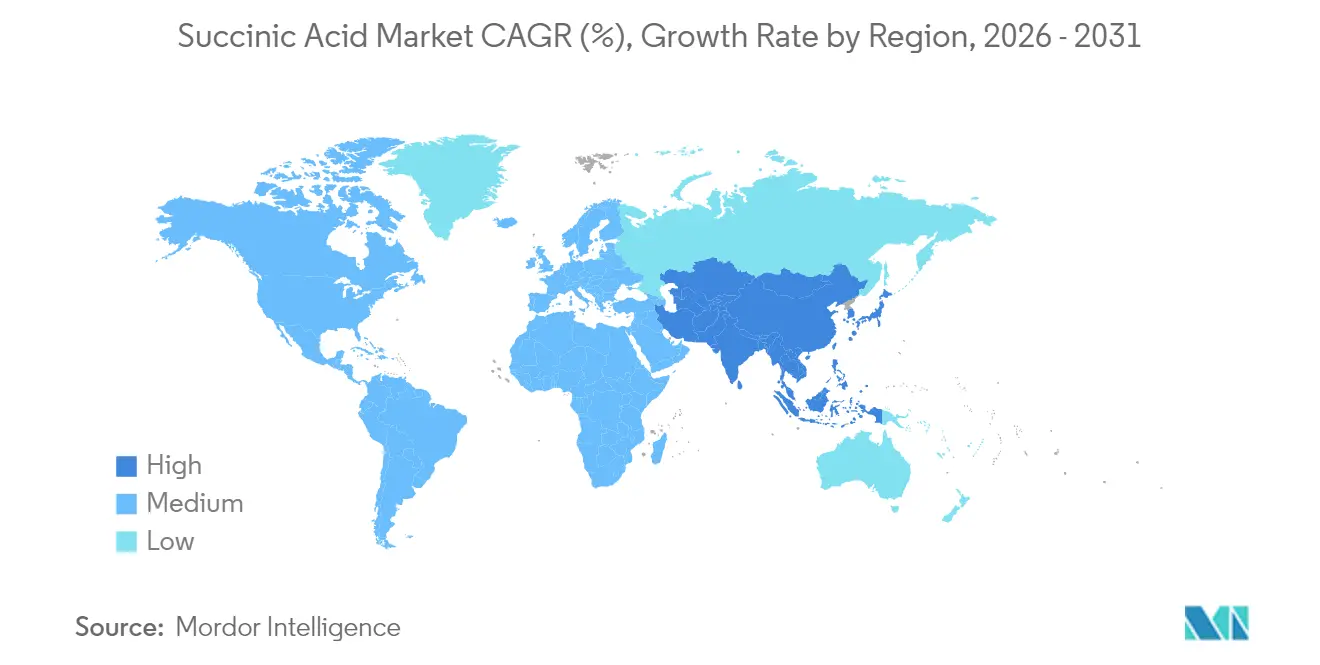

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Succinic Acid Market Analysis by Mordor Intelligence

Succinic acid market size in 2026 is estimated at USD 321.5 million, growing from 2025 value of USD 293.43 million with 2031 projections showing USD 507.28 million, growing at 9.56% CAGR over 2026-2031. The market growth is driven by the shift from petroleum-based to bio-based production methods, reduced fermentation costs, and increased corporate sustainability initiatives focusing on renewable intermediates. The market expansion is supported by increasing demand for biodegradable polymers, specifically polybutylene succinate, along with broader adoption in food and cosmetic applications. Regulatory support in Europe and North America contributes to market development. Companies are investing in advanced fermentation technologies that reduce CO₂ emissions during production, aligning with net-zero objectives. The Asia-Pacific region is establishing manufacturing centers to ensure feedstock diversity and strengthen supply chain stability.

Key Report Takeaways

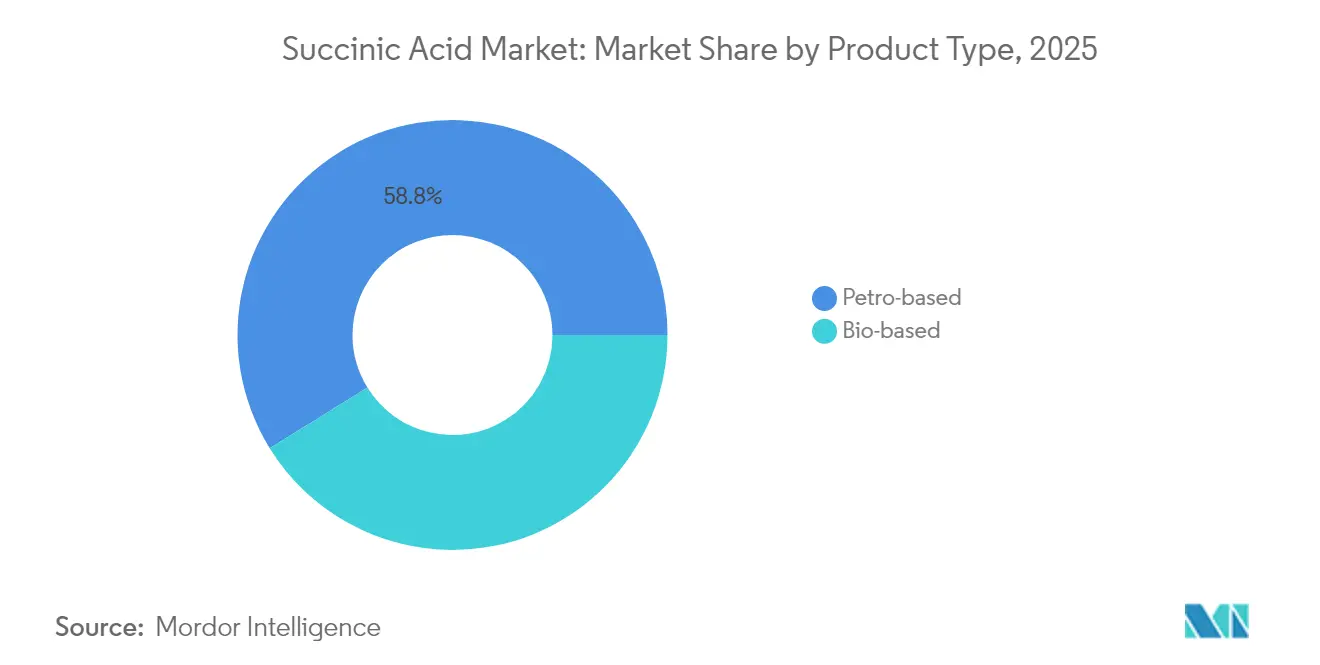

- By product type, petro-based production led with 58.82% of the succinic acid market share in 2025, while bio-based production is forecast to grow at 11.02% CAGR from 2026-2031.

- By grade, industrial/technical grade accounted for 35.72% of the succinic acid market size in 2025; cosmetic grade is projected to expand at 10.55% CAGR during 2026-2031.

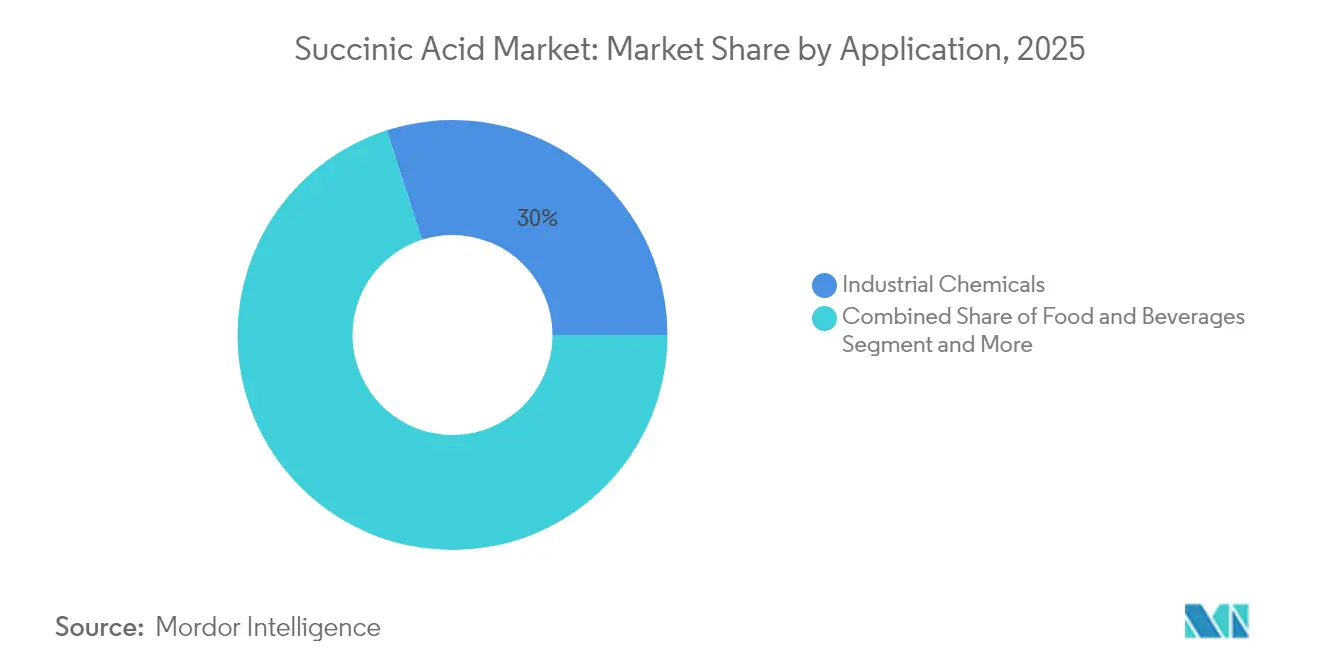

- By application, industrial chemicals held 29.95% of the succinic acid market size in 2025, whereas personal care and cosmetics is advancing at 10.18% CAGR through 2031.

- By geography, Europe commanded 31.64% of the succinic acid market in 2025, and Asia-Pacific is set to record the fastest 10.31% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Succinic Acid Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for biodegradable polymers | +2.1% | Global, with Asia-Pacific and Europe leading adoption | Medium term (2-4 years) |

| Regulatory support for bio-based chemicals | +1.8% | Europe and North America primarily | Long term (≥ 4 years) |

| Expanding food and beverage usage as acidity regulator and flavor enhancer | +1.4% | Global, with emerging markets showing rapid growth | Short term (≤ 2 years) |

| Growing demand in personal care and cosmetics | +1.6% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Advancements in bio-based production technologies | +1.9% | Global, with technology hubs in developed markets | Long term (≥ 4 years) |

| Rising demand for green solvents and industrial chemicals | +1.3% | Industrial regions globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for biodegradable polymers

Polybutylene succinate (PBS) production has emerged as the primary growth catalyst for succinic acid demand, with automotive and packaging industries mandating biodegradable alternatives to conventional plastics. Technical University of Munich researchers achieved breakthrough fermentation efficiency using the marine bacterium Vibrio natriegens, reducing production time to 2-3 hours compared to traditional 24-48 hour cycles. This technological advancement addresses the critical bottleneck of fermentation scalability that previously limited bio-based succinic acid competitiveness. Polymer manufacturers increasingly specify bio-based succinic acid for PBS production to meet circular economy regulations, particularly in Europe, where extended producer responsibility frameworks penalize non-biodegradable packaging materials.

Regulatory support for bio-based chemicals

Government policy frameworks have crystallized around bio-based chemical incentives, with the U.S. Department of Energy's 2025 sustainable chemistry roundtable identifying succinic acid as a priority platform chemical for industrial decarbonization [1]Source: U.S. Department of Energy, “2025 Sustainable Chemistry Framework,” energy.gov. Owing to the rising demand for bio-based chemicals, various countries are investing heavily in biotechnology initiatives. According to the Ministry of Science and Technology data from 2024, the Government of India launched the BioF3 (Biotechnology for Economy, Environment and Employment) policy to foster high-performance biotechnology manufacturing in the country [2]Source: Ministry of Science & Technology, “The Rise of India’s Bioeconomy From $10bn to $165.75bn in a Decade,” pib.gov.in. FDA recognition of succinic acid as Generally Recognized as Safe (GRAS) for food applications removes regulatory barriers for expanded usage in food and beverage formulations, with maximum allowable levels established for condiments and meat products. These regulatory endorsements create preferential market access for bio-based succinic acid producers while establishing quality standards that favor established manufacturers with proven production capabilities.

Expanding food and beverage usage as acidity regulator and flavor enhancer

Food industry adoption accelerates as manufacturers seek clean-label alternatives to synthetic additives, with succinic acid's natural occurrence in plants and animals providing consumer acceptance advantages over artificial preservatives. The compound's dual functionality as both pH control agent and a flavor enhancer enables formulators to reduce ingredient complexity while maintaining product stability and taste profiles. Average daily intake remains significantly below toxicity thresholds at less than 0.01 mg per person, creating substantial headroom for expanded food applications without safety concerns. Emerging market food processors increasingly specify bio-based succinic acid to align with sustainability positioning, particularly in organic and premium product categories where environmental credentials influence purchasing decisions. The compound's role in the citric acid cycle provides metabolic compatibility that synthetic alternatives cannot match, supporting its adoption in functional foods and nutraceutical applications.

Growing demand in personal care and cosmetics

Cosmetic formulators have identified succinic acid's anti-inflammatory and exfoliating properties as key differentiators in premium skincare products. The compound's natural origin and biodegradability align with consumer preferences for sustainable beauty products, particularly among millennials and Gen Z demographics who prioritize environmental impact in purchasing decisions. Bio-based succinic acid's molecular structure enables gentle exfoliation without the irritation associated with synthetic alpha-hydroxy acids, creating opportunities in sensitive skin formulations. Personal care manufacturers increasingly specify USDA Certified Biobased ingredients to meet sustainability targets, with Roquette's BIOSUCCINIUM® achieving 100% biobased content certification. The compound's compatibility with other natural ingredients facilitates clean beauty formulations that command premium pricing while reducing regulatory complexity across international markets.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs | -2.3% | Global, particularly affecting emerging market adoption | Short term (≤ 2 years) |

| Limited commercial-scale production infrastructure | -1.9% | Developing regions primarily | Medium term (2-4 years) |

| Energy-intensive purification undermining eco-benefits | -1.4% | All production regions | Long term (≥ 4 years) |

| Competition from alternative bio-based acids | -1.1% | Global, with varying intensity by application | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited commercial-scale production infrastructure

The collapse of several pioneering companies, including BioAmber, has reduced available production capacity while deterring new investment in manufacturing infrastructure. Developing regions lack the technical expertise and capital access required for fermentation facility construction, concentrating production in established chemical manufacturing hubs. The specialized nature of bio-based production requires different equipment and processes compared to traditional chemical plants, limiting the ability to repurpose existing facilities and increasing capital requirements. Feedstock supply chain development lags behind production capacity needs, particularly for non-food biomass sources that require preprocessing infrastructure investment.

Competition from alternative bio-based acids

Adipic acid production from biomass-derived feedstocks presents direct competition for applications in polyester and nylon manufacturing, with established supply chains and lower switching costs for downstream users. Malonic acid and other dicarboxylic acids offer similar functionality in specific applications while benefiting from different production economics and feedstock availability. The development of alternative bio-based platform chemicals creates competition for the same feedstock resources, potentially increasing raw material costs and supply volatility. Established petroleum-based chemical producers have responded to bio-based competition by improving process efficiency and reducing prices, maintaining cost advantages in price-sensitive applications. The emergence of new bio-based acids with superior performance characteristics or lower production costs threatens succinic acid's position in developing applications before market establishment occurs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bio-Based Transformation Accelerates

Bio-based succinic acid is projected to grow at a CAGR of 11.02% during 2026-2031, while petro-based succinic acid maintains a 58.82% market share in 2025. The higher growth rate of bio-based production reflects increasing adoption of sustainable manufacturing methods, driven by regulatory requirements and corporate environmental goals. The shift toward bio-based production aligns with global sustainability initiatives and growing environmental consciousness across industries. Petro-based production retains its market leadership due to established infrastructure and lower costs, particularly in industrial applications where price sensitivity outweighs environmental concerns.

The cost advantage of petro-based production stems from decades of process optimization and economies of scale in existing facilities. Bio-based alternatives are gaining traction in premium segments such as food, pharmaceuticals, and cosmetics, where sustainability requirements justify higher prices and consumer preferences influence purchasing decisions. These premium segments demonstrate increasing willingness to absorb the additional costs associated with bio-based production methods, driven by end-user demand for environmentally responsible products.

By Grade: Cosmetic Applications Drive Premium Growth

Industrial/Technical Grade applications dominate with 35.72% market share in 2025. This segment dominates due to its extensive use in chemical manufacturing, polymer production, and industrial processing, where operational costs remain a primary consideration over environmental factors. The industrial/technical grade segment serves as a crucial component in manufacturing processes, particularly in the production of plastics, resins, and industrial chemicals. These applications require large volumes of raw materials to maintain continuous production cycles and meet the demands of various end-use industries.

The Cosmetic Grade segment is expected to grow at a CAGR of 10.55% through 2031, driven by premium pricing and increased adoption in personal care formulations. This growth is primarily attributed to rising consumer demand for natural and sustainable ingredients in personal care products, particularly among younger consumers who prioritize environmental considerations in their purchasing decisions. The segment's expansion is further supported by increasing disposable income, growing awareness of clean beauty products, and stringent regulations promoting the use of eco-friendly ingredients. Manufacturers are investing in research and development to create innovative, sustainable cosmetic-grade materials that meet both performance requirements and environmental standards. Additionally, the rise of clean beauty trends and natural cosmetics has encouraged formulators to incorporate more plant-based and biodegradable ingredients, further stimulating market growth in this segment.

By Application: Personal Care Emergence Challenges Industrial Dominance

The industrial chemicals application maintain 29.95% market share in 2025. Succinic acid's versatility as a chemical intermediate has made it increasingly valuable in the production of various industrial chemicals, including solvents, lubricants, and polymers. Its bio-based production methods align with the growing global emphasis on sustainable manufacturing processes, making it an environmentally friendly alternative to petroleum-derived chemicals. Furthermore, succinic acid's role as a crucial raw material in the synthesis of biodegradable polymers, particularly PBS (Polybutylene Succinate), has expanded its market potential. The compound's applications in metal plating, coating additives, and as a corrosion inhibitor have also contributed to its growing industrial demand.

Personal Care and Cosmetics applications demonstrate the fastest growth at 10.18% CAGR for 2026-2031. Primarily, succinic acid's exceptional moisturizing and anti-aging properties have made it a sought-after ingredient in skincare formulations. Its ability to enhance skin barrier function and promote collagen production has garnered attention from leading cosmetic manufacturers. Furthermore, the increasing consumer preference for sustainable and bio-based ingredients has boosted succinic acid's appeal, as it can be produced through environmentally friendly fermentation processes. The compound's versatility as a pH adjuster, antimicrobial agent, and emollient has expanded its use across various cosmetic products, including facial creams, serums, and hair care items.

Geography Analysis

Europe commands 31.64% market share in 2025, leveraging established regulatory frameworks supporting bio-based chemicals and mature manufacturing infrastructure. Germany and France lead regional production capacity with integrated chemical complexes that facilitate downstream processing and distribution. The region's extended producer responsibility frameworks for packaging materials create preferential demand for biodegradable polymers derived from bio-based succinic acid.

Asia-Pacific emerges as the fastest-growing region with 10.31% CAGR for 2026-2031, driven by rapid industrialization and expanding manufacturing capacity across China, India, and Southeast Asia. Hyosung's USD 1 billion investment in Vietnam for bio-based 1,4-butanediol production exemplifies the region's strategic positioning in bio-based chemical manufacturing, with the facility targeting 50,000 metric tons of annual capacity by 2026. China's dominance in chemical manufacturing provides established infrastructure for succinic acid production scale-up, while India's growing pharmaceutical and personal care industries create expanding demand for higher-grade products. The region benefits from abundant agricultural waste feedstocks, including rice straw and corn stalks that provide cost-effective raw materials for bio-based production. Government policies supporting industrial decarbonization and circular economy development create favorable conditions for bio-based chemical adoption across the region.

North America maintains a significant market presence despite facing competitive pressure from lower-cost Asian production. The U.S. Department of Agriculture's 2024 biomass supply chain report identifies abundant feedstock availability as a key competitive advantage, with established agricultural infrastructure supporting renewable raw material supply . The U.S. Department of Energy's sustainable chemistry roundtable prioritizes succinic acid as a platform chemical for industrial decarbonization, providing policy support for domestic production development. Canada's experience with BioAmber's failed commercialization provides lessons for risk management and market development strategies, highlighting the importance of realistic cost projections and market pricing assumptions.

Competitive Landscape

The succinic acid market maintains moderate fragmentation, with market fragmentation creating significant opportunities for industry consolidation as production technologies continue to mature and scale requirements increase. The competitive landscape is characterized by strategic partnerships between established chemical manufacturers and specialized biotechnology firms, combining large-scale manufacturing capabilities with advanced fermentation expertise to achieve commercial viability in the market.

Companies invest in technological advancements to improve fermentation efficiency and downstream processing. They focus on metabolic engineering and separation technologies to reduce production costs and enhance product quality. The industry's reorganization into Custom Solutions and Advanced Technologies segments reflects a shift toward specialization, targeting high-value applications that command premium prices.

Many Companies demonstrate a significant strategic shift by producing derivatives directly instead of commodity succinic acid, effectively avoiding commodity pricing pressures in the market. Geographic expansion strategies systematically prioritize regions with advantageous feedstock availability and supportive regulatory frameworks, particularly in Asia-Pacific markets where sustained industrial growth drives increased demand for bio-based chemicals across multiple applications.

Succinic Acid Industry Leaders

Roquette Frères

Mitsubishi Chemical Group

Nippon Shokubai Co., Ltd.

Air Water Performance Chemical Inc.

Anhui Sunsing Chemicals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Pfanstiehl, Inc., a manufacturer of injectable excipients, cGMP bioprocessing components, and active pharmaceutical ingredients (APIs), introduced High Purity Low Endotoxin Low Metals (HPLE-LMTM) Succinic Acid. The product serves pharmaceutical, biopharmaceutical, and injectable applications. Pfanstiehl's HPLE-LMTM Succinic Acid is available for research and development and commercial manufacturing scales.

- September 2024: Lygos partnered with CJ Bio to establish 40,000 metric tons per year biobased chemicals facility in Fort Dodge, Iowa, focusing on polyaspartates and malonates production with potential expansion to 100,000 tons annually

- May 2024: Sustainea joint venture between Braskem and Sojitz announced strategic partnership with Origin Materials for 100% bio-based materials development, highlighting expanding renewable chemicals market opportunities

- April 2024: Evonik, a specialty chemicals company headquartered in Germany, opened its new office and R&D facility in Thane. The 100,000-square-foot Evonik India facility includes laboratories serving pharmaceutical, oral care, personal care, food, feed, and agriculture industries.

Global Succinic Acid Market Report Scope

Succinic acid is an organic acid that occurs naturally and can be synthesized for the usage of generating solvents, dyes, photographic chemicals, etc.

The succinic acid market is segmented by type and application. Based on type, the market is segmented into bio-based and petro-based. Based on application, the market is segmented into food and beverage, pharmaceutical, industrial, and other applications. Also, the study provides an analysis of the succinic acid market in emerging and established markets across the world, including North America, Europe, Asia-Pacific, South America, Middle-East and Africa.

For each segment, the market sizing and forecasts have been done based on value (in USD million).

| Petro-based |

| Bio-based |

| Industrial/Technical Grade |

| Food Grade |

| Pharmaceutical Grade |

| Cosmetic Grade |

| Industrial Chemicals |

| Food and Beverage |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Petro-based | |

| Bio-based | ||

| By Grade | Industrial/Technical Grade | |

| Food Grade | ||

| Pharmaceutical Grade | ||

| Cosmetic Grade | ||

| By Application | Industrial Chemicals | |

| Food and Beverage | ||

| Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the succinic acid market?

The succinic acid market stands at USD 321.5 million in 2026 and is projected to reach USD 507.28 million by 2031 at a 9.56% CAGR.

Which region leads the succinic acid market?

Europe held 31.64% of global revenue in 2025, supported by strong regulatory incentives and mature production infrastructure.

Which application segment is growing fastest?

Personal Care and Cosmetics is set to expand at a 10.18% CAGR through 2031, fueled by demand for natural and sustainable skincare ingredients.

What are the main restraints for succinic acid adoption?

High production costs, limited large-scale fermentation capacity, energy-intensive purification, and competition from other bio-acids slow near-term uptake.

Page last updated on: