Proanthocyanidins Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

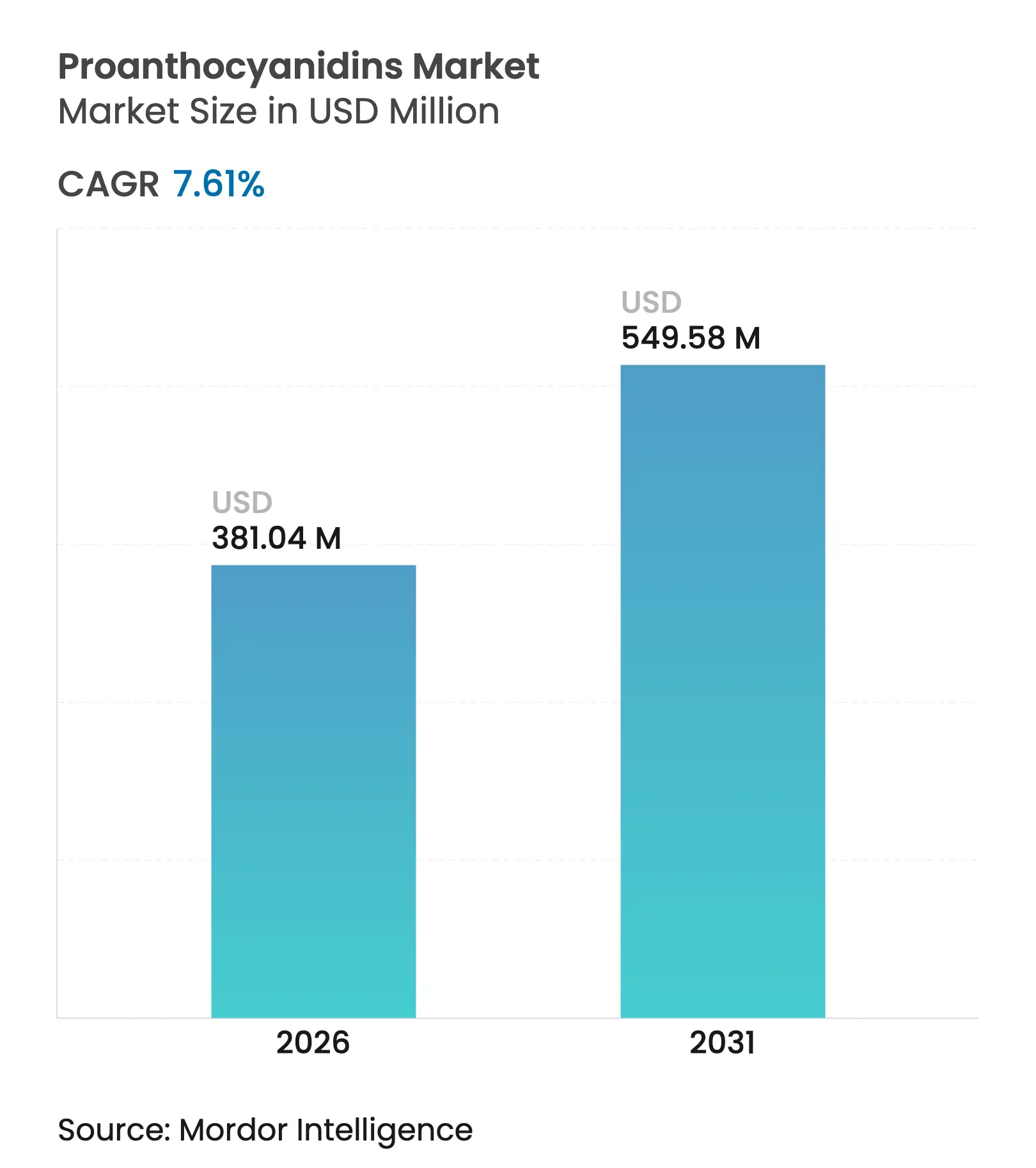

| Market Size (2026) | USD 381.04 Million |

| Market Size (2031) | USD 549.58 Million |

| Growth Rate (2026 - 2031) | 7.61 % CAGR |

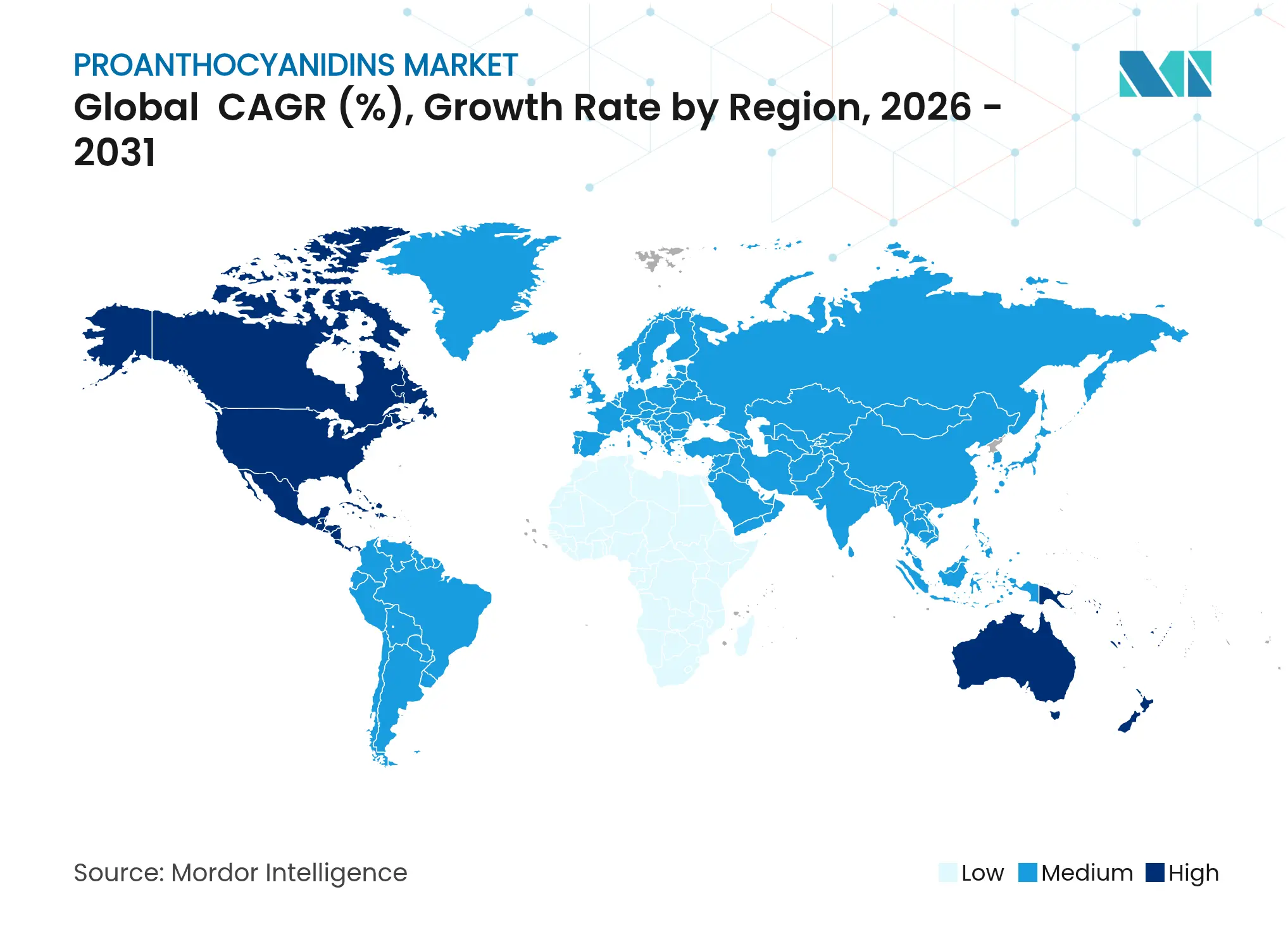

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Proanthocyanidins Market Analysis by Mordor Intelligence

The global proanthocyanidins market size was valued at USD 354.10 million in 2025 and estimated to grow from USD 381.04 million in 2026 to reach USD 549.58 million by 2031, at a CAGR of 7.61% during the forecast period (2026-2031). Increasing regulatory restrictions on synthetic antioxidants and a growing consumer preference for natural, clean-label botanical ingredients are driving this growth. Consumers are increasingly seeking products with minimal artificial additives, aligning with the clean-label trend. Additionally, rising awareness of the health benefits of proanthocyanidins, such as their antioxidant and anti-inflammatory properties, their diverse applications in the food, pharmaceutical, and cosmetic industries, and ongoing research and development activities to enhance their functionality and bioavailability further support the market expansion. The FDA's 2024 approval of grape seed extract containing oligomeric proanthocyanidins as a supplemental ingredient, with a recommended maximum daily intake of 100 mg proanthocyanidins, signals regulatory confidence in these compounds' safety profile, according to the Health Canada data[1]Source: Health Canada, "Modification to the List of permitted supplemental ingredients to enable the use of grape seed extract", canada.ca.

Key Report Takeaways

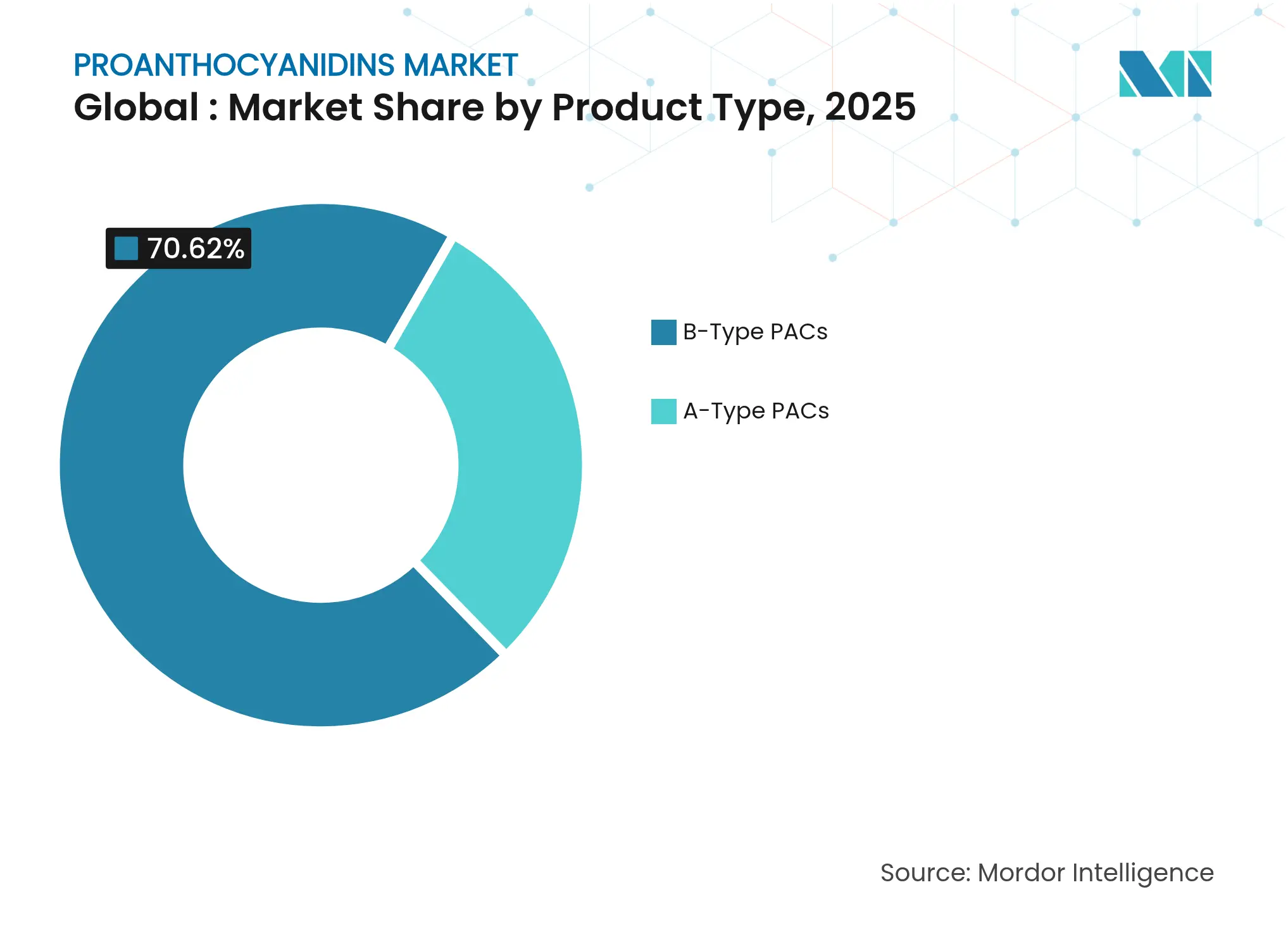

- By type, B-Type compounds accounted for 70.62% share in 2025, while A-Type proanthocyanidins will grow fastest at a 8.88% CAGR over the forecast period.

- By source, grape seed held 51.74% of the proanthocyanidins market share in 2025; cranberry is poised for an 8.34% CAGR from 2026-2031.

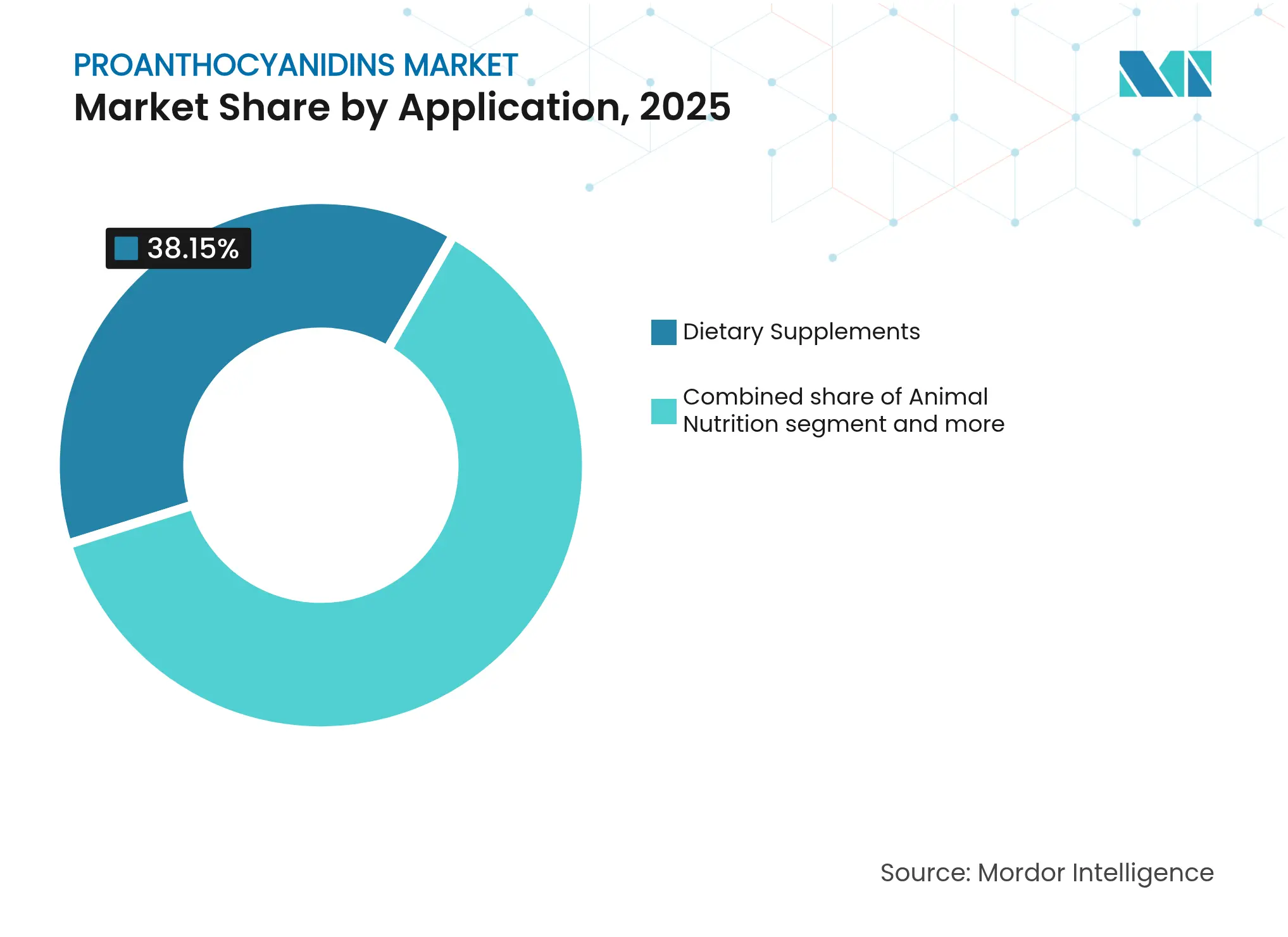

- By application, dietary supplements led with 38.15% revenue share in 2025, whereas animal nutrition is set to expand at a 8.71% CAGR through 2031.

- By geography, North America commanded 32.21% of 2025 revenue; Asia-Pacific is projected to register a 9.06% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Proanthocyanidins Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing demand for clean-label botanical antioxidants Increasing demand for clean-label botanical antioxidants | +1.8% | Global, with early adoption in North America and Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecasts:+1.8% | Geographic Relevance:Global, with early adoption in North America and Europe | Impact Timeline:Medium term (2-4 years) |

Rapid growth in demand for natural nutraceuticals Rapid growth in demand for natural nutraceuticals | +2.1% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) | |||

Expanding applications in functional foods and beverages Expanding applications in functional foods and beverages | +1.5% | Global, concentrated in developed markets | Medium term (2-4 years) | |||

Rising incidence of chronic lifestyle diseases Rising incidence of chronic lifestyle diseases | +1.2% | Global, particularly Asia-Pacific and North America | Long term (≥ 4 years) | |||

Growing consumer preference for herbal and natural medicines Growing consumer preference for herbal and natural medicines | +0.9% | Global, with stronger adoption in Europe and Asia-Pacific | Medium term (2-4 years) | |||

Innovation in extraction technologies Innovation in extraction technologies | +0.5% | Global, led by technology hubs in North America and Europe | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing demand for clean-label botanical antioxidants

Regulatory pressure on synthetic antioxidants creates unprecedented opportunities for proanthocyanidin adoption across food and beverage applications. The FDA's qualified health claim approval for cocoa flavanols in February 2023, requiring a minimum of 200 mg per serving for cardiovascular benefits, establishes a regulatory precedent that validates polyphenolic compounds' therapeutic potential[2]Source: U.S. Food and Drug Administration, “Qualified Health Claims for Cocoa Flavanols,” fda.gov. This approval mechanism enables proanthocyanidin suppliers to pursue similar health claims, particularly for grape seed and cranberry extracts with established safety profiles. The clean-label movement accelerates as food manufacturers respond to consumer scrutiny of ingredient lists, with proanthocyanidins offering dual functionality as natural preservatives and health-promoting compounds. European regulations limiting synthetic antioxidant usage in organic products further amplify demand for botanical alternatives. Market penetration accelerates through private label partnerships, where retailers leverage clean-label positioning to differentiate premium product lines and capture health-conscious consumer segments.

Rapid growth in demand for natural nutraceuticals

Asia-Pacific's expanding middle class drives nutraceutical consumption patterns that favor traditional medicine integration with modern delivery systems. China's regulatory approval of new food raw materials, including proanthocyanidins, in 2024 opens pathways for domestic market penetration in the world's largest nutraceutical market. The convergence of aging demographics and rising healthcare costs creates sustained demand for preventive health solutions, positioning proanthocyanidins as cost-effective alternatives to pharmaceutical interventions. Clinical validation of proanthocyanidins' anti-inflammatory and antioxidant properties through peer-reviewed research strengthens physician recommendations and insurance reimbursement potential. Digital health platforms increasingly recommend personalized nutraceutical regimens based on genetic testing and biomarker analysis, creating targeted demand for specific proanthocyanidin formulations.

Expanding applications in functional foods and beverages

Technological breakthroughs in taste masking and stability enhancement enable proanthocyanidin integration into mainstream beverage categories previously constrained by astringency concerns. Ultrasound-assisted extraction and subcritical water processing preserve bioactive compounds while reducing bitter flavor compounds, facilitating incorporation into sports drinks and ready-to-drink teas. Microencapsulation technologies protect proanthocyanidins from degradation during processing and storage, enabling shelf-stable formulations with consistent bioactivity. Regulatory frameworks increasingly support structure-function claims for functional foods, reducing barriers to market entry for proanthocyanidin-enhanced products. Strategic partnerships between ingredient suppliers and food manufacturers accelerate product development cycles, with co-innovation models sharing development costs and market risks.

Rising incidence of chronic lifestyle diseases

Cardiovascular disease prevalence drives demand for evidence-based nutritional interventions, with proanthocyanidins demonstrating clinically significant benefits in multiple randomized controlled trials. Healthcare systems increasingly emphasize preventive medicine approaches to manage chronic disease costs, creating institutional demand for validated nutritional interventions. Proanthocyanidins' multi-target mechanisms, including endothelial function improvement and inflammation reduction, position these compounds for integration into comprehensive chronic disease management protocols. Insurance coverage expansion for preventive nutrition programs creates reimbursement pathways for proanthocyanidin supplements prescribed by healthcare providers. Digital therapeutics platforms incorporate proanthocyanidin supplementation into personalized treatment algorithms, driving precision medicine adoption in chronic disease management.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Price volatility of key raw fruits and seeds Price volatility of key raw fruits and seeds | -1.4% | Global, particularly regions dependent on agricultural imports | Short term (≤ 2 years) | (~) % Impact on CAGR Forecasts:-1.4% | Geographic Relevance:Global, particularly regions dependent on agricultural imports | Impact Timeline:Short term (≤ 2 years) |

Limited bioavailability of high-polymer proanthocyanidins Limited bioavailability of high-polymer proanthocyanidins | -0.8% | Global, affecting all application segments | Medium term (2-4 years) | |||

High costs of production and extraction processes High costs of production and extraction processes | -1.2% | Global, with higher impact in developing markets | Medium term (2-4 years) | |||

Stringent regulatory requirements for approval Stringent regulatory requirements for approval | -0.9% | North America and Europe primarily, expanding to Asia-Pacific | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Price volatility of key raw fruits and seeds

Agricultural commodity price fluctuations create significant margin pressure for proanthocyanidin manufacturers, as grape and cranberry harvests remain vulnerable to weather-related supply disruptions. Climate change increases supply chain volatility through more frequent and severe extreme weather events across major growing regions, affecting crop yields and quality. While forward contracting mechanisms exist, they offer limited protection against multi-year supply disruptions, requiring manufacturers to maintain higher inventory levels and accept reduced working capital efficiency. The availability of grape seeds varies with wine industry demand cycles, creating competition between proanthocyanidin extraction and traditional wine production. This competition intensifies during periods of reduced grape harvests or increased wine production. Some manufacturers pursue vertical integration by acquiring agricultural assets to secure raw material supplies, though the high capital requirements restrict this approach to larger market participants. These integrated operations often include dedicated farming operations, processing facilities, and storage infrastructure to maintain a consistent supply.

Limited bioavailability of high-polymer proanthocyanins

The absorption of high-polymer proanthocyanidins is limited by their molecular size, which affects their therapeutic effectiveness in various medical applications. Research shows that only proanthocyanidins with a polymerization degree under 4 can be absorbed effectively by the body, highlighting a significant challenge in developing effective treatments. The natural occurrence of high-polymer compounds presents significant challenges for their biological activity and potential therapeutic applications across different medical conditions. The regulatory requirements for bioavailability testing extend development timelines and increase costs, making it difficult for small manufacturers to enter the market. These requirements include extensive safety assessments, stability studies, and validation protocols. The varying bioavailability between products creates challenges in educating consumers about proper dosing and expected outcomes, particularly regarding the relationship between product formulation and therapeutic benefits. This complexity affects healthcare providers' ability to make informed recommendations and patients' understanding of treatment options.

Segment Analysis

By Type: A-Type PACs Challenge B-Type Dominance

In 2025, B-Type proanthocyanidins command a dominant 70.62% market share, primarily derived from grape seeds and cocoa. These compounds are widely used due to their established supply chains and cost-effectiveness, making them a preferred choice in the food and beverage sector. Meanwhile, A-Type proanthocyanidins are on a growth trajectory, boasting a 8.88% CAGR through 2031. This surge is largely attributed to their specialized health applications, particularly in preventing urinary tract infections, which are supported by their unique bioactivity profiles. The structural nuances between A-Type and B-Type linkages endow them with distinct properties. Notably, A-Type compounds exhibit heightened bacterial anti-adhesion properties, which play a critical role in bolstering claims related to urinary health. However, the manufacturing of A-Type proanthocyanidins is intricate, necessitating specialized extraction techniques to preserve their structural integrity. This complexity not only creates barriers to entry but also safeguards premium pricing for established suppliers, ensuring a competitive advantage in the market.

Meanwhile, strides in synthetic biology and fermentation methods present viable alternatives to conventional plant extraction. Companies like HealthTech Bioactives are at the forefront, collaborating with Abolis Biotechnologies to pioneer sustainable, solvent-free production techniques for high-value polyphenols. These advancements aim to address the challenges of traditional extraction methods, such as high costs and environmental concerns, while ensuring scalability and consistency in production. The clinical validation of A-Type proanthocyanidins' distinct mechanisms bolsters their premium status in both pharmaceutical and nutraceutical realms, where their efficacy in targeted health applications is increasingly recognized. In contrast, B-Type compounds enjoy cost benefits and well-established supply chains, particularly in the food and beverage sector, where they are extensively utilized for their antioxidant properties. Furthermore, as regulatory frameworks evolve, they increasingly acknowledge the unique attributes of various proanthocyanidin types, paving the way for targeted health claims and specialized applications. This regulatory support is expected to drive innovation and expand the scope of proanthocyanidin applications across multiple industries.

Note: Segment shares of all individual segments available upon report purchase

By Source: Grape Seed Dominance Faces Cranberry Innovation

Extraction methods for cranberry proanthocyanidins boast enhanced bioavailability over their grape seed counterparts. This advantage has propelled the cranberry segment to an impressive 8.34% CAGR forecasted through 2031, driven by increasing consumer awareness of its health benefits and its growing application in functional foods and beverages. Meanwhile, grape seed extracts command a substantial 51.74% market share in 2025, attributed to their established presence in the market and widespread use in dietary supplements and cosmetics. The FDA's GRAS designation for cranberry extract powder, rich in proanthocyanidins, underscores its safety for use in beverages and processed fruits, paving the way for wider commercial adoption. Grape seed extracts continue to dominate the market, bolstered by established supply chains, cost efficiencies, and a steady raw material supply sourced from wine production by-products, which ensures consistent availability and competitive pricing.

Cocoa-derived proanthocyanidins are increasingly recognized for their cardiovascular health claims, supported by scientific studies linking them to improved heart health and reduced risk of chronic diseases. In contrast, apple and pine bark variants cater to niche markets, finding their place in dietary supplements and pharmaceuticals due to their unique antioxidant properties and specific health benefits. Technological advancements in extraction methods have markedly boosted efficiency across all sources. For instance, subcritical water extraction techniques have upped yield rates by 30% over traditional methods, enhancing the economic viability of production, and ultrasound-assisted processing has slashed extraction times by 40%, enabling faster turnaround and reduced operational costs. Furthermore, utilizing grape pomace not only curtails waste in wine production but also stands out as an eco-friendly method to source valuable proanthocyanidins, aligning with the growing emphasis on sustainability in the industry.

By Application: Animal Nutrition Emerges as Growth Driver

Animal nutrition applications demonstrate exceptional growth potential at 8.71% CAGR through 2031, driven by regulatory restrictions on antibiotic growth promoters and increasing demand for natural feed additives that enhance livestock performance. Clinical studies demonstrate that grape seed proanthocyanidin supplementation at 400 mg/kg improves jejunal antioxidant capacity and gut microbial diversity in poultry, reducing oxidative stress while maintaining growth performance. Dietary supplements maintain market leadership with 38.15% share in 2025, supported by expanding consumer awareness of proanthocyanidins' cardiovascular and anti-aging benefits.

Food and beverage applications benefit from technological advances in taste masking and stability enhancement, enabling integration into mainstream product categories previously constrained by astringency concerns. Pharmaceutical applications focus on specialized delivery systems that address bioavailability challenges, with liposomal formulations demonstrating significant improvements in therapeutic efficacy. Personal care and cosmetics segments leverage proanthocyanidins' antioxidant properties for anti-aging formulations, with encapsulation technologies protecting active compounds from degradation during product storage and application.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America commands 32.21% market share in 2025, anchored by robust regulatory frameworks that facilitate proanthocyanidin commercialization and established nutraceutical distribution networks. The FDA's systematic approach to GRAS determinations for botanical extracts creates predictable pathways for market entry, with recent approvals for grape seed extract and cranberry powder establishing precedents for similar compounds. Strategic acquisitions like Barentz's planned acquisition of China's Fengli Group signal increasing integration between North American companies and Asian supply chains, leveraging regional expertise to capture growth opportunities across markets.

Asia-Pacific emerges as the fastest-growing region at 9.06% CAGR through 2031, driven by expanding middle-class populations and increasing health consciousness among aging demographics. The region's traditional medicine heritage creates cultural acceptance for plant-based health solutions, facilitating proanthocyanidin adoption in both traditional and modern delivery formats. Manufacturing capacity expansion across Southeast Asian countries provides cost-competitive production platforms for global supply chains, while regulatory harmonization efforts reduce barriers to cross-border trade.

Europe maintains steady growth supported by the European Food Safety Authority'supdated novel foods guidance, effective February 2025, which standardizes safety assessment procedures and reduces regulatory uncertainty for proanthocyanidin-based products. The region's emphasis on sustainable agriculture and circular economy principles drives demand for grape pomace and other agricultural by-product utilization, creating synergies between environmental objectives and proanthocyanidin production. South America and Middle East and Africa represent emerging opportunities, with Brazil's agricultural sector providing potential raw material sources and the UAE's position as a regional distribution hub facilitating market access across the Middle East and North Africa.

Competitive Landscape

Market Concentration

The proanthocyanidins market exhibits moderate fragmentation, with established companies implementing vertical integration to maintain a stable supply of raw materials and ensure quality control. These companies often control the entire supply chain, from sourcing raw materials to final product manufacturing, ensuring consistent quality standards. New market entrants differentiate themselves through specialized extraction methods and innovative delivery systems, focusing on niche applications and unique formulation technologies. Ingredient suppliers and manufacturers form strategic partnerships to share development risks and facilitate innovation, enabling faster market penetration and product commercialization.

Companies focus their research and development on improving bioavailability through advanced delivery mechanisms, with significant investments in liposomal encapsulation and nanoparticle formulations to enhance absorption rates. These technological developments aim to overcome traditional bioavailability limitations of proanthocyanidins. Self-emulsifying systems show positive results in increasing compound effectiveness, driving continuous product development innovation across various applications. The U.S. Food and Drug Administration's GRAS evaluation process offers clear regulatory guidelines for market participants, benefiting companies with comprehensive safety data and clinical validation.

New product introductions now follow a structured pathway, prioritizing consumer safety. The animal nutrition segment is poised for significant growth, fueled by global restrictions on antibiotic growth promoters. These restrictions aim to address concerns over antibiotic resistance and ensure safer food production practices. As these regulations shift, there's a heightened demand for natural alternatives to boost livestock performance. This trend, especially in the realm of antibiotic-free animal products, paves the way for expanded proanthocyanidin applications in feed formulations, offering sustainable and effective solutions for livestock health and productivity.

Proanthocyanidins Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Alvinesa Natural Ingredients acquired Chilean Industrias Vínicas and Argentine Dervinsa, enhancing its position in the grape-derived ingredients market. The acquisition provides year-round access to high-quality raw materials and expands production capacities, with revenue targets increasing from USD 116.24 million in 2023 to over USD 174.36 million.

- May 2024: HealthTech Bioactives and Abolis Biotechnologies announced a strategic partnership to develop sustainable, fermentation-based production methods for high-value polyphenols, including proanthocyanidins. The collaboration aims to address sourcing challenges and increase manufacturing capacities while reducing costs compared to traditional extraction methods, with initial focus on two specific polyphenol molecules and plans to expand to eight additional compounds

- April 2024: Nordmann's partner Layn has introduced a new water-soluble grape seed extract manufactured in Italy. The extract contains high concentrations of oligomeric proanthocyanidins (OPC) while maintaining low levels of gallic acid and monomers.

Table of Contents for Proanthocyanidins Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Increasing demand for clean-label botanical antioxidants

- 4.2.2Rapid growth in demand for natural nutraceuticals

- 4.2.3Expanding applications in functional foods and beverages

- 4.2.4Rising incidence of chronic lifestyle diseases

- 4.2.5Growing consumer preference for herbal and natural medicines

- 4.2.6Innovation in extraction technologies

- 4.3Market Restraints

- 4.3.1Price volatility of key raw fruits and seeds

- 4.3.2Limited bioavailability of high-polymer proanthocyanins

- 4.3.3High costs of production and extraction processes

- 4.3.4Stringent regulatory requirements for approval

- 4.4Supply-Chain Analysis

- 4.5Technological Outlook

- 4.6Regulatory Landscape

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers/Consumers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitute Products

- 4.7.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Type

- 5.1.1B-Type PACs

- 5.1.2A-Type PACs

- 5.2By Source

- 5.2.1Grape Seed

- 5.2.2Cranberry

- 5.2.3Cocoa

- 5.2.4Apple

- 5.2.5Pine Bark

- 5.2.6Others

- 5.3By Application

- 5.3.1Dietary Supplements

- 5.3.2Food and Beverage

- 5.3.3Pharmaceuticals

- 5.3.4Personal Care and Cosmetics

- 5.3.5Animal Nutrition

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.1.4Rest of North America

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3Italy

- 5.4.2.4France

- 5.4.2.5Spain

- 5.4.2.6Netherlands

- 5.4.2.7Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2India

- 5.4.3.3Japan

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4South America

- 5.4.4.1Brazil

- 5.4.4.2Argentina

- 5.4.4.3Rest of South America

- 5.4.5Middle East and Africa

- 5.4.5.1South Africa

- 5.4.5.2Saudi Arabia

- 5.4.5.3United Arab Emirates

- 5.4.5.4Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Ranking Analysis

- 6.4Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1Artemis International

- 6.4.2Botaniex Inc.

- 6.4.3Givaudan SA

- 6.4.4Indena S.p.A.

- 6.4.5Nexira

- 6.4.6Eevia Health Oy

- 6.4.7Polyphenolics

- 6.4.8Xi’an Yuensun Bio-Tech

- 6.4.9Fruit d’Or

- 6.4.10Martin Bauer Group

- 6.4.11Hunan Sunfull Bio-Tech

- 6.4.12Blue California

- 6.4.13Ajinomoto Health and Nutrition

- 6.4.14Silvateam

- 6.4.15GrAP’Sud

- 6.4.16Kemin Industries

- 6.4.17Pure Encapsulations

- 6.4.18Indena Spa

- 6.4.19Simson Pharma

- 6.4.20Chemecea Pharma

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Global Proanthocyanidins Market Report Scope

The global proanthocyanidins market is segmented by source into cranberry, grape seed, and others. By application, the scope includes food & beverage, dietary supplements, pharmaceuticals, and personal care & cosmetics. By geography, the scope includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa.