Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

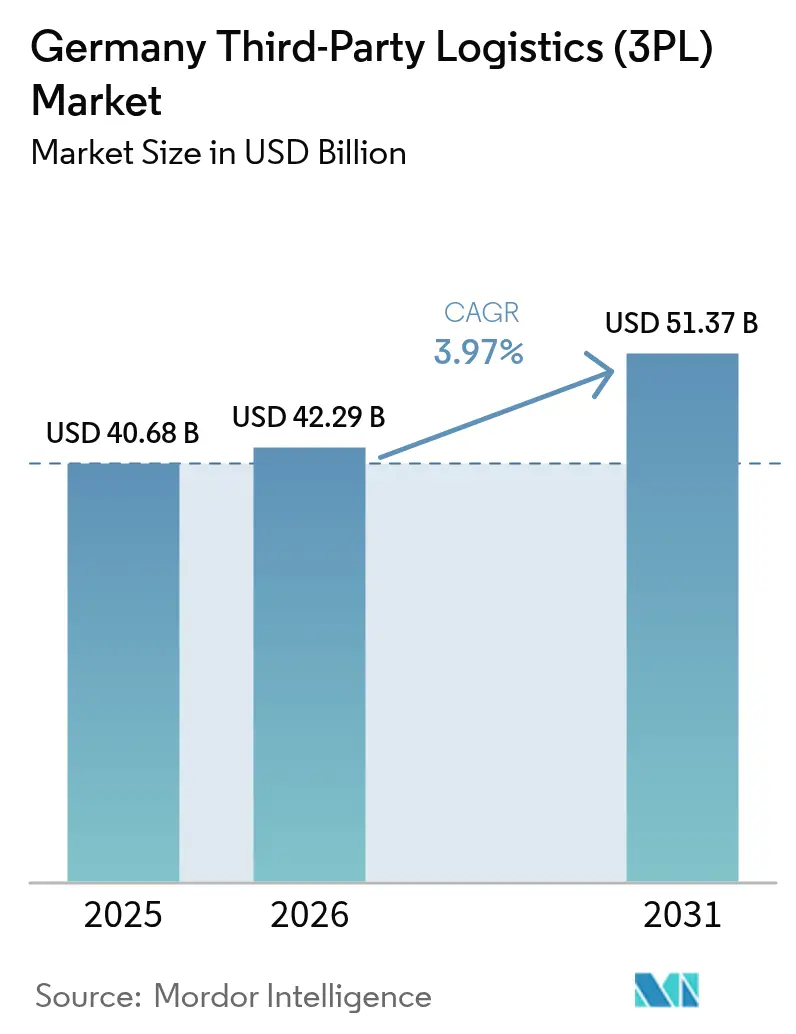

| Base Year Market Size (2025) | USD 40.68 Billion |

| Market Size (2026) | USD 42.29 Billion |

| Market Size (2031) | USD 51.37 Billion |

| Growth Rate (2026 - 2031) | 3.97% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Third-Party Logistics (3PL) Market Analysis by Mordor Intelligence

The Germany Third-Party Logistics Market size was valued at USD 40.68 billion in 2025 and estimated to grow from USD 42.29 billion in 2026 to reach USD 51.37 billion by 2031, at a CAGR of 3.97% during the forecast period (2026-2031).

Structural shifts favoring outsourced logistics, the nation’s central role in European trade, and rising defense spending combine with e-commerce momentum to sustain demand. Post-Brexit route realignments move cross-border volumes toward German hubs, while labor cost pressures accelerate warehouse automation. State support for green transport and ESG-linked financing further strengthens long-term opportunities for providers that can blend sustainability with technology leadership.

Key Report Takeaways

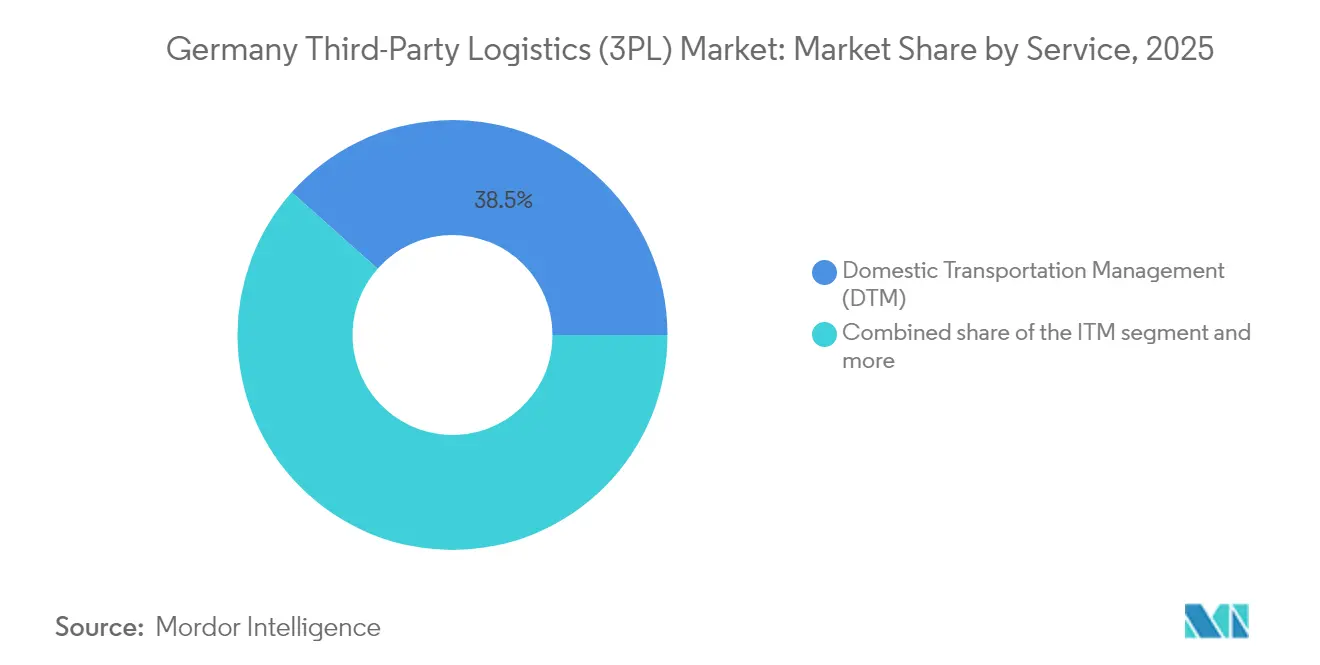

- By service, Domestic Transportation Management held 38.45% of the Germany third-party logistics market share in 2025; Value-Added Warehousing & Distribution is projected to post a 6.55% CAGR through 2031.

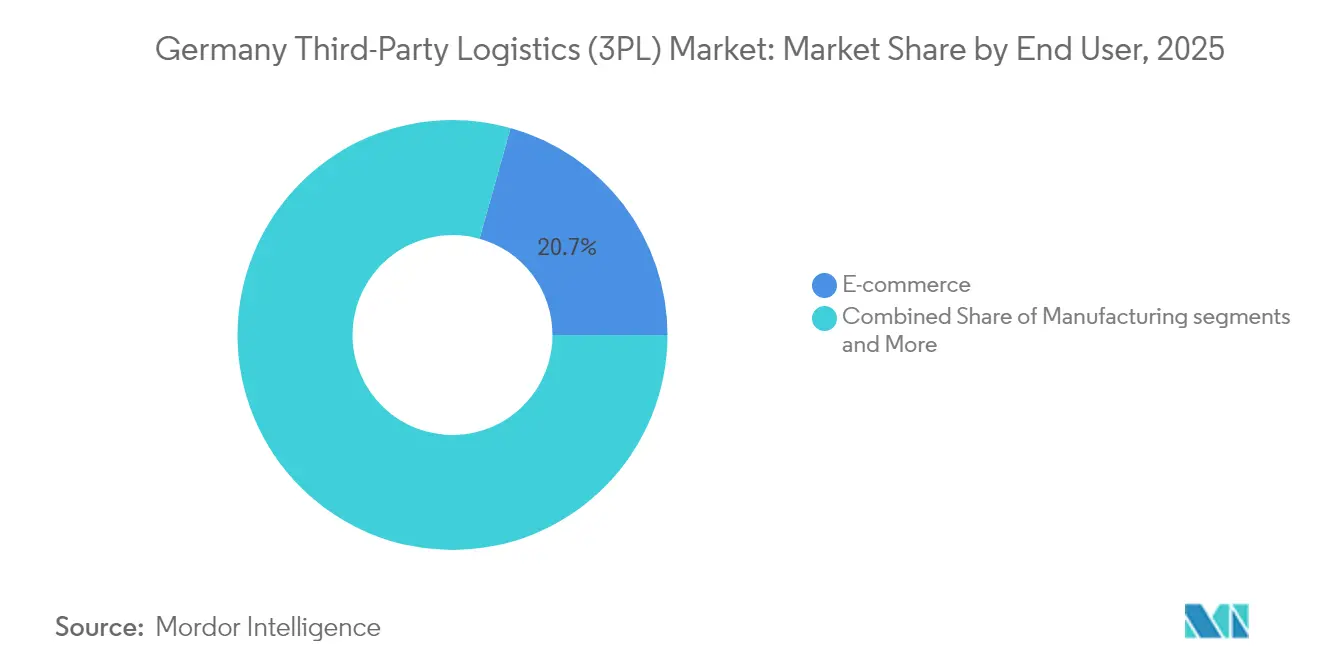

- By end user, E-commerce accounted for 20.65% of the Germany third-party logistics market size in 2025, whereas Automotive is on track for a 4.12% CAGR to 2031.

- By logistics model, Asset-Light solutions commanded 41.35% of 2025 revenue, while Hybrid models are set to rise at 4.96% CAGR.

- By region, North Rhine-Westphalia led with 22.60% revenue in 2025; Baden-Württemberg is the fastest-growing state at a 4.18% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Third-Party Logistics (3PL) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce parcel volumes surge beyond pre-pandemic baseline | +0.8% | Nationwide; peaks in NRW, Bavaria, Baden-Württemberg | Medium term (2-4 years) |

| Omnichannel retail drives inventory decentralization | +0.6% | Urban centers and major hubs | Medium term (2-4 years) |

| Rising cross-border B2C flows after Brexit rerouting | +0.4% | Western corridors, chiefly NRW & Hamburg | Short term (≤ 2 years) |

| Automation ROI improves with USD 13.2 minimum wage | +0.7% | Nationwide; strongest in high-wage regions | Long term (≥ 4 years) |

| ESG-linked loans spur green warehousing retrofits | +0.3% | Major industrial clusters | Long term (≥ 4 years) |

| Bundeswehr re-armament lifts defense-logistics spend | +0.5% | Defense-manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce Parcel Volumes Surge Beyond Pre-Pandemic Baseline

Parcel demand continues to outpace 2019 benchmarks as consumers shift more discretionary purchases online. Smartphones drive 57% of checkouts, forcing fulfillment networks to accommodate smaller, faster deliveries. Germany’s average 1.44-day transit time and 94.39% first-attempt delivery success entrench the country as a preferred distribution base. DHL processes 6.7 million domestic parcels daily and targets over 5% annual e-commerce revenue growth, illustrating how incumbent operators redirect resources from declining mail toward parcel logistics[1]Frank Appel, “Deutsche Post DHL Group FY 2024 Presentation,” DHL Group, dhl.com]. Scalability in last-mile capacity remains a decisive competitive lever as parcel density spreads across suburban and rural zones.

Omnichannel Retail Drives Inventory Decentralization

Retailers now split stock across multiple micro-fulfillment locations to meet next-day commitments. REWE’s USD 275 million Magdeburg center embodies this pivot, operating 49,500 m² with 50% automation and throughput of 286,000 daily packages. Distributed nodes shorten lead times but multiply planning complexity, pushing merchants to outsource visibility and allocation tasks. Asset-Light 3PLs gain traction by layering advanced WMS and analytics over shared facilities, enabling retailers to flex capacity without owning warehouses.

Rising Cross-Border B2C Flows Post-Brexit Rerouting

UK-EU barriers have rerouted many parcels through German consolidation points. Logistics costs along the German-British corridor climbed 13%, yet providers recoup volume by handling onward EU shipments that previously traveled direct. Custom brokerage, carbon border rules, and VAT administration add value-added revenue streams. German hubs thus serve as gateways for non-EU retailers seeking single-point access to the Schengen area, reinforcing the Germany third-party logistics market as Europe’s distribution backbone.

Automation ROI Improves with USD 13.2 Minimum Wage

The nationwide wage floor uplifts pay scales and narrows payback periods for robotics. DHL plans to add 1,000 Boston Dynamics units on top of 7,500 existing robots, achieving unloading speeds of 700 cases per hour. Tele-operated yard trucks from FERNRIDE, piloted with DB Schenker, let one operator manage several vehicles, alleviating labor shortages while enhancing safety. Over the long term, automation diffuses beyond flagship hubs into midsize facilities, altering workforce profiles toward maintenance, analytics, and remote operations[2]Silke Reinhardt, “German Minimum Wage Commission Report 2024,” Federal Ministry of Labor and Social Affairs, bmrs.bund.de.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural truck-driver shortage (>80,000 vacancies) | -0.9% | Nationwide; acute in eastern & rural areas | Short term (≤ 2 years) |

| High electricity tariffs limit cold-chain expansion | -0.4% | Nationwide; energy-intensive sites | Medium term (2-4 years) |

| Strict Sunday truck ban complicates planning | -0.2% | Nationwide | Long term (≥ 4 years) |

| Near-shoring to CEE shifts volume outward | -0.6% | Border regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Structural Truck-Driver Shortage (More than 80,000 Vacancies)

With fewer than 3% of drivers under 25, retirements outpace recruits, leaving fleets short of capacity. Annual economic drag hits USD 11 billion as routes are deferred or priced higher. Regulatory hurdles for non-EU drivers and lifestyle concerns depress new entries, forcing 3PLs to increase wages and invest in retention amenities. Larger operators buffer the impact with autonomous yard tractors and optimized routing, whereas small firms face margin compression and the risk of exit[3]Dirk Engelhardt, “Driver Shortage Position Paper 2025,” Federal Association of Road Haulage, bgl-ev.de.

High Electricity Tariffs Limit Cold-Chain Capacity Expansion

Germany’s layered taxes and levies keep industrial power prices among Europe’s highest. Cold-storage operators, where refrigeration can account for 40% of costs, hesitate to build new space without long-term tariff clarity. Exemptions favor very large power consumers, leaving midsize 3PLs at a disadvantage. Solar and battery retrofits mitigate some exposure, yet capital outlays raise barriers to entry, constraining cold-chain growth until energy policy stabilizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Domestic Transportation Dominates Amid Warehousing Acceleration

Domestic Transportation Management contributed 38.45% to 2025 revenue, underlining the Germany third-party logistics market size derived from the country’s 13,000-km Autobahn grid and dense industrial clusters. Regular groupage and full-truckload moves support export production and intra-EU supply chains. Meanwhile, Value-Added Warehousing & Distribution is projected to grow 6.55% annually through 2031 as retailers decentralize inventory and manufacturers demand postponement services. This shift raises the Germany third-party logistics market share of facility-based offerings, encouraging providers to retrofit space with shuttle systems, voice-directed picking, and temperature-controlled zones.

Automation and real-time visibility reshape service boundaries. Carriers such as Rhenus trimmed network transit times by 34% after redesigning hub flows, proving that IT-enabled routing can unlock capacity without expanding fleets. Clients increasingly request transport-related warehousing, expecting single-invoice, end-to-end solutions. Consequently, 3PLs bundle consolidation, cross-dock, and final-mile under unified contracts, blurring the lines between legacy transport and storage segments.

By End User: Retail Leads While Automotive Accelerates

E-commerce retained a 20.65% revenue share in 2025 thanks to robust parcel demand, same-day delivery pledges, and returns processing complexity. The segment’s scale cements the Germany third-party logistics market size foundation for high-throughput sortation centers. Automotive, however, is poised for a 4.12% CAGR as electrification, battery import logistics, and just-in-sequence delivery of lightweight components intensify outsourcing. Battery pack regulations favor certified 3PL warehouses that meet stringent fire-safety norms, providing a premium niche.

Partnerships evidence the trend: DHL Supply Chain now orchestrates 100,000 annual moves for Vitesco Technologies across 12 European plants, centralizing control-tower functions to trim emissions and cost. Automotive volume volatility drives demand for flexible contracts with surge capacity, pushing 3PLs to invest in shared, modular spaces rather than dedicated warehouses. Across manufacturing, life-sciences cold-chain, and tech-electronics high-value cargo sustain steady bookings, even as energy & utilities clients grapple with commodity cycles.

By Logistics Model: Asset-Light Preference Amid Hybrid Growth

Customers gravitate toward Asset-Light offerings, which claimed 41.35% of 2025 turnover, to avoid capital lock-in and leverage 3PL technology stacks. Yet, Hybrid models will lead growth at 4.96% CAGR as shippers co-locate dedicated fleets with variable 3PL capacity. Germany’s third-party logistics market rewards providers that can orchestrate outsourced and owned assets through API-connected platforms, delivering cost and service transparency.

Truck-as-a-Service solutions accelerate the Asset-Light shift, particularly for zero-emission vehicles where acquisition costs remain high. Subscription bundles covering vehicles, charging, and maintenance de-risk electric adoption, allowing shippers to pilot clean transport without balance-sheet strain. Simultaneously, sectors with irregular demand—notably FMCG promotions—adopt Hybrid setups, expanding private fleets for peak season while maintaining spot access to third-party carriers.

Geography Analysis

North Rhine-Westphalia (NRW) secured 22.60% of 2025 revenue, the largest share within the Germany third-party logistics market, anchored by Duisburg’s inland port and Cologne’s multimodal nodes. The region funnels goods to 500 million consumers within three driving hours and hosts Germany’s second-largest air cargo hub at Cologne/Bonn airport. NRW’s smart-logistics clusters leverage 5G corridors and university partnerships, positioning the state for continued supremacy as digital-control-tower adoption spreads.

Baden-Württemberg shows the fastest trajectory at a 4.18% CAGR to 2031. Its USD 223.3 billion export base, 5.6% R&D intensity, and concentration of automotive innovators such as Bosch and Daimler sustain demand for high-spec warehousing. The Northern Black Forest’s combined rail-road terminal enhances intra-European reach, while lower land costs around Augsburg attract new fulfillment investments. The state’s 3.2% unemployment rate signals labor tightness that heightens interest in automation partnerships with logistics providers.

Bavaria maintains a solid share through Munich’s economic heft and proximity to Alpine borders, capturing Austrian and CEE flows. Hamburg capitalizes on early adoption of shore power and hydrogen bunkering to position its port for carbon-neutral freight, offering shippers ESG-compliant gateway options. Eastern states, benefitting from lower real estate prices and EU funds, woo e-commerce operators seeking lower total landed cost to Poland and the Czech Republic. Germany’s polycentric structure, backed by seamless highway and rail links, enables multi-hub network design where inventory placement follows real-time demand.

Competitive Landscape

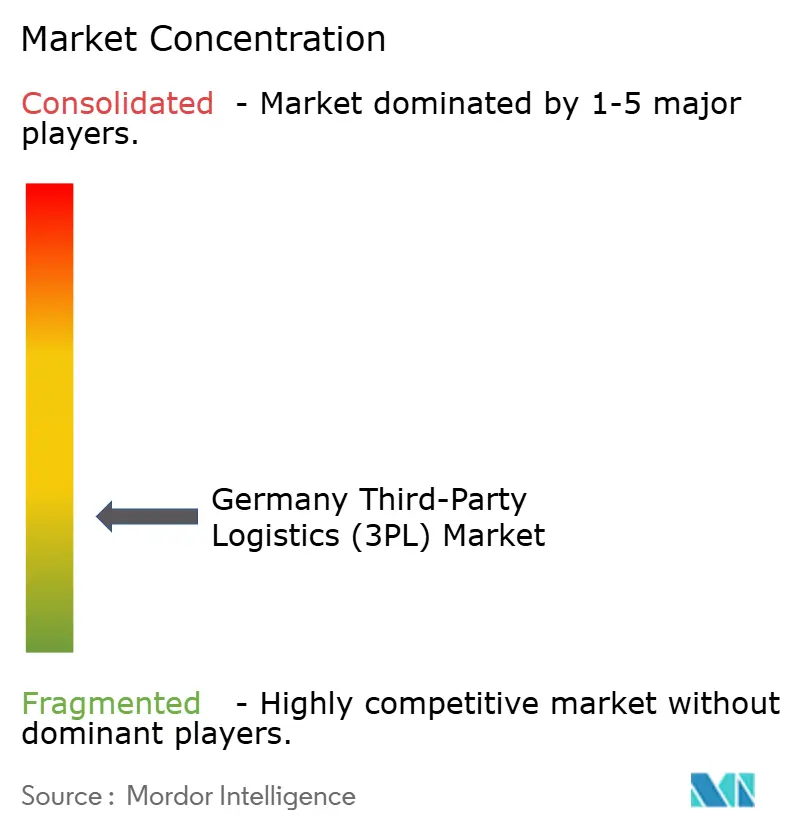

The market is fragmented. In April 2025 when DSV closed its USD 15.73 billion purchase of DB Schenker, forming a USD 45.76 billion revenue leader spanning 90 countries. Scale affords the merged group bargaining power in air and ocean procurement and funds R&D in robotics and visibility platforms. The deal signals a pivot from pure volume growth toward high-tech, asset-optimized service models across the Germany third-party logistics market.

Automation remains a differentiator. DHL Group’s additional 1,000 robots complement 7,500 deployed units, with capex earmarked at USD 1.1 billion for automation between 2025-2027. Early pilots generated 25% productivity gains and 80% incident reduction. Smaller providers specialize in staying relevant—offering EV battery storage compliant with ADR regulations or catering to defense supply chains requiring security accreditation.

Sustainability shapes bidding criteria. Tender documents increasingly stipulate carbon reporting and renewable-power sourcing. Operators able to guarantee solar-backed warehousing and HVO-powered trucking win multi-year contracts at premium rates. Those lagging in green upgrades confront potential customer attrition as Scope 3 targets tighten from 2026 onward.

Germany Third-Party Logistics (3PL) Industry Leaders

Deutsche Post DHL

Dachser

Kuehne + Nagel

DSV

Hellmann Worldwide Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: DHL and Boston Dynamics signed an agreement to deploy 1,000 additional robots, targeting 700-case-per-hour unloading speeds.

- April 2025: DSV finalized the USD 15.73 billion DB Schenker acquisition, pledging USD 1.1 billion investment in German operations over five years.

- January 2025: DHL Supply Chain acquired Inmar Supply Chain Solutions, adding 14 returns centers and 800 staff to strengthen North American reverse-logistics capabilities.

- January 2025: Rheinmetall secured a USD 363 million Bundeswehr order for 568 logistics vehicles within a broader USD 3.85 billion framework.

Germany Third-Party Logistics (3PL) Market Report Scope

A 3PL (third-party logistics) provider offers outsourced logistics services, which encompass anything that involves managing one or more facets of procurement and fulfillment activities. The report offers a complete background analysis of the German 3PL market, including a market overview, market size estimation for key segments, emerging trends by segments, and market dynamics. The report also offers the Impact of Geopolitics and Pandemics on the Market.

Germany's Third-Party Logistics (3PL) market is Segmented by Type (Domestic Transportation Management, International Transportation Management, and Value-added Warehousing and Distribution) and End User. The report offers market sizes and forecasts in value (USD billion) for all the above segments.

By Service

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing & Distribution (VAWD) |

By End User

| Automotive |

| Energy & Utilities |

| Manufacturing |

| Life Sciences & Healthcare |

| Technology & Electronics |

| E-commerce |

| Consumer Goods & FMCG |

| Food & Beverages |

| Others |

By Logistics Model

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet & Warehouses) |

| Hybrid |

By States – Germany (Value)

| North Rhine-Westphalia |

| Bavaria (Bayern) |

| Baden-Württemberg |

| Rest of States |

| By Service | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing & Distribution (VAWD) | ||

| By End User | Automotive | |

| Energy & Utilities | ||

| Manufacturing | ||

| Life Sciences & Healthcare | ||

| Technology & Electronics | ||

| E-commerce | ||

| Consumer Goods & FMCG | ||

| Food & Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet & Warehouses) | ||

| Hybrid | ||

| By States – Germany (Value) | North Rhine-Westphalia | |

| Bavaria (Bayern) | ||

| Baden-Württemberg | ||

| Rest of States | ||

Key Questions Answered in the Report

What is the 2026 value of the Germany third-party logistics market?

The sector is worth USD 42.29 billion in 2026.

How fast will third-party logistics in Germany grow through 2031?

Revenue is forecast to expand at a 3.97% CAGR, reaching USD 51.37 billion.

Which service dominates outsourced logistics demand in Germany?

Domestic Transportation Management leads with 38.45% of 2025 revenue.

Which German state shows the quickest logistics growth outlook?

Baden-Württemberg is projected to post a 4.18% CAGR between 2026-2031.

Page last updated on: