Europe Industrial Waste Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

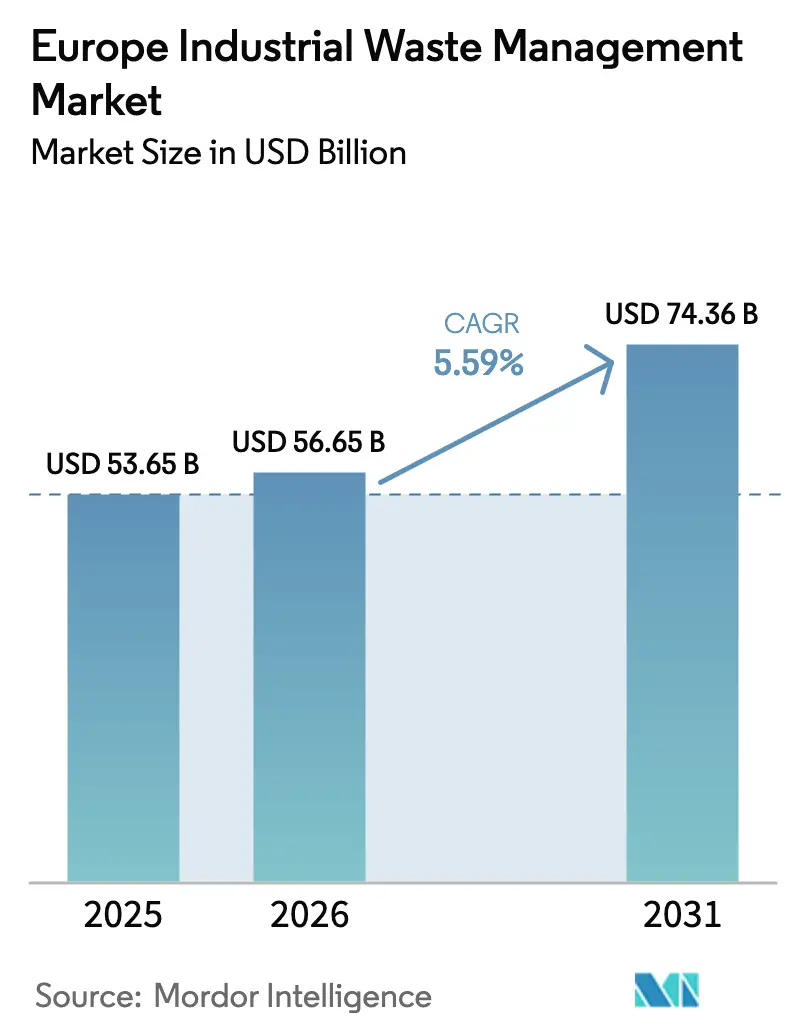

| Base Year Market Size (2025) | USD 53.65 Billion |

| Market Size (2026) | USD 56.65 Billion |

| Market Size (2031) | USD 74.36 Billion |

| Growth Rate (2026 - 2031) | 5.59% CAGR |

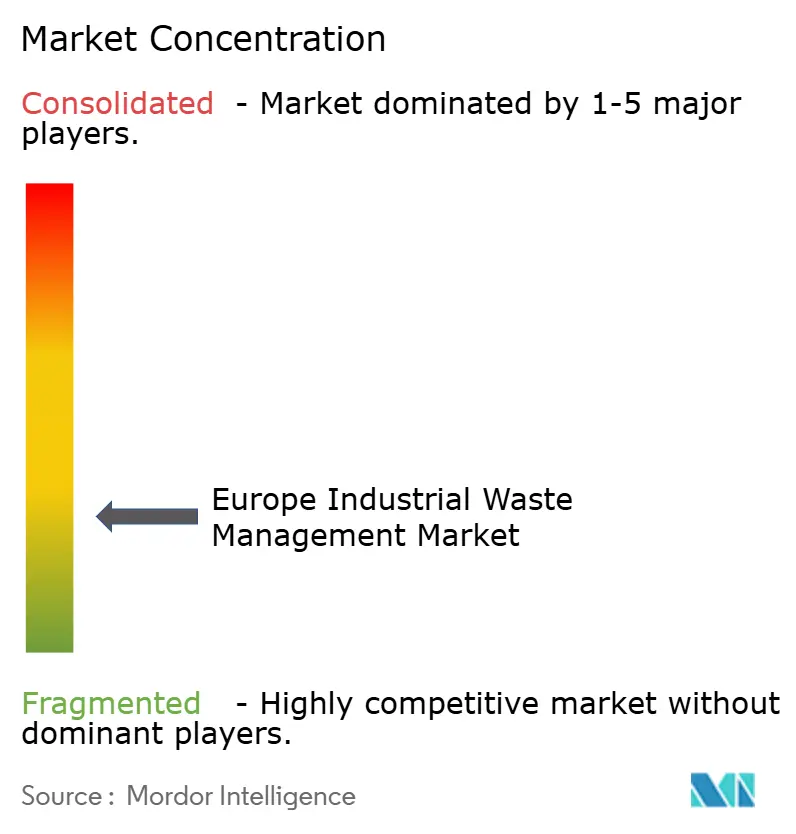

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Industrial Waste Management Market Analysis by Mordor Intelligence

The European Industrial Waste Management Market size in 2026 is estimated at USD 56.65 billion, growing from 2025 value of USD 53.65 billion with 2031 projections showing USD 74.36 billion, growing at 5.59% CAGR over 2026-2031. This healthy trajectory reflects the region’s rapid transition toward a circular economy, propelled by tight EU regulations, rising industrial output, and persistent investor scrutiny of environmental performance. Hazardous waste volumes are climbing 2.25% each year, while non-hazardous streams are shifting toward higher-value recovery routes. Recycling infrastructure, digital tracking mandates, and industrial symbiosis initiatives are enabling operators to capture larger portions of secondary raw-material demand, especially for electric-vehicle battery inputs. Strategic acquisitions worth more than USD 11 billion in 2024 alone signal accelerated consolidation as players seek scale, technology, and geographic reach. Lingering pressure points, including labor shortages in Eastern Europe, volatile recycled-material prices, and uneven enforcement of EU rules, continue to shape investment and operating decisions across the European industrial waste management market[1]European Commission, “Digital Waste Shipment System (DIWASS) Factsheet,” ec.europa.eu.

Key Report Takeaways

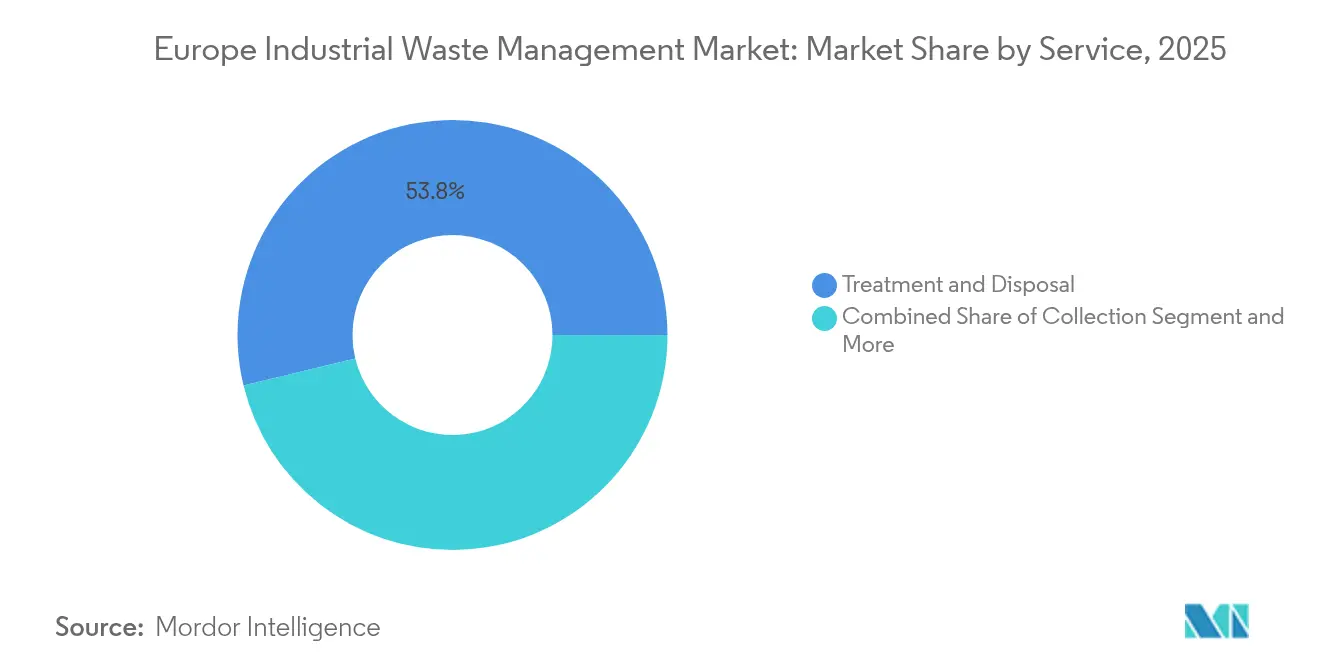

- By service, Treatment & Disposal led with 53.78% of the European industrial waste management market share in 2025; Recycling & Material Recovery is advancing at a 6.72% CAGR through 2031.

- By disposal method, Landfill accounted for a 44.32% share of the European industrial waste management market size in 2025, while Incineration & Energy Recovery is forecast to expand at a 7.31% CAGR to 2031.

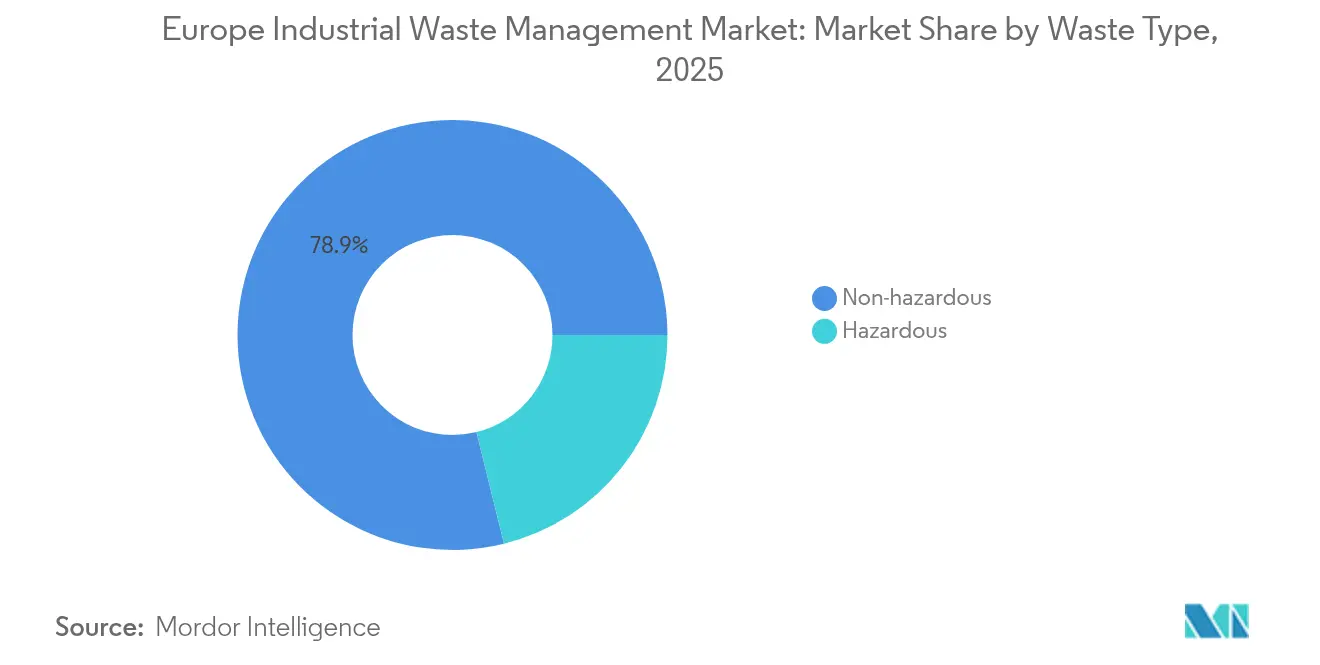

- By waste type, Non-hazardous waste held 78.85% of the European industrial waste management market share in 2025, and Hazardous waste is progressing at a 5.15% CAGR over the same horizon.

- By industry, Construction Materials captured 31.95% of the European industrial waste management market size in 2025; Electrical & Electronics exhibits the fastest growth at an 7.96% CAGR through 2031.

- By geography, Germany commanded 23.12% of the European industrial waste management market in 2025, whereas the Rest-of-Europe bloc shows the strongest expansion at a 7.12% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple regions, with Europe forming one of the important contributors. Mordor Intelligence's global industrial waste management market size report represents that cumulative total.

Europe Industrial Waste Management Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU waste-management directives | 1.8% | EU-wide, with enforcement variations across Eastern Europe | Long term (≥ 4 years) |

| Increasing industrial waste generation volumes | 1.2% | Global, with highest impact in Germany, Netherlands, Belgium | Medium term (2-4 years) |

| Demand for secondary raw materials in EV battery supply chains | 1.1% | Germany, France, Poland, Hungary automotive corridors | Medium term (2-4 years) |

| Growing corporate sustainability & ESG pressure | 0.9% | Western Europe core, expanding to Central & Eastern Europe | Medium term (2-4 years) |

| Digital tracking & blockchain for waste traceability | 0.7% | NORDICS and BENELUX leading, gradual EU adoption | Short term (≤ 2 years) |

| Industrial symbiosis parks for waste-to-input exchange | 0.6% | Germany, Netherlands, Denmark with spillover to neighboring regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent EU Waste Management Directives

New EU rules create a decisive pull toward higher recovery rates and full traceability. The Packaging and Packaging Waste Regulation, effective February 2025, requires all packaging to be recyclable by 2030 and sets a 15% reuse mandate by 2040. The updated Waste Framework Directive tightens extended-producer-responsibility schemes and standardizes classification codes to ease cross-border movements. Meanwhile, the Waste Shipments Regulation bans exports of plastic waste to non-OECD states from November 2026 and enforces digital tracking via the DIWASS system. These laws push industrial generators to partner with certified providers capable of meeting stringent targets, which directly expands high-value segments such as recycling, energy recovery, and hazardous-waste neutralization. Although enforcement still varies across member states, the cumulative regulatory push adds 1.8 percentage points to the forecast CAGR of the European industrial waste management market.

Increasing Industrial Waste Generation Volumes

Europe’s factories, chemical parks, and construction sites continue to produce larger waste streams as output grows and product cycles shorten. Hazardous waste climbed 2.25% per year between 2010 and 2024, with chemical and petrochemical hubs in Germany’s Rhine-Ruhr region and the Netherlands generating the bulk of complex by-products requiring specialized treatment. Construction-material manufacturing alone discharges close to 400 million tonnes of largely non-hazardous debris annually, reinforcing demand for advanced sorting and recovery services. Electronics producers amplify the trend by releasing difficult-to-process miniaturized components rich in rare earth elements and precious metals. Although the Industrial Emissions Directive obliges plants to adopt best available techniques for waste minimization, the build-out of battery and renewable-energy supply chains offsets reduction gains. Overall, greater industrial output directly fuels volume growth in the European industrial waste management market, prompting operators to expand capacity, upgrade technology, and refine logistics networks.

Demand for Secondary Raw Materials in EV Battery Supply Chains

Surging electric-vehicle production triggers appetite for recycled lithium, cobalt, and nickel. Battery-grade materials sourced from waste streams can cut carbon footprints and hedge against volatile commodity prices. Germany, France, and BENELUX dominate early-stage demand as cell-making plants scale up, while Eastern Europe begins to follow. Dedicated recovery facilities emerge next to gigafactories, enabling short supply loops that align with extended-producer-responsibility mandates and cut logistics costs. Operators with hydrometallurgical or pyrometallurgical expertise are poised to capture premium margins, adding 0.6 percentage points to the CAGR of the European industrial waste management market.

Growing Corporate Sustainability & ESG Pressure

Industrial clients face unprecedented scrutiny from investors, regulators, and customers who demand evidence of circular practices. Under the Corporate Sustainability Reporting Directive, firms must disclose granular waste generation and treatment data, motivating them to outsource to providers that guarantee 95% diversion or better. Veolia’s GreenUP program, backed by USD 2.18 billion (EUR 2 billion) through 2027, exemplifies how service providers invest to meet stringent ESG goals. In parallel, automakers and electronics brands impose closed-loop sourcing requirements on suppliers, thus stimulating demand for secondary materials and certified treatment channels. Carbon-accounting frameworks now include Scope 3 emissions from waste handling, rewarding low-carbon solutions such as anaerobic digestion over incineration. Together, these forces elevate contract values, accelerate the adoption of advanced technologies, and reinforce the growth outlook for the European industrial waste management market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for advanced treatment facilities | -1.4% | EU-wide, particularly acute in Eastern Europe | Medium term (2-4 years) |

| Skilled-labour shortage in Eastern Europe | -1.1% | Poland, Czech Republic, Slovakia, Hungary | Short term (≤ 2 years) |

| Fragmented regulatory enforcement across EU | -0.8% | Eastern Europe primary, with compliance gaps in Southern Europe | Long term (≥ 4 years) |

| Volatile prices for recycled industrial materials | -0.6% | Global impact with regional variations in commodity exposure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for Advanced Treatment Facilities

Building state-of-the-art recycling or waste-to-energy assets is capital-intensive. A typical plant costs USD 4-10 million per MW, while advanced recycling installations run USD 54-218 million (EUR 50-200 million) depending on scale. LyondellBasell’s German chemical-recycling project secured USD 43.6 million (EUR 40 million) in EU funding, and CIRCTEC raised USD 163.5 million (EUR 150 million) for Europe’s largest tire-pyrolysis unit. Carbon-capture retrofits add USD 109-164 per tonne of CO₂ capacity. Eastern Europe struggles to mobilize such funding because local financiers view waste assets as higher-risk, slowing deployment, and shaving 0.8 percentage points off the European industrial waste management market growth rate[2]European Investment Bank, “Financing the Circular Economy 2024,” eib.org.

Skilled-Labor Shortage in Eastern Europe

Czech Republic logged more than 215,000 open technical positions in 2024, and wage inflation in waste services runs 10-20% annually across Poland, Slovakia, and Hungary. Operators accelerate automation, but robotics cannot fully replace certified technicians needed for hazardous-waste handling. Installation of AI systems rises, yet maintenance demands specialized staff still in short supply. As a result, operating costs swell and capacity expansions stall, clipping 1.1 percentage points from the European industrial waste management market’s CAGR in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Treatment & Disposal Retains Primacy as Recycling Surges

Treatment & Disposal accounted for 53.78% of the European industrial waste management market share in 2025, cementing its role as the backbone of hazardous-waste neutralization and legacy infrastructure. This dominance stems from significant sunk investment in incinerators, physicochemical plants, and secure landfills that serve Germany, the Netherlands, and Belgium. Large chemical clusters rely on these facilities to comply with EU directives that forbid untreated hazardous output. Steady upgrades such as flue-gas cleaning and carbon-capture units maintain regulatory conformity and underpin stable cash flows. Collection and logistics services, though smaller, benefit from rising volume and specialized transport mandates for toxic streams. Digital route optimization and the impending DIWASS platform streamline cross-border documentation and elevate service value across the European industrial waste management market.

Recycling & Material Recovery is the fastest-growing service at a 6.72% CAGR through 2031, reflecting the pivot to circular models. Projects like LyondellBasell’s German chemical-recycling plant and CIRCTEC’s tire-pyrolysis unit illustrate capital intensity and innovation depth needed to unlock polymer and rubber value. Industrial symbiosis networks multiply feedstock availability by turning one firm’s waste into another’s input, especially in chemical parks. EU extended-producer-responsibility schemes under the PPWR mandate minimum recycled content in packaging, driving sustained demand. These dynamics propel the segment’s share upward across the European industrial waste management market and attract equity capital despite high technical hurdles.

By Disposal Method: Landfill Legacy Under Pressure from Energy Recovery

Landfill maintained a 44.32% slice of the European industrial waste management market size in 2025, anchored in historical capacity, simple permitting, and lower gate fees in parts of Eastern Europe. Yet escalating landfill taxes, stricter contamination thresholds, and public opposition have begun to erode its long-held lead. Operators face mounting obligations to capture methane and monitor leachate, inflating operational expenditures. Some choose to downsize or retrofit inactive cells into solar farms, diversifying revenue but shrinking pure landfill tonnage within the European industrial waste management market.

Incineration & Energy Recovery displays the quickest expansion at 7.31% CAGR, buoyed by more than USD 2.18 billion (EUR 2 billion) invested annually in new waste-to-energy units across the continent. SUEZ’s USD 1.53 billion (EUR 1.4 billion) Toulouse facility, which integrates carbon capture, showcases evolving emission standards and added revenue through renewable-electricity certificates. Refuse-derived-fuel programs supply cement kilns, potentially displacing up to 85% of fossil heat needs. Enhanced thermal-plant efficiencies and co-location with district-heating networks boost attractiveness, progressively drawing volumes away from landfill and raising the profile of energy-recovery routes within the European industrial waste management market.

By Waste Type: Non-Hazardous Base Faces Rising Hazard Complexity

Non-hazardous waste captured 78.85% of the European industrial waste management market share in 2025, thanks to vast construction, packaging, and manufacturing residuals. Construction-and-demolition debris dominates tonnage, and existing recycling centers deliver aggregates back to roadbuilding and concrete mixes, supporting mandatory recycling thresholds. Symbiosis frameworks further monetize non-hazardous by-products by linking producers with neighboring industries that value secondary inputs. Policy incentives and reduced landfill levies for inert materials help sustain steady growth, although mature infrastructure means the segment’s CAGR will lag the market average.

Hazardous waste, while smaller, is advancing at a 5.15% CAGR until 2031. Electronics assembly, battery gigafactories, and specialty-chemical plants generate intricate waste streams requiring advanced stabilization, solvent recovery, or metallurgical extraction. EU shipment rules impose tight tracking and treatment standards, favoring large operators with pan-European permits and specialized incinerators. High gate fees and capacity scarcity bolster margins, positioning hazardous-waste handling as a premium niche within the European industrial waste management market.

By Industry: Construction Materials Dominant as Electronics Accelerate

Construction Materials commanded 31.95% of the European industrial waste management market size in 2025, propelled by ongoing renovation and infrastructure expansion across Germany, France, and the Nordics. Projects generate heavy volumes of concrete, metals, and timber that must meet diversion targets before landfill acceptance. Dedicated sorting lines and mobile crushers enhance onsite recovery rates, while regulated aggregates supply road beds and precast units, forming closed loops that align with circular-economy goals.

Electrical & Electronics, with an 7.96% CAGR, is the fastest-moving industrial client segment. Shorter product lifecycles, rising chip demand, and EV adoption inflate waste streams rich in precious metals and critical minerals. WEEE legislation imposes producer responsibility, stimulating certified collection schemes and specialist recovery plants. Automated dismantling lines and hydrometallurgical processes yield high-purity outputs for new battery and semiconductor production, elevating strategic interest in this segment across the European industrial waste management market.

Geography Analysis

Germany held 23.12% of the European industrial waste management market in 2025, underpinned by the continent’s densest network of waste-to-energy plants, cutting-edge recycling hubs, and stringent enforcement of EU directives. Its Rhine-Ruhr chemical corridor exemplifies integrated treatment architecture, where hazardous incineration, solvent recovery, and industrial symbiosis occur within a single cluster. High tipping fees for landfills and generous renewable-energy tariffs stabilize revenue for thermal operators. National strategy emphasizes carbon-neutral waste management by 2045, driving pilot carbon-capture retrofits and AI-enabled material-sorting installations.

France and Italy remain sizable, although regional compliance disparities create patchy performance. France’s updated anti-waste law accelerates reuse and bans the destruction of unsold goods, expanding the service scope for providers able to guarantee double-digit diversion rates. Italy’s North-South divide persists, with Lombardy approaching EU recycling targets while southern regions still depend heavily on landfill. Both countries witness public-private partnerships financing new energy-recovery units to close capacity gaps in the European industrial waste management market.

The Rest-of-Europe grouping, which encompasses Eastern and smaller Western states, shows the fastest growth at 7.12% CAGR to 2031. EU accession and structural-fund inflows finance state-of-the-art facilities in Poland, the Czech Republic, and Slovakia. Yet acute skilled-labor deficits spur automation and cross-border talent mobility programs. Investment vehicles anchored by Macquarie and EDF track local concessions, consolidating fragmented municipal operators. Harmonization of waste codes and DIWASS adoption reduces administrative frictions, opening space for integrated service offerings across borders within the European industrial waste management market.

Coverage of the industrial waste management market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for North America and Middle East, alongside detailed country-level intelligence for United Arab Emirates, each shaped by local operating conditions.

Competitive Landscape

Consolidation defines the competitive tone as private-equity funds and infrastructure investors inject fresh capital. The USD 2.60 billion (GBP 2.1 billion) buy-out of Biffa by Energy Capital Partners and Macquarie’s acquisition of Renewi exemplify a rush to assemble pan-regional platforms capable of offering bundled collection, treatment, and recovery solutions. Such a scale lets players spread R&D costs for AI sorting, blockchain tracking, and carbon-capture modules across multiple sites, reinforcing pricing power in the European industrial waste management market.

Technology leadership is the new battleground. Veolia’s robotic sorting at Southwark increases throughput and purity, enabling premium offtake contracts for recycled polymers. LyondellBasell, SUEZ, and OMV compete to commercialize chemical-recycling pathways that transform mixed plastics into virgin-quality feedstock. Operators leverage predictive analytics to optimize fleet dispatch, shrinking fuel consumption and meeting ESG metrics that win large industrial accounts. Capital intensity and intellectual-property barriers raise entry thresholds, fostering a moderate concentration structure.

Niche specialists focus on high-value waste streams such as battery materials and medical waste or on digital marketplaces that match industrial by-products with end-users. Partnerships with gigafactories or pharmaceutical groups secure stable feedstock and long-term purchase agreements. Eastern Europe offers white-space to deploy advanced technology, but success hinges on mitigating labor shortages through automation and cross-training. Regulatory mastery also differentiates winners; firms boasting ISO 14001, EMAS, and cross-border shipment authorizations command higher margins in the European industrial waste management market.

Europe Industrial Waste Management Industry Leaders

Veolia

Suez

Remondis

PreZero International

Biffa PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Macquarie Asset Management and BCI finalized the acquisition of Renewi to expand circular-economy operations and capture synergies across BENELUX and UK assets.

- May 2025: REMONDIS bought Schroll, enhancing hazardous-waste coverage in Austria and adjacent Central-European markets.

- March 2025: EQT entered talks for a majority stake in Waga Energy to scale biomethane production from landfill gas across Europe.

- February 2025: Energy Capital Partners closed the USD 2.60 billion (GBP 2.1 billion) takeover of Biffa, earmarking funds for advanced-treatment capacity and nationwide route integration.

Europe Industrial Waste Management Market Report Scope

Industrial waste management is the process of collecting, transporting, treating, and disposing of industrial waste. This waste can include contaminated soil, dry pesticides, and chemical waste.

The European industrial waste management market is segmented by type (construction and demolition waste, manufacturing waste, oil and gas waste, and other waste (chemical waste, mining waste, agriculture waste, nuclear waste), service (recycling, landfill, incineration, and other services), and country (Germany, France, United Kingdom, Spain, and Italy). The report offers market sizes and forecasts in value (USD) for all the above segments.

| Collection |

| Transportation & Logistics |

| Treatment & Disposal |

| Recycling & Material Recovery |

| Landfill |

| Recycling |

| Incineration & Energy Recovery (RDF, SRF, WtE) |

| Non-hazardous |

| Hazardous |

| Chemicals & Petrochemicals |

| Oil & Gas |

| Power Generation |

| Metal & Mining |

| Food & Beverage Processing |

| Pharmaceuticals |

| Electrical & Electronics |

| Construction Materials |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Service | Collection |

| Transportation & Logistics | |

| Treatment & Disposal | |

| Recycling & Material Recovery | |

| By Disposal Method | Landfill |

| Recycling | |

| Incineration & Energy Recovery (RDF, SRF, WtE) | |

| By Waste Type | Non-hazardous |

| Hazardous | |

| By Industry | Chemicals & Petrochemicals |

| Oil & Gas | |

| Power Generation | |

| Metal & Mining | |

| Food & Beverage Processing | |

| Pharmaceuticals | |

| Electrical & Electronics | |

| Construction Materials | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the European industrial waste management market in 2026?

The European industrial waste management market size reached USD 56.65 billion in 2026.

What is the forecast CAGR for European industrial waste services?

The market is projected to grow at a 5.59% CAGR from 2026 to 2031.

Which service category holds the biggest share?

Treatment & Disposal leads with 53.78% of the market in 2025.

Which country dominates industrial waste management in Europe?

Germany holds 23.12% of regional revenue thanks to advanced infrastructure and strict enforcement.

What is the fastest-growing industry segment for waste volume?

Electrical & Electronics waste streams are expanding at an 7.96% CAGR through 2031.

How will digital tracking affect cross-border waste shipments?

The EU’s DIWASS blockchain system, mandatory from May 2026, will cut paperwork and improve traceability, lowering administrative costs by roughly 30%.

Page last updated on: