Europe Third-Party Logistics (3PL) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

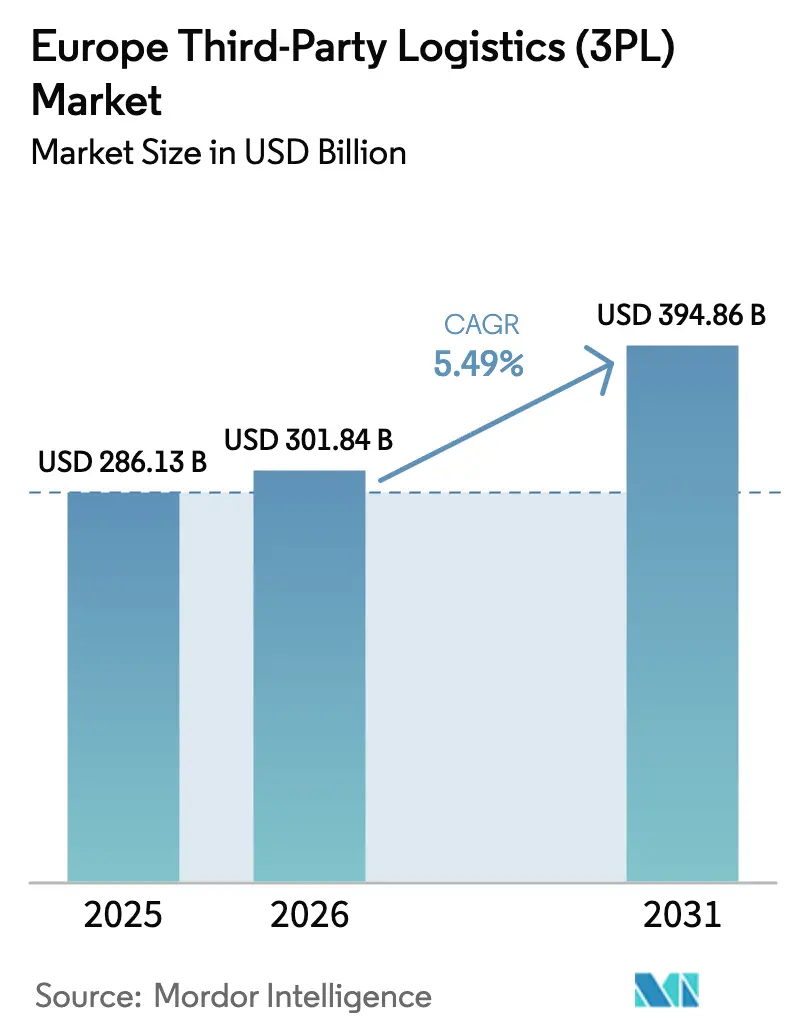

| Base Year Market Size (2025) | USD 286.13 Billion |

| Market Size (2026) | USD 301.84 Billion |

| Market Size (2031) | USD 394.86 Billion |

| Growth Rate (2026 - 2031) | 5.49% CAGR |

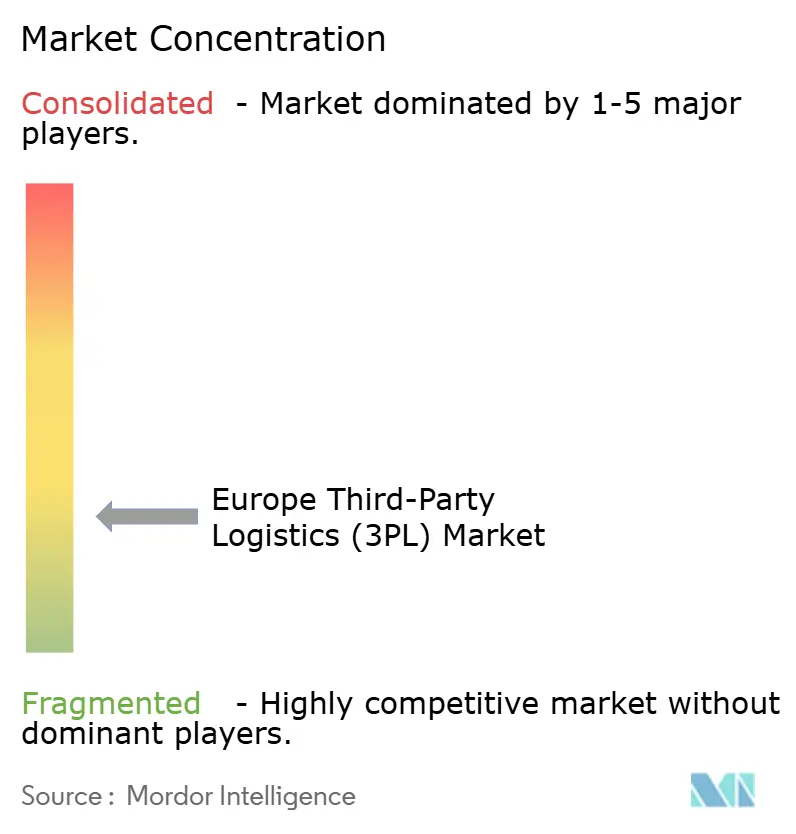

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Third-Party Logistics (3PL) Market Analysis by Mordor Intelligence

The Europe Third-Party Logistics market size is expected to grow from USD 286.13 billion in 2025 to USD 301.84 billion in 2026 and is forecast to reach USD 394.86 billion by 2031 at 5.49% CAGR over 2026-2031.

The growth trajectory reflects resilient demand despite geopolitical disruptions, with e-commerce parcel surges, cold-chain outsourcing, and green-logistics mandates acting as primary catalysts. Providers are accelerating automation and AI investments to alleviate labor shortages, while consolidation delivers scale efficiencies that support aggressive pricing strategies. Capacity constraints in tier-1 hubs intensify real-estate inflation, yet route diversification and near-shoring trends unlock volume along intra-EU freight corridors. Regulations such as Fit-for-55 and the Carbon Border Adjustment Mechanism create compliance costs but open opportunities for low-emission service differentiation.

Key Report Takeaways

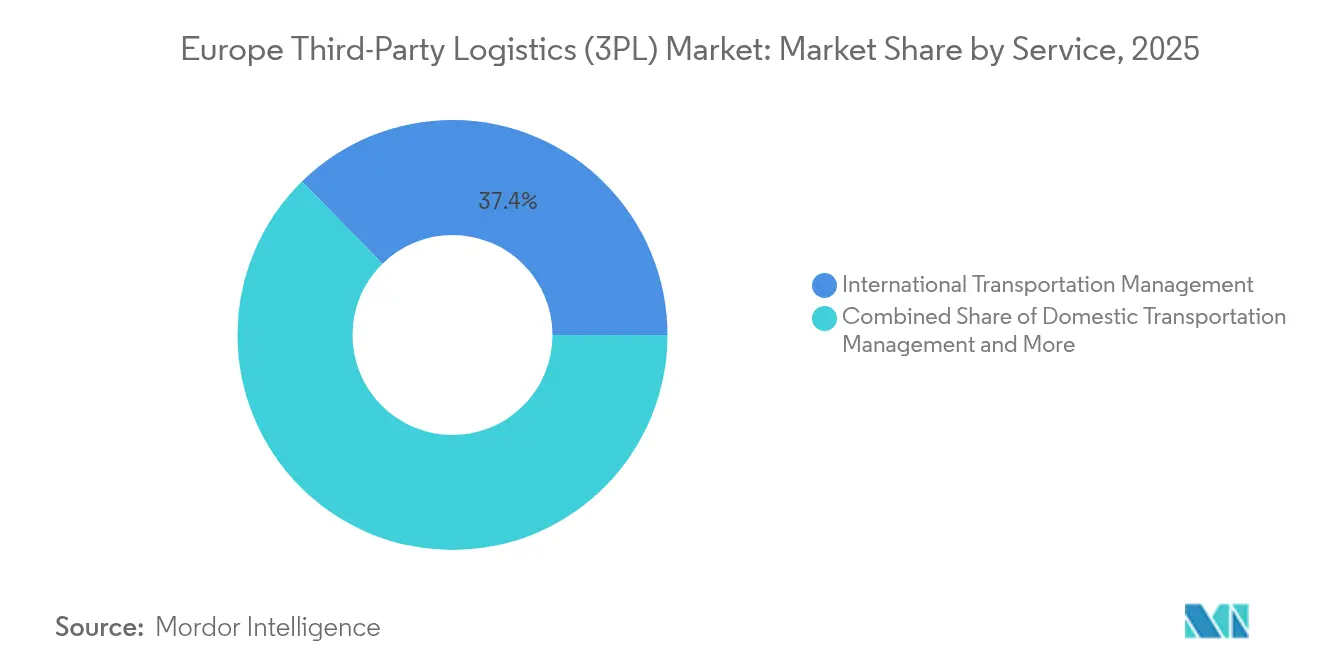

- By service, International Transportation Management led with 37.35% revenue share in 2025, while Value-Added Warehousing and Distribution is projected to expand at a 6.95% CAGR through 2031.

- By end-user, manufacturing captured 25.40% of the Europe third-party logistics market share in 2025, whereas retail & e-commerce is advancing at an 8.35% CAGR to 2031.

- By logistics model, asset-heavy providers held 40.20% share of the Europe third-party logistics market size in 2025; asset-light approaches post the highest forecast CAGR at 6.05% between 2026-2031.

- By country, Germany commanded 15.85% revenue share in 2025, while the Netherlands is forecast to grow at a 6.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Third-Party Logistics (3PL) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce parcel boom stretching cross-dock capacity | +1.2% | Germany, Netherlands, UK, France | Short term (≤ 2 years) |

| Pharmaceutical cold-chain outsourcing wave | +0.8% | Germany, Netherlands, Belgium, Switzerland | Medium term (2-4 years) |

| OEM near-shoring fuelling intra-EU shuttle freight | +0.9% | Germany, Poland, Czech Republic, Hungary | Medium term (2-4 years) |

| Green-logistics mandates (EU Fit-for-55) | +0.6% | EU-wide | Long term (≥ 4 years) |

| Carbon Border Adjustment Mechanism compliance demand | +0.4% | EU border countries | Long term (≥ 4 years) |

| Cargo-bike micro-hub adoption in low-emission zones | +0.3% | Berlin, Amsterdam, Paris, Milan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-Commerce Parcel Boom Stretching Cross-Dock Capacity

Parcel volumes exceed pre-pandemic projections, pushing European cross-dock hubs toward maximum utilization. Major retailers deploy cargo-bike fleets and electric vans to navigate low-emission zones, as demonstrated by Amazon’s Berlin micromobility hub[1]“Amazon launches first micromobility hub in Berlin,” Amazon, aboutamazon.com. Advanced demand-forecasting engines and dynamic slotting algorithms enable 3PLs to trim parcel handling times and unlock short-term capacity. Providers that scale automated sortation technologies secure favorable contracts from omnichannel retailers seeking next-day delivery coverage across the Europe third-party logistics market.

Pharmaceutical Cold-Chain Outsourcing Wave

Life-science shippers outsource temperature-controlled transport to meet stringent GDP guidelines and preserve biologic drug efficacy. UPS expanded its European cold-chain footprint through the Frigo-Trans and BPL acquisitions, signaling aggressive investment in validated storage and real-time monitoring networks. Limited pharmaceutical warehousing capacity in Germany and the Netherlands creates premium pricing power for certified operators. As biologics pipelines grow, specialized 3PLs gain a durable competitive edge within the Europe third-party logistics market.

OEM Near-Shoring Fuelling Intra-EU Shuttle Freight

Automotive and electronics manufacturers relocate assembly closer to EU demand centers, driving high-frequency shuttle services linking Central and Eastern European plants. Shuttle corridors between Germany and Poland witness volume spikes that reward providers with synchronized cross-dock networks and customs know-how. The shift from just-in-time to just-in-case inventory strategies escalates regional warehousing uptake and underpins rising contract values across the Europe third-party logistics market.

Green-Logistics Mandates (EU Fit-for-55)

Fit-for-55 measures compel carriers to adopt alternative-fuel fleets and optimize route mileage to align with decarbonization targets. Large 3PLs pilot hydrogen trucks on German autobahn lanes and retrofit warehouses with on-site solar power to lower Scope 1 and 2 emissions. Providers offering granular CO₂-tracking dashboards meet corporate ESG disclosure demands, positioning sustainability competence as a deal-winning differentiator in the Europe third-party logistics market[2]“Fit for 55 Package,” European Commission, ec.europa.eu.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver and warehouse labor crunch | -0.7% | Germany, Netherlands, UK, Nordics | Short term (≤ 2 years) |

| Industrial real-estate cost inflation in tier-1 hubs | -0.5% | Amsterdam, Frankfurt, Paris, London | Medium term (2-4 years) |

| EU Data Act limits on telematics data monetization | -0.2% | EU-wide | Medium term (2-4 years) |

| East-West trade-lane volatility from Russia sanctions | -0.4% | Eastern Europe, Baltics, Finland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Driver and Warehouse Labor Crunch

Germany reported more than 70,000 unfilled truck-driver positions in 2024, a deficit that forces wage hikes and lengthens recruitment cycles[3]“Professional Truck Drivers: Appreciation Has Right of Way,” Dachser, dachser.com. Automation adoption accelerates, with robotics installs rising 30% year-over-year in major facilities as operators strive to reduce labor dependency. Providers maintaining structured apprenticeship programs and advanced employee-retention schemes mitigate service disruptions, preserving customer trust across the Europe third-party logistics market.

Industrial Real-Estate Cost Inflation in Tier-1 Hubs

Rents in logistical hotspots such as Amsterdam and Frankfurt escalated through 2024, reflecting land scarcity and e-commerce warehouse competition. Smaller 3PLs relocate to secondary markets, extending delivery lead times but easing cost pressure. Large operators with long-duration leases or build-to-suit agreements safeguard margins and uphold network density across the Europe third-party logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Value-Added Warehousing and Distribution Accelerates

The Europe third-party logistics market size for International Transportation Management reached a 37.35% revenue share in 2025, driven by complex customs clearance and multimodal freight consolidation. Yet Value-Added Warehousing and Distribution (VAWD) is projected to record a 6.95% CAGR (2026-2031), the fastest across services. Retailers outsource omnichannel fulfillment, returns handling, and kitting, pushing VAWD providers to deploy robotics for piece-picking and automated packaging. As e-commerce demand stays buoyant, the Europe third-party logistics market will see VAWD progressively narrow the share gap with international forwarding. Domestic Transportation Management remains buoyant, supported by near-shoring and urban delivery innovations such as cargo-bike fleets.

Second-order effects amplify VAWD’s pull: merchants seek inventory postponement to delay final product customization until orders arrive, while omnichannel models require synchronized stock views across stores and online channels. International forwarding faces rising compliance costs from IMO and FuelEU regulations, limiting margin upside. Providers that blend forwarding expertise with downstream warehousing generate cross-selling synergies, reinforcing their positioning across the Europe third-party logistics market.

By End-User Industry: Retail & E-Commerce Momentum

Manufacturing captured the largest slice of 2025 revenues at 25.40%, reflecting ongoing automotive assembly, chemicals, and industrial machinery flows. Nonetheless, retail & e-commerce is forecast to expand at an 8.35% CAGR (2026-2031), outpacing all other verticals. Fast-fashion firms outsource reverse logistics to specialists such as ID Logistics, which handles more than 130 million returns annually. Social-commerce and subscription business models add SKU complexity that boosts demand for pick-to-unit capabilities. Pharmaceutical and healthcare enterprises ramp up outsourcing of GDP-compliant storage, creating stable, regulation-anchored volumes for cold-chain specialists across the Europe third-party logistics market.

The Europe third-party logistics industry also benefits from consumer goods private-label growth, which elevates direct-to-store deliveries. Automotive players accelerate electric-vehicle component sourcing within Europe, sustaining dedicated shuttle demand. Although manufacturing faces overcapacity risks, the diversification of component production into Central Europe upholds freight flows and safeguards warehouse occupancy rates.

By Logistics Model: Asset-Light Strategy Gains Pace

Asset-heavy operators controlled 40.20% of 2025 revenues, leveraging fleet density and large facility footprints to guarantee secured capacity. Asset-light providers, however, are projected to deliver a 6.05% CAGR (2026-2031), buoyed by capital-flexibility appeal to shippers. DSV’s mega-acquisition spree demonstrates how a network orchestrator can scale without owning every physical asset, instead integrating subcontracted fleets and shared warehouses. Hybrid models combine contract-dedicated assets with flex capacity, aligning with cyclical volume swings across the Europe third-party logistics market.

Higher borrowing costs in 2025-2026 elevate the hurdle rate for warehouse development, making asset-light models doubly attractive. Nonetheless, shippers with temperature-controlled or high-value cargo often favor asset-heavy relationships anchored in dedicated infrastructure. Market leaders invest in AI-driven asset-utilization dashboards that increase tractor-trailer productivity and prolong asset-heavy relevance within the Europe third-party logistics market.

Geography Analysis

Germany retained a 15.85% share of 2025 revenues, anchored by its manufacturing economy, Rhine waterway, and extensive autobahn network. The Europe third-party logistics market size in Germany continues to benefit from automotive clusters in Bavaria and Baden-Württemberg, and chemicals production in North Rhine-Westphalia. Yet driver shortages and warehouse land scarcity near Frankfurt and Hamburg tighten capacity, motivating providers such as GEODIS to upgrade twenty regional sites with automation and solar installations. Germany’s proactive adoption of electric trucks supports early compliance with Fit-for-55 thresholds and lowers shipper Scope 3 emissions.

The Netherlands is positioned as the fastest-growing geography, anticipated to log a 6.95% CAGR to 2031. Rotterdam’s deep-water port funnels 24,000-TEU mega-ships to inland depots, while Schiphol excels in high-value airfreight consolidation. Brexit-related customs complexity channels UK shippers through Dutch distribution centers, expanding bonded-warehouse demand across the Europe third-party logistics market.

Competitive Landscape

The Europe third-party logistics market is moderately fragmented. However, DSV closed a EUR 14.3 billion (USD 14.9 billion) takeover of DB Schenker in April 2025, constructing the world’s largest freight forwarder and catalyzing a new wave of merger activity. Deutsche Post DHL pledged USD 2.3 billion to double healthcare logistics turnover by 2030, expanding cold-chain warehouses and last-mile medical distribution fleets.

GXO launched a continent-wide partnership with Blue Yonder to roll out AI-enabled warehouse-management systems, cutting picking time and elevating inventory accuracy. ID Logistics entered the United Kingdom with an 18,000 m² site in Northampton dedicated to high-velocity return flows, signaling mid-tier specialization strategies.

Technological differentiation intensifies as providers deploy goods-to-person robotics, yard-management sensors, and predictive ETA algorithms. Asset-light orchestrators integrate spot-market capacity and digitally broker loads, while asset-heavy incumbents automate to defend margins. Specialized niches, including pharmaceutical GDP compliance and battery-pack handling, offer outsized profitability. Sustainability credentials—validated emissions dashboards and green-fleet ratios—act as tender-shortlisting criteria, further segmenting the Europe third-party logistics market.

Europe Third-Party Logistics (3PL) Industry Leaders

Deutsche Post DHL

Kuehne + Nagel International AG

DSV A/S

Rhenus Logistics

CEVA Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: GXO Logistics formed a multi-year partnership with Blue Yonder to roll out AI-driven warehouse-management platforms across its European sites, aiming to accelerate throughput and real-time forecasting

- April 2025: Deutsche Post DHL committed USD 2.3 billion toward European healthcare-logistics expansion, targeting a revenue doubling by 2030.

- April 2025: DSV finalized its EUR 14.3 billion (USD 14.9 billion) acquisition of DB Schenker, establishing a freight-forwarding leader with combined revenue above USD 43 billion.

- September 2024: ID Logistics opened an 18,000 m² facility at Prologis Grange Park, Northampton, to manage fast-fashion returns and hired 300 staff.

Europe Third-Party Logistics (3PL) Market Report Scope

| Domestic Transportation Management | Road |

| Air | |

| Others | |

| International Transportation Management | Road |

| Air | |

| Sea | |

| Multimodal / Intermodal | |

| Value-Added Warehousing and Distribution (VAWD) |

| Automotive |

| Energy and Utilities |

| Manufacturing |

| Life Sciences and Healthcare |

| Technology and Electronics |

| Retail and E-commerce |

| Consumer Goods and FMCG |

| Food and Beverages |

| Others |

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet and Warehouses) |

| Hybrid |

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| Netherlands |

| Russia |

| Rest of Europe |

| By Service | Domestic Transportation Management | Road |

| Air | ||

| Others | ||

| International Transportation Management | Road | |

| Air | ||

| Sea | ||

| Multimodal / Intermodal | ||

| Value-Added Warehousing and Distribution (VAWD) | ||

| By End-User Industry | Automotive | |

| Energy and Utilities | ||

| Manufacturing | ||

| Life Sciences and Healthcare | ||

| Technology and Electronics | ||

| Retail and E-commerce | ||

| Consumer Goods and FMCG | ||

| Food and Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet and Warehouses) | ||

| Hybrid | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe third-party logistics market in 2026?

The market was valued at USD 301.84 billion in 2026, with a forecast to reach USD 394.86 billion by 2031.

Which service segment is growing fastest within European 3PL?

Value-Added Warehousing and Distribution is projected to deliver a 6.95% CAGR between 2026-2031.

Which country shows the highest growth potential?

The Netherlands is forecast to lead growth with a 6.95% CAGR through 2031, buoyed by Rotterdam port and Schiphol airfreight connectivity.

Why are asset-light 3PL models gaining popularity?

Shippers favor asset-light providers for capital efficiency and scalability, driving a 6.05% segment CAGR over the forecast period.

What impact do EU sustainability regulations have on logistics providers?

Fit-for-55 rules compel investments in alternative-fuel fleets and carbon-tracking systems, increasing compliance costs but opening premium service opportunities.

Which vertical offers the strongest growth outlook?

Retail & e-commerce is expected to expand at an 8.35% CAGR, propelled by omnichannel fulfillment and complex returns management requirements.

Page last updated on: