United States Saccharin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

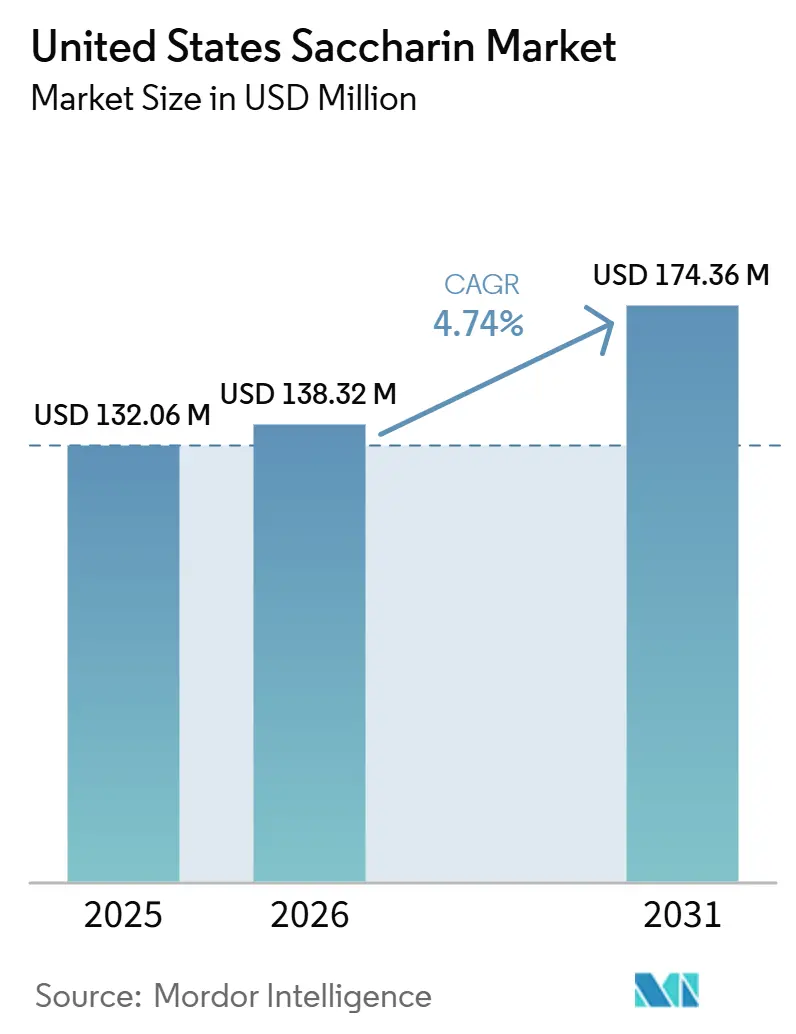

| Base Year Market Size (2025) | USD 132.06 Million |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 138.32 Million |

| Market Size (2031) | USD 174.36 Million |

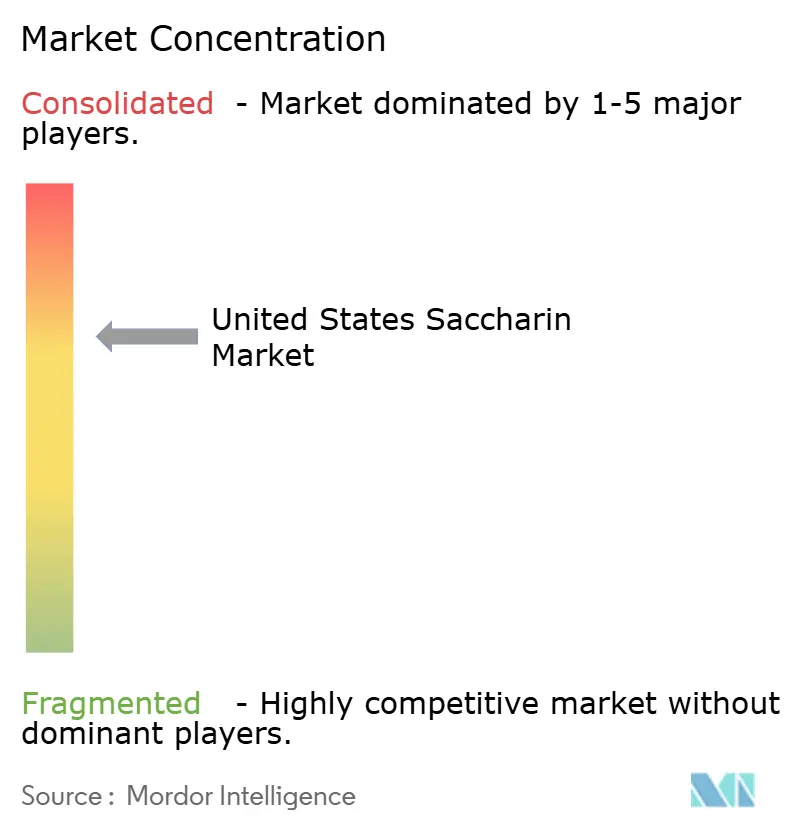

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Saccharin Market Analysis by Mordor Intelligence

The United States saccharin market size was valued at USD 132.06 million in 2025 and is estimated to grow from USD 138.32 million in 2026 to reach USD 174.36 million by 2031, at a CAGR of 4.74% during the forecast period (2026-2031). The United States saccharin market is supported by a durable health need, because adult obesity remained high in the latest NHANES cycle, which keeps demand in place for calorie-free sweetening systems used in food, beverages, and medicine. The United States saccharin market also benefits from a stable regulatory base, since saccharin remains one of the high-intensity sweeteners permitted in the country and is listed under 21 CFR 180.37 with an acceptable daily intake of 15 mg/kg body weight per day. Supply conditions continue to matter in the United States saccharin market, because domestic production is limited and buyers rely on certified imported material for food, pharmaceutical, and personal care use. Competition in the United States saccharin market remains active across price, grade, and service, with certified suppliers holding stronger positions where documentation, consistency, and application support matter more than spot pricing. At the same time, the United States saccharin market faces pressure from clean-label preferences, natural sweetener substitution, and closer labeling scrutiny, which keeps growth steady rather than rapid.

Key Report Takeaways

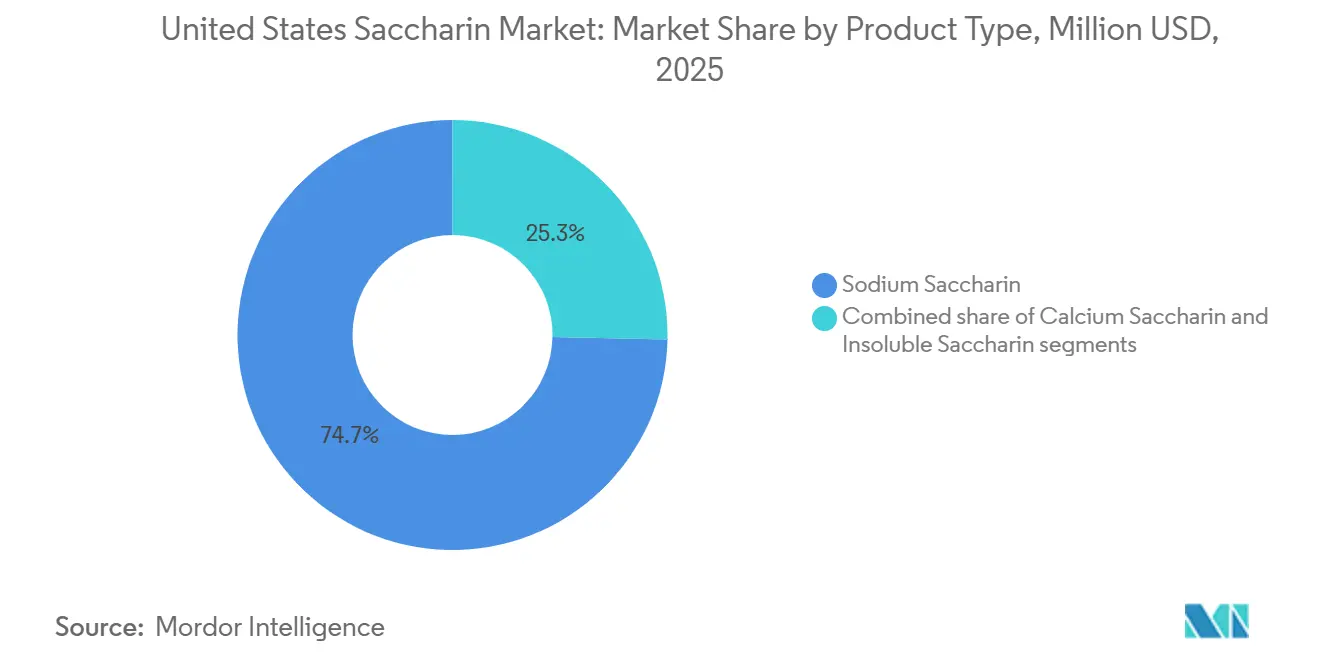

- By product type, sodium saccharin led with 74.67% share in 2025, while calcium saccharin is forecast to expand at 5.64% CAGR through 2031.

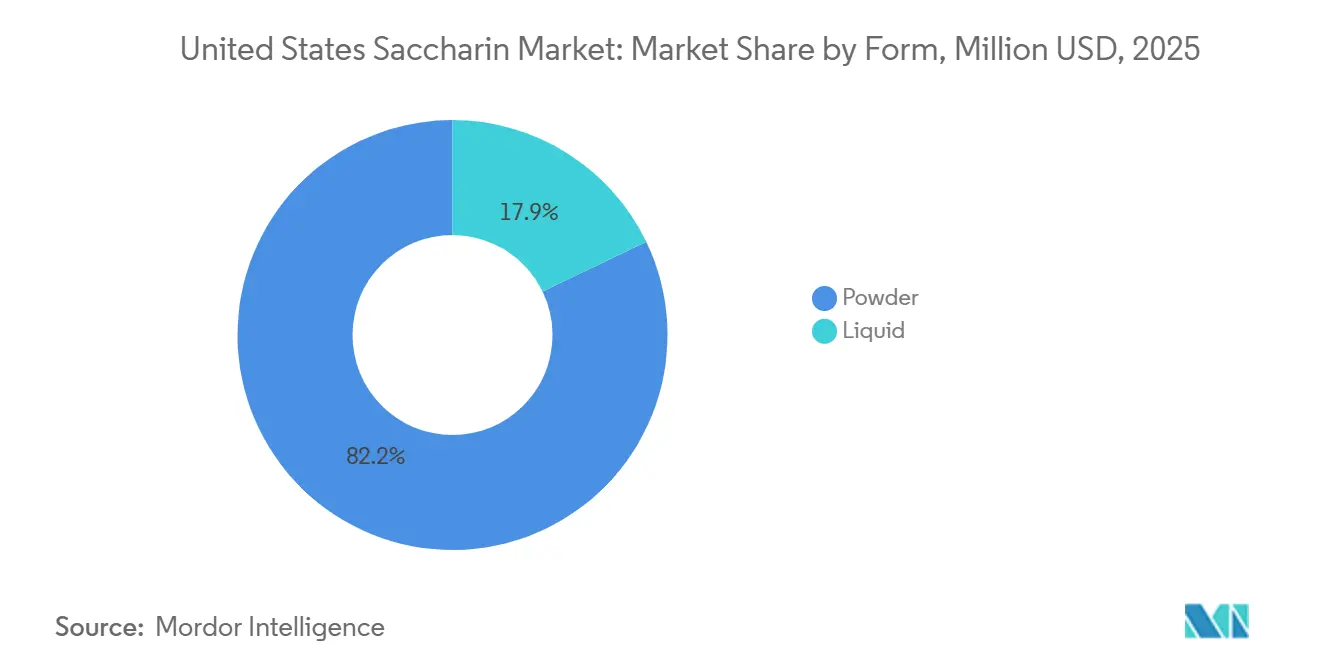

- By form, powder held 82.15% share in 2025 and also recorded the fastest projected CAGR at 5.87% through 2031.

- By application, food and beverages accounted for 68.73% share in 2025, while pharmaceuticals segment is projected to grow at 5.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Saccharin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of obesity and diabetes is accelerating demand for zero-calorie sweeteners | +1.5% | National, with elevated demand in Southern United States with higher obesity and diabetes concentrations | Short term (≤ 2 years) |

| Increasing consumer preference for low-glycemic food ingredients | +0.9% | National, concentrated among health-focused demographics in urban and suburban centers | Medium term (2–4 years) |

| Expanding use of saccharin in oral care formulations | +0.6% | National, with spillover demand from global oral care supply chains | Medium term (2–4 years) |

| Growth in convenience and packaged food consumption | +0.8% | National, amplified in food manufacturing hubs in the Midwest and Mid-Atlantic | Short term (≤ 2 years) |

| Growing use of saccharin in veterinary pharmaceuticals and animal nutrition | +0.4% | National, with early-stage growth in specialized veterinary pharmaceutical compounding | Long term (≥ 4 years) |

| Consumption of sugar-free chewing gum, confectionery, and desserts | +0.7% | National, strongest in mass-market retail and convenience channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Prevalence of obesity and diabetes driving consistent demand

The structural health burden supporting saccharin demand continues to intensify, as clinical data indicate. The 2021–2023 National Health and Nutrition Examination Survey (NHANES) measured US adult obesity at 40.3%, with 9.7% of adults classified as severely obese[1]Source: National Center for Health Statistics, “National Health and Nutrition Examination Survey,” CDC, cdc.gov. In parallel, the Gallup 2025 National Health and Well-Being Index reported diabetes diagnoses at an all-time high of 13.8%, creating a recurring structural demand floor for zero-calorie sweeteners in food and medicine. Saccharin’s zero-calorie and blood-sugar-neutral profile makes it highly relevant for diabetic-compliant product formulations, including sugar-free syrups, chewable medications, and dietary beverages. Pediatric use of saccharin is also increasing in pharmaceutical formulations, an often-overlooked demand driver. Its regulatory acceptance in oral liquid suspension manufacturing supports formulation decisions when a patient’s glycemic sensitivity is a clinical constraint. This demand remains insulated from broader “clean label” sentiment because functional requirements, rather than aesthetic preferences, drive its use.

Consumer shift toward low-glycemic ingredients reshaping formulation strategy

The transition from sugar reduction as a marketing differentiator to an operational reformulation requirement is well underway. The 2025 IFIC Food & Health Survey found that “low in sugar” ranked among the top three purchase-driving claims cited by US consumers, with 34% identifying it as a key consideration. According to industry formulation analysis reported by Innova, 5% of US food and beverage product launches in 2025 carried a “no added sugar” or “sugar-free” claim. Saccharin offers a significantly lower cost per sweetness unit than stevia concentrates or monk fruit extracts, which require multi-step agricultural extraction. This cost advantage makes saccharin the default specification in price-sensitive reformulation programs. The advantage becomes more pronounced as packaged food companies aim to absorb inflationary pressures without raising retail prices. The GLP-1 medication wave is also driving a nuanced structural shift. GLP-1 users reduce caloric intake and show the largest reductions in sugary food consumption, expanding the net addressable base of low-calorie product consumers. This trend positions saccharin favorably within the accelerating dietary management segment.

Expanding use in oral care: an underappreciated volume driver

Market analyses focused on food and beverages often understate saccharin’s role in oral care formulations. Formulators use sodium saccharin at concentrations as low as 0.01%–0.1% to mask the metallic and bitter notes of fluoride, surfactants, and antibacterial actives such as chlorhexidine. This improves the palatability of toothpaste, mouthwash, and dental rinse products, particularly in children’s formulations. Multiple US patent applications dated 2024–2025 include sodium saccharin as a standard sweetening component in dentifrice compositions, including a 2025 filing for arginine-based toothpaste and a 2025 filing for high-sodium-bicarbonate dentifrice formulations. As the oral care industry shifts toward specialized antibiotic-alternative compounds and functional active ingredients, formulations are becoming more bitter and complex, increasing the value of saccharin’s masking efficiency. The Calorie Control Council’s 2025 Regulatory Handbook lists saccharin’s acceptable daily intake (ADI) at 15 mg/kg bw/day under the FDA’s interim food additive listing, giving formulators established safety headroom for broader use concentrations.

Sugar-free confectionery and packaged foods creating a durable demand layer

The US sugar-free confectionery segment is expanding at a measurable pace. Annual gum sales are projected to increase by USD 1.2 billion and reach USD 3.9 billion by 2025, with sugar-free variants accounting for nearly 90% of total gum sales. In the broader confectionery market, gummies and chewy candies remain the most dynamic sugar-free format, growing by 10%–12% annually as polyol and fiber-bulking systems improve texture without requiring reformulation of sweetener systems. The FDA's 2026 Human Foods Program agenda, which explicitly targets sugar reduction strategies and the assessment of non-nutritive sweeteners, is expected to increase industry investment in reformulation and drive ingredient demand for cost-effective sweeteners, including saccharin[2]Source: U.S. Food and Drug Administration, “Human Foods Program Constituent Updates,” FDA, fda.gov. Spanish-language industry analysis indicates that sodium saccharin manufacturers and suppliers in the United States report 5%–7% annual growth momentum, supported by demand from beverages and low-calorie snacks. This convergence of regulatory intent and consumer behavior reinforces demand stability across packaged food and confectionery verticals during the forecast period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lingering consumer concerns regarding the safety of artificial sweeteners | -0.7% | National, more acute in premium and natural food channels on the West Coast and the Northeast | Short term (≤ 2 years) |

| Growing popularity of stevia, monk fruit, and allulose | -1.0% | National, amplified in health-specialty retail and clean-label product launches | Medium term (2–4 years) |

| Stringent food labeling and regulatory compliance requirements | -0.4% | National compliance influence significantly under FDA 21 CFR 180.37 and proposed MAHA labeling reviews | Medium term (2–4 years) |

| Fluctuations in raw material and manufacturing costs | -0.3% | Global supply chain, with downstream effects concentrated among US importers reliant on Chinese and Korean producers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer safety perceptions creating selective demand compression

Residual skepticism about artificial sweeteners remains one of the most persistent structural restraints on saccharin’s addressable market in the United States. The 2025 Innova Health and Nutrition survey is expected to show that at least one-quarter of US consumers actively limit artificial sweeteners, even as they seek to reduce sugar intake. This behavioral contradiction narrows the effective commercial window for saccharin-containing product launches. The MAHA movement’s 2026 food policy agenda, which may include a potential FDA review of ingredient labeling for non-nutritive sweeteners, could introduce regulatory uncertainty. Some large consumer packaged goods companies have already pre-empted this risk by reformulating premium and children’s product lines to remove synthetic sweeteners. Under 21 CFR 180.37, the compliance framework classifies saccharin as an interim food additive that remains technically “pending additional study.” This unusual regulatory position permits legal use but does not provide the definitive “generally recognized as safe” status that newer additives hold. As a result, saccharin may remain vulnerable in brand-conscious reformulation decisions, even where scientific evidence supports its safety.

Natural sweetener alternatives eroding market share in premium applications

Competitive pressure from stevia, monk fruit, and allulose remains uneven. It is concentrated in high-visibility, premium, and clean-label product categories, where brand equity depends heavily on ingredient perception. In June 2025, the European Food Safety Authority concluded that D-allulose could not be established as safe as a novel food due to incomplete toxicological data, stalling EU market access, while the United States continues to permit allulose. This regulatory asymmetry may accelerate US product development using allulose and monk fruit blends, positioning them as premium alternatives to saccharin in high-margin categories. In 2025, Manus Bio launched a commercially scalable, fermentation-derived monk fruit sweetener in the United States, offering domestic food and beverage brands a supply-chain-resilient alternative to Chinese-grown monk fruit. Together, these alternatives are directing new product development investment away from saccharin in the premium food and beverage market, even as saccharin maintains strong positions in cost-sensitive, industrial, and pharmaceutical applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sodium Saccharin Dominates, Calcium Saccharin Emerging with Precision Applications

Sodium Saccharin is projected to hold a 74.67% market share in 2025, supported by decades of regulatory acceptance, broad use across the food, pharmaceutical, and personal care sectors, and a well-established supply chain led by primary producers in China, South Korea, and India. Its solubility profile and taste characteristics make it the default specification for high-volume applications, including diet beverages, sugar-free confectionery, cough syrups, and oral care products. Insoluble Saccharin serves a specialized niche, mainly in food applications requiring controlled-release or delayed sweetness delivery; its market contribution remains modest and stable. Calcium Saccharin is expected to grow the fastest, at a 5.64% CAGR through 2031. Notably, Blue Jet Healthcare confirmed the successful scale-up and initial commercial production of Calcium Saccharin during FY2024-25 in response to a specific formulation requirement from an FMCG customer[3]Source: Blue Jet Healthcare, “Annual Report FY2024-25,” Blue Jet Healthcare, bluejethealthcare.com. This signals real-world demand for Calcium Saccharin in oral care and pharmaceutical formulations, where its lower bitterness threshold compared to Sodium Saccharin offers a measurable taste-profile advantage. Both Sodium Saccharin and Calcium Saccharin are explicitly listed under the FDA's 21 CFR 180.37, maintaining compliance eligibility across all key US application categories.

The product type segment also has a notable supply chain dimension. Henan Kaifeng Pingmei Shenma Xinghua Fine Chemical accounts for an outsized share of Chinese saccharin production. Collectively, Chinese producers exported 19,000 metric tons in 2024, a 19% increase from the previous year, with the United States among the key receiving markets. This production surge kept commodity-grade Sodium Saccharin prices under pressure, with US import prices averaging USD 9,579 per ton in 2024. However, pharmaceutical-grade specifications command a significant premium, reflected in the US average export price of USD 38,262 per ton in 2024. This price differential confirms that product type selection in this market is not only a formulation decision but also a strategic choice that separates commodity saccharin from value-added saccharin trade flows.

By Form: Powder's Dual Leadership Reflects Industrial Specification Logic

Powder form is expected to account for 82.15% of the US saccharin market in 2025 and remain the fastest-growing form, registering a CAGR of 5.87% through 2031. Its position as both the largest and fastest-growing form indicates deepening industrial adoption rather than cyclical momentum. Powder saccharin’s dominance stems from its process compatibility. It blends uniformly into dry mixes, tableted pharmaceutical formulations, dry beverage powders, powdered sweetener blends, and bakery premixes without adding moisture or requiring dissolution steps. Large food manufacturers and pharmaceutical compounders operating continuous-process lines would need process modifications to switch to alternative sweetener forms, creating strong inertia against substitution. Liquid saccharin plays a smaller role in beverage concentrate manufacturing and certain pharmaceutical liquid formulations where manufacturers prefer precise volumetric dosing. Its share reflects niche application needs rather than broad competition with powder. Growth in powder-form saccharin also benefits from the expanding domestic market for dry protein supplements, meal-replacement powders, and flavored hydration packets, where calorie-neutral sweetening in a dry, stable powder form is a technical requirement.

The alignment between the dominant segment and the forecast CAGR for powder saccharin highlights a counterintuitive trend. Although natural sweetener alternatives continue to gain consumer visibility, food-grade and pharmaceutical-grade saccharin powder is growing in volume within its industrial customer base. Japanese industry analysis confirms that the clean-label movement is shifting demand away from saccharin in consumer-visible products. However, industrial and pharmaceutical buyers continue to maintain and expand their specifications for the ingredient because of its stability, cost advantages, and regulatory predictability (GII Japan, US Saccharin Market Report, 2025). This bifurcation in demand, with declining consumer visibility alongside growing industrial specification, may not be evident from aggregate market figures alone. However, it has significant implications for how producers and distributors position their product offerings through 2031.

By Application: Food and Beverages Anchors Volume, Pharmaceuticals Commands Growth Premium

Food and Beverages is expected to hold 68.73% of the 2025 US saccharin market, supported by use across sugar-free chewing gum (nearly 90% of all gum sales are sugar-free, according to NCA), diet carbonated beverages, bakery and confectionery, dairy desserts, and tabletop sweetener packets such as Sweet'N Low. Beverage formulations lead the segment, especially carbonated soft drinks, where saccharin’s cost efficiency at an industrial scale supports price-competitive “diet” positioning. Bakery and Confectionery, Dairy Products, and other Food and Beverage sub-categories also represent significant volume applications. Saccharin’s heat stability across a pH range of 6.5–8.5 at temperatures of up to 100°C gives it technical advantages over less stable sweeteners.

The Pharmaceuticals segment, projected to grow at a CAGR of 5.03% through 2031, concentrates the market’s margin potential and structural resilience. Manufacturers use saccharin in pediatric oral liquid formulations, cough syrups, chewable tablets, and taste-masking systems for bitter active pharmaceutical ingredients. Its USP and BP monograph acceptance makes it a specification default in regulated drug manufacturing. Personal Care and Cosmetics represents a meaningful adjacent growth opportunity, with multiple 2024–2025 patent filings detailing sodium saccharin use at concentrations of 0.01%–0.1% in toothpaste and mouthwash, including arginine-based and high-sodium-bicarbonate toothpastes. Animal Feed remains a small but operationally distinct use case. The European Commission’s Regulation EU 2024/1727, which banned sodium saccharin in animal feed from July 2024 due to groundwater environmental concerns, has created regulatory divergence with the United States, where no equivalent prohibition exists. US compound feed manufacturers and veterinary pharmaceutical compounders therefore retain saccharin as a permissible palatability-enhancing ingredient, though the EU development warrants monitoring as a precedent-setting regulatory signal.

Geography Analysis

The United States is expected to account for a high share of North American saccharin consumption volume in 2025, reflecting its clear United States saccharin market share within the regional trade structure. This position highlights the extent to which regional demand is concentrated in one country, with volume supported by its large packaged food, pharmaceutical, and personal care manufacturing base. The United States saccharin market also serves as the primary destination for North American procurement activity, as most qualified demand comes from U.S. buyers rather than neighboring markets. Domestic production remains limited, so the country relies heavily on imports from Asia for a significant share of its usable supply. This import dependence increases the importance of logistics, quality certification, and supplier diversification compared to a fully domestic production system. Manufacturing density shapes the first geographic layer within the country. Food processing corridors in the Midwest, Mid-Atlantic, and Southeast continue to concentrate major saccharin demand, as these regions host large-scale beverage, bakery, confectionery, and packaged food operations. Therefore, the United States saccharin market follows the physical map of industrial production more closely than the map of the end-consumer population alone. Regions with strong contract manufacturing and ingredient-handling infrastructure also tend to support faster and more predictable procurement cycles. This pattern explains why demand clusters around established processing hubs rather than spreading evenly across all states.

Pharmaceutical concentration forms the second geographic layer. New Jersey, Pennsylvania, Illinois, and Indiana remain important because they support regulated manufacturing, formulation, and distribution networks that can absorb specification-grade saccharin for oral dosage and liquid products. In these states, purchasing often depends on validation standards, documentation control, and supply continuity rather than the lowest available spot price. This gives certified material a stronger position in the United States saccharin market, where pharmaceutical buyers have limited tolerance for supply disruptions. It also creates a regional premium for suppliers that can combine technical support with compliance-ready documentation.

Innovation-led demand creates the third layer in states such as California, Texas, New York, and Florida, where reduced-sugar and functional product development remains active. These markets matter because they influence new launches and reformulation activity, even when final production later shifts to lower-cost manufacturing states. The United States saccharin market can still participate in this innovation cycle, as cost-sensitive brands need a familiar and effective high-intensity sweetener. At the same time, these states show more visible natural sweetener substitution pressure in premium categories. As a result, the geographic picture remains mixed, with mainstream industrial demand concentrated in manufacturing hubs and substitution pressure appearing more strongly in innovation-heavy consumer markets.

Competitive Landscape

The US saccharin competitive landscape is moderately fragmented at the distribution and specification levels but highly concentrated at the manufacturing level. No more than 4–5 producers globally control meaningful volumes of pharmaceutical-grade saccharin. Chinese producers, primarily Henan Kaifeng Pingmei Shenma Xinghua Fine Chemical and Tianjin North Food Co., dominate the supply structure, along with South Korea’s Kyung-In Synthetic Corporation, India’s Blue Jet Healthcare, and PMC Specialties Group in the United States. PMC Specialties Group, the only significant domestic producer, operates under its SYNCAL brand in Cincinnati, Ohio.

PMC Specialties emphasizes product reliability, regulatory compliance, and application-specific formulation support. The company competes on service depth rather than price against lower-cost Asian producers. In its Q4 FY2025 earnings, Blue Jet Healthcare reported marginal growth of 4% in its high-intensity sweetener segment despite global headwinds, supported by stable volumes and improved price realizations. This performance shows that pharmaceutical-grade and FMCG-grade saccharin remain defensible niches for certified quality producers. A filed patent insight from 2025 further highlights saccharin’s role in active product development. Multiple US toothpaste formulation patents explicitly specify sodium saccharin as a standard sweetening component, reinforcing Blue Jet Healthcare’s long-term customer stickiness in FMCG contracts.

White space in the competitive landscape exists at the intersection of pharmaceutical CDMO services and saccharin supply. Companies that combine high-grade saccharin supply with technical pharmaceutical formulation support, including documentation, compliance audit support, and customized specifications, are well positioned to capture a disproportionate share of the growing pharmaceuticals application segment. Chinese spot-market producers remain a persistent pricing challenge for commodity applications. In FY2024, they drove a 20%–30% price discount, which compressed margins for quality producers. This price pressure is accelerating competitive stratification: commodity producers compete on volume and spot price, while certified-grade suppliers compete on regulatory documentation, application expertise, and supply continuity agreements with large FMCG and pharmaceutical customers. The compliance landscape under FDA 21 CFR 180.37, which includes specific use conditions requiring saccharin substitution for a “valid special dietary purpose,” creates natural market discipline. This framework sustains demand from regulated end users while limiting arbitrary reformulation risk.

United States Saccharin Industry Leaders

PMC Specialties Group, Inc.

Salvi Chemical Industries Ltd.

JMC Corporation

Kyung-In Synthetic Corporation

Chemcopia Ingredients Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Heartland Food Products Group acquired Whole Earth Brands' Americas business: The transaction included the Equal artificial sweetener brand, which contained saccharin as a key component, along with Whole Earth, Swerve, and Chuker brands across North America and Latin America. The deal strengthened Heartland's position in the US tabletop sweetener market and consolidated distribution for saccharin-based products alongside its Splenda portfolio.

- March 2026: Blue Jet Healthcare broke ground on a INR 23,000 million (approximately USD 272 million) greenfield facility in Vizag, India: The 102-acre site in Andhra Pradesh was planned to produce contrast media intermediates, high-intensity sweeteners, including saccharin, and multipurpose chemistry products. Phase I involved INR 10,000 million (approximately USD 118 million) and targeted 1,000 KL of additional capacity by July 2027, strengthening Blue Jet's global saccharin supply for pharmaceutical and FMCG customers, including US accounts.

- July 2025: Blue Jet Healthcare approved the first phase of the Vizag manufacturing facility and committed INR 10,000 million in capital expenditure toward capacity additions for sweeteners and pharmaceutical intermediates, strategically pre-positioning the company ahead of the February 2026 groundbreaking.

United States Saccharin Market Report Scope

Saccharin is a zero-calorie, artificial sweetener used to replace sugar in foods and beverages. The United States saccharin market is segmented by product type, form, and application. By product type, the market is segmented into sodium saccharin, calcium saccharin, and insoluble saccharin. By Form, the market is segmented into powder and liquid. By application, the market is segmented into food and beverages, pharmaceuticals, personal care and cosmetics, animal feed, and others. The Market Forecasts are Provided in Terms of Value (USD).

| Sodium Saccharin |

| Calcium Saccharin |

| Insoluble Saccharin |

| Powder |

| Liquid |

| Food and Beverages | Bakery and Confectionery |

| Beverages | |

| Dairy Products | |

| Others | |

| Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Animal Feed | |

| Others |

| By Product Type | Sodium Saccharin | |

| Calcium Saccharin | ||

| Insoluble Saccharin | ||

| By Form | Powder | |

| Liquid | ||

| By Application | Food and Beverages | Bakery and Confectionery |

| Beverages | ||

| Dairy Products | ||

| Others | ||

| Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Animal Feed | ||

| Others | ||

Key Questions Answered in the Report

What is the 2031 outlook for saccharin demand in the United States?

The United States saccharin market is projected to reach USD 174.36 million by 2031 from USD 138.32 million in 2026, which reflects a 4.74% CAGR over 2026-2031.

Which product type currently leads saccharin sales in the country?

Sodium saccharin led with 74.67% share in 2025, supported by long-standing use across food, pharmaceutical, and personal care formulations.

Which form is expected to grow the fastest through 2031?

Powder is both the largest and fastest-growing form, with 82.15% share in 2025 and a projected 5.87% CAGR through 2031.

Why do food and beverages remain the main use case for saccharin?

Food and beverages held 68.73% share in 2025 because saccharin remains widely used in diet beverages, gum, confectionery, bakery products, and tabletop sweeteners.

Page last updated on: