Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

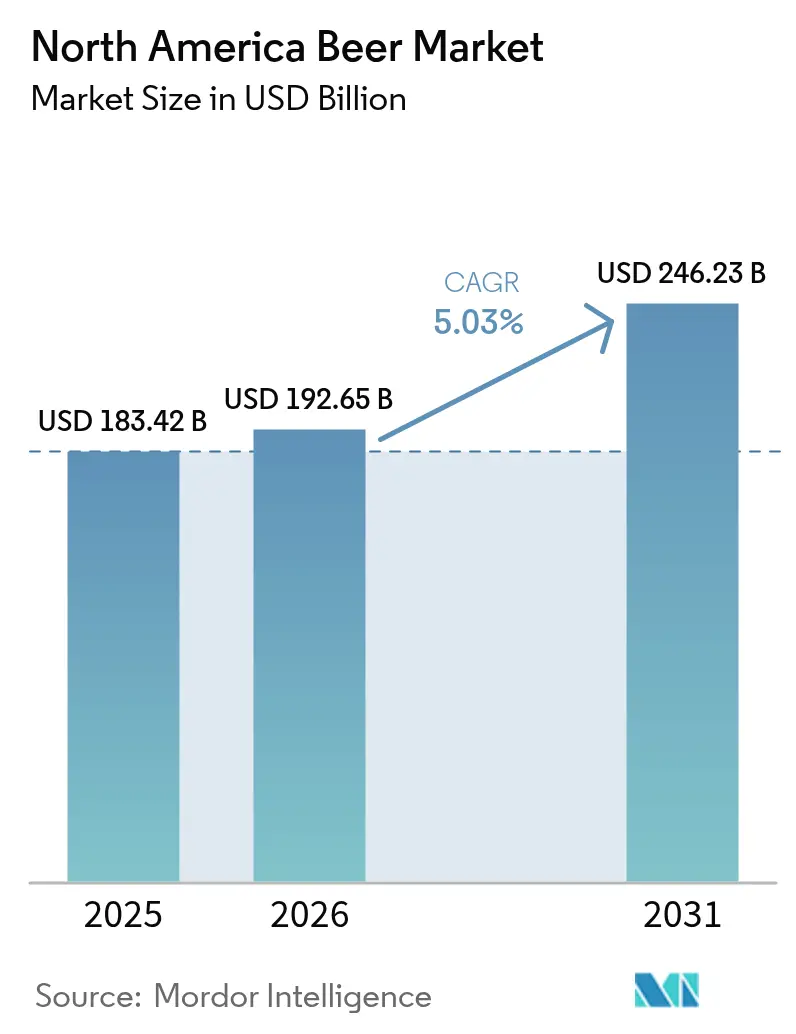

| Base Year Market Size (2025) | USD 183.42 Billion |

| Market Size (2026) | USD 192.65 Billion |

| Market Size (2031) | USD 246.23 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Beer Market Analysis by Mordor Intelligence

The North American beer market size is expected to grow from USD 183.42 billion in 2025 to USD 192.65 billion in 2026 and is forecast to reach USD 246.23 billion by 2031 at 5.03% CAGR over 2026-2031. Consumers are trading down in volume yet trading up in value as premium, low-alcohol, and non-alcoholic offerings build momentum. Craft brewers continue to influence flavor experimentation, while multinational groups accelerate portfolio rationalization to protect margins. E-commerce penetration deepens brand access, and investments in aluminum can infrastructure support sustainability targets. Upstream, shrinking barley acreage and water stress weigh on input costs, nudging brewers toward alternative grains and higher hedging activity.

Key Report Takeaways

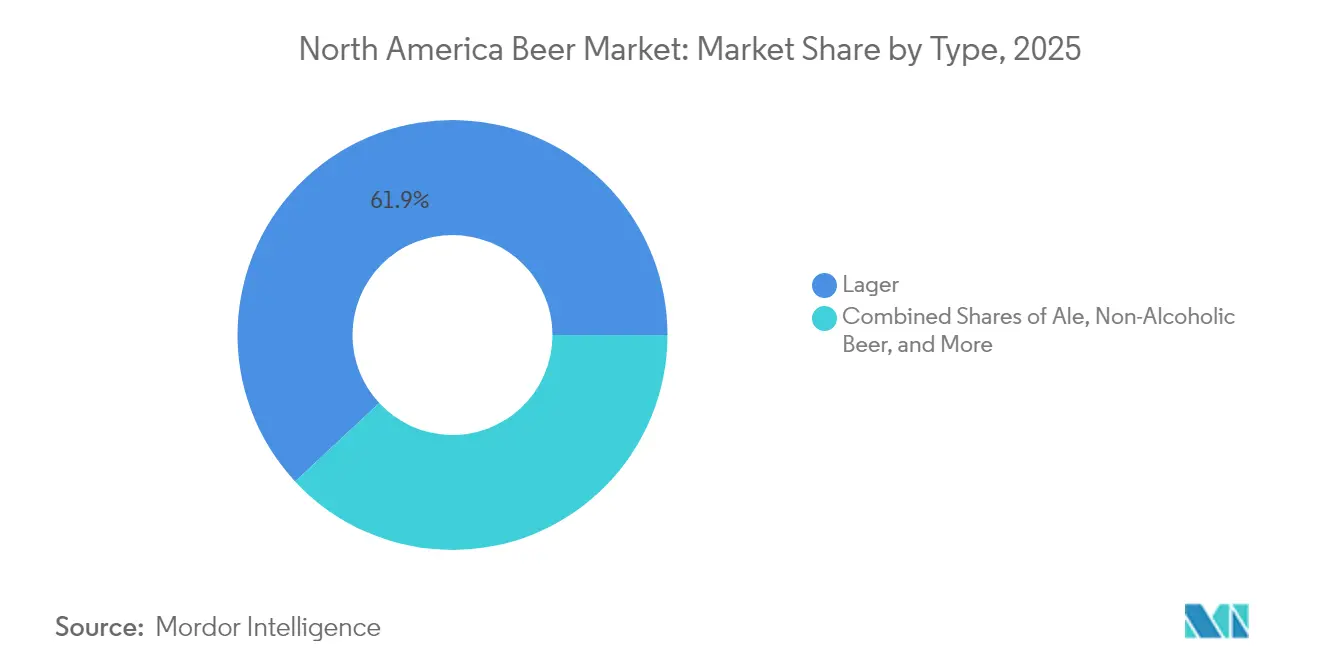

- By type, Lager led with 61.92% of the North American beer market share in 2025; Ale is projected to register a 6.08% CAGR through 2031.

- By category, Standard accounted for 56.15% of the North American beer market share in 2025, while Premium is set to expand at a 6.74% CAGR to 2031.

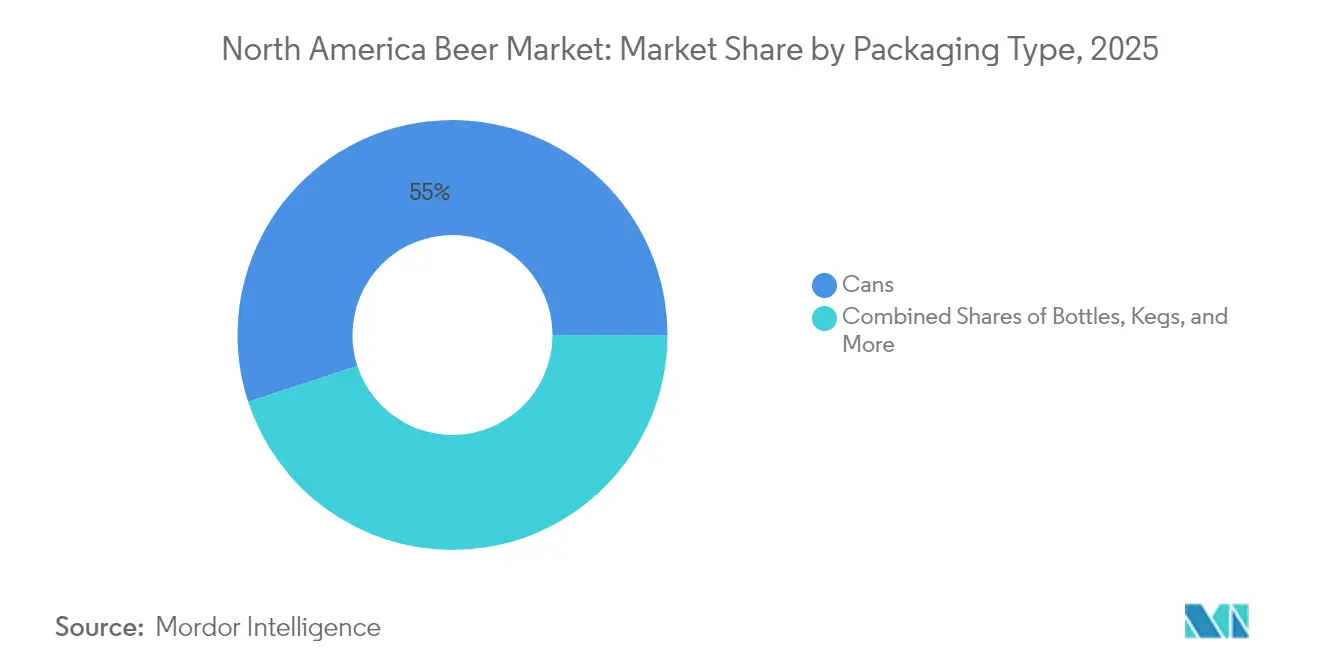

- By packaging, Cans commanded a 55.02% share in 2025 and are on track for a 6.37% CAGR, the highest across formats.

- By distribution, Off-Trade captured 71.55% sales in 2025; On-Trade is recovering fastest with a 6.86% CAGR forecast.

- By geography, the United States held 77.85% of the 2025 share, whereas Mexico is expected to grow at a 7.05% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Beer Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in craft beer segment | +0.8% | United States, Canada | Medium term (2-4 years) |

| Innovations in flavors and brewing techniques | +0.6% | North America | Medium term (2-4 years) |

| Expansion of low-alcohol and non-alcoholic beer | +1.2% | Global, strongest in North America | Long term (≥ 4 years) |

| Popularity of ready-to-drink (RTD) and flavored malt beverages | +0.9% | North America, Mexico | Short term (≤ 2 years) |

| Increasing E-commerce and direct-to-consumer sales | +0.7% | United States, Canada | Medium term (2-4 years) |

| Sustainability initiatives in packaging and brewing | +0.5% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Craft Beer Segment

In North America, the craft beer segment, while navigating a broader market contraction, is still at the forefront of innovation and premiumization, albeit at a more tempered pace than in years past. The industry witnessed a phase of rationalization, marked by 399 brewery closures juxtaposed with 335 new openings. This trend underscores a maturing market, emphasizing the imperative for operational efficiency amidst intensifying competition. In response, craft brewers are streamlining their portfolios, zeroing in on top-selling products, and diversifying into non-beer beverages, all to tap into a wider consumer appetite. This strategic shift not only elevates craft beer's status as a premium category, but also allows it to command superior margins, aligning with the changing consumer preference for quality over sheer volume.

Innovations in Flavors and Brewing Techniques

Technological advancements in hop extraction and flavor consistency are revolutionizing brewing capabilities by addressing persistent challenges related to ingredient variability and production efficiency. Abstrax Hops introduced Quantum Brite in February 2024, a water-soluble hop extract that eliminates the need for hop removal, reduces beer loss, and claims 100% utilization rates. Additionally, their Omni Hop Profiles utilize terpene-driven recreations to deliver consistent flavors year after year, regardless of harvest variability. These innovations allow brewers to achieve precise flavor profiles while cutting costs and minimizing waste, which is particularly beneficial given the ongoing volatility in hop prices. This technology enables smaller craft brewers to compete with larger operations by providing access to consistent, high-quality flavor compounds that were previously difficult to source or replicate. Advanced botanical analysis, which identifies over 500 compounds in hop profiles, creates opportunities for customization and flavor banking. This allows brewers to develop unique signature tastes, helping their products stand out in competitive market segments.

Expansion of Low-Alcohol and Non-Alcoholic Beer

In 2024, non-alcoholic beer became the fastest-growing segment in the beer category, achieving a year-over-year sales increase of approximately 30%. This growth was primarily driven by health-conscious consumers and the growing "sober-curious" movement, particularly among younger demographics. Over a 12-week period, Molson Coors' non-alcoholic brands recorded an impressive 89% growth. Notably, Blue Moon Non-Alcoholic entered the top 10 non-alcoholic brews by dollar share within its first year of launch. Advancements in brewing techniques have enabled the segment to closely replicate traditional beer flavors while retaining the social and cultural aspects of beer consumption. Major brewers are heavily investing in this expanding category. For example, Peroni Nastro Azzurro 0.0% achieved 83.5% dollar sales growth over a 52-week period, supported by lifestyle marketing efforts such as Formula 1 sponsorships. This growth aligns with a broader consumer trend toward mindful drinking, extending beyond traditional Dry January campaigns and driving consistent, year-round demand for premium non-alcoholic alternatives that sustain brand equity and profit margins.

Popularity of Ready-to-Drink (RTD) and Flavored Malt Beverages

RTD cocktails and flavored malt beverages are capturing market share from traditional beer by offering convenience, variety, and appeal to consumers seeking alternatives to standard beer profiles. The segment benefits from crossover appeal, attracting both beer drinkers seeking variety and spirits consumers preferring lower-alcohol options with consistent quality and portability. Anheuser-Busch's USD 16 million investment in its Los Angeles brewery specifically targeted expanded packaging capabilities for "beyond beer" brands including Cutwater and NÜTRL, demonstrating major brewers' commitment to diversifying their portfolios. The category's growth is supported by improved distribution networks and retail placement, with RTD products increasingly positioned alongside traditional beer rather than in separate spirits sections. Innovation in flavor profiles, packaging formats, and alcohol content optimization creates opportunities for premium pricing while addressing consumer demand for authentic cocktail experiences in convenient formats.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent and complex regulatory/tax environment | -0.9% | North America, strongest in Canada | Short term (≤ 2 years) |

| Rising Consumption of Alternative Beverages | -1.4% | United States, Canada | Medium term (2-4 years) |

| Trade barriers and cross-border tariffs | -0.6% | US-Mexico, US-Canada borders | Short term (≤ 2 years) |

| Barley Yield Volatility due to Water Scarcity | -0.8% | US Plains states, Western Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent and Complex Regulatory/Tax Environment

Beer producers in North America face increasing tax burdens and regulatory complexities. In April 2024, Canada introduced a 4.7% federal beer tax hike, marking the largest increase in nearly 40 years. Beer Canada[1]Beer Canada, “4.7% Federal Beer Tax Hike,” beer-canada.prowly.com estimates this tax hike will cost taxpayers approximately CAD 40 million during the 2025-26 fiscal year. Currently, taxes make up about 46% of retail beer prices in Canada. The regulatory landscape is further complicated by proposed federal labeling mandates, such as TTB's[2]TTB, "Beer - Notices of Proposed Rulemaking", www.ttb.gov"Alcohol Facts" requirements, which mandate per-serving disclosures of alcohol content, calories, and nutrients. With a five-year compliance period, these mandates impose significant costs for label redesign and supply chain adjustments. Additionally, state-level variations in distribution rules, licensing, and packaging regulations add another layer of complexity. Producers must navigate multiple compliance frameworks, increasing operational costs and restricting market access. These combined regulatory pressures limit pricing flexibility and reduce profitability, particularly for smaller craft brewers who lack the scale to efficiently manage these challenges.

Rising Consumption of Alternative Beverages

Consumer preferences are shifting significantly, posing a structural threat to the traditional beer market. Younger demographics, especially Gen Z and millennials, are leading this shift, favoring hard seltzers, non-alcoholic formats, and other alternative alcoholic and non-alcoholic beverages. According to the International Bottled Water Association[3]International Bottled Water Association, "Consumption share of beverages in the United States", www.bottledwater.org data from 2024, 20.31% of people consumed soft drinks in the United States. These groups are increasingly drawn to "sober-curious" trends, opting for drinks they view as healthier, more convenient, or simply more varied. This trend isn't just about consumers swapping one drink for another. Many of these alternative beverages are sidestepping the usual beer distribution channels and retail partnerships, presenting challenges for established beer supply chains. Furthermore, while traditional brewing relies on malt barley, many of these new beverages are turning to fermented sugar. This shift not only changes the demand for raw materials but also threatens the economic viability of traditional brewing, exerting long-term pressures on the entire beer ecosystem.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Lager Dominance Faces Ale Innovation

In 2025, Lager holds a commanding 61.92% market share, while Ale, growing at a 6.08% CAGR through 2031, stands out as the fastest-growing type. This trend highlights increasing consumer interest in complex flavor profiles and the appeal of craft brewing. The Lager segment thrives on established consumer preferences, efficient production methods, and strong brand recognition driven by major brewers. In contrast, Ale's growth is propelled by the expansion of craft breweries and premiumization trends, which yield higher margins. Stout and Porter cater to niche markets with loyal consumers, benefiting from seasonal demand and food pairing opportunities. Pilsner, with its crisp and accessible flavor, continues to attract both traditional and emerging consumer groups, ensuring stable performance.

Non-Alcoholic Beer emerges as the most dynamic growth segment, leveraging advanced brewing techniques to closely replicate traditional beer characteristics while addressing the needs of health-conscious consumers. New Holland Brewing's collaboration with Dungeons & Dragons to launch limited-edition Dragon's Milk products illustrates how traditional beer types can evolve through strategic partnerships and premium positioning. The 'Others' category includes hybrid products and experimental styles that blur traditional boundaries, creating opportunities for differentiation and premium pricing. Innovations such as Abstrax Hops' Quantum Brite system in hop extraction are transforming the industry by delivering consistent flavor across beer types, reducing production costs, and minimizing waste, thereby supporting both traditional and innovative brewing approaches.

By Category: Premium Acceleration Amid Standard Stability

In 2025, Standard beer holds a 56.15% market share, ensuring stable volumes and offering affordable price points that attract a broad consumer base. Meanwhile, the Premium segment is experiencing strong growth, with a 6.74% CAGR. This growth is driven by consumers' willingness to pay more for perceived quality, distinctive flavors, and engaging brand experiences. The Premium segment's expansion is further supported by the influence of craft brewing, the prestige associated with imported beers, and the appeal of limited-edition releases, which cater to consumers seeking unique and exclusive products. In contrast, the Standard category remains the market's cornerstone, consistently providing quality and value that appeal to cost-conscious consumers and those seeking high-volume consumption.

The Premium segment's growth is driven by a strategic emphasis on high-quality ingredients, artisanal production methods, and compelling brand storytelling that justifies premium pricing. Tilray's acquisition of craft breweries from Molson Coors highlights this focus on premium positioning, with the company aiming to rise from the ninth to the fifth-largest craft beer player in the U.S., prioritizing revenue growth over volume expansion. The distinction between categories is becoming increasingly blurred: Standard brands are introducing premium extensions, while Premium brands are offering more accessible options, creating a dynamic and fluid competitive landscape. Digital marketing and direct-to-consumer channels are particularly advantageous for the Premium segment, enabling targeted messaging and fostering relationships that enhance margins and build brand loyalty.

By Packaging Type: Cans Lead Innovation and Sustainability

In 2025, cans hold a leading 55.02% market share and are expected to grow at a 6.37% CAGR through 2031. This growth is driven by their sustainability benefits, consumer convenience, and superior ability to protect beer quality throughout the supply chain. Aluminum cans, with their infinite recyclability, outperform glass bottles not only in recyclability but also in shielding beer from light and oxygen, which can degrade quality. On the other hand, bottles maintain a significant market presence due to their premium positioning and traditional consumer appeal. This is particularly evident in on-premise settings, where glass packaging is associated with quality and authenticity.

Kegs serve the on-premise sector efficiently, especially in high-volume venues. However, they face challenges from the increasing adoption of canned beer in bars and restaurants, which prioritize operational flexibility and waste reduction. Reflecting this shift, Molson Coors has committed USD 85 million to eliminate plastic six-pack rings from its North American brands by the end of 2025. This initiative highlights how packaging innovation can drive both sustainability and competitive advantage, particularly for Coors Light. The 'Others' category is expanding, including emerging packaging formats such as larger cans and innovative closures. These formats enhance the consumer experience while ensuring product integrity. Supporting this evolution, Sidel has introduced its EvoFILL Can Compact technology, capable of processing up to 40,000 cans per hour with a filling accuracy of ±1 ml, demonstrating how advancements in packaging equipment contribute to market growth and operational efficiency.

By Distribution Channels: Off-Trade Dominance with On-Trade Recovery

In 2025, Off-Trade channels hold a dominant 71.55% market share, highlighting a consumer preference for home consumption, competitive pricing, and convenient shopping — trends that emerged during the pandemic and have continued amid economic uncertainties. Within the Off-Trade segment, Specialty/Liquor Stores provide curated selections and expert advice, particularly benefiting the craft and premium beer categories. On the other hand, Other Off-Trade Channels, such as grocery and convenience stores, offer extensive market reach and encourage impulse purchases. The dominance of Off-Trade is further reinforced by the growth of e-commerce, exemplified by AB InBev's BEES platform, which processed 20 million orders in Q3 2024, generating a gross merchandising value of over USD 5.5 billion, as reported by Consumer Goods Technology.

On-Trade channels, meanwhile, are growing at a faster rate, with a projected CAGR of 6.86% through 2031. This growth is driven by the recovery of the hospitality sector, premiumization trends favoring on-premise consumption, and experiential dining that emphasizes beer pairings and exploration. The On-Trade channel benefits from higher profit margins, opportunities for brand building, and consumers' willingness to pay premium prices for curated experiences and social interactions. For instance, Redhook Brewery's partnership with the University of Washington's NIL collective to launch Montlake Gameday Gold Lager illustrates how On-Trade strategies can foster community connections and brand loyalty, extending beyond traditional retail relationships, as noted by Tilray Brands. Additionally, digital integration is increasingly blurring the lines between channels; tools like QR codes and mobile ordering enable seamless transitions from on-premise discovery to off-premise purchases, creating omnichannel experiences that enhance consumer engagement and boost sales conversions.

Geography Analysis

The United States maintains overwhelming market dominance with 77.85% share in 2025, supported by extensive distribution infrastructure, diverse consumer preferences, and established brewing capacity, yet faces structural challenges from declining beer consumption and increasing competition from alternative beverages. Mexico emerges as the fastest-growing geography at 7.05% CAGR through 2031, driven by Grupo Modelo's USD 3.6 billion investment program for 2025-2027 that focuses on brewery modernization, circular economy initiatives, and expanded production capacity.

The Mexican market benefits from beer's position as the country's largest agro-food export at USD 6.163 billion in 2023, with Grupo Modelo representing approximately 1% of Mexico's GDP, demonstrating the industry's economic significance and growth potential. Canada provides market stability through established brewing traditions and regulatory frameworks, while facing headwinds from significant tax increases and trade tensions that could affect cross-border beer flows. The 4.7% federal beer tax increase in April 2024 represents the largest single federal alcohol tax hike in approximately 40 years, creating cost pressures that may constrain consumption growth.

Rest of North America encompasses smaller markets that benefit from regional preferences and niche positioning, though their limited scale restricts their impact on overall market dynamics. Trade relationships across North American borders face potential disruption from proposed tariffs, with industry stakeholders warning that 25% tariffs on Mexican and Canadian imports could substantially raise consumer prices and trigger retaliatory measures that would harm the entire regional beer ecosystem.

Competitive Landscape

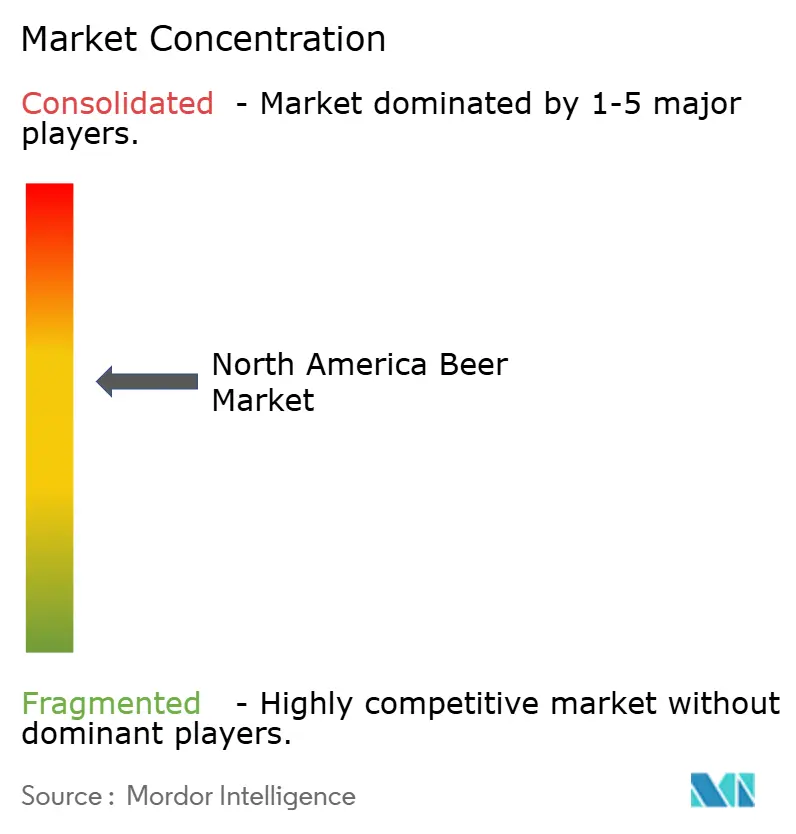

The North American beer Market exhibits moderate concentration with a market intensity, indicating significant consolidation opportunities remain as major players pursue portfolio optimization and operational efficiency gains. Strategic realignments accelerated through 2024-2025, with notable transactions including Tilray's acquisition of four craft breweries from Molson Coors, AB InBev's new contract brewing agreement with Pabst, and multiple regional craft brewery partnerships that demonstrate industry efforts to balance scale advantages with local market expertise.

Competition increasingly centers on premiumization strategies, sustainability initiatives, and digital transformation capabilities that enable direct consumer relationships and operational efficiency. Technology adoption emerges as a critical competitive differentiator, with AB InBev's BEES platform achieving over 90% revenue penetration in select markets and generating over USD 5.5 billion in quarterly gross merchandising value, while packaging innovations like Four Peaks Brewing's adoption of CIRT recycling technology create consumer engagement opportunities and environmental benefits.

White-space opportunities exist in non-alcoholic beer segments, direct-to-consumer channels, and cross-category products that blur traditional beverage boundaries. Emerging disruptors leverage specialized positioning, community connections, and agile operations to compete effectively against larger incumbents, while established players respond through acquisition strategies and innovation investments that maintain market position while accessing new growth vectors.

North America Beer Industry Leaders

-

Constellation Brands

-

Anheuser-Busch InBev

-

Boston Beer Company

-

Heineken NV

-

Carlsberg Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: BrewDog USA launched its newest Headliner beer, BrewDog IPA. It balances bright tropical and citrus notes with subtle pine and a clean, mellow bitterness, dry-hopped with Chinook and Citra hops.

- July 2025: Wrexham Lager Beer Co Ltd, the oldest lager brand in the United Kingdom, launched in Canada, in partnership with British Columbia Liquor Store (BCLS) and Liquor Control Board of Ontario (LCBO). The products are available through various retailers.

- May 2025: US Brewery launched a 100% quinoa beer. The beer is vegan and gluten-free. The beer has a refreshing, bright taste with a hint of sweetness, and is a good alternative to both traditional craft beers and white wine.

- May 2024: The Boston Beer Company announced the launch of its newest creation: Samuel Adams American Light. This distinctly American light craft lager featured a crisp and refreshing taste, making it an ideal choice for everyday drinking occasions.

North America Beer Market Report Scope

Beer is a fermented beverage made up of grains such as malt, water, hops, and yeast. It is one of the oldest and most commonly consumed alcoholic drinks around the globe. The North American beer market is segmented by type, distribution channel, and country. By type, The North America Beer market is segmented into Lager, Ale, and Others. By distribution channel, the market is segmented into On-Trade and Off-Trade channels. By country, the market is studied in the United States, Canada, Mexico, and the rest of North America. For each segment, the market sizing and forecasts have been done based on value (in USD Million).

By Type

| Lager |

| Ale |

| Non-Alcoholic Beer |

| Others |

By Category

| Standard |

| Premium |

By Packaging Type

| Cans |

| Bottles |

| Kegs |

| Others |

By Distribution Channels

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Other Off-Trade Channels |

Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Type | Lager | |

| Ale | ||

| Non-Alcoholic Beer | ||

| Others | ||

| By Category | Standard | |

| Premium | ||

| By Packaging Type | Cans | |

| Bottles | ||

| Kegs | ||

| Others | ||

| By Distribution Channels | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Other Off-Trade Channels | ||

| Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

What is the current value of the North America beer market?

The market is valued at USD 192.65 billion in 2026.

How fast is premium beer growing within North America?

Premium category revenue is projected to climb at a 6.74% CAGR through 2031.

Which packaging format is expanding quickest?

Aluminum cans are forecast for a 6.37% CAGR, backed by sustainability and convenience benefits.

How are brewers addressing carbon reduction?

Strategies include CO₂ capture, aluminum recycling, and elimination of plastic six-pack rings.

Page last updated on: