Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

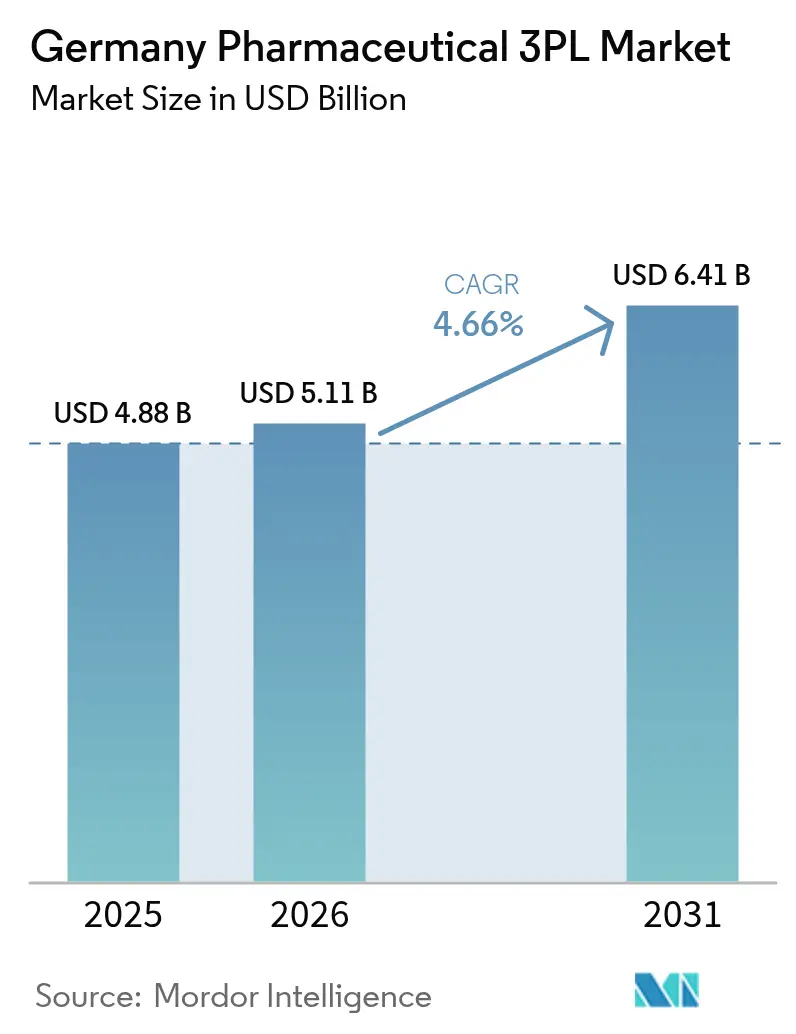

| Base Year Market Size (2025) | USD 4.88 Billion |

| Market Size (2026) | USD 5.11 Billion |

| Market Size (2031) | USD 6.41 Billion |

| Growth Rate (2026 - 2031) | 4.66% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Pharmaceutical 3PL Market Analysis by Mordor Intelligence

The Germany Pharmaceutical 3PL Market size was valued at USD 4.88 billion in 2025 and estimated to grow from USD 5.11 billion in 2026 to reach USD 6.41 billion by 2031, at a CAGR of 4.66% during the forecast period (2026-2031).

The measured expansion signals a maturing logistics landscape shaped by stringent Good Distribution Practice (GDP) mandates, rising biologics volumes, and sustained domestic drug demand. Temperature-controlled services already represent 58% of all third-party pharmaceutical logistics activities, and providers that demonstrate best-in-class compliance command premium pricing. Strategic consolidation is accelerating as large integrators acquire cold-chain specialists to secure scale and end-to-end control, while automation and digital traceability tools are gaining traction as defenses against excursion risk and labor shortages. The German pharmaceutical 3PL market is also benefiting from government incentives to reshore manufacturing capacity, which are lengthening domestic supply chains and increasing inventory holding requirements.

Key Report Takeaways

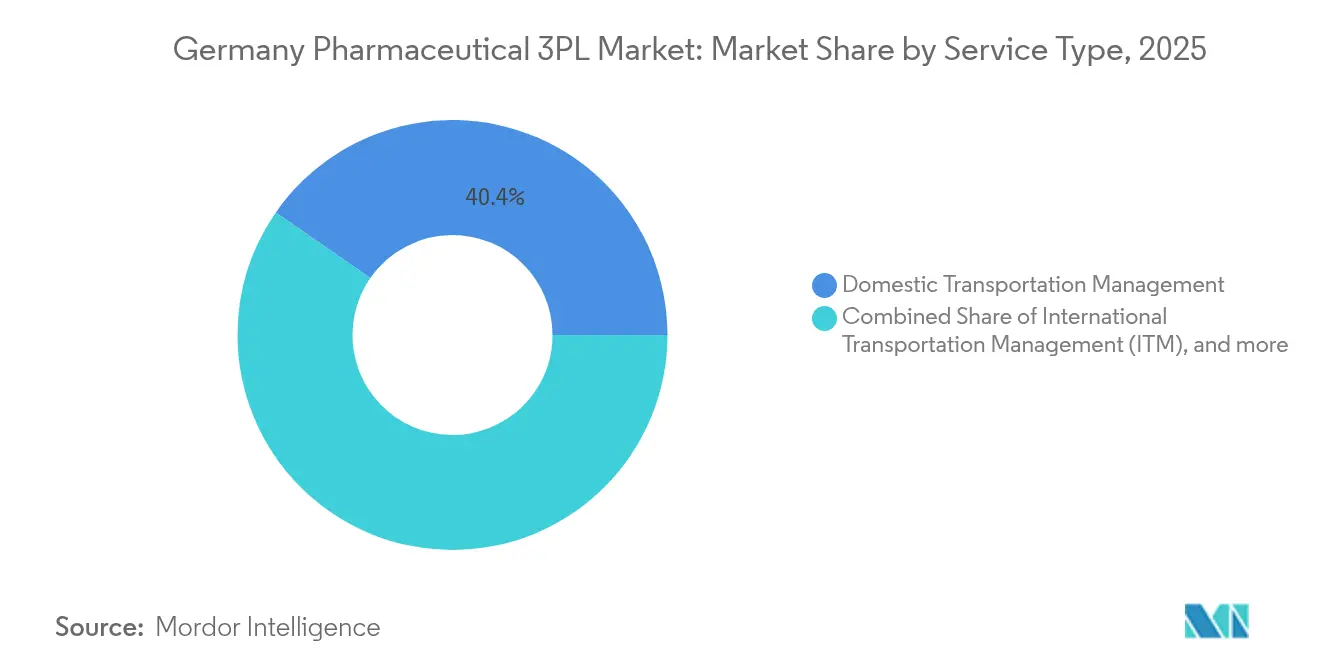

- By service type, Domestic Transportation Management held 40.35% of the German pharmaceutical 3PL market share in 2025, while Value-Added Warehousing & Distribution is advancing at a 5.72% CAGR between 2026-2031.

- By temperature type, cold-chain services commanded 57.75% of the German pharmaceutical 3PL market size in 2025 and are expanding at a 5.76% CAGR between 2026-2031.

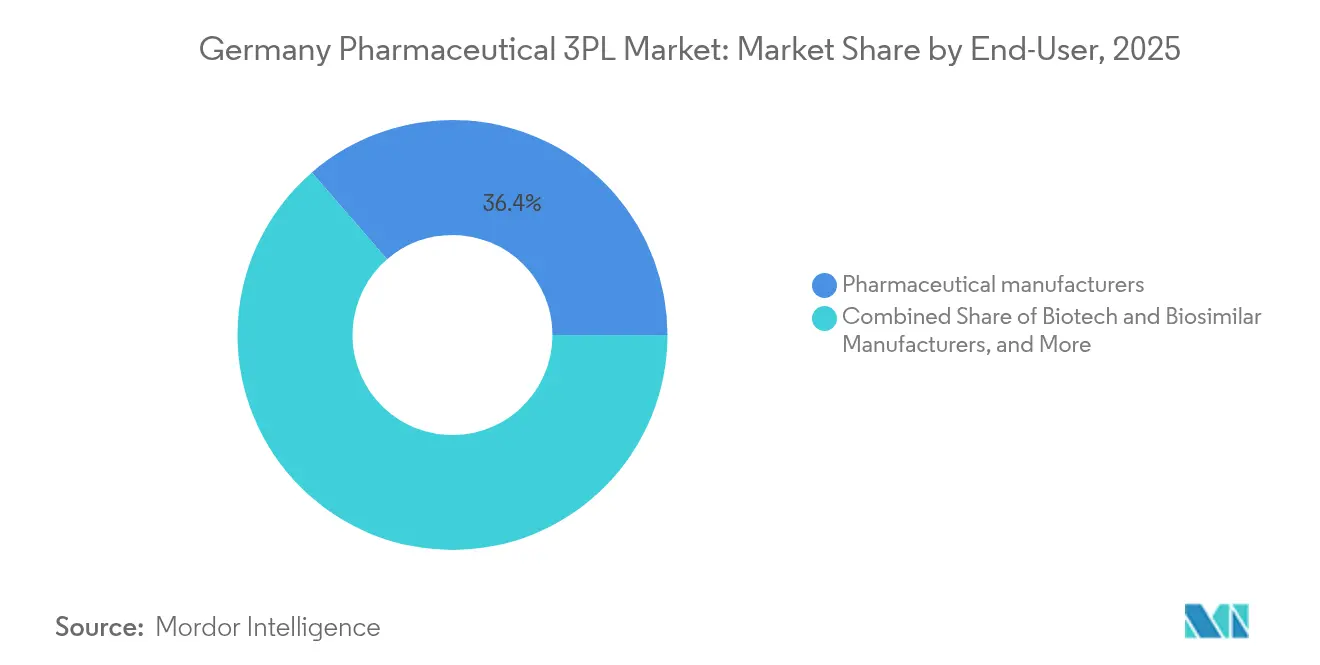

- By end user, pharmaceutical manufacturers led with 36.35% revenue share in 2025; e-pharmacies & direct-patient services record the highest projected CAGR at 5.92% between 2026-2031.

- By product type, prescription drugs accounted for 35.40% of the German pharmaceutical 3PL market size in 2025, whereas cell & gene therapies are forecast to grow at a 6.25% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Pharmaceutical 3PL Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong domestic pharmaceutical demand | +1.2% | Germany and wider EU | Medium term (2–4 years) |

| E-commerce channel acceleration for Rx & OTC drugs | +0.9% | Urban Germany | Short term (≤ 2 years) |

| Rising biologics & advanced-therapy volumes requiring GDP-compliant cold chain | +1.4% | Germany and Europe | Long term (≥ 4 years) |

| End-to-end digital visibility solutions lowering excursion risk | +0.7% | Germany and DACH | Medium term (2–4 years) |

| Sustainability-driven modal shift reducing carbon footprint | +0.6% | Germany within EU Green Deal | Long term (≥ 4 years) |

| Surge in decentralized/virtual clinical trials driving direct-to-patient logistics needs | +0.6% | Germany, with global clinical trial networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Domestic Pharmaceutical Demand

Prescription volumes are growing in line with an aging population, and Germany’s pharmaceutical industry generated more than EUR 200 billion in revenue in 2024, supporting 350,000 jobs. Capacity constraints inside manufacturers have triggered greater outsourcing of inventory management and distribution to compliant 3PL partners. Berlin’s 2023 Pharmaceutical Strategy introduced manufacturing incentives and faster clinical-trial approvals, further increasing logistics complexity that favors specialized providers.

E-commerce Channel Acceleration for Rx & OTC Drugs

Mail-order leaders such as DocMorris scaled aggressively after regulators cleared the apo-rot acquisition, underpinning a last-mile model that demands ambient and cooled fulfillment lines inside GDP-certified facilities. Four-month ERP integrations highlight the IT intensity of this segment, prompting 3PLs to invest in automated picking and serialized, item-level tracking. As consumers embrace home delivery, e-pharmacies need partners that combine wholesale shipping with direct-to-patient drop-offs.

Rising Biologics & Advanced-Therapy Volumes Requiring GDP-Compliant Cold Chain

Thermo Fisher Scientific opened Germany’s first dedicated cryocenter for cell & gene therapies, providing storage down to –196 °C and establishing new performance benchmarks. Marken expanded its Frankfurt site to add cryogenic capacity, while Panasonic’s vacuum-insulated boxes now hold –75 °C for 18 days without dry ice. These investments cement Germany as a European hub for ultra-low-temperature logistics, lifting demand for 3PLs that can guarantee an end-to-end chain of custody.

End-to-End Digital Visibility Solutions Lowering Excursion Risk

Pharma shippers spend roughly USD 14 billion a year worldwide on cold transport and storage, driving adoption of IoT sensors and blockchain authentication that cut annual product-loss costs of up to USD 35 billion. German providers use Testo’s real-time monitoring and automated deviation alerts to meet IATA CEIV Pharma certification standards, thereby lowering liability and audit costs.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High operating costs for GDP/GMP-compliant facilities | –0.8% | Germany & EU | Medium term (2–4 years) |

| Skilled labor shortages in temperature-controlled logistics | –1.1% | German pharma clusters | Short term (≤ 2 years) |

| Energy-price volatility inflating warehouse OPEX | –0.6% | Germany & Europe | Short term (≤ 2 years) |

| Scarcity of GDP-approved urban micro-fulfilment space limiting last-mile service expansion | -0.5% | Germany, concentrated in major urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Operating Costs for GDP/GMP-Compliant Facilities

Annual audit and documentation expenses can top EUR 1 million for large warehouses, and new in-transit verification rules require continuous monitoring in road freight as well. A Cologne distributor lost its license in July 2024 after repeated GDP breaches, underscoring the financial stakes of non-compliance.

Skilled Labor Shortages in Temperature-Controlled Logistics

Germany’s pharma supply chain lacks 176,000 qualified workers, with 70,000 unfilled truck-driver posts worsening last-mile bottlenecks. DACHSER responds by training 100 drivers a year, yet retirements mean the gap will persist. Expertise in cold-chain handling and sensor technology is especially scarce[1]European Compliance Academy, “GDP Guideline Update 2024,” ECA, eca.de.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Warehousing Gains Momentum

Domestic Transportation Management retained 40.35% of the German pharmaceutical 3PL market share in 2025, confirming the country’s status as a distribution bridge into Europe. Value-Added Warehousing & Distribution, the fastest-rising service, is growing at 5.72% CAGR as manufacturers outsource GDP-compliant storage, labeling, and serialization. The German pharmaceutical 3PL market size for warehousing is set to expand further as fully automated silos such as SSI SCHAEFER’s build for Losan Pharma go live in 2025. International air corridors stay vital for emergency biologics; Lufthansa Cargo’s Cool/td-Active network secures -20 °C to +30 °C moves across 89 stations.

The traditional divide between trucking and storage blurs as 3PLs package transport, inventory visibility, and regulatory filing into single contracts. DHL’s planned EUR 2 billion healthcare network and DSV’s acquisition of DB Schenker exemplify scale-seeking strategies that lock in captive volumes and higher asset utilization.

By Temperature Type: Cold Chain Dominance

Cold-chain operations cover 57.75% of 2025 revenue and expand at a 5.76% CAGR. Growth is fueled by vaccines, biologics, and cell therapies that lose efficacy once temperatures stray beyond narrow windows. The German pharmaceutical 3PL market share for ultra-low-temperature services keeps rising as Secop’s next-gen compressors cut energy draw inside -80 °C freezers by double-digit percentages. Ambient logistics face fee pressure because digital direct shipping reduces warehouse dwell time for OTC lines.

Regulatory scrutiny elevates barriers to entry; EU GDP demands validation of every transport lane, forcing smaller providers either to invest or exit. Automation offsets some operating costs: new warehouse management systems linked to predictive HVAC algorithms achieve 30% energy savings, a margin buffer amid volatile power prices.

By End User: E-Pharmacies Drive Growth

Pharmaceutical manufacturers generated the largest share at 36.35% in 2025, yet e-pharmacies & direct-to-patient services record the swiftest 5.92% CAGR. The German pharmaceutical 3PL market size for e-pharmacy fulfillment gains from higher prescription reimbursements and consumer preference for home delivery. Providers must integrate pick-by-light stations, tamper-evident packaging, and secure driver authentication to satisfy data-protection rules.

Biotech firms and clinical-trial sponsors require white-glove, validated lanes with a chain-of-identity, sustaining demand for higher-margin premium services. Hospitals and retail pharmacies still command large volumes, but consolidation keeps their growth moderate. WHO guidance on emergency stockpiling continues to anchor wholesaler relevance for pandemic-readiness.

By Product Type: Cell Therapies Lead Innovation

Prescription drugs ranked first with 35.40% revenue, yet cell & gene therapies accelerate fastest at 6.25% CAGR, lifting cold-chain revenue. The German pharmaceutical 3PL market size for cell therapy logistics is small but lucrative because each patient-specific lot can exceed USD 250,000 in value at release. Fraunhofer’s RNAuto project, aiming to automate mRNA manufacturing, underscores the technical hurdles that deepen reliance on specialist carriers.

Biopharmaceuticals and biosimilars retain steady expansion as European patent cliffs unlock competition, while vaccine volumes remain resilient following updated COVID-19 and RSV immunization campaigns. OTC products migrate toward parcel carriers and automated lockers, curbing traditional 3PL margins for this category.

Geography Analysis

Germany’s central location, dense highway network, and cargo-friendly airports give the German pharmaceutical 3PL market an unrivaled reach across continental Europe. Clusters in Rhein-Main, North Rhine-Westphalia, and Bavaria generate the bulk of cold-chain demand, prompting UPS Healthcare to commission a 27,200 m² Giessen hub that can reach 80% of Europe within 24 hours. Eastern states attract greenfield investments due to lower energy tariffs and abundant renewables, a hedge against power-cost volatility.

The ALBVVG act requires six-month inventory buffers for rebate drugs, spurring additional warehouse leasing across federal states. Pending EU regulation on critical medicines will assign shared-stock obligations across members, favoring 3PLs with pan-European facilities and standardized SOPs. Germany’s rail corridors into the Czech Republic and Poland offer cost-effective, low-carbon access to growth markets, while Rhine river congestion keeps waterway use limited to bulk APIs.

Energy prices diverge regionally, pushing network redesigns that blend renewable-powered campuses in the north with existing Frankfurt-based air gateways. Automation offsets higher labor costs in southern warehouses, ensuring service levels demanded by advanced therapies.

Competitive Landscape

The German pharmaceutical 3PL market balances global integrators with expert mid-caps. DHL, DSV, and Kuehne Nagel use global scale, multi-temperature fleets, and IT suites to win multi-year, multimillion-euro contracts. Niche players penetrate high-complexity niches—cell therapy transport, clinical trial returns, and hazardous substance handling—where expertise outweighs volume. Technology now separates leaders from laggards: 3PLs deploying blockchain traceability, AI excursion prediction, and autonomous mobile robots reduce spoilage, enhance audit readiness, and increase picking productivity.

M&A remains brisk. DSV’s EUR 14.3 billion purchases of DB Schenker vault it into the top tier, while Nippon Express’ full takeover of Simon Hegele expands Asian-European clinical logistics lanes[3]Simon Hegele Healthcare Solutions, “Integration into Nippon Express Group Completed,” Simon Hegele, simon-hegele.com. Capital-intensive cold-chain buildouts discourage new entrants, especially under Germany’s rigorous licensing regime. Yet white-space persists in direct-to-patient biologics, where only a few carriers combine GDP vans, trained nurses, and real-time, patient-level tracking.

Germany Pharmaceutical 3PL Industry Leaders

DHL Logistics

Rhenus Logistics

Ceva Logistics

MSK Pharma Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: CEVA Logistics started a 17,000 m² three-zone pharma hub in Strasbourg to bolster regional cold-chain capacity.

- July 2025: Logwin AG bought Hanse Service and Pharma logistics partner, adding 7,600 m² GDP storage in Hamburg.

- April 2025: DHL Group earmarked EUR 2 billion for DHL Health Logistics to double healthcare revenue and expand Pharma Hubs by 2030.

- April 2025: UPS Healthcare opened its first German site, a 27,200 m² GDP facility in Giessen, powered by solar panels generating 850,000 kWh annually.

Germany Pharmaceutical 3PL Market Report Scope

The study captures the market value of the German pharmaceutical 3PL market. The report provides a comprehensive background analysis of the German pharmaceutical 3PL market, covering the current market trends, restraints, technological updates, and detailed information on various segments and the competitive landscape of the industry.

The German Pharmaceutical 3PL Market is segmented by service (domestic transportation management, international transportation management, and value-added warehousing and distribution), and by temperature control (controlled/cold chain logistics, and non-controlled/non-cold chain logistics). The report offers market sizes and forecast in value (USD) for all the above segments.

By Service Type

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing & Distribution (VAWD) |

By Temperature Type

| Cold Chain |

| Non-cold Chain |

By End User

| Pharmaceutical Manufacturers |

| Biotech & Biosimilar Manufacturers |

| Clinical Research & Trial Sponsors |

| Hospitals & Retail Pharmacies |

| Healthcare Distributors & Wholesalers |

| E-pharmacies & Direct-to-Patient Services |

| Others |

By Product Type

| Prescription Drugs |

| OTC & Consumer Health Products |

| Biopharmaceuticals & Biosimilars (ex-CGT) |

| Cell & Gene Therapies |

| Vaccines & Blood-derived Products |

| Veterinary Pharmaceuticals & Animal Health Products |

| Medical Devices, Diagnostics & Combination Products |

| Clinical-trial Materials (Investigational Medicinal Products) |

| Others |

| By Service Type | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing & Distribution (VAWD) | ||

| By Temperature Type | Cold Chain | |

| Non-cold Chain | ||

| By End User | Pharmaceutical Manufacturers | |

| Biotech & Biosimilar Manufacturers | ||

| Clinical Research & Trial Sponsors | ||

| Hospitals & Retail Pharmacies | ||

| Healthcare Distributors & Wholesalers | ||

| E-pharmacies & Direct-to-Patient Services | ||

| Others | ||

| By Product Type | Prescription Drugs | |

| OTC & Consumer Health Products | ||

| Biopharmaceuticals & Biosimilars (ex-CGT) | ||

| Cell & Gene Therapies | ||

| Vaccines & Blood-derived Products | ||

| Veterinary Pharmaceuticals & Animal Health Products | ||

| Medical Devices, Diagnostics & Combination Products | ||

| Clinical-trial Materials (Investigational Medicinal Products) | ||

| Others | ||

Key Questions Answered in the Report

How large is the German pharmaceutical 3PL market in 2026?

The market is valued at USD 5.11 billion in 2026 and is forecast to reach USD 6.41 billion by 2031 at a 4.66% CAGR.

Which service type is growing fastest within Germany’s pharma logistics?

Value-Added Warehousing & Distribution is expanding at a 5.72% CAGR, reflecting demand for GDP-compliant inventory and packaging solutions.

Why is cold-chain logistics so dominant in Germany?

Cold-chain services hold 57.75% share because biologics, vaccines, and cell & gene therapies require strict temperature control, driving premium outsourced demand.

What is the biggest restraint facing Germany’s pharmaceutical logistics providers?

Acute labor shortages-176,000 open positions, including 70,000 truck drivers-are the largest drag, subtracting an estimated 1.1 percentage points from forecast CAGR.

How are sustainability goals influencing German pharma transport?

Shippers shift freight from air to sea and adopt alternative fuels, enabling CO₂ reductions such as Merck Healthcare’s 10,000-ton annual saving from modal shifts.

Which end-user segment will grow quickest to 2031?

E-pharmacies and direct-to-patient channels lead with a 5.92% CAGR as consumers increasingly order prescription and OTC drugs online.

Page last updated on: