Black Beer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 70.37 Billion |

| Market Size (2031) | USD 85.72 Billion |

| Growth Rate (2026 - 2031) | 4.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Black Beer Market Analysis by Mordor Intelligence

The black beer market size was valued at USD 67.65 billion in 2025 and estimated to grow from USD 70.37 billion in 2026 to reach USD 85.72 billion by 2031, at a CAGR of 4.02% during the forecast period (2026-2031). Consumer demand for premium and craft beer experiences drives this growth. Black beer attracts both connoisseurs and traditional consumers with its robust flavors, deep color, and high malt content. Metropolitan populations and younger consumers influence manufacturers to create innovative products. The market expands through increased female participation, supported by targeted marketing and diverse products. The expansion of distribution networks is also accelerating market reach. While bars and pubs remain influential, the rise of off-trade channels like retail chains, e-commerce platforms, and specialty stores is making black beer more accessible to a wider audience. Packaging trends are reinforcing this momentum, as the convenience and eco-friendliness of cans appeal to modern consumers, while bottled variants maintain a stronghold among those seeking premium, traditional presentation. The Asia-Pacific region shows strong growth potential as disposable incomes rise, urbanization continues, and consumers embrace international beverage trends. These factors point to sustained growth in the black beer segment, creating opportunities for market expansion and product innovation across regions.

Key Report Takeaways

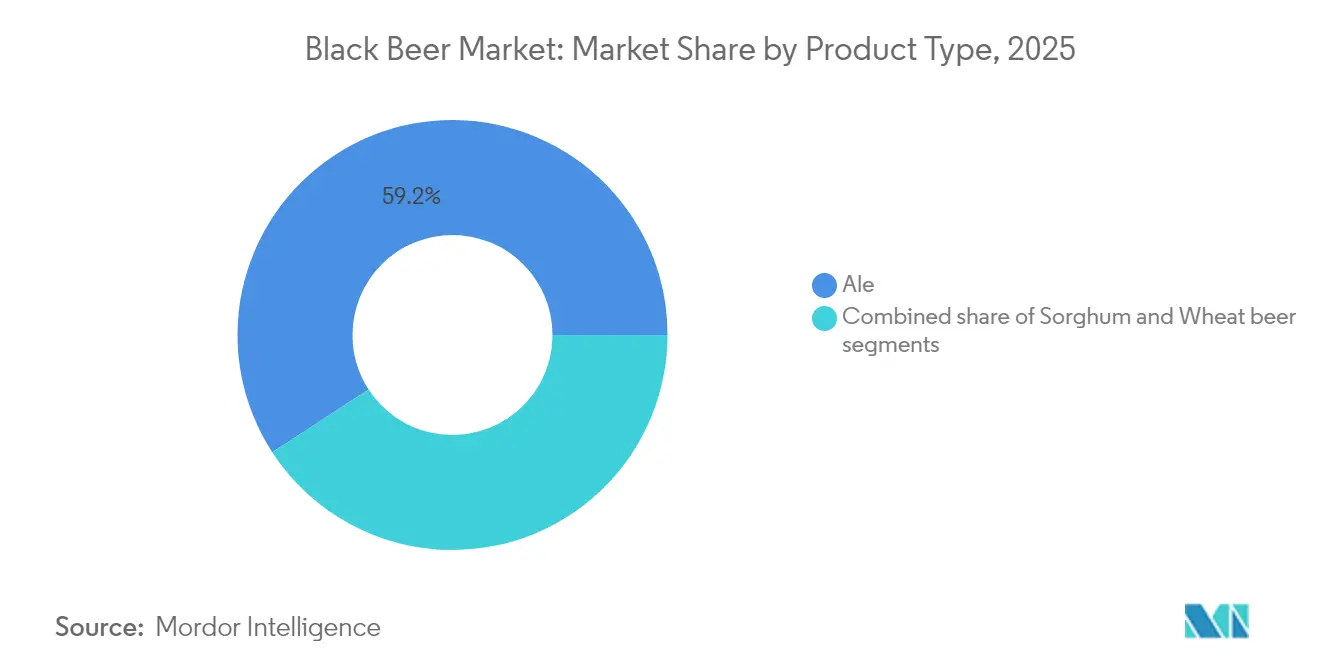

- By product type, ale led with 59.17% of black beer market share in 2025, while Wheat Beer is forecast to expand at a 4.42% CAGR through 2031.

- By end user, men accounted for 68.78% share of the black beer market size in 2025, but the women segment holds the fastest projected CAGR at 4.66% to 2031.

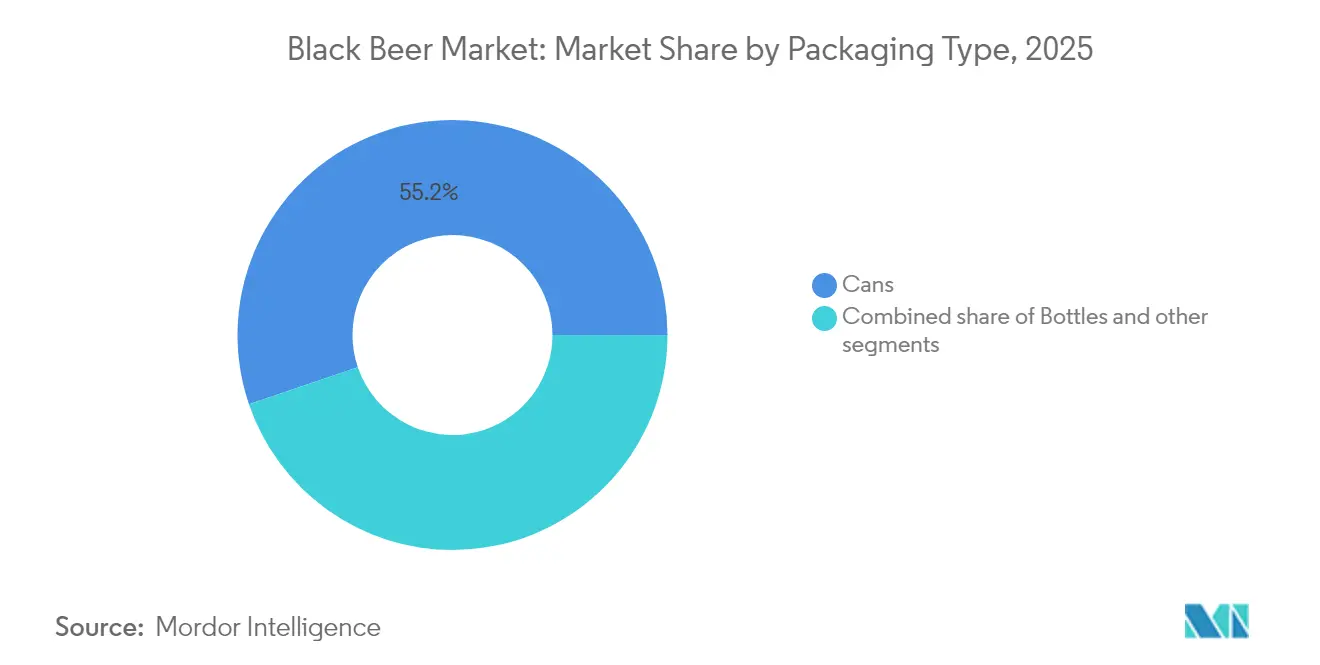

- By packaging, cans dominated with 55.21% of the black beer market share in 2025; bottles are advancing at a 4.9% CAGR through 2031.

- By distribution channel, the on-trade segment captured 57.74% share of the black beer market size in 2025, whereas the off-trade segment is set to grow at a 4.15% CAGR to 2031.

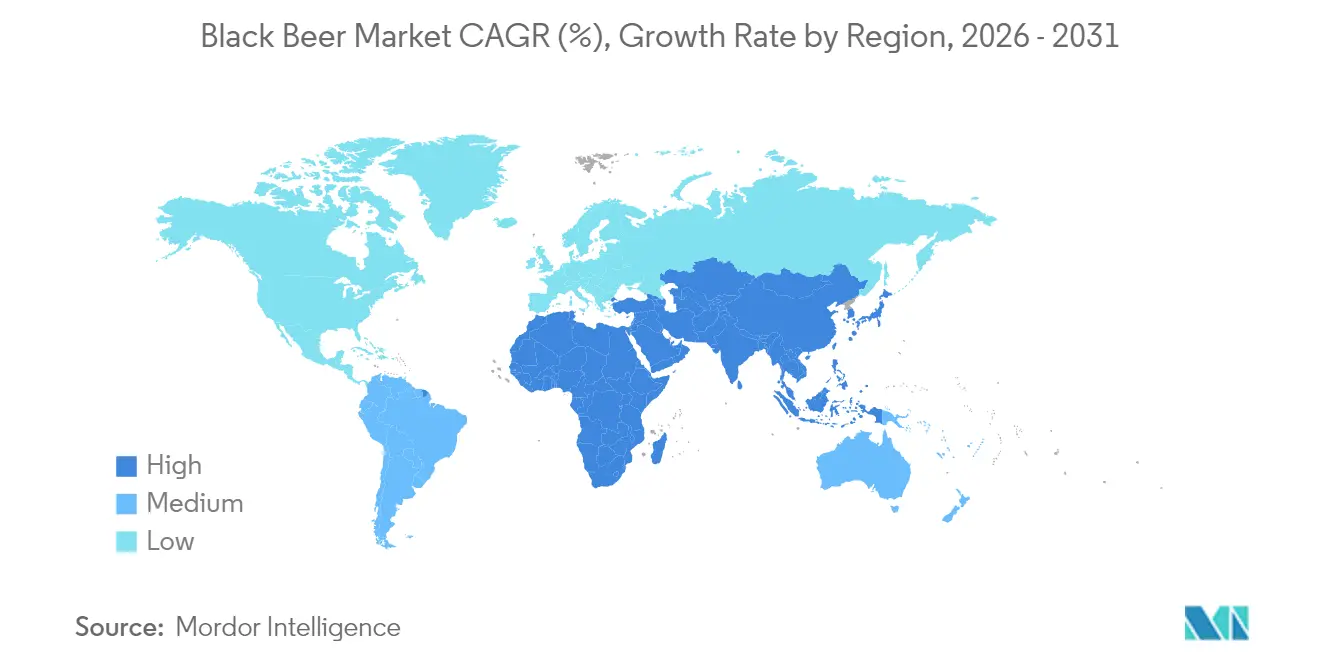

- By geography, Europe held 41.22% of the black beer market share in 2025, while Asia-Pacific shows the highest regional CAGR at 4.96% between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Black Beer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of craft beer culture and microbreweries | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growing tourism and hospitality sector | +0.8% | Europe, North America, emerging Asia-Pacific destinations | Short term (≤ 2 years) |

| Health awareness and perceived benefits of dark beer | +0.7% | North America, Europe, Urban Asia-Pacific | Medium term (2-4 years) |

| Rising consumer preference for unique and complex flavors | +1.0% | Global, with early adoption in urban centers | Long term (≥ 4 years) |

| Cultural influence and social media trends | +0.6% | Global, with highest impact in digitally connected markets | Short term (≤ 2 years) |

| Strategic marketing highlighting product heritage | +0.4% | Europe, North America, premium segments globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth of Craft Beer Culture and Microbreweries

The expansion of craft beer culture and microbreweries serves as a fundamental catalyst in the dark beer market's evolution, emphasizing superior quality and localized production methodologies. These establishments distinguish themselves from conventional mass-market manufacturers through the strategic incorporation of regional ingredients and distinctive flavor profiles, thereby addressing the increasing consumer demand for differentiated beverage experiences. The implementation of supportive governmental policies, encompassing regulatory frameworks and fiscal incentives, has contributed significantly to the craft brewing industry's development. Furthermore, microbreweries have established themselves as integral community establishments, facilitating various engagement initiatives through organized events and tasting sessions, which subsequently enhance customer retention. This transformation in the brewing landscape is evidenced by data from the Brewers Association, which documented 9,796 operational craft breweries in the United States during 2024, representing a 0.36% increase from the previous year, thus demonstrating the sustained growth and market presence of craft brewing establishments [1]Source: Brewers Association, "Brewers Association Reports 2024 U.S. Craft Brewing Industry Figures", www.brewersassociation.org .

Growing Tourism and Hospitality Sector

The expansion of the tourism and hospitality industry serves as a fundamental driver for the global black beer market growth by facilitating breweries' access to international consumer bases. The emergence of beer tourism as a significant market phenomenon has manifested through structured brewery tours, organized festivals, and curated tasting events that prominently feature black beer varieties, including stouts, porters, and dark lagers. This systematic international exposure effectively introduces black beer to diverse consumer demographics and establishes its position as a premium craft beverage option, thereby encouraging market participants to explore beyond conventional lagers and ales. The established beer markets of Europe and North America, characterized by their deep-rooted beer traditions, have experienced substantial growth in tourist participation at specialty beer events, consequently strengthening the demand for black beer products across both traditional and craft brewery segments. This trend is further substantiated by the UN Tourism World Tourism Barometer (May 2025), which indicates that international tourist arrivals surpassed 300 million in Q1 2025, demonstrating an increase of 14 million (5%) compared to the previous year 2024 [2]Source: UN Tourism, “World Tourism Barometer," unwto.org .

Health Awareness and Perceived Benefits of Dark Beer

Black beer's market positioning is transitioning from a traditional heavy beverage to a wellness-oriented drink, thereby increasing its appeal among health-conscious consumers. Stouts and porters are experiencing increased market penetration due to their complex flavor profiles and nutritional composition, specifically their higher concentrations of antioxidants, B vitamins, and essential minerals compared to light beers. The category demonstrates particular resonance among urban, educated consumers who prioritize both taste and health benefits in their beverage selections. The growing recognition of dark beer's digestive benefits and antioxidant properties has substantially enhanced its market acceptance. In response to this market evolution, brewers are strategically developing organic black beers and lower-alcohol variants that maintain the characteristic richness while addressing contemporary health preferences. This transformation in consumer preferences, coupled with the industry's adaptability to health-conscious trends, continues to drive the growth and innovation in the black beer segment, establishing a robust foundation for sustained market expansion.

Rising Consumer Preference for Unique and Complex Flavors

The market is experiencing a transformative evolution as consumers demonstrate heightened sophistication in their beer preferences, particularly gravitating toward dark beers with multifaceted flavor compositions. Breweries strategically diversify their product portfolios through methodical flavor innovation, incorporating premium ingredients such as coffee, chocolate, and herbs to develop distinctive offerings that command higher price points in the market. This sustained consumer demand for sophisticated flavor profiles accelerates technological advancements in brewing methodologies, including cold crushing and hybrid yeast processes, enabling precise flavor control and production consistency. These advanced production techniques enable manufacturers to establish distinctive flavor signatures, thereby strengthening their market position and competitive differentiation in an increasingly sophisticated beverage landscape. The continuous refinement of brewing processes and flavor development capabilities positions manufacturers to effectively respond to evolving consumer preferences while maintaining product quality and consistency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent government regulations | -0.6% | Global, with particular impact in emerging markets | Medium term (2-4 years) |

| Consumer's inclination toward no/low alcohol products | -0.5% | North America, Europe, Urban Asia | Long term (≥ 4 years) |

| Premium pricing limiting mass market adoption | -0.4% | Global, with highest impact in price-sensitive markets | Medium term (2-4 years) |

| Logistics challenges in maintaining product quality | -0.3% | Global, with particular impact on international trade | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Government Regulations

Government regulations aimed at sustainability and public health create significant barriers in the global black beer market. These regulations increase operational costs, add compliance requirements, and limit marketing options for brewers, particularly affecting small and medium-sized craft breweries. Key regulatory requirements include alcohol content disclosure, advertising restrictions, packaging standards, and distribution controls, which affect product launches and market expansion. Zoning and licensing laws restrict microbrewery and taproom expansion in urban areas, while high excise duties on high-ABV beverages increase black beer prices, reducing consumer demand. Restrictions on alcoholic beverage advertising, particularly in digital media, limit brand visibility and consumer outreach. Manufacturers also face increased costs due to varying regulations across countries and regions, requiring modifications to labeling, packaging, and formulations. These regulatory requirements affect global brewers focusing on specialized products like black beer, impacting their expansion plans. In the United States, for instance, the Alcohol and Tobacco Tax and Trade Bureau (TTB) enforces strict compliance for labeling and formulation through processes such as the Certificate of Label Approval (COLA).

Consumer’s Inclination Toward No/Low Alcohol Products

The increasing consumer preference for moderate alcohol consumption and alcohol-free alternatives represents a significant market restraint for the black beer industry. The shift is particularly evident among health-conscious consumers, especially younger demographics, who actively seek products that deliver beer-like experiences without alcohol content. This transformation in consumer behavior has compelled major breweries to invest substantially in developing non-alcoholic dark beer alternatives to maintain market relevance. Notable industry players, such as Diageo, have strategically expanded their zero-alcohol product portfolio, introducing alcohol-free versions of traditional products like Guinness to address this evolving market demand. The market faces continued pressure as consumers increasingly select low-alcohol or alcohol-free options driven by health consciousness, social considerations, and religious factors. This ongoing transition in consumer preferences is anticipated to further impact traditional black beer sales, necessitating continuous product innovation and portfolio diversification from manufacturers to maintain market position and meet changing consumer requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ale’s Heritage Sustains Category Leadership

The black beer market demonstrates a significant preference for ale, which secured a commanding 59.17% market share in 2025. This dominance stems from Europe's deeply rooted brewing traditions, which have established rigorous quality and authenticity benchmarks that resonate throughout global markets. These traditional elements have effectively strengthened consumer confidence and maintained Ales' premium market positioning, successfully attracting both traditional consumers and enthusiasts seeking the complex flavor profiles characteristic of stouts and porters. The continuous evolution of the ale segment through strategic flavor innovations, including the incorporation of tropical fruit elements, smoked malts, and single-origin cocoa beans, has expanded the category's appeal.

The wheat beer segment exhibits substantial growth potential, with projections indicating a 4.42% CAGR through 2031. The category has attracted consumers seeking approachable flavor profiles and those with dietary preferences. Market expansion has been particularly notable in the gluten-conscious segment, where sorghum-based alternatives have successfully addressed health-conscious consumer demands while maintaining high flavor standards. The implementation of advanced production methodologies, particularly cold crashing techniques, has significantly enhanced product clarity and stability throughout the distribution chain. Additionally, brewers' strategic exploration of alternative grain varieties has strengthened supply chain resilience and fostered continuous product innovation. These developments have positioned wheat beer as a key segment in the black beer market, with strong growth prospects ahead.

By End User: Women Propel Inclusive Growth

Males constitute 68.78% of the dark beer market share in 2025, demonstrating the category's historically male-dominated consumer demographic. This reflects the category's long-standing association with male drinkers, influenced by historical marketing strategies, cultural norms, and consumption patterns. The robustness, bitterness, and fuller-bodied profile of dark beers like stouts and porters align with traditional male taste preferences, reinforcing their dominance in this segment. This consumer behavior continues to influence product positioning, packaging design, and advertising strategies, maintaining men as the primary target audience for dark beer brands globally.

The female consumer segment demonstrates substantial growth potential, with a projected Compound Annual Growth Rate (CAGR) of 4.66% during 2026-2031, driven by evolving social norms, increased economic independence, and broader acceptance of women in alcohol-related social spaces. This trend is particularly evident in markets like Japan, where research from the National Center of Neurology and Psychiatry revealed that approximately 72% of female respondents reported alcohol consumption within the previous year in 2023, reflecting changing attitudes toward female drinking . The projected growth rate signals significant untapped potential, prompting brands to diversify offerings with smoother, more aromatic dark beers and inclusive marketing. Product innovations focusing on health, flavor, and moderation, such as lower-alcohol or botanically infused dark beers, are enhancing appeal among women, accelerating their adoption in this category.

By Packaging Type: Bottles Regain Prestige Through Eco-Innovation

In the global black beer market, packaging serves as a crucial element for sustainability, consumer appeal, and market differentiation. Cans maintain market dominance in 2025, accounting for 55.21% of total category volume. Their lightweight nature reduces transportation costs and environmental impact, while their ability to shield contents from light ensures product quality and freshness. Furthermore, cans are highly recyclable, aligning with the growing consumer preference for eco-friendly packaging solutions. Additionally, their seamless integration with mobile canning systems enables smaller brewers to scale production efficiently, offering a cost-effective and flexible solution for meeting the increasing consumer demand. This combination of functional and environmental benefits solidifies cans as the preferred packaging choice in the black beer market.

Glass bottles represent the fastest-growing packaging segment, with a CAGR of 4.9%. This growth reflects increasing consumer association of glass packaging with premium quality and enhanced drinking experience. The adoption of recyclable, weight-reduced brown glass is increasing, particularly in Europe, where deposit-return systems improve environmental sustainability while maintaining the UV protection essential for dark beer preservation. Manufacturers enhance product differentiation through bottle design features such as molded embossing and foil stamping. The industry's commitment to sustainability extends to both can and bottle formats through the implementation of plant-based carrier handles.

By Distribution Channel: Digital Off-Trade Accelerates Reach

In 2025, global dark beer sales saw the on-trade segment commanding a significant 57.74% share. This surge is largely attributed to a growing consumer preference for premium experiences in venues like pubs, taprooms, and craft beer bars. Patrons are drawn to these spots not just for their ambiance, but also for expert recommendations and exclusive, limited-edition brews. This trend underscores the on-trade segment's pivotal role in brand discovery and fostering community ties. On the other hand, the off-trade segment is poised for growth, with projections indicating a 4.15% CAGR from 2026 to 2031. This expansion is driven by a surge in at-home consumption, the rise of digital retail, and the popularity of subscription models. E-commerce platforms are becoming the go-to for consumers, offering both convenience and a diverse range of niche dark beer brands, often absent from traditional retail shelves.

Specialty and liquor stores maintain their significance in off-trade distribution by providing curated dark beer selections and expert recommendations. E-commerce has emerged as the fastest-growing distribution channel, supported by regulatory changes in markets like South Korea that now permit online alcohol sales. This digital shift particularly benefits craft and specialty dark beer producers by enabling direct consumer access without traditional retail limitations. Supermarkets and convenience stores continue to enhance their dark beer offerings through dedicated craft sections and temperature-controlled displays, supporting product quality and premium positioning.

Geography Analysis

Europe holds 41.22% market share in 2025, building on its established brewing heritage and consumers who value dark beer complexity. The region shows robust growth in craft and specialty beers, notably in France and the United Kingdom, emphasizing quality production. Sustainability initiatives are gaining prominence, exemplified by Carlsberg Marston's Brewing Company's implementation of Snap Pack technology. This new packaging system replaces traditional plastic wraps with a glue-based solution, reducing plastic waste by 76% in multipacks.

Asia-Pacific demonstrates the highest growth potential with a 4.96% CAGR forecast for 2026-2031. This growth stems from increasing disposable incomes, urban development, and evolving consumer preferences. China and India lead regional expansion, with their growing middle classes embracing premium and craft beer options. Regional marketing approaches, including Chinese New Year special edition packaging, strengthen brand presence and consumer connections. North America remains a key market, with the United States at the forefront of innovation and craft spirits production. Consumer preference for authentic, local products has strengthened the craft brewery segment. The American Crafts Spirits Association reports that United States craft spirits reached 13.5 million 9 L cases in retail sales in 2023, showing a -3.6% year-over-year change. South America and the Middle East and Africa display growth potential, particularly in Brazil, Argentina, and South Africa, where increasing consumer sophistication and tourism create new market opportunities.

Competitive Landscape

The black beer market demonstrates a moderately fragmented competitive landscape characterized by the presence of established global brewing corporations, including Diageo, Heineken, and Anheuser-Busch InBev, operating in conjunction with regional specialists and craft breweries. The competitive environment presents two distinct strategic approaches: operational scale optimization and product authenticity differentiation. Global manufacturers implement comprehensive portfolio strategies focused on premiumization, as exemplified by Molson Coors' strategic initiative to position one-third of its global brand portfolio within the above-premium segment.

The market structure facilitates significant opportunities for craft breweries, which capitalize on their operational flexibility and deep local market understanding to develop specialized products. These smaller manufacturers establish strong consumer loyalty through product differentiation and market segmentation strategies. This competitive dynamic generates opportunities in hybrid product categories that incorporate traditional dark beer characteristics while addressing evolving consumer preferences, particularly in the development of low-alcohol variants with sophisticated flavor profiles.

The competitive landscape continues to evolve through market entrants implementing technological innovations and alternative business models. Direct-to-consumer e-commerce platforms enable smaller manufacturers to establish independent distribution channels and direct consumer relationships. Contract brewing services reduce market entry barriers by providing production capabilities to brand-focused enterprises. Additionally, technological advancements in brewing processes facilitate enhanced flavor development and product standardization. Diageo demonstrates the effective use of technology in market expansion, achieving 1% organic net sales growth in the first half of fiscal 2025 despite inflationary pressures. The company positions Guinness in the premium segment while developing zero-alcohol alternatives to meet the demands of health-conscious consumers.

Black Beer Industry Leaders

-

Diageo plc

-

Heineken Holding N.V

-

Anheuser-Busch InBev SA/NV

-

Allagash Brewing Co.

-

Kirin Holdings Company, Limited.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Schlafly Beer introduced its British Pub Pack spring variety pack, featuring four traditional British-style brews. The 12-pack includes Schlafly's flagship Pale Ale, along with Scotch Ale, English IPA, and Northern English Brown Ale.

- January 2025: Yuengling expanded into Illinois in early 2025, introducing its full portfolio, including the popular dark brew Black & Tan, to bars and retail outlets. The move marked its 28th state entry and continued its Midwest growth strategy. This followed expansions into Kansas, Missouri, and Oklahoma through its partnership with Molson Coors.

- May 2024: Diageo invested EUR 100 million to decarbonize its St. James's Gate brewery in Dublin 8. The investment supported the company's objective to achieve net-zero carbon emissions at the site and improve its energy and water efficiency, aiming to establish it as one of the world's most efficient breweries by 2030.

- September 2023: Nigerian Breweries launched Goldberg Black, a dark lager with 6% ABV. The beer is brewed with dark malt and contains caramel notes, providing a distinct taste and aroma. The launch represents the company's efforts to expand its product portfolio and meet Nigerian consumer preferences.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global black beer market as every dark-hued style such as stout, porter, schwarzbier, and other roasted-malt variants that leave the brewery in bottles, cans, or kegs and reach consumers through on-trade or off-trade channels. Values are calculated at brewer-gate prices in constant 2024 US dollars, according to Mordor Intelligence analysts.

Scope exclusion: Non-alcoholic malt beverages and home-brew batches fall outside this boundary.

Segmentation Overview

-

By Product Type

- Ale

- Sorghum

- Wheat Beer

-

By End User

- Men

- Women

-

By Packaging Type

- Bottles

- Cans

- Others

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Specialty/Liquor Stores

- Others Off Trade Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with brew-masters, aluminum-can suppliers, distributors, and grocery buyers across North America, Europe, and Asia-Pacific. Their feedback confirmed channel splits, premiumization rates, and festival-linked demand swings that raw data alone cannot expose.

Desk Research

We collected production, trade, and consumption series from Eurostat beverage tables, the United States Alcohol and Tobacco Tax and Trade Bureau, UN Comtrade HS-2203 flows, and the Brewers Association craft output survey. Our team then drew price clues from company 10-Ks, press releases, and news captured on Dow Jones Factiva while D&B Hoovers snapshots mapped brewer footprints. Extra context from the World Packaging Organization and national statistics offices helped us reconcile packaging shifts and excise changes. These references are illustrative; many other open sources informed the baseline.

Market-Sizing & Forecasting

We start with a top-down split of global beer output by applying verified dark-beer penetration ratios and then run a selective bottom-up check that rolls stout and porter shipment samples against average selling prices. Variables such as per-capita beer intake, craft brewery count, can share, excise duty moves, and tourist flows feed a multivariate regression that projects demand to 2030. Weighted averages from neighboring markets bridge any shipment gaps, and every step is logged for reproducibility.

Data Validation & Update Cycle

Outputs travel through three layers of variance checks, peer comparison, and senior analyst review. We refresh models each year and issue interim tweaks whenever tax hikes, regulation, or major mergers materially shift outlooks so clients receive a live view.

Why Mordor's Black Beer Baseline Commands Credibility

Published estimates often diverge because firms choose narrower geographies, drop on-trade kegs, or freeze prices before rolling forecasts, while our yearly recalibration and globally harmonized scope reduce those pitfalls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 67.65 B (2025) | Mordor Intelligence | - |

| USD 31.47 B (2025) | Regional Consultancy A | Tracks retail bottles and cans only and omits keg volumes |

| USD 25.92 B (2024) | Trade Journal B | Uses a craft brewer survey with limited regional reach |

| USD 51.61 B (2030) | Global Consultancy C | Applies fixed average price and rolls forward with a straight CAGR |

These contrasts show how Mordor's disciplined source mix, clear scope selection, and timely refresh give decision-makers a transparent and dependable baseline.

Key Questions Answered in the Report

What is the current size of the dark beer market?

The dark beer market is worth USD 70.37 billion in 2026, with expectations to reach USD 85.72 billion by 2031.

Which product type leads the dark beer category?

Ale dominates, holding 59.17% market share in 2025 thanks to its rich heritage and broad flavor range.

Which region is growing the fastest for dark beer?

Asia-Pacific posts the highest forecast CAGR at 4.96% between 2026 and 2031, driven by rising middle-class demand and localized craft offerings.

How are sustainability efforts influencing dark beer packaging?

Lightweight glass, bio-based carrier handles, and water-efficient brewing lines are propelling bottle growth at a 4.9% CAGR while meeting circular-economy targets.

Page last updated on: