Germany Chemical Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

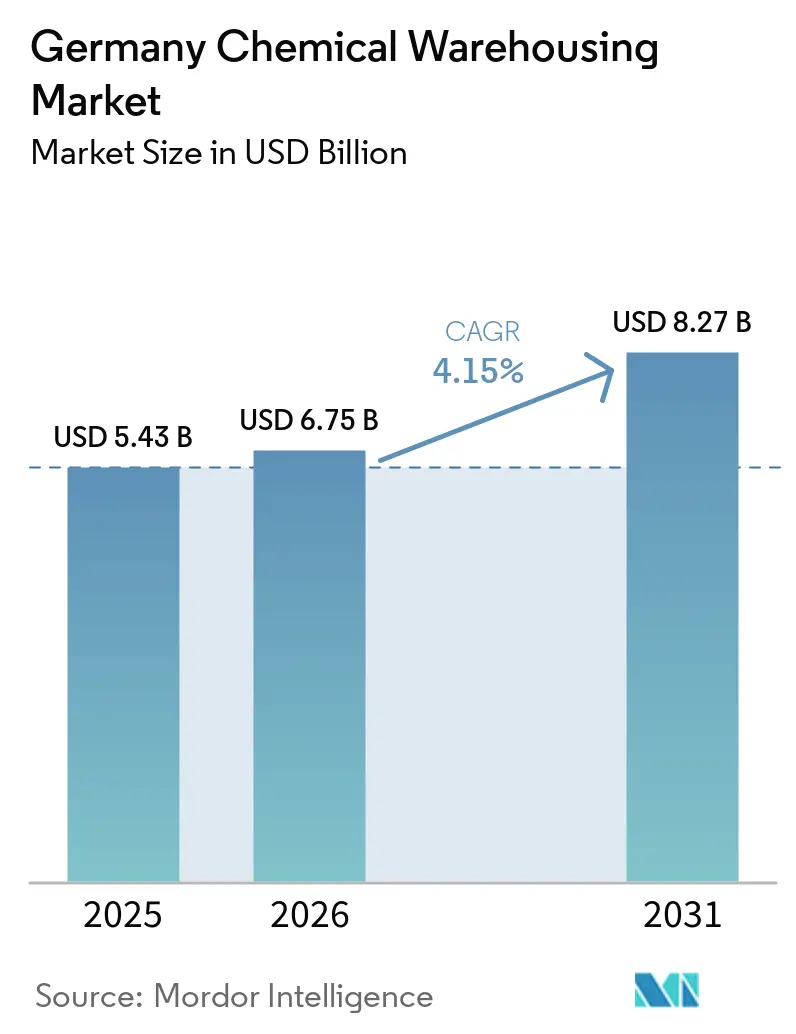

| Base Year Market Size (2025) | USD 5.43 Billion |

| Market Size (2026) | USD 6.75 Billion |

| Market Size (2031) | USD 8.27 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

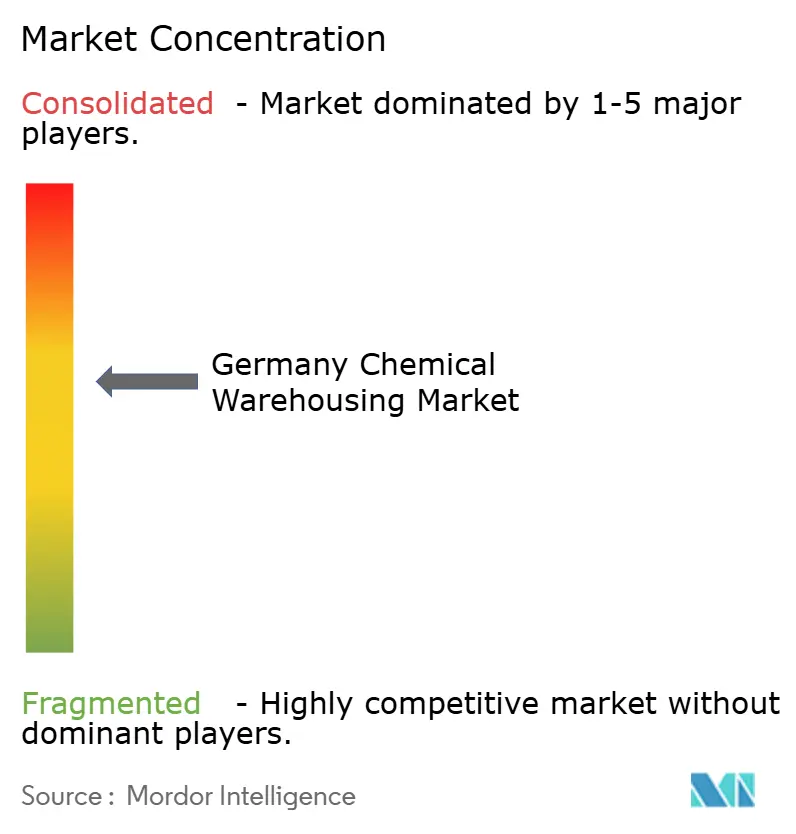

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Chemical Warehousing Market Analysis by Mordor Intelligence

The Germany chemical warehousing market size is expected to increase from USD 5.43 billion in 2025 to USD 6.75 billion in 2026 and reach USD 8.27 billion by 2031, growing at a CAGR of 4.15% over 2026-2031.

Germany’s evolving chemicals mix, tighter REACH Annex VIII rules, and the rise of battery-materials clusters are reshaping storage requirements well beyond traditional petrochemical and specialty-chemical inventories. Operators able to prove granular traceability, handle sub-zero biologics, and manage liquid CO₂ for carbon-capture pilots are winning long-term contracts. In contrast, volatile industrial power tariffs lift climate-control costs, and Burgerinitiative activism stretches permitting cycles, making site selection and energy strategy pivotal for margins.

Key Report Takeaways

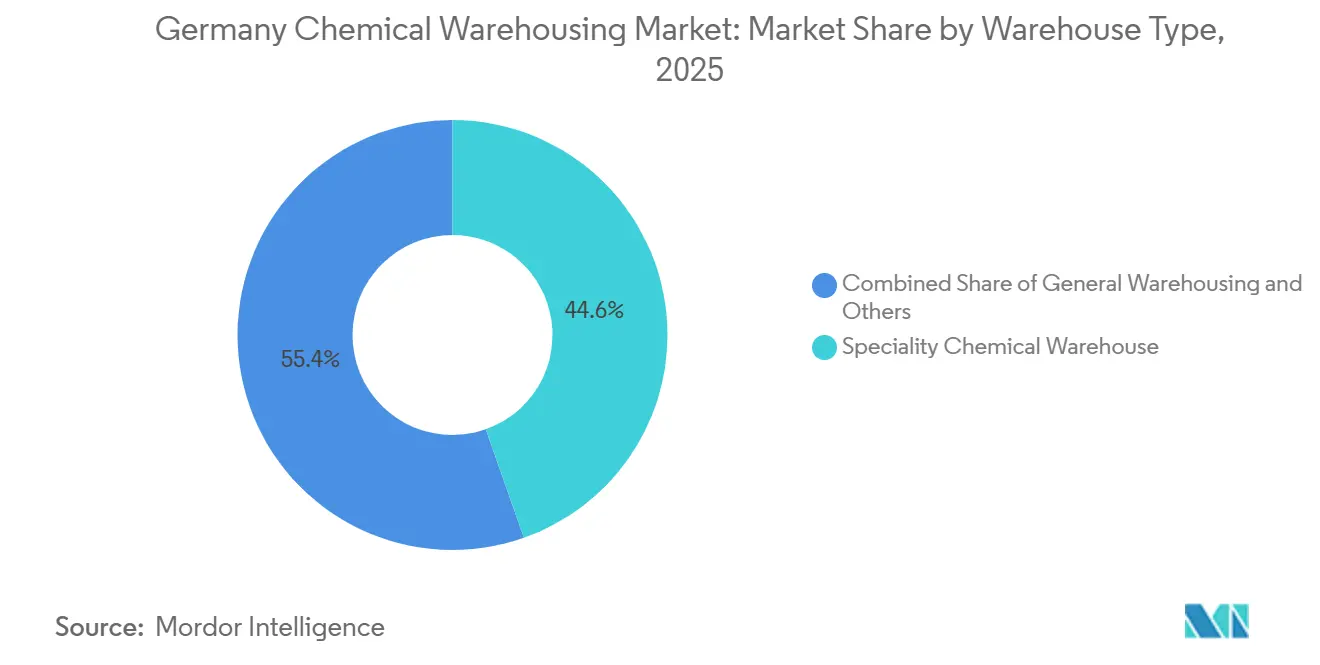

- By warehouse type, specialty chemical warehouses captured 44.65% of the Germany chemical warehousing market share in 2025, whereas temperature-controlled chemical warehouses are forecast to post the fastest 5.77% CAGR to 2031.

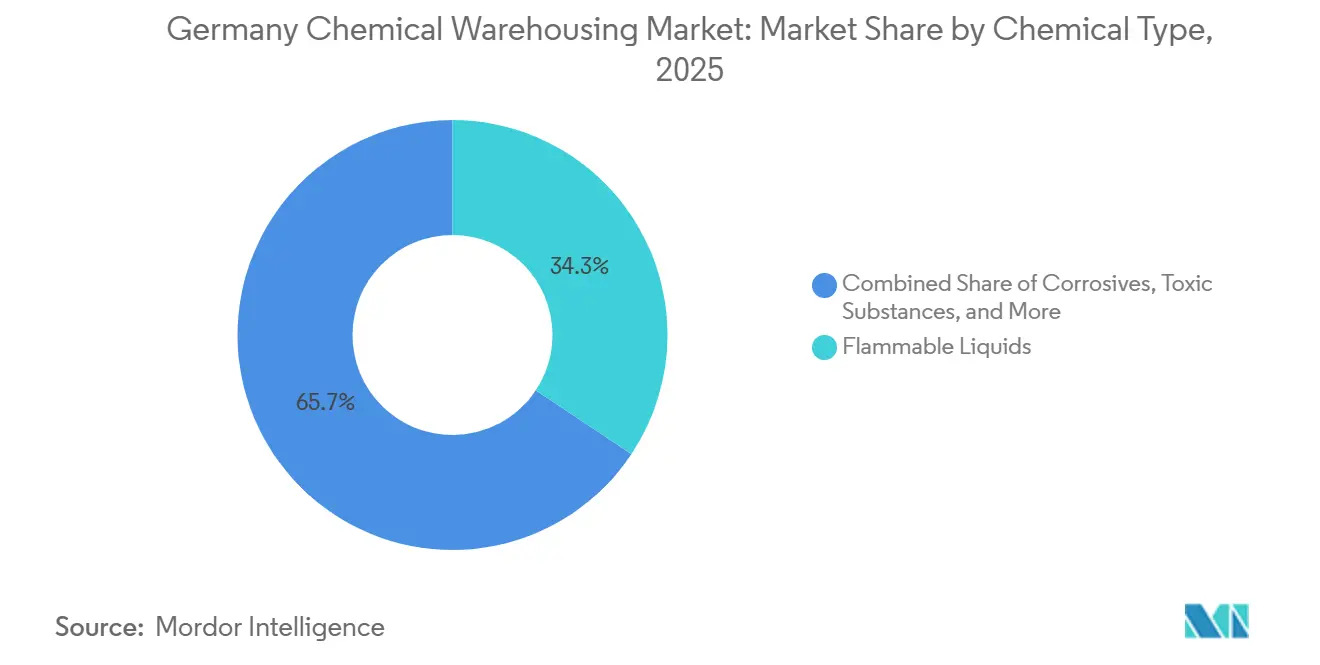

- By chemical type, flammable liquids led with 34.33% share of the Germany chemical warehousing market size in 2025, yet toxic substances storage is projected to expand at a 5.85% CAGR through 2031.

- By end-user industry, specialty chemicals manufacturing accounted for 34.37% of Germany chemical warehousing market size in 2025, while pharmaceuticals & life sciences are advancing at a 5.80% CAGR on the back of biologics and cell-therapy scale-ups.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of Germany. The chemical warehousing market share in our global report expresses these relative weights.

Germany Chemical Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enforcement-driven demand for REACH Annex VIII-compliant storage | +0.7% | National manufacturing hubs | Short term (≤ 2 years) |

| East-German battery-materials boom boosting solvent & electrolyte warehousing | +0.6% | Saxony, Brandenburg, Thuringia | Medium term (2-4 years) |

| Biochemical scale-ups requiring segregated GMO-free storage zones | +0.5% | National biotech clusters | Medium term (2-4 years) |

| Deployment of modular “ChemCube” micro-warehouses near innovation campuses | +0.4% | Urban innovation districts | Long term (≥ 4 years) |

| CCU pilot plants are creating a need for liquid CO₂ and intermediate storage | +0.3% | NRW, coastal regions | Long term (≥ 4 years) |

| Railport electrification catalyzing multimodal chemical hubs | +0.3% | Rhine-Ruhr corridor, Hamburg hinterland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Enforcement-Driven Demand for REACH Annex VIII Compliant Storage

Since January 2024, the European Chemicals Agency has intensified audits that test whether warehouses can segregate and trace mixtures at the batch level, compelling upgrades in inventory software, RFID tagging, and dedicated ventilation zones. In 2025, 34% of inspected German facilities failed segregation tests, triggering retrofit bills of EUR 1.2-1.8 million (USD 1.3-2.0 billion) per mid-sized site. Larger 3PLs amortize these costs across national networks, gaining price power, while smaller depots face margin compression or forced exit from the Germany chemical warehousing market. Blockchain-based chain-of-custody modules are becoming standard add-ons to warehouse-management systems, creating a new tech-service revenue stream for leading operators.

East-German Battery-Materials Boom Boosting Solvent & Electrolyte Warehousing

BASF’s cathode plant in Schwarzheide and Northvolt’s gigafactory pipeline ignite demand for lithium-salt and electrolyte solvent storage engineered for <100 ppm humidity and nitrogen blanketing. Land in Saxony and Brandenburg costs 30-40% below western zones, drawing developers eager to supply bespoke “dry-room” warehouses that interface with ISO tank cleaning stations. As automotive OEMs push for regionalized supply chains, intermodal routes linking eastern chemical hubs to final assembly plants reinforce the Germany chemical warehousing market’s eastward shift[1]BASF, “Schwarzheide Cathode Materials Investment,” BASF, basf.com.

Biochemical Scale-Ups Requiring Segregated GMO-Free Storage Zones

EU GMO labeling rules cap accidental GMO presence at 0.9%, prompting bio-based chemical producers to demand certified GMO-free warehousing. German capacity for recombinant proteins and bio-PDO grew 18% over 2024-2025, and certified warehouses now command 15-20% rate premiums. Pharmaceutical-grade depots extend clean-room protocols to chemical storage, leveraging existing validation systems to win biotech contracts within the Germany chemical warehousing market[2]European Commission, “GMO Labeling Regulations,” EC, ec.europa.eu.

Deployment of Modular “ChemCube” Micro-Warehouses Near Innovation Campuses

Prefabricated, 200-500 m² hazmat units can be installed in 8-12 weeks, reducing upfront capex by up to 70%. DHL’s 2026 rollout across Munich, Berlin, and Heidelberg innovation zones exemplifies the model’s appeal to start-ups seeking flexible lease terms. As Germany’s research campuses commercialize laboratory breakthroughs, micro-warehouses close the logistics gap between bench-scale chemistry and industrial supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile energy tariffs are inflating refrigeration & ventilation Opex | –0.5% | National, temperature-controlled sites | Short term (≤ 2 years) |

| Stricter DIN 14096 fire-protection code prolonging certification cycles | –0.3% | National facilities | Medium term (2-4 years) |

| Regulatory limbo on Li-ion bulk storage delaying investment decisions | –0.2% | Battery-materials hubs | Short term (≤ 2 years) |

| Bürgerinitiative-led opposition stalling hazmat site permitting | –0.2% | Bavaria, Hesse, Baden-Württemberg | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Energy Tariffs Inflating Refrigeration & Ventilation Opex

Industrial electricity prices in 2025 remained highly volatile and elevated across Europe, significantly increasing operating costs for temperature-controlled and sub-zero warehousing. This led to a meaningful rise in refrigeration and energy-related expenses year over year. Some mid-sized pharma-grade logistics operators were forced to exit parts of the German chemical warehousing market after struggling to renegotiate long-term fixed energy contracts. Although onsite solar and battery storage solutions help reduce grid dependence and improve efficiency, their high upfront capital requirements limit adoption mainly to larger, well-capitalized players.

Stricter DIN 14096 Fire-Protection Code Prolonging Certification Cycles

As of 2025, stricter fire safety requirements for flammable-liquid storage, including higher sprinkler density standards, have significantly increased compliance complexity for new warehouse developments. This has extended certification timelines, slowing the commissioning of new facilities and tightening available capacity in regulated segments. At the same time, elevated retrofit costs per square meter are putting pressure on older depots, forcing operators to either invest heavily in upgrades or consider exiting the market. As a result, compliant, modern facilities are gaining stronger pricing power, accelerating consolidation within the industrial and chemical warehousing sector[3]DIN, “DIN 14096 Fire Protection Standard,” Deutsches Institut für Normung, din.de .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Specialty Dominance Meets Cold-Chain Acceleration

Specialty chemical warehouses represented 44.65% of the Germany chemical warehousing market size in 2025, anchored by the country’s EUR 200 billion (USD 234.36 billion) chemicals base. Temperature-controlled depots, although smaller, are projected to grow at a 5.77% CAGR, driven by biologics, mRNA vaccines, and high-value excipients requiring -80 °C to 25 °C multipoint storage. Energy-efficient refrigeration, robotic shuttles, and IoT climate sensors differentiate market leaders, while smaller general warehouses struggle to finance DIN 14096 upgrades and lose share inside the Germany chemical warehousing market.

A second wave of investment now targets smart cold-chain nodes that co-locate -80 °C freezers and 2-8 °C rooms under one roof, cutting transit risks for cell therapies. Operators that combine these zones with specialty bays for catalysts or electronic chemicals increase cross-selling potential. As consolidation proceeds, multi-temperature mega-sites position themselves as one-stop hubs for pharmaceutical and specialty clients.

By Chemical Type: Toxic Substances Outpace Traditional Flammables

Flammable liquids held 34.33% of the Germany chemical warehousing market size in 2025, reflecting the country’s petrochemical heritage. Yet, toxic substances storage is forecast to rise at a 5.85% CAGR on surging API and agrochemical throughput. Battery-grade lithium salts need nitrogen-blanketed, ultra-dry rooms that overlap with toxic-class requirements, magnifying growth.

Operators developing multi-classification campuses with physically segregated cells can host flammables, toxics, and corrosives in one permitted footprint, extracting greater yield per hectare of zoned industrial land. Imminent EU PFAS foam restrictions spur investment in fluorine-free suppression, a shift that favors new builds over legacy depots inside the Germany chemical warehousing market.

By End-User Industry: Pharma Surge Reshapes Demand Mix

Specialty chemicals manufacturing accounted for 34.37% of 2025 demand, but pharmaceuticals & life sciences show the fastest 5.80% CAGR to 2031. Outsourced 3PL models dominate, as BioNTech’s Mainz campus and Boehringer Ingelheim’s Biberach plant rely on external GDP-certified cold-chain warehousing. Basic chemicals remain volume staples, while agrochemicals benefit from precision-farming trends.

Warehouse operators able to layer GMP, GDP, and GMO-free certifications on a single site win multi-industry contracts. End-user diversification shields revenues from single-sector downturns, a trait valued by investors appraising the Germany chemical warehousing industry’s resilience.

Geography Analysis

North Rhine-Westphalia anchors the largest warehouse footprint, clustering capacity around CHEMPARK Leverkusen, Dormagen, and Marl. Baden-Württemberg follows with Ludwigshafen’s mega-site and pharma corridors near Stuttgart. Bavaria maintains agrochemical and specialty clusters but faces strong local permitting resistance that slows new HAZMAT builds. Hamburg’s port-adjacent depots command premium rents for customs-bonded storage and seamless ocean-rail transfer, forming a critical import-export valve for the Germany chemical warehousing market.

East German states Saxony, Brandenburg, and Thuringia are becoming capacity frontiers, catalyzed by battery-materials plants and government land grants. Developers trade lower land prices for investments in workforce upskilling and utility upgrades. Railport electrification along the Betuweroute improves access to Rhine-Ruhr consumers, mitigating the risk of river-low-water disruptions. Lower Saxony and Schleswig-Holstein see rising CCU and hydrogen projects that will need cryogenic CO₂ and ammonia storage over the next decade.

Regional strategies, therefore, balance cost, infrastructure, and permitting timelines. Operators diversify footprints: mature western hubs offer dense supplier networks and rapid emergency response, while eastern builds secure long-dated growth options and faster approvals, collectively stabilizing service levels across the Germany chemical warehousing market.

Mordor Intelligence examines the chemical warehousing market across diverse other regional markets as well, including Europe, North America, and Middle East, while also offering granular country-level perspectives for United Kingdom, Italy, Canada, France, Japan, and China and more.

Competitive Landscape

The top five providers, DSV, DHL Supply Chain, Rhenus, HOYER, and TALKE, control about 38% of national capacity, signaling moderate concentration. DSV’s 2024 acquisition of DB Schenker lifted its share to roughly 12%, creating a scale advantage in IT amortization and network density. Market leaders deploy IoT sensors for Annex VIII traceability, AI-driven slotting, and blockchain custody, whereas smaller depots upgrade selectively, often supported by German development-bank green loans.

Strategic moves emphasize vertical integration: HOYER’s 2026 battery-electrolyte site couples storage with tank cleaning and nitrogen supply. TALKE’s RFID rollout across five warehouses demonstrates how digitized compliance can become a selling point to specialty clients. Niche specialists prosper by offering cryogenic CO₂ cells for CCU pilots or GMO-free certification for biochemical intermediates. Modular micro-warehouses, championed by DHL, introduce a new competitive tier targeted at start-ups and campus labs[4]TALKE, “REACH Annex VIII Compliance Investment,” TALKE, talke.com .

Energy volatility and DIN 14096 retrofits accelerate consolidation, but regulatory complexity also raises entry barriers, protecting incumbent margins. The Germany chemical warehousing market therefore exhibits a steady shift from fragmented regional players toward scale-driven or deeply specialized operators.

Germany Chemical Warehousing Industry Leaders

DHL Group

Rhenus Logistics

HOYER Group

TALKE Logistics

Bertschi AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: DHL Supply Chain announced a carbon-neutral logistics hub in Rheinbach, Germany (26,600 m²). The site enhances regional warehousing capacity for industrial and chemical clients, especially in the Rhineland cluster.

- March 2026: DHL Supply Chain extended its logistics partnership with iglo Germany for another five years. DHL will continue managing central warehouse and in-plant logistics operations, demonstrating long-term contracts and operational stability in Germany-based warehousing.

- February 2026: DHL Group expanded its global airfreight cold chain network for healthcare logistics. This strengthens temperature-controlled storage and transport capabilities, which are directly applicable to chemical and specialty materials logistics.

- April 2025: DSV completed the acquisition of DB Schenker. This created one of the largest global logistics companies, significantly strengthening warehousing and chemical logistics capabilities in Germany.

Germany Chemical Warehousing Market Report Scope

| General Warehousing |

| Speciality Chemical Warehouse |

| Hazardous Materials (HAZMAT) Warehouses |

| Temperature-Controlled Chemical Warehouses |

| Flammable Liquids |

| Corrosives |

| Toxic Substances |

| Oxidizers |

| Others |

| Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing |

| Pharmaceuticals & Life Sciences |

| Agrochemicals |

| Paints, Coatings & Adhesives |

| Food & Feed Additives |

| Oil & Gas / Petrochemicals |

| Others |

| By Warehouse Type | General Warehousing |

| Speciality Chemical Warehouse | |

| Hazardous Materials (HAZMAT) Warehouses | |

| Temperature-Controlled Chemical Warehouses | |

| By Chemical Type | Flammable Liquids |

| Corrosives | |

| Toxic Substances | |

| Oxidizers | |

| Others | |

| By End-user Industry | Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing | |

| Pharmaceuticals & Life Sciences | |

| Agrochemicals | |

| Paints, Coatings & Adhesives | |

| Food & Feed Additives | |

| Oil & Gas / Petrochemicals | |

| Others |

Key Questions Answered in the Report

How large is the Germany chemical warehousing market today?

The Germany chemical warehousing market size is USD 6.75 billion in 2026, on track to reach USD 8.27 billion by 2031.

What CAGR is forecast for German chemical warehousing between 2026 and 2031?

Market value is projected to grow at a 4.15% CAGR over the 2026-2031 period.

Which warehouse type is expanding fastest?

Temperature-Controlled Chemical Warehouses lead growth with a 5.77% CAGR through 2031, driven by biologics and mRNA vaccine logistics.

Which chemical class shows the strongest demand momentum?

Storage of Toxic Substances, such as pharmaceutical APIs and battery salts, is forecast to rise at a 5.85% CAGR to 2031.

What is the main regulatory driver affecting warehouse investments?

Strict enforcement of REACH Annex VIII traceability rules is triggering multi-million-euro upgrades across German facilities.

How are energy costs impacting warehouse operators?

Power price volatility lifted refrigeration and ventilation expenses by up to 28% in 2025, prompting solar and battery installations to hedge future tariffs.

Page last updated on: