Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 308.51 Billion |

| Market Size (2031) | USD 376.06 Billion |

| Growth Rate (2026 - 2031) | 4.04% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Beer Market Analysis by Mordor Intelligence

The European beer market size is projected to grow substantially, increasing from USD 308.51 billion in 2026 to USD 376.06 billion by 2031, at a CAGR of 4.04%. In terms of market volume, the market is expected to grow from 36.81 billion liters in 2026 to 41.43 billion liters by 2031, at a CAGR of 2.39% during the forecast period (2026-2031). Brewers are increasingly focusing on premium products, which cater to evolving consumer preferences for higher-quality beverages. Additionally, there is a significant expansion in low- and no-alcohol beer offerings, aligning with the growing demand for healthier and more lifestyle-oriented options. Furthermore, the adoption of recyclable packaging is gaining traction, reflecting both environmental concerns and regulatory pressures. These trends collectively contribute to higher average selling prices, even as overall beer volumes stabilize.

Key Report Takeaways

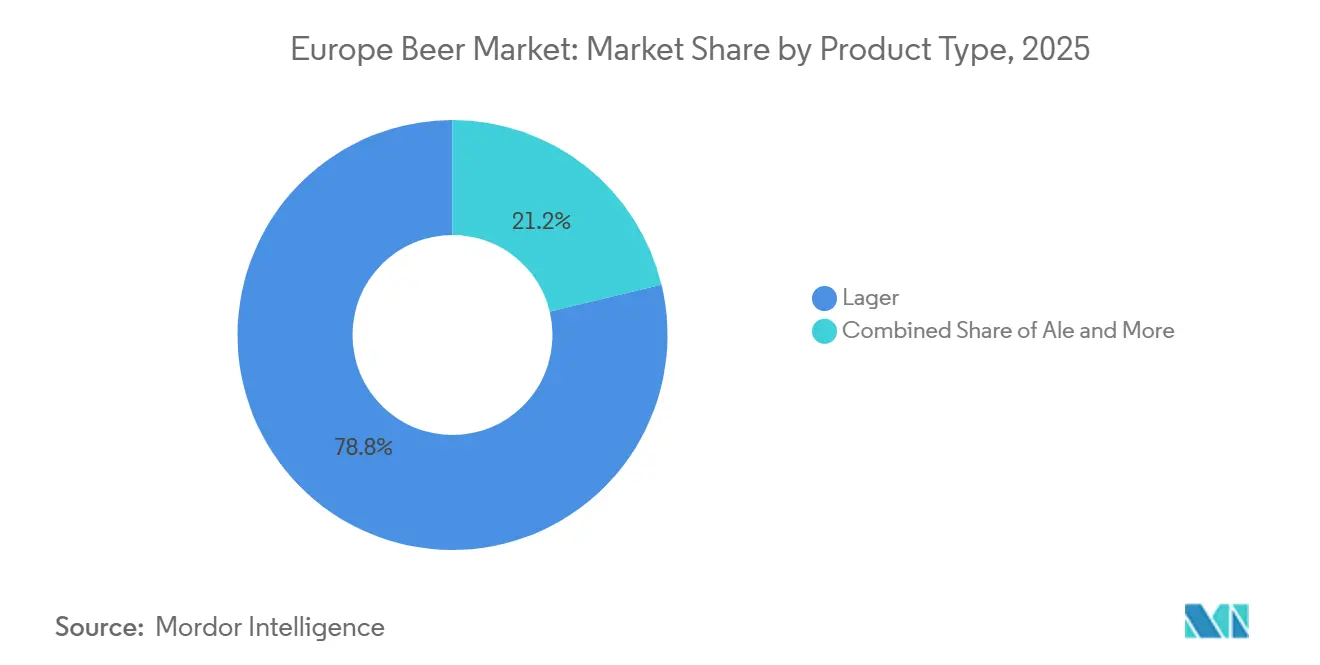

- By product type, lager held 78.76% of the European beer market share in 2025; ale is projected to register the highest 5.66% CAGR through 2031.

- By category, the standard segment accounted for 85.65% of the European beer market size in 2025, while premium is forecast to expand at a 4.72% CAGR to 2031.

- By packaging type, bottles dominated with 42.35% revenue share in 2025; cans are expected to exhibit the strongest 5.05% CAGR over the forecast period.

- By distribution channel, off-trade controlled 51.22% revenue share in 2025, whereas on-trade is anticipated to post a 4.76% CAGR until 2031.

- By geography, the United Kingdom commanded a 21.32% share of 2025 sales, while France is set to record the fastest 4.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Beer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Craft Beer Renaissance | +1.2% | Global, with a concentration in the United Kingdom, Germany, and France | Medium term (2-4 years) |

| Innovative Product and Flavor Formats | +0.8% | Western Europe, expanding to Central Europe | Short term (≤ 2 years) |

| Low-Alcohol/Non-Alcoholic Expansion | +1.5% | Global, led by Germany, Scandinavia | Long term (≥ 4 years) |

| Advancements in Brewing Technology | +0.6% | Developed European markets, technology hubs | Medium term (2-4 years) |

| Sustainable Brewing and Supply Chains | +0.9% | Europe-wide, driven by regulatory compliance | Long term (≥ 4 years) |

| Sophisticated Branding and Storytelling | +0.7% | Premium markets across Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Craft Beer Renaissance

France, now home to the EU's largest network of 2,500 independent brewers, showcases the paradox of the European craft beer renaissance[1]Source: Brewers of Europe, "European Beer Trends 2024", brewersofeurope.eu. Despite this burgeoning presence, craft segments account for only 5-10% of total market volume, as Brewers of Europe highlights. This suggests that while craft brewing may not dominate in market share, its influence is palpable, exerting premiumization pressures on mainstream brands. Data from The Brewers of Europe revealed that in 2024, Germany had 836 microbreweries[2]Source: The Brewers of Europe, "EUROPEAN BEER TRENDS - 2025", brewersofeurope.eu. Moreover, the sector grapples with consolidation pressures. Rising production costs, 44% hikes in barley malt and 20% in aluminum cans, are prompting brewery closures and market exits. Major brewing groups, once keen on craft acquisitions, are now pivoting, channeling resources into their flagship international brands. This craft renaissance has birthed a divided market: while successful artisanal producers champion premiumization, many others face extinction, inadvertently bolstering large-scale producers who seamlessly integrate craft-inspired innovations without the associated complexities.

Innovative Product and Flavor Formats

Brewers are moving beyond traditional beer categories, using flavor diversification to meet changing consumer tastes and support premium pricing. In France, artisanal beers are projected to capture a 27% market share by 2025, and brewers are adopting innovative techniques like accelerated fermentation to boost production efficiency. Sustainability is also a key focus, highlighted by 1664 Blonde's commitment to 100% sustainable malt by 2026. This initiative, involving 120 farmers and spanning 2,765 hectares, ensures digital traceability from barley to bottle. Technology is playing a pivotal role, allowing breweries to experiment with flavors while ensuring consistent quality. Automated systems now process 230-235 cans per minute, offering greater flexibility in recipe management. While the flavored beer segment has seen a 14% growth in Europe, overall volumes have declined, underscoring the need for brewers to balance novelty with consumer acceptance. The challenge remains: how to scale these innovative formats without losing cost competitiveness to established products.

Low-Alcohol/Non-Alcoholic Expansion

Projected to surpass ale as the world's second-largest beer category by 2025, non-alcoholic beer segments are witnessing remarkable growth. In 2024, as per the European Union, European beer production hit 34.7 billion liters: while alcoholic beer output nudged up by 0.6%, low-alcohol varieties surged by 11.1%, underscoring a clear consumer shift towards moderation[3]Source: Eurostat, "Beer production increases to 34.7 billion litres", ec.europa.eu. Leading this shift, European markets, particularly Germany, are witnessing a drop in traditional beer volumes, yet a surge in non-alcoholic sales, pushing global retail sales to new heights. The allure of non-alcoholic beers isn't limited to health-conscious consumers; it's also being driven by regulatory measures. For instance, with Ireland mandating cancer warning labels on alcoholic drinks, zero-proof alternatives gain a competitive edge. Seizing this momentum, Carlsberg's January 2025 acquisition of Britvic aims to bolster its non-alcoholic market share from 16% to 30%, eyeing annual cost savings of EUR 100 million. Innovations in production are refining taste profiles, breaking down traditional adoption barriers. Meanwhile, partnerships with health-centric retailers are broadening distribution channels, reaching audiences beyond the conventional beer market. These moves underscore a strategic belief: non-alcoholic segments can chart a growth trajectory, even as alcohol consumption wanes. However,

Advancements in Brewing Technology

Amid climate-related disruptions, European brewing is being reshaped by technological advancements, focusing on automation, sustainability, and bolstered supply chain resilience. Spanish startup Ekonoke showcases the potential of innovation with its hydroponic hop cultivation systems. These systems cut the growth cycle from 6 months to just 3, using 15 times less water. Their groundbreaking approach has drawn investments from Hijos de Rivera and AB InBev. This innovation is timely, as European hop production has seen a 40% decline due to climate change, jeopardizing both the quality and availability of beer. Brewing automation now spans beyond mere production. Facilities are adopting systems that not only boost production rates and enhance sanitation protocols but also allow for flexible recipe management across varied product lines. Digital transformation in brewing isn't limited to production. Breweries are engaging consumers through innovations like QR codes for supply chain transparency and specialized e-commerce platforms for direct sales. The real competitive edge lies with brewers who adopt a holistic technological approach, weaving it seamlessly through production, distribution, and customer engagement, rather than chasing isolated automation projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Competition from Other Alcoholic Beverages | -0.9% | Western Europe, particularly wine regions | Medium term (2-4 years) |

| Raw Material Volatility and Availability | -1.1% | Global, acute in Northern Europe | Short term (≤ 2 years) |

| Environmental Regulations and Sustainability Pressures | -0.7% | Europe-wide, strictest in Nordic countries | Long term (≥ 4 years) |

| Increasing Regulations Against Alcohol | -0.8% | Europe-wide, varying by member state | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Competition from Other Alcoholic Beverages

Ready-to-Drink (RTD) beverages are emerging as formidable competitors in the beverage market. Their mainstream acceptance was notably highlighted at ProWein 2024, where RTDs were extensively showcased. This growing popularity exerts competitive pressure, especially in traditional wine regions. Here, consumers are increasingly gravitating towards convenience-oriented products that deliver diverse flavors without the complexities of brewing. The challenge posed by RTDs isn't limited to merely substituting traditional beverages. They are also vying for prime distribution channels. Retailers, in pursuit of higher margins, are giving these RTDs premium shelf space and heightened marketing attention, often at the expense of traditional beer categories. Meanwhile, spirits and wine producers, capitalizing on their established brand recognition and robust distribution networks, are strategically positioning themselves to tap into beer consumption moments. This is particularly evident among younger consumers, who are showing diminished brand loyalty and a greater propensity to experiment across various beverage categories. As the lines between traditional beverage categories continue to blur, the competitive landscape grows more intricate. This evolution compels beer producers to pivot towards innovation and strategic positioning to safeguard their market share, moving away from a reliance on historical consumption trends.

Raw Material Volatility and Availability

Climate change, geopolitical tensions, and regulatory restrictions are disrupting raw material supply chains, jeopardizing production continuity and cost predictability. In 2024, the European Union, the world's leading barley producer, harvested about 50.4 million metric tons for the 2024/2025 marketing year, surpassing expectations, as reported by the US Department of Agriculture. However, protein variability in France, ranging from 9-12%, introduces quality inconsistencies that affect brewing specifications. EU pesticide regulations are tightening, limiting the use of Etoxazole and Bifenazate, which heightens vulnerabilities in hop production. Simultaneously, climate change is slashing European hop yields by 40%. Research into alternative grains reveals that while rice malt production costs are about 20% steeper than barley malt, rice boasts better yields and demands less land for equivalent extract production. Energy cost inflation is adding to the pressures on raw materials. German brewers, facing high personnel costs and a tepid consumer sentiment, are feeling the pinch in competitiveness, leading to calls for government tax relief. To bolster supply chain resilience, strategies emphasizing diversification and forging long-term supplier partnerships are essential, ensuring a balance between cost optimization and consistent quality and availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Lager Dominance Faces Ale Innovation

In 2025, Lager holds a dominant 78.76% market share, but Ale segments are outpacing with a robust 5.66% CAGR projected through 2031. This shift underscores a changing consumer palate, leaning towards intricate flavors and craft-inspired brews. As the market matures, there's a noticeable transition: consumers once driven by Lager's volume are now gravitating towards Ales, valuing unique taste profiles and willing to pay a premium. Meanwhile, the Non/Low-Alcohol Beer category is surging, riding the wave of heightened health consciousness and regulatory nudges towards lower-alcohol options. Specialty and seasonal variants, grouped under Other Beer Types, may hold a smaller volume share, but their premium pricing indicates a savvy niche positioning.

Established beer categories are being reshaped by innovative segments, resonating more with today's consumer values and lifestyles. The European craft beer scene is booming, with Germany and the UK at the forefront, while France, Spain, and Italy are catching up, showing a growing appetite for craft varieties. Thanks to technological strides, Ale brewers can now produce at scale without sacrificing the artisanal touch that sets them apart from mainstream Lagers. This landscape suggests that while diversifying portfolios is crucial, brewers must also hone their core competencies. The burgeoning Ale market demands distinct production skills and marketing strategies, diverging from traditional Lager methods.

By Category: Premium Positioning Accelerates Value Creation

Despite the Standard category commanding an 85.65% share in 2025, premium segments are projected to grow at a 4.72% CAGR through 2031. This trend underscores the industry's shift towards premiumization, emphasizing value extraction over sheer volume. The disparity in category performance highlights consumers' readiness to pay more for perceived quality, authentic brand narratives, and enriched experiences. For premium positioning to thrive, brands must consistently deliver quality, craft compelling narratives, and forge partnerships with distribution channels that elevate their luxury status through curated retail environments and top-notch service.

While the Standard category remains resilient, driven by price-sensitive consumers valuing accessibility, its declining growth rates hint at a potential erosion. This shift could be fueled by improving economic conditions and a more discerning consumer base. The push towards premiumization is evident, with brands like Birra Moretti successfully repositioning themselves. Once a niche Italian import, Birra Moretti has ascended to UK market leadership, thanks to its Mediterranean authenticity messaging and unwavering quality. Distribution strategies are now honing in on premium channels, targeting specialty retailers, upscale hospitality venues, and direct-to-consumer platforms, all aimed at bolstering margins. The evolving dynamics hint at a long-term market tilt towards premiumization. Yet, the Standard segments continue to play a pivotal role, ensuring volume maintenance and safeguarding market share amidst competitive challenges.

By Packaging Type: Sustainability Drives Can Adoption

Driven by sustainability mandates, convenience preferences, and supply chain optimization, cans are projected to grow at a 5.05% CAGR through 2031. In contrast, bottles commanded a 42.35% market share in 2025. This shift in packaging underscores a growing environmental consciousness, with the recyclability of aluminum gaining prominence over the traditional perception of glass as a premium material. European aluminum producers, united under the European Aluminium Packaging Group, are pushing for a bold target: 100% recycling of beverage cans by 2030. Their strategy includes developing standardized alloys that can utilize up to 100% recycled content.

While bottle packaging continues to lead the market, benefiting from a premium image and a consumer preference for glass during formal occasions, it faces growth challenges. These challenges stem from tightening environmental regulations and the rising transportation costs of glass, especially when juxtaposed with the lightweight nature of aluminum. Meanwhile, the "other packaging" category is evolving, embracing innovative formats. These include sustainable materials and designs tailored for convenience, catering to diverse consumption contexts and demographic tastes. The EU's Packaging and Packaging Waste Regulation is tightening its grip, mandating a rise in recycled content, 25% by 2025 and 30% by 2030. This push creates compliance challenges, especially for formats lacking a robust recycling infrastructure. As brewers navigate this landscape, they're making strategic packaging choices. These decisions weigh the scales of sustainability compliance, cost efficiency, and brand image, with many investing in innovations that not only benefit the environment but also uphold product quality and consumer allure.

By Distribution Channel: On-Trade Recovery Drives Growth

Despite Off-Trade channels commanding a 51.22% share in 2025, On-Trade channels are projected to grow at a 4.76% CAGR through 2031. This trend underscores a rebound in the hospitality sector and a growing consumer inclination towards social experiences, which not only justify premium pricing but also present opportunities for deeper brand engagement. The disparity in growth rates highlights a post-pandemic shift: while consumers are flocking back to bars, restaurants, and entertainment venues, they've retained some of the convenience-driven purchasing habits formed during lockdowns. For On-Trade channels to thrive, breweries must forge partnerships with hospitality operators. These operators, by emphasizing quality, service, and compelling brand narratives, can elevate customer experiences and command higher prices per unit than their retail counterparts.

Leading the Off-Trade channel are Specialty/Liquor Stores and Other Off-Trade Channels, each catering to unique consumer segments with tailored value propositions and service offerings. Specialty retailers, with a focus on craft and premium products, not only command higher margins but also offer expert guidance and curated selections, appealing to discerning consumers. In contrast, Other Off-Trade channels, encompassing supermarkets, convenience stores, and e-commerce platforms, prioritize volume and convenience, offering competitive pricing to meet mainstream consumer demands. This evolution in distribution channels is largely driven by digital transformation. Online platforms now facilitate direct-to-consumer sales, subscription services, and personalized recommendations, often sidestepping traditional retail middlemen. To succeed in channel strategy, it's crucial to grasp the varied consumer behaviors, service expectations, and margin dynamics across different distribution formats, all while ensuring brand consistency and upholding quality standards throughout the supply chain.

Geography Analysis

The United Kingdom commanded a 21.32% share of 2025 sales, while France is set to record the fastest 4.65% CAGR through 2031. In Europe's beer landscape, three tiers of maturity reveal distinct trends. In core Western economies, a shift towards premiumization has taken precedence over volume-driven growth. For instance, while domestic beer consumption in Germany has waned, exports have surged, underscoring a strategy that capitalizes on the nation's heritage and quality. Meanwhile, mid-tier Southern markets like Spain and Italy are not only diversifying internationally but are also cultivating local craft scenes, pushing per-capita spending limits higher. In contrast, emerging markets in Central and Eastern Europe, spanning from Poland to Romania, are adding incremental hectoliters at appealing cost structures. However, with their lower price elasticity, there's a pronounced shift towards value brands, especially those packaged in returnable glass.

Under the EU Green Deal, regulatory alignments are tightening cost pressures, albeit unevenly. For instance, Nordic nations have adopted stricter carbon baselines compared to their Mediterranean counterparts. On a brighter note, standardized labeling rules for calorie counts and ingredient disclosures are easing cross-border operations. The ebb and flow of tourism further complicate matters: take Greek island pubs, which transition from a winter lull to summer's bustling crowds, testing the limits of supply chain agility. All these dynamics suggest that the most lucrative opportunities lie where premiumization meets youthful demographics and lighter regulatory oversight, a sweet spot currently found in France and select Baltic states.

Brewers, on the lookout for geopolitically stable territories, are casting their nets beyond the EU, eyeing markets like Switzerland and the U.K. While progressive mutual-recognition agreements on container-deposit schemes and excise stamps promise to smoothen trade, challenges persist. Logistics costs are still high, driven by a shortage of drivers and fuel taxes. However, integrated route-planning platforms are emerging as a game-changer, optimizing back-hauls and minimizing empty mileage. This not only translates to logistical savings but also bolsters competitive retail pricing, ensuring the European beer market continues its growth trajectory, even amidst flat demand.

Regulatory Landscape

Beer sold in Europe operates under EU food information and safety rules, alongside country-level alcohol controls covering areas such as excise duties, marketing limits, and deposit return schemes. At the EU level, Regulation (EU) No 1169/2011 sets the framework for mandatory food information, which shapes how brewers present ingredient and nutrition information on packs, while packaging and other materials that contact beer are governed by Regulation (EC) No 1935/2004. Additive use is also controlled through EU additive legislation, including early-2024 updates that amended Annex II categorizations and terminology, requiring breweries to confirm that stabilizers, preservatives, and processing aids remain permitted for relevant beverage categories.

Environmental and packaging compliance continues to tighten and increasingly affects format choices and labeling workflows. In June 2026, the European Commission adopted Commission Implementing Decision (EU) 2026/1425, which sets rules for calculating, verifying, and reporting recycled plastic content in single-use plastic beverage bottles under Directive (EU) 2019/904. Separately, evolving national deposit return scheme rollouts, including market impacts cited by major brewers in Poland, add operational complexity for packaging design, reverse logistics, and reporting, reinforcing the value of recyclable formats and traceable packaging claims.

Competitive Landscape

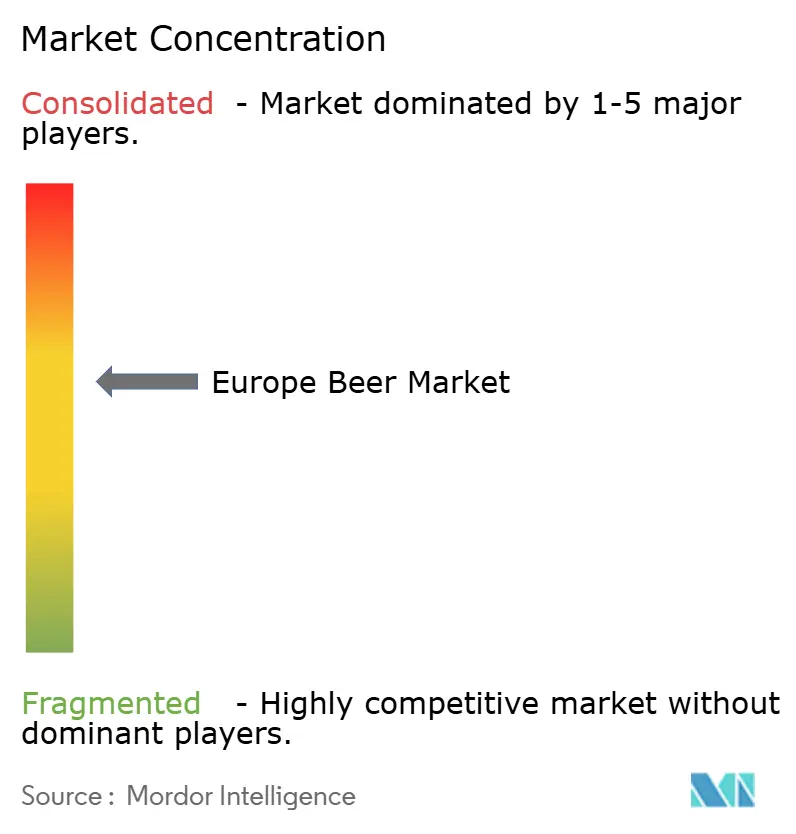

In Europe, the beer sector is moderately concentrated, with the top five multinational groups controlling about 65% of the region's production. This concentration grants them significant bargaining power over suppliers and retailers. AB InBev and Heineken dominate, holding over a third of the total volume. Their extensive brewery networks across the continent not only cut down on freight distances but also allow for flexible promotional strategies. Currently, they're prioritizing premium offerings over expanding their craft beer range.

Meanwhile, mid-sized players like Royal Unibrew and Asahi Europe are making strategic acquisitions, such as Norway's Hansa Borg, to diversify their portfolios. They're not just focusing on beer anymore; cider and energy drinks are now part of the mix, reducing their reliance on any single category. National brands like Mahou-San Miguel leverage deep-rooted local ties and culinary connections, securing prominent placements in local markets. Even in areas where global brands dominate, Mahou-San Miguel's local loyalty ensures they commands a significant presence. While private-label brands are struggling to gain traction, it's largely due to the high costs of sustainability compliance. These costs deter retailers from stocking less-distinguished products, giving established brands a chance to maintain their market share.

Operational performance is increasingly being shaped by technological advancements. Breweries that have adopted closed-loop CO₂ recovery systems are reaping benefits, saving up to 1.6 kg of CO₂ per hectoliter. This not only curtails their Scope 1 emissions but also reduces excise tax burdens in regions with stringent regulations. Additionally, digital tracking of kegs has led to impressive return rates exceeding 98%, significantly cutting down on capital expenditure tied to floating container pools. Companies that successfully merge environmental benefits with clear, transparent narratives are not just enhancing their market positions but are also able to command higher price premiums, contributing to the overall growth of the European beer market.

Europe Beer Industry Leaders

-

Asahi Group Holdings Ltd

-

Carlsberg Group

-

Anheuser Busch InBev

-

Heineken N.V.

-

Molson Coors Beverage Co.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Non-alcohol and low-alcohol beer is a key focus for portfolio expansion and capacity allocation, as consumers move toward moderation and regulators increase pressure around alcohol communication. The Brewers of Europe data indicates that in 2025 EU beer production declined by 2.9% and consumption fell by 3.2%, while non-alcohol beer grew by 5.9%, supporting continued shelf space and on-trade listings for alcohol-free propositions. Supply-side commitments also reflect this demand shift: Diageo opened the Littleconnell Brewery in Newbridge, Ireland, in May 2026 as part of a near EUR 1 billion (2020-2029) investment program, and confirmed plans for a Brewery 2 investment of about EUR 400 million at the same site to double capacity for Guinness and Guinness 0.0, with work scheduled to begin in 2026.

Decarbonization, circularity, and packaging-system readiness are also becoming practical advantage areas as EU sustainability reporting and packaging rules raise data and compliance requirements for multi-country footprints. Heineken referenced packaging deposit return scheme phasing effects in Poland in its 2026 updates, pointing to an operational driver for more standardized packaging, improved return logistics, and adaptable route-to-market execution. Targeted capex for lower-carbon operations is advancing at the same time: in April 2026 Heineken announced a EUR 12 million investment into low-carbon production at its Craiova and Ungheni facilities, and Carlsberg-backed investment activity has included a EUR 12 million can-line program in Lviv that added high-throughput canning capability, aligning with the market shift toward cans and recyclability-led pack formats. R&D pathways are broadening revenue pools beyond beer itself, including EU-backed circular-economy work such as the CHEERS project (led by Mahou), which validates industrial-scale upcycling of brewery side-streams, including wastewater and CO2, into bio-based products and links cost, compliance, and sustainability narratives for European brewers.

Recent Industry Developments

- May 2026: Diageo opened the Littleconnell Brewery in Newbridge, Ireland, as part of its near EUR 1 billion investment program for 2020-2029. The company also confirmed plans for a roughly EUR 400 million Brewery 2 at the site to double capacity for Guinness and Guinness 0.0, with work scheduled to begin in 2026, strengthening supply for both alcoholic and alcohol-free beer demand.

- January 2025: Carlsberg Group completed the acquisition of Britvic plc and formed Carlsberg Britvic in the UK. The deal expands Carlsberg's non-beer beverage footprint and provides a broader route-to-market platform that can support cross-category execution in a region where beer volumes face competitive pressure from alternative beverages.

- March 2024: Krombacher Brewery, in collaboration with Starnberger, announced plans to bring the Starnberger brand to broader international markets. The move extends a craft-led proposition into additional European geographies, reinforcing premiumization and portfolio differentiation strategies beyond core beer markets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of beer sold across Europe, including mainstream and premium beer, as well as low and no-alcohol beer, across on-trade and off-trade channels. The sizing is built in USD value terms, supported by volume signals in liters to keep pricing and demand aligned.

Scope exclusions: We do not include cider, wine, spirits, or flavored malt beverages that are not classified as beer in official statistics.

Segmentation Overview

-

By Product Type

- Ale

- Lager

- Non/Low-Alcohol Beer

- Other Beer Types

-

By Category

- Standard

- Premium

-

By Packaging Type

- Bottles

- Cans

- Others

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Specialty/Liquor Stores

- Others Off Trade Channels

-

By Geography

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

-

Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the outer guardrails for the model, especially for beer production, trade, and consumption trends across major European countries. We typically referenced public sources such as Eurostat, national statistical offices, the European Commission trade data, UN Comtrade, and FAOSTAT, and then cross-checked these with association releases and reputable press coverage.

On the commercial side, company annual reports, investor presentations, and regulatory updates helped us translate volume movements into value impacts, since pricing and premium mix can move faster than consumption. A paid subscription for company financials and intelligence, and another for shipment-level import and export checks, were used selectively to validate totals and spot sudden changes in product flows. The sources listed here are illustrative only, and many other public documents were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the assumptions behind pricing, premiumization, channel mix, and low and no-alcohol adoption, which are difficult to pin down from public data alone. We spoke with a mix of brewery-side stakeholders, distributors, on-trade buyers, and retail category contacts across key beer-consuming countries, and the inputs were used to confirm the demand signals and adjust conversion factors where gaps appeared.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 14% | |

| Mid tier: 48% | Functional/Unit leaders: 27% | |

| Smaller Players: 16% | Managers: 59% |

Market-Sizing & Forecasting

The core build uses a top-down approach where production, trade, and apparent consumption patterns are reconstructed for Europe and then translated into value using pricing and mix assumptions that fit each channel. To keep the totals realistic, we corroborated results with selective bottom-up approximations, such as sampled brand and pack price checks, distributor channel feedback, and a limited roll-up of reported revenues for exposed beer portfolios.

Inputs that mattered most in this market included beer volume in liters, on-trade versus off-trade share shifts, premium versus standard mix, low and no-alcohol penetration, and packaging preferences that can change realized prices. When a country-level data series was incomplete, the gap was filled using nearby period trends plus peer-country ratios, and then re-checked through primary feedback to avoid over-smoothing.

For forecasting, scenario analysis was used so demand and price can be stressed separately, and then combined into a practical base case. The forward view was anchored to expected changes in disposable income pressure, channel normalization, and premiumization pace, and then adjusted using expert consensus gathered during interviews.

Data Validation & Update Cycle

Outputs were checked through triangulation across value, volume, and channel signals, and any sharp jumps were reviewed back to the underlying assumptions before sign-off. We also ran variance checks across countries to confirm that implied per-capita consumption and price levels stayed within believable ranges.

Each report goes through multi-step analyst review, and re-contacts are triggered when a key input changes materially, such as alcohol tax shifts, major route-to-market changes, or sustained pricing shocks. Reports are refreshed annually, and before delivery an analyst completes a final update pass so clients receive the latest view.

Mordor Intelligence's Europe Beer Market Size Versus Other Published Estimates

Published market sizes for European beer rarely match because the pricing basis and product boundaries are not treated the same way, and the assumed path of premium mix and low and no-alcohol growth can also shift the value outcome quickly.

Some external figures lean toward retail selling price measurements or focus on a narrower country set with simplified channel coverage, which can push values up or down depending on what gets counted and how currency timing is handled. In Mordor Intelligence sizing, beer is counted as category-specific value across both on-trade and off-trade for Europe, and nearby alcohol categories like cider are kept out even if they sit next to beer on shelves.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 308.51 B (2026) | |

| Trade Data Publisher A | USD 155.24 B (2024) | Uses retail selling prices and a different time window, so the value basis and inflation pass-through are not comparable to a category-value build tied to channel mix. |

| Global Consultancy B | USD 219.62 B (2024) | Uses a different base year and coverage set, and does not clearly state the price basis in the accessible summary, which can change the reported value even with similar volume assumptions. |

The table shows that the biggest spread comes from price basis and what gets grouped into the beer value pool, followed by the year chosen for the snapshot. By keeping inputs tied to observable volume signals and then converting to value with stated channel and mix assumptions, the estimate stays traceable and can be repeated when new data points arrive.

Key Questions Answered in the Report

What is the projected revenue value for the European beer market in 2031?

The European beer market is expected to reach USD 376.06 billion by 2031.

Which product type is expanding the fastest?

Ale is forecast to grow at a 5.66% CAGR through 2031, the quickest among major styles.

Which country will add the most incremental sales through 2031?

France is set to deliver the fastest growth, expanding at a 4.65% CAGR as younger consumers favor beer over wine.

How concentrated is the competitive landscape?

A concentration score of 7 indicates moderate consolidation, with the top five brewers responsible for around 65% of regional output.

Page last updated on: