Ginger Beer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.45 Billion |

| Market Size (2031) | USD 8.61 Billion |

| Growth Rate (2026 - 2031) | 7.50% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

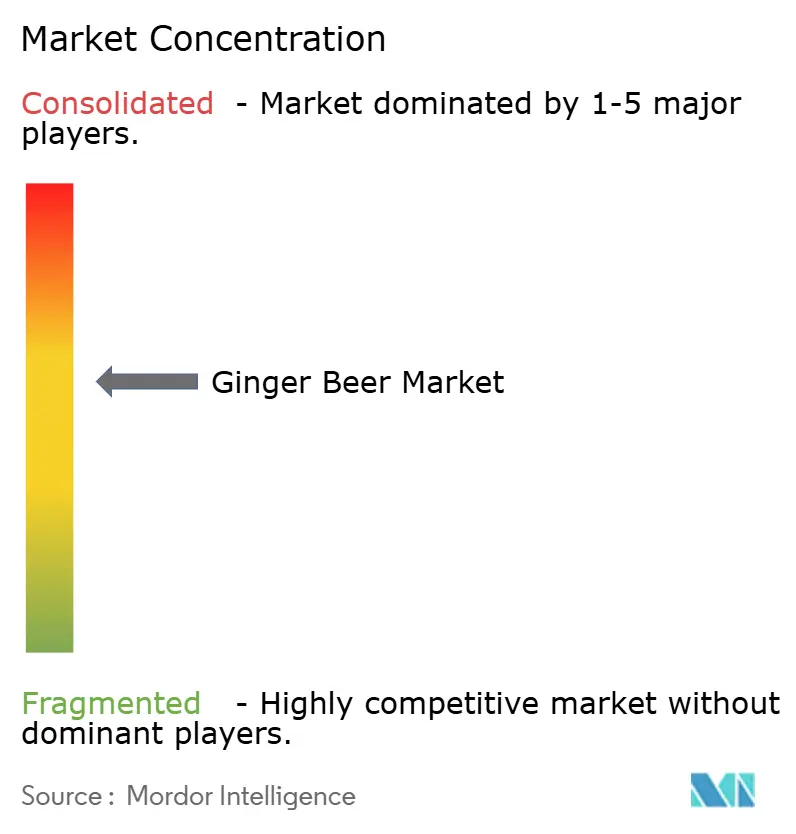

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ginger Beer Market Analysis by Mordor Intelligence

The global ginger beer market was valued at USD 5.95 billion in 2025 and is estimated to grow from USD 6.45 billion in 2026 to USD 8.60 billion by 2031, at a CAGR of 7.50% during the forecast period (2026-2031). Rising consumer interest in premium mixers, functional sodas, and no- and low-alcohol social occasions underpins this trajectory, reflecting sustained structural expansion. Non-alcoholic variants continue to drive recurring purchases among everyday consumers, including Moscow Mule enthusiasts and sober-curious shoppers, while alcoholic lines gain traction through increasing presence in ready-to-drink (RTD) formats, boosting visibility across convenience and on-premise channels. Brand owners also benefit from evolving flavor innovation, as ginger remains a top emerging RTD alcohol flavor, encouraging premium infusions such as blood orange, yuzu, and elderflower that enhance product differentiation and pricing power.

Key Report Takeaways

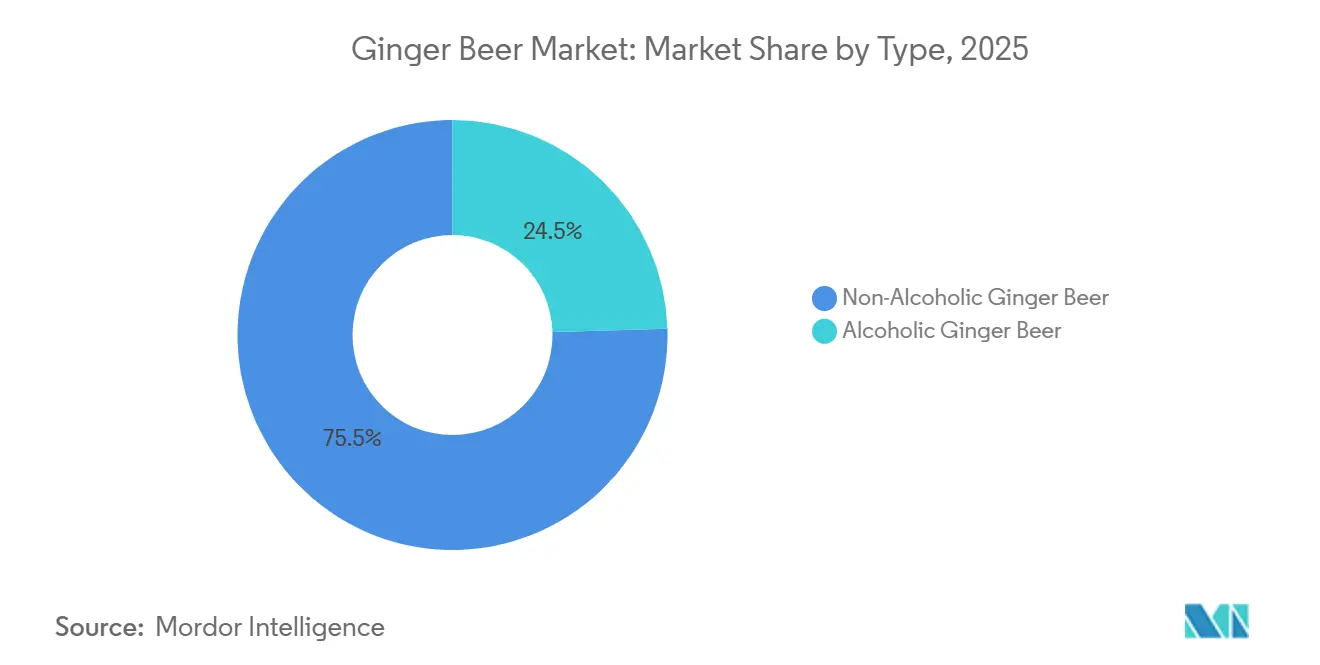

- By type, non-alcoholic products led with 75.46% of the ginger beer market share in 2025, while alcoholic products are projected to grow at a 7.85% CAGR through 2031.

- By flavor, original recipes accounted for 63.70% share of the ginger beer market size in 2025; flavoured variants post the highest forecast CAGR at 9.01% to 2031.

- By packaging, glass bottles commanded 48.05% share in 2025, whereas aluminium cans are expanding at a 7.70% CAGR through 2031.

- By distribution channel, off-trade outlets captured 69.12% share in 2025, while on-trade is advancing at an 8.65% CAGR on the back of cocktail-culture recovery.

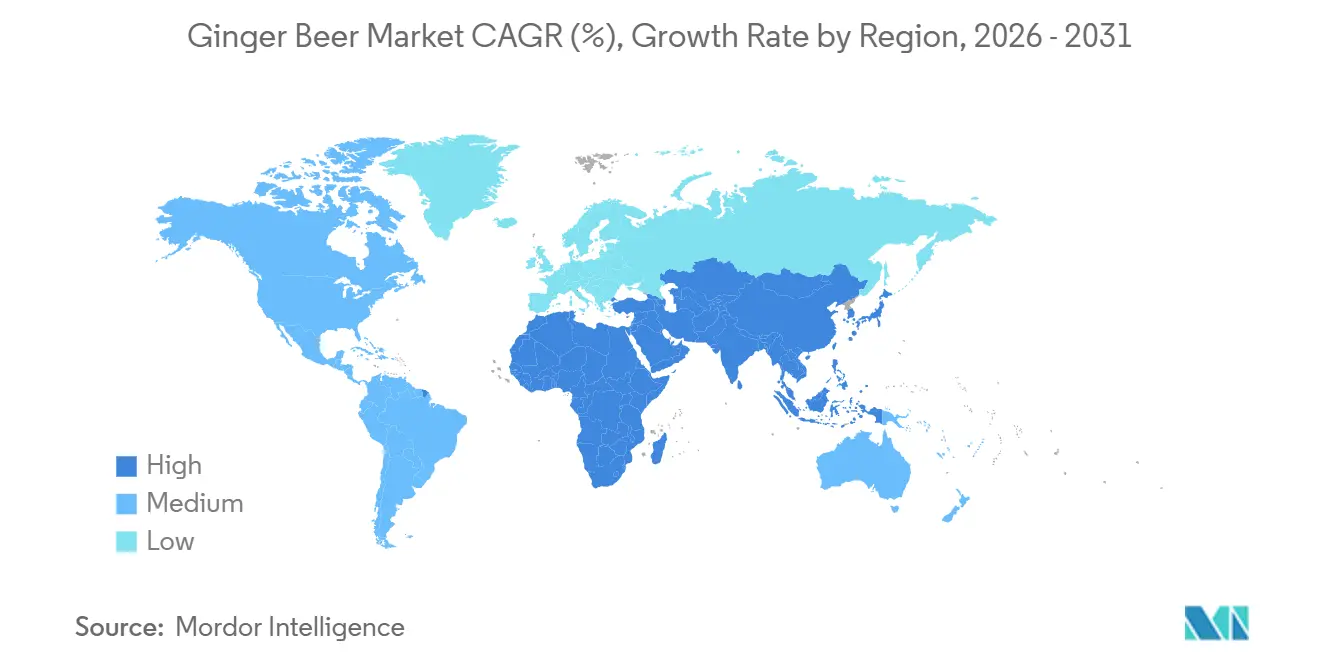

- By geography, North America held 32.54% revenue share in 2025; Asia-Pacific is forecast to be the fastest-growing region at a 10.50% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ginger Beer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Flavor Innovation & Diversification | +1.4% | Global, particularly Asia-Pacific emerging markets | Medium term (2-4 years) |

| Expansion of the Craft Beverage Segment | +1.2% | Global, with North America & Europe leading | Long term (≥ 4 years) |

| Premiumization & Heritage-Led Positioning | +1.0% | North America & Europe core, expanding to APAC | Medium term (2-4 years) |

| Growth of Cocktail Culture & RTD Segment | +1.6% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Influence of Global Culinary Fusion Flavors | +0.9% | Asia-Pacific and Latin America drive fusion profiles | Medium term (2-4 years) |

| Adoption of Technology-Driven Product Development | +0.7% | Global, with advanced manufacturing regions leading | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Flavor Innovation and Portfolio Diversification

Flavor innovation is moving beyond traditional ginger profiles, with brands layering blood orange, yuzu, elderflower, and adaptogenic botanicals to enhance differentiation and premium appeal. This strategy strengthens shelf visibility and supports higher price realization, as seen in premium-positioned variants like blood orange ginger beer collaborations. Functional integration is also accelerating, with offerings combining high ginger content, prebiotic fiber, and adaptogens while maintaining low-calorie profiles, appealing to health-conscious consumers. Reed’s SodaSmarter line exemplifies functional product innovation by incorporating 2,000–5,000 mg of organic ginger, prebiotic fiber, and mushroom adaptogens within a low-calorie (30–45 kcal) format, effectively positioning the brand at the intersection of health benefits and indulgent beverage experiences[1]Source: Reed’s Inc., “Reed’s Launches New Multifunctional Soda Line,” reedsinc.com. Flavor houses continue to rank ginger among top emerging RTD alcohol flavors, driven by strong consumer preference for novelty-led purchases. This broad experimentation expands consumption occasions, extends trial, and strengthens pricing architecture.

Expansion of the Craft Beverage Segment

As consumer expectations evolve, the craft beverage movement remains at the forefront, emphasizing authenticity, slow-brewed processes, and small-batch production that differentiate offerings from mass-produced alternatives. This shift reflects a broader consumer preference for artisanal quality, with craft ginger beer brands commanding significant 20-25% price premiums over conventional sodas. Brands leveraging heritage-driven narratives, such as extended brewing cycles and organic ingredient positioning, are strengthening their premium appeal while building strong regional followings. Moreover, regulatory bodies are lending a hand, easing compliance challenges for smaller producers. Notably, the TTB's formula exemptions, tailored for traditional fermentation, have been a boon for craft ginger beer makers[2]Source: GOV.UK, “Soft drinks levy extended,” gov.uk. This supportive regulatory landscape positions craft producers advantageously, allowing them to harness greater value as consumers increasingly gravitate towards premium, locally-sourced options.

Premiumization and Heritage-Led Brand Positioning

Heritage branding continues to carve out sustainable competitive advantages by reinforcing provenance, premium inputs, and authenticity that extend beyond price-based competition. In the ginger beer market, brands emphasizing origin stories, such as sourcing multiple ginger varieties and maintaining clean-label certifications, are strengthening their premium positioning and securing higher shelf prices. This approach not only enhances retail value perception but also drives bartender endorsements, increasing on-premise visibility and brand recall. Packaging innovation further amplifies this premium narrative, with a growing shift toward aluminum formats perceived as both sustainable and upscale, enabling brands to increase value per ounce. Product reformulations are also evolving, blending natural ginger with adjacent functional cues such as caffeine to tap into energy-drink crossover demand. Heritage cues are equally influential in off-premise channels, where consumers increasingly seek “bar-quality” experiences at home, boosting demand for premium mixers. Bartender-driven brand specification creates a halo effect, encouraging at-home replication and reinforcing pricing power.

Growth of Cocktail Culture and the RTD Segment

The growing cocktail culture continues to expand ginger beer consumption beyond traditional uses, positioning it as a key mixer in premium cocktails and ready-to-drink (RTD) beverages. Signature serves such as Moscow Mules and Dark & Stormies act as gateway occasions, accelerating adoption across both on-premise and at-home settings. The market is evolving through RTD innovation, with ginger beer brands collaborating with spirits companies to launch pre-mixed offerings, including higher-ABV Moscow Mules and hard ginger ales, catering to convenience-driven consumers. Cross-category success in highball-style drinks further highlights the spillover potential of ginger-forward profiles into broader alcohol segments. On-premise demand remains strong, supported by robust mixer sales and the continued popularity of ginger among top flavor choices. Meanwhile, the rise of craft canned cocktails is enhancing visibility across alcohol aisles, convenience channels, and bar menus. This dual-channel momentum strengthens ginger beer’s role in both experiential consumption and everyday convenience, sustaining long-term market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Pressures from Sugar Taxes & HFSS Norms | -1.2% | Europe & UK core, expanding globally | Short term (≤ 2 years) |

| Intensifying Competition from Alternative Drinks | -0.8% | Global, particularly in premium segments | Medium term (2-4 years) |

| Supply Chain Volatility in Premium Ginger | -0.9% | Global, with emerging markets most affected | Short term (≤ 2 years) |

| Cold-Chain Gaps in Emerging Markets | -0.6% | Asia-Pacific, MEA, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Pressures from Sugar Taxes and HFSS Norms

Sugar taxes and HFSS (High in Fat, Salt, and Sugar) regulations continue to reshape product formulation and commercialization strategies in the beverage industry. The UK’s extension of the Soft Drinks Industry Levy, lowering the taxable threshold to 4.5g per 100ml from 2028, alongside Scotland’s HFSS rules restricting multibuy promotions and in-store placement, intensifies compliance pressures[3]Source: Alcohol and Tobacco Tax and Trade Bureau, "Formulation Exemptions for Traditional Fermentation," ttb.gov. Companies must now balance taste, cost, and regulatory alignment, facing a strategic choice between investing in alternative sweeteners and smaller pack formats or absorbing levy costs at the risk of volume decline. These evolving regulations also constrain promotional flexibility and retail visibility, directly impacting sales strategies. While the regulatory burden is expected to trim approximately 1.2 percentage points from forecast CAGR, it simultaneously accelerates innovation in zero- and low-sugar variants. Brands that successfully reformulate while maintaining taste profiles can command a higher price per ounce, turning compliance into a competitive advantage amid shifting consumer preferences toward healthier options.

Intensifying Competition from Alternative Beverage Categories

As functional sodas, hard seltzers, and kombuchas increasingly target health-conscious consumers with low-sugar positioning and strong wellness narratives, competition in the alternative beverage sector continues to intensify. The rapid scale-up of prebiotic sodas, demonstrated by high-growth, low-sugar brands achieving substantial retail sales, highlights the shifting competitive benchmark toward functionality and regulatory alignment. This crowded landscape is further complicated by RTD fatigue, with many consumers perceiving an oversupply of choices and showing limited willingness to trial new products. As a result, shelf-space competition is becoming more acute, particularly in premium and better-for-you segments. To remain competitive, ginger beer brands must clearly differentiate through authentic spice profiles, cocktail versatility, and functional ginger benefits. Consequently, the category is doubling down on heritage positioning and flavor authenticity to sustain consumer interest, protect shelf velocity, and defend market share against emerging alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Non-Alcoholic Dominance Faces Alcoholic Acceleration

Despite non-alcoholic variants commanding a dominant 75.46% market share in 2025, the alcoholic ginger beer segment is projected to grow at a faster 7.85% CAGR, driven by the rapid expansion of hard ginger ales and spirit-based RTDs. This divergence reflects increasing consumer openness to alcoholic formats, particularly as products such as higher-ABV Moscow Mule variants secure prime cooler placements, boosting impulse purchases and attracting new consumer segments. Regulatory frameworks continue to support this growth, although distribution remains more complex due to licensing requirements and on-premise dependencies.

Non-alcoholic ginger beer’s continued dominance highlights its entrenched role as both a mixer and a wellness-oriented beverage. Brands are increasingly enhancing value propositions by incorporating functional ingredients such as high-dose ginger, adaptogens, and prebiotics, repositioning products toward gut health and daily consumption occasions. At the same time, alcoholic producers are also integrating functional cues, signaling convergence between indulgence and wellness trends. Distribution strategies are diverging across segments, with non-alcoholic variants scaling efficiently through retail and e-commerce channels, while alcoholic offerings rely on regulated distribution networks and bar programs. This dual-track expansion strengthens overall market resilience, reducing dependence on any single channel or regulatory environment while sustaining long-term growth potential.

By Flavor: Original Resilience, Flavored Momentum

Classic recipes continue to dominate the ginger beer market, accounting for a 63.70% share in 2025, supported by strong bartender loyalty and their essential role in staple cocktails such as Moscow Mules and Dark & Stormies. This stability reflects entrenched consumer expectations and the importance of consistency in both on-premise and at-home consumption. However, flavored variants are projected to grow faster at a 9.01% CAGR through 2031, driven by rising demand for innovative and visually appealing offerings. Flavors such as blood orange, yuzu, elderflower, hibiscus, and chili are leading this shift, enhancing shelf visibility and enabling seasonal, limited-time launches that expand consumption occasions. Brands are leveraging a single ginger base to diversify into adjacent categories, including prebiotic sodas, mocktails, and functional beverages, reinforcing portfolio flexibility. Similarly, companies must carefully manage SKU expansion to avoid cannibalizing core products. Leading players are therefore adopting a balanced strategy, retaining a flagship original variant while introducing a limited number of rotating flavored SKUs aligned with regional taste preferences, ensuring both innovation and brand consistency.

By Packaging: Heritage Glass Packaging Blended with Sustainable Aluminum Innovation

Aluminum cans are projected to grow at a CAGR of 7.70%, driven by rising demand for sustainability, convenience, and suitability for e-commerce and bulk retail channels. Meanwhile, glass bottles retained a leading 48.05% market share in 2025, supported by their strong premium positioning and heritage appeal. This dynamic highlights the increasing influence of environmental considerations alongside consumer preference for tactile, high-quality packaging. While aluminum benefits from high recycling rates and lightweight logistics, glass continues to anchor brand authenticity and premium perception.

The shift toward aluminum is further reinforced by cost efficiencies and supply-chain advantages, with brands transitioning select SKUs to cans to reduce freight and breakage while expanding into club and convenience channels. At the same time, innovations such as digital can printing and resealable aluminum formats are narrowing the gap between premium and mass packaging.

Glass packaging maintains its importance in on-premise and craft positioning, where visual appeal and brand storytelling are critical. PET bottles continue to serve price-sensitive segments but face challenges due to weaker sustainability and premium perceptions. Leading brands are therefore adopting multi-format packaging strategies to balance cost, convenience, and brand equity across diverse consumption occasions.

By Distribution Channel: Off-Trade Scale Meets On-Trade Velocity

Off-trade channels continue to dominate the ginger beer market, accounting for 69.12% of value in 2025, driven by strong volume throughput in supermarkets, hypermarkets, and e-commerce platforms supported by promotions and secondary displays. This channel provides scale and consistent demand, further amplified by the rise of online retail and rapid-delivery platforms that act as digital impulse purchase channels for premium mixers.

In contrast, on-trade channels are projected to grow at a robust 8.65% CAGR, fueled by increasing integration of premium ginger beers into cocktail and mocktail menus across bars, restaurants, and clubs. Higher per-unit pricing in on-premise settings significantly boosts value realization, while bartender endorsements and menu placements enhance brand visibility and consumer trial. E-commerce is emerging as a key growth lever within off-trade, enabling direct-to-consumer engagement, subscription models, and data-driven product innovation. The optimal strategy blends high-volume off-trade distribution with high-margin on-trade placements, creating a halo effect that strengthens brand equity. By leveraging off-trade scale to support on-trade premiumization, brands can maximize both penetration and profitability across channels.

Geography Analysis

North America leads the ginger beer market with a 32.54% value share in 2025, underpinned by a well-established craft beverage ecosystem, strong cocktail culture, and continued on-premise recovery. The U.S. remains the growth engine, supported by dominant players leveraging scale and distribution partnerships to expand reach and reduce logistics costs. Strategic alliances and capital market access are further enabling innovation and portfolio expansion, while Canada and Mexico contribute incremental growth through expanding retail and RTD alcohol displays. The region’s outlook remains anchored in premiumization and product innovation.

Europe reflects a balance between heritage strength and regulatory pressure. Sugar taxes and HFSS restrictions are accelerating reformulation and zero-sugar innovation, while also compressing margins on traditional offerings. However, strong consumer willingness to pay for functional and premium beverages sustains growth opportunities. Competitive intensity is rising, particularly in Southern Europe, where new product launches and functional hybrids are reshaping the landscape. Localization strategies, including near-shoring production, are becoming increasingly important to manage costs and regulatory shifts.

Asia-Pacific is the fastest-growing region, projected to expand at a 10.50% CAGR through 2031, driven by urbanization, rising incomes, and rapid development of e-commerce and cold-chain infrastructure. However, infrastructure gaps, particularly in markets like India, continue to constrain widespread premium distribution, limiting reach to urban centers. Developed markets such as Japan and Australia support premium growth through advanced logistics, while China represents a major long-term opportunity due to cultural alignment with ginger and increasing demand for functional beverages.

South America and the Middle East & Africa currently represent smaller shares but offer strong long-term potential, supported by rising beverage consumption and urbanization trends. Infrastructure limitations, particularly in cold storage, favor shelf-stable packaging formats such as cans and PET bottles in the near term. Brands are increasingly leveraging localized flavor profiles to connect with regional preferences while maintaining core product identity, enabling expansion even in logistics-constrained environments.

Competitive Landscape

The ginger beer market remains moderately concentrated, with a mid-range concentration level, where heritage leaders coexist with agile craft and regional innovators. Key players such as Fever-Tree, Bundaberg, Reed’s, Fentimans, Gosling’s, and Q Mixers collectively account for well below 80% of total share, leaving ample room for niche entrants to scale through differentiated offerings. Established brands continue to leverage premium positioning, distribution strength, and on-premise visibility, reinforcing their competitive edge while maintaining market balance.

Strategic partnerships and acquisitions are increasingly shaping the landscape, with large beverage companies targeting high-growth, functional, and premium segments. Recent investments in adjacent categories, particularly gut-health beverages, a broader consolidation trend that could extend to functional ginger beer players. These moves enable faster market penetration while combining brand equity with expansive distribution networks. Technology is emerging as a critical differentiator, with leading beverage companies adopting AI-driven demand forecasting, supply chain optimization, and targeted marketing to enhance margins and operational efficiency. Mid-sized players are also investing in automation and flexible production systems to remain competitive.

Meanwhile, smaller entrants continue to carve out space through niche positioning, such as single-origin sourcing, functional ingredients, and sustainability-led narratives, to avoid direct price competition. However, as the market matures, scaling challenges persist, making strategic alliances or acquisitions increasingly likely. Overall, while the industry remains fragmented, consolidation is expected to accelerate around premiumization and functional innovation themes.

Ginger Beer Industry Leaders

-

Fever-Tree Drinks Plc

-

Bundaberg Brewed Drinks Pty Ltd.

-

Reed’s Inc.

-

Gosling Brothers Limited

-

Fentimans Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Q Mixers expanded its portfolio with the launch of Q Refreshers, a 7.5-oz sparkling canned range fortified with electrolytes and vitamins, strategically positioned as a dual-use product for both mixing and standalone consumption, with distribution scaled across major retail and e-commerce channels, including Kroger, H-E-B, and Amazon.

- March 2026: Stoli Group relaunched its ginger beer with a reformulated profile featuring natural ginger, chili, lemon, and coffee-bean-derived caffeine, targeting a threefold increase in global volumes while prioritizing expansion across Southern Europe and China.

- February 2025: Molson Coors Beverage Company acquired an 8.5% stake in Fever-Tree Drinks plc and exclusive US commercialization rights for its premium mixer portfolio, including ginger beer. The strategic partnership, valued at USD 200 million, makes Molson Coors the second-largest shareholder in Fever-Tree. The agreement enables Molson Coors to use its distribution network to expand Fever-Tree's premium mixer presence across North America.

- January 2025: Carlsberg completed its acquisition of Britvic plc, a major UK soft drinks company with significant ginger beer portfolio presence, following regulatory approval from UK competition authorities. The acquisition strengthens Carlsberg's non-alcoholic beverage portfolio and provides enhanced distribution capabilities for premium mixer brands across European markets.

Global Ginger Beer Market Report Scope

Ginger beer, a carbonated beverage made from fermented or brewed ginger, sugar, and water, is widely consumed both as a standalone refreshment and as a key cocktail mixer.

The global ginger beer market is analyzed across several dimensions, including product type, flavor profile, packaging type, distribution channels, and geography. By product type, the market is segmented into alcoholic and non-alcoholic ginger beer. By flavor profile, it includes traditional and flavored variants (such as citrus, botanical, and spice-infused). Packaging type is categorized into glass bottles, aluminum cans, PET bottles, and kegs. Distribution channels comprise supermarkets/hypermarkets, convenience stores, specialty retailers, online stores, and on-trade channels such as bars and restaurants. Geographically, the study covers key markets including North America, Europe, Asia-Pacific, South America, and Middle East, and Africa.

For each segment, market sizing and forecasts are provided in terms of value (USD million) and volume (liters).

| Non-Alcoholic Ginger Beer |

| Alcoholic Ginger Beer |

| Original/Traditional Ginger Beer |

| Flavored Ginger Beer |

| Bottles (Glass) |

| Cans |

| PET Bottles |

| Kegs |

| On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets |

| Online Retail | |

| Specialty Stores | |

| Other Off-Trade Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Type | Non-Alcoholic Ginger Beer | |

| Alcoholic Ginger Beer | ||

| By Flavor | Original/Traditional Ginger Beer | |

| Flavored Ginger Beer | ||

| By Packaging | Bottles (Glass) | |

| Cans | ||

| PET Bottles | ||

| Kegs | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets | |

| Online Retail | ||

| Specialty Stores | ||

| Other Off-Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global ginger beer market?

The ginger beer market size was valued at USD 5.95 billion in 2025.

How fast is the market expected to grow?

The category is projected to expand at a 7.50% CAGR, reaching USD 8.61 billion by 2031.

Which product type leads the market?

Non-alcoholic variants hold 75.46% of ginger beer market share, serving as the primary revenue driver.

Which region offers the strongest growth outlook?

Asia-Pacific is forecast to grow the fastest at a 10.50% CAGR, propelled by rising urban incomes and cocktail adoption.

Page last updated on: