Germany 3PL Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

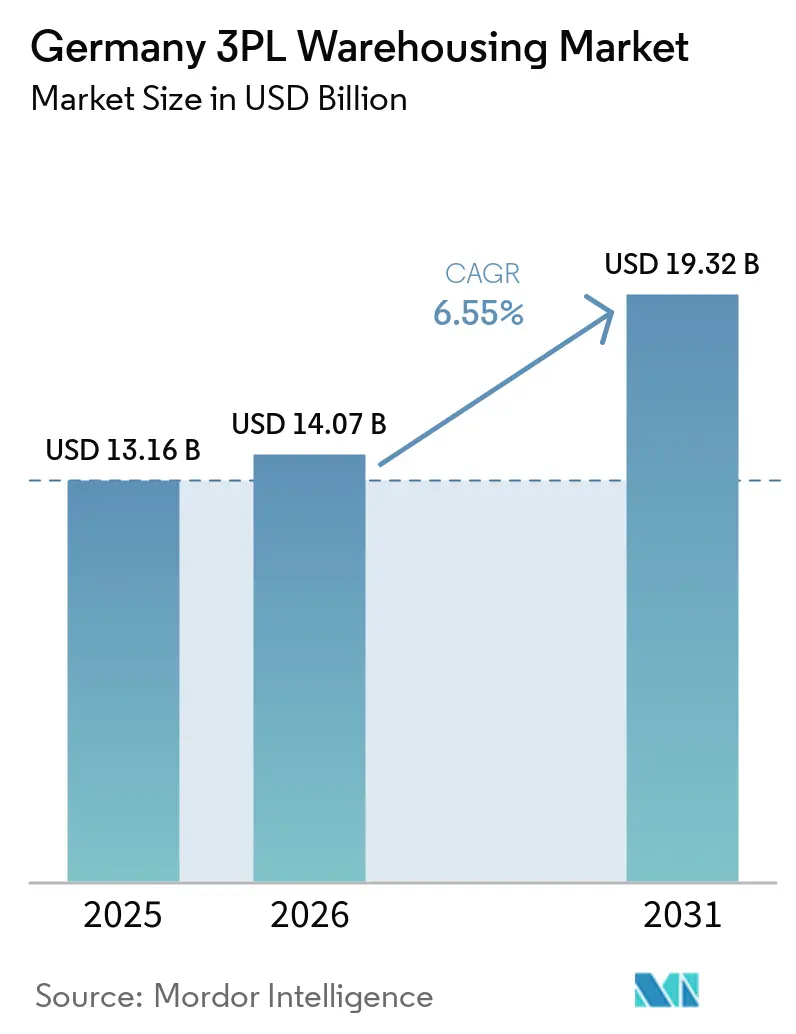

| Base Year Market Size (2025) | USD 13.16 Billion |

| Market Size (2026) | USD 14.07 Billion |

| Market Size (2031) | USD 19.32 Billion |

| Growth Rate (2026 - 2031) | 6.55% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany 3PL Warehousing Market Analysis by Mordor Intelligence

The Germany 3PL warehousing market size was valued at USD 13.16 billion in 2025 and is projected to grow from USD 14.07 billion in 2026 to reach USD 19.32 billion by 2031, growing at a CAGR of 6.55% during 2026-2031.

The Germany 3PL warehousing market continues to benefit from the country’s role as Europe’s manufacturing and transit backbone, with borders to 9 countries and a central position across the Frankfurt, Hamburg, and Rhine-Ruhr logistics triangle, where supply remains tight and prime logistics space commands some of the continent’s highest rents. This cycle differs from the pre-2020 pattern because post-pandemic inventory buffering, faster e-commerce fulfillment, and rising pharmaceutical cold-chain demand are all exerting pressure on warehouse capacity simultaneously. Logistics take-up across Germany’s top 7 markets reached 1.3 million sqm in H1 2025, while prime vacancy in Munich and Frankfurt stayed below 3%, which kept occupiers focused on longer lease terms and automation-ready buildings. The Germany 3PL warehousing market is also being shaped by the need for more specialized facilities, especially where compliance, temperature control, and late-stage customization are now part of the contract scope rather than add-on services. Competition remains moderate rather than highly consolidated, but the DSV and Schenker integration, energy limits in urban hubs, and long development timelines are changing how providers choose locations and commit capital.

Key Report Takeaways

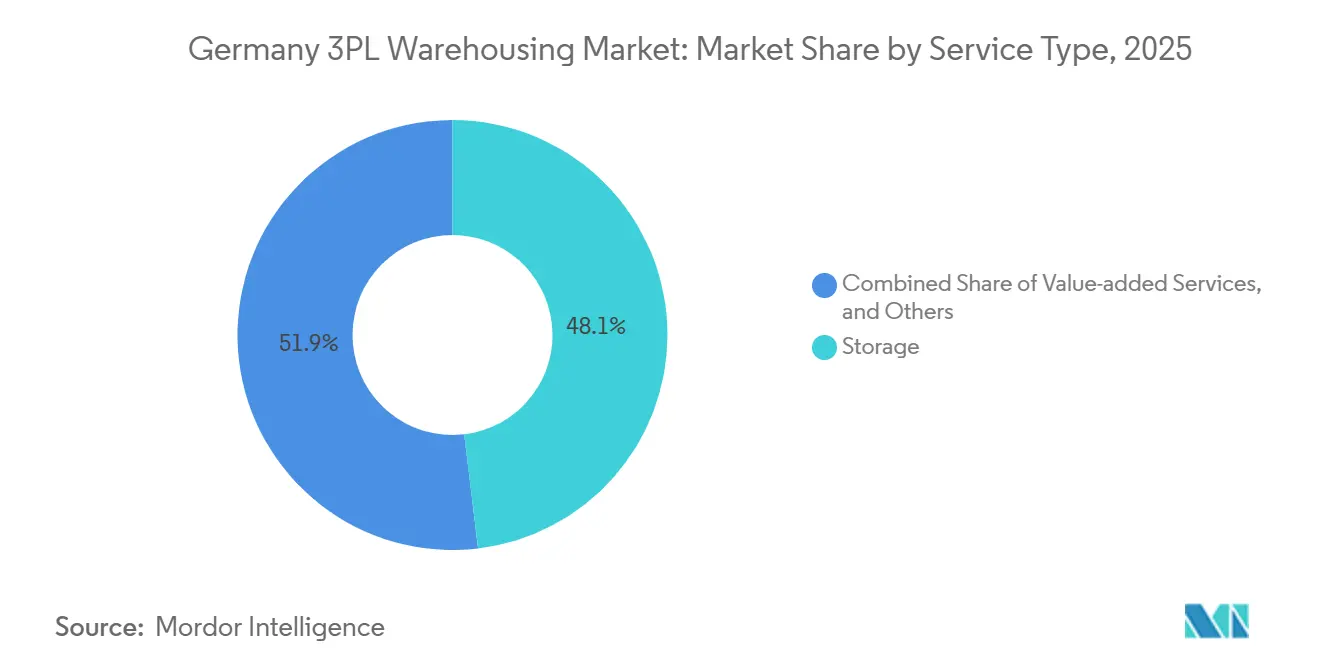

- By service type, storage services held 48.11% of the Germany 3PL warehousing market share in 2025, while value-added services and others are forecast to expand at a 9.38% CAGR through 2031.

- By warehouse type, general shared and multi-client warehousing accounted for 54.83% of the Germany 3PL warehousing market size in 2025, while dedicated contract warehousing is projected to grow at an 8.55% CAGR through 2031.

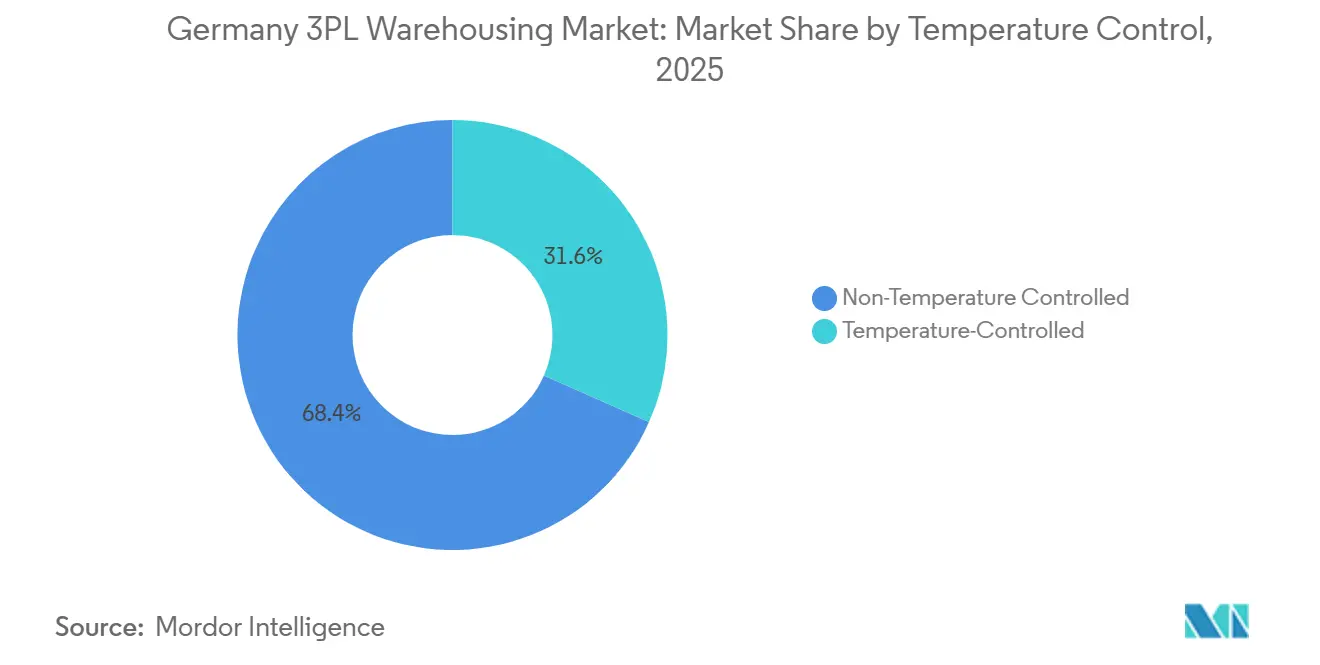

- By temperature control, non-temperature-controlled facilities led with 68.37% market share in 2025, while temperature-controlled warehousing is set to advance at a 10.26% CAGR through 2031.

- By technology adoption, manual operations held 49.4% market share in 2025, while fully automated warehousing is expected to record the highest growth at 12.23% CAGR through 2031.

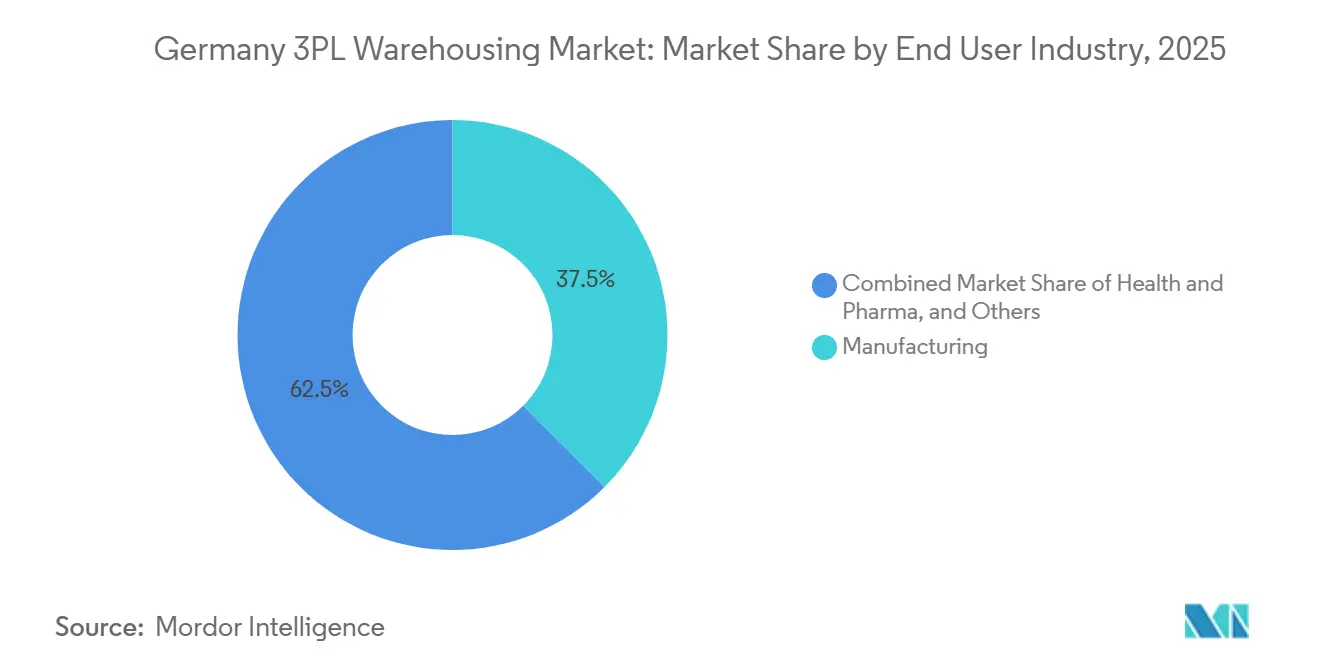

- By end user industry, manufacturing captured 37.5% market share in 2025, while healthcare and pharma is expected to grow at a 9.69% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany 3PL Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Same-/Next-Day Fulfilment Pressure | +1.2% | National, with concentration in Rhine-Ruhr, Frankfurt/Rhine-Main, Hamburg, and Munich metropolitan corridors | Short term (≤ 2 years) |

| Pharmaceutical Biologics Cold-Chain Boom | +1.0% | National, focal points in Rhine-Main, Rhineland-Palatinate, and Bavaria | Medium term (2-4 years) |

| Near-Shoring of Automotive Tier-1 Suppliers | +0.6% | Baden-Württemberg, Bavaria, Lower Saxony, and Thuringia industrial corridors | Medium term (2-4 years) |

| Automation ROI Rise Amid Labor Shortages | +0.7% | National, most acute in Rhine-Ruhr, Hamburg, Munich, and Berlin | Long term (≥ 4 years) |

| Rapid Adoption of Carbon-Neutral Warehouse Standards | +0.4% | Global, with early gains in Hamburg, Leipzig-Halle, Rhine-Ruhr, and Rhineland | Medium term (2-4 years) |

| Digital Marketplace Platforms for On-Demand Space | +0.3% | National, with spill-over to adjacent DACH markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-Commerce Same-/Next-Day Fulfillment Pressure

The Germany 3PL warehousing market is seeing stronger fulfillment pressure because online retail demand now depends as much on delivery speed and returns handling as on basic storage. Germany’s online retail market generated EUR 80.6 billion (USD 87.0 billion) in 2024 and served 68 million online shoppers, with average annual spend reaching EUR 2,200 (USD 2,376) per shopper. Next-day delivery has become the normal service expectation in categories such as apparel, electronics, and beauty, and same-day service is moving from a premium option to a competitive differentiator in dense urban areas. Returns matter just as much as outbound speed because Germany continues to record very high fashion return rates, which means reverse logistics capacity is now a core warehouse function rather than an optional add-on. This is pushing operators toward sites near major population centers even when rents are high and new land is scarce. As urban greenfield options tighten, large brownfield retrofits and edge-of-city nodes are becoming a more practical route for operators that still need scale and fast cut-off windows[1]"Aktionsplan Güterverkehr und Logistik – nachhaltig und effizient in die Zukunft." Bundesministerium für Verkehr (BMV, bundesregierung.de/breg-de/suche/aktionsplan-gueterverkehr-und-logistik-nachhaltig-und-effizient-in-die-zukunft.

Pharmaceutical Biologics Cold-Chain Boom

The Germany 3PL warehousing market is getting a strong lift from pharmaceutical logistics because biologics, biosimilars, and specialty therapies need stricter storage control than conventional products. DHL Group opened Florstadt 4 in May 2025 as a 30,000 sqm multi-temperature warehouse, which expanded the Florstadt health logistics campus to 100,000 sqm and more than 140,000 pallet positions. The rise of temperature-sensitive products is changing procurement behavior because GDP and GMP compliance now play a direct role in contract awards and renewals. This shift is also raising the value of digitally auditable, multi-temperature, and certified facilities, since biopharma clients want fewer weak points across storage, handling, and release processes. Vetter Pharma’s EUR 150 million (USD 163.5 million) expansion in Ravensburg, which adds 16,000 pallet positions and targets 68,000 positions by 2028, also points to rising demand for outsourced overflow, buffer storage, and support capacity around manufacturer-owned sites. The result is that cold-chain warehousing is no longer a niche within the Germany 3PL warehousing market, but a faster-growing layer that increasingly shapes network planning.

Near-Shoring of Automotive Tier-1 Suppliers

The Germany 3PL warehousing market is also benefiting from automotive supply chain reconfiguration, as OEMs continue to reduce dependence on long and volatile inbound flows. Mercedes-Benz’s 130,000 sqm International Consolidation Centre in Bischweier, operated by Seifert Logistics, was designed to receive, bundle, and pre-assemble components from regional suppliers before global distribution, with handling capacity estimated at 440 inbound and outbound trucks per day at full ramp. This kind of operating model increases demand for dedicated sequencing and contract warehousing rather than simple pallet storage. It also favors providers that can support just-in-time and just-in-sequence flows close to automotive corridors in Baden-Württemberg, Bavaria, Lower Saxony, and Thuringia. Germany’s industrial base remained under pressure in 2024, but near-shoring still supported local warehousing demand because more suppliers and assemblers wanted regional inventory buffers after repeated disruptions. That is why dedicated capacity is outgrowing shared space in the automotive-facing part of the Germany 3PL warehousing market.

Automation ROI Rise Amid Labor Shortages

The Germany 3PL warehousing market is moving further toward automation because labor shortages are raising the cost of keeping manual facilities reliable at scale. Manual operations still accounted for 49.4% of the market in 2025, but fully automated warehousing is expected to grow at 12.23% annually through 2031, which makes it the fastest-growing technology segment in the current forecast period. This transition is being pushed by the need for steady throughput, more consistent picking accuracy, and a lower dependence on hard-to-fill warehouse roles. It is also widening the gap between larger providers and smaller regional operators because automation requires capital, integration capability, and a stronger engineering support base. The commercial case becomes clearer when warehouse operators need to serve round-the-clock e-commerce, cold-chain, or contract logistics programs without service disruption. In practice, automation is becoming part of how large providers defend margins and service levels in the Germany 3PL warehousing market[2]"EURES Report on labour shortages and surpluses 2024 – Germany shortage occupations." Europäische Kommission (EURES), ela.europa.eu/sites/default/files/2025-06/EURES_Report_on_labour_shortages_and_surpluses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity and Cost of Prime Industrial Land in Hub Cities | -0.5% | National, most acute in Munich, Frankfurt, Düsseldorf, Hamburg, and Berlin | Long term (≥ 4 years) |

| Rising Electricity Prices for Temperature-Controlled Sites | -0.4% | National, with early pressure in Berlin, North Rhine-Westphalia, and Bavaria | Medium term (2-4 years) |

| Strict GDP/GMP Audits Delaying Pharma Warehouse Onboarding | -0.3% | National, particularly Frankfurt/Rhine-Main and Bavaria pharma clusters | Medium term (2-4 years) |

| Fragmented SME 3PL Base Slowing Uniform Tech Adoption | -0.3% | National, with high concentration in Central and Eastern Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity and Cost of Prime Industrial Land in Hub Cities

The Germany 3PL warehousing market faces a structural land problem because the tightest logistics corridors are also the ones where demand is strongest. Prime logistics rents in 2025 reached EUR 11.0 per sqm per month (USD 12.0) in Munich, EUR 8.7 (USD 9.5) in Frankfurt, and EUR 8.5 (USD 9.3) in Stuttgart, which confirms that core hubs remain supply-constrained. The long-run space gap is becoming more difficult to close because land-use policy is tightening at both German and EU levels. Brownfield redevelopment offers one route forward, but it brings contamination risk, fragmented ownership, and longer remediation periods, which slow project delivery. This issue is most severe for mid-sized operators that cannot pre-emptively acquire land or finance more complex formats. Over time, land scarcity is likely to keep the Germany 3PL warehousing market tilted toward larger providers with stronger balance sheets and deeper developer relationships.

Rising Electricity Prices for Temperature-Controlled Sites

The Germany 3PL warehousing market faces a clear cost challenge in temperature-controlled warehousing because refrigeration and climate control consume a large share of site electricity. Loxxess reduced electricity costs by more than 10% in 2025 by shifting from fixed-price purchasing toward a hybrid energy model that combined direct power purchase agreements with flexible spot-market procurement, while also avoiding 1,900 tons of CO2. That example shows the scale of the problem, because only operators with stronger energy management capabilities can soften volatility without putting service reliability at risk. Grid saturation in some urban areas adds another constraint, especially for automated and temperature-controlled buildings that need more dependable power access. The transition under electricity market reform may support long-term procurement visibility, but near-term exposure to price swings remains a real issue for cold-chain operators. This keeps energy strategy tightly linked to site selection in the Germany 3PL warehousing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Services Redefining Contract Scope

Storage services held 48.11% of the Germany 3PL warehousing market share in 2025, which reflects the continued need for inventory buffering across automotive, retail, and consumer goods supply chains. Distribution and inventory management remain essential because they connect warehouse capacity with pick-pack execution, transport planning, and stock visibility across national networks. Value-added services and others are projected to expand at a 9.38% CAGR through 2031, well above the overall rate and indicating that contract scope is moving beyond basic space provision. This part of the Germany 3PL warehousing market is growing because clients want late-stage customization without taking on their own site, labor, and systems costs. Kitting, labeling, returns processing, and co-packing now sit closer to the center of warehouse economics than they did a few years ago.

That shift is being driven by two pressures at once. E-commerce orders need more unit-level handling, tailored packaging, and faster returns workflows, while healthcare products need tighter documentation and more controlled handling procedures. Germany’s packaging and producer responsibility rules also make compliant labeling and preparation services more valuable for customers that want a single outsourced workflow. This is where reputable operators can build better margins, since certified and process-heavy work is harder to replace than standard storage. The Germany 3PL warehousing industry is therefore moving toward contracts where labor content, systems integration, and compliance execution all matter more. Operators with proven capability in consumer electronics and healthcare are better placed to capture this premium layer of demand.

By Warehouse Type: Dedicated Contracts Gaining as Compliance Requirements Tighten

General shared and multi-client warehousing accounted for 54.83% of the German 3PL warehousing market size in 2025, underscoring how strongly shippers still value capital efficiency and national reach. Multi-client buildings remain attractive because they allow 3PL providers to spread fixed costs across multiple customers and varying seasonal demand patterns. This model is especially useful in e-commerce and FMCG, where peak patterns move quickly and overflow flexibility matters. FIEGE’s 55,000 sqm Hamminkeln project and 52,000 sqm Hessisch Lichtenau project, both targeted for autumn 2026, show that multi-user capacity is still being added in carefully selected nodes. For many occupiers, shared warehousing remains the most practical route into the Germany 3PL warehousing market.

Dedicated contract warehousing remains the fastest-growing warehouse type, with a 8.55% CAGR through 2031, as some customers cannot operate in shared environments. Pharmaceutical, automotive, sequencing, and hazardous-goods users need stronger process control, contamination separation, or security arrangements than a general multi-client site can provide. That requirement increases the value of purpose-built facilities and longer contract terms. It also raises entry barriers because validation, engineering design, and customer approval become more demanding. Bonded warehousing remains smaller, but it is becoming more relevant for non-EU flows entering Germany’s port system as customs documentation and clearance requirements tighten. This leaves the Germany 3PL warehousing market with a dual structure where shared space leads on volume and dedicated space leads on compliance-driven growth.

By Temperature Control: Cold-Chain Capacity Race Sets New Benchmarks

Non-temperature-controlled warehousing represented 68.37% of the Germany 3PL warehousing market share in 2025, which reflects the wide ambient-storage needs of manufacturing, retail, e-commerce, and general consumer goods. Temperature-controlled space remains smaller in base, but it is projected to grow at 10.26% CAGR through 2031, making it one of the strongest growth pockets in the full market. This reflects rising demand for biologic medicines, food cold-chain networks, and mixed-use campuses that can serve multiple temperature bands from a single site. The growth profile also shows that cold-chain capability is moving from a specialist add-on to a core infrastructure in selected customer verticals. In this part of the Germany 3PL warehousing market, facility design and handling discipline matter just as much as simple cubic capacity.

The operational gap between certified cold-chain providers and basic refrigerated storage operators is widening. Trans-o-flex reported that untempered vehicles exposed to 23 °C ambient conditions could see internal cargo temperatures exceed 50 °C, which supports shipper demands for active monitoring across loading, transit, and unloading rather than only in static storage. GEODIS strengthened its position in February 2025 by receiving GDP certification for pharmaceutical ocean freight in Hamburg, complementing its CEIV Pharma-certified air freight operation in Frankfurt and creating certified coverage across both key modes[3]"Good Distribution Practice (GDP) – Guidelines on Good Distribution Practice of medicinal products for human use." European Medicines Agency (EMA), ema.europa.eu/en/medicines/human/overview-good-distribution-practice-guidelines. That kind of end-to-end compliance reduces handoff risk in pharmaceutical logistics. It also gives certified providers a stronger case when customers review network integrity rather than individual warehouses in isolation. This is why temperature control is becoming one of the clearest differentiation points in the Germany 3PL warehousing market.

.

By Technology Adoption: Automation Economics Accelerating Transition

Manual warehouse operations held 49.4% market share in 2025, which means the Germany 3PL warehousing market is still running a large installed base of labor-intensive sites. Semi-automated facilities occupy the middle ground, where operators add guided picking, conveyors, and warehouse management tools without fully rebuilding the site around robotics. Fully automated warehousing is forecast to expand at 12.23% CAGR through 2031, which makes it the highest-growth technology segment in the current structure. That trend reflects the need for consistent throughput, fewer process errors, and better labor resilience in high-volume contracts. It also shows that automation is spreading from showcase sites into mainstream contract logistics planning.

The biggest limit is no longer only equipment availability. Operators also need systems integrators, planners, and service teams that can deploy and support automation after go-live. GEODIS’s 80,000 sqm automated high-bay pallet warehouse south of Hamburg, with 120,000 pallet positions across 12 levels and annual throughput above 1.5 million pallets, shows the scale at which automation can become a core operating model. Large providers can absorb those requirements more easily because they have stronger procurement leverage and better access to customer volumes. Smaller firms often move more cautiously and remain in the semi-automated layer for longer. As a result, the Germany 3PL warehousing market is likely to see a wider productivity gap open between top-tier and mid-tier operators over the forecast period[4]"46 meters high, 80,000 pallet spaces – Largest fully automated high bay warehouse in Belgium." Warehousing Logistiek, warehouselogistiek.eu/en/automation/46-meters-high-80-000-pallet-spaces/.

By End User Industry: Healthcare Premium Over-Indexes While Manufacturing Holds the Base

Manufacturing retained 37.5% market share of the Germany 3PL warehousing market in 2025, which confirms that factory-linked logistics remains the anchor demand pool for the country. Manufacturing customers continue to outsource inbound sequencing, production support, and finished-goods storage to specialist providers that can scale more efficiently than in-house networks in many cases. Consumer goods, food and beverage, and retail-linked fulfillment add another steady layer of volume and keep multi-client networks well utilized. This broad base matters because it provides the revenue stability that lets operators invest in more specialized capabilities elsewhere. In practical terms, manufacturing continues to give the Germany 3PL warehousing market its largest demand foundation.

Healthcare and pharma is forecast to grow at 9.69% CAGR through 2031, which makes it the fastest-growing end-user vertical in the current segmentation. Pharmaceutical manufacturers are increasingly treating GDP and GMP-compliant 3PL warehousing as a strategic capability rather than a commodity purchase. That raises the value of documentation systems, traceability, validated handling, and clean operating procedures across the warehouse estate. It also opens room for adjacent demand in areas such as cell therapy logistics and EV battery-related reverse flows, where safety, documentation, and specialist handling become more important. The Germany 3PL warehousing industry is therefore becoming more polarized between large-volume baseline sectors and smaller but higher-value specialist verticals. Operators that can balance those two demand types are likely to preserve utilization while improving contract quality.

Geography Analysis

The Germany 3PL warehousing market remains geographically concentrated around a small number of strategic corridors, with Rhine-Ruhr, Frankfurt and Rhine-Main, Hamburg and Bremen, and Munich and Bavaria carrying most of the commercial weight. In 2025, take-up across Germany’s top 7 logistics markets reached 5.2 million sqm, with the Ruhr area leading at 528,000 sqm, followed by Frankfurt and Rhine-Main at 485,000 sqm and Berlin at 431,000 sqm. North Rhine-Westphalia remains the single largest logistics real estate cluster because it combines dense motorway access, Benelux connectivity, and proximity to Duisburg’s inland port system. Frankfurt and Rhine-Main retain a strong role because they connect national road flows, air cargo, and pharmaceutical traffic in one corridor. Munich and the southern belt continue to operate in the tightest supply conditions, with rents moving higher as occupiers compete for scarce modern stock.

Leipzig-Halle is the clearest growth geography because it offers lower rents, strong multimodal links, and more room for large-format development than the saturated western hubs. Prime rents there stood at EUR 5.9 per sqm per month (USD 6.4) in 2025, which kept the location cost-competitive even as other major markets tightened. DHL Supply Chain’s third Leipzig-Halle campus node, opened in November 2025, reflects how large providers are using eastern Germany to complement tighter western networks while still supporting fast cut-off operations through Leipzig Airport. The Hamburg and Bremen gateway also holds a distinct role in pharmaceutical and maritime logistics because cold-chain handling and port access meet in one regional system. GEODIS’s GDP-certified pharmaceutical ocean freight operation in Hamburg supports that positioning and reduces the need for certified handoffs between ocean and inland logistics.

A two-speed pattern is becoming more visible across the country. Western and southern Germany are defined by land scarcity, very tight vacancy, and a stronger push toward automation or higher-density formats. Eastern Germany offers more developable land and lower rents, but it can be harder to scale technical and engineering labor at the same speed as new warehouse investment. Maersk’s lease of the full 71,800 sqm Panattoni Park Bad Hersfeld Ost, due to operate from August 2026, shows that international players still view Germany as a core European distribution location despite rising cost pressure. Across all regions, tighter land-use targets mean greenfield supply will remain limited, which makes brownfield redevelopment and disciplined site selection more important across the Germany 3PL warehousing market.

Competitive Landscape

The Germany 3PL warehousing market is moderately concentrated, with DHL Supply Chain, DACHSER, DSV including Schenker, Rhenus, and Kuehne+Nagel forming the leading group while a large mid-tier of German specialists and international challengers remains active. The largest providers benefit from scale in contract logistics, transport integration, customer coverage, and capital spending, but they do not operate in a winner-takes-all structure. This keeps pricing discipline important and leaves space for regional specialists in automotive, healthcare, food logistics, and multi-user operations. The most important strategic move in 2025 was DSV’s EUR 14.3 billion (USD 15.6 billion) acquisition of DB Schenker, which created a much larger combined logistics network and sharply increased DSV’s German footprint. DSV’s investor material also showed that the integration would triple its employee count in Germany, which underlines how much the local competitive balance has shifted.

Large providers are also competing through facility quality rather than only through network size. DHL Supply Chain has pushed carbon-neutral and DGNB Gold-certified capacity in Leipzig-Halle and Rheinbach, which strengthens its appeal in tenders where sustainability and operating standards are screened alongside price. Kuehne+Nagel’s lease for a new 7,600 sqm air cargo warehouse in Frankfurt CargoCity South shows another route to competitive positioning, where specialized air cargo capacity supports healthcare, semiconductor, and data center-linked flows. FIEGE’s recent investments in new multi-user sites and sustainability systems show how strong mid-tier operators are still finding room to expand within selected niches. The market therefore remains open enough for differentiated models to work, even as scale advantages clearly matter more than before.

The most attractive white space still sits in specialist areas where standard warehousing is not enough. Mid-sized GDP-compliant cold-chain facilities, urban micro-fulfillment, and reverse logistics for EV battery systems all remain less saturated than mainstream shared storage. That supports providers that can combine compliance, automation, and customer-specific handling without having to match the full national footprint of the largest groups. The competitive gap is also widening because the largest operators can absorb more of the cost tied to certifications, technology upgrades, and energy investments. Mid-sized firms remain relevant, but they need sharper positioning and stronger partnerships to defend margins. In that sense, the Germany 3PL warehousing market is becoming tougher to enter at scale, while still leaving room for specialists that know where not to compete.

Germany 3PL Warehousing Industry Leaders

-

DHL Group

-

DACHSER

-

FIEGE Logistics

-

Rhenus Logistics

-

Hellmann Worldwide Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: DHL Supply Chain broke ground on a 26,600 sqm carbon-neutral logistics centre in Rheinbach, Rhineland, targeting DGNB Gold and operational by August 2026, with a 1.0 MWp PV system, 229 kW battery storage, and modular design for e-commerce fulfilment or automated solutions.

- February 2026: Kuehne+Nagel signed a lease with Fraport AG for a new 7,600 sqm air cargo warehouse in Frankfurt Airport’s CargoCity South, expanding its total footprint there to more than 20,000 sqm, with the facility due by end-2028 and targeted at healthcare, semiconductor, and cloud-infrastructure logistics.

- January 2026: FIEGE took over logistical process flows for MANN+HUMMEL’s European aftermarket central warehouse in Niederaichbach, expanding the automotive parts 3PL mandate across Southern Germany’s tier-1 supplier network.

- November 2025: DHL Supply Chain opened its third carbon-neutral logistics centre at the Leipzig-Halle Campus, with 34,000 sqm, 55,000 pallet positions, DGNB Gold certification, and more than 450 employees.

Germany 3PL Warehousing Market Report Scope

| Storage |

| Distribution and Inventory Management |

| Value-Added Services and Others (Kitting, Labelling) |

| General Shared / Multi-client Warehousing |

| Dedicated Contract Warehousing |

| Bonded Warehousing |

| Non-Temperature Controlled |

| Temperature Controlled |

| Manual |

| Semi-automated |

| Fully Automated |

| Manufacturing |

| Consumer Goods |

| Food and Beverage |

| Retail and E-commerce |

| Healthcare and Pharma |

| Other End-user Industries |

| By Service Type | Storage |

| Distribution and Inventory Management | |

| Value-Added Services and Others (Kitting, Labelling) | |

| By Warehouse Type | General Shared / Multi-client Warehousing |

| Dedicated Contract Warehousing | |

| Bonded Warehousing | |

| By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | |

| By Technology Adoption | Manual |

| Semi-automated | |

| Fully Automated | |

| By End User Industry | Manufacturing |

| Consumer Goods | |

| Food and Beverage | |

| Retail and E-commerce | |

| Healthcare and Pharma | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the projected value of Germany 3PL warehousing by 2031?

The Germany 3PL warehousing market is projected to reach USD 19.32 billion by 2031, rising from USD 13.16 billion in 2025 at a 6.55% CAGR over 2026-2031.

Which service segment leads in Germany 3PL warehousing?

Storage services led in 2025 with 48.11% share, supported by inventory buffering and the need for more resilient supply chain positioning.

Which warehouse type is growing the fastest in Germany?

Dedicated contract warehousing is the fastest-growing warehouse type, with an 8.55% CAGR through 2031, driven by compliance-heavy sectors such as pharma and automotive sequencing.

Why is cold-chain warehousing expanding faster than ambient space in Germany?

Growth is being driven by biologics, biosimilars, food cold-chain demand, and stricter GDP and GMP handling needs, which push customers toward certified multi-temperature facilities.

How important is automation in German 3PL warehousing?

Automation is becoming central because manual operations still hold 49.4% share, while fully automated warehousing is forecast to grow at 12.23% CAGR through 2031.

Which end-user vertical offers the strongest growth potential?

Healthcare and pharma is the fastest-growing end-user segment at 9.69% CAGR through 2031, reflecting stronger demand for validated cold-chain and regulated storage capability.

Page last updated on: