Germany Bulky Waste Collection Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

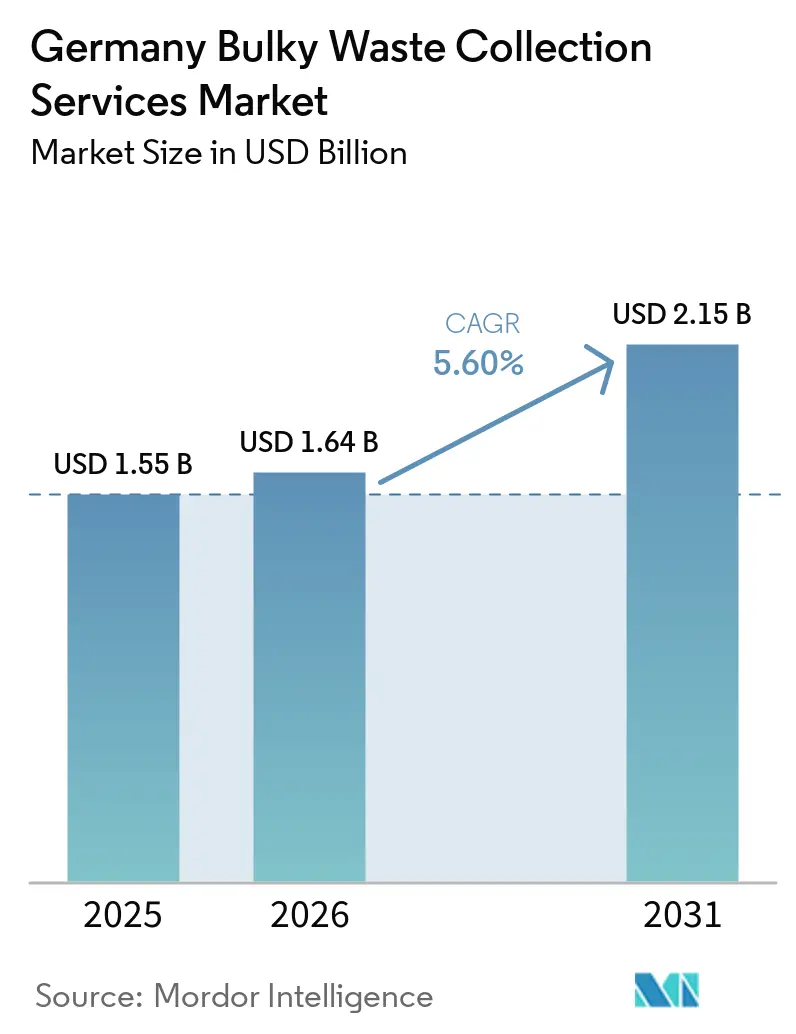

| Base Year Market Size (2025) | USD 1.55 Billion |

| Market Size (2026) | USD 1.64 Billion |

| Market Size (2031) | USD 2.15 Billion |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

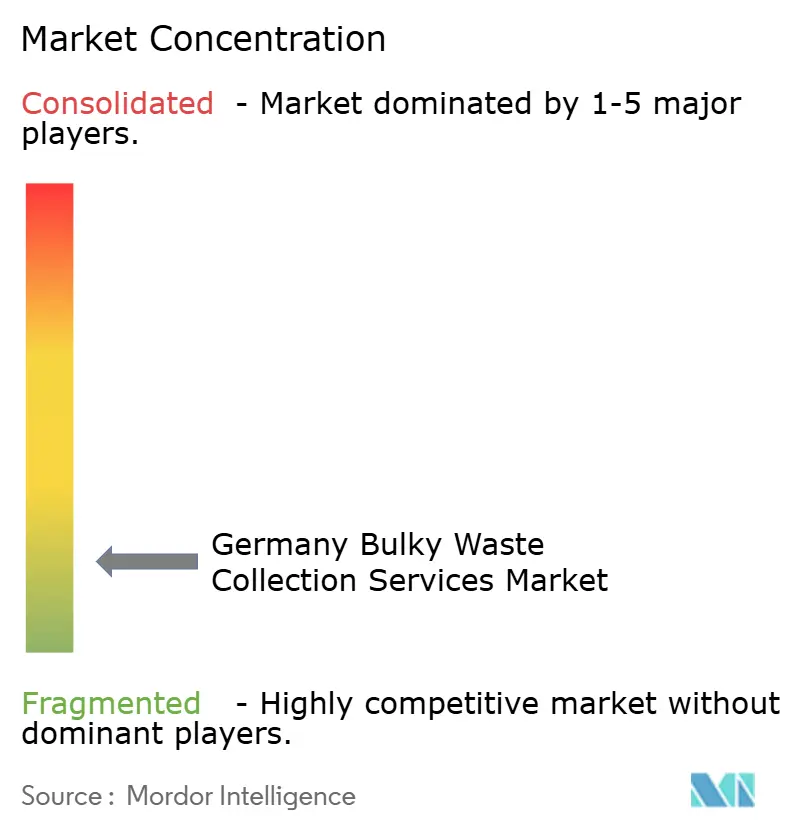

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Bulky Waste Collection Services Market Analysis by Mordor Intelligence

The Germany Bulky Waste Collection Services Market size is expected to grow from USD 1.55 billion in 2025 to USD 1.64 billion in 2026 and is forecast to reach USD 2.15 billion by 2031 at 5.60% CAGR over 2026-2031.

The shift toward on-demand booking, visible across Berlin, Munich, and Hamburg, is pushing operational models away from rigid calendar pick-ups toward user-scheduled services that align capacity with real-time demand signals. Residential sources remain the volume anchor, as dense city districts generate steady flows of furniture and household items, while policy measures, such as extended producer responsibility for mattresses, reinforce separate take-back channels that expand service throughput. Technology investments by large municipal and private operators are widening performance gaps with smaller haulers, a trend reinforced by pilots using computer vision, IoT container monitoring, and GPS-verified pickups that improve route efficiency and auditability. Regulatory tightening, including higher fines for fly-tipping in Berlin, nudges households toward formal booking channels, although enforcement capacity remains a constraint.

Key Report Takeaways

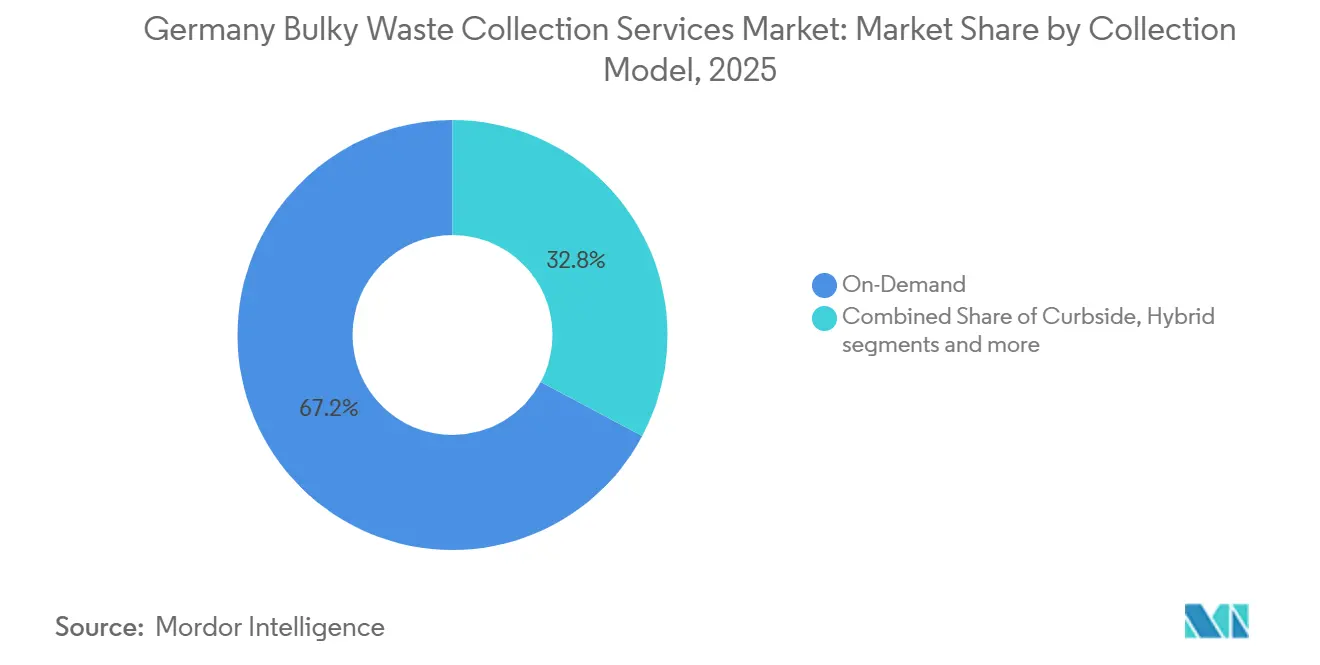

- By collection model, the on-demand segment led with 67.21% of the Germany bulky waste collection services market share in 2025, and it is projected to post the fastest growth at a 5.93% CAGR to 2031.

- By source, the residential segment accounted for 71.42% of the Germany bulky waste collection services market size in 2025 and is forecast to grow at a 6.23% CAGR through 2031.

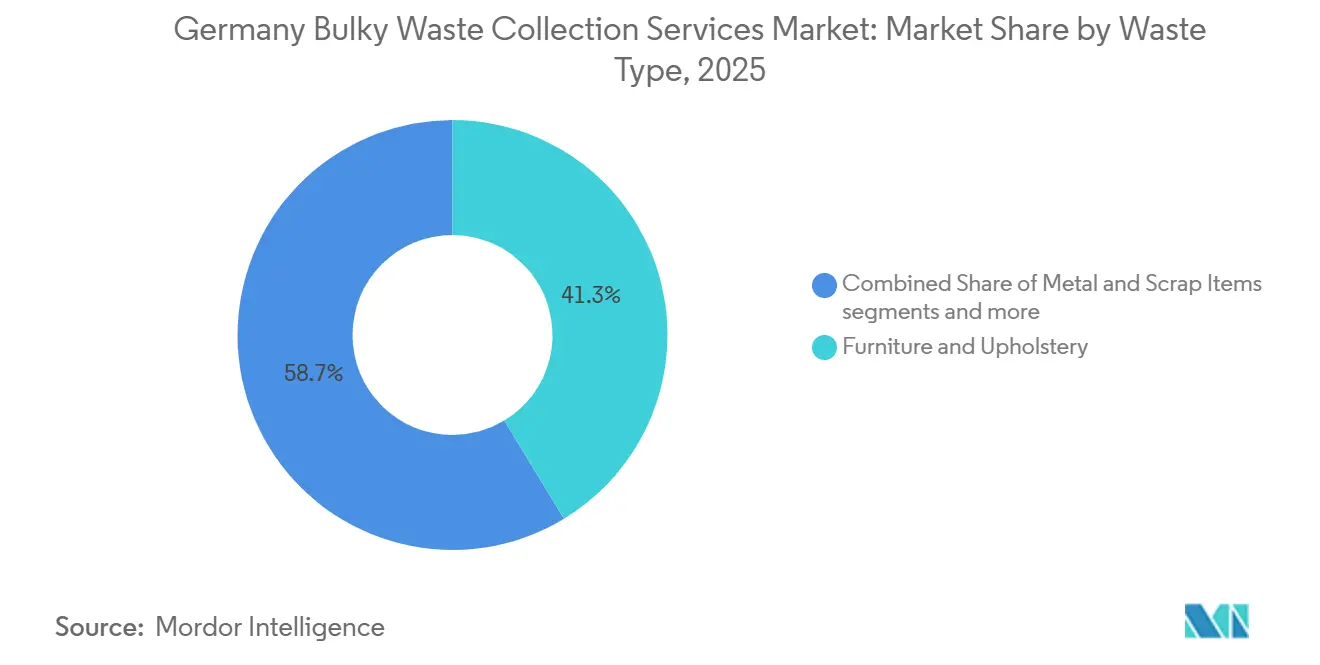

- By waste type, the furniture and upholstery segment accounted for 41.32% in 2025 and is expected to expand at a 6.41% CAGR to 2031, the fastest among waste types.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Bulky Waste Collection Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Circular Economy Act Mandating Separate Bulky Waste Collection | +1.2% | Global (all federal states), strongest in Berlin, NRW, Bavaria | Medium term (2-4 years) |

| Digitalization of Sperrmüll Booking Through Municipal Apps and Online Portals | +0.9% | National, with early gains in Berlin, Hamburg, Munich | Short term (≤ 2 years) |

| Growing Urban Population Density in Berlin, Munich, and Hamburg | +0.8% | Berlin, Munich, Hamburg core, spillover to Rhine-Ruhr | Long term (≥ 4 years) |

| EPR Expansion for Mattresses and Upholstered Furniture from 2025 | +1.4% | National | Medium term (2-4 years) |

| Renovation Boom in Altbau Buildings Driving Collection Demand | +1.1% | Urban centers, Western states | Medium term (2-4 years) |

| Dual System Deutschland (DSD) Standards Pushing Collection Efficiency | +0.6% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Circular Economy Act Mandating Separate Bulky Waste Collection

Germany’s Kreislaufwirtschaftsgesetz requires public waste authorities to provide separate bulky waste collection that enables preparation for reuse and component-level recycling. This mandate clarifies operational expectations for tenders and strengthens the case for investments in pre-sorting and documentation[1]Federal Ministry of Justice, “§20 KrWG Einzelnorm,” Gesetze im Internet, gesetze-im-internet.de. The 2025 expansion of separate collection obligations for textiles under EU waste rules further normalizes source-separated flows that interact with bulky waste logistics at municipal depots. Clear compliance pathways and sanctioning tools reduce planning risk for municipal operators and private contractors that invest in reuse and recycling infrastructure. Public reporting requirements and federal oversight increase transparency across the Germany bulky waste collection services market, helping align municipal service levels with diversion goals. The regulatory alignment across federal and EU levels supports stable growth planning for route design, depot capacity, and reuse partnerships.

Digitalization of Sperrmüll Booking Through Municipal Apps and Online Portals

Municipal apps and peer-to-peer integrations are reshaping booking behavior by letting residents choose collection slots, verify handovers, and receive confirmations. Berlin’s cooperation with Tiptapp enables paid on-demand pickups that close the loop with disposal proof, which shortens response times compared with fixed quarterly rounds. Hamburg’s Stadtreinigung app streamlines access to collection calendars, site navigation, and guidance on waste types, reducing call-center backlogs and improving scheduling accuracy. Timestamped bookings and address-level data flow into municipal systems and support route optimization that matches daily demand clusters. Digital channels also reduce incentives for curbside dumping because missed bookings can be rescheduled more quickly than waiting for the next fixed neighborhood day. The net effect is a steady migration in the Germany bulky waste collection services market toward dynamic capacity planning that favors operators with real-time dispatch and data governance credibility.

Growing Urban Population Density in Berlin, Munich, and Hamburg

Germany’s largest city-regions concentrate demand for bulky waste collection because multi-family housing generates consistent volumes of furniture and white goods. Service density and short travel distances enable more efficient daily route design, strengthening the business case for frequent on-demand slots in inner districts. Public operators in these cities also pilot micro-collection methods, including cargo bikes and AI-enabled cleaning vehicles, that fit narrow streets and align with low-emission goals. The combination of urban density and digital adoption accelerates the shift to data-driven resource allocation across depots and crews. Over time, population concentration leads to predictable booking peaks around move-in seasons and local renovation cycles, thereby enhancing forecasting quality. These structural factors reinforce the lead of large city-states in shaping service models that later expand to mid-sized municipalities.

EPR Expansion for Mattresses and Upholstered Furniture from 2025

The Bundesrat’s June 2025 resolution to implement extended producer responsibility for mattresses unlocks producer-financed take-back and reverse logistics. Germany disposes of millions of mattresses each year, and EPR is designed to shift these streams into dedicated collection and recycling channels that reduce incineration. Producer responsibility organizations are expected to define quality and handling standards that reward collectors who deliver dry, segregated items. This favors operators with covered vehicles, pre-sort stations, and proven compliance systems, which can change tender outcomes in municipalities that value high-quality material flows. As these requirements cascade into upholstered furniture, the Germany bulky waste collection services market gains a more reliable revenue stream that can offset labor and fuel cost inflation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sperrmüll Collection Frequency Reductions in Cost-Pressured Municipalities | -0.7% | Rural and mid-sized municipalities, Eastern states | Short term (≤ 2 years) |

| Illegal Dumping Competition from Schwarzentsorgung | -0.5% | Berlin, Ruhr region, border areas | Short term (≤ 2 years) |

| Driver Shortages in Eastern German States | -0.9% | Saxony, Brandenburg, Saxony-Anhalt, Mecklenburg-Vorpommern | Medium term (2-4 years) |

| High Labor Costs Under IG BAU Collective Agreements | -0.6% | National (unionized municipal operators) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sperrmüll Collection Frequency Reductions in Cost-Pressured Municipalities

Wage increases set by IG BAU for 2025 and 2026 have raised operating costs for unionized operators, putting pressure on municipalities to adjust service models. Some smaller jurisdictions respond by reducing calendar-based bulky-waste rounds and shifting demand toward paid on-demand slots. When scheduled pick-ups are cut back, event-day volumes rise, straining crew capacity and risking interim overflow and resident dissatisfaction. Budget constraints also delay digital pilots in mid-sized municipalities, limiting the diffusion of IoT-enabled route optimization. The net effect is a patchwork of service frequency across the Germany bulky waste collection services market, with better-resourced cities moving faster than rural districts.

Illegal Dumping Competition from Schwarzentsorgung

Berlin increased fines for illegal bulky-waste dumping to USD 1,635-11,990 for general violations and to USD 16,350 if hazardous materials are involved, which raises the cost of non-compliance for households and brokers. Despite higher penalties, illegal disposal networks exploit enforcement gaps and border dynamics, diverting tonnage away from licensed operators. Each illegal tonne represents lost revenue for formal channels and adds unplanned cleanup costs to municipal budgets. Cities deploy targeted surveillance and multilingual guidance, but deterrence depends on sustained inspections and prosecution. Over time, visible enforcement improves channel adherence and supports the growth of compliant services in the Germany bulky waste collection market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Collection Model: On-Demand Ascendancy Reflects Digital Infrastructure Maturity

On-demand collection model led with a 67.21% of the Germany bulky waste collection services market share in 2025 and is projected to record the fastest growth at a 5.93% CAGR through 2031 as digital booking becomes the default in large cities. Residents can request service within short windows through municipal integrations, such as Berlin’s cooperation with Tiptapp, which verifies proper drop-off with GPS-verified receipts. The Germany bulky waste collection services market has shifted toward this format because route planners can prioritize bookings by neighborhood clusters and reduce miles per pickup. Municipalities are pairing on-demand pickup with micro-collection assets such as e-cargobikes for dense cores and small loads that do not require a full truck. Hybrid strategies that mix neighborhood-day events and flexible routes are expanding in mid-sized cities that deploy container sensors to trigger demand-based service.

The curbside calendar model remains in rural and lower-digitized areas, yet it is losing share as smartphone adoption and municipal apps reduce booking friction. Contracted B2B frameworks also support on-demand logic because property managers and commercial estates require prioritized windows and confirmations. The Germany bulky waste collection services market benefits from on-demand data streams that enable continuous improvements in crew assignment and trip planning. EPR-related reimbursements for mattresses starting in 2025 add financial stability to models that can deliver high-quality segregated items. Taken together, these elements make on-demand both the largest and fastest-growing format in the Germany bulky waste collection services market.

By Source: Residential Dominance Sustained by Dense Urban Cores

The residential segment accounted for 71.42% in 2025, underscoring the central role of households in the German bulky waste collection services market. Berlin, Hamburg, and Munich anchor this pattern because dense neighborhoods generate steady volumes of furniture and appliances that align with frequent on-demand rounds. Federal support for renovating older housing, including EUR 350 million (USD 381.5 million) for a program that helps young families acquire and retrofit older stock, sustains residential flows as fixtures and furnishings are replaced. These upgrades are complemented by municipal zero-waste strategies that promote reuse and separate streams, which improve material quality at depots[2]Berlin Senate, “Zero Waste Strategy 2030,” Berlin.de, berlin.de. The Germany bulky waste collection services market benefits from residential pickup integrated with app-based notifications, depot wayfinding, and proof of delivery, which reduces no-shows.

Commercial sources remain smaller but can be episodic and high-volume when offices relocate or hotels refurbish, which supports contracted service frameworks. Industrial sources are usually handled outside municipal frameworks, which limits crossover into residential routes. Public buildings contribute through scheduled clear-outs that align with budget cycles and sustainability targets. Year-round flows, predictable peaks during moving seasons, and growing household use of digital channels support the Germany bulky waste collection services market size from residential sources. As EPR systems for textiles and mattresses scale, residential sources will remain dominant while collection quality standards rise.

By Waste Type: Furniture & Upholstery Leads Amid Material-Specific Recovery Targets

Furniture and upholstery led with 41.32% in 2025 and is projected to expand at a 6.41% CAGR to 2031, the fastest among waste types in the Germany bulky waste collection services market. The 2025 shift to EPR for mattresses is expected to channel a significant share of upholstered items into producer-financed take-back programs that reward high-quality segregation. These programs incentivize covered transport and dry storage at pre-sort hubs to protect material value and support downstream recycling yields. Municipal reuse strategies and depot infrastructure improvements increase the visibility of these streams, making performance-based contracting more feasible. These dynamics collectively secure the segment’s leadership in the Germany bulky waste collection services industry.

Other streams, such as metal items and white goods, are subject to specific regulations on component removal and safe handling. Construction-related items sometimes enter bulky-waste channels from home renovations, which require clear municipal guidance to avoid contamination of streams intended for reuse or material recycling. As digital product passports are developed for complex items, identification and sorting at depots can improve traceability and support market-based incentives for recyclability. The Germany bulky waste collection services market continues to prioritize furniture and upholstered items because they deliver reliable volumes and respond well to source-separation rules. This underpins steady investment in handling standards and reverse logistics tailored to this stream.

Geography Analysis

Western states accounted for the largest share of activity in 2025, reflecting higher urbanization, stronger renovation pipelines, and more advanced deployment of digital booking and sensor networks in cities such as Cologne, Munich, and Stuttgart. Eastern states, while currently contributing a smaller share, are set to experience a swifter projected CAGR through 2031 as municipalities ramp up the digitalization of routes and weave smart city pilots into public services. Northern states benefit from port-linked logistics and established recycling flows, which support stable collection throughput in their urban centers. The Germany bulky waste collection services market reflects this regional spread in operator strategies and tender requirements, particularly in cities that seek audit-ready documentation and digital service confirmations.

Berlin stands out for both scale and experimentation with service models, including app-mediated on-demand pickups and micro-collection pilots using e-cargobikes that fit narrow streets and reduce emissions. The city also increased fines in November 2025 to deter illegal dumping, which pushes more activity into formal booking channels and supports higher capture rates for reuse and recycling. Hamburg’s municipal app further illustrates how digital reminders and guidance reduce missed appointments and direct residents to the right drop-off points. Cities like Wuppertal demonstrate the impact of container fill-level sensing and dynamic routing on service reliability and emissions. The Germany bulky waste collection services market gains from these urban pilots as technology readiness and procurement templates spread to neighboring municipalities.

Mid-sized and smaller municipalities exhibit gradual adoption curves, with budgets and staffing determining the pace of the digital transition[3]Stadt Gera, “Smart Waste Management,” Stadt Gera, stadt-gera.de. Gera’s smart city program illustrates how sensor data and AI-supported routing can reduce complaints and make pick-up windows more predictable for residents. Mannheim’s underground container sensors highlight another path to data-driven adjustments in collection intervals to match compaction and fill dynamics. Across regions, tender criteria now more often specify ISO-certified environmental management, GDPR-compliant data handling, and digital verification of services. These elements together create a consistent direction of travel in the Germany bulky waste collection services market despite differing starting points.

Competitive Landscape

The Germany bulky waste collection services market is fragmented, with a balanced mix of municipal incumbents and large private groups, as well as regional SMEs active in local tenders. Municipal operators such as BSR and Stadtreinigung Hamburg leverage public trust, year-round communication channels, and direct control of recycling centers to maintain strong positions. Private leaders deploy digital tools and data science to optimize routes and document quality, which resonates with performance-based tender structures. The combination creates intense competition for multi-year framework agreements in large cities and room for specialization among mid-sized operators.

Technology choices are becoming strategic differentiators. Remondis has scaled computer vision for litter mapping and smart container pilots that improve route design, service verification, and hotspot identification. BSR’s adoption of e-cargobikes for small-volume urban pick-ups illustrates a low-emission option that can undercut van-based collections in narrow streets. Citywide or district-level LoRaWAN networks, such as in Wuppertal, enable flexible, fill-level-driven routes and reduce reliance on static calendars. These examples show why larger contract holders can scale digitalization, while small haulers face investment hurdles that limit their ability to compete on data-rich tenders.

A new cohort of route-optimization vendors is also shaping the competitive landscape. Zebrafant.ai’s sensor-free prediction tools expand access to AI-based scheduling for municipalities that lack infrastructure budgets, enabling measurable reductions in spilled containers and operating costs. Vendors that integrate with municipal back ends and prioritize GDPR-compliant processing gain procurement advantages. As extended producer responsibility programs for mattresses scale, operators that build strong PRO relationships and meet handling standards are positioned to capture higher-quality streams at better economics. These dynamics suggest that capability gaps in digital operations and EPR compliance will shape the next phase of competition in the Germany bulky waste collection services market.

Germany Bulky Waste Collection Services Industry Leaders

Remondis SE & Co. KG

ALBA Group

Berliner Stadtreinigung (BSR)

PreZero Stiftung & Co. KG

Veolia Environnement SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Zebrafant.ai expanded to six federal states, reported covering more than 2 million citizens, and recorded over 500,000 scanned fill-level events using sensor-free prediction, reducing spills and costs for municipal partners.

- February 2026: IG BAU and ISS Facility Services finalized a collective wage agreement that delivers 5.7% total increases over 22 months, adding near-term labor cost pressure to facility-linked waste services.

- November 2025: Berlin raised fines for illegal dumping of bulky waste to USD 1,635-USD 11,990, and to USD 16,350 for hazardous material cases, to improve deterrence and shift disposal into formal channels.

Germany Bulky Waste Collection Services Market Report Scope

| Curbside |

| On-Demand |

| Hybrid |

| Contracted B2B |

| Others |

| Residential |

| Commercial |

| Industrial |

| Municipal/Government |

| Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets) |

| Furniture & Upholstery |

| Metal & Scrap Items |

| White Goods/Appliances |

| Construction & Demolition |

| Others (Event-specific Waste, Biomedical/Institutional) |

| By Collection Model | Curbside |

| On-Demand | |

| Hybrid | |

| Contracted B2B | |

| Others | |

| By Source | Residential |

| Commercial | |

| Industrial | |

| Municipal/Government | |

| Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets) | |

| By Waste Type | Furniture & Upholstery |

| Metal & Scrap Items | |

| White Goods/Appliances | |

| Construction & Demolition | |

| Others (Event-specific Waste, Biomedical/Institutional) |

Key Questions Answered in the Report

What is the current size and growth outlook for the Germany bulky waste collection services market?

The Germany bulky waste collection services market size stands at USD 1.55 billion in 2025 and is projected to reach USD 2.15 billion by 2031 at a 5.6% CAGR over 2026-2031.

Which collection model leads in Germany’s bulky waste services?

On-demand models lead with 67.21% in 2025 and are also the fastest growing with a 5.93% CAGR through 2031, driven by municipal apps and digital booking.

What sources contribute most to bulky waste volumes in Germany?

Residential sources account for 71.42% of 2025 volumes, supported by dense urban cores and renovation activity backed by federal programs.

Which waste type is the largest in Germany’s bulky waste stream?

Furniture and upholstery hold 41.32% in 2025 and are expected to grow at a 6.41% CAGR to 2031, supported by mattress EPR implementation.

How is illegal dumping being addressed in major German cities?

Berlin increased fines in November 2025 to USD 1,635-11,990, and to USD 16,350 for hazardous cases, which encourages use of formal collection channels.

What technologies are improving bulky waste collection performance in Germany?

Cities deploy AI mapping, container sensors, and app-based booking that enable dynamic routing and verified service delivery, as seen in Remondis pilots and Wuppertal’s LoRaWAN rollout.

Page last updated on: