Sweden Renewable Gas From Waste Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

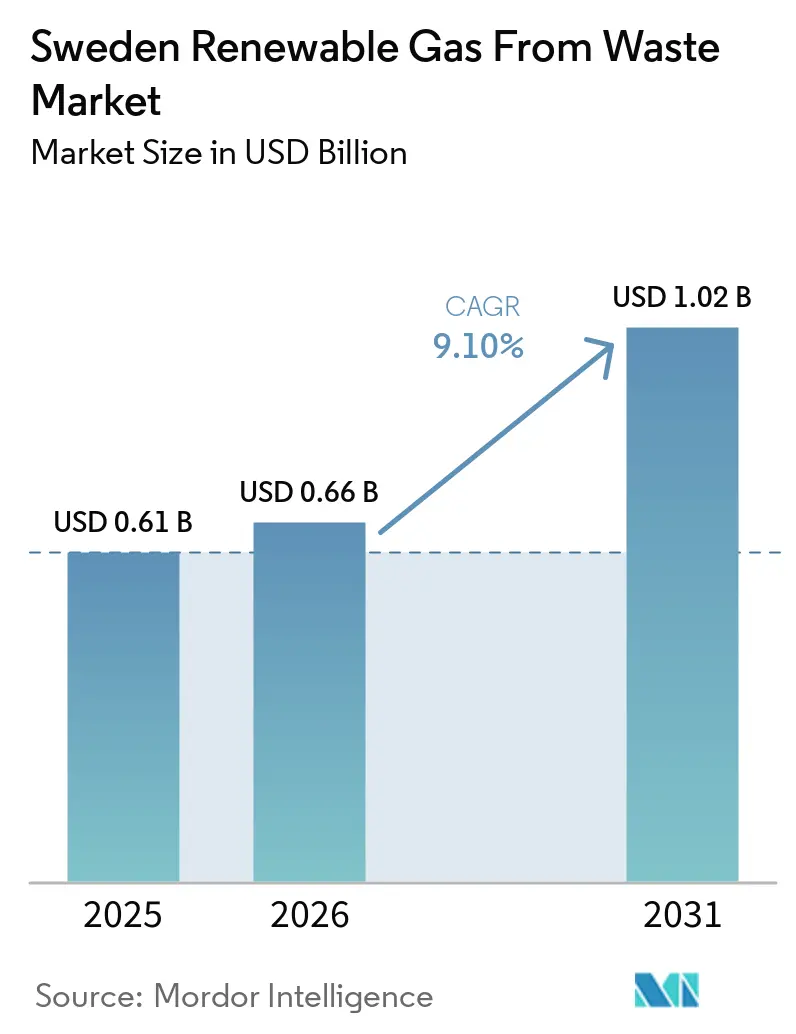

| Base Year Market Size (2025) | USD 0.61 Billion |

| Market Size (2026) | USD 0.66 Billion |

| Market Size (2031) | USD 1.02 Billion |

| Growth Rate (2026 - 2031) | 9.10% CAGR |

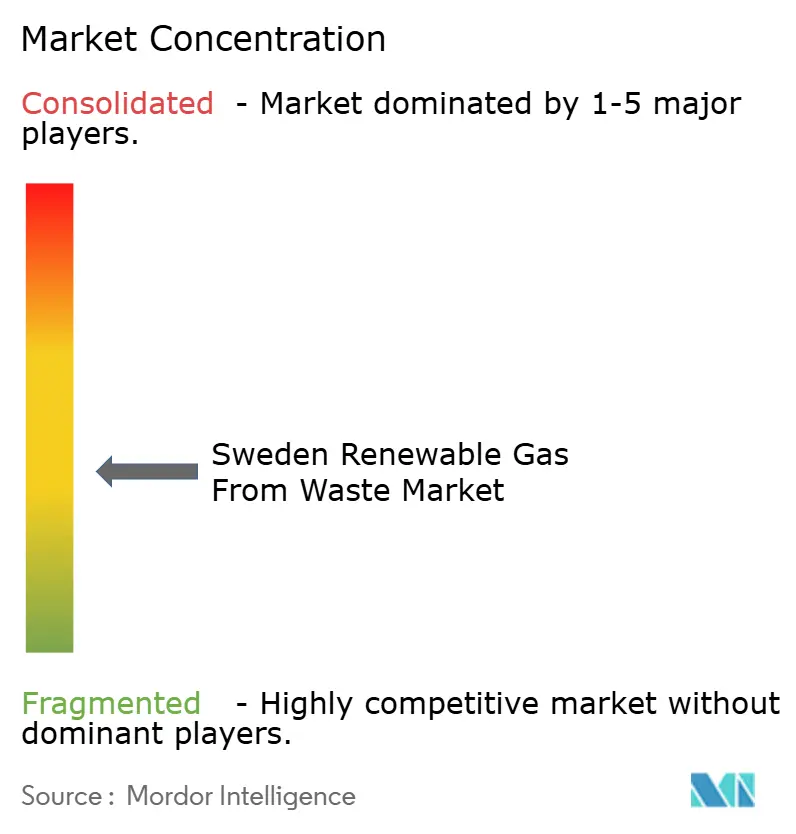

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Renewable Gas From Waste Market Analysis by Mordor Intelligence

The Sweden Renewable Gas From Waste Market size was valued at USD 0.61 billion in 2025 and is estimated to grow from USD 0.66 billion in 2026 to reach USD 1.02 billion by 2031, at a CAGR of 9.10% during the forecast period (2026-2031).

The stronger outlook reflects a more stable policy setting after Sweden regained the tax exemption for non-food-based biogas, which restored commercial confidence across production, distribution, and end-use markets. Growth is also being supported by Sweden’s mandatory bio-waste separation rules, which are widening the supply of sorted organic material and improving feedstock visibility for project developers. At the same time, record support through Klimatklivet, rising liquefied biogas demand from heavy transport, and grid connection investments in western Sweden are shifting the market from a municipal utility base toward a larger industrial fuel and infrastructure opportunity. The main limits remain competition for sustainable feedstock from other bioeconomy uses, the gap between current domestic production and the sector’s 2030 ambition, and the absence of a harmonized guarantee-of-origin route that would improve cross-border pricing for Swedish renewable gas.

Key Report Takeaways

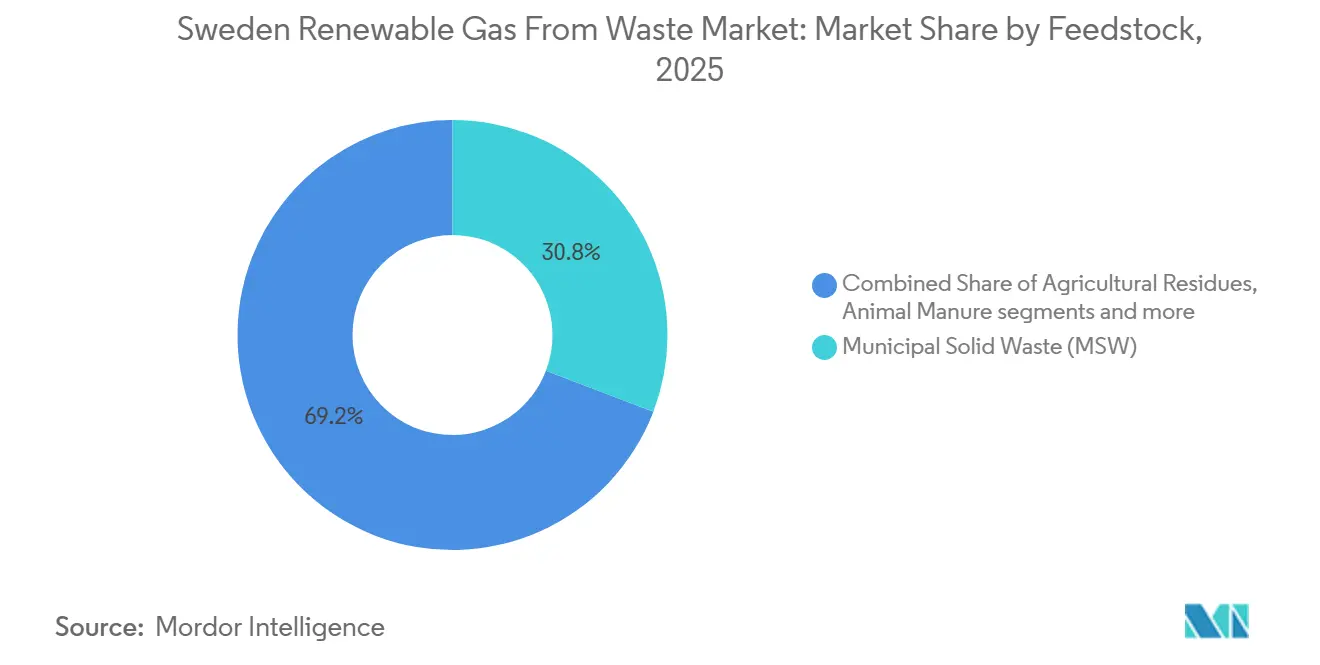

- By feedstock, municipal solid waste led with a 30.8% of the Sweden renewable gas from waste market size in 2025, while food waste is forecast to expand at a CAGR of 10.5% through 2031.

- By technology, anaerobic digestion held a 42.8% of the Sweden renewable gas from waste market share in 2025, while biogas upgrading systems are projected to grow at a CAGR of 12.4% through 2031.

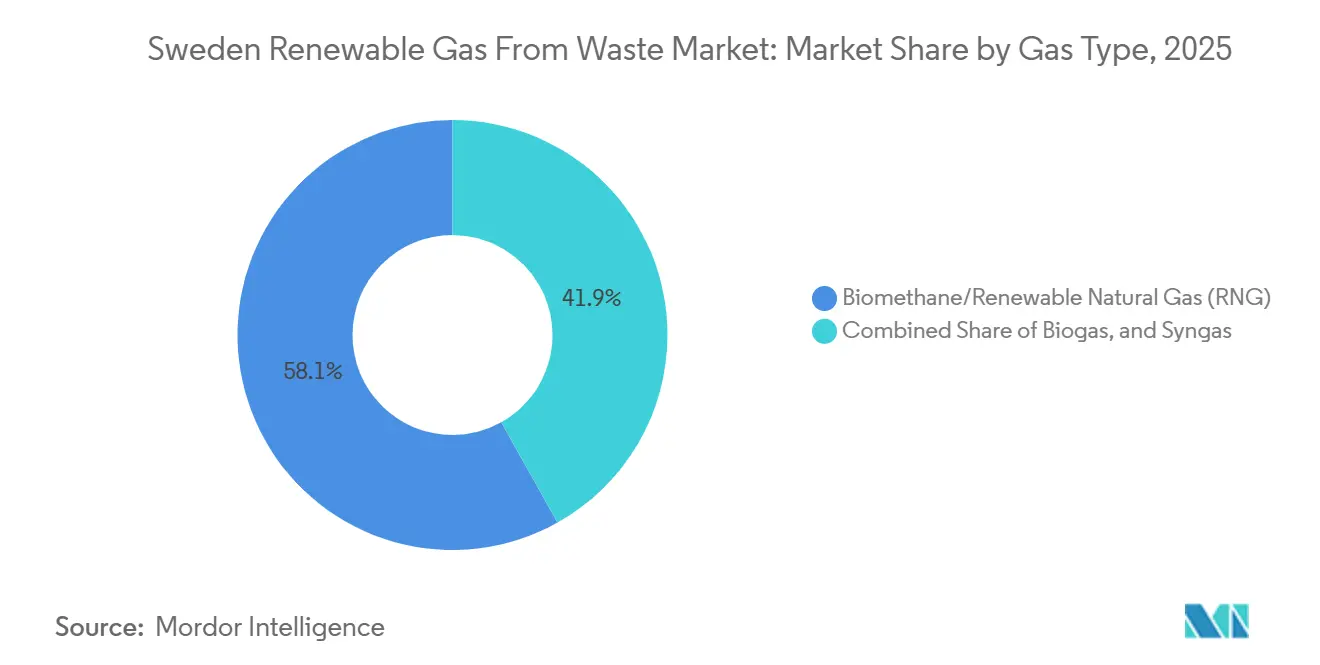

- By gas type, biomethane/renewable natural gas (RNG) accounted for 58.1% of revenue in 2025 and is expected to record the fastest growth at a 13.2% CAGR through 2031.

- By application, transportation fuel captured a 34.6% share in 2025, while grid injection is projected to advance at a CAGR of 14.1% through 2031.

- By component, gas processing and upgrading units represented 31.4% of the market share in 2025, while monitoring and control systems are forecast to grow at a 12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Sweden Renewable Gas From Waste Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reinstated Biogas Tax Exemption Reviving Industrial and Transport Demand | +2.5% | National, with the strongest gains in Västra Götaland, Skåne, and Greater Stockholm | Short term (≤ 2 years) |

| Mandatory Municipal Organic Waste Separation Expanding Feedstock Supply | +2.2% | National, with early gains in Stockholm, Gothenburg, and Malmö | Medium term (2-4 years) |

| Klimatklivet Climate Investment Scheme Funding Waste-to-Gas Projects | +1.8% | National, with notable disbursements in Östergötland, Västra Götaland, Gotland, and Jönköping | Short term (≤ 2 years) |

| Surging Heavy Transport Sector Demand for Liquefied Biogas | +1.5% | National, with strongest uptake along the E4 and E6 transport corridors | Medium term (2-4 years) |

| Nordion Energi’s 100% RNG Grid Vision Accelerating Injection Capacity | +0.9% | Primarily southwestern Sweden, with spillover into Skåne and Halland | Long term (≥ 4 years) |

| European Union REPowerEU Biomethane Target Reinforcing Sweden’s National Policy Alignment | +0.7% | National, with the strongest effect on grid-connected producers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reinstated Biogas Tax Exemption Reviving Industrial and Transport Demand

In the Sweden renewable gas from waste market, the removal of the tax exemption reversed the most significant commercial disruption in the past 2 years. The European Commission approved Sweden’s tax exemption schemes for non-food-based biogas and bio-propane used for heating and as motor fuel on October 23, 2024, restoring the legal basis for the incentive. The Swedish Tax Agency then moved the system back to direct deductions from the March 2025 reporting period, which reduced administrative friction for producers, distributors, and buyers. Nordion Energi reported that biogas accounted for 39.3% of all gas traded on the western Swedish grid in Q1 2025, demonstrating how quickly demand and injection volumes responded once fiscal clarity returned. The measure also improved buyer confidence in transport and industrial uses, where biogas economics are highly sensitive to fuel tax treatment, and where projects that had been delayed began moving again after the reinstatement.

Mandatory Municipal Organic Waste Separation Expanding Feedstock Supply

The Sweden renewable gas from waste market is also benefiting from structural improvements in feedstock availability, rather than solely from stronger fuel demand. Sweden’s requirement for the separate collection of bio-waste from households and businesses took effect on January 1, 2024, under the Waste Ordinance, which brought Article 22 of the EU Waste Framework Directive into operational practice. The obligation covers restaurants, food retail, canteens, and parts of the food industry, widening the collection base beyond residential sorting and making the feedstock pool more reliable for plant operators. Because municipalities are responsible for property-near collection, developers can secure long-term supply contracts with less uncertainty over local collection practices. The rollout is not fully uniform because Naturvårdsverket confirmed that dispensation applications continued into 2026, so smaller municipalities still face a slower ramp-up in sorted organic waste volumes.

Klimatklivet Climate Investment Scheme Funding Waste-to-Gas Projects

The Sweden renewable gas from waste market continues to rely on Klimatklivet as the main public financing tool for new capacity, especially where project economics remain tight at the construction stage. The Swedish government set the 2026 Klimatklivet appropriation at SEK 4.5 billion (USD 489.7 million), with an authorization ceiling of SEK 8 billion (USD 870.6 million), and reopened support for farm-scale biogas for electricity and heat through a directive issued in December 2025. Project awards show how broad the support base has become, with grants tied to Gasum’s Götene plant, Biogas Nordöstra Skaraborg in Tibro, and SuderGas on Gotland. The program is also beginning to support a broader business model, as Naturvårdsverket reported more applications for combined biogas and bio-CCU facilities in 2026. This reduces financing risk for projects that need additional revenue from captured biogenic carbon dioxide, digestate utilization, or higher-value biomethane output to secure final investment approval.

Surging Heavy Transport Sector Demand for Liquefied Biogas (LBG)

The Sweden renewable gas from waste market is seeing one of its clearest demand signals from long-haul freight, where liquefied biogas aligns with fleet range requirements. Swedish LBG production rose by 41% in 2024 to 253 GWh, while domestic LBG consumption increased by 21% to 755 GWh, meaning demand is expanding faster than local supply and imports are still filling the gap. This demand is anchored in heavy trucks because LBG offers a long driving range, rapid refueling, and easier fleet conversion for operators already working with gas-based logistics solutions. More than 30 public liquid-gas filling stations were operating nationally by 2025, extending commercial access from northern Sweden to the south and supporting broader route planning for fleet operators. Nordion Energi’s liquefaction plant at the Port of Gothenburg, due for completion in autumn 2026 with an annual capacity of 250 GWh, strengthens this route further because it will serve road transport and maritime bunkering from one site.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Availability of Sustainable Feedstock Due to Competition from Other Bioeconomy Sectors | -1.8% | National | Medium term (2-4 years) |

| Large Gap Between Current 2.4 TWh Output and the 10 TWh 2030 Ambition | -1.2% | National, with the strongest supply challenge in northern and rural areas | Long term (≥ 4 years) |

| Absence of a Dedicated National Biomethane Production Target in NECP | -0.9% | National, with the greatest effect on large-scale project finance | Long term (≥ 4 years) |

| No Harmonized Guarantee of Origin Registry for Domestic Renewable Gas | -0.6% | National, with cross-border effects concentrated in European Union bilateral trade | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Availability of Sustainable Feedstock Due to Competition from Other Bioeconomy Sectors

The Sweden renewable gas from waste market depends on a stable supply of sustainable organic feedstock, but these same waste and residue streams are also being pursued by other bioeconomy uses. This reduces the volume that can be secured for biogas and biomethane production, especially in regions where multiple projects rely on similar feedstock sources. The issue is more pronounced for large plants because they need long-term supply contracts to support financing, plant utilization, and operating efficiency. When feedstock access becomes less certain, developers may delay project execution, scale down planned capacity, or face higher sourcing pressure. This limits the pace at which the Sweden renewable gas from waste market can expand, even when policy support and end-user demand remain favorable.

Large Gap Between Current 2.4 TWh Output and 10 TWh 2030 Ambition

The Sweden renewable gas from waste market also faces a scale challenge because current output remains well below the level needed to meet the sector’s 2030 ambition. Domestic biogas production reached 2.4 TWh in 2024, while industry and parliamentary discussions continue to center on a 10 TWh target for 2030, leaving a large buildout gap even after recent investment commitments. Sweden’s domestic consumption stands at around 4.1 TWh, so a meaningful share of use is still covered by imports, which expose buyers to external supply conditions and limit the strategic value of local circular feedstocks. The constraint is not only technical, as SLU Future Food and Linköping University indicated that better use of manure and organic waste streams could support production in the 7-10 TWh range. The harder issue is that plant development often takes several years, which means the pipeline funded today will close only part of the gap by the end of the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Organic Waste Diversity Anchoring Production Resilience

Municipal solid waste held a 30.8% share of the Sweden renewable gas from waste market in 2025, reflecting the strength of Sweden’s collection systems and the direct routing of sorted organic streams into biological treatment. The segment benefits from a mature municipal role in waste handling, which gives developers a more predictable base load of feedstock than many privately assembled supply chains. The January 2024 bio-waste separation rule reinforced this position by expanding access to pre-sorted organics from households, restaurants, food retail outlets, and commercial kitchens. In the Swedish renewable gas from waste industry, this matters because large digestion assets need stable volumes more than occasional spot availability. Municipal solid waste also offers a practical hedge against volatility in single-source feedstock categories because collection is recurring and geographically distributed.

Food waste is the fastest-growing feedstock segment, with the food waste segment of the Sweden renewable gas from waste market projected to expand at a CAGR of 10.5% through 2031. This growth follows the same 2024 sorting rule, but it is stronger because food waste from restaurants, supermarkets, and catering sites is now entering formal collection streams more consistently than before. Agricultural residues and animal manure form the second major supply pillar, and their role is expected to improve as farm-scale projects regain access to funding under Klimatklivet from 2026. Sewage sludge remains important but is growing more slowly because plant expansion depends on wastewater infrastructure upgrades. At the same time, landfill waste and industrial organic waste are more site-specific and less responsive to broad national policy. Feedstock selection is also shaped by Sweden’s HBK sustainability framework, which favors well-documented sources that can demonstrate life-cycle greenhouse gas savings.

By Technology: Upgrading Infrastructure Becoming the Critical Bottleneck

Anaerobic digestion retained the leading technology position with a 42.8% share in 2025, reflecting its suitability for food waste, manure, sewage sludge, and municipal organic fractions. The technology also carries the lowest development risk because Sweden already has operating experience, known yield profiles, and a clear regulatory path for permitting and sustainability documentation. In the Sweden renewable gas from waste market, this installed base gives anaerobic digestion an advantage that newer routes have not yet matched. Landfill gas recovery is now a mature and declining segment because Sweden sends very little new organic waste to landfills, which limits the formation of fresh gas at legacy sites. Gasification and pyrolysis remain relevant for harder-to-digest residues, but their broader role still depends on more favorable capital costs and proven commercial economics at scale.

Biogas upgrading systems are the fastest-growing technology segment, and this segment of the Sweden renewable gas from waste market is projected to rise at a CAGR of 12.4% through 2031. The reason is straightforward: upgraded gas can enter the grid, move into transport fuel channels, or be liquefied for higher-value uses, while raw biogas has a narrower set of commercial outlets. EnviTec Biogas commissioned an EnviThan membrane-based upgrading system for a Swedish operator in 2024, showing that international technology suppliers already see Sweden as a growth market for advanced upgrading equipment. Nordion Energi’s 2024 investment plan to enable more producer connections adds another layer of support because new grid access increases the value of meeting biomethane specifications. Other component technologies will still grow, but the greatest value creation lies in the step that converts raw gas into a tradable, low-carbon fuel.

By Gas Type: Biomethane/ Renewable Natural Gas (RNG) Strengthening Commercial Demand

Biomethane/renewable natural gas (RNG) accounted for 58.1% of revenue in 2025, making it the leading gas type in the Sweden renewable gas from waste market. This position reflects the stronger commercial value of upgraded gas compared with untreated biogas, especially in grid injection, transport fuel, and liquefied biogas applications. Nordion Energi reported that the western Swedish gas grid reached a 39.3% biogas share in Q1 2025, which supports continued demand for upgraded gas quality across the value chain. Raw biogas still has a role in on-site heat and power applications, particularly at wastewater treatment plants and municipal utility facilities, where internal consumption reduces distribution requirements. Syngas remains a small segment because commercial-scale gasification output from waste streams is still limited in Sweden.

Biomethane/ Renewable Natural Gas (RNG) is also the fastest-growing gas type, with a projected 13.2% CAGR through 2031. Growth is supported by corporate decarbonization programs, stronger demand for transport fuels, and the expanding need for certified renewable gas in industrial and logistics applications. In the Sweden renewable gas from waste market, the premium for this segment depends not only on gas quality but also on the ability to document sustainability and trade attributes across borders. Sweden’s Energy Agency operates the domestic gas registry, but Sweden is still outside the AIB Gas Scheme, which limits seamless certificate transfer to buyers in other European markets. This means producers with strong certification pathways and established buyer contracts are likely to secure the best pricing and the strongest export-linked demand.

By Application: Transportation Fuel Leads as Grid Injection Accelerates

Transportation fuel accounted for a 34.6% share of the Sweden renewable gas from waste market in 2025, reflecting the long buildout of Sweden’s vehicle-gas network and the practical suitability of biomethane for freight and fleet use. The application remains strongest in counties with dense logistics activity and stronger gas infrastructure, especially Västra Götaland, Skåne, Östergötland, and the Uppsala region.[2]Statistics Sweden, “Deliveries of Natural Gas, Biomethane and Hydrogen Gas for Transport,” Statistics Sweden, scb.se Combined heat and power remains important because many municipal utilities already use biogas in local district heating and electricity systems. Industrial and building heat demand also remains relevant, but those uses are more dependent on pipeline access and local connection economics. As a result, transport continues to lead because it can absorb both compressed and liquefied gas across a wider national footprint.

Grid injection is the fastest-growing application, with the grid injection segment of the Sweden renewable gas from waste market projected to increase at a CAGR of 14.1% through 2031. This high growth rate stems from a small current base. Still, it also reflects a genuine shift in infrastructure planning, as Nordion Energi has moved from passive network operation to active connection development. The company’s green grid plan aims to remove the distance barrier that long discouraged mid-sized producers from upgrading gas for injection. Nordion reported 20 connection inquiries from existing and planned plants soon after the plan was announced, suggesting real pent-up demand rather than merely theoretical interest. Tekniska verken’s addition of food-certified bio-CO2 recovery to its Linköping biogas operations also suggests that more producers will aim to increase value per ton of feedstock rather than sell only a basic gas stream.

By Component: Gas Processing Leads, Monitoring Systems Emerge as Margin Enhancer

Gas processing and upgrading units accounted for 31.4% of revenue in 2025, making them the largest component group in the Sweden renewable gas from waste market. This result aligns with the broader product mix, as producers are increasingly focused on biomethane and LBG rather than on-site use of untreated gas. Upgrading skids, separation systems, and gas-cleaning equipment is the most value-intensive part of many new plants, which keeps their revenue weight above that of more standardized hardware. Digesters and fermentation systems remain essential, but their revenue growth follows plant count and plant size more directly than product upgrade economics. Gas collection systems are comparatively mature, so value gains there come more from emission control and methane loss reduction than from major design shifts.

Monitoring and control systems are the fastest-growing component segment, projected to grow at a 12% CAGR through 2031. This reflects tighter operating standards because larger sites need better data on feedstock origin, gas yield, system uptime, and sustainability reporting. Sweden’s HBK framework requires documented control systems for qualifying facilities, which turns monitoring from an optional efficiency tool into a compliance requirement. Smarter waste collection and sorting also increase the value of plant-side digital control, as more variable organic streams require tighter feed management. In the Sweden renewable gas from waste market, that means digital systems can improve margins even when their direct revenue share remains smaller than that of core gas hardware.

Geography Analysis

Western Sweden already accounts for the greatest operating weight in the Swedish renewable gas from waste market, as the western gas grid reached a 39.3% biogas share in the first quarter of 2025 and remains the country’s most developed gas corridor. Västra Götaland benefits from network access, livestock density, and a cluster of experienced developers, which gives it better economics than isolated off-grid regions. Nordion Energi’s SEK 2.2 billion (USD 239.4 million) investment plan, adopted in 2024, focuses on enabling more renewable gas connections in this southwestern corridor and supports a large increase in connected production by 2030. The region also has a strong manure-based model because Biogas Västra Skaraborg is developing a farmer-linked supply system in Vara that reduces aggregation risk and helps stabilize feedstock flow. This makes western Sweden the best-positioned area for grid injection, LBG production, and larger multi-feedstock assets.

Southern Sweden forms the second major cluster in the Sweden renewable gas from waste market because Skåne combines intensive agriculture, food-processing residues, and useful proximity to broader gas trade routes. Gasum received environmental approval in 2026 for a large-scale plant in Hörby and made an investment decision on a second plant in Sjöbo, with start-up plans for 2028 and 2029, respectively. Scandinavian Biogas also received backing from Klimatklivet for its Örkelljunga LBG project in Skåne, which deepens the regional production base. The Stockholm-Uppsala area anchors central Sweden through great urban demand, major municipal energy infrastructure, and new pipeline integration that expands gas logistics within the capital region. Tekniska verken’s expanded Linköping facility and Stockholm-linked infrastructure upgrades strengthen this corridor as a demand and distribution center rather than only a feedstock location.

Gotland and northern Sweden account for smaller volumes, but they remain important to the Sweden renewable gas from waste market because they show where future diversification could come from. Gotland secured targeted support for SuderGas, showing that islands and remote systems can still move forward when grant support bridges the scale disadvantage. The main difference is that many northern and inland producers remain off-grid, so they depend on trucked compressed and liquefied biogas rather than injection into a regional gas system. Bio-waste collection is also phasing in unevenly because some smaller municipalities continued under dispensations into 2026, which delays the full feedstock benefit outside the largest urban areas. This leaves Sweden with a clear regional hierarchy in which the southwest leads on infrastructure, the south grows through new plant announcements, central Sweden anchors major demand nodes, and peripheral regions expand more selectively.

Competitive Landscape

The Sweden renewable gas from waste market is moderately concentrated. Gasum, St1 Biokraft, Tekniska verken, and a small group of other scaled operators are building positions in LBG and upgraded biomethane. At the same time, many municipal utilities and farm-linked projects still produce for local use or for smaller distribution footprints. This means a single dominant supplier does not control the market. Yet, scale matters more than before because new investment is increasingly tied to liquefaction, upgrading, and large feedstock contracts. In the Sweden renewable gas from waste market, access to capital and infrastructure now separates the leading expansion players from operators that mainly defend local niches. That structure supports selective consolidation without removing the role of municipal and cooperative assets.

Gasum is one of the clearest examples of expansion through repeatable project execution. The company opened its Götene plant in January 2025 with 120 GWh of LBG output and, in 2026, made investment decisions for two more large Swedish plants in Hörby and Sjöbo.[3]Gasum, “Gasum Opens New Biogas Plant in Götene, Sweden,” Gasum, gasum.com St1 Biokraft is following a similar scale strategy through Nordic LBG investments and infrastructure additions, such as the Stockholm pipeline, inaugurated in 2026, which more than doubled LBG production capacity in the greater Stockholm region. Tekniska verken has taken another route by expanding its Linköping site and adding food-certified bio-CO2 recovery, which improves overall plant economics rather than only increasing gas volume. These moves show that leadership in this market can come from scale, asset integration, or higher value capture from each unit of feedstock.

Technology and infrastructure partnerships are becoming a second competitive screen in the Sweden renewable gas from waste market. EnviTec Biogas entered Sweden with its EnviThan upgrading platform and is also linked to the BVS project in Vara, demonstrating how technology suppliers are moving closer to project development rather than remaining solely equipment vendors. Nordion Energi’s green grid strategy and its Gothenburg liquefaction investment create another kind of advantage because producers connected to those systems gain access to broader off-take routes. Smaller operators still hold a defensible position, as they control local feedstock and maintain municipal relationships. Still, they are less likely to lead the next wave of large greenfield LBG assets. The competitive direction, therefore, points toward a market in which a few well-financed developers shape capacity growth. At the same time, a broader group of local operators remains important for collection, processing, and regional supply.

Sweden Renewable Gas From Waste Industry Leaders

Gasum Oy

St1 Biokraft AB

Aneo Biogas Sverige AB

Tekniska verken i Linköping AB

Stockholm Exergi AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: St1 Biokraft inaugurated a new gas pipeline connecting its facilities in Henriksdal (Nacka) and Gladö Kvarn (Huddinge) via the Stockholm gas network, more than doubling liquefied biogas production capacity in the greater Stockholm region and strengthening regional fossil-free fuel security of supply.

- April 2026: Naturvårdsverket reported a rising number of applications to Klimatklivet for combined biogas and bio-CCU facilities, including a SEK 27 million (USD 2.9 million) grant to Biogas Västra Skaraborg to capture and commercialize biogenic CO2 as an additional revenue stream alongside LBG production.

- March 2026: Gasum's Board of Directors made investment decisions on two additional large-scale biogas plants in Sweden, one in Hörby, Skåne, planned to start production in 2028, and one in Sjöbo, planned for 2029, in support of the company's strategic goal of supplying 7 TWh of renewable gas annually to Nordic customers by 2027.

- December 2025: Sweden's government issued a directive enabling farm-scale biogas for electricity and heat to again receive Klimatklivet support from 2026, with the program's appropriation proposed at SEK 4.5 billion (USD 489.7 million) for 2026 and an authorization ceiling of SEK 8 billion (USD 870.6 million).

Sweden Renewable Gas From Waste Market Report Scope

The Sweden Renewable Gas From Waste Market is Segmented by Feedstock (Municipal Solid Waste, Food Waste, Animal Manure, and More), by Technology (Anaerobic Digestion, Gasification, and More), by Gas Type (Biogas, Syngas, and More), by Application (Electricity Generation, Grid Injection, and More), and by Component (Gas Collection, Digesters & Fermentation, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Municipal Solid Waste (MSW) |

| Agricultural Residues |

| Animal Manure |

| Industrial Organic Waste |

| Sewage Sludge |

| Food Waste |

| Others |

| Anaerobic Digestion |

| Landfill Gas Recovery |

| Gasification |

| Pyrolysis |

| Biogas Upgrading Systems |

| Others |

| Biogas |

| Biomethane/Renewable Natural Gas (RNG) |

| Syngas |

| Electricity Generation |

| Combined Heat & Power (CHP) |

| Grid Injection |

| Transportation Fuel |

| Industrial Heating |

| Residential & Commercial Heating |

| Others |

| Gas Collection Systems |

| Digesters & Fermentation Systems |

| Gas Processing & Upgrading Units |

| Compressors & Storage Systems |

| Power Generation Equipment |

| Monitoring & Control Systems |

| Others |

| By Feedstock | Municipal Solid Waste (MSW) |

| Agricultural Residues | |

| Animal Manure | |

| Industrial Organic Waste | |

| Sewage Sludge | |

| Food Waste | |

| Others | |

| By Technology | Anaerobic Digestion |

| Landfill Gas Recovery | |

| Gasification | |

| Pyrolysis | |

| Biogas Upgrading Systems | |

| Others | |

| By Gas Type | Biogas |

| Biomethane/Renewable Natural Gas (RNG) | |

| Syngas | |

| By Application | Electricity Generation |

| Combined Heat & Power (CHP) | |

| Grid Injection | |

| Transportation Fuel | |

| Industrial Heating | |

| Residential & Commercial Heating | |

| Others | |

| By Component | Gas Collection Systems |

| Digesters & Fermentation Systems | |

| Gas Processing & Upgrading Units | |

| Compressors & Storage Systems | |

| Power Generation Equipment | |

| Monitoring & Control Systems | |

| Others |

Key Questions Answered in the Report

What is the expected value of the Sweden renewable gas from waste market by 2031?

The report projects the sector to reach USD 1.02 billion by 2031, rising from USD 0.66 billion in 2026 at a 9.1% CAGR.

What is driving growth in renewable gas from waste across Sweden?

The main supports are the restored biogas tax exemption, mandatory bio-waste separation, continued Klimatklivet funding, and rising LBG demand from heavy transport.

Which feedstock leads revenue generation in Sweden?

Municipal solid waste accounted for 30.8% of revenue in 2025, driven by Sweden's established municipal collection base and stronger sorting rules introduced in 2024.

Which application is growing the fastest in this sector?

Grid injection is the fastest-growing application with a 14.1% CAGR through 2031, supported by Nordion Energi’s connection strategy and more producer interest in upgraded gas.

Why is liquefied biogas important for Sweden’s transport transition?

LBG demand rose strongly in 2024 because it fits long-haul freight better than many other low-carbon options and can serve road transport, maritime, and off-grid industrial users.

What is the main challenge holding back faster expansion?

The biggest constraint is the gap between current domestic output of 2.4 TWh and the 10 TWh ambition for 2030, combined with uneven infrastructure access and limited long-term policy visibility.

Page last updated on: