Germany E-commerce Warehouse Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

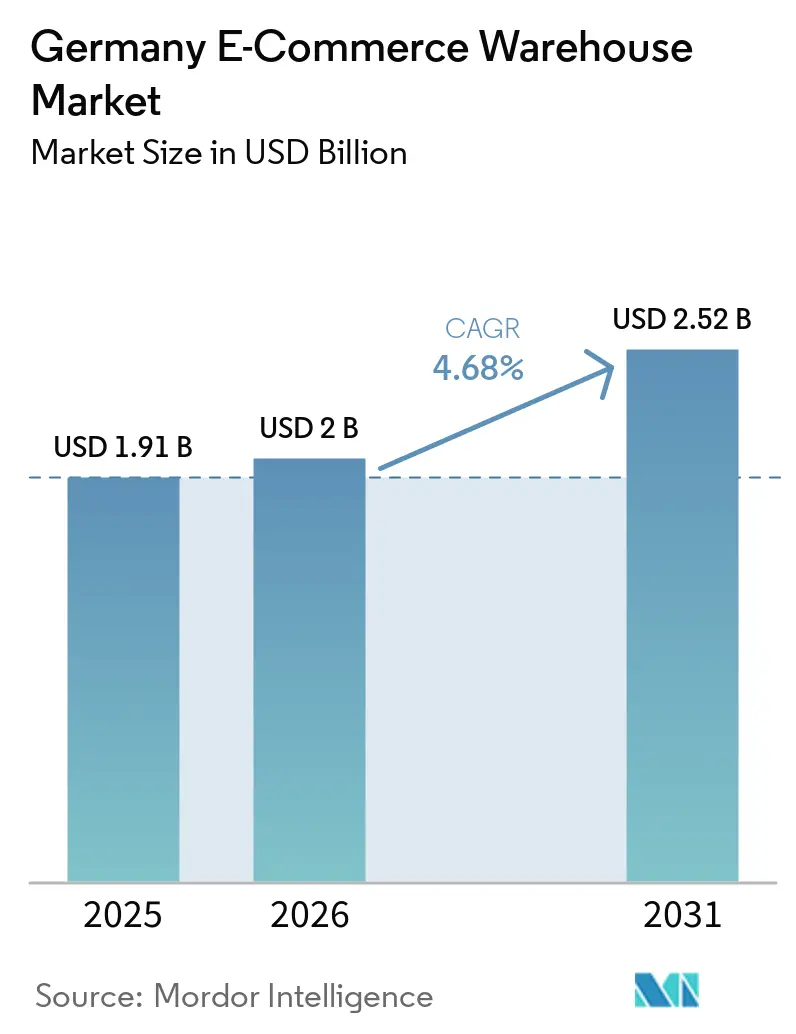

| Base Year Market Size (2025) | USD 1.91 Billion |

| Market Size (2026) | USD 2 Billion |

| Market Size (2031) | USD 2.52 Billion |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany E-commerce Warehouse Market Analysis by Mordor Intelligence

The Germany E-commerce Warehouse Market size is expected to grow from USD 1.91 billion in 2025 to USD 2.00 billion in 2026 and is forecast to reach USD 2.52 billion by 2031 at 4.68% CAGR over 2026-2031.

An investment shift toward automation retrofits, multi-temperature capabilities, and vertical expansions is redefining capacity planning as operators favor density over new footprints. Germany’s role as the European Union’s main cross-border fulfillment gateway concentrates new builds near border crossings and intermodal hubs, allowing merchants to serve continental demand from a single inventory pool. At the same time, the maturation of online grocery and quick-commerce is pulling cold-chain investments into urban and suburban micro-fulfillment nodes, while subscription commerce is stabilizing order profiles and improving space utilization. Heightened ESG scrutiny and green-warehouse financing incentives are also accelerating the adoption of renewable energy systems, sustainable materials, and building-performance certification programs across both new and retrofitted sites.

Key Report Takeaways

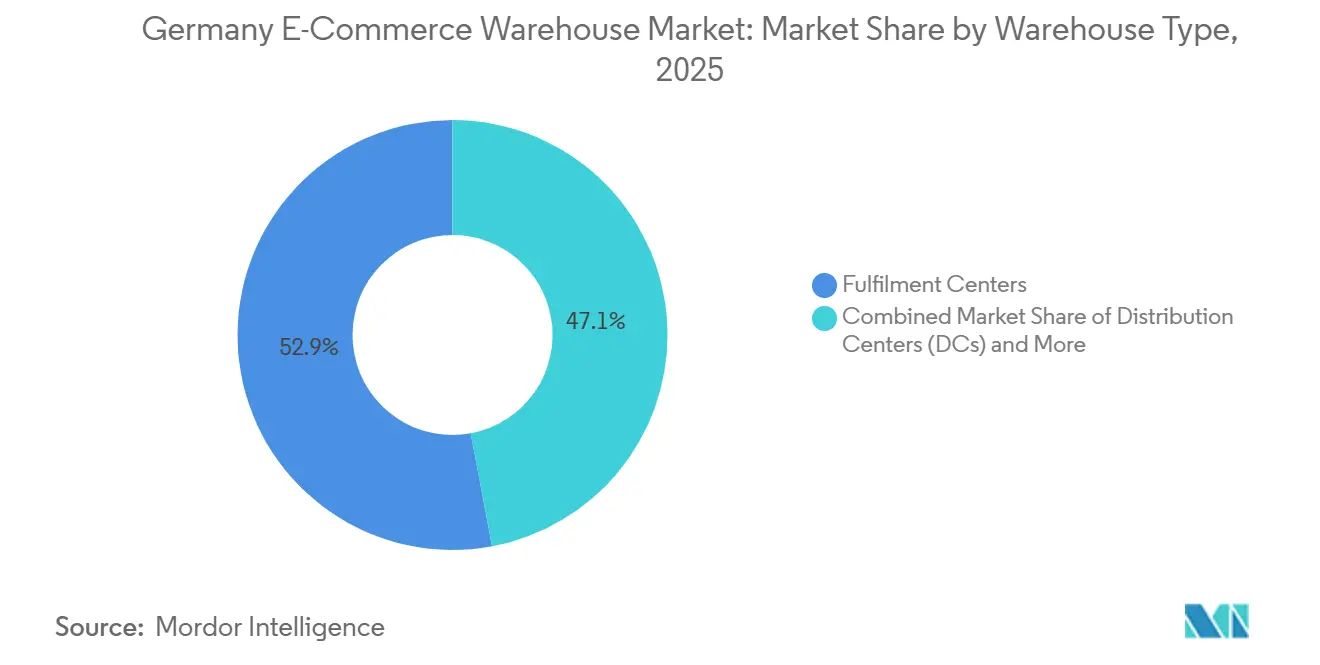

- By warehouse type, fulfilment centres led with 52.94% of the Germany E-commerce Warehouse Market share in 2025, while dark stores and micro-fulfillment centers recorded the fastest projected CAGR at 9.1% through 2031.

- By service type, storage accounted for 54.11% of the Germany E-commerce Warehouse Market size in 2025; value-added services are forecast to expand at a 7.92% CAGR to 2031.

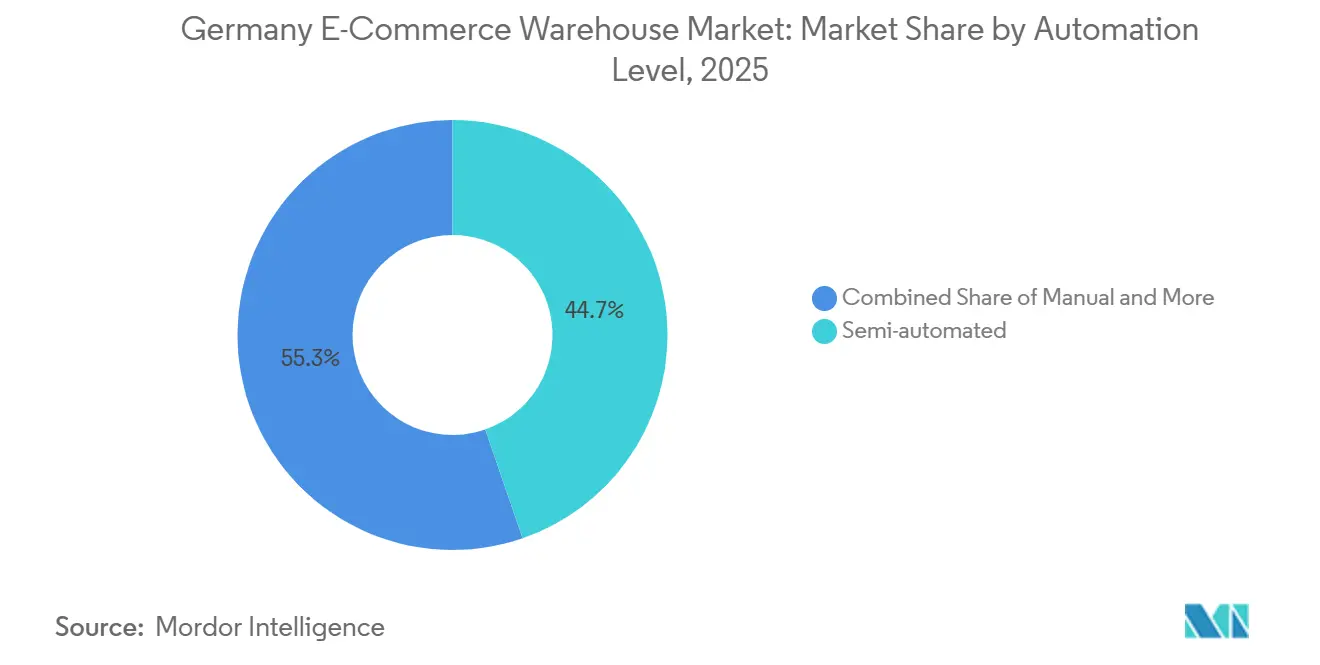

- By automation level, semi-automated facilities held 44.7% of the Germany E-commerce Warehouse Market share in 2025, whereas automated operations advance at a 7.14% CAGR through 2031.

- By end-user industry, apparel and footwear represented 29.74% of demand in 2025; grocery & FMCG is projected to grow at 10.67% CAGR up to 2031.

- By geography, North Rhine-Westphalia captured 25.27% of the 2025 value, and Bavaria is set to expand at a 6.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany E-commerce Warehouse Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming cross-border EU e-commerce flows | +1.1% | Border regions, NRW logistics corridors | Medium term (2-4 years) |

| Acceleration of online grocery and q-commerce demand | +0.9% | Metropolitan areas, mid-tier cities | Short term (≤ 2 years) |

| Surge in subscription/auto-replenishment commerce | +0.6% | National, consumer goods clusters | Medium term (2-4 years) |

| Omni-channel inventory consolidation by legacy retailers | +0.7% | Retail-dense regions, suburban nodes | Short term (≤ 2 years) |

| Vertical automated mezzanine retrofits | +0.5% | Urban-adjacent parks | Medium term (2-4 years) |

| ESG-linked green-warehouse financing incentives | +0.4% | National, high in Bavaria and B-W | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Booming Cross-Border EU E-Commerce Flows

Germany’s central geography and Rhine-Alpine corridor connectivity make it the preferred consolidation point for pan-European e-commerce. Operators deploy customs-bonded zones that defer duties until final delivery, lowering working-capital exposure for merchants. DHL’s 1 million-parcel-per-day hub in nearby Poznan exemplifies network extensions that knit German and Eastern European facilities into a single fulfillment mesh. Growth in multi-currency invoicing, localized packaging, and VAT-compliant documentation strengthens demand for value-added services, while multilingual labor pools and in-house brokerage expertise emerge as competitive moats[1]"E-commerce in the EU: Market integration and cross-border trade." European Commission, commission.europa.eu.

Acceleration of Online Grocery & Q-Commerce Demand

Online grocery sales are on track to hit EUR 18 billion (USD 20.6 billion) by 2030 as penetration climbs to 17% of food outlays. REWE’s EUR 250 million (USD 286 million) Magdeburg hub processes 286,000 packages daily with 50% automation, showing the capital intensity of multi-temperature fulfillment. Quick-commerce brands place micro-fulfillment nodes within 3-5 km of customers, compressing delivery windows below 60 minutes. Multi-zone storage grids that integrate ambient, chilled, and frozen SKUs inside the same automation framework are becoming standard, allowing high-velocity SKU handling without capacity trade-offs[2]“Online trade in goods and services.” Destatis, destatis.de.

Surge in Subscription/Auto-Replenishment Commerce

Predictable replenishment cycles from subscription programs cut safety-stock buffers and smooth outbound volumes, lifting space efficiency while easing labor scheduling. DHL’s Strategy 2030 bundles fulfillment with last-mile capabilities, positioning the firm to capture subscription-led growth as brands seek one-stop logistics partners. Lower return ratios further trim reverse-logistics complexity, especially in consumer packaged goods and personal-care verticals that now bypass traditional retail channels in favor of direct-to-consumer shipments.

Omni-channel Inventory Consolidation by Legacy Retailers

Retailers are merging store and online stock into hybrid facilities capable of pallet replenishment and single-unit picking. Otto Group’s AI-enabled Polish site handles up to 110 million annual parcels and illustrates the investment scale required to stay relevant against pure-play e-commerce rivals. Demand rises for sophisticated warehouse-management systems that can reroute inventory across channels based on real-time margin signals, enabling operators to monetize every cubic foot throughout seasonal swings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electric-grid capacity bottlenecks for high-power automation | -0.6% | Industrial zones with legacy grids | Short term (≤ 2 years) |

| Rising cybersecurity threats to warehouse OT systems | -0.4% | National, automation-heavy sites | Medium term (2-4 years) |

| Stricter EU packaging and waste-compliance directives | -0.5% | EU-wide, state-level variance | Medium term (2-4 years) |

| Construction-material supply shocks and cost spikes | -0.7% | High-growth regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Electric-Grid Capacity Bottlenecks for High-Power Automation

Robotic systems typically consume 3-5 MW of continuous power, frequently surpassing the spare capacity of local substations. This high energy demand often creates significant challenges for infrastructure readiness. With connection queues stretching up to 18 months, rollouts face delays, nudging operators towards phased deployments or temporary semi-automated solutions to maintain operational continuity. The scale of necessary upgrades is underscored by partnerships with utilities, exemplified by DHL-E.ON’s DC electrification program, which highlights the critical need for modernized energy infrastructure to support advanced robotic systems.

Rising Cybersecurity Threats to Warehouse OT Systems

Tightly integrated WMS, ERP, and robotic controls enlarge the attack surface. Ransomware that targets operational technology can freeze picking bots and paralyze fulfillment for days. GXO’s AI-driven orchestration stack underlines both the sophistication and vulnerability of next-generation sites, forcing operators to invest in zero-trust architectures, redundancies, and cyber-insurance to maintain shipper confidence[3]"Automation and robotics in logistics systems." Fraunhofer Institute for Material Flow and Logistics, iml.fraunhofer.de.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Fulfilment Centers Anchor Market Amid Micro-Format Acceleration

Fulfilment centers held 52.94% of the Germany E-commerce Warehouse Market size in 2025, reflecting their versatility across product categories and order profiles. Dark Stores and micro-fulfilment centers, however, post a brisk 9.1% CAGR through 2031 as quick-commerce players require inventory within minutes of end users. The rise of cold-chain automation brings multi-zone temperature designs to both large fulfilment hubs and compact urban nodes. Distribution centres continue to serve bulk replenishment for legacy retailers, while cold-chain warehouses gain traction among pharma and fresh-food operators. Reverse-logistics hubs and bonded sites populate the others category, offering specialized value propositions like duty-deferred storage and returns processing.

Technical sophistication grows in all formats. Flaschenpost’s Langenfeld facility processes 1,000 orders per hour via integrated ambient and chilled AutoStore grids, showcasing how automation harmonizes speed and temperature control. Legacy fulfilment centres reply with modular robotics that flex capacity across seasons, minimizing sunk costs while future-proofing against evolving product mixes. Blurred lines between warehouse types emerge as omni-channel merchants demand spaces able to pivot from bulk pallet moves to single-unit picks with minimal reconfiguration.

By Service Type: Storage Foundation Challenged by Value-Added Acceleration

Storage remains foundational at 54.11% of 2025 revenue, a function every operator must offer. Yet Value-Added Services grow 7.92% CAGR to 2031 as brands outsource kitting, labeling, and localization to reduce lead times and complexity. Picking and packing, the labor-intensive heart of e-commerce, drives most automation spend because accuracy and speed here translate directly into customer satisfaction. REWE’s Magdeburg hub, automated to 50% across storage and pick zones, illustrates how integrated service bundles cut dwell times and curb workforce dependency.

Operators who master regulatory compliance, testing, and light customization create sticky relationships and margin uplifts. AI-enhanced WMS solutions optimize order batching and labor allocation, while robotics shrinks error rates and supports 24/7 peaks. As commoditized storage yields lower margins, diversified service portfolios become decisive in client retention and contract renewals.

By Automation Level: Semi-Automated Plurality Amid Full-Automation Momentum

Semi-automated sites accounted for 44.7% of the Germany E-commerce Warehouse Market share in 2025 value because they balance capex with flexibility, appealing to operators serving mixed-volume customers. Automated facilities, however, notch a 7.14% CAGR as robotics costs fall and labor shortages deepen. Manual operations persist for irregular SKUs or low-volume niches but steadily lose share. Robots-as-a-Service deals, like GXO’s one-hour-install Reflex units, compress payback periods and democratize access to high-end automation.

Penetration has climbed to 25% from 5% ten years ago, with modular architectures enabling phased rollouts that avoid service interruptions. Cloud-based orchestration allows continuous optimization of bot fleets and conveyor speeds, squeezing further efficiency as volumes rise[4]"Industry 5.0 and digital transformation in logistics and manufacturing." European Commission, ec.europa.eu.

By End-User Industry: Apparel Dominance Gives Way to Grocery Momentum

Apparel and footwear still led demand in 2025 at 29.74%, underpinned by Germany’s fashion-savvy consumer base and elevated return rates requiring reverse-logistics expertise. Grocery and FMCG, however, surge ahead at 10.67% CAGR as cold-chain automation solves profitability hurdles in rapid-delivery models. Consumer Electronics call for anti-static handling and high-value security, pharmaceuticals/beauty and wellness rely on GDP-certified climates down to -70 °C, and Home Essentials and Furnishings contend with volumetric diversity that taxes vehicle cubage and handling gear.

DHL’s EUR 2 billion (USD 2.29 billion) health-logistics expansion in Florstadt creates 100,000 m² of temperature-mapped space, signaling strong pharma demand. Grocery specialists integrate ambient and chilled grids under one roof, slashing order-assembly times while curbing energy waste through AI load balancing. Electronics merchants adopt same-day goals in metro zones, prompting forward stocking and cushioned packaging protocols that reduce damage claims.

Geography Analysis

North Rhine-Westphalia commanded 25.27% of the Germany E-commerce Warehouse Market share in 2025, leveraging the Rhine-Alpine artery and Duisburg’s inland port to provide cost-efficient multimodal links to Benelux and France. Space turnover in the Ruhr climbed 115% in 2025 as operators flocked to proximate labor pools and bonded-warehousing infrastructure. Close-in locations cut inbound lead times and outbound transit, enabling same-day coverage across multiple EU capitals.

Bavaria posts the fastest growth at 6.58% CAGR to 2031, propelled by Munich’s technology cluster and a pivot toward electric-vehicle supply chains. Craiss’s Augsburg center on the A8 exemplifies new builds that target R&D-heavy industries demanding tight delivery tolerances. The regional government’s push for sustainability aligns with operators seeking DGNB labels and renewables integration.

Baden-Württemberg’s EUR 30.3 billion (USD 34.7 billion) annual R&D outlay and density of Mittelstand champions sustain premium demand for just-in-time, high-precision logistics. Operators deploy advanced automation and quality-control labs that dovetail with automotive and machinery exporters facing global competition.

The Rest of the states' bucket, including Berlin-Brandenburg and Saxony, gains share through land-cost advantages and investment incentives such as GVZ Freienbrink’s 50% subsidy packages. These emerging nodes complement established corridors by offering overflow capacity and niche specialization in, for example, battery supply chains and reverse logistics.

Competitive Landscape

DSV’s EUR 14.3 billion (USD 16.4 billion) takeover of DB Schenker creates a 17.5 million m² behemoth and resets the German hierarchy, prompting rivals to scale through mergers or strategic alliances. GXO embeds automation in over half of new contracts, using robotics partnerships to accelerate deployment cycles and bind customers to its digital ecosystem.

CEVA, bolstered by its integration of Bolloré Logistics, now boasts a warehouse footprint spanning 11.7 million m² and pro forma revenues hitting USD 20.2 billion. This strategic acquisition not only enhances CEVA's operational capabilities but also strengthens its position in the competitive logistics market. The move underscores the ambition of mid-tier players to carve out a significant presence on the global stage, as they aim to compete with larger, established players by expanding their service offerings and geographic reach.

Niche champions carve defensible turf in pharmaceutical cold-chain, fashion returns, and high-tech spare-parts fulfillment. DHL’s DGNB-Gold Florstadt site positions it as the go-to partner for biopharma shippers, while quick-commerce specialists like Flink rely on ultra-dense micro-fulfillment nodes. Technology adoption now separates winners from laggards, with AI-driven orchestration and predictive analytics converting data into operational edge.

Germany E-commerce Warehouse Industry Leaders

-

GXO Logistics

-

CMA CGM Group (Including CEVA Logistics)

-

Kuehne+Nagel

-

DSV A/S

-

DHL Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: GXO Logistics announced a strategic agreement with Blue Yonder to incorporate AI-driven forecasting and real-time data into its warehouse operations. This initiative aims to enhance inventory visibility, improve order fulfillment speed, and enable scalability for high-volume e-commerce warehouses across Germany and Europe.

- May 2025: DHL’s Florstadt campus added 30,000 m² of climate-neutral warehouse space, lifting the total to 100,000 m².

- April 2025: DHL Group announced EUR 2 billion (USD 2.29 billion) through 2030 for GDP-certified pharma hubs and expanded cold-chain capacity.

- April 2025: DSV completed its EUR 14.3 billion (USD 16.4 billion) acquisition of DB Schenker, pledging EUR 1 billion (USD 1.15 billion) for German infrastructure upgrades.

Germany E-commerce Warehouse Market Report Scope

| Fulfilment Centres |

| Distribution Centres (DCs) |

| Cold-Chain Warehouses |

| Dark Stores / Micro-Fulfillment Centers |

| Others (Reverse Logistics Hubs, Bonded Warehouses, Hybrid-Use Spaces, etc.) |

| Storage |

| Picking and Packing |

| Value-Added Services and Others (Kitting, Labelling) |

| Manual |

| Semi-Automated |

| Automated |

| Apparel and Footwear |

| Consumer Electronics |

| Grocery and FMCG |

| Pharmaceuticals, Beauty and Wellness |

| Home Essentials and Furnishings |

| Others |

| North Rhine-Westphalia |

| Bavaria (Bayern) |

| Baden-Württemberg |

| Rest of States |

| By Warehouse Type | Fulfilment Centres |

| Distribution Centres (DCs) | |

| Cold-Chain Warehouses | |

| Dark Stores / Micro-Fulfillment Centers | |

| Others (Reverse Logistics Hubs, Bonded Warehouses, Hybrid-Use Spaces, etc.) | |

| By Service Type | Storage |

| Picking and Packing | |

| Value-Added Services and Others (Kitting, Labelling) | |

| By Automation Level | Manual |

| Semi-Automated | |

| Automated | |

| By End-User Industry | Apparel and Footwear |

| Consumer Electronics | |

| Grocery and FMCG | |

| Pharmaceuticals, Beauty and Wellness | |

| Home Essentials and Furnishings | |

| Others | |

| By States – Germany (Value) | North Rhine-Westphalia |

| Bavaria (Bayern) | |

| Baden-Württemberg | |

| Rest of States |

Key Questions Answered in the Report

How large will Germany’s e-commerce warehouse space be by 2031?

The Germany E-commerce Warehouse Market size is projected to reach USD 2.52 billion by 2031, expanding at a 4.68% CAGR from 2026 to 2031.

Which German state offers the greatest growth potential for new warehouses?

Bavaria leads with a 6.58% forecast CAGR through 2031, fueled by Munich’s tech hub and automotive supply-chain shifts.

What warehouse type is growing fastest in Germany?

Dark stores and micro-fulfillment centers are advancing at a 9.1% CAGR as quick-commerce pushes inventory closer to urban consumers.

How are operators funding green-warehouse upgrades?

Banks cut lending spreads by up to 50 basis points for projects that achieve DGNB or BREEAM ratings, making sustainability upgrades financially attractive.

What is the main barrier to full automation in German warehouses?

Electric-grid capacity constraints delay high-power robotic deployments, often adding more than a year to large retrofit projects.

Page last updated on: