Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

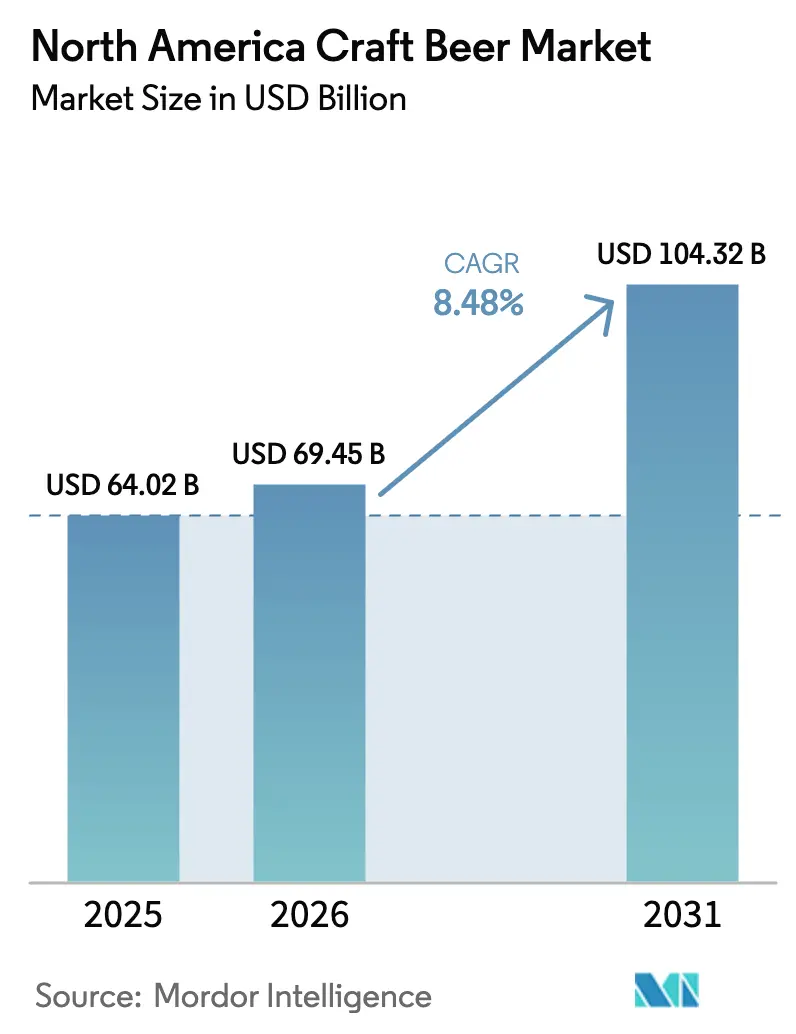

| Base Year Market Size (2025) | USD 64.02 Billion |

| Market Size (2026) | USD 69.45 Billion |

| Market Size (2031) | USD 104.32 Billion |

| Growth Rate (2026 - 2031) | 8.48% CAGR |

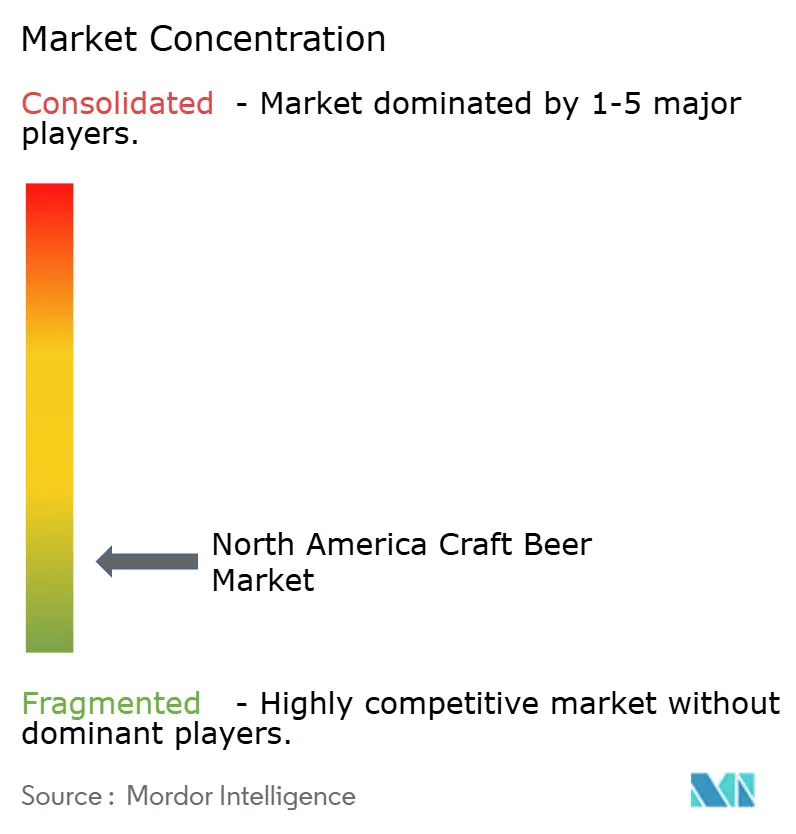

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Craft Beer Market Analysis by Mordor Intelligence

The North America craft beer market size was valued at USD 64.02 billion in 2025 and estimated to grow from USD 69.45 billion in 2026 to reach USD 104.32 billion by 2031, at a CAGR of 8.48% during the forecast period (2026-2031). Driven by heightened consumer awareness, the market is witnessing an expansion, with a pronounced tilt towards flavorful, low-alcohol options. While health-conscious consumption patterns and regulatory restrictions pose challenges, the demand for unique flavors, bolstered by continuous product innovation and rising spending power, fuels the market's growth. This trajectory underscores the market's resilience and its premium positioning within the broader beer industry. North America's craft beer market is in flux, adapting to diversifying consumer preferences in styles, packaging, and purchasing channels. Ale remains the dominant style, while lagers are growing rapidly. While the market is predominantly male, a notable increase in female consumption suggests untapped expansion potential. Although cans dominate packaging due to their convenience and portability, there's a notable surge in variety packs and alternative formats, reflecting consumers' desire for curated experiences. The craft beer scene in the region boasts a rich tapestry of microbreweries and brewpubs, each showcasing unique local flavors and brewing techniques.

Key Report Takeaways

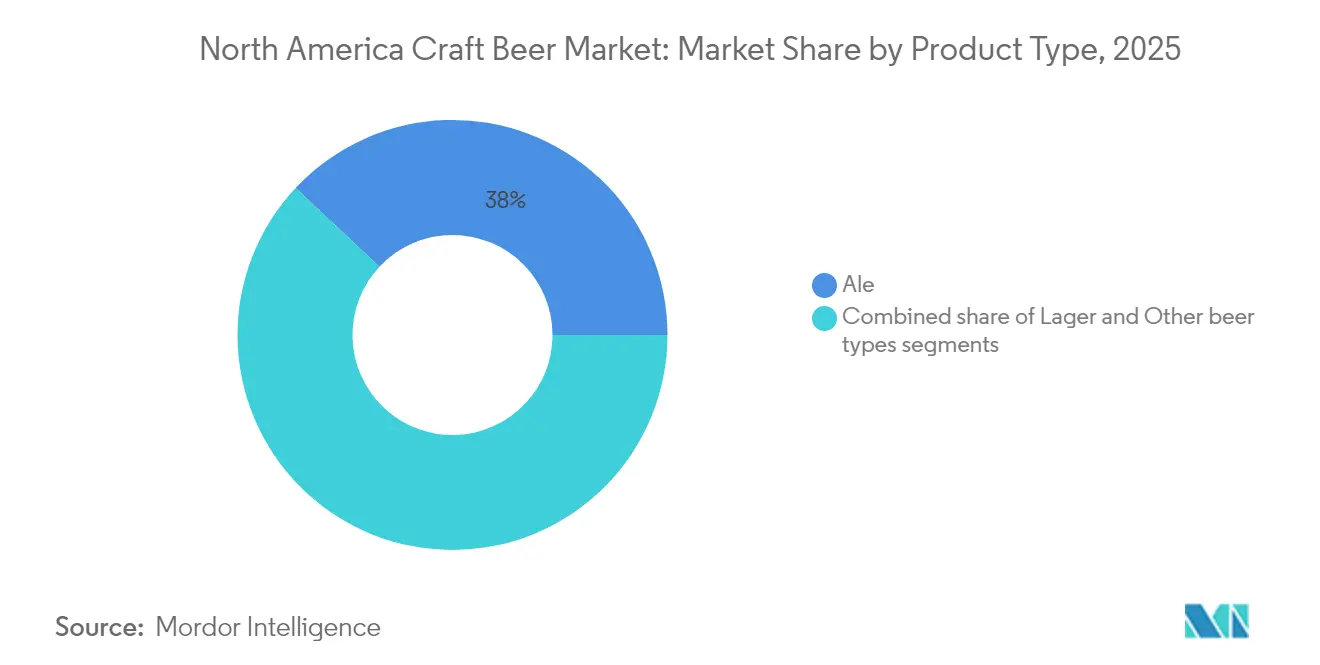

- By product type, ale held 38.02% of the North America craft beer market share in 2025, while lager types are projected to post the fastest 12.37% CAGR for 2026-2031.

- By end user, men dominated consumption with 68.75% share of the market size in 2025, whereas the women’s segment is tracking a 12.58% CAGR for 2026-2031.

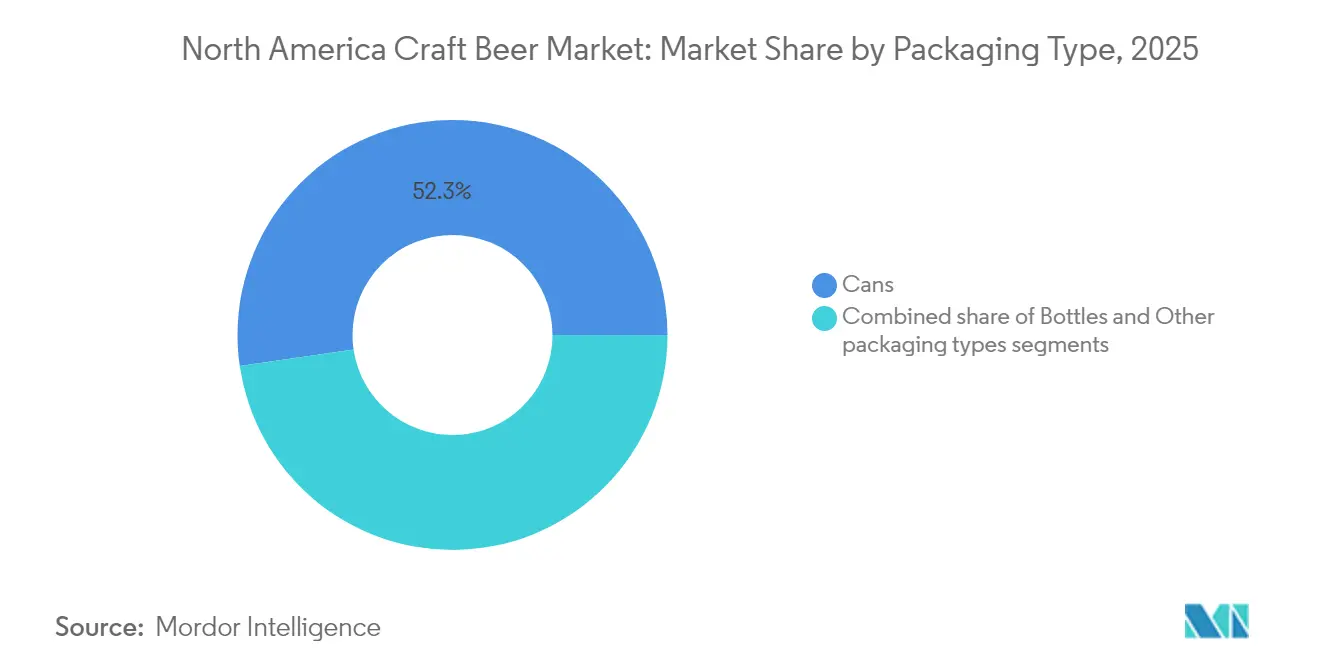

- By packaging, cans captured a dominant 52.31% share of North America's craft beer market in 2025, with a robust growth rate of 12.79% CAGR for 2026-2031.

- By distribution channel, on-trade venues led with 53.74% revenue share in 2025, while off-trade sales via retail and e-commerce are advancing at a 12.86% CAGR for 2026-2031.

- By geography, the United States accounted for 87.11% of North America's craft beer market size in 2025, whereas Mexico is the fastest-growing national market with a 13.19% CAGR for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Craft Beer Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising number of microbreweries due to strong demand | +2.1% | North America, with early gains in California, Texas, North Carolina | Medium term (2-4 years) |

| Product differentiation in terms of ingredients, flavors, and alcohol content | +1.8% | North America core markets, spill-over to Mexico | Long term (≥ 4 years) |

| Rising disposable income and willingness to pay premium prices for high-quality, artisanal beverages | +1.5% | North America urban centers, expanding to Canada and Mexico | Medium term (2-4 years) |

| Growing beer tourism and brewery experiences attracting domestic and international visitors | +1.2% | North America, with early gains in Portland, Asheville, Burlington | Long term (≥ 4 years) |

| Surge in demand for low alcohol beverages | +0.9% | North America, led by U.S. and Canada | Short term (≤ 2 years) |

| Technological advancement in terms of production | +0.7% | North America, particularly U.S. and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Number of Microbreweries Due to Strong Demand

The proliferation of microbreweries across North America demonstrates a significant shift in consumer preferences toward locally produced, authentic craft beer experiences. These establishments effectively capitalize on their local presence by fostering strong community relationships and minimizing distribution expenses through shorter supply chains. According to the Brewers Association, the United States recorded 9,796 operational craft breweries in 2024, comprising 2,029 microbreweries and 279 regional craft breweries [1]Source: Brewers Association, “Brewers Association Reports 2024 U.S. Craft Brewing Industry Figures,” brewersassociation.org. The growth of these establishments is supported by reduced regulatory requirements and the increasing mainstream acceptance of craft beer as a premium beverage choice across various age groups and consumer segments. The microbrewery expansion trend continues to shape the North American craft beer market, supported by consumers seeking unique, locally produced beverages and a regulatory environment that enables new market entrants to establish and operate brewing facilities. The emergence of microbreweries has also encouraged innovation in brewing techniques and flavor profiles, leading to a diverse range of craft beer offerings that cater to evolving consumer tastes.

Product Differentiation in Terms of Ingredients, Flavors, and Alcohol Content

Innovation in craft beer ingredients and flavor profiles remains a significant market driver in North America, as breweries strive to establish competitive differentiation through ongoing experimentation and innovation. The development of unique taste experiences enables craft brewers to capture and retain consumer interest in an increasingly competitive market. Breweries actively invest in research and development to create distinctive flavor combinations using specialized ingredients, helping them maintain their market position and meet evolving consumer demands. The industry's emphasis on product differentiation extends beyond traditional brewing methods to incorporate novel ingredients and brewing techniques. For instance, Lallemand Brewing's introduction of Aurora Northern IPA Yeast in April 2025 exemplifies this trend, combining the drinkability of West Coast IPAs with enhanced yeast aromatics. This innovation exemplifies how ingredient development directly addresses consumer preferences for balanced, flavorful options. These strategic ingredients and flavor innovations align with current consumer trends toward moderation and unique sensory experiences.

Rising Disposable Income and Willingness to Pay Premium Prices for High-Quality, Artisanal Beverages

Consumer disposable income in North America continues to rise, as demonstrated by the U.S. Bureau of Economic Analysis data, which reported personal income growth of USD 210.1 billion (a 0.8% monthly rate) and a personal consumption expenditures (PCE) increase of USD 47.8 billion (0.2%) in April 2025 [2]Source: U.S. Bureau of Economic Analysis, “Personal Income and Outlays, April 2025,” bea.gov. This upward trend in disposable income has a significant influence on the craft beer market dynamics, as consumers exhibit greater financial flexibility to explore premium beverage options. The increased purchasing power enables consumers to allocate more spending toward craft beer products, despite their higher price points compared to traditional mass-produced beers. Additionally, this economic environment aligns with shifting consumer preferences toward artisanal and locally produced beverages, where buyers prioritize unique flavor profiles, innovative brewing methods, and authentic craft experiences. The craft beer industry benefits from consumers' willingness to invest in quality and variety, supporting the market's growth through increased experimentation with different breweries, styles, and limited-edition releases.

Growing Beer Tourism and Brewery Experiences Attracting Domestic and International Visitors

Beer tourism continues to emerge as a significant economic driver in North America's craft beer market, with craft breweries functioning as destination attractions that combine production education, tasting experiences, and local cultural immersion. According to the Canadian Craft Brewers Association, Canadian craft breweries alone support up to 8,000 tourism jobs while generating economic benefits in underserved communities [3]Source: Canadian Craft Brewers Association, “Pre-Budget Consultation in Advance of the 2025 Budget,” ccba-ambc.org. The integration of breweries into local tourism circuits has created additional revenue streams for both urban and rural regions, contributing to regional economic development and job creation. Beer tourism has evolved beyond traditional brewery visits, with establishments now offering comprehensive experiences that include guided production tours, expert-led tastings, food pairing events, and seasonal festivals. These experiential offerings extend visitor engagement beyond conventional tasting rooms, creating sustainable revenue streams that complement core beer sales. The tourism-focused approach enables craft breweries to build stronger brand loyalty while fostering deeper connections with their local communities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent government regulations | -1.4% | North America, particularly affecting U.S.-Canada-Mexico cross-border trade | Long term (≥ 4 years) |

| Consumer's inclination toward no/low alcohol products | -1.0% | North America, with strongest impact in U.S. and Canada urban centers | Medium term (2-4 years) |

| Raw material cost inflation and supply chain challenges impact beer production | -1.1% | North America, with spillover effects from U.S. to Canada and Mexico | Short term (≤ 2 years) |

| Religious and cultural constraints affecting beer market growth | -0.8% | North America, particularly affecting Mexico and conservative U.S. markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Government Regulations

Regulatory complexity in the North American craft beer market continues to escalate, primarily due to the implementation of new U.S. tariffs that impose a 25% duty on imports from Canada and Mexico. These tariffs particularly affect aluminum packaging materials, which are essential for craft beer canning operations. The trade tensions have further intensified with Canada's retaliatory measures, including 25% counter-tariffs on USD 30 billion worth of U.S. goods. This bilateral trade friction, combined with varying state-level regulatory requirements, creates substantial operational and compliance challenges for craft breweries operating across multiple jurisdictions. The impact of these regulatory hurdles extends to tax revenue, with the Federation of Tax Administrators projecting potential losses of USD 5 billion in alcohol tax revenue due to market disruptions [4]Source: Federation of Tax Administrators, “The Barrel – January 2025,” taxadmin.org . The intricate web of federal, state, and international regulations, coupled with trade barriers, creates a challenging business environment that significantly constrains the growth potential of the North American craft beer market.

Raw Material Cost Inflation and Supply Chain Challenges Impact Beer Production

Raw material costs have emerged as a significant constraint in the North American craft beer market, with substantial increases in the prices of essential ingredients such as malted barley and hops, alongside packaging materials like aluminum cans. The impact of these cost increases has been particularly severe on production economics, forcing breweries to revise their pricing strategies and operational models. Supply chain complications, characterized by persistent fluctuations in commodity prices and logistical bottlenecks, have resulted in extended procurement timelines for essential brewing ingredients and packaging materials. These operational hurdles have compelled craft breweries to implement several adaptive measures, including adjustments to production schedules, price adjustments, and maintaining larger inventory reserves. The market has experienced a notable trend toward consolidation, with smaller craft breweries facing difficulties in absorbing escalating costs. Meanwhile, larger craft beer producers have maintained their competitive edge through economies of scale and investments in technological infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ale Dominance Meets Innovation Surge

Ale beer dominates the market, accounting for a 38.02% share in 2025, driven by consumer preference for hop-forward flavor profiles and traditional brewing methods. The category's strength stems from the continued popularity of IPAs and the established brewing expertise across North America's craft brewery network, where traditional styles experience a resurgence alongside modern interpretations. Regional craft breweries consistently expand their ale portfolios to include session ales, barrel-aged varieties, and small-batch experimental releases. The robust distribution networks across major metropolitan areas facilitate wider access to craft ales, while taproom culture continues to foster direct consumer engagement. Local ingredients and terroir-driven brewing approaches further differentiate North American ales in the craft beer landscape.

Lager is the fastest-growing category, expanding at a 12.37% CAGR driven by a resurgence in the popularity of clean, crisp beer styles and advancements in production techniques. Craft brewers, leveraging technological innovations such as temperature-controlled fermentation, are not only achieving the refined quality synonymous with traditional lagers but also preserving the authenticity of small-batch production. This segment is further bolstered by a growing demand for low- and no-alcohol variants, reflecting the broader trend of health-conscious consumption. Moreover, partnerships between American and Mexican brewers have birthed a wave of hybrid styles, broadening the category's appeal. The rising trend of fruit-infused lagers, coupled with contemporary takes on European classics, underscores the category's momentum in North America's dynamic craft beer scene.

By End User: Male Loyalty Versus Female Expansion

Men account for 68.75% of craft beer consumption in 2025, maintaining their traditional demographic dominance through established preferences for hop-forward ales and brewery experiences. However, the women's segment demonstrates significant growth with a 12.58% CAGR, driven by industry inclusivity initiatives and product diversification efforts across the market. The North American craft beer landscape continues to evolve, with male consumers showing strong brand loyalty and preference for higher ABV offerings. Regional breweries report that male consumers frequently participate in beer festivals and taproom events, contributing to sustained market engagement.

Companies like Talea Beer Co. are implementing gender-inclusive approaches through targeted product development and marketing that emphasize community building over traditional masculine imagery. This shift reflects broader cultural changes toward inclusive consumption experiences, with craft breweries leveraging storytelling and authenticity to connect with expanding consumer bases while maintaining their core customer relationships. North American breweries are increasingly hosting women-focused tasting events and educational sessions to foster market growth. Many craft breweries have expanded their product portfolios to include fruit-forward beers and lower-alcohol options that appeal to diverse taste preferences.

By Packaging: Can Innovation Drives Sustainability

In 2025, cans command a dominant 52.31% share of the craft beer packaging market, with projections indicating a robust 12.79% CAGR. This surge is largely attributed to a growing preference for sustainability, the convenience of cans, and their superior ability to protect products compared to traditional glass. Notably, younger, environmentally conscious consumers are increasingly embracing cans. This shift has prompted North American craft breweries, especially smaller ones, to pivot from bottles to cans, investing heavily in canning lines. Aluminum cans offer advantages such as lightweight transport, reduced carbon emissions, and enhanced protection from light and oxygen, ensuring product quality during storage and distribution.

Eco-friendly innovations and advanced packaging technologies bolster this upward trajectory. Breweries are delving into biodegradable materials and recyclable options. Moreover, digital printing on cans facilitates flexible designs, catering to small-batch and seasonal demands. The trend of variety packs resonates with consumer curiosity and trial behavior, while premium packaging enhancements cater to the growing demand for distinctive unboxing experiences. Although glass bottles maintain a foothold in premium and gift-oriented markets, cans are undeniably reshaping the landscape, championing versatility and aligning seamlessly with sustainability-focused consumer values.

By Distribution Channel: On-Trade Resilience Meets Off-Trade Acceleration

On-trade channels dominate the craft beer market, accounting for a 53.74% share in 2025, primarily driven by taprooms that serve as essential revenue generators for craft breweries. These establishments offer higher margins, direct consumer relationships, and product education opportunities that enhance brand differentiation. The segment's growth is further supported by beer tourism, with breweries creating destination experiences through guided tours, food pairings, and seasonal events that extend beyond traditional tasting room offerings. Local festivals and craft beer-focused events contribute significantly to on-trade sales, providing platforms for breweries to showcase new products and connect with enthusiasts.

Off-trade channels are experiencing rapid growth at a 12.86% CAGR, fueled by e-commerce adoption and sustained home consumption trends. This expansion is supported by improved packaging technologies and digital platforms, which enable direct-to-consumer sales where permitted. The market is evolving toward hybrid distribution models, where breweries leverage both channels synergistically, using taproom experiences for brand building while capturing retail sales through partnerships. The integration of technology, including mobile ordering, subscription services, and virtual tasting experiences, creates an omnichannel approach that maximizes consumer engagement across North America's craft beer ecosystem. Specialty bottle shops and craft-focused retail stores have emerged as important off-trade venues, offering curated selections and expert recommendations to consumers.

Geography Analysis

The United States holds a commanding 87.11% market share in the North American craft beer market in 2025, supported by its established craft brewing infrastructure. The Northeast and Mountain West regions exhibit high craft beer density, driven by tourism and lifestyle preferences, while regional variations reflect distinct local preferences and regulatory frameworks. The proliferation of microbreweries and brewpubs across urban centers continues to strengthen the market position. Consumer demand for unique, locally produced beverages and the integration of taproom experiences into community spaces further solidifies the U.S. market dominance.

Mexico presents significant growth potential with a projected CAGR of 13.19% during 2026-2031, driven by the expansion of independent breweries. The country benefits from USMCA trade agreements and its proximity to U.S. markets, while increasing disposable income among urban consumers fuels domestic demand for artisanal beverages. The emergence of craft brewing clusters in major metropolitan areas, particularly Mexico City and Monterrey, demonstrates the market's evolution. Local brewers increasingly incorporate traditional Mexican ingredients and brewing techniques, creating distinctive products that appeal to both domestic and international consumers.

Canada maintains a notable market presence despite facing regulatory challenges, particularly regarding excise tax structures that create competitive disadvantages compared to U.S. breweries. The concentration of craft breweries in British Columbia and Ontario continues to drive innovation in the segment. Canadian craft brewers differentiate themselves through sustainable practices and the use of locally-sourced ingredients, maintaining consumer loyalty despite pricing pressures.

Competitive Landscape

The North American craft beer market maintains a fragmented structure that enables strategic consolidation while preserving the artisanal authenticity valued by consumers. Major industry players actively pursue portfolio expansion through acquisitions, as demonstrated by Tilray Brands Inc.'s significant acquisition of four craft breweries from Molson Coors Beverage Co. in August 2024. This strategic move, which included Hop Valley Brewing Co., Terrapin Beer Co., Revolver Brewing, and Atwater Brewery, expanded Tilray's beverage portfolio to 18 brands. The market's fragmentation continues to provide opportunities for both established players and new entrants to capture market share through strategic acquisitions and organic growth.

Breweries across the market focus on building consumer relationships through direct-to-consumer strategies, enhanced taproom experiences, and beer tourism initiatives. These approaches help establish brand loyalty while securing higher profit margins. Additionally, companies are increasingly implementing sustainability measures, including the adoption of renewable energy and circular packaging practices, to meet the growing demands of environmentally conscious consumers. The emphasis on experiential marketing and sustainability initiatives has become particularly important in attracting and retaining millennial and Gen Z consumers.

The market structure supports diverse operational models, accommodating both large-scale breweries that pursue operational efficiencies and smaller craft producers that focus on local authenticity. This diversity creates distinct market segments that cater to varying consumer preferences and price points, contributing to the ongoing evolution of the region's craft beer ecosystem. The coexistence of different operational scales enables innovation across the market, as smaller breweries often pioneer new flavors and styles while larger producers optimize distribution and market reach.

North America Craft Beer Industry Leaders

Boston Beer Company

Heineken NV

Constellation Brands

Anheuser-Busch InBev

Sierra Nevada Brewing Co

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sierra Nevada Brewing Co. partnered with North Star Carbon & Impact to deploy a new ESG platform, aiming to measure and reduce greenhouse gas emissions.

- May 2025: Policy Kings Brewery opened in Salt Lake City’s Central 9th neighborhood, becoming Utah’s first Black-owned brewery and offering craft beer alongside live soul and rap programming.

- August 2024: Holiday Brewing Company expanded into Texas through a distribution agreement with Dynamo Specialty Distributing. The company introduced Texas-specific labels for its Favorite Blonde Ale, along with its core beer portfolio and seasonal offerings.

- July 2024: Asbury Park Brewery used Microsoft Copilot AI to formulate AI-IPA, a 6% ABV hazy IPA featuring citrus, mango, and pine notes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the North America craft beer market as the retail value generated by independently owned breweries that produce six million barrels or less each year, using traditional recipes or innovative, flavor-driven variants sold through on-trade and off-trade channels across the United States, Canada, Mexico, and the rest of the region.

Scope Exclusion: Imports of global mass-produced beer lines marketed as "craft-styled" and all home-brewed volumes remain outside this study.

Segmentation Overview

- By Product Type

- Ale

- Lager

- Other Beer Types

- By End User

- Men

- Women

- By Packaging

- Bottles

- Cans

- Others

- By Distribution Channel

- On-Trade

- Off-Trade

- By Geography

- United States

- Canada

- Mexico

- Rest of North America

Detailed Research Methodology and Data Validation

Primary Research

To bridge gray areas, we conducted interviews with brew-pub operators, can manufacturers, regional distributors, and festival organizers across various U.S. states, Canadian provinces, and Mexican metropolitan hubs. These dialogues sharpened assumptions on average selling prices, rotating tap preferences, and seasonality patterns that desk work hinted at but could not quantify alone.

Desk Research

We started with public datasets such as Brewers Association production tallies, Alcohol and Tobacco Tax and Trade Bureau shipment filings, USDA hops acreage reports, Statistics Canada beer volume surveys, and Mexico's INEGI beverage output tables. We then linked them to company 10-Ks, investor decks, and news archives accessed through Dow Jones Factiva and D&B Hoovers. These sources mapped brewery counts, barrel yields, packaging shifts, and excise tax movements that ground our regional supply picture.

The team next screened trade journals, Questel patent abstracts on novel yeast strains, and Health Canada policy notes on container deposit rules to trace flavor innovation and regulatory inflection points. The sources cited illustrate, not exhaust, the secondary corpus consulted for validation.

Market-Sizing & Forecasting

Mordor analysts reconstruct the 2024 baseline through a top-down synthesis of national production and trade data, which is cross-checked with selective bottom-up roll-ups of sampled brewery revenues and channel checks. Five market fingerprints, average retail price per 16-ounce equivalent, barrels per operating craft brewer, share of cans in packaging mix, on-trade penetration, and hop acreage trends drive our multivariate regression forecast to 2030. Gaps in bottom-up coverage are filled with weighted moving averages informed by primary expert consensus.

Data Validation & Update Cycle

Outputs pass three-layer variance reviews, anomaly alerts, and peer sign-offs before release. We refresh models annually and trigger interim updates if excise policy, raw-material cost, or merger activity materially shifts trajectories. A pre-publication sweep ensures clients receive the latest view.

Why Mordor's North America Craft Beer Baseline Commands Confidence and Reliability

Published estimates often diverge because each firm picks its own scope, price ladders, and refresh rhythm. By anchoring figures to brewer-level demarcation and yearly updates, Mordor narrows comparability gaps for decision-makers.

Key gap drivers include whether flavored malt beverages are bundled, treatment of tap-room margins, Mexico's inclusion, and currency conversion timing. Some publishers rely on single-year brewer surveys, whereas we triangulate live production filings and channel mix pivots before sign-off.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 64.02 B (2025) | Mordor Intelligence | |

| USD 33.0 B (2024) | Regional Consultancy A | Excludes tap-room revenues and Mexico; limited channel coverage |

| USD 25.0 B (2025) | Global Consultancy B | Uses sampled brewer surveys; slower update cadence; narrower packaging scope |

Collectively, the comparison shows that Mordor's variable-rich model, transparent scope choices, and disciplined refresh cadence deliver a balanced, reproducible baseline clients can trust.

Key Questions Answered in the Report

What is the current size of the North America craft beer market and how fast is it growing?

The market is valued at USD 69.45 billion in 2026 and is forecast to reach USD 104.32 billion by 2031, reflecting an 8.48% CAGR.

Which product category holds the largest share of the North America craft beer market?

Ale styles lead with 38.02% market share in 2025, driven by sustained consumer enthusiasm for hop-forward and hazy IPA variants.

What are the primary factors driving market expansion through 2031?

Growth stems from a rising number of microbreweries, continuous flavor innovation, higher disposable income, and beer-tourism experiences that deepen consumer engagement.

How are packaging preferences evolving among craft beer consumers?

Cans dominate with a 52.31% share in 2025 because they offer portability, recyclability, and superior product protection, while smart and eco-friendly formats are gaining traction.

Page last updated on: