Denmark Renewable Gas From Waste Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

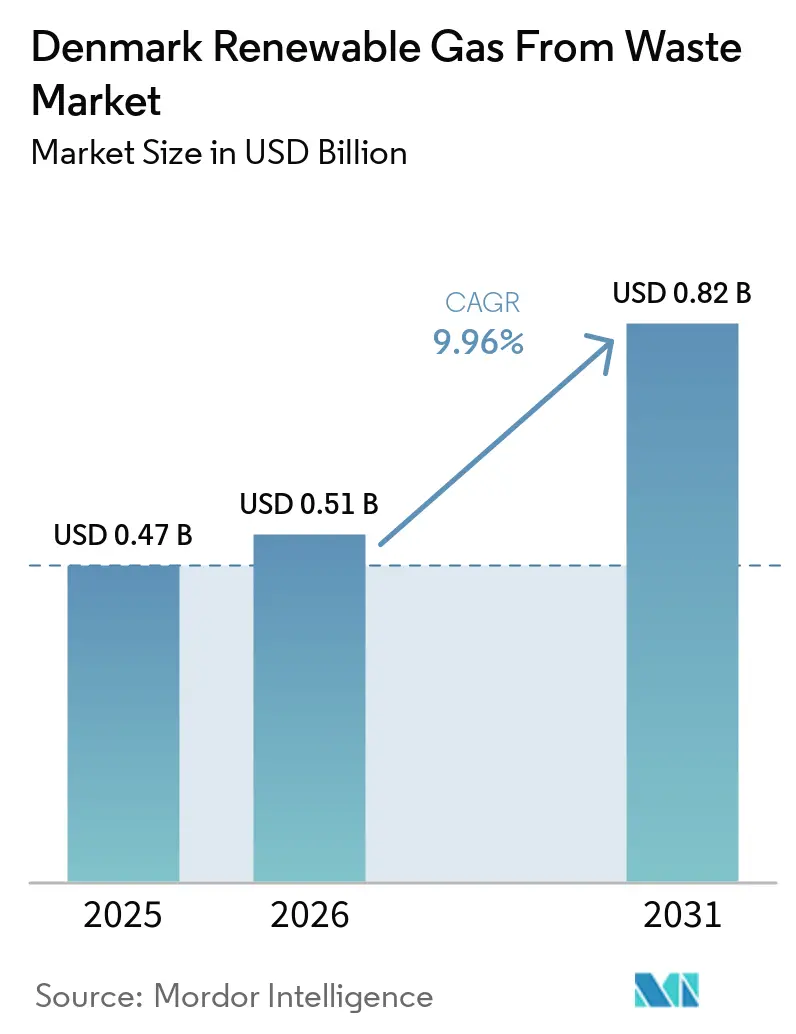

| Base Year Market Size (2025) | USD 0.47 Billion |

| Market Size (2026) | USD 0.51 Billion |

| Market Size (2031) | USD 0.82 Billion |

| Growth Rate (2026 - 2031) | 9.96% CAGR |

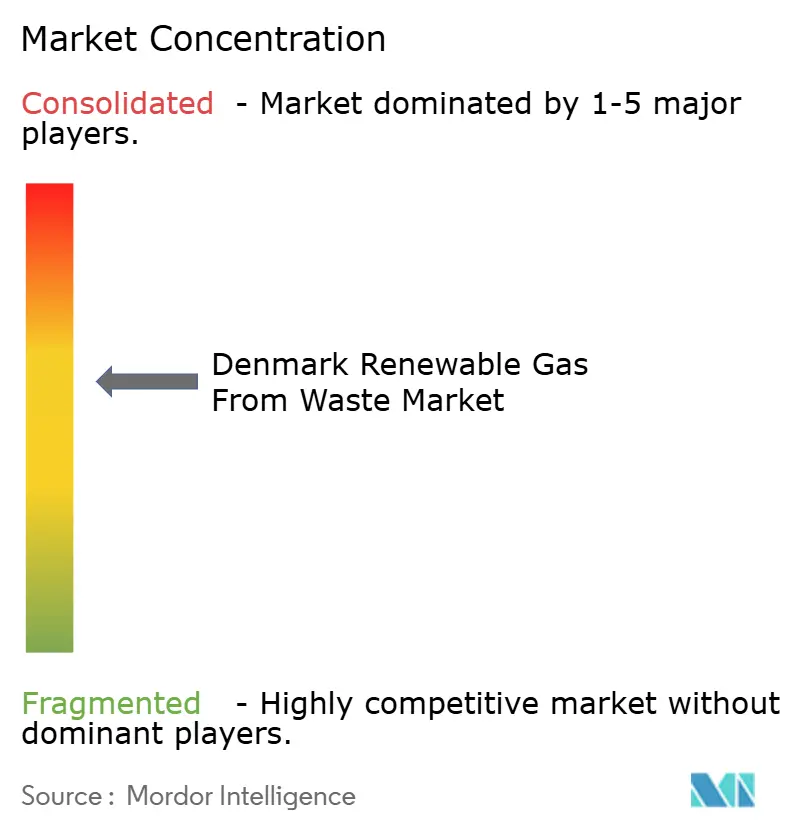

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark Renewable Gas From Waste Market Analysis by Mordor Intelligence

The Denmark Renewable Gas From Waste Market size is expected to increase from USD 0.47 billion in 2025 to USD 0.51 billion in 2026 and reach USD 0.82 billion by 2031, growing at a CAGR of 9.96% over 2026-2031.

Denmark injected 8.3 TWh of biomethane into the gas grid in the October 2024 to September 2025 gas year, up from 8.1 TWh in the previous gas year, confirming continued volume growth even while operating costs remain challenging for some plants. The main drivers behind this expansion are Denmark's ambition to reach 100% green gas by 2032, the European Commission's approval of a EUR 1.7 billion (USD 2.0 billion) support scheme for upgraded biogas and e-methane, and sustained institutional funding for large bioenergy projects. Denmark already sourced more than 40% of its national gas consumption from biogas in 2025, and the Denmark renewable gas from waste market continues to attract institutional and infrastructure investors and support further capacity additions. Feedstock depth from livestock farming and food processing remains a core advantage for the Denmark renewable gas from waste market. However, high biomass input costs and limits on Guarantee of Origin monetization still weigh on smaller operators and slow fully unsubsidized expansion.

Key Report Takeaways

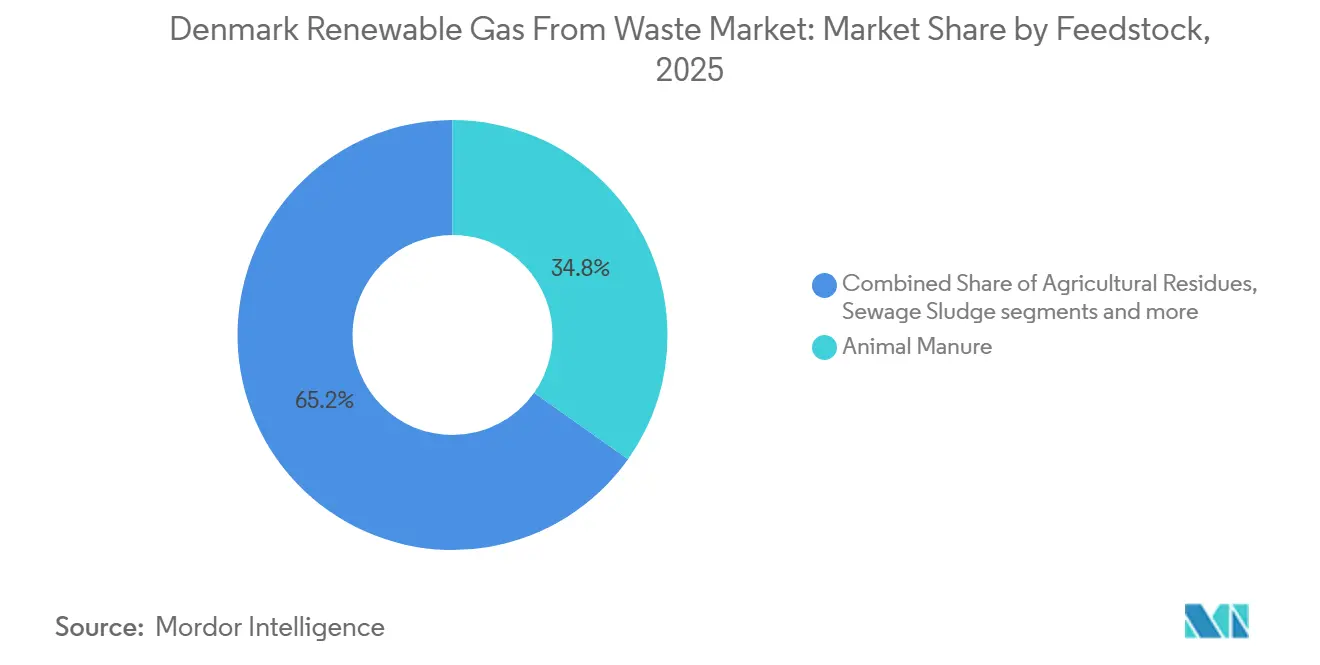

- By feedstock, animal manure led with a 34.80% of the Denmark renewable gas from waste market size in 2025, while food waste is forecast to expand at a 10.70% CAGR through 2031.

- By technology, anaerobic digestion held a 49.20% of the Denmark renewable gas from waste market share in 2025, while biogas upgrading systems recorded the highest projected CAGR at 12.80% through 2031.

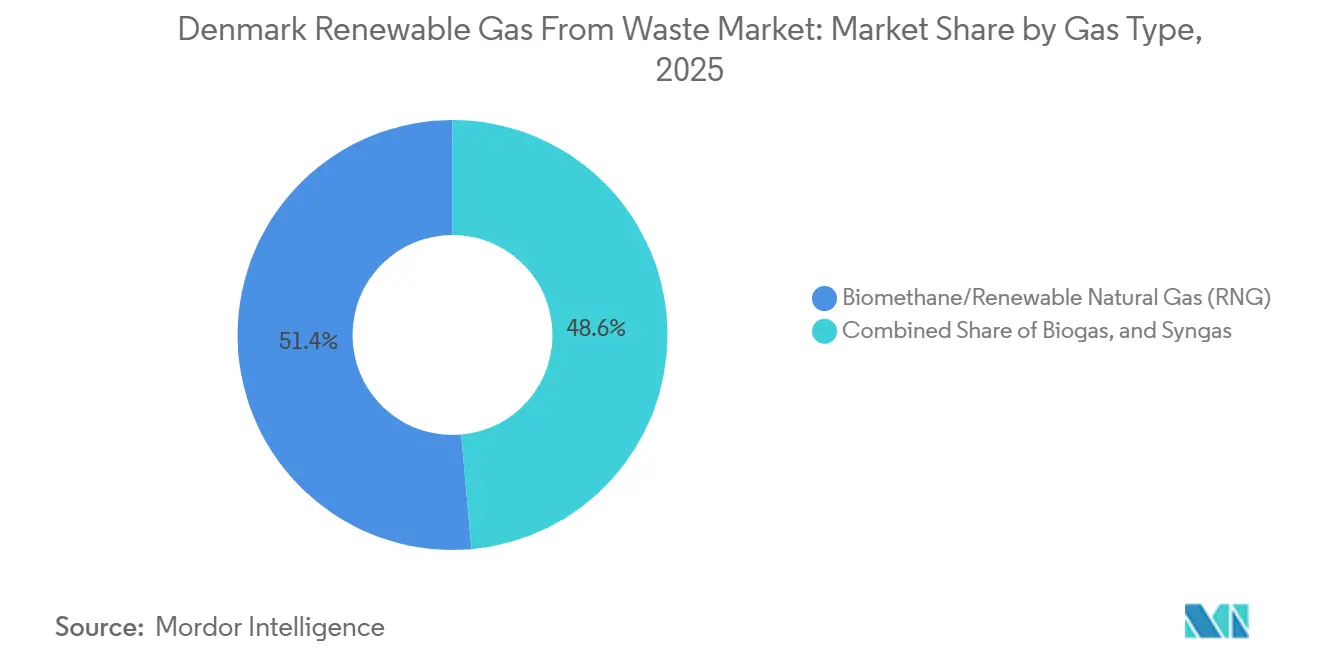

- By gas type, biomethane/renewable natural gas (RNG) accounted for 51.4% of the Denmark renewable gas from waste market share in 2025 and is projected to grow at a 12.5% CAGR through 2031.

- By application, grid injection captured a 35.60% share in 2025, while transportation fuel is projected to grow at a 12.20% CAGR through 2031.

- By component, gas processing and upgrading units held a 34.50% share in 2025, while monitoring and control systems are forecast to grow at a 11.40% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Denmark Renewable Gas From Waste Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copenhagen Infrastructure Partners Funding Danish Biomethane Projects | +2.5% | National, concentrated in Jutland and Lolland-Falster | Medium term (2-4 years) |

| European Union Approved State Support Scheme for Renewable Gas Grid Injection | +2.1% | National, with grid connection hubs across Jutland and Zealand | Medium term (2-4 years) |

| Biomethane Covering Over 40% of Danish Gas Consumption in 2025 | +1.6% | National | Short term (≤ 2 years) |

| 100% Green Gas Ambition by 2032 Supporting Long-Term Investment | +1.2% | National | Long term (≥ 4 years) |

| Strong Agricultural and Food Waste Base Supporting Feedstock Supply | +0.9% | National, dominant in Western and Southern Jutland | Short term (≤ 2 years) |

| Maize Silage Ban Redirecting Demand Toward Organic Waste Feedstock | +0.6% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Copenhagen Infrastructure Partners Funding Danish Biomethane Projects

Institutional capital is changing how the Danish renewable gas from waste market is financed and developed. Copenhagen Infrastructure Partners backed Sindal Biogas in Northern Jutland in May 2024. They committed to expanding the plant to process 500,000 tonnes of biomass annually, with planned production of up to 34 million cubic meters of upgraded biogas for injection into the grid. In May 2026, the European Investment Fund committed EUR 200 million (USD 235.3 million) to CIP’s Advanced Bioenergy Fund II, which has a target size of EUR 1.5 billion (USD 1.8 billion) and is intended to scale industrial biogas projects across Europe. In the Denmark renewable gas from waste market, this type of capital raises expectations for project size, offtake quality, engineering discipline, and emissions accounting. It also increases the likelihood that smaller, less efficient plants will have to consolidate, upgrade, or exit as the Danish renewable gas from waste market shifts toward larger, better-capitalized assets.

European Union Approved State Support Scheme for Renewable Gas Grid Injection

The Denmark renewable gas from waste market received a major policy signal when the European Commission approved Denmark’s EUR 1.7 billion (USD 2.0 billion) state aid scheme on December 16, 2024.[1]European Commission, “Commission Approves EUR 1.7 Billion Danish Aid for Renewable Gas Production,” European Commission, ec.europa.eu The scheme covers five bidding rounds from 2024 to 2030, and supports the upgrade of biogas and e-methane for grid injection over 20 years, materially improving project bankability. It is expected to support 7.9 PJ of renewable gas production per year and reduce greenhouse gas emissions by 450,000 tonnes of CO2 annually from 2033. Because support is tied to competitive bidding and sustainability rules under RED II and RED III, the Denmark renewable gas from waste market is being pushed toward cleaner feedstock choices and stronger documentation standards at the same time. The effect extends beyond producers because upgrading system suppliers, compressor vendors, metering specialists, and monitoring providers can now plan their sales cycles around a clearer procurement pipeline in Denmark.

Biomethane Covering Over 40% of Danish Gas Consumption in 2025

Biogas accounted for more than 40% of Denmark’s gas consumption in 2025, placing the country at the top of Europe on this metric and giving Denmark renewable gas from waste market unusual visibility relative to its small population.[2]Biogas Danmark, “Biogas Dækker Over 40 Procent Af Danmarks Gasforbrug,” Biogas Danmark, biogas.dk This milestone matters because it shows that renewable gas is no longer a pilot pathway in Denmark, but a material part of the energy system. ENTSOG’s 2026 reporting also showed 8.3 TWh of renewable gas injections in the October 2024 to September 2025 gas year, confirming that the installed base continues to deliver measurable volumes. A higher substitution rate also changes competition within the Denmark renewable gas from waste market because future advantage will depend less on simply adding output and more on flexibility, dispatchability, traceability, and carbon performance. That is important in a country where total gas demand is expected to decline over time, making market positioning more sensitive to operational quality than to volume alone.[3]IEA Bioenergy, “Country Report Denmark 2024,” IEA Bioenergy Task 37, ieabioenergy.com

100% Green Gas Ambition by 2032 Driving Sustained Large-Scale Biomethane Investment

Long-range climate policy remains one of the clearest supports for the Denmark renewable gas from waste market. Denmark’s Climate Agreement for Energy and Industry 2020 established that support for biogas and other green gases should be awarded through competitive bids over 20-year periods. Denmark’s Climate Act also made a 70% reduction in greenhouse gas emissions by 2030, relative to 1990 levels, legally binding, tying gas decarbonization to a statutory obligation rather than a voluntary target. The target for full green gas coverage moved from 2030 to 2032, but the shift did not remove the core demand signal for new capacity and grid integration. The IEA (International Energy Agency Bioenergy country report projects Danish biogas and biomethane production of 14-15 TWh by 2030 and 17 TWh by 2035, indicating that the Denmark renewable gas from waste market still requires steady capacity additions over a long period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green Gas Target Pushed Back from 2030 to 2032 | -1.1% | National | Long term (≥ 4 years) |

| Tender Subsidies Limiting Guarantee of Origin Sales | -0.8% | National, greater impact on export-oriented plants in Jutland | Medium term (2-4 years) |

| No Domestic CO2 Tax Refund Mechanism for Grid-Injected Biogas | -0.5% | National | Short term (≤ 2 years) |

| Rising Feedstock Costs and Regulatory Uncertainty Slowing New Approvals | -0.3% | National, spillover to related partner hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Green Gas Target Pushed Back from 2030 to 2032

The Denmark renewable gas from waste market has continued to grow, but the pace has not been strong enough to preserve the original 2030 target for full green gas coverage. Danish Energy Agency projections and Biogas Danmark’s outlook both showed that production growth had flattened after 2022 and that the 100% milestone would move to 2032 under current conditions. Shell Biogas A/S reported a loss of DKK 700 million (USD 110.25 million) in 2025 on revenue of DKK 830 million (USD 130.7 million), underscoring the difficulty of achieving profitability even for a large operator. This matters in the Denmark renewable gas from waste market because weaker margins reduce the willingness of smaller developers to move forward without visible support, which, in turn, slows the pipeline needed to meet the revised 2032 target. At the same time, Denmark remains one of Europe's most mature biogas markets, with strong policy commitments to decarbonize the gas grid and reduce dependence on fossil natural gas. The need to close the gap between current production levels and long-term renewable gas ambitions is expected to drive additional investments in feedstock utilization, plant efficiency improvements, and capacity expansion projects across the country.

Tender Subsidies Incompatible with Guarantee of Origin Sales

A second major restraint in the Denmark renewable gas from waste market is the interaction between production support and guarantee of origin sales. Energinet’s guidelines and the Danish Energy Agency’s bidding conditions state that producers receiving a price premium under the tender scheme cannot also receive GoOs for those same subsidized volumes unless they renounce the premium for the relevant production quantity. This is commercially important because 70.2% of Danish GoOs for network-delivered biogas were bought by foreign companies in 2024, especially in Sweden and Germany, showing that the export market already matters for revenue formation. At the same time, the Oxford Institute for Energy Studies reported that European biomethane production costs had not fallen materially since the late 2010s and that median operating costs rose by 6% from 2022 to 2023. In the Denmark renewable gas from waste market, this means GoO income is not just an additional benefit, but a meaningful part of revenue stacking for many projects. When subsidy rules limit access to that value, project economics become harder to close, especially for new entrants that lack the scale or integration advantages of larger operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Manure Anchors Supply as Waste Streams Gain Ground

Animal manure accounted for the largest share of feedstock at 34.80% in 2025, reflecting Denmark’s very dense cattle and pig farming base and the long-standing link between farm waste management and anaerobic digestion. In the Denmark renewable gas from waste market, manure remains the most reliable, low-cost stream because it is available in large volumes and aligns well with digestate recycling back to farmland. That circular structure matters because it supports gas production while also reducing pressure on synthetic fertilizer use and helping farms manage nutrient handling. Food waste is expected to grow the fastest, at a 10.70% CAGR through 2031, as household sorting systems, municipal collection programs, and industrial food waste treatment channels become more mature. Agricultural residues, industrial organic waste, sewage sludge, and other biodegradable streams are gaining relevance for various reasons, including local regulations, treatment costs, and collection efficiency.

A key shift in this segment is the phaseout of maize silage as an eligible energy crop from August 2025, which pushes Denmark renewable gas from the waste industry closer to genuinely waste-based production. This is important because it changes feedstock demand not by shrinking the whole resource base, but by redirecting it toward manure, straw, food residues, and other biodegradable waste. According to the international energy agency (IEA) Bioenergy country report, Denmark's domestic bioresources, such as manure, straw, and biodegradable waste, are projected to exceed the anticipated production range of 14-15 TWh by 2030. That gap shows that availability is not the main bottleneck for the Denmark renewable gas from waste market. The stronger constraint is how quickly plants can secure, pre-treat, contract, and finance more complex waste streams while meeting sustainability rules under the European Union framework.

By Technology: Anaerobic Digestion Dominates While Upgrading Systems Accelerate

Anaerobic digestion held the largest share of 49.20% of the technology market in 2025 and remains the operational backbone of the Denmark renewable gas from waste market. Denmark has spent decades building a large agricultural biogas base, so most existing assets, operator knowledge, and feedstock logistics are still organized around AD. The IEA Bioenergy country report noted that nearly 80% of Danish biogas output was being upgraded and injected into the gas grid by 2022, indicating how far the technology base has already shifted away from electricity-led CHP use. That installed base gives the Denmark renewable gas from waste market a practical advantage, as developers do not need to build an entirely new system from scratch. They are increasingly upgrading and repurposing plants that already have access to feedstock, operating history, and local acceptance.

Biogas upgrading systems are expected to be the fastest-growing technology category, with a 1.80% CAGR through 2031, as the remaining Combined Heat & Power (CHP)-oriented plants continue to convert, and new large plants are designed for grid-quality output from the start. This shift is reinforced by support design, as Denmark’s current tender framework favors renewable gas injected into the network rather than electricity generation from raw biogas. Landfill gas recovery remains active but is strategically scaled back because Denmark’s waste system diverts much more organic material from landfills than other markets do. Gasification and pyrolysis are still emerging, yet they are attracting attention in niche areas such as sludge and difficult organic residues. GreenLab Skive is developing a full-scale microwave-based pyrolysis plant intended to process sewage sludge and organic waste into green fuel and biochar by 2027, which shows where the next layer of technology diversification may come from.

By Gas Type: Biomethane / Renewable Natural Gas (RNG) Lead the Revenue Base and Growth Outlook

Biomethane/renewable natural gas (RNG) accounted for 51.4% of the Denmark renewable gas from waste market share in 2025 and is projected to expand at a 12.5% CAGR through 2031. This confirms that upgraded renewable gas remains the core commercial product in the market. Its leading position reflects Denmark’s long-standing focus on grid injection and the practical advantage of using existing gas network infrastructure. Biomethane and RNG also benefit from better compatibility with industrial users, transport applications, and long-term offtake structures than less mature gaseous alternatives. In the Denmark renewable gas from waste market, this gives the segment a stronger revenue profile and a clearer path for capacity additions over the forecast period.

The segment’s momentum is also linked to rising demand from heavy transport and other end uses that require low-carbon drop-in fuels. As more plants shift from raw biogas output toward upgraded gas, the commercial center of the market continues to move toward biomethane and RNG. This is strengthening investment in upgrading systems, gas quality control, and injection-linked infrastructure across the value chain. Biogas remains relevant where on-site energy use continues, but its role is becoming smaller in proportional terms as upgraded gas captures more of the Denmark renewable gas from waste market size. Syngas remains limited to a much smaller base, with growth still tied to early-stage project development rather than broad commercial deployment.

By Application: Grid Injection Leads While Transportation Fuel Draws Fastest Growth

Grid injection held the largest share in 2025 at 35.60% and remains the core outlet for the Denmark renewable gas from waste market. This reflects a deliberate policy design, as Denmark has spent years favoring network-connected biomethane over isolated heat and power uses. The transmission role of Energinet and the distribution role of Evida make the system wide enough for producers to reach domestic users and cross-border markets without building private delivery infrastructure. For the Denmark renewable gas from waste market, network access is a structural strength because it expands the buyer pool and supports long-term offtake planning. It also helps explain why electricity generation and CHP are no longer the center of commercial value creation.

Transportation fuel is expected to be the fastest-growing application through 2031, registering a 12.20% CAGR, as freight and maritime users seek lower-carbon fuels that can be deployed in existing gas-based equipment. This growth path matters because it gives the Denmark renewable gas from waste market a second demand engine beyond basic grid substitution. Industrial heating is also becoming increasingly relevant as companies seek to reduce their use of fossil gas under tighter emissions rules. However, pricing and tax design can still limit faster take-up in some cases. Residential and commercial heating is growing more slowly because it depends mainly on biomethane blended into the grid rather than on dedicated retail structures. The direction is clear, however, because the Denmark renewable gas from waste market is moving toward applications that value traceable low-carbon gas and are willing to sign longer offtake agreements.

By Component: Gas Processing Units Dominate as Monitoring Systems Become More Important

Gas processing and upgrading units held the largest component position in 2025 at 35.40% because they are the essential conversion step between raw biogas and pipeline-quality biomethane. In the Denmark renewable gas from waste market, this equipment accounts for a large share of project capex because producers need reliable purification, compression, and quality control to meet network specifications. Investment has been concentrated in upgrading platforms such as membrane separation and pressure swing adsorption, both of which have become central to grid-injection projects. That pattern is unlikely to reverse because the Denmark renewable gas from waste market is still converting older plants and building new ones to upgrade gas output. As a result, the most capital-intensive part of the supply chain remains concentrated in systems that clean, standardize, and meter gas rather than in systems built only for local heat or power use.

Monitoring and control systems are expected to be the fastest-growing component category, registering 11.40% CAGR through 2031, as compliance, efficiency, and traceability requirements increase. Operators now place greater value on real-time data on feedstock quality, fermentation performance, grid injection metering, and emissions documentation than they did when plants primarily produced on-site energy. This is especially important in the Denmark renewable gas from waste market because subsidy eligibility, methane management, and Guarantee of Origin (GoO) documentation all depend on better operational records. Digesters and fermentation systems remain large spending items, but they are more mature and standardized than the digital and analytical layer being added to plants. Compressors, storage equipment, and liquefaction-linked assets also matter, though recent setbacks in the bioLNG chain show that downstream commercialization still depends heavily on certificate values and fuel pricing.

Geography Analysis

The Denmark renewable gas from waste market operates within a single national framework, but plant capacity is unevenly distributed across the country. Western and Southern Jutland form the main production cluster because these areas combine dense livestock farming, available land, and strong access to the gas network. That concentration gives the Denmark renewable gas from waste market a clear agricultural anchor, with manure-based feedstock chains operating at a scale hard for many other European markets to match. Sindal Biogas in Northern Jutland illustrates this pattern because CIP committed to expanding the plant to process 500,000 tonnes of biomass annually and produce up to 34 million cubic meters of upgraded biogas for grid injection. In practical terms, Jutland’s advantage comes from the close fit between feedstock supply, land availability, and proximity to transmission infrastructure.

Zealand, Lolland, and Funen have a different profile within the Denmark renewable gas from waste market, as industrial organic waste and food processing residues play a larger role there. Shell Biogas A/S’s Abed facility on Lolland is designed to process 400,000 tonnes of biomass annually, including 100,000 tonnes of beet pulp from Nordic Sugar, and produce around 20 million cubic meters of biomethane for the Danish grid. This shows that geography is not only about where manure is abundant, but also about where industrial residue streams can be aggregated efficiently. It also means the Denmark renewable gas from waste market is not dependent on one single feedstock geography, even if Jutland remains the main cluster. Instead, regional specialization is emerging around different waste streams and plant types.

Denmark’s national performance is strong even by European standards. ENTSOG (European Network of Transmission System Operators for Gas) reported 8.3 TWh of biomethane injections into the Danish gas network during the October 2024 to September 2025 gas year, placing Denmark behind only the very largest producers in absolute terms while keeping its per-capita output among the highest in Europe. The IEA’s Renewables 2025 report ranked Denmark among the top five European biomethane producers, alongside Germany, France, Italy, and the Netherlands. This standing supports the Denmark renewable gas from waste market by giving Danish operators credibility in cross-border certificate trading and low-carbon fuel markets. It also shows that future growth will depend less on proving the concept and more on finding new waste streams, improving plant economics, and raising utilization of residues such as straw.

Competitive Landscape

The Denmark renewable gas from waste market is moderately concentrated. Shell Biogas A/S is the largest single operator in Denmark, with 13 plants. Yet, the national base also includes more than 60 grid-connected biogas plants spread across farmer-owned cooperatives, regional operators, and institutionally backed platforms. This structure means that scale matters, but feedstock access, local contracting strength, and grid position remain equally important in day-to-day competition. The Denmark renewable gas from waste market is therefore shaped by both large multi-plant portfolios and smaller operators that are deeply embedded in regional manure and waste collection networks.

Shell remains an important participant due to its plant portfolio, its September 2025 integration of Nature Energy into Shell Low Carbon Solutions Biogas, and the start of gas deliveries from a new Denmark facility in the same period. At the same time, Shell Biogas A/S reported a DKK 697 million (USD 109.8 million) loss in 2025 despite revenue rising to DKK 830 million (USD 130.7 million), which shows that scale alone does not protect operators from weak gas prices, lower certificate values, and high biomass input costs. Institutional capital is also becoming a stronger competitive force, with Copenhagen Infrastructure Partners expanding its Denmark biomethane platform through the Sindal Biogas acquisition and capacity expansion, while also extending its bioenergy investment pipeline through ABF II. This is raising the minimum efficient scale for new projects and increasing pressure on undercapitalized plants. The competitive field is also supported by technology and processing specialists, including companies involved in system upgrades, plant engineering, and feedstock pretreatment, which are becoming increasingly important as projects move toward larger, more complex waste-based configurations.

Strategic differentiation in the Denmark renewable gas from waste market is increasingly built around feedstock security, upgrading efficiency, methane management, and the ability to secure stable revenues from grid injection and environmental attributes. GreenLab Skive Biogas demonstrated this adaptive approach in 2025 by broadening its feedstock base to include locally sourced grass seed straw, following the tightening of the maize silage ban, which reduced input options. Regional plants continue to matter because they are often closer to manure, food waste, and agricultural residue streams than the largest national portfolios. As a result, the Denmark renewable gas from waste market is not defined by a single company, but by the interaction among large portfolio operators, institutional investors, regional biogas producers, and technology-led waste-processing participants.

Denmark Renewable Gas From Waste Industry Leaders

Shell Low Carbon Solutions Biogas

BioCirc Group

Bigadan A/S

Tønder Biogas A/S

Gemidan Ecogi A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Shell completed the full integration and rebranding of Nature Energy under the Shell Low Carbon Solutions Biogas umbrella, and now operates 13 biogas plants in Denmark. In the same month, the company delivered first gas molecules from organic waste and residues to the Danish grid from a new facility.

- August 2025: The full prohibition on maize silage as a biogas input energy crop entered into force in Denmark, as mandated by the Climate Agreement on Energy and Industry 2020 and implemented progressively since 2021. The Danish Energy Agency confirmed the energy crop limit for all biogas plants is set at 4% by weight, with maize classified as non-eligible from the 2025/26 reporting period.

Denmark Renewable Gas From Waste Market Report Scope

The Denmark Renewable Gas From Waste Market is Segmented by Feedstock (Municipal Solid Waste, Food Waste, and More), by Technology (Anaerobic Digestion, Gasification, Pyrolysis, and More), by Gas Type (Biogas, Syngas, and More), by Application (Electricity Generation, Grid Injection, and More), and by Component (Gas Collection, Digesters & Fermentation, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Municipal Solid Waste (MSW) |

| Agricultural Residues |

| Animal Manure |

| Industrial Organic Waste |

| Sewage Sludge |

| Food Waste |

| Others |

| Anaerobic Digestion |

| Landfill Gas Recovery |

| Gasification |

| Pyrolysis |

| Biogas Upgrading Systems |

| Others |

| Biogas |

| Biomethane/Renewable Natural Gas (RNG) |

| Syngas |

| Electricity Generation |

| Combined Heat & Power (CHP) |

| Grid Injection |

| Transportation Fuel |

| Industrial Heating |

| Residential & Commercial Heating |

| Others |

| Gas Collection Systems |

| Digesters & Fermentation Systems |

| Gas Processing & Upgrading Units |

| Compressors & Storage Systems |

| Power Generation Equipment |

| Monitoring & Control Systems |

| Others |

| By Feedstock | Municipal Solid Waste (MSW) |

| Agricultural Residues | |

| Animal Manure | |

| Industrial Organic Waste | |

| Sewage Sludge | |

| Food Waste | |

| Others | |

| By Technology | Anaerobic Digestion |

| Landfill Gas Recovery | |

| Gasification | |

| Pyrolysis | |

| Biogas Upgrading Systems | |

| Others | |

| By Gas Type | Biogas |

| Biomethane/Renewable Natural Gas (RNG) | |

| Syngas | |

| By Application | Electricity Generation |

| Combined Heat & Power (CHP) | |

| Grid Injection | |

| Transportation Fuel | |

| Industrial Heating | |

| Residential & Commercial Heating | |

| Others | |

| By Component | Gas Collection Systems |

| Digesters & Fermentation Systems | |

| Gas Processing & Upgrading Units | |

| Compressors & Storage Systems | |

| Power Generation Equipment | |

| Monitoring & Control Systems | |

| Others |

Key Questions Answered in the Report

What is the projected value of Denmark renewable gas from waste by 2031?

It is forecast to reach USD 0.82 billion by 2031, rising from USD 0.51 billion in 2026 at a 9.96% CAGR.

What is driving growth in Denmark’s renewable gas from waste space?

The main supports are the 100% green gas ambition by 2032, the EU-approved EUR 1.7 billion support scheme, strong feedstock availability, and continued institutional investment.

Which feedstock is most important in Denmark?

Animal manure remains the leading feedstock because Denmark has a dense livestock sector and a mature manure-to-digestion model.

Why is transportation fuel becoming more important?

Freight and maritime users are adopting renewable gaseous fuels more actively, which is making transportation fuel the fastest-growing application through 2031.

Who is the leading company in Denmark’s renewable gas from waste field?

Shell Biogas A/S is the largest operator by fleet size in Denmark, with 13 plants, although the wider field remains fragmented across many other operators.

What is the biggest commercial challenge for new projects?

A major issue is that subsidized production cannot fully monetize Guarantee of Origin sales at the same time, which weakens revenue stacking for some projects.

Page last updated on: