Brewer's Yeast Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

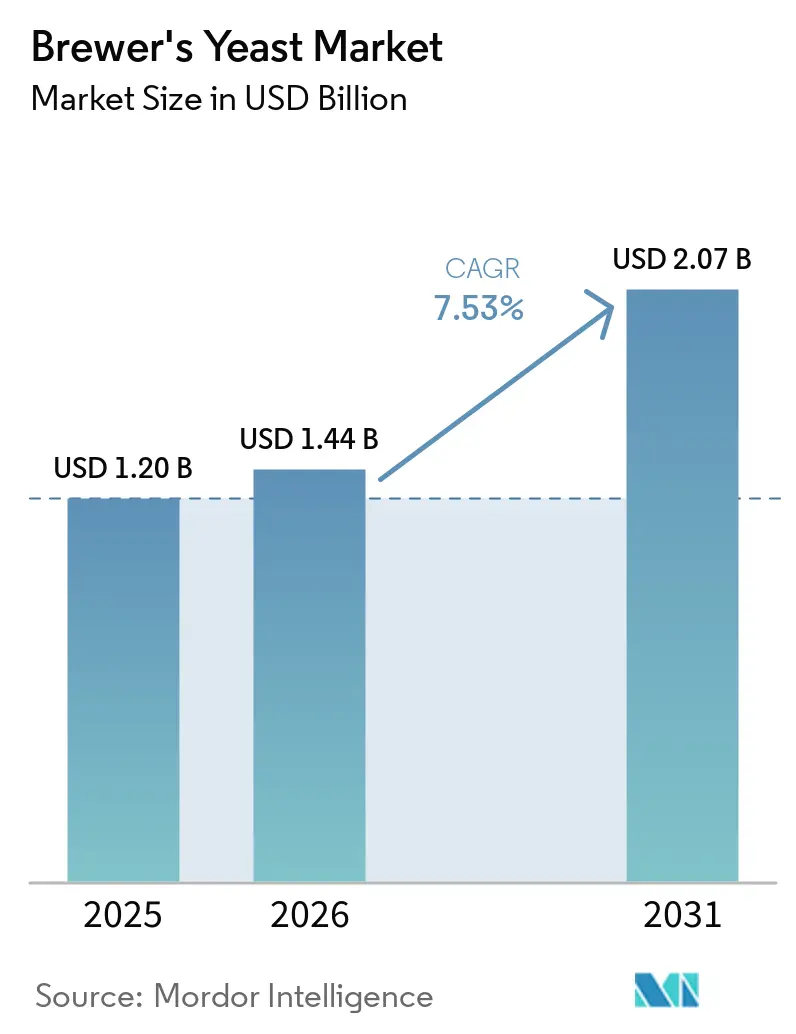

| Market Size (2026) | USD 1.44 Billion |

| Market Size (2031) | USD 2.07 Billion |

| Growth Rate (2026 - 2031) | 7.53% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

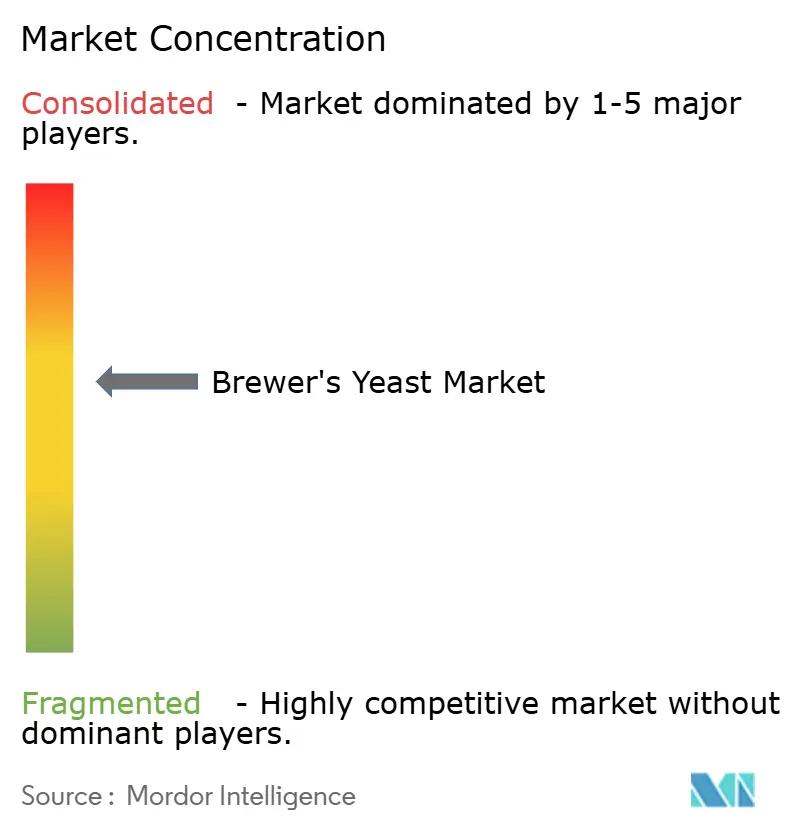

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brewer's Yeast Market Analysis by Mordor Intelligence

The brewing yeast market size is expected to increase from USD 1.20 billion in 2025 to USD 1.44 billion in 2026 and is forecast to reach USD 2.07 billion by 2031 at a CAGR of 7.53% over 2026 to 2031. The brewing yeast market is moving forward because brewers are paying more for reliable strains, cleaner fermentation performance, and stronger flavor differentiation as premium beer categories expand across several regions. Beer demand remains uneven by geography, which is pushing suppliers in the brewing yeast market to balance large volume contracts in mature countries with faster growth opportunities in India, Southeast Asia, and selected African markets. The brewing yeast market is also benefiting from a wider shift toward circular value creation, as spent yeast is now being used in flavor ingredients, functional food inputs, and animal nutrition rather than being treated only as a disposal stream. Competition in the brewing yeast market remains moderately concentrated, with global fermentation specialists using strain libraries, manufacturing scale, and technical support to protect their positions while smaller specialists stay relevant through customization and service.

Key Report Takeaways

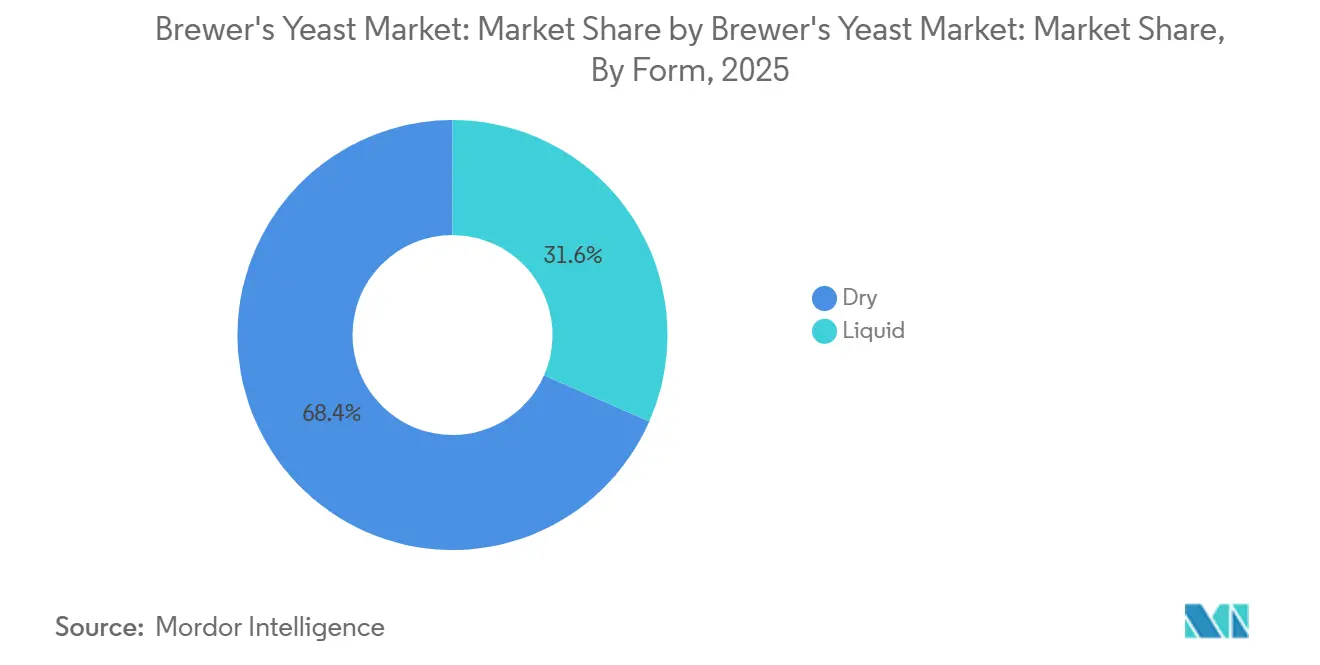

- By form, dry brewing yeast held 68.40% of the market in 2025, while liquid brewing yeast is projected to grow at the fastest 8.31% CAGR through 2031.

- By application, lager accounted for 58.70% of the brewing yeast market size in 2025, while ale is forecast to expand at the fastest 9.50% CAGR through 2031.

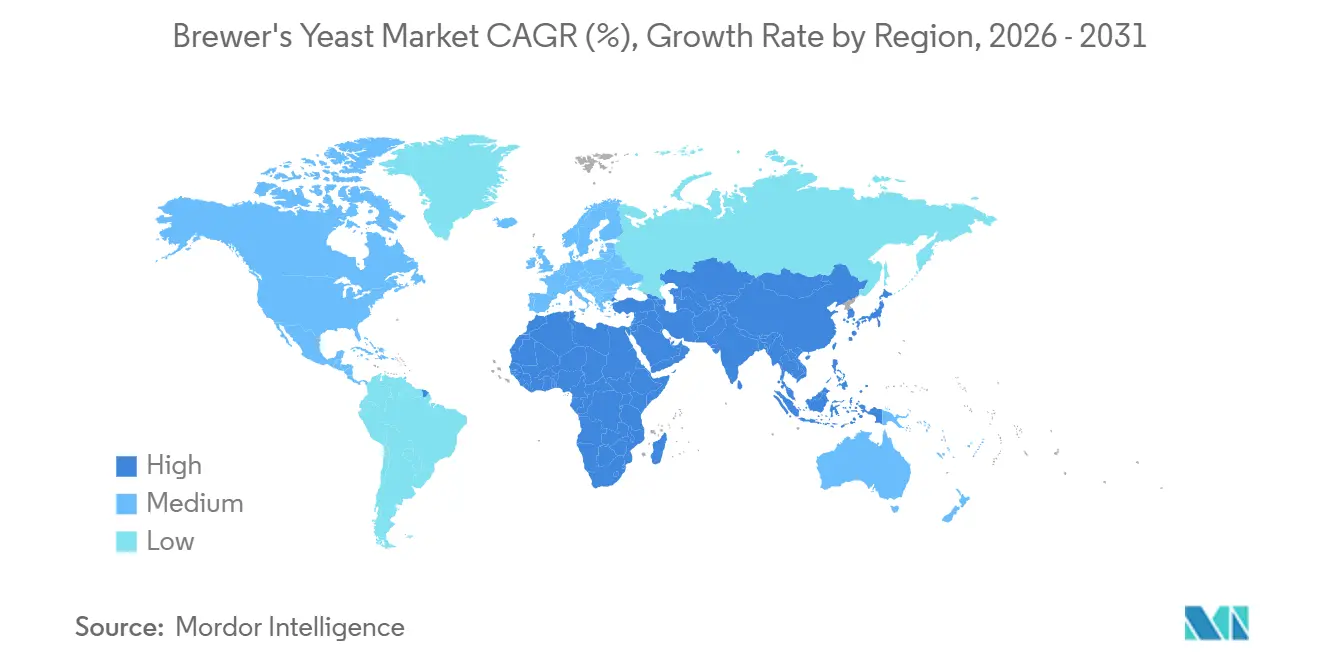

- By geography, Europe held 36.53% of the market in 2025, while the Asia Pacific is projected to grow at the fastest 11.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Brewer's Yeast Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for natural and functional brewing ingredients | +1.4% | Global, with early concentration in North America, EU, and Australia | Medium term (2-4 years) |

| Expansion of craft beer and premium brewing output | +1.2% | North America and EU, with spillover to Asia-Pacific and South America | Medium term (2-4 years) |

| Increasing global beer consumption | +0.9% | Asia Pacific core, especially India, Vietnam, and Indonesia, and Middle East and Africa | Long term (≥ 4 years) |

| Craft breweries focus on flavor innovation and yeast-derived characteristics | +0.8% | North America and Western Europe | Short term (≤ 2 years) |

| Adoption of genetically modified and functional yeast strains | +0.6% | North America, EU, and Australia | Medium term (2-4 years) |

| Brewery side-stream monetization improves circular economy economics | +0.5% | EU core, especially Germany, Belgium, and the Czech Republic | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing demand for natural and functional brewing ingredients

The brewing yeast market is seeing a clear move away from purely commodity purchasing and toward specification-led sourcing. Brewers are asking for traceability, non-Genetically Modified Organism (GMO) documentation, and clearer strain origin records because ingredient transparency now supports brand positioning in premium beer categories. This is shifting leverage toward suppliers that can prove supply chain control and documented strain performance. The functional side of the brewing yeast market is also gaining weight, because beta-glucans, nucleotides, and mannoproteins are being viewed as useful in-process contributors rather than only downstream additives. Lallemand Brewing’s portfolio expanded from 2 dry yeast strains in 2000 to 20 specialized strains by 2025, which shows how supplier development has followed demand for more targeted fermentation tools[1]Source: Lallemand Brewing, “Setting a New Standard in Yeast Performance,” Lallemand Brewing, lallemandbrewing.com. This pattern is strongest in North America, Australia, and premium craft segments in Europe, where brewers are more willing to pay for proof, consistency, and differentiation.

Expansion of craft beer and premium brewing output

The brewing yeast market continues to draw support from premium brewing even when craft beer volumes soften. United States craft beer production fell 5% in 2025 to 21.9 million barrels, but craft still held a 13.3% volume share and a 24.6% dollar share of total retail beer sales, which shows that value remained stronger than volume[2]Brewers Association, “A Year of Correction for Craft Beer, With Early Signals of Recovery,” Brewers Association, brewersassociation.org. That gap matters for the brewing yeast market because breweries that compete on taste, style, and identity usually spend more per batch on specialized strains. The lower brewery count in the United States also points to a more selective environment, where surviving operators need sharper product distinction to hold shelf space. In Europe, the independent brewing sector is expected to grow further through 2029, especially in premium and specialty styles. As craft expansion continues in the Asia-Pacific and South America, the brewing yeast market gains a longer runway for specialty dry strains and fresh liquid formats.

Craft breweries focus on flavor innovation and yeast-derived characteristics

Flavor development is a significant demand driver in the brewing yeast market. Craft brewers are increasingly utilizing yeast as a flavor-enhancing tool rather than solely as a fermentation agent. This shift is notable as biotransformation has transitioned from being a niche brewing technique to a practical method for creating tropical and citrus flavor notes without altering the overall process design. By leveraging biotransformation, brewers can achieve unique and complex flavor profiles that cater to evolving consumer preferences for innovative and diverse beer options. In November 2025, Fermentis introduced SafLager SH-45, a yeast strain designed to release free thiols from hop precursors, enabling lager brewers to achieve aroma profiles traditionally associated with ale formats. This development highlights the growing importance of yeast strain selection in tailoring beer characteristics to meet market demands. Such product innovations promote more frequent strain refresh cycles, driving recurring purchases in the brewing yeast market.

Adoption of genetically modified and functional yeast strains

The brewing yeast market is also shifting as engineered strains move closer to mainstream commercial use. In the United States, companies such as Berkeley Yeast and Omega Yeast have been able to commercialize genetically modified strains through the Food and Drug Administration's voluntary consultation route, especially for craft brewing applications focused on aroma expression and process efficiency. In the United Kingdom, Lallemand UK filed an application, GM/26/01, in March 2026, to market Sourvisiae for sour beer production, which marked an important step in the post-Brexit regulatory setting. White Labs has already commercialized its ModiGen D series to reduce diacetyl formation across repeated generations, showing that functional performance is now a live commercial selling point rather than only a research topic. These developments favor better-resourced participants in the brewing yeast market because they require strain development capability, compliance management, and sustained customer education.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices of molasses, barley, and other fermentation inputs | -0.8% | Global, with acute pressure in EU and North America | Short term (≤ 2 years) |

| High drying and energy costs in liquid-to-dry processing | -0.6% | EU, North America, and Australia | Medium term (2-4 years) |

| Pricing pressure from plant-based and synthetic protein alternatives | -0.5% | North America and EU premium segments | Medium term (2-4 years) |

| Regulatory friction on health claims and strain-specific labeling | -0.4% | EU core, with spillover to Asia Pacific regulatory systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile prices of molasses, barley, and other fermentation inputs

Input cost instability remains a real brake on the brewing yeast market. Molasses exposure affects direct yeast propagation economics, while barley volatility matters through the wider brewing system and through price transmission across the beer value chain. Academic work on Germany covering 2015 to 2024 found that malting barley prices were more sensitive to external shocks than hop prices and adjusted more slowly after disruption. That matters because long contract cycles can delay price recovery for suppliers in the brewing yeast market even when raw material pressure rises quickly. Smaller producers are more exposed because they often lack the scale, procurement tools, or hedging capacity available to global suppliers. Even if barley conditions improve in the near term, the brewing yeast market still faces margin risk whenever energy and crop shocks feed through the supply chain.

High drying and energy costs in liquid-to-dry processing

Energy intensity is another persistent restraint for the brewing yeast market. Converting liquid culture into a stable dry product requires controlled drying conditions, and that makes power and heat costs important to plant economics. The European energy shock of 2022 and 2023 showed how quickly fermentation and drying operations can face cost escalation when gas and electricity markets tighten. This is especially relevant because dry yeast held 68.4% of the brewing yeast market share in 2025, so a large part of the total supply depends on energy-heavy processing. Large integrated suppliers can spread this pressure across multiple plants and regions, but mid-tier regional manufacturers have less flexibility. The high capital cost of advanced drying systems also slows capacity expansion, which can leave the brewing yeast market exposed to tighter supply and less stable pricing during demand spikes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Dry Format's Logistics Advantage Sustains Volume Lead

Dry brewing yeast held 68.40% of the brewing yeast market share in 2025, which kept it as the lead format across large-scale brewing systems. The main advantage is not price alone, because extended shelf life and lower refrigeration dependence make dry yeast easier to move across national and regional supply networks. That is especially important in India, Southeast Asia, and Sub-Saharan Africa, where cold-chain depth still shapes how breweries manage input risk. Large industrial lager breweries also continue to favor dry yeast because it supports repeatable fermentation outcomes in standardized, high-throughput operations. In the brewing yeast industry, that combination of logistics and process stability keeps dry yeast closely aligned with the biggest production volumes.

Liquid brewing yeast is projected to expand at an 8.31% CAGR through 2031, which makes it the fastest-growing form segment in the brewing yeast market size mix. Growth is centered on breweries that value fresh culture performance, brand-specific flavor identity, and tighter control over fermentation expression. Craft brewers in North America and Western Europe often treat proprietary liquid strains as part of the beer’s signature, which reduces switching and helps suppliers defend premium pricing. Fermentis’ work on thiol-active strains also shows that liquid and specialty culture demand can rise when brewers want new aroma outcomes without reworking the whole brewhouse.

By Application: Lager's Industrial Scale Anchors the Market, Ale Accelerates on Craft Tailwinds

Lager accounted for 58.70% of the brewing yeast market size in 2025, which reflects the continued dominance of bottom-fermented beer in global production. Europe remains central to that position because brewing traditions in Germany, the Czech Republic, and Poland support steady yeast demand from established lager styles. China also remains important to the brewing yeast market because large-volume lager production still depends on proven strains that can deliver industrial consistency at scale. Premium lager innovation is now lifting value within this segment as brewers adopt strains that support more expressive aroma outcomes. The smaller group of other applications, including wheat beer, stout, and specialty formats, remains steady through premium brewing channels in countries such as Germany and Belgium.

Ale is forecast to grow at the fastest 9.50% CAGR through 2031, and this keeps it as the clearest growth application within the brewing yeast market. Craft brewing remains the main reason, because ale styles are still the natural base for experimentation, hop-forward recipes, and new brand launches. In the United States, craft beer production fell in 2025, but the segment still held a 24.6% dollar share and a 13.3% volume share of retail beer sales, which shows that value intensity remained strong. Ale is also where engineered and specialty strains can gain traction more quickly because brewers in this space are more willing to test differentiated biological tools.

Geography Analysis

Europe held 36.53% of the brewing yeast market share in 2025, which kept it as the largest regional base for demand. The region benefits from brewing traditions that support both large stable lager volumes and premium specialty production. The Czech Republic remained the world leader in per-capita beer consumption in 2024 at 148.8 liters per person, which shows how deeply beer remains embedded in regional demand patterns as reported by Kirin Holding[3]Source: Kirin Holdings Company Limited, “Global Beer Consumption by Country in 2024,” Kirin Holdings, kirinholdings.com. Germany continues to matter because purity-focused brewing practices support demand for reliable, certified yeast inputs. The United Kingdom also adds to the brewing yeast market through a craft revival, with beer consumption rising and supporting more interest in specialty strains.

Asia Pacific is forecast to grow at the fastest 11.11% CAGR through 2031, which makes it the main expansion engine for the brewing yeast market size outlook. India led regional momentum with 14.6% beer consumption growth in 2024, and Vietnam and Indonesia are also benefiting from urbanization and rising middle-class demand. This growth base supports dry yeast strongly because mainstream breweries in these markets still place a high value on transport ease and process stability. China remains a major part of regional demand even as its domestic beer market matures, because its brewing scale still drives large yeast procurement volumes. Japan and Australia contribute a different layer to the brewing yeast market through technically advanced craft brewing, where premium and specialty strains can gain traction faster than in volume-led systems.

North America shows a split pattern in the brewing yeast market, with softer beer volume but firmer value demand in premium brewing. With United States beer consumption declined, yet surviving breweries are leaning harder into differentiated products that require more strain selection and fermentation control. South America is becoming a useful secondary growth pocket, with Brazil and Mexico posting beer consumption gains in 2024. The Middle East and Africa remain smaller in value, but brewery investment and rising production volumes are gradually widening the addressable base for the brewing yeast market

Competitive Landscape

The brewing yeast market remains moderately concentrated, with Lesaffre, Lallemand, and Angel Yeast forming the most visible global supply anchors. Their position comes from integrated fermentation capabilities, wider plant networks, and deeper strain libraries that cover industrial and craft requirements. This leaves the brewing yeast market semi-consolidated rather than tightly closed, because regional specialists and niche laboratories still serve brewers who want closer technical support or unusual strain profiles. The largest suppliers are strongest where customers need quality assurance, steady volume fulfillment, and access to broader application knowledge. Smaller specialists remain relevant where brewers value responsiveness, collaboration, and culture customization over scale alone.

Lesaffre has made some of the clearest strategic moves in the brewing yeast market. In September 2024, it acquired Altar from Ginkgo Bioworks to strengthen adaptive laboratory evolution capability and speed up strain development. In 2025, it completed the acquisition of DSM-Firmenich’s yeast extract business, which widened its reach across yeast-derived ingredients. In June 2025, it also finalized a joint venture with Zilor and took a 70% stake in Biorigin, which strengthened its derivative capacity in food and animal nutrition. These steps show that leadership in the brewing yeast market is increasingly tied to control over the wider yeast lifecycle and not only to brewing input sales.

Lallemand has focused more on application science and partnership-led commercialization in the brewing yeast market. Its January 2025 partnership with EvodiaBio brought Yops yeast-derived aroma solutions to low- and no-alcohol beer producers, which linked strain innovation to a fast-developing beer niche. Its February 2026 Aurora trial with Uiltje Brewing showed a similar focus on biotransformation and practical craft brewery deployment. White Labs also keeps a place in the brewing yeast market through engineered ModiGen strains that address diacetyl control, which helps smaller specialists stay important in high-value niches. The competitive gap now appears widest in newer craft markets such as India, Brazil, and Southeast Asia, where technical service networks are still less developed than in Europe and North America.

Brewer's Yeast Industry Leaders

Lesaffre Group

Angel Yeast Co., Ltd

Lallemand Inc.

Associated British Foods plc

Leiber GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Lallemand launched the LalBrew Aurora partnership trial with Uiltje Brewing (Netherlands), showcasing the strain's biotransformation capabilities for IPA and hop-forward styles in a commercially active European craft brewery.

- November 2025: Lesaffre's subsidiary Fermentis launched SafLager SH-45 globally, a lager yeast strain engineered for exceptional thiol biotransformation, enabling tropical and citrus hop character in cold-fermented lagers with potential for reduced hop quantity per batch.

- June 2025: Lesaffre completed the formation of a joint venture with Zilor, acquiring a 70% controlling stake in Biorigin and its carbon-neutral production facility in Quatá, São Paulo, strengthening the group's yeast derivatives capacity for human food and animal nutrition globally.

Global Brewer's Yeast Market Report Scope

Brewers' yeast (Saccharomyces cerevisiae) is a microorganism employed in the brewing industry to ferment sugars present in wort into alcohol and carbon dioxide. It plays an integral role in defining the flavor, aroma, and overall characteristics of beer during fermentation. The brewer's yeast market is segmented into form, application, and geography. By form, the market is segmented into dry and liquid. By Application, the market is segmented into lager, ale, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Dry |

| Liquid |

| Ale |

| Lager |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Egypt | |

| Rest of Middle East and Africa |

| By Form | Dry | |

| Liquid | ||

| By Application | Ale | |

| Lager | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of brewing yeast worldwide?

The brewing yeast market stands at USD 1.44 billion in 2026 and is forecast to reach USD 2.07 billion by 2031 at a 7.5% CAGR.

Which form category leads current demand?

Dry yeast led with 68.4% share in 2025 because it offers longer shelf life, easier transport, and better suitability for large industrial brewing systems.

Which application is growing the fastest through 2031?

Ale is projected to expand at a 9.5% CAGR through 2031, supported by craft brewing growth and stronger use of differentiated strains.

Which region offers the strongest growth outlook?

Asia Pacific is forecast to grow at an 11.1% CAGR through 2031, led by strong beer demand growth in India and broader momentum in Southeast Asia.

Page last updated on: