Market Overview

| Study Period | 2021 - 2031 |

|---|---|

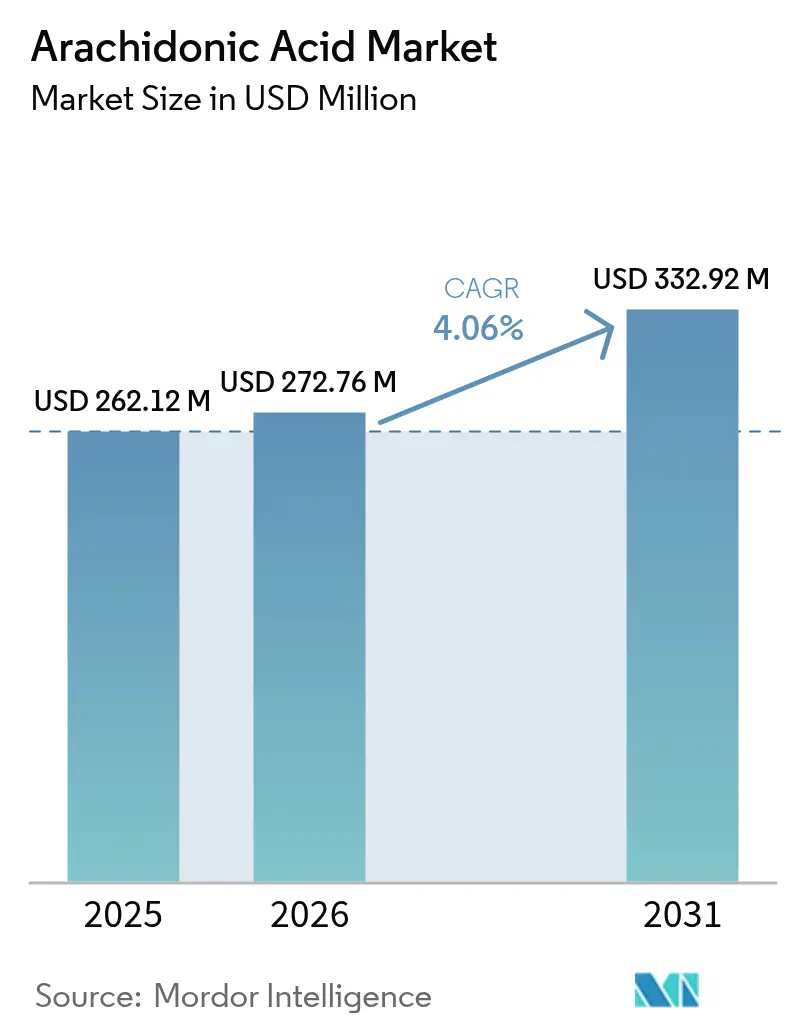

| Market Size (2026) | USD 272.76 Million |

| Market Size (2031) | USD 332.92 Million |

| Growth Rate (2026 - 2031) | 4.06% CAGR |

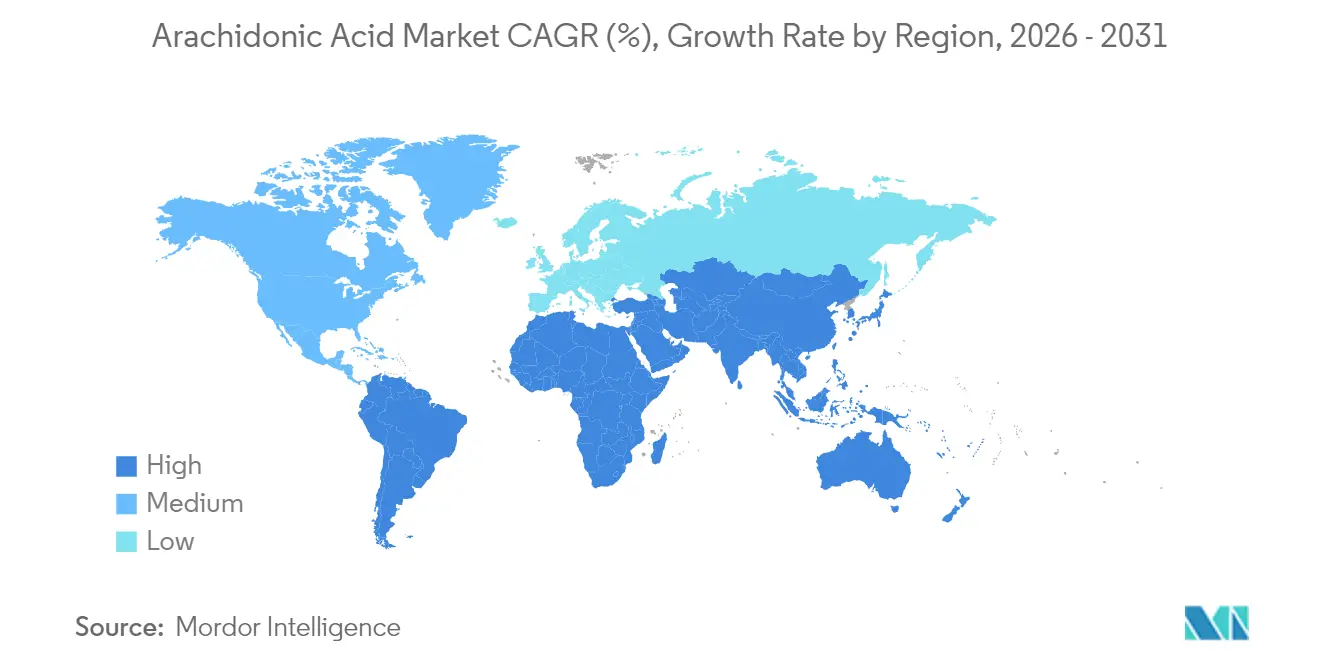

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Arachidonic Acid Market Analysis by Mordor Intelligence

The arachidonic acid market size was valued at USD 262.12 million in 2025 and estimated to grow from USD 272.76 million in 2026 to reach USD 332.92 million by 2031, at a CAGR of 4.06% during the forecast period (2026-2031). Steady global demand for arachidonic acid (ARA) is on the rise, primarily due to its crucial role in human health. This demand surge, especially pronounced in sectors like infant nutrition, pharmaceuticals, and functional foods, is propelling the expansion of the Arachidonic Acid market. ARA, an omega-6 polyunsaturated fatty acid, plays a pivotal role in brain development, immune function, and cellular signaling. Its significance is underscored by its inclusion as a key additive in infant formulas, aiming to replicate the nutritional profile of breast milk. For instance, after a thorough safety evaluation, Health Canada greenlit the use of ARASCO (an ARA oil derived from Mortierella alpina) in infant formulas on October 21, 2024. Concurrently, with rising birth rates in developing regions and a global uptick in awareness about early childhood nutrition, the demand for ARA-enriched infant formulas is witnessing a pronounced surge. Beyond infant nutrition, ARA's therapeutic potential in addressing neurological, cardiovascular, and inflammatory conditions has piqued the interest of pharmaceutical and nutraceutical firms, broadening its application spectrum. Furthermore, a health-conscious populace, alongside escalating investments in advanced nutritional and functional ingredients, is amplifying ARA's incorporation into dietary supplements and fortified foods. Collectively, these dynamics are not only bolstering global demand for ARA but also catalyzing the growth of the Arachidonic Acid market.

Key Report Takeaways

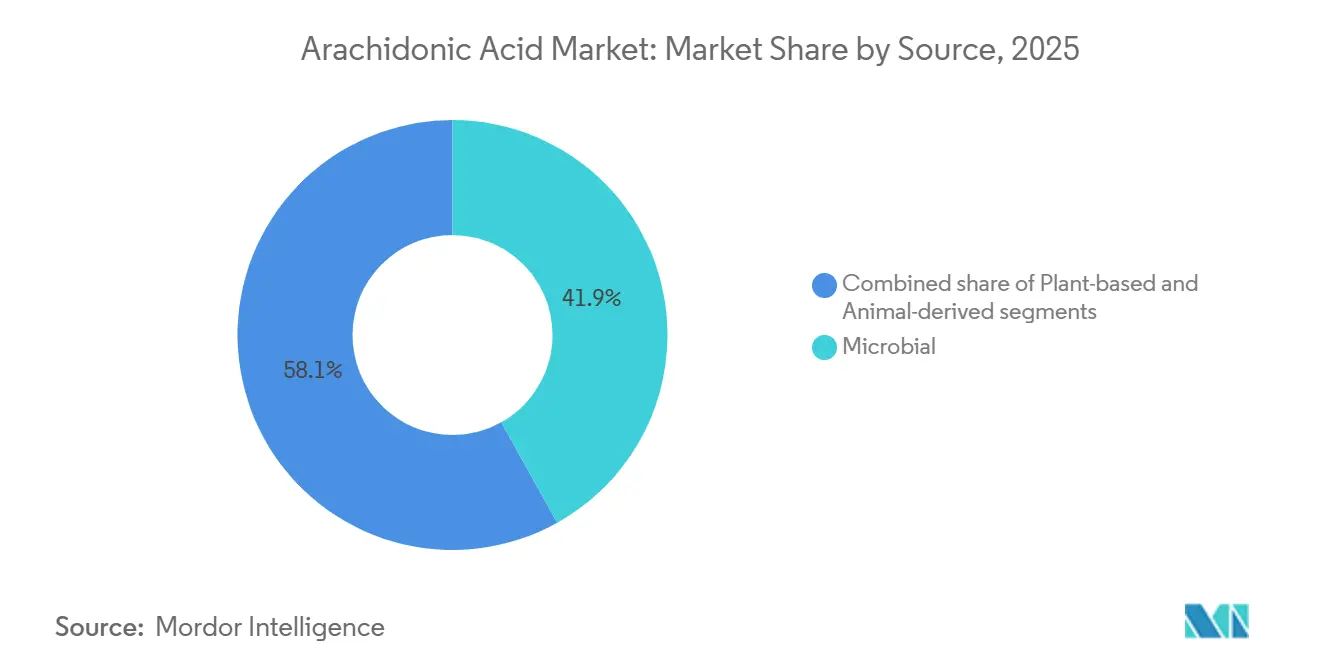

- By source, microbial fermentation commanded 41.91% of arachidonic acid market share in 2025; plant-based sources are projected to expand at a 5.99% CAGR through 2031.

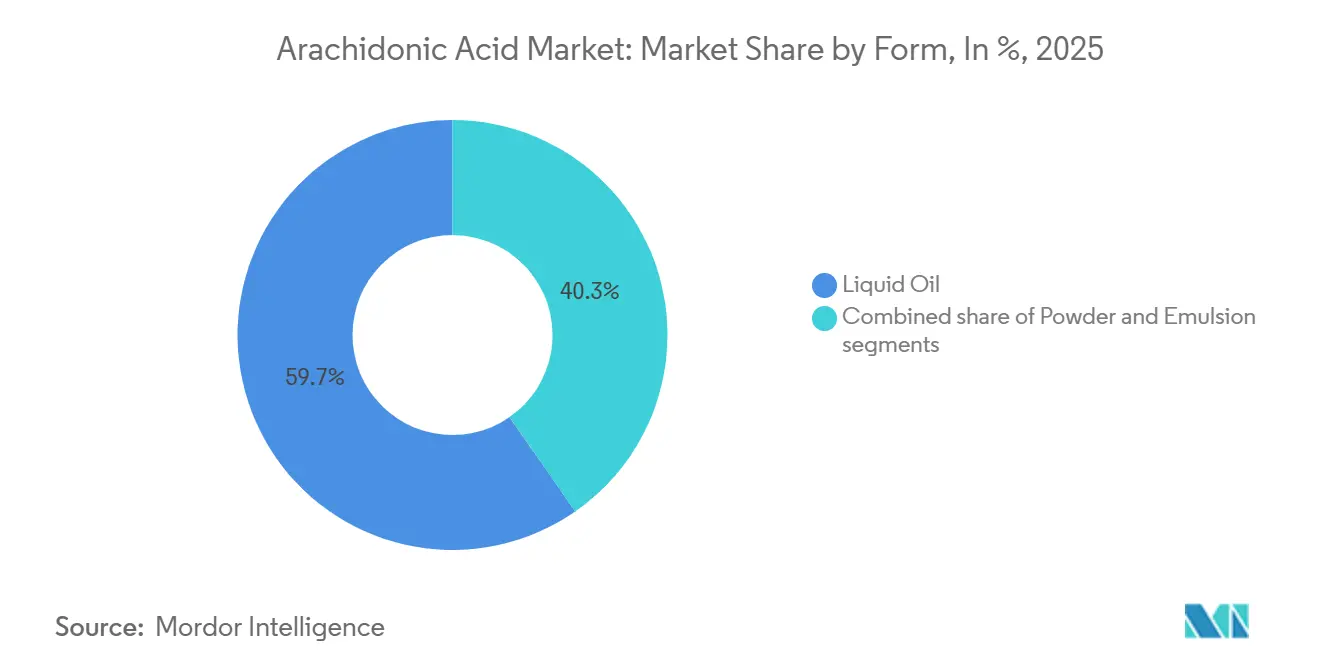

- By form, liquid oils accounted for 59.67% of the arachidonic acid market size in 2025, while powders are set to grow at 5.72% CAGR to 2031.

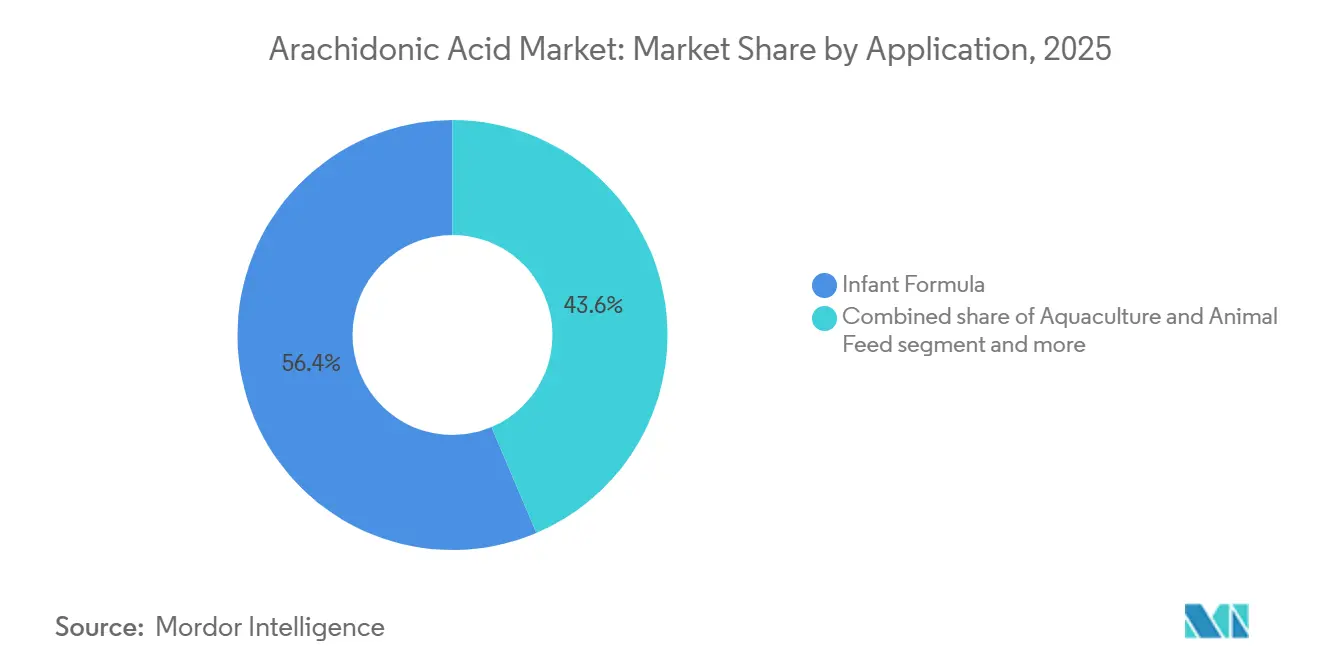

- By application, infant formula held 56.39% of arachidonic acid market share in 2025; aquaculture and animal feed is poised to be the fastest at 6.15% CAGR to 2031.

- By geography, North America led with 30.92% revenue share in 2025; Asia-Pacific is projected to grow at 5.59% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Arachidonic Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for arachidonic acid (ara)-fortified infant formula | +1.2% | Global, with strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Growing health consciousness and dietary supplement use | +0.8% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Increasing geriatric population and lifestyle-related disorders | +0.6% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Emerging aquaculture feed enrichment use-cases | +0.7% | Asia-Pacific core, spill-over to Latin America | Medium term (2-4 years) |

| Consumer preference for functional lipids and omega fatty acids | +0.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Growing focus on preventive healthcare and wellness products | +0.4% | Global, strongest in high-income markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for arachidonic acid (ara)-fortified infant formula

Surging demand for ARA-fortified infant formulas is driving the global ARA market's growth. ARA, an essential omega-6 fatty acid found naturally in breast milk, is pivotal for infant brain development, immune function, and visual acuity. With rising awareness of early-life nutrition, parents and healthcare providers increasingly favor infant formulas that mimic human milk's nutritional profile, emphasizing both DHA and ARA. This trend is notably strong in regions like Asia-Pacific, Latin America, and Africa, where breastfeeding rates are declining or birth rates are on the rise. These areas are witnessing a heightened demand for premium, nutritionally complete infant formulas. For context, the Central Intelligence Agency reported that in 2024, Niger boasted the world's highest birth rate at 46.6 births per 1,000 inhabitants, followed by Angola, Benin, Mali, and Uganda [1]Central Intelligence Agency, "Ranking of the 20 countries with the highest birth rate", www.cia.gov. Regulatory bodies and scientific endorsements have underscored ARA's significance in infant nutrition, leading more formula manufacturers to integrate it into their offerings. Consequently, ARA has emerged as a vital ingredient in the infant nutrition landscape, fueling the global ARA market's expansion.

Growing health consciousness and dietary supplement use

Global health consciousness is on the rise, and with it, the demand for dietary supplements. As consumers increasingly recognize the significance of targeted nutrition for their well-being, the demand for functional ingredients especially those supporting cognitive health, immune function, and inflammatory responses has surged. Arachidonic acid (ARA) is pivotal in these areas. For instance, a 2023 survey by the Council for Responsible Nutrition (CRN) revealed that a record 74% of United States adults turned to dietary supplements [2]Council for Responsible Nutrition (CRN), "2023 CRN Consumer Survey on Dietary Supplements", www.crnusa.org. Fitness enthusiasts and athletes are gravitating towards ARA-based supplements, drawn by their potential to boost muscle growth, strength, and recovery, solidifying ARA's place in sports nutrition. Meanwhile, an aging population is on the lookout for supplements to bolster brain and cardiovascular health. Given ARA's role in neural signaling and anti-inflammatory processes, it's no wonder interest in ARA is intensifying. This heightened demand has led supplement manufacturers to blend ARA into capsules, softgels, and powders, often pairing it with DHA and other omega fatty acids for a holistic health approach. Consequently, as health awareness grows and proactive supplementation becomes the norm, the global ARA market is witnessing a broad expansion across diverse consumer demographics.

Increasing geriatric population and lifestyle-related disorders

As individuals age, they face heightened risks of chronic health challenges, including cognitive decline, cardiovascular diseases, joint inflammation, and diminished immune responses. ARA has emerged as a key player in addressing these concerns, given its established roles in cell signaling, inflammation modulation, and brain health. This has spurred a surge in interest for ARA-infused nutritional and pharmaceutical products, all aimed at managing age-related ailments and enhancing the quality of life for seniors. For example, data from ChildStats.gov indicates that in 2023, 17.7% of the U.S. population was aged 65 or older, marking a notable rise from previous years. Additionally, the uptick in lifestyle-related ailments like obesity, type 2 diabetes, and metabolic syndrome, often linked to sedentary lifestyles and poor dietary choices has amplified the demand for functional ingredients such as ARA, which bolster systemic health. In response, healthcare professionals and supplement manufacturers are increasingly incorporating ARA into their formulations, catering to the nutritional needs of both the aging population and those at risk. As a result, these demographic shifts and health trends are driving a robust and expanding global demand for ARA in pharmaceutical, nutraceutical, and functional food markets.

Consumer preference for functional lipids and omega fatty acids

Health-conscious consumers are increasingly turning to foods and supplements that promise specific physiological benefits, such as enhanced brain function, bolstered immunity, and reduced inflammation. As a result, functional lipids, particularly ARA, are gaining traction. ARA, an essential omega-6 fatty acid, plays a pivotal role in maintaining cell membrane integrity, fostering neurological development, and modulating immune responses. Consequently, ARA has found its way into a diverse array of health-centric products, from infant formulas and dietary supplements to fortified foods. This trend is further fueled by a growing recognition of omega fatty acids as vital elements in preventive health and wellness routines. Highlighting this trend, a 2023 survey by the Council for Responsible Nutrition (CRN) revealed that a record 74% of U.S. adults reported taking dietary supplements. In response to the surging demand for transparent, scientifically-backed nutritional solutions, manufacturers are now pairing ARA with omega-3s, such as DHA and EPA, crafting more holistic and potent formulations. This global pivot towards functional lipids not only broadens ARA's application horizons but also propels its market growth across the nutrition, pharmaceutical, and wellness sectors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from alternative omega-6 fatty acid sources | -0.9% | Global, strongest in cost-sensitive markets | Short term (≤ 2 years) |

| High production costs associated with extraction and processing | -0.7% | Global, particularly affecting emerging markets | Medium term (2-4 years) |

| Strict regulatory requirements for arachidonic acid usage in infant formula and dietary supplements | -0.5% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Price volatility of raw materials affecting production costs and market stability | -0.6% | Global, with acute impact in Asia-Pacific production hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from alternative omega-6 fatty acid sources

Alternative sources of omega-6 fatty acids are challenging the growth of the global arachidonic acid (ARA) market. These alternatives are not only more cost-effective but also more readily available and scalable for both manufacturers and consumers. ARA is known for its unique physiological benefits, especially concerning neural and immune functions. However, other omega-6 fatty acids, like linoleic acid, are proving to be more economically viable. Linoleic acid is abundant in vegetable oils, including soybean, sunflower, and corn oil. For context, the USDA Foreign Agricultural Service reported that in the 2023/24 period, global usage of soybean oil exceeded 63.87 million metric tons. Due to their lower production costs and well-established supply chains, these alternative omega-6s are frequently incorporated into functional foods, dietary supplements, and infant nutrition products. Additionally, regulatory and consumer concerns regarding excessive omega-6 intake especially its potential association with pro-inflammatory effects have prompted manufacturers to adopt a more balanced omega profile. This often means reducing or substituting ARA with other fatty acids. As a result, the competitive edge of these more affordable and accessible omega-6 sources is curtailing ARA's penetration into the mass market. This limitation is stifling ARA's broader acceptance in mainstream nutritional and pharmaceutical products, ultimately hindering its market growth.

High production costs associated with extraction and processing

High production costs tied to the extraction and processing of arachidonic acid (ARA) significantly hinder the global ARA market's growth. Typically, ARA undergoes a complex, resource-intensive fermentation process using microorganisms like Mortierella alpina. This is followed by rigorous purification and quality control to adhere to strict food and pharmaceutical standards. Such processes demand advanced biotechnological infrastructure, substantial energy input, and skilled labor, culminating in heightened operational expenses. For context, McKinsey highlighted a USD 250 billion investment is essential to align bio-based ingredients with price parity, a challenge for smaller firms. Consequently, ARA's price point remains notably higher than other omega-6 fatty acids or rival nutritional ingredients, curtailing its affordability and limiting its market reach. Manufacturers of infant formula, dietary supplements, and functional foods face a dilemma: the elevated input cost of ARA often leads to pricier end products. This can alienate price-sensitive consumers, particularly in developing regions. Moreover, challenges like limited economies of scale and the demand for consistent quality in niche applications exacerbate production hurdles. Collectively, these cost-related challenges stifle broader adoption and decelerate the global expansion of the ARA market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sources: Microbial dominates, while plant-based drives innovation

Microbial sources generated 41.91% of the arachidonic acid market in 2025 dominating the market. Food and cosmetic manufacturers favor microbial-based arachidonic acid (ARA) for its unmatched consistency, scalability, and purity. By employing microbial fermentation, often with fungi such as Mortierella alpina, producers can achieve high-quality ARA in a controlled manner, sidestepping the inconsistencies tied to animal or plant sources. This precision is paramount in sectors like infant nutrition and cosmetics, where safety, allergen management, and regulatory adherence are non-negotiable. Beyond quality, microbial-based ARA resonates with sustainability and ethical considerations, aligning seamlessly with vegan and clean-label movements, thus appealing to both producers and consumers.

The plant-based lines, though niche, clock the fastest 5.99% CAGR through 2031, leveraging CRISPR and algae photobioreactors. On the other hand, the demand for plant-based ARA is on the rise. This surge is fueled by biotechnological advancements and refined extraction methods, enhancing yields from genetically modified plants or algae. Coupled with the growing popularity of plant-based diets, a consumer shift towards natural and eco-friendly ingredients, and regulatory pushes to minimize synthetic or animal-derived dependencies, the momentum is undeniable. In this evolving landscape, while microbial-based ARA reigns supreme in industrial applications for its reliability, plant-based ARA is carving out a significant niche, championing the ideals of clean, green, and ethical nutrition and personal care.

By Form: Liquid Oil applications dominate, while powder applications expand

In 2025, liquid oils commanded a 59.67% market share, bolstered by GRAS-cleared Mortierella alpina derivatives that blend seamlessly into oils and fats. Food and cosmetic manufacturers favor liquid arachidonic acid (ARA) for its formulation ease, superior bioavailability, and compatibility with oil-based systems. In the food sector, particularly in infant nutrition, liquid ARA integrates effortlessly into emulsions and lipid-based formulas, closely resembling breast milk's natural fat composition. Likewise, in cosmetics, liquid ARA is the go-to for creams, serums, and lotions, blending seamlessly with other lipophilic ingredients to enhance skin health and barrier function. Its fluid nature also streamlines dosing and homogenization during production.

Meanwhile, powdered forms are witnessing a robust 5.72% CAGR, driven by demand from sports nutrition and geriatric products for shelf-stable sachets. The demand for powdered ARA is on the rise, thanks to its stability, extended shelf life, and transport ease. Powdered ARA is making waves in dietary supplements, sports nutrition, and functional foods, where precise dosing, capsule compatibility, and dry-blend capabilities are paramount. With technological advancements and refined encapsulation techniques, powdered ARA is carving a niche across an expanding array of products. Thus, while liquid ARA remains the frontrunner in oil-based and high-bioavailability applications, powdered ARA is positioning itself as a practical and scalable alternative for a wider product range.

By Application: Infant formula dominates, while aquaculture and animal feed grows

Infant formula commanded a 56.39% share in 2025, fortified by mandatory inclusion laws across Europe, China, and parts of North America. Infant formula manufacturers are driving high demand for arachidonic acid (ARA) due to its pivotal role in early brain development, immune function, and visual acuity in infants. ARA, alongside DHA, is naturally found in breast milk. Its addition to infant formula not only mirrors the nutritional profile of human milk but also aligns with parental expectations and regulatory standards in numerous countries. Consequently, ARA has become a staple in premium and medically endorsed formulas, particularly in regions with lower breastfeeding rates or a pronounced emphasis on fortified infant nutrition.

Aquaculture and animal feed is growing at a 6.15% CAGR through 2031 reflects seafood boom especially in Asia-Pacific and scientific validation of species-specific ARA thresholds. Simultaneously, the aquaculture and animal feed industries are witnessing a surge in ARA demand. Ongoing research underscores ARA's benefits in enhancing growth performance, bolstering immune resilience, and promoting reproductive health in both fish and livestock. With the rising popularity of sustainable and efficient feed formulations, especially for high-value aquaculture species, ARA's incorporation is seen as a means to boost health and survival rates. Furthermore, the expanding aquaculture production is poised to amplify ARA's usage in aqua feed manufacturing. For example, the FAO reported a rise in global fish production from 186.6 million metric tons in 2023 to 190 million metric tons in 2024 . While current ARA volumes in animal nutrition lag behind those in infant formula, this segment is rapidly expanding, fueled by surging global protein demand and strides in animal health science. Collectively, these dynamics are propelling a significant uptick in ARA demand across both human and animal nutrition sectors.

Geography Analysis

In 2025, North America held a dominant 30.92% market share, bolstered by established formula brands and strong GRAS pathways. North America's stable policies and established retail channels have paved the way for the early adoption of functional lipids. The FDA's GRAS notifications, which encompass a range of ARA-rich oils, provide formulators with a clear market entry route. Canada's acceptance of Ahiflower oil highlights its receptiveness to new fatty acids, inadvertently intensifying competition and driving quality enhancements among ARA suppliers.

Meanwhile, Asia-Pacific, with a 5.59% CAGR, benefited from rising disposable incomes, favorable demographics, and a rapidly expanding aquaculture sector. Updates to China's GB regulations are pushing local producers to reformulate, leading to a surge in short-term ingredient orders. Asia-Pacific stands out for its scale and rapid pace: China's stricter standards are amplifying the urgency for global sourcing, and in India, reductions in feed tariffs are enhancing aquaculture's profitability. Japan's older demographic is increasingly purchasing fortified foods, underscoring a growing demand for adult nutrition. Meanwhile, Australia's rigorous clean-label regulations are favoring high-purity imports, benefiting suppliers who can demonstrate microbiological controls. Together, these dynamics are shifting the arachidonic acid market towards a more diversified set of demand centers.

Europe's 1% cap on fat-based ARA, coupled with EFSA's ongoing review, poses stringent compliance challenges for manufacturers operating in the region. These regulatory measures, however, play a crucial role in ensuring product safety and quality, thereby bolstering foundational demand for compliant products. Germany and France, recognized for their strong preference for premium organic formulas, lead the region in consumption, reflecting a growing consumer inclination toward high-quality and sustainable options. Furthermore, European retailers are increasingly committing to sustainability goals, which are driving a shift toward microbial sourcing of ingredients. This transition not only aligns with environmental objectives but also significantly reduces the carbon footprint associated with the reliance on imported fish oils, offering a more eco-friendly alternative for the market.

Competitive Landscape

The arachidonic acid market is fragmented, with multiple companies competing without a single dominant player. Companies like Cargill, Incorporated, DSM-Firmenich AG, and BASF SE maintain their competitive positions through established regulatory compliance and global distribution networks. These companies focus on research and development to enhance product quality and expand their market presence. They also form strategic partnerships and invest in production facilities to strengthen their position in key regions and meet growing market demand.

Emerging start-ups are increasingly utilizing synthetic biology to carve out a niche in the arachidonic acid market. Furthermore, start-ups are building intellectual-property portfolios that include high-titer strains and solvent-free purification processes. While these advancements create barriers to entry for competitors, they also open up opportunities for generating licensing revenue, adding another dimension to the competitive landscape.

Supply-chain resilience is becoming a critical differentiator in the arachidonic acid market. Companies that integrate feedstock contracts and regional tolling operations are better positioned to mitigate the impact of commodity price fluctuations. This approach not only reduces volatility but also appeals to infant-formula OEMs, which operate under stringent zero-defect mandates. By ensuring a stable and reliable supply chain, these firms can effectively address the demands of their clients while maintaining a competitive advantage in the market.

Arachidonic Acid Industry Leaders

-

Cargill, Incorporated

-

DSM-Firmenich AG

-

BASF SE

-

Cabio Biotech

-

Merck Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Louis Dreyfus Company (LDC) acquired BASF’s Food and Health Performance Ingredients business, including a production site and state-of-the-art research and development center in Illertissen, Germany, and three application labs outside of Germany.

- May 2023: Avanti Polar Lipids, LLC has teamed up with Bioz to introduce Bioz Badges. This AI-driven tool provides real-time insights into the applications of the company's products. With Bioz Badges, customers can track the global usage of the company's products in research studies, gaining insights into the when, where, how, and why of their application.

Global Arachidonic Acid Market Report Scope

The arachidonic acid market is distributed in a different segment on the source, form, application, and by geography. By source, arachidonic acid market is segmented into animal and plant; by form into dry and liquid; by its application into food & beverage and pharmaceutical. The food & beverage segment is further divided into infant formula and dietary supplements. Among food & beverage sub-segments, infant nutrition holds the dominant share of the market and being driven by regulatory support.Also, the study provides an analysis of the arachidonic acid market in the emerging and established markets across the globe, including North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

By Source

| Microbial |

| Animal-derived |

| Plant-based |

By Form

| Liquid Oil |

| Powder |

| Emulsion |

By Application

| Infant Formula |

| Dietary Supplements |

| Functional Beverages |

| Pharmaceuticals |

| Aquaculture and Animal Feed |

| Cosmetics and Personal Care |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Source | Microbial | |

| Animal-derived | ||

| Plant-based | ||

| By Form | Liquid Oil | |

| Powder | ||

| Emulsion | ||

| By Application | Infant Formula | |

| Dietary Supplements | ||

| Functional Beverages | ||

| Pharmaceuticals | ||

| Aquaculture and Animal Feed | ||

| Cosmetics and Personal Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving current growth in the arachidonic acid market?

Regulatory tightening around infant-formula nutrition, rising aquaculture feed enrichment, and growing adult supplement use are the primary drivers influencing a projected 4.06% CAGR to 2031.

Which source segment leads the arachidonic acid industry?

Microbial fermentation leads with 41.91% revenue share, owing to high-purity yields and sustainable production advantages.

How large is the arachidonic acid market size within infant formula?

Infant formula applications accounted for 56.39% of the arachidonic acid market share in 2025, reflecting mandatory inclusion across multiple regions.

Which region is expanding fastest for arachidonic acid demand?

Asia-Pacific is forecast to grow at 5.59% CAGR through 2031, driven by higher birth rates, aquaculture expansion, and evolving food regulations.

What are the main cost barriers for new arachidonic acid producers?

High capital outlays for fermentation infrastructure, substrate price volatility, and stringent purification standards pose significant cost challenges.

Are plant-based arachidonic acid sources commercially viable?

Yes. Engineered soybean platforms are advancing at a 5.99% CAGR, but widespread adoption depends on regulatory approvals and cost competitiveness.

Page last updated on: