Germany Finished Vehicle Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

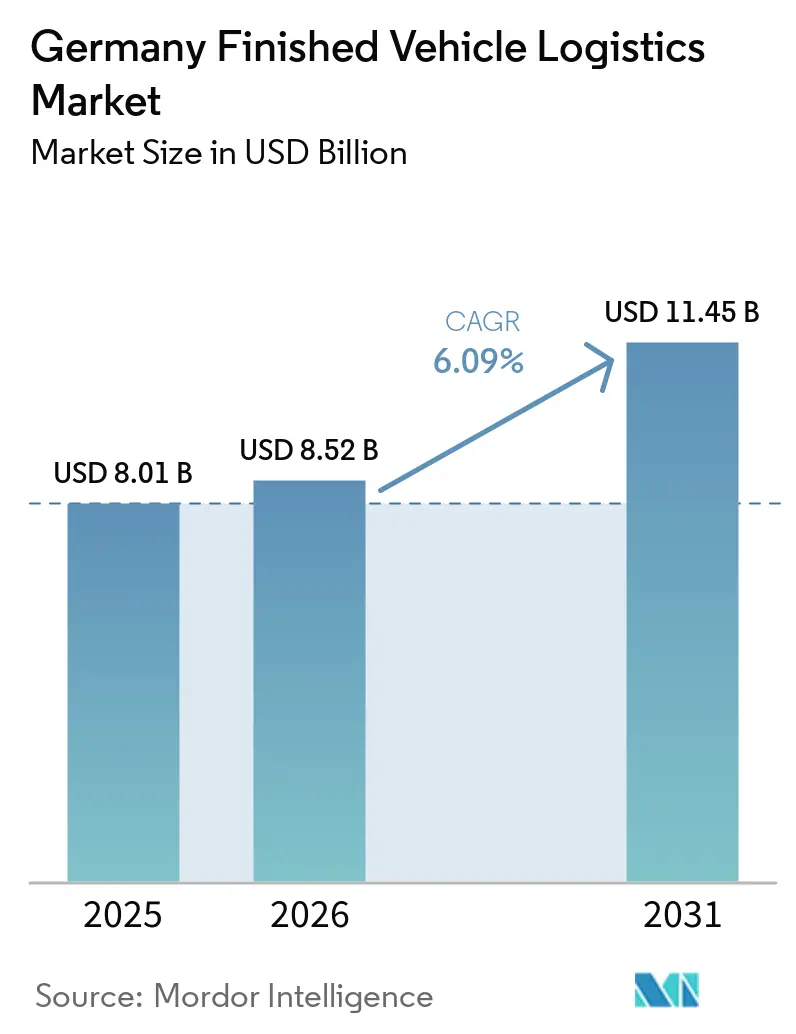

| Base Year Market Size (2025) | USD 8.01 Billion |

| Market Size (2026) | USD 8.52 Billion |

| Market Size (2031) | USD 11.45 Billion |

| Growth Rate (2026 - 2031) | 6.09% CAGR |

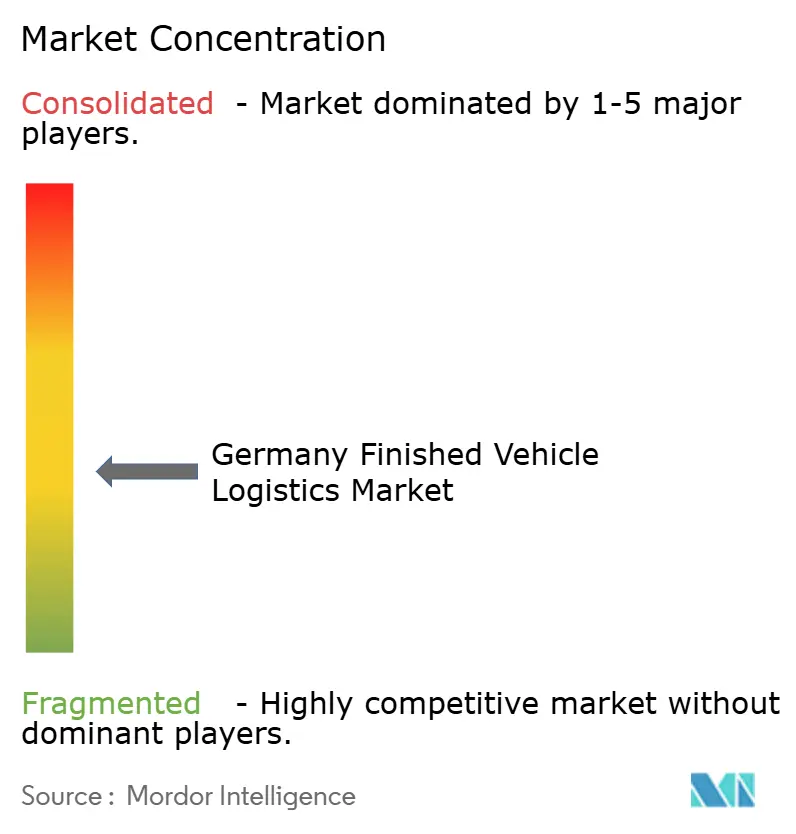

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Finished Vehicle Logistics Market Analysis by Mordor Intelligence

The Germany finished vehicle logistics were valued at USD 8.01 billion in 2025 and are expected to reach USD 8.52 billion in 2026 and USD 11.45 billion by 2031, growing at a CAGR of 6.09% over 2026-2031.

The Germany finished vehicle logistics market is currently undergoing structural transformation as it adapts to declining conventional vehicle volumes and a rapid shift toward electric mobility. The market faces ongoing challenges, including driver shortages, capacity constraints, and the need to reconfigure transport networks to accommodate EV-specific battery-handling requirements. Despite moderate volume pressure from expiring EV subsidies, the market is showing signs of stabilization as electric vehicle sales surge. The future outlook is cautiously positive, driven by rising EV export demand, digitalization of fleet systems, and stronger OEM partnerships with logistics providers. Sustainability mandates and EU environmental regulations are accelerating the adoption of greener supply chain practices, positioning the market for steady long-term expansion despite trade uncertainties.

Key Report Takeaways

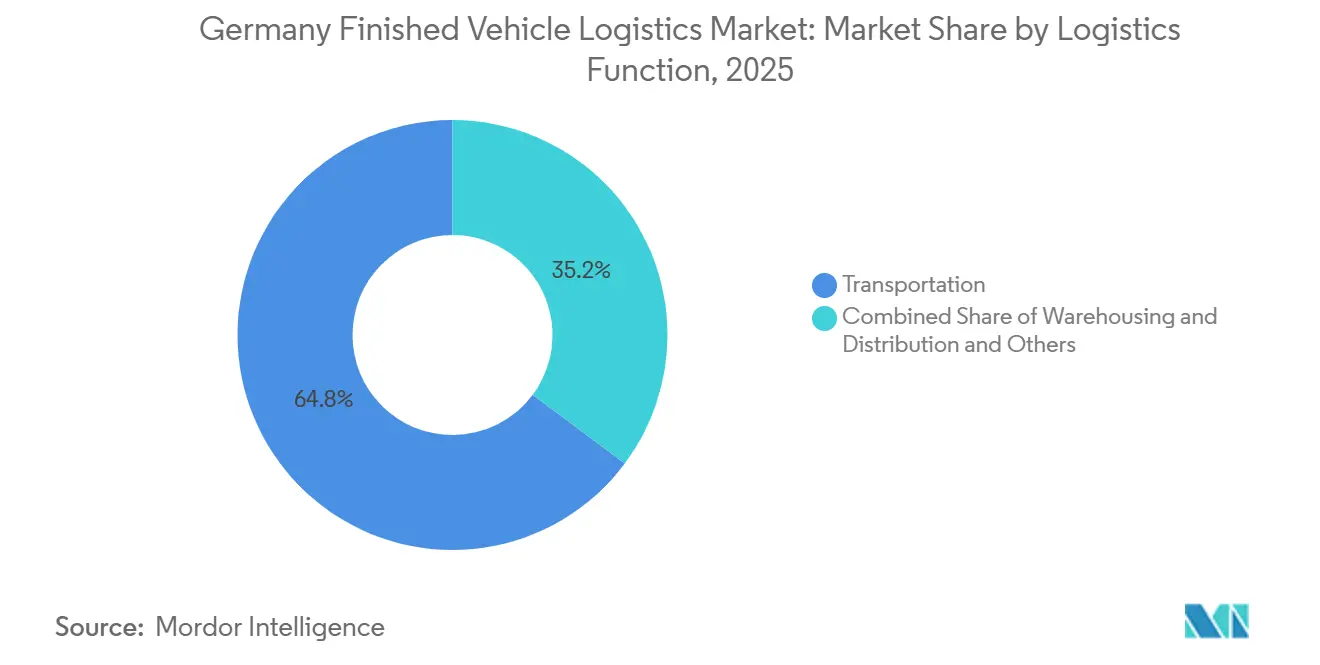

- By logistics function, transportation held 64.86% of the Germany finished vehicle logistics market share in 2025, while warehousing and distribution is projected to expand at 7.84% through 2031.

- By destination, domestic flows held 62.51% of the Germany finished vehicle logistics market share in 2025, while international logistics is forecast to grow at a 7.44% CAGR through 2031.

- By type of vehicles, passenger vehicles, including two-and three-wheelers, accounted for 66.47% of the Germany finished vehicle logistics market size in 2025, and this segment is projected to grow at a 6.52% CAGR through 2031.

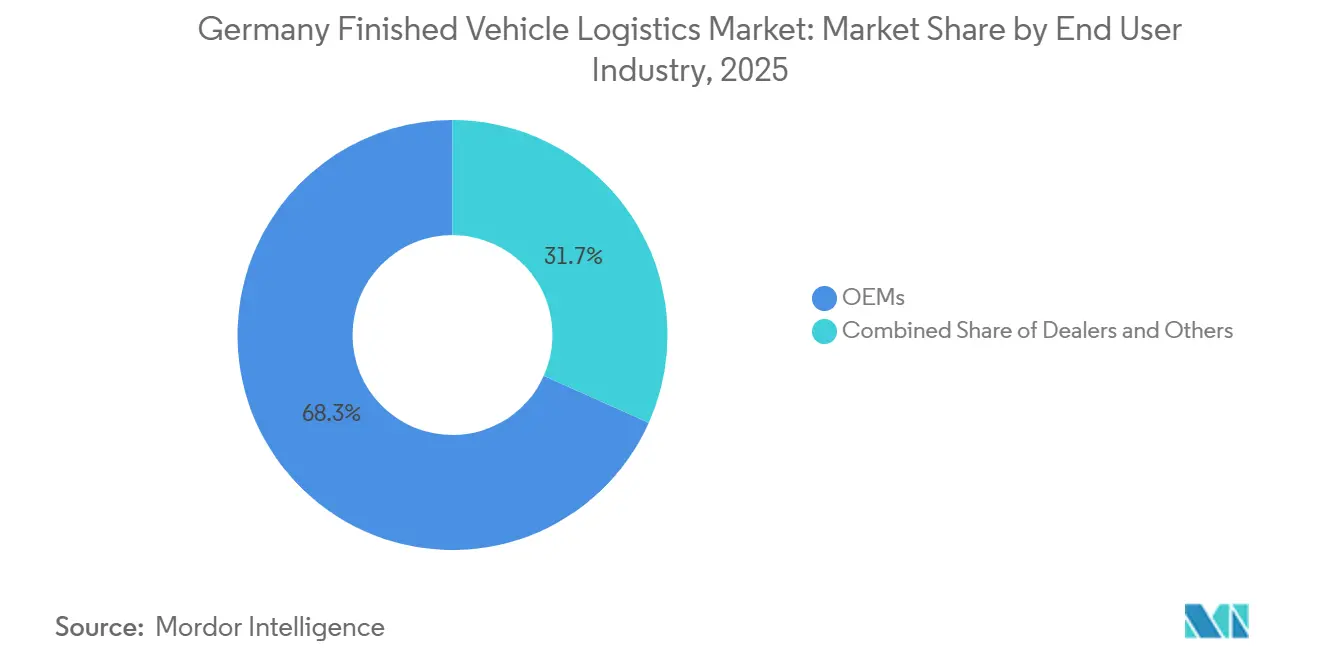

- By end-user industry, OEMs held 68.30% of the Germany finished vehicle logistics market share in 2025, and this segment is projected to expand at a 6.22% CAGR through 2031.

- By region, North Rhine-Westphalia accounted for 34.70% of the Germany finished vehicle logistics market size in 2025, and it is expected to grow at a 7.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Finished Vehicle Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM Demand for Just-in-Sequence Vehicle Deliveries | +0.80% | National, with early gains in North Rhine-Westphalia, Bavaria, and Lower Saxony | Medium term (2-4 years) |

| Rail-Linked Port and Inland Terminal Capacity Expansion | +0.90% | National, concentrated at North Sea ports and major inland hubs | Short term (≤ 2 years) |

| EV-Specific Vehicle Handling and Pre-Delivery Processing Needs | +0.70% | National, with concentration in Bavaria and Baden-Württemberg | Short term (≤ 2 years) |

| Digital Visibility, Damage Reduction, and Exception Management | +0.50% | National, with the strongest effect in OEM outbound flows | Medium term (2-4 years) |

| Low-Emission Logistics Procurement by German OEMs | +0.40% | National | Long term (≥ 4 years) |

| Plant and Port Network Reconfiguration Toward Intermodal Flows | +0.60% | National, with spillover into Belgium and the Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

OEM Demand for Just-in-Sequence Vehicle Deliveries

German automakers continue to run build-to-order production systems that leave little room for sequencing mistakes, so just-in-sequence delivery remains central to finished vehicle logistics contracts and to service design in the Germany finished vehicle logistics market. BMW is preparing its Munich plant for Neue Klasse production from August 2026, following a major plant overhaul[1]Source: BMW Group, “BMW Group Plant Munich, Ready for the Neue Klasse,” BMW Group Newsroom, bmwgroup.com. That change is directly tied to new outbound flow planning as electric and combustion programs share the same manufacturing footprint. Audi is also tightening production and logistics integration through joint Ingolstadt and Gyor activity for the Q3 and through preparations for a new electric model in Ingolstadt, with rail already embedded in body transport between sites. At the provider level, warehouse sequencing, automated movements, and real-time status sharing are no longer optional add-ons; OEMs increasingly expect them as part of standard execution. This makes technology depth more important in carrier selection because a provider now has to prove both physical handling capability and consistent event-level reporting across the vehicle journey. Operators that cannot support synchronized delivery windows and transparent milestone tracking are therefore more likely to lose share in the Germany finished vehicle logistics market when large OEM tenders are reissued.

Rail-Linked Port and Inland Terminal Capacity Expansion

Rail-linked infrastructure is becoming one of the clearest competitive advantages in the Germany finished vehicle logistics market because it reduces truck dependence, supports lower-emission contracts, and improves the quality of long-distance connections between ports and inland compounds. Duisport gives North Rhine-Westphalia an unusually strong position because it handles more than 100 million tons a year across 21 port basins, 10 container terminals, and around 200 kilometers of its own rail network. ARS Altmann AG supports this intermodal shift with more than 4,000 dedicated rail wagons, the largest privately owned vehicle rail fleet in Europe, and a major advantage in plant-to-port transport planning. OBB Rail Cargo Group expanded its Verona-Duisburg service to 10 weekly round trips in 2026, improving west German intermodal connectivity and adding resilience to cross-border automotive flows[2]Source: OBB Rail Cargo Group, “From TransFER Verona Wuppertal to TransFER Verona Duisburg,” Rail Cargo Group, railcargo.com. As more flows are redesigned around intermodal execution, providers with rail access, terminal control, and strong multimodal scheduling are better positioned to capture contract growth. This is raising the value of fixed infrastructure ownership inside the Germany finished vehicle logistics market because access to rail-linked nodes now affects both service reliability and emissions performance.

EV-Specific Vehicle Handling and Pre-Delivery Processing Needs

Electric vehicles have increased handling complexity across the Germany finished vehicle logistics market because compounds now need charging capability, battery-aware safety processes, trained staff, and longer technical checks before retail or fleet handover. CEVA Logistics is building Battery Logistics Centers across 10 European countries by 2027, and the program includes reverse logistics for battery reuse and recycling, which shows how battery-related handling is moving into mainstream logistics design. The same shift is visible at the compound level because EV programs require more structured pre-delivery work than internal combustion vehicles, especially when software updates and charging cycles must be completed before release. These added steps increase dwell time, extend the use of technical bays, and raise the share of revenue that comes from compound services rather than simple transport mileage. That pattern explains why Warehousing and Distribution is outgrowing other functions, even when overall vehicle output is not rising at the same speed. The operational result is that providers with EV-ready compounds and technical processing space are moving into stronger positions in the Germany finished vehicle logistics market than carriers built solely on road delivery.

Digital Visibility, Damage Reduction, and Exception Management

Damage costs, delayed status updates, and unresolved handover disputes continue to shape service quality in the Germany finished vehicle logistics market, making digital visibility tools more central to contract execution than they were a few years ago. Providers are using control towers, connected yards, telematics feeds, and structured exception management to identify where delays or condition issues occur and to shorten claim resolution cycles. Schnellecke Logistics is already linking fleet modernization and broader transport process change through its electric truck rollout, and the same operating model depends on tighter control over asset and shipment status. German OEM programs increasingly require event-level reporting, pushing smaller carriers to integrate digital workflow data to remain part of approved transport networks. This changes competition because the gap between a basic carrier and an integrated operator is now measured as much by data quality as by transport coverage. As a result, platform capability is becoming a real differentiator in the German finished vehicle logistics market, particularly for premium brands and fleet buyers who demand tighter control over damage exposure and delivery timing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rail Slot Scarcity and Long Lead-Time Planning Constraints | -0.60% | National, with the strongest effect on key port corridors | Short term (≤ 2 years) |

| Driver Shortages and Wage Pressure in Road Carrying | -0.80% | National, with heavier strain in eastern German states and road-heavy domestic routes | Short term (≤ 2 years) |

| Infrastructure Bottlenecks Across German Corridors and Ports | -0.50% | National, with a concentration in North Rhine-Westphalia and the North Sea port hinterland | Medium term (2-4 years) |

| Damage Risk, Empty Backhauls, and Asset Underutilization | -0.30% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Driver Shortages and Wage Pressure in Road Carrying

Germany continues to face a shortage of professional drivers, and finished vehicle logistics feels that pressure more sharply because car carrying requires specialized loading, securing, and condition-control skills. This problem affects more than just recruitment because equipment can sit idle even when order books are healthy, lowering asset utilization and slowing service recovery during demand spikes. The pressure is strongest for operators that depend heavily on domestic truck movements, where rate discipline is tight, and route flexibility is limited. Wage inflation and compliance costs also hit smaller regional carriers harder because they have less room to spread cost increases across a broader service mix. These conditions reduce the ability of road-only providers to absorb volume swings or take on more technical work around dealer and fleet deliveries. The driver gap, therefore, acts as a clear near-term restraint on the Germany finished vehicle logistics market, even though it does not alter the longer-term shift toward multimodal, compound-led value creation.

Infrastructure Bottlenecks Across German Corridors and Ports

German logistics infrastructure is under pressure because rail works, port congestion risks, and road constraints are simultaneously affecting the same transport network. North Sea gateway flows remain particularly exposed because both export and import vehicle programs must move through a limited set of ports and hinterland connections that already carry high automotive intensity. When rail reliability declines, road carriers are expected to absorb more volume, but that response is constrained by the same driver shortage already affecting the road transport base. Providers are therefore balancing cost, delivery time, and compound dwell more tightly than before, and that raises execution risk when plants or ports face sudden schedule changes. These network limits also reduce the practical value of low-cost single-mode solutions, as reliability now matters more than headline transport prices alone. In the near term, this makes intermodal flexibility a commercial necessity in the Germany finished vehicle logistics market rather than a purely environmental option.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Transportation Volume Masks a Warehousing-Led Earnings Shift

Transportation held 64.86% of the Germany finished vehicle logistics market share in 2025. Road transport remained the main delivery mode for dealer, leasing, and fleet handovers because last-mile vehicle distribution still depends on flexible truck access across domestic routes. Rail handled the main medium- and long-distance plant-to-port corridors, making asset ownership more valuable for operators who could control capacity directly rather than rely solely on third parties. ARS Altmann AG stood out in this layer with more than 4,000 rail wagons, giving it one of the strongest positions in rail infrastructure across Europe[3]Source: ARS Altmann AG, “Rail Logistics,” ARS Altmann AG, ars-altmann.de. Sea transport and inland waterways remained secondary within Germany itself, but they still supported export and overflow flows tied to major gateway corridors.

Warehousing and distribution is projected to grow at a 7.84% CAGR from 2026 to 2031, making it the fastest-growing logistics function in the Germany finished vehicle logistics market. The reason is not simple storage demand alone because the value shift comes from longer EV pre-delivery routines, software validation, charging readiness, campaign work, and condition-control processes before release. BLG Logistics handled 4.2 million vehicles across its network in 2025, while AutoTerminal Bremerhaven alone processed 1.25 million, underscoring how much compound throughput still matters even in softer production conditions.

By Destination: Domestic Stability Anchors Market While International Flows Accelerate

Domestic flows held 62.51% of the Germany finished vehicle logistics market share in 2025, making them the largest destination category. This volume rested on dealer replenishment, leasing handovers, and fleet deliveries across the country’s dense urban and industrial corridors, where service frequency and handover quality matter as much as basic route coverage. Domestic demand is relatively stable because it is tied to Germany’s large new-vehicle market and to replacement cycles that continue even when export conditions weaken. At the same time, domestic work places more pressure on road-based execution because last-mile delivery windows, driver availability, and condition-sensitive handovers all affect service cost. That is why pure road-haul operators serving this layer are facing tighter margin conditions than multimodal or compound-led providers.

International logistics is forecast to expand at a 7.44% CAGR through 2031, making it the faster-moving destination layer in the Germany finished vehicle logistics market. Export flows remain important because German assembly output still serves wide dealer and distributor networks across Europe and outside Europe, which keeps port access and rail connectivity central to competitive positioning. Import flows are rising faster in this category because more vehicles are arriving from non-German production bases and require inland processing before release into local channels.

By Type of Vehicles: Passenger Vehicles Sustain Volume Leadership While EV Complexity Reshapes Unit Economics

Passenger vehicles, including two- and three-wheelers, captured 66.47% of the Germany finished vehicle logistics market size in 2025 and are projected to grow at a 6.52% CAGR through 2031. Their lead reflects the continued weight of German passenger vehicle production, the scale of premium OEM output, and the growing role of imported EV passenger models that need technical preparation before release.

EV passenger units change the economics of handling because charging, software updates, insurance exposure, and battery-related safety requirements increase the service content per vehicle compared with internal combustion models. Commercial vehicles remain the second-largest segment and require more specialized transport equipment, including low-bed or high-capacity assets for heavier loads and more stringent handling conditions. Off-highway vehicles are the smallest category by volume. Still, they tend to produce higher revenue per unit because compounds and carriers must manage non-standard dimensions, loading methods, and equipment constraints.

By End-user Industry: OEM Concentration Creates Contract Visibility but Amplifies Volume Risk

OEMs held 68.30% of the market in 2025 and are forecast to grow at a 6.22% CAGR through 2031, keeping automakers as the dominant customer group in the Germany finished vehicle logistics market. This reflects the close link between finished vehicle movement and plant scheduling because outbound logistics is still planned around production releases, model mix, dealer allocation, and export timing. Long contract cycles can provide providers with better revenue visibility, especially when transport, compounds, and technical services are bundled into a single agreement. The same structure also creates concentration risk because a change in output, plant strategy, or vehicle technology at one major automaker can quickly affect logistics volumes. BLG’s AutoTerminal Bremerhaven handled 1.25 million vehicles in 2025, demonstrating how changes in automaker throughput can be reflected directly in logistics volumes at scale.

Dealers formed the second tier and usually received vehicles through compounds and controlled delivery networks rather than procuring them themselves. Even so, dealer expectations are becoming more important because EV handover quality, software readiness, vehicle condition, and delivery timing now affect the retail experience more directly than before. The others category, which includes rental, fleet leasing, and public fleets, is evolving faster in service terms because these customers need short, condition-guaranteed delivery cycles and strong tracking discipline. That demand supports providers that can pair inspection quality with reliable scheduling rather than compete only on transport price.

Geography Analysis

North Rhine-Westphalia accounted for 34.70% of the Germany finished vehicle logistics market in 2025 and is projected to grow at a 7.04% CAGR through 2031. The region benefits from the Port of Duisburg, which handles more than 100 million tons each year across 21 port basins, 10 container terminals, and around 200 kilometers of its own rail network. That combination gives NRW a strong role in moving vehicles between North Sea gateways, inland compounds, and central European destinations. OBB Rail Cargo Group expanded its Verona-Duisburg service to 10 weekly round-trip trains in 2026, further strengthening intermodal links into western Germany. The region also benefits from its dense logistics real estate base, which supports compound operations, consolidation, and redistribution work tied to both domestic and imported vehicle programs.

Bavaria held the second-largest regional position because it combines major passenger vehicle production with new EV and battery-linked activity around key automotive clusters. BMW’s Munich plant is preparing for Neue Klasse production from August 2026, which will add new outbound requirements in the second half of the year as plant flows adapt to the new product mix. Audi’s production network around Ingolstadt and Gyor also supports rail-based body movement and closer cross-site coordination for new model programs. These factors keep Bavaria important for higher-value passenger vehicle logistics and for EV-specific processing beyond simple transport.

Baden-Wurttemberg remains important because it anchors premium automaker networks and high-value vehicle flows tied to Porsche and Mercedes-Benz operations. MOSOLF commissioned the first 3.3 MWp phase of a planned 24 MWp photovoltaic parking canopy at Kippenheim in April 2026, which shows how compounds in the state are being adapted for energy-linked vehicle handling and future charging needs.

Competitive Landscape

The Germany finished vehicle logistics market is moderately fragmented at the premium tier, with MOSOLF Group, BLG Logistics Group, and ARS Altmann AG holding visible positions in compound, road, and private rail operations. The broader field remains fragmented because many regional carriers still operate on specific dealer routes, plant corridors, or local fleet handover programs rather than on a national integrated model. This structure means scale matters, but asset ownership matters more because rail wagons, terminal access, EV-ready compounds, and technical processing space are harder to replicate than brokerage capacity. ARS Altmann’s fleet of more than 4,000 rail wagons gives it a durable advantage in rail-based vehicle movements and in multimodal contract execution. BLG Logistics also played a strong network role in 2025, handling 4.2 million vehicles across its system and 1.25 million through AutoTerminal Bremerhaven, which underlines the importance of port-linked terminal scale.

Strategic moves are becoming increasingly infrastructure-led. MOSOLF is deepening its position through energy-linked compound investment, and the Kippenheim photovoltaic canopy shows how vehicle storage space is now being adapted for sustainability, charging support, and broader operating efficiency. CEVA Logistics is building Battery Logistics Centers across 10 European countries by 2027, expanding its role beyond transport into battery compliance, reuse, and reverse logistics support. Schnellecke Logistics is also integrating MAN eTGX electric trucks into its fleet in 2026, following earlier pilots, demonstrating how providers are pairing transport decarbonization with contract renewal and operating model repositioning[4]Source: Schnellecke Logistics, “Schnellecke Logistics Takes the Next Step in Decarbonizing Transport Logistics with Its First Electric Trucks,” Schnellecke Logistics, schnellecke.com..

Large customers are also setting a higher qualification bar. Wallenius Wilhelmsen’s 2025 annual report showed how full sustainability disclosure has become a standard expectation for major vehicle logistics contracts rather than a differentiator used by only a few global players. That matters in Germany because premium OEMs, leasing operators, and international vehicle programs increasingly expect clear reporting on environmental performance and process control from transport partners. The most open competitive space still lies in integrated EV flows that combine port handling, inland compounds, charging, technical readiness, and dealer delivery into a single coordinated system. Another attractive area sits in higher-service fleet and leasing deliveries, where condition control, timing discipline, and live tracking are worth more than the lowest transport tariff. Competitive outcomes in the German finished vehicle logistics market will therefore depend on which companies can combine physical assets, deep technical processing, and transparent data into a single operating model.

Germany Finished Vehicle Logistics Industry Leaders

MOSOLF Group

ARS Altmann AG

BLG Logistics Group

DSV A/S

Duvenbeck Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: MOSOLF Group commissioned the first 3.3 MWp phase of a 24 MWp photovoltaic parking canopy at its Kippenheim compound, built with Swiss energy group Axpo, generating up to 3.7 GWh annually on full completion by end-2026. The 109,000 m², 54,000-module installation will rank among Europe's largest logistics-sector photovoltaic canopies.

- April 2026: Schnellecke Logistics commenced integration of 20 MAN eTGX electric trucks into its transport fleet, 10 units by end-2026 and 10 more by end-2027, following successful pilot runs in Braunschweig in August 2025 and Zwickau in March 2026; the deployment is part of a broader decarbonization program that also includes a switch to HVO100 fuel, targeting over 1 million liters of HVO10 use in 2026 and 2027 combined.

- June 2025: DHL Group, Daimler Truck, and Hylane signed a cooperation agreement for 30 Mercedes-Benz eActros 600 battery-electric trucks under a "Transport as a Service" model, the largest single electric truck contract in Germany in 2025.

- March 2025: Duvenbeck Group commenced series operations with the MAN eTGX Ultra Low Liner electric truck on the Herne-to-Wolfsburg VW plant logistics route, one of the first logistics specialists globally to run this truck type in automotive OEM plant transport the group has a letter of intent to deploy up to 120 MAN eTGX units by 2026 for VW logistics in the Rhine-Ruhr and Benelux regions.

Germany Finished Vehicle Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing & Distribution | |

| Value-added Services and Others |

| Domestic | |

| International | Import/Inbound |

| Export/Outbound |

| Passenger Vehicles (Including Two and Three-Wheelers) |

| Commercial Vehicles |

| Off-Highway Vehicles |

| OEMs |

| Dealers |

| Others (Rental Companies, Fleet leasing companies, Government & Defense Fleets, etc.) |

| North Rhine-Westphalia |

| Bavaria (Bayern) |

| Baden-Wurttemberg |

| Rest of States |

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing & Distribution | ||

| Value-added Services and Others | ||

| By Destination | Domestic | |

| International | Import/Inbound | |

| Export/Outbound | ||

| By Type of Vehicles | Passenger Vehicles (Including Two and Three-Wheelers) | |

| Commercial Vehicles | ||

| Off-Highway Vehicles | ||

| By End-user Industry | OEMs | |

| Dealers | ||

| Others (Rental Companies, Fleet leasing companies, Government & Defense Fleets, etc.) | ||

| By Region | North Rhine-Westphalia | |

| Bavaria (Bayern) | ||

| Baden-Wurttemberg | ||

| Rest of States | ||

Key Questions Answered in the Report

What is the current size of the Germany finished vehicle logistics sector?

The Germany finished vehicle logistics market size is estimated at USD 8.52 billion in 2026 and is projected to reach USD 11.45 billion by 2031, at a 6.09% CAGR over 2026-2031.

Which logistics function is growing the fastest in vehicle distribution in Germany?

Warehousing and distribution is the fastest-growing function, with a projected 7.84% CAGR through 2031, because EV charging, software validation, and pre-delivery work are lengthening processing time.

Why is North Rhine-Westphalia leading regional demand?

North Rhine-Westphalia held 34.70% of the market in 2025 and is projected to grow at 7.04% through 2031, supported by Duisburg’s scale and strong inland rail connectivity.

Which customer group drives the largest share of demand?

OEMs led with 68.30% of demand in 2025 because finished vehicle logistics remain tightly linked to factory output, allocation planning, and dealer supply programs.

How are EVs changing finished vehicle logistics in Germany?

EVs require charging, software updates, battery-aware safety systems, and longer pre-delivery routines, which increase compound dwell time and raise the value of technical processing services.

What is the main near-term challenge for providers in Germany?

Driver shortages and infrastructure bottlenecks remain the main near-term constraints because they affect road capacity, intermodal flexibility, and delivery reliability across key automotive corridors.

Page last updated on: