Saudi Arabia 3PL Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

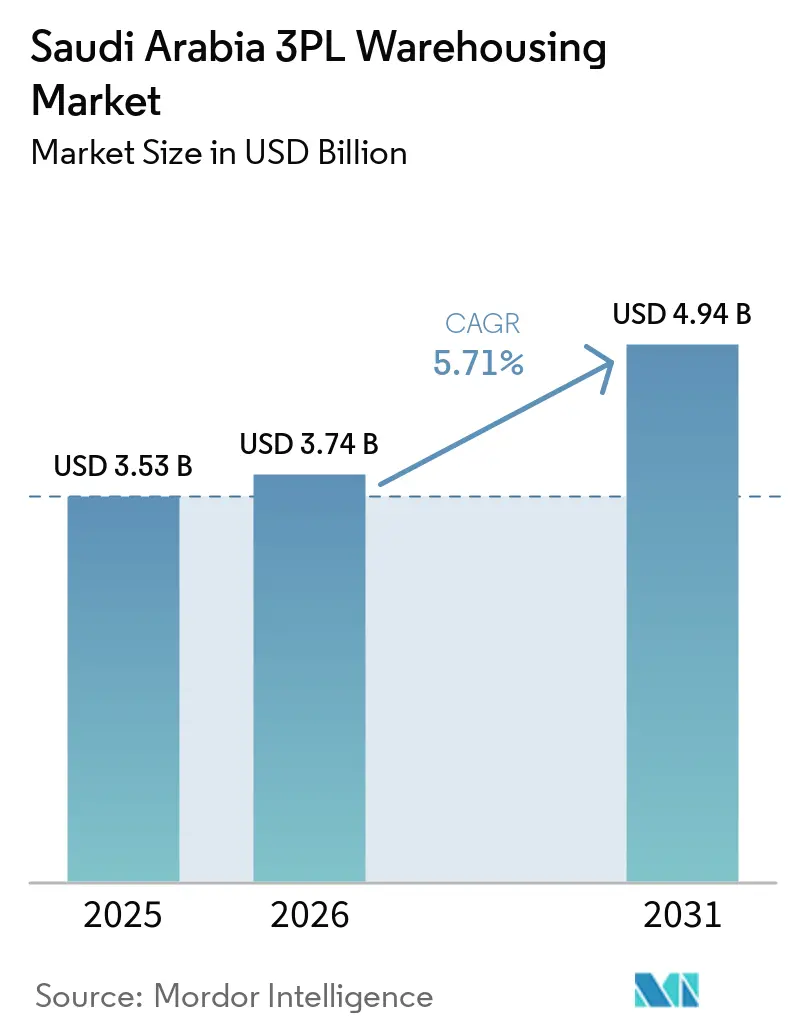

| Base Year Market Size (2025) | USD 3.53 Billion |

| Market Size (2026) | USD 3.74 Billion |

| Market Size (2031) | USD 4.94 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia 3PL Warehousing Market Analysis by Mordor Intelligence

The Saudi Arabia 3PL warehousing market size was valued at USD 3.53 billion in 2025 and estimated to grow from USD 3.74 billion in 2026 to reach USD 4.94 billion by 2031, at a CAGR of 5.71% during the forecast period (2026-2031).

The National Industrial Development and Logistics Program activated 24 logistics centers by 2025 within a master plan of 60, reinforcing a spatial infrastructure pull on 3PL operators. The logistics sector contributed SAR 82 billion (USD 21.84 billion) to GDP in 2025 and employed 421,000 professionals, while national policy continues to target SAR 115 billion (USD 30.64 billion) in GDP contribution and 600,000 jobs by 2030. Demand in the Saudi Arabia 3PL warehousing market is also being supported by SAR 280 billion (USD 74.60 billion) in transport and logistics investment contracts, with 80% of the logistics project pipeline open to private participation. Outsourced warehousing is gaining ground as logistics centers, port-linked infrastructure, and modern distribution networks replace fragmented in-house storage across retail, manufacturing, and trade flows. The SAR 7 billion (USD 1.86 billion) Landbridge railway is adding another layer of demand because intermodal freight flows require bonded and transfer-oriented storage buffers between rail, road, and port nodes, which supports long-term capacity needs in the Saudi Arabia 3PL warehousing market.

Key Report Takeaways

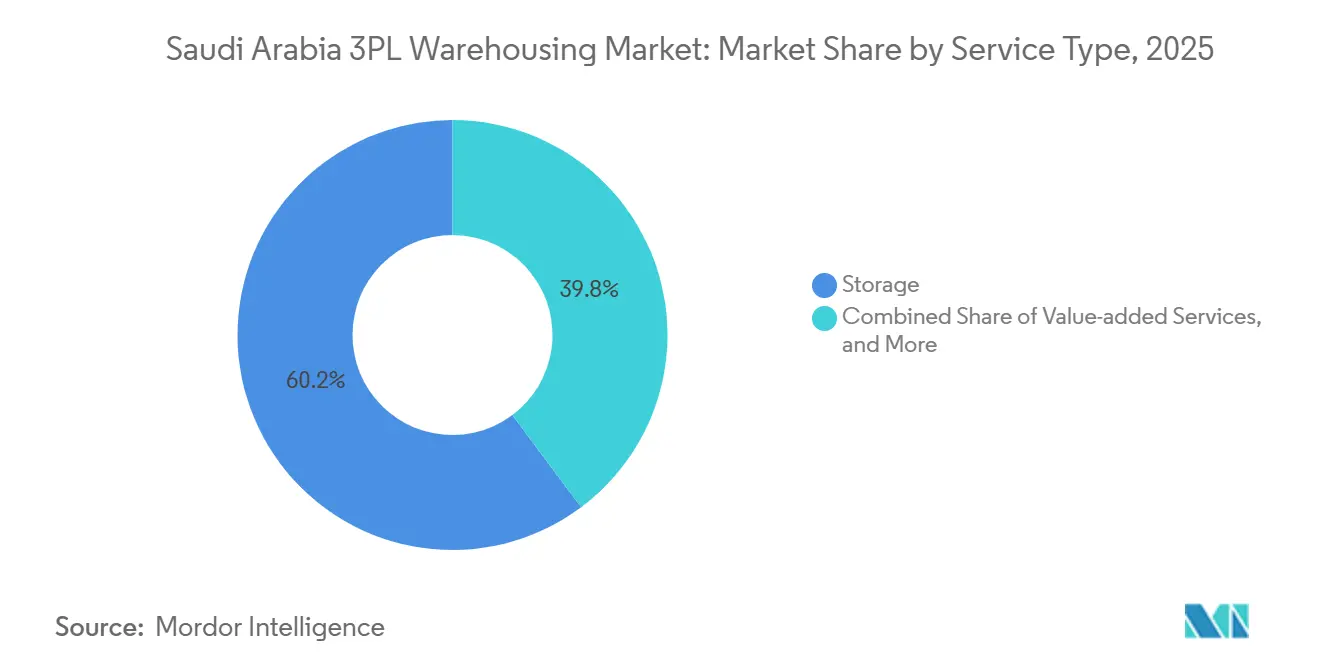

- By service type, storage led with 60.21% of the Saudi Arabia 3PL warehousing market size in 2025, while value-added services recorded the highest projected CAGR at 8.55% through 2031.

- By warehouse type, general shared or multi-client warehousing held 53.09% of the Saudi Arabia 3PL warehousing market share in 2025, while bonded warehousing posted the fastest projected CAGR at 7.72% through 2031.

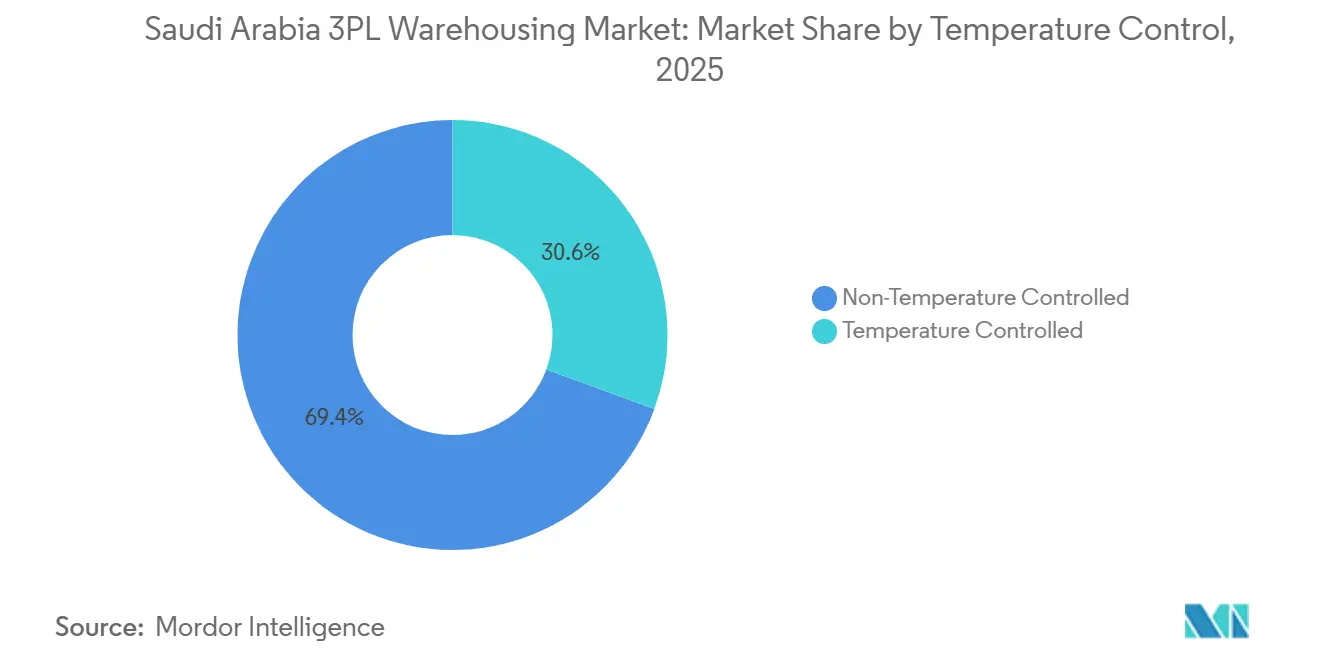

- By temperature control, non-temperature-controlled warehousing accounted for 69.4% of the Saudi Arabia 3PL warehousing market share in 2025, while temperature-controlled warehousing is forecast to advance at a 9.43% CAGR through 2031.

- By technology adoption, manual warehousing captured 63.83% of the Saudi Arabia 3PL warehousing market share in 2025, while fully automated warehousing is forecast to expand at an 11.39% CAGR through 2031.

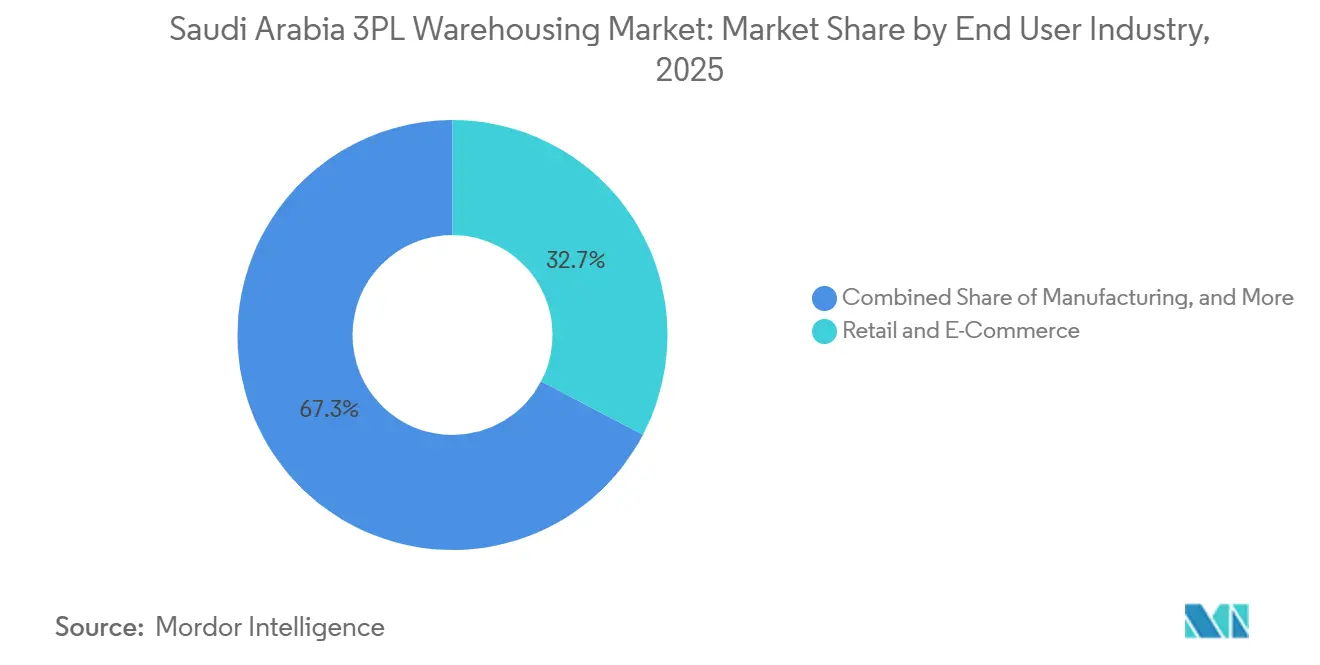

- By end user industry, retail and e-commerce accounted for 32.67% of the Saudi Arabia 3PL warehousing market size in 2025, while healthcare and pharma recorded the highest projected CAGR of 8.85% through 2031.

- By geography, Central Saudi Arabia held 42.5% of the Saudi Arabia 3PL warehousing market in 2025, while Western Saudi Arabia is forecast to grow at a 7.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia 3PL Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Logistics Infrastructure Investments | +1.6% | National, concentrated in Riyadh, Jeddah, Dammam, and 24 activated logistics centers | Long term (≥ 4 years) |

| Rising E-Commerce Order Volumes | +1.3% | National, led by Riyadh, Makkah, and Eastern Province | Short term (≤ 2 years) |

| Expansion of FMCG and Modern Retail Networks | +0.7% | National, with strong pull in Riyadh and Jeddah and growing relevance in Madinah and Dammam | Medium term (2-4 years) |

| FDI Liberalization of the Logistics Sector | +0.6% | National, with early gains in KAEC, Jazan SEZ, SPARK, and SILZ | Medium term (2-4 years) |

| Cold-Chain Demand for Domestic Vaccine Production | +0.5% | National, with pharmaceutical concentration in Riyadh and food cold-chain pull in Eastern and Western Saudi Arabia | Long term (≥ 4 years) |

| Re-Export Push Via Bonded SEZs | +0.4% | KAEC, Ras Al-Khair, Jazan, and SILZ | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Logistics Infrastructure Investments

Government-backed logistics buildout is widening the addressable base for the Saudi Arabia 3PL warehousing market. More than USD 75 billion in transport and logistics investment contracts have been signed since the launch of Vision 2030, and the Budget Forum 2026 confirmed SAR 280 billion (USD 74.60 billion) in total contracts, with 80% of the pipeline open to private investment. The National Transport and Logistics Strategy continues to frame warehousing demand around integrated logistics platforms rather than isolated storage estates[1]“National Transport and Logistics Strategy,” Ministry of Transport and Logistics Services, mot.gov.sa. The logistics-center rollout and the rise in port throughput are pushing more cargo into compliant Grade A facilities that support distribution, customs handling, and value-added services. This raises outsourcing demand because manufacturers and retailers that do not operate facilities at the required service standard are increasingly shifting volumes to specialized 3PL providers in the Saudi Arabia 3PL warehousing market.

Rising E-Commerce Order Volumes

Order growth is raising space demand and service complexity across the Saudi Arabia 3PL warehousing market. Saudi Arabia’s delivery sector processed more than 118 million orders in Q1 2026, up 49% year over year, after 124 million orders in Q4 2025 and 103 million in Q3 2025. Riyadh accounted for 44% of Q1 2026 delivery orders, while Makkah and the Eastern Province followed with 22.2% and 16.2%, which explains why fulfillment investment remains concentrated in the Central and Western corridors. Modern Trade still carried 70% of FMCG distribution in 2025, but e-commerce gained 2 percentage points year over year to reach 5.6% of FMCG sales, which changed order profiles from pallet movement to each-pick and returns-heavy workflows. This shift is supporting higher demand for kitting, labeling, returns handling, and flexible floor layouts, which lifts the revenue mix for operators that can combine storage with service-intensive fulfillment in the Saudi Arabia 3PL warehousing market.

Expansion of FMCG and Modern Retail Networks

Retail expansion remains a durable demand source for the Saudi Arabia 3PL warehousing market because physical store growth still needs consolidated replenishment capacity. Saudi Arabia’s food retail sales exceeded USD 50 billion in 2024 and were expected to grow 5% in 2025, while 5 major chains, LuLu, Tamimi, Panda, Danube, and Othaim, represented more than 80% of retail revenues[2]“Retail Foods Annual, Saudi Arabia,” USDA GAIN Report, apps.fas.usda.gov. BinDawood Holding added 9 new retail locations in FY 2025, including 4 supermarkets and 5 Dash convenience stores, indicating continued inventory pooling and store-support needs. Spinneys also entered Saudi Arabia with plans to reach 12 stores in Riyadh and Jeddah by 2028, reinforcing the case for regional distribution hubs serving modern retail footprints. As organized retail replaces fragmented wholesaler networks, warehousing demand is shifting toward integrated storage, labeling, and replenishment services, which support longer contracts and more stable utilization in the Saudi Arabia 3PL warehousing market.

Re-Export Push Via Bonded SEZs

Bonded trade policy is widening the role of the Saudi Arabia 3PL warehousing market in regional redistribution flows. Saudi Arabia approved regulatory frameworks for 4 special economic zones in January 2026, and the rules took effect on April 16, 2026, offering suspended customs duties, zero withholding tax, and zero VAT on inter-SEZ transfers for qualifying operators. Draft regulations published in April 2026 set out Central Bonded Zones and Dedicated Bonded Zones, providing 3PL operators with both shared and investor-controlled formats for handling customs-sensitive cargo. The Riyadh Integrated Special Logistics Zone, next to King Khalid International Airport, adds a bonded air cargo layer to the wider logistics network and links domestic distribution with international freight corridors. Re-export logistics centers had already expanded to 23 by 2024, so policy incentives are reinforcing an established trade direction rather than creating a new one from zero. This makes bonded warehousing a stronger commercial proposition in the Saudi Arabia 3PL warehousing market because one licensed site can serve import, export, and re-export flows with better asset utilization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Industrial-Land and Warehouse Construction Costs | -0.8% | National, acute in Riyadh, Jeddah, and Dammam prime logistics corridors | Long term (≥ 4 years) |

| Skilled Labor Shortages in Advanced Warehousing | -0.6% | Eastern Province and Riyadh, with spillover across all major logistics hubs | Medium term (2-4 years) |

| Patchy Digitization of Inland Customs Clearance | -0.3% | Inland dry ports and secondary city customs points | Short term (≤ 2 years) |

| Grid Reliability Challenges for Remote Cold Stores | -0.3% | Northern and Southern Saudi Arabia and secondary cities with weaker backup systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Industrial-Land and Warehouse Construction Costs

Rising development costs are limiting the speed at which new Grade A space can be added to the Saudi Arabia 3PL warehousing market. Riyadh’s industrial and logistics construction cost reached USD 3,112 per square meter in 2025, up from USD 2,593 per square meter in 2024. Saudi Arabia’s Construction Cost Index rose 1.1% year over year in December 2025, with energy costs up 9.9% and labor costs up 1.7%, which confirms that cost pressure remains embedded in the build environment[3]“Construction Cost Index Rises 1.1% in December 2025,” General Authority for Statistics, stats.gov.sa. Industrial and logistics rents also rose in Riyadh, Jeddah, and parts of Dammam, which narrows development returns for operators that cannot fully pass higher occupancy costs to customers. With a limited Grade A supply under construction, vacancy tightening is likely to remain a stronger pricing force than new supply delivery in the early years of the Saudi Arabia 3PL warehousing market forecast.

Skilled Labor Shortages in Advanced Warehousing

Talent shortages are slowing the transition to higher-spec operations in the Saudi Arabia 3PL warehousing market. The Transport General Authority projected a national shortfall of 15,000 skilled logistics professionals by 2026, and the Eastern Province alone required 25% of that intake. Demand for professionals with SAP EWM or Manhattan Associates implementation experience exceeded supply by a ratio of 4:1 in the Eastern Province, and open roles were taking 6 to 8 months to fill on average. A sector white paper also showed that 57% of respondents saw high workloads as the main barrier to internal training investment, which means capability building is not keeping pace with automation deployment. Automated shuttle systems, high-bay storage, and sortation equipment therefore risk running below design throughput during early operating periods, especially where Saudization targets require parallel spending on training and localization in the Saudi Arabia 3PL warehousing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Services Reshape the Revenue Mix

Storage held 60.21% of the Saudi Arabia 3PL warehousing market size in 2025, while value-added services is projected to expand at an 8.55% CAGR through 2031. Distribution and inventory management accounted for most of the remaining revenue base, providing operators with a recurring stream tied to replenishment-led customer contracts. In the Saudi Arabia 3PL warehousing market, this structure still reflects the central role of basic storage in manufacturing, FMCG, and retail flows, where pallet storage and dispatch remain the core service need. At the same time, the faster growth of kitting, labeling, co-packing, and returns handling shows that customer demand is moving beyond pure square-meter leasing.

That shift is tied to the way modern retail and e-commerce are changing warehouse work. BinDawood Holding added 9 new core retail locations in FY 2025, which supports a more consolidated replenishment model and increases the need for pre-store handling within shared logistics facilities. NielsenIQ’s full-year 2025 update showed e-commerce gaining 2 percentage points of FMCG share year over year to 5.6%, which shifts orders from full-pallet movements to each-pick, packing, and return-ready workflows. Swisslog’s 2025 AutoStore deployment for Chalhoub Group in Riyadh, with 67,000 bins and 42 robots, shows how operators are building the automation backbone needed to support service-led revenue in the Saudi Arabia 3PL warehousing market. This is why service breadth is becoming a stronger differentiator than storage alone, especially for clients that want warehousing, order preparation, and omnichannel support from the same site.

By Warehouse Type: Bonded and Contract Models Drive Differentiation

General shared or multi-client warehousing accounted for 53.09% of the Saudi Arabia 3PL warehousing market share in 2025, while bonded warehousing is forecast to grow at a 7.72% CAGR through 2031. Dedicated contract warehousing remained the second-largest format, as large retailers and FMCG groups still value controlled environments, dedicated equipment, and customer-specific service settings. The Saudi Arabia 3PL warehousing industry still depends heavily on shared space because many users want flexibility without the capital commitment of a dedicated footprint. Even so, growth is clearly shifting toward formats that offer advantages in customs, compliance, or service specialization.

Bonded warehousing is benefiting the most from that change. The new SEZ frameworks that took effect in April 2026 improved the economics of duty suspension, VAT relief, and customs-sensitive cargo handling, which makes bonded facilities more attractive for regional trade flows. Prime Grade A multi-client warehouse space in Riyadh had already been operating under tight supply conditions, which pushed some occupiers toward build-to-suit and contract formats to lock in long-term capacity. Saudi Global Ports is developing the 1 million-square-meter Dammam Integrated Logistics Zone with bonded, unbonded, and cold-chain facilities, demonstrating how port-linked campuses are being designed to accommodate multiple warehouse formats in one location. As this buildout continues, the Saudi Arabia 3PL warehousing market is likely to allocate a rising share of new investment to bonded facilities rather than conventional shared sheds[4]“Dammam Integrated Logistics Zone,” Saudi Global Ports, saudiglobalports.com.sa.

By Temperature Control: Cold-Chain Expansion Outpaces Ambient Growth

Non-temperature controlled warehousing accounted for 69.4% of the Saudi Arabia 3PL warehousing market share in 2025, while temperature-controlled warehousing is set to grow at a 9.43% CAGR through 2031. Ambient storage remains dominant because manufacturing, consumer goods, and general retail still account for the broadest volume base in the Saudi Arabia 3PL warehousing market. Temperature-controlled space, however, is being lifted by demand from pharmaceuticals, vaccine distribution, fresh food retail, and imported perishables. The segment’s growth rate shows that specialized handling needs are rising faster than the base demand for standard storage.

Healthcare is a major part of that story. NUPCO secured SAR 2.5 billion (USD 666.15 million) in February 2025 to strengthen healthcare logistics infrastructure, including advanced storage and transport systems for temperature-sensitive medicines and vaccines. Saudi Food and Drug Authority distribution standards continue to raise the entry threshold for pharmaceutical storage, positioning certified cold-store operators to capture a larger share of specialized contracts in the Saudi Arabia 3PL warehousing market. Food retail growth is reinforcing the same trend because Saudi Arabia’s food retail market remained above USD 50 billion and leading supermarket groups continue to expand store networks that need chilled and frozen replenishment support. Capacity remains concentrated in Riyadh, Jeddah, and Dammam because weaker grid reliability and thinner freight density reduce the viability of advanced cold stores in secondary regions, which gives incumbents in the main cities firmer pricing and utilization conditions.

By Technology Adoption: Automation Investment Accelerates

Manual warehousing retained 63.83% of the 2025 Saudi Arabia 3PL warehousing market share, while fully automated warehousing is projected to grow at an 11.39% CAGR through 2031. This means the installed base in the Saudi Arabia 3PL warehousing market is still dominated by paper-based, labor-intensive, or lightly digitized operating models, especially in ambient and general trade facilities. Semi-automated warehouses sit between these two poles and are becoming the most practical upgrade path for operators that want better throughput without a full robotics commitment. Fully automated systems are growing from a smaller base, but their growth rate shows how quickly performance benchmarks are rising.

The leading examples already in operation are raising customer expectations. Aramex launched a robotic sorting facility at Jeddah Islamic Port in January 2025, featuring 120 automated guided vehicles and a capacity of 4,000 shipments per hour, setting a visible local benchmark for automated parcel and fulfillment handling. CJ Logistics opened a cross-border e-commerce Global Distribution Center at SILZ in February 2026, using multi-shuttle systems and goods-to-person conveyors, demonstrating how advanced warehouse designs are entering Saudi operations. The Saudi Arabia 3PL warehousing industry still faces a talent gap because WMS-skilled engineers remain scarce, and that can leave newly automated sites running below design capacity during early ramp-up periods. For this reason, many operators are pairing equipment spending with retrofit programs, RF scanning, conveyor systems, and training partnerships rather than moving directly from manual to full automation in one step.

By End User Industry: Pharma Challenges Retail’s Dominant Position

Retail and e-commerce accounted for 32.67% of the Saudi Arabia 3PL warehousing market size in 2025, while healthcare and pharma are forecast to expand at an 8.85% CAGR through 2031. Retail demand remains the largest anchor in the Saudi Arabia 3PL warehousing market because domestic delivery volumes, omnichannel formats, and store replenishment all require a broad distribution footprint. Consumer Goods and Food and Beverage added another major share of demand, which keeps ambient capacity central to the current revenue mix. Manufacturing and other end-user industries also remain relevant, as industrial zones in Jubail, Yanbu, and SPARK continue to drive warehouse demand for production support and inventory staging.

Healthcare is still smaller in absolute terms, but its growth pace is changing facility design and customer mix. Domestic pharmaceutical output, GDP-compliant storage requirements, and NUPCO-backed logistics spending are raising the need for certified multi-temperature space rather than simple pallet storage. SAL’s Riyadh distribution center serves pharmaceutical, FMCG, and e-commerce customers within a single footprint, which shows how mixed-vertical occupancy is emerging as a practical model in the Saudi Arabia 3PL warehousing industry. As a result, contract value is moving toward operators that can combine compliance, chain-of-custody visibility, and flexible service execution for different end-user groups under one roof. This change is gradually narrowing the gap between the Saudi Arabia 3PL warehousing market’s largest tenant base and its fastest-growing one.

Geography Analysis

Central Saudi Arabia held 42.5% of the Saudi Arabia 3PL warehousing market share in 2025, while Western Saudi Arabia is projected to grow at a 7.09% CAGR through 2031. Riyadh remains the core of Central demand because it concentrates national distribution activity, administrative functions, and multimodal links across road, rail, and air cargo networks. The city accounted for 44% of domestic delivery orders in Q1 2026, reinforcing its role as the Kingdom’s main fulfillment center. DHL Supply Chain announced a EUR 130 million (USD 143 million) investment to build a 53,000-square-meter multi-user warehouse at Riyadh’s SILZ under a 26-year lease, which shows how global operators are positioning capacity in the Central corridor. SAL also signed an agreement to establish a SAR 4 billion (USD 1.06 billion) logistics zone in Falcon City, north of Riyadh, across 1.56 million square meters, which points to the largest absolute share of future capacity landing in Central Saudi Arabia.

Eastern Saudi Arabia remains the second-largest geography because it combines petrochemical output, energy-sector logistics, SPARK, and direct seaport access through Dammam. ASMO, the Saudi Aramco and DHL Supply Chain joint venture, broke ground in February 2026 on a 1.4 million-square-meter logistics hub at SPARK that includes a 43,000-square-meter temperature-controlled warehouse, supporting the province’s role in industrial and specialist logistics. The Western region is the fastest-growing geography in the Saudi Arabia 3PL warehousing market because Jeddah Islamic Port is the Kingdom’s main maritime gateway and Makkah accounted for 22.2% of domestic delivery orders in Q1 2026. Bahri is developing a 95,436 square meter logistics center at Jeddah Islamic Port, and Mawani signed a SAR 250 million (USD 66.61 million) lease in March 2026 with Sultan Logistics for a 200,000-square-meters zone at the same port, which confirms the pace of investment in Western Saudi Arabia.

Northern and Southern Saudi Arabia currently hold smaller shares in the Saudi Arabia 3PL warehousing market because logistics infrastructure is thinner and consumption density is lower. Jazan could become the most important change point in the South because the SEZ framework took effect on April 16, 2026 and supports food-processing and metals-conversion activity that will need warehousing, distribution, and bonded handling capacity. Port-linked investment is also spreading beyond the top 2 corridors, as Mawani signed a SAR 200 million (USD 53.29 million) agreement in December 2025 with ARASCO for a 40,000-square-meters food-grade storage and distribution center at King Abdulaziz Port in Dammam. Even so, grid reliability limits and weak cold-store economics still constrain pharmaceutical-grade and temperature-controlled expansion in the North and South, which means the Saudi Arabia 3PL warehousing market remains geographically concentrated around Riyadh, Jeddah, and Dammam.

Competitive Landscape

The Saudi Arabia 3PL warehousing market is moderately concentrated, with global logistics groups, national champions, port-linked operators, and niche domestic providers all competing across overlapping service layers. DSV’s February 2026 go-live integration of Schenker’s Saudi Arabia operations created a unified network spanning 29 facilities and more than 1,150 specialists, which clearly strengthened scale and coverage in contract logistics, air and sea, and road transport. SAL reported a 16% revenue increase to SAR 445.8 million (USD 118.78 million) in Q1 2026, while Bahri reported SAR 285 million (USD 75.94 million) in integrated logistics revenue in the same period, which shows that national operators are building broader warehouse and logistics propositions rather than staying in narrow service lanes. Tamer Logistics also remains relevant with more than 300,000 square meters of premium multi-temperature warehousing across 7 cities, and its Kuehne+Nagel partnership adds international contract logistics depth.

Competition is becoming less about raw floor space and more about certification, automation, and service integration. White-space opportunities remain strongest in fully automated multi-temperature facilities, bonded warehousing in newly activated SEZ sites, and healthcare cold-chain storage that meets SFDA GDP standards. Aramex’s February 2026 launch of a unified AI data platform on Google Cloud across more than 600 cities shows that data visibility is now part of the competitive offer for customers that want real-time inventory and network transparency. Kuehne+Nagel became the first logistics company to secure Authorized Economic Operator certification for customs brokerage in Saudi Arabia, which gives it a compliance edge in both inland and port-linked operations. This is creating a clear split inside the Saudi Arabia 3PL warehousing market between certified operators that can serve pharmaceutical, food-grade, and bonded cargo at premium yields and non-certified operators that compete mainly on basic storage pricing.

Strategic moves in 2025 and 2026 show how operators are responding to that pressure. DHL chose SILZ for a new multi-user warehouse, which links warehousing, bonded handling, and airport-adjacent trade flows in a single location and strengthens its position in the Saudi Arabia 3PL warehousing market. Agility Logistics Parks and ROSHN finalized a SAR 2.5 billion (USD 666.15 million) joint venture in February 2026 to develop a 650,000-square-meter logistics park in Jeddah, which increases modern Grade A and multi-client capacity in the Western corridor. Swisslog’s automation project in Riyadh shows that warehouse technology suppliers are also shaping competitive standards by enabling faster order handling and denser storage. Together, these moves suggest that the Saudi Arabia 3PL warehousing market will continue to reward operators that combine geographic reach with bonded access, automation capability, and compliance-ready service design.

Saudi Arabia 3PL Warehousing Industry Leaders

DHL Group

Almajdouie Logistics

Aramex

Bahri

DSV A/S (Including DB Schenker)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mawani signed a SAR 250 million (USD 66.61 million) lease agreement with Sultan Logistics for a new 200,000-square-meter logistics zone at Jeddah Islamic Port (Al-Khomra area), including modern warehouses and refrigerated container facilities, advancing Jeddah's role as a bonded logistics hub.

- February 2026: ROSHN Group and Agility Logistics Parks finalized a SAR 2.5 billion (USD 666.15 million) joint venture agreement to develop a 650,000-square-meter, three-phase logistics park in Jeddah, with construction commencing in Q4 2026, adding significant Grade A multi-client and bonded capacity to the Western region.

- November 2025: DHL Supply Chain announced an EUR 130 million (USD 143 million) investment to build a 53,000-square-meter multi-user warehouse at Riyadh's SILZ under a 26-year lease, with construction commencing in Q1 2026 and completion expected in Q2 2027. The hub will serve technology, retail, automotive, energy, and e-commerce tenants.

- October 2025: SAL Logistics Services launched a new 45,000 sqm warehouse and distribution center at The Logistics Park in southern Riyadh, adding integrated office space and a Transport Control Tower Hub to digitally monitor trucking operations and connect warehousing, distribution, and logistics services.

Saudi Arabia 3PL Warehousing Market Report Scope

| Storage |

| Distribution and Inventory Management |

| Value-Added Services and Others (kitting, labelling) |

| General Shared / Multi-client Warehousing |

| Dedicated Contract Warehousing |

| Bonded Warehousing |

| Non-Temperature Controlled |

| Temperature Controlled |

| Manual |

| Semi-automated |

| Fully Automated |

| Manufacturing |

| Consumer Goods |

| Food and Beverage |

| Retail and E-commerce |

| Healthcare and Pharma |

| Other End-user Industries |

| Central (Riyadh, Al-Qassim, and Hail) |

| Eastern (Ash-Sharqiyah) |

| Western (Al-Bahah, Makkah, Medina, and Tabuk) |

| Northern (Al-Jouf and Arar) |

| Southern (Asir, Jazan, and Najran) |

| By Service Type | Storage |

| Distribution and Inventory Management | |

| Value-Added Services and Others (kitting, labelling) | |

| By Warehouse Type | General Shared / Multi-client Warehousing |

| Dedicated Contract Warehousing | |

| Bonded Warehousing | |

| By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | |

| By Technology Adoption | Manual |

| Semi-automated | |

| Fully Automated | |

| By End User Industry | Manufacturing |

| Consumer Goods | |

| Food and Beverage | |

| Retail and E-commerce | |

| Healthcare and Pharma | |

| Other End-user Industries | |

| By Region | Central (Riyadh, Al-Qassim, and Hail) |

| Eastern (Ash-Sharqiyah) | |

| Western (Al-Bahah, Makkah, Medina, and Tabuk) | |

| Northern (Al-Jouf and Arar) | |

| Southern (Asir, Jazan, and Najran) |

Key Questions Answered in the Report

What is the current and forecast value of Saudi Arabia 3PL warehousing?

The Saudi Arabia 3PL warehousing market was valued at USD 3.53 billion in 2025, is estimated at USD 3.74 billion in 2026, and is forecast to reach USD 4.94 billion by 2031 at a 5.71% CAGR.

Which service category leads revenue and which one is growing the fastest?

Storage led with 60.21% of revenue in 2025, while Value-Added Services is the fastest-growing service category with an 8.55% CAGR through 2031.

Why is bonded warehousing becoming more important in Saudi Arabia?

Bonded Warehousing is projected to grow at 7.72% CAGR because SEZ incentives, customs-duty suspension, and re-export activity are making bonded sites more efficient for regional trade flows.

What is driving growth in temperature-controlled facilities?

Temperature Controlled warehousing is growing at 9.43% CAGR due to healthcare logistics upgrades, stricter pharmaceutical handling requirements, and continued expansion in chilled and frozen food retail.

Which part of Saudi Arabia leads warehousing demand?

Central Saudi Arabia led with 42.5% of revenue in 2025, supported by Riyadh’s role in domestic distribution, air cargo, dry port connectivity, and large-scale new logistics investments.

How are leading operators differentiating themselves in Saudi Arabia 3PL warehousing?

Leading operators are investing in bonded capacity, warehouse automation, AEO and GDP-linked compliance, and large multi-user sites, with examples including DHL at SILZ, DSV’s Schenker integration, and Agility’s Jeddah logistics park JV.

Page last updated on: