United States 3PL Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

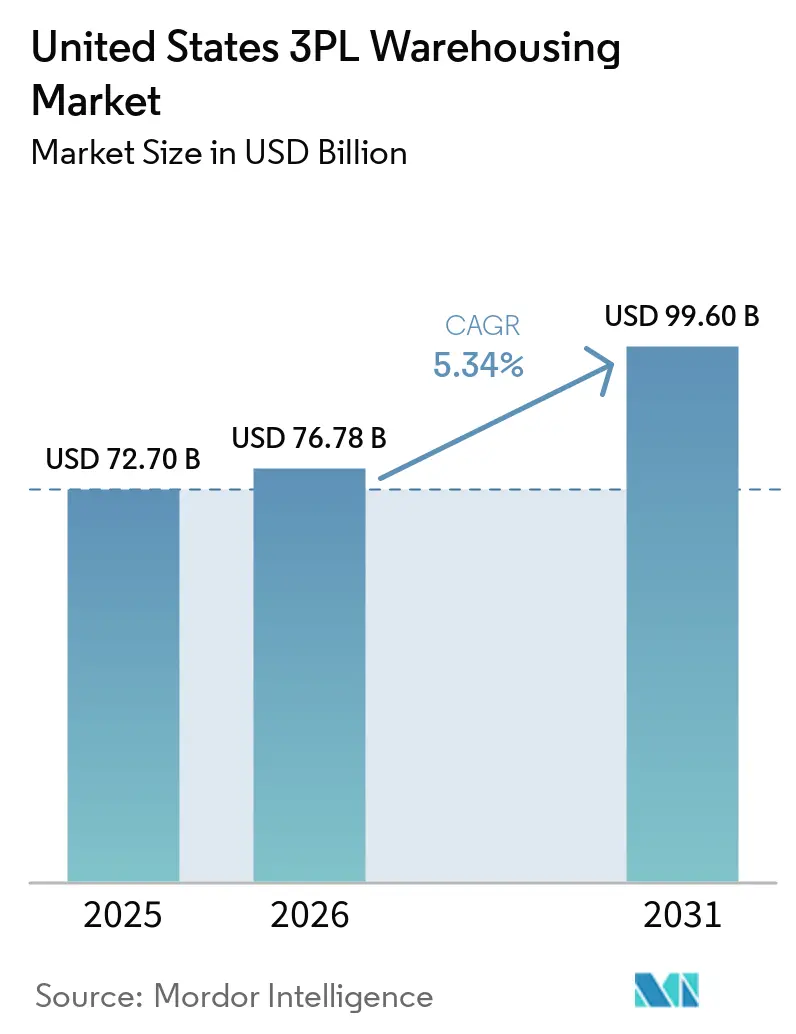

| Base Year Market Size (2025) | USD 72.70 Billion |

| Market Size (2026) | USD 76.78 Billion |

| Market Size (2031) | USD 99.60 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States 3PL Warehousing Market Analysis by Mordor Intelligence

The United States 3PL warehousing market size was valued at USD 72.70 billion in 2025 and estimated to grow from USD 76.78 billion in 2026 to reach USD 99.60 billion by 2031, at a CAGR of 5.34% during the forecast period 2026-2031.

The United States 3PL warehousing market is expanding because shippers are moving fixed warehouse assets into variable-cost contracts that can absorb tariff swings, changing sourcing routes, and faster fulfillment expectations. That shift is taking place at the same time as manufacturing supply chains are moving closer to the United States, which is increasing the need for both border-proximate space and inland buffer inventory. E-commerce operators are also adding denser fulfillment networks, and Prologis indicated that e-commerce tenants are expected to represent a larger share of new warehouse leasing in 2026 than in 2025. National vacancy reached 7.0% in Q1 2026, down 10 basis points from the late-2025 peak, while net absorption rose to 40 million square feet in the quarter, pointing to a market moving past the oversupply correction seen in 2024. As tighter capacity, automation spending, and nearshoring-related freight flows converge, the United States 3PL warehousing market is entering a phase where operating capability matters as much as warehouse footprint.

Key Report Takeaways

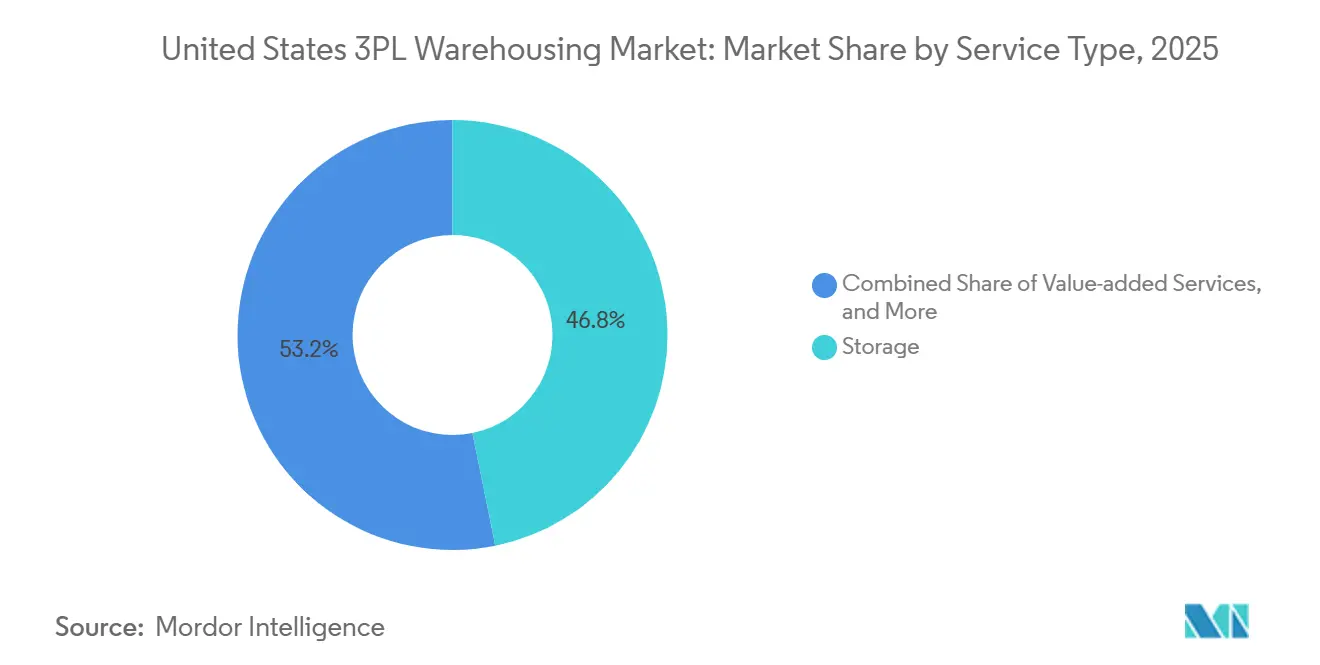

- By service type, storage held 46.81% of the United States 3PL warehousing market size in 2025, while value-added services and others are projected to expand at 8.18% through 2031.

- By warehouse type, general shared or multi-client warehousing held 49.32% of the United States 3PL Warehousing market share in 2025, while dedicated contract warehousing is projected to grow at 7.35% through 2031.

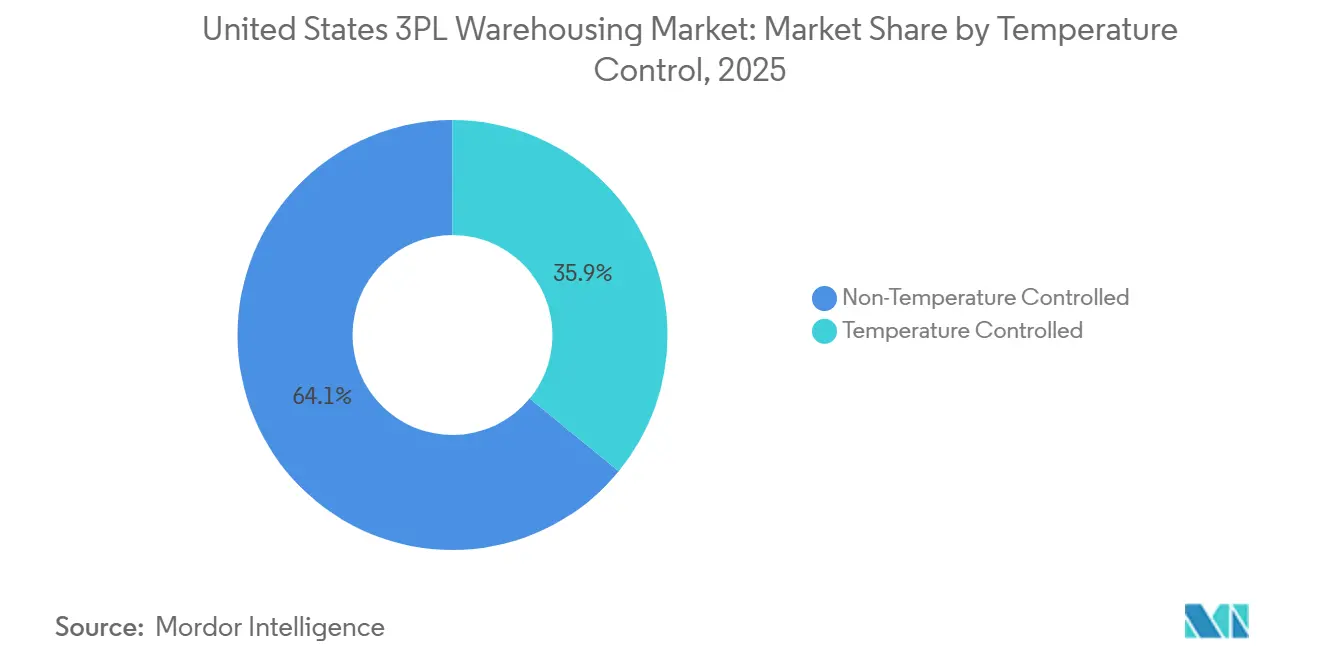

- By temperature control, non-temperature-controlled warehousing held 64.07% of the United States 3PL warehousing market share in 2025, while temperature-controlled warehousing is forecast to expand at 9.06% through 2031.

- By technology adoption, semi-automated facilities accounted for 52.14% of the United States 3PL warehousing market size in 2025, while fully automated warehousing is projected to grow at 11.02% through 2031.

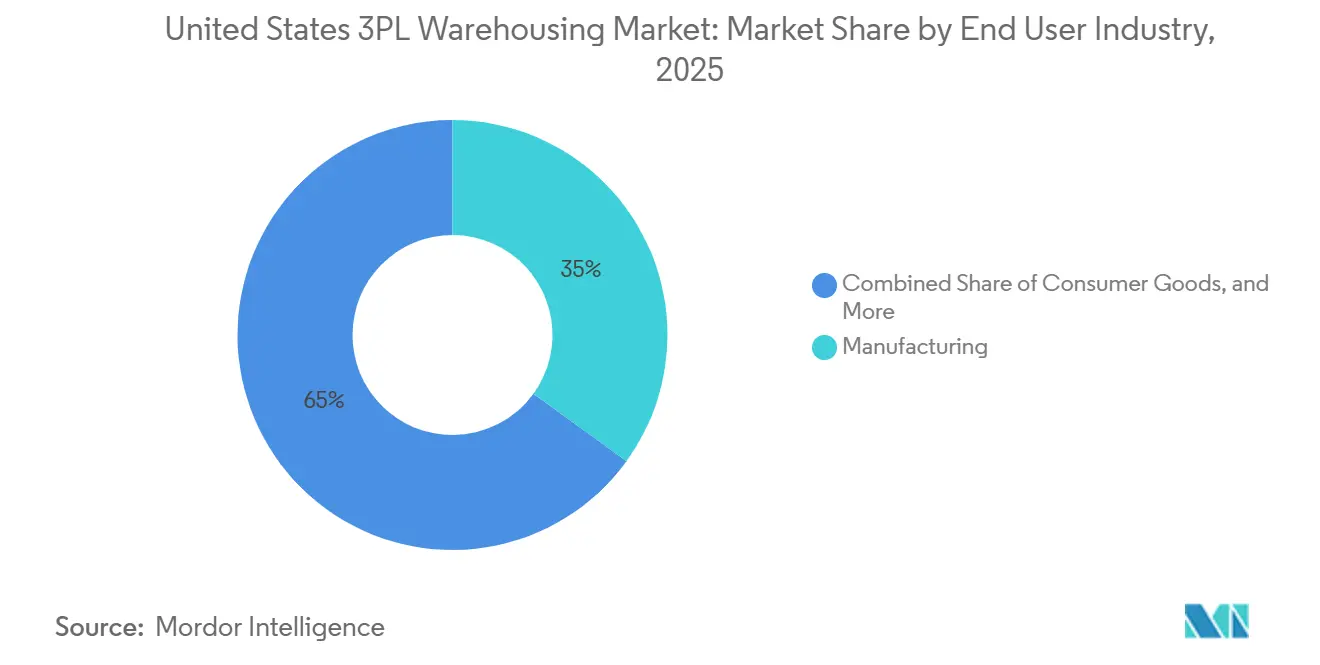

- By end user, manufacturing held 34.95% of the United States 3PL warehousing market share in 2025, while healthcare and pharma are forecast to expand at 8.48% CAGR through 2031.

- By geography, the West accounted for 26.6% of the United States 3PL warehousing in 2025, while the Southwest is projected to grow by 6.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States 3PL Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Fulfillment Boom Post-Pandemic Baseline | +1.8% | National, concentrated in Inland Empire, NJ and PA corridor, Chicago, Dallas-Fort Worth | Medium term (2-4 years) |

| Nearshoring and Reshoring of the United States Supply Chains | +1.2% | Southwest, Southeast manufacturing corridors, Midwest inland hubs | Long term (≥ 4 years) |

| Cold-Chain Expansion for Food and Pharma | +0.7% | National, with early gains in Atlanta, Savannah, Chicago O'Hare, Memphis, Kansas City | Long term (≥ 4 years) |

| Warehouse Automation and Robotics Cost Advantages | +0.6% | National, strongest in high-labor-cost coastal markets and high-volume fulfillment hubs | Medium term (2-4 years) |

| Institutional REIT Investment Expanding Capacity | +0.4% | National, concentrated in Sunbelt logistics corridors and I-65 and I-85 development zones | Short term (≤ 2 years) |

| State-Level Logistics Tax Incentives in the Southeast and Midwest | +0.3% | Southeast and Midwest, with national spillover through supply chain adjacency | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Fulfillment Boom Post-Pandemic Baseline

Third-party fulfillment is now embedded in everyday operating models, with 84% of brands using a third-party fulfillment company for at least some orders, and 44.0% planning to increase their number of fulfillment centers in 2026. The storage surge seen during the pandemic period has matured, but order complexity has kept demand firm because omnichannel compliance, branded packaging, kitting, and returns work all require more warehouse touches. That shift favors 3PL operators that can manage multiple sites rather than only a single large distribution center. The removal of the Section 321 de minimis exemption is also pushing cross-border e-commerce sellers to establish more domestic fulfillment footprints in the United States. More than 75% of brands plan to add at least 1 new sales channel in 2026, which means inventory placement and order orchestration become more demanding across every channel. As a result, the United States 3PL warehousing market is gaining more revenue from service intensity than from basic storage alone[1]“ShipBob’s 2026 State of Ecommerce Fulfillment Report,” PR Newswire, prnewswire.com.

Nearshoring and Reshoring of the United States Supply Chains

Nearshoring is increasing warehouse demand in 2 linked steps, with freight first needing border transload and bonded capacity, and then moving into inland buffer stock and regional distribution space. Kuehne+Nagel’s El Paso bonded warehouse reached full capacity within 1 year of opening, which led the company to announce a 60% expansion through a new adjacent site in November 2025. That example shows how border markets are tightening before inland warehouse networks have fully adjusted. Once manufacturers commit to North American production footprints, they also need more stable warehouse arrangements to protect against supply interruptions and rate volatility. This favors dedicated, bonded, and high-compliance facilities in the Southwest and selected Midwest corridors. The United States 3PL warehousing market is therefore benefiting not only from trade rerouting, but also from the longer operating cycles that follow those sourcing decisions.

Cold-Chain Expansion for Food and Pharma

Cold-chain demand is rising because food traceability and pharmaceutical handling rules make temperature-controlled logistics harder to internalize. Lineage agreed in April 2025 to acquire 4 Tyson Foods cold storage warehouses for USD 247 million and to commit more than USD 740 million to 2 fully automated greenfield warehouses with Tyson as anchor tenant. That scale of capital deployment shows that temperature-controlled 3PL capacity is being built around long-duration customer relationships instead of short-term spot demand. FDA Food Safety Modernization Act requirements also raise the compliance burden for refrigerated food handling, which makes certified providers more difficult to replace once they are integrated into a shipper’s network. In pharma, the same pattern applies because validated handling, documentation, and temperature assurance all increase switching costs. This is one reason the United States 3PL warehousing market is seeing faster growth in cold-chain capacity than in standard ambient formats.

Warehouse Automation and Robotics Cost Advantages

Labor costs continue to support the case for warehouse automation, with wages in transportation and warehousing up 3.5% year over year through March 2026[2]“Employment Cost Index, March 2026,” U.S. Bureau of Labor Statistics, U.S. Bureau of Labor Statistics, bls.gov. Automation is no longer used so operators are also using it to improve retention, standardize workflows, and protect service levels in tight labor markets. GXO opened a new 600,000-square-foot Hasbro distribution center in Georgia in March 2026 using its GXO IQ cloud-native operating system, demonstrating how automation is now embedded in long-term customer programs rather than treated as a separate back-office project. Kenco’s 2026 Innovation Report found that 83% of surveyed North American supply chain executives have a dedicated 2026 innovation budget, and nearly half are allocating at least USD 500,000. The same report also showed that established technologies are preferred over experimental deployments, which supports a broad shift toward proven automation tools. That is keeping automation near the center of competition in the United States 3PL warehousing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Labor Shortages and Wage Inflation | -0.8% | National, acute in coastal markets and high-growth Midwest and Southeast hubs | Short term (≤ 2 years) |

| Urban-Core Land Scarcity and Zoning Hurdles | -0.5% | Northeast, West Coast, and selected constrained infill markets | Long term (≥ 4 years) |

| Rising Interest-Rate Driven Cap-Ex Squeeze | -0.4% | National, most acute for mid-tier 3PLs pursuing greenfield development and automation programs | Medium term (2-4 years) |

| ESG Compliance Costs for Temperature-Controlled Sites | -0.3% | National, amplified in California, the Northeast, and cold-chain hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute Labor Shortages and Wage Inflation

Labor remains a direct limit on warehouse output because open positions are still elevated across the national logistics base. The latest JOLTS release showed more than 800,000 job openings in transportation, warehousing, and utilities in March 2026[3]“Job Openings and Labor Turnover Summary, 2026 M03 Results,” U.S. Bureau of Labor Statistics, bls.gov. Wage growth is compounding the issue, since transportation and warehousing compensation continued to rise through early 2026. High turnover makes the problem harder to solve because operators spend more time training and retraining staff instead of stabilizing productivity. Automation can ease some of the pressure, but it also increases the need for workers who can operate and support more technical systems. For that reason, labor remains one of the clearest near-term limits on the United States 3PL warehousing market.

Urban-Core Land Scarcity and Zoning Hurdles

Urban infill development remains difficult because the land supporting last-mile delivery is limited and is increasingly constrained by local zoning rules. The new industrial deliveries totaled 281 million square feet in 2025, the lowest annual volume since 2017 and 35% below 2024. That slowdown matters most in major consumption centers, where fast delivery expectations are strongest and replacement sites are scarce. Developers and operators are responding by shifting more projects toward secondary markets with better land access and smoother approvals. That helps add capacity, but it can also lengthen delivery routes and raise transport costs for dense urban demand zones. The result is that land scarcity and zoning hurdles continue to restrain the United States 3PL warehousing market, where service speed carries the highest value.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Storage Revenue Anchors the Base as Value-Added Services Accelerate

Storage accounted for 46.81% of the United States 3PL warehousing market in 2025, indicating that pallet and inventory capacity still form the basis of this market. That large share has remained resilient because many shippers are holding more domestic buffer stock to reduce exposure to tariff changes, lead-time volatility, and sourcing realignment. Distribution and inventory management also remain important for retailers and manufacturers running multi-channel inventory pools. Even so, the growth pattern has moved toward more labor-intensive services rather than pure storage contracts. Value-added services and others, including kitting, labeling, repackaging, and returns handling, are projected to expand at an 8.18% CAGR through 2031.

This faster growth reflects a customer mix that wants fulfillment partners to absorb more process steps inside the same warehouse footprint. ShipBob reported that brands are increasing channel counts and fulfillment complexity, which supports higher revenue per client even as total storage demand grows more slowly. That changes pricing discussions, because contracts move away from a narrow storage rate and toward charges tied to touches, handling rules, and service commitments. Kenco’s 5-year partnership with GreyOrange shows how mid-tier operators are using orchestration software and robotics to scale those higher-value activities across fulfillment centers. In the United States 3PL warehousing industry, this service mix shift supports margins for operators that can pair labor discipline with workflow automation.

By Warehouse Type: Multi-Client Flexibility Continues to Outsize Dedicated Formats

General shared or multi-client warehousing held 49.32% of United States 3PL warehousing market share in 2025, which confirms that flexibility still carries strong value after the inventory swings seen in 2024. Many shippers continue to prefer shared capacity because it allows them to scale space up or down without tying capital to dedicated buildings. This format also suits tenants that need regional coverage but do not yet want a site built around a single operating model. At the same time, dedicated contract warehousing is projected to grow at 7.35% through 2031, which is faster than any other warehouse format. That faster growth reflects a different customer set, mainly larger manufacturers and regulated shippers that want assured capacity once they commit to a more stable supply chain footprint.

The split between these 2 formats shows that the market is serving 2 kinds of risk management at once. Shared space helps customers stay flexible during volume swings, while dedicated space protects them against capacity shortages and price spikes once demand becomes more predictable. Bonded warehousing has also gained relevance as importers look for ways to defer duties and manage policy uncertainty around inbound goods. DSV’s 1.2 million-square-foot multi-client facility near Columbus, Ohio, which opened in early 2025, shows how a single asset can serve both high-spec industrial users and e-commerce tenants when the design is right. In the United States 3PL warehousing market, warehouse type selection increasingly depends on how much flexibility, compliance, and cost visibility each shipper needs.

By Temperature Control: Cold-Chain Outpaces Ambient Growth by a Wide Margin

Non-temperature-controlled warehousing accounted for 64.07% of the United States 3PL warehousing market in 2025, indicating that ambient space still dominates the installed base across the market. That position is expected because most industrial goods, consumer products, and standard retail inventory do not require specialized handling conditions. Still, temperature-controlled warehousing is projected to expand at 9.06% through 2031, which makes it the fastest-growing sub-segment in this category. The difference in growth rates points to a market where compliance and handling sensitivity are increasing faster than broad pallet demand. Food safety, biologics distribution, specialty therapies, and tighter customer service expectations are all adding weight to cold-chain investment decisions.

Lineage’s April 2025 Tyson transaction illustrates how large operators are securing long-term volume through anchor-tenant relationships while adding automated, modern facilities at scale. Americold’s 2025 sustainability report also showed more than USD 23 million invested in energy efficiency initiatives across its network, including automated refrigeration controls and optimization projects, which highlights how operating cost, ESG compliance, and facility modernization are now linked. Cold-chain operators therefore compete on certification, energy performance, and reliability instead of basic space alone. Ambient warehousing will remain the largest base, but the faster growth is clearly shifting toward temperature-managed networks. That keeps cold-chain specialization important across the broader United States 3PL warehousing industry.

By Technology Adoption: Semi-Automation Represents the Largest Transition Cohort

Semi-automated facilities accounted for 52.14% of the United States 3PL warehousing market share in 2025, which makes them the largest operating cohort in this market. That base includes facilities that use warehouse management systems, conveyor support, scanning, and limited robotics, without full end-to-end integration. It matters because these sites are the most likely candidates for the next round of capital deployment. Fully automated warehousing is projected to grow at 11.02% through 2031, which is well ahead of manual and semi-automated models. The spread between the largest and fastest-growing formats shows that the market is still in transition rather than at a final automation endpoint.

Kenco’s 2026 survey indicates that operators are not waiting for a single breakthrough technology before spending, since most already have defined budgets and clear priorities. GXO’s 2026 outlook also pointed to continued AI and robotics deployment across its United States warehouse network after another year with more than USD 1 billion in new business wins. That suggests automation is moving from an optional improvement to a standard client expectation in large accounts. Manual operations will remain relevant in lower-volume and irregular-item environments, but they are becoming more specialized rather than dominant. The United States 3PL warehousing market is therefore likely to see the biggest near-term change inside existing semi-automated facilities rather than only in brand-new robotic sites.

By End User Industry: Manufacturing Scale Masks Healthcare and Pharma Acceleration

Manufacturing held 34.95% of the United States 3PL warehousing market size in 2025, reflecting the scale of automotive, industrial, and chemicals programs that rely on warehousing for inbound flow control and outbound distribution. These customers often need stable operating routines, contractual capacity, and predictable sequencing support. That is why manufacturing remains the largest end-user base even as other sectors grow faster. Healthcare and pharma, however, are projected to expand at 8.48% through 2031, the fastest rate among end users. The growth gap shows that regulated storage and handling are becoming a larger part of overall warehouse demand.

Healthcare and pharma require stricter documentation, validated handling processes, and more controlled temperature ranges, which raise the value of specialized 3PL capacity. Consumer goods, food, and beverages also remain important because e-commerce, grocery, and shelf-ready requirements are increasing handling complexity across standard retail flows. Retail and e-commerce demand remains high, but the focus has shifted from opening new sites to improving returns handling, inventory placement, and forecasting accuracy within existing networks. DHL Group’s March 2026 announcement of 10 dedicated North American data center logistics sites adding more than 7 million square feet shows that higher-spec end uses outside traditional retail are also broadening the customer base for the United States 3PL warehousing market. As a result, the end-user mix is becoming more diverse even while manufacturing continues to hold the largest share.

Geography Analysis

The West held 26.6% of the United States 3PL warehousing market share in 2025, which kept it as the largest regional base. That position is tied to Pacific gateway cargo flows and to the deep distribution infrastructure built around Southern California. Even after the vacancy correction that followed the 2022 peak, large-format demand has remained firm in major western and adjacent inland corridors. National industrial vacancy was 7.0% in Q1 2026, and net absorption reached 40 million square feet, which supports the view that the market is moving back toward tighter conditions after the earlier oversupply phase. In practice, the West remains central to network design because it handles import-heavy freight while still offering the density required for fast replenishment[4]“Warehousing and Storage: NAICS 493,” U.S. Bureau of Labor Statistics, bls.gov.

The Southeast became the most active development corridor through 2025, with Dallas-Fort Worth, Atlanta, Nashville, Indianapolis, and Charlotte leading absorption gains. That activity is supported by port access, pro-industrial zoning in several states, and a steady pipeline of REIT-backed warehouse projects. LXP Industrial Trust reported 97.1% occupancy across its Southeast assets at the end of 2025, with rent growth on renewals above 29%, which shows how tight well-located logistics space remained in that region. The Midwest remains essential for national distribution because its rail connectivity and central geography help operators serve broad customer coverage with fewer total nodes.

The Southwest is the fastest-growing regional segment, with United States 3PL warehousing market size in the Southwest forecast to grow at 6.72% through 2031. Texas and Arizona are driving that pace because nearshoring flows from Mexico are concentrating more freight in border and inland corridors. Kuehne+Nagel’s El Paso expansion shows how quickly bonded and cross-border capacity can tighten once manufacturing and trade volumes build around those gateways. The same region is also benefiting from semiconductor and data-center related investment, which broadens warehouse demand beyond standard retail distribution. Secondary markets such as Phoenix, Reno, and Denver are attracting spillover from more constrained coastal locations, and that is helping the Southwest capture a larger share of new logistics capital. For the United States 3PL warehousing market, geography is increasingly shaped by a mix of trade exposure, land availability, and the ability to support specialized customers over long operating cycles.

Competitive Landscape

The United States 3PL warehousing market remains fragmented, but it still has a long tail of regional, specialist, and vertical-focused operators. Large national networks such as DHL Supply Chain, GXO Logistics, Ryder, and DSV compete on density, technology, and operating consistency, while Lineage and Americold hold strong positions in temperature-controlled logistics. That means scale alone is not enough, because customers are increasingly choosing providers based on service depth, compliance profile, and automation readiness. The result is a market where major operators have clear advantages in large national contracts, but smaller firms can still win in specialized lanes, regulated sectors, and regional manufacturing corridors. Competition has become more intense in the mid-market, where providers such as Kenco, NFI Industries, and Saddle Creek are pursuing dedicated contracts and higher-value service work.

A major shift came in April 2025 when DSV completed its acquisition of DB Schenker, creating a larger combined logistics platform and making the United States a priority integration market. GXO is pushing a different strategy by combining customer-specific automation with contract expansion, and the company said its new business wins exceeded USD 1 billion for the third straight year in its full-year 2025 results. Kenco has used both acquisition and technology partnership moves to strengthen its position, including the addition of The Shippers Group and the GreyOrange orchestration partnership. These moves show that operators are investing to deepen capability, not only to expand footprint.

Specialized white spaces remain open in pharmaceutical-grade cold chain, bonded warehousing for duty-sensitive importers, and data-center equipment logistics. DHL Group’s plan to add more than 7 million square feet across 10 dedicated North American data center logistics sites is a good example of how large providers are targeting these less crowded niches. Americold and Lineage are also shaping competition through cold-chain modernization, where capital intensity and compliance create higher barriers to entry than in standard dry storage. Compliance standards such as CTPAT, GMP-aligned food handling, GDP, and ISO-based quality systems are becoming basic entry requirements for major contracts rather than optional differentiators. This is making the United States 3PL warehousing market harder for underinvested operators to serve at scale. The competitive gap is therefore widening between providers that can finance compliance, automation, and network expansion, and those that cannot.

United States 3PL Warehousing Industry Leaders

DHL Group

GXO Logistics

Ryder System, Inc.

United Parcel Services of America, Inc. (UPS)

FedEx

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Penske Logistics launched Supply Chain Insight, a cloud-native platform built on Microsoft Azure with Snowflake as the core data engine, offering 85+ KPIs for consolidated transportation, warehousing, and partner data across the full supply chain network.

- March 2026: GXO Logistics and Hasbro opened a new flagship 600,000-square-foot distribution center in Midway, Liberty County, Georgia, powered by GXO IQ, an AI-powered, cloud-native WMS. The facility supports omnichannel distribution and Hasbro Pulse direct-to-consumer operations, employing up to 125 seasonal workers during peak holiday periods.

- January 2026: Penske Logistics partnered with Augment to deploy an agentic AI supply chain platform, validating approximately 600,000 loads in its initial phase with an anticipated 30-40% productivity gain by automating routine tracking, dispatch, and carrier communication processes.

- November 2025: Kuehne+Nagel expanded its El Paso, Texas facility by 60% through a new 20,252-square-meter bonded warehouse adjacent to its existing 33,723-square-meter site, which had reached full capacity within a year of opening, adding 53 dock doors, 65 trailer spaces, and cross-dock capabilities for northbound and southbound US-Mexico freight.

United States 3PL Warehousing Market Report Scope

| Storage |

| Distribution and Inventory Management |

| Value-Added Services and Others (Kitting, Labeling) |

| General Shared / Multi-client Warehousing |

| Dedicated Contract Warehousing |

| Bonded Warehousing |

| Non-Temperature Controlled |

| Temperature Controlled |

| Manual |

| Semi-automated |

| Fully Automated |

| Manufacturing |

| Consumer Goods |

| Food and Beverage |

| Retail and E-commerce |

| Healthcare and Pharma |

| Other End-user Industries |

| Northeast |

| Southeast |

| Midwest |

| Southwest |

| West |

| By Service Type | Storage |

| Distribution and Inventory Management | |

| Value-Added Services and Others (Kitting, Labeling) | |

| By Warehouse Type | General Shared / Multi-client Warehousing |

| Dedicated Contract Warehousing | |

| Bonded Warehousing | |

| By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | |

| By Technology Adoption | Manual |

| Semi-automated | |

| Fully Automated | |

| By End User Industry | Manufacturing |

| Consumer Goods | |

| Food and Beverage | |

| Retail and E-commerce | |

| Healthcare and Pharma | |

| Other End-user Industries | |

| By Region | Northeast |

| Southeast | |

| Midwest | |

| Southwest | |

| West |

Key Questions Answered in the Report

How large is the United States 3PL warehousing market in 2026?

The United States 3PL warehousing market is valued at USD 76.78 billion in 2026 and is projected to reach USD 99.6 billion by 2031 at a 5.34% CAGR.

Which service category leads current revenue generation?

Storage is the largest service category, with a 46.81% share in 2025, because basic inventory holding still anchors most warehouse contracts.

Which warehouse format is growing the fastest?

Dedicated contract warehousing is the fastest-growing format, with a 7.35% CAGR through 2031, as larger shippers seek secured capacity and more operating control.

Why is cold-chain capacity growing faster than ambient space?

Temperature-controlled warehousing is projected to grow at 9.06% through 2031 because food safety, pharma handling, and traceability requirements raise the need for specialized 3PL facilities.

What is driving automation investment across the United States 3PL facilities?

Rising labor costs, persistent job openings, and the need for better throughput are pushing operators toward robotics, AI-enabled workflows, and semi-to-fully automated site upgrades.

Which region shows the strongest growth outlook?

The Southwest is the fastest-growing region, with a 6.72% CAGR through 2031, supported by nearshoring flows, border logistics demand, and manufacturing investment in Texas and Arizona.

Page last updated on: