Root Beer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

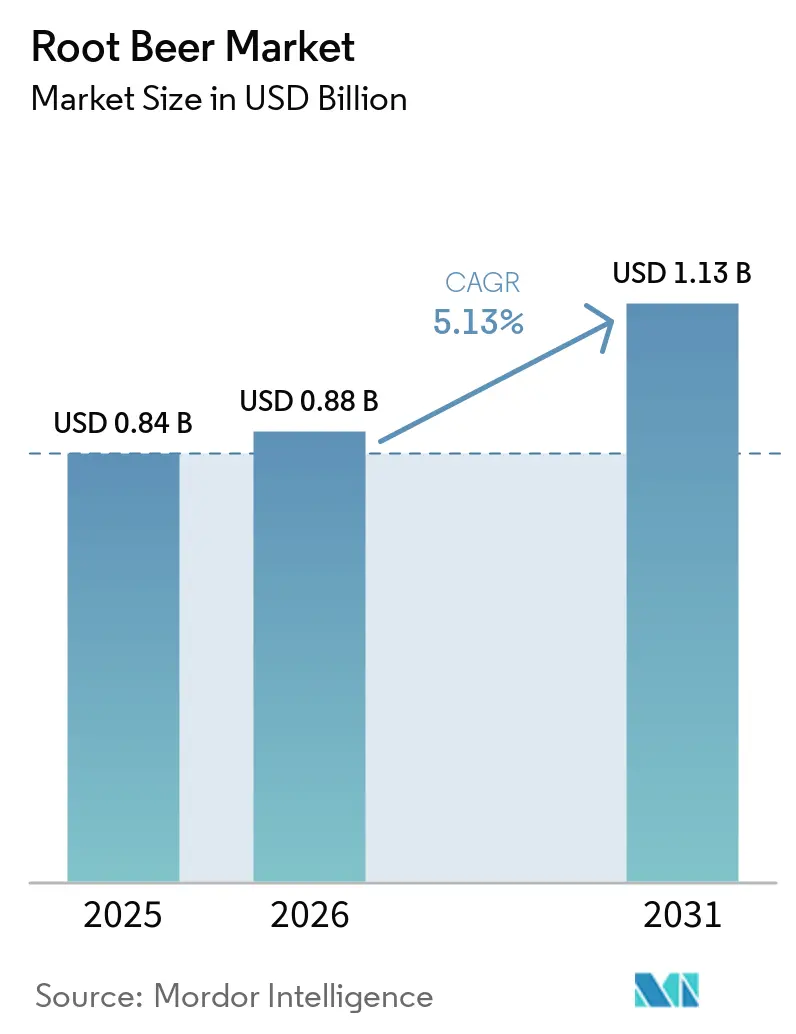

| Market Size (2026) | USD 0.88 Billion |

| Market Size (2031) | USD 1.13 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Root Beer Market Analysis by Mordor Intelligence

The root beer market was valued at USD 0.84 billion in 2025, reached USD 0.88 billion in 2026, and is projected to grow to USD 1.13 billion by 2031, registering a compound annual growth rate (CAGR) of 5.13% during the forecast period of 2026–2031. The market benefits from root beer's distinctive combination of creamy sweetness, herbal flavors, vanilla undertones, and nostalgic appeal, which continues to attract consumers across various age groups. Market growth is further driven by shifting consumer preferences toward premium, craft-style, and clean-label beverages made with natural ingredients, such as cane sugar and botanical extracts, while minimizing artificial additives. Additionally, innovation in flavored variants, limited-edition products, and premium packaging is appealing to younger consumers seeking unique and experiential beverage options.

Key Report Takeaways

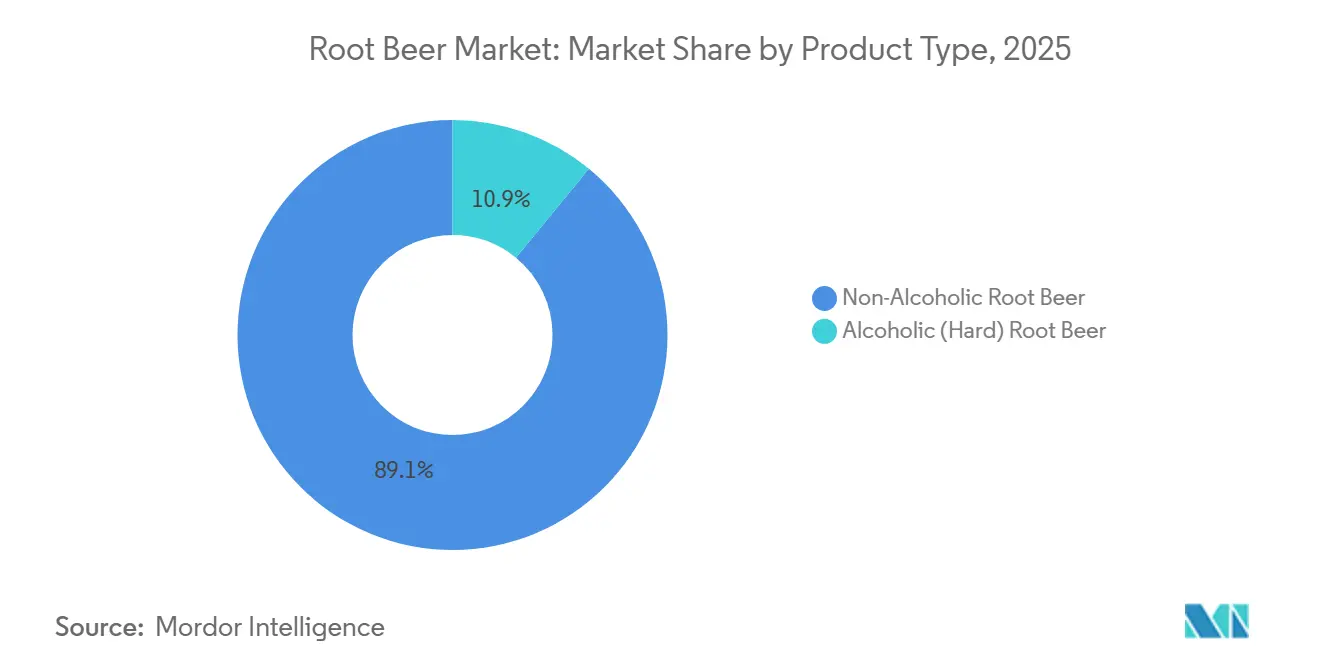

- By product type, non-alcoholic formats held 89.06% of the root beer market share in 2025, while hard root beer is forecast to accelerate at a 5.56% CAGR through 2031.

- By flavor, original recipes commanded 72.12% share of the root beer market size in 2025, whereas flavored variants are projected to expand at 6.32% CAGR over 2026-2031.

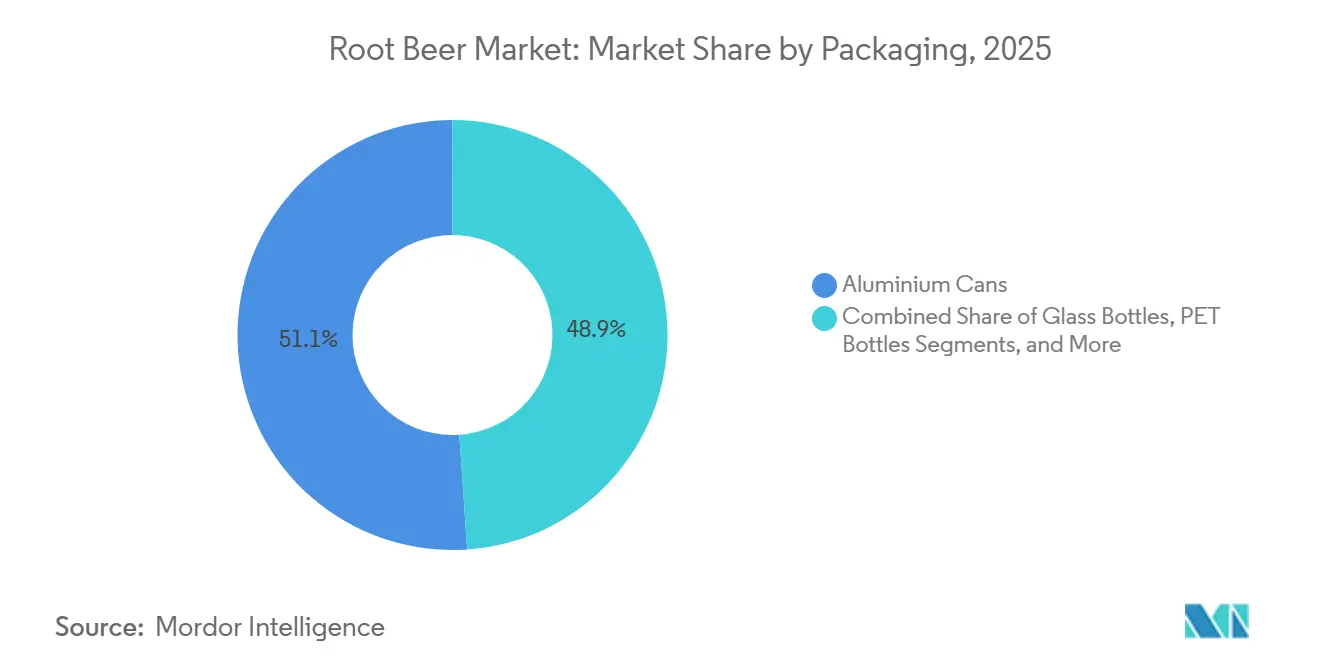

- By packaging, aluminum cans led with 51.09% of 2025 revenue; PET bottles record the highest forecast CAGR at 6.81% to 2031.

- By distribution channel, off-trade outlets accounted for 77.98% of 2025 sales, yet on-trade venues are advancing at 5.85% CAGR to 2031.

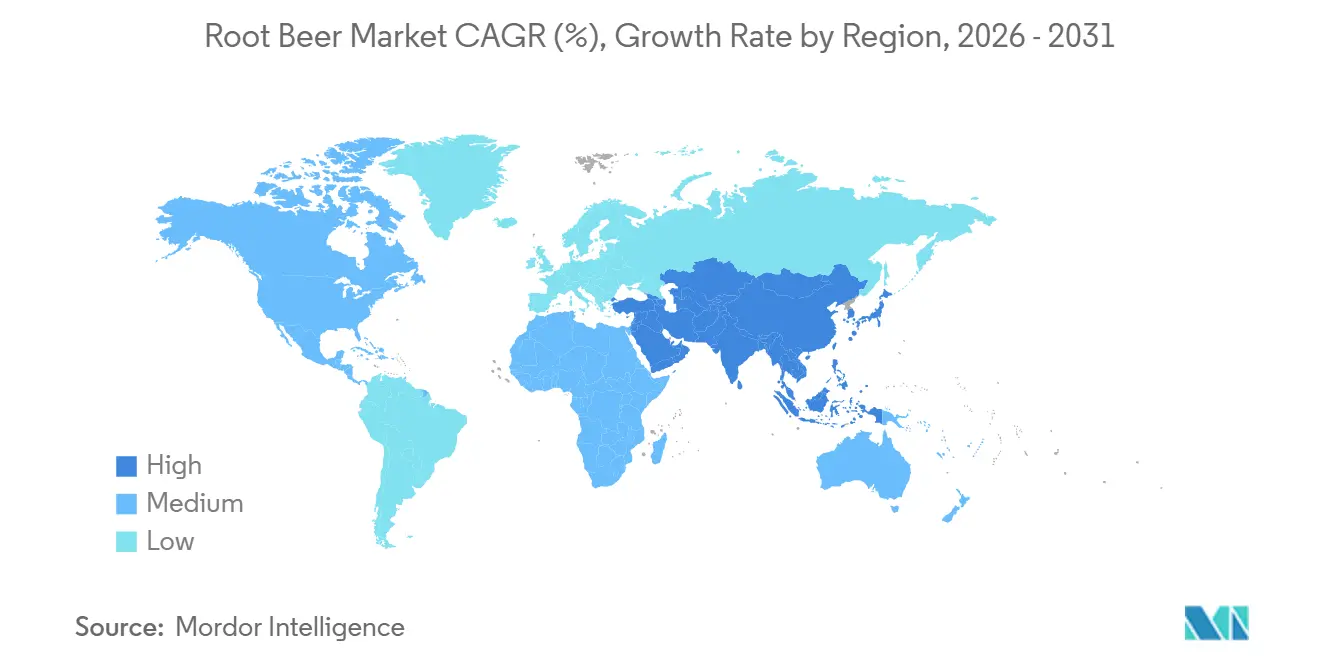

- By geography, North America captured 62.32% share in 2025, but Asia-Pacific is the fastest-growing region at 6.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Root Beer Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in craft and artisanal root beer | +1.2% | North America, Europe (Germany, United Kingdom), Asia-Pacific (Japan, South Korea) | Medium term (2-4 years) |

| Increasing preference for unique and bold flavors | +0.9% | Global, with concentration in North America and urban Asia-Pacific markets | Short term (≤ 2 years) |

| Growth in premiumization and natural ingredient claims | +1.5% | North America, Europe, select Asia-Pacific (Japan, Australia) | Long term (≥ 4 years) |

| Rising health and wellness consciousness | +1.1% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Growing social media and influencer-led beverage trends | +0.7% | Global, youth-skewed markets (Gen Z, millennials in urban centers) | Short term (≤ 2 years) |

| Popularity of root beer floats and dessert pairings | +0.6% | North America, emerging in Asia-Pacific foodservice | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth in Craft and Artisanal Root Beer

The increasing demand for craft and artisanal beverages is a significant factor driving the global root beer market. Consumers are showing a preference for premium soft drinks that emphasize authentic production methods, natural ingredients, and unique brand narratives. Craft root beer manufacturers are capturing market share by focusing on small-batch production, traditional brewing methods, locally sourced ingredients, and heritage-focused branding—areas where large-scale brands often face challenges in replicating at a mass-market level. For example, Sprecher Brewing Company employs a fire-brewing process using direct flame instead of steam, which enhances caramelized flavor profiles and reinforces a handcrafted product identity. Additionally, the company uses raw Wisconsin honey as its primary sweetener, rather than cane sugar or high-fructose corn syrup, further emphasizing its commitment to natural ingredients and regional authenticity.

Increasing preference for unique and bold flavors

The increasing consumer preference for unique and bold flavor profiles is a significant driver of the global root beer market. Consumers are shifting away from traditional cola and citrus soft drinks, seeking beverages with differentiated taste experiences. Root beer appeals to this demand with its distinctive combination of creamy sweetness, herbal notes, vanilla undertones, and spiced complexity. This makes it particularly attractive to consumers looking for adventurous and memorable refreshment options. Younger demographics, in particular, are showing a growing interest in beverages that offer novelty, indulgence, and a strong flavor identity. This trend is encouraging brands to innovate beyond conventional formulations. For example, in August 2025, REDCON1 introduced JOLT Root Beer, which features a bold root beer flavor, 200 mg of caffeine, and a sugar-free formulation. Such innovations highlight how brands are modernizing root beer by incorporating functional benefits and delivering intense flavor experiences.

Growth in premiumization and natural ingredient claims

The growing consumer preference for premium beverages and clean-label products is a key factor driving the global root beer market. Consumers are increasingly prioritizing beverage quality, opting for products made with natural sweeteners, botanical extracts, real spices, and familiar ingredients instead of conventional mass-market formulations. This trend has led root beer manufacturers to position their products as premium options, emphasizing enhanced taste authenticity, small-batch production, glass bottle packaging, and transparent ingredient lists. Consequently, premium root beer is gaining traction among consumers willing to pay a higher price for superior flavor, artisanal quality, and formulations perceived as healthier. Claims highlighting natural ingredients, such as cane sugar, honey, vanilla extract, herbal blends, the absence of artificial colors, high-fructose corn syrup, and preservatives, are further enhancing the appeal of the category among health-conscious consumers.

Rising health and wellness consciousness

Increasing health and wellness awareness is a significant factor influencing the global root beer market. Consumers are progressively seeking beverages that support lower sugar intake, calorie management, and healthier lifestyle objectives. Concerns about obesity, diabetes, and excessive sugar consumption are driving a shift away from traditional full-sugar carbonated drinks toward diet, zero-sugar, reduced-calorie, and naturally sweetened alternatives. In response, root beer manufacturers are expanding their healthier product offerings while preserving the familiar taste profiles that consumers prefer. This focus on wellness-driven innovation is enabling the category to attract health-conscious consumers and maintain long-term demand. For example, according to the Centers for Disease Control and Prevention (CDC), in 2024, all states in the United States reported an adult obesity prevalence of 25% or higher, indicating that at least one in four adults was affected [1]Source: Centers for Disease Control and Prevention (CDC), "Adult Obesity Prevalence Maps", cdc.gov. This growing public health concern is fueling demand for sugar-free, low-calorie, and health-oriented beverage options.

Restraints Impact Analysis of Root Beer Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from broader soft drink categories | -1.3% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Health regulations and sugar content scrutiny | -0.9% | North America, Europe, Latin America (Mexico), select Asia-Pacific | Long term (≥ 4 years) |

| Higher costs for premium and natural formulations | -0.6% | Global, cost pressure most acute in emerging markets | Short term (≤ 2 years) |

| Relatively small addressable consumer base | -0.4% | Global, niche appeal limits mass-market penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from broader soft drink categories

Competition from broader soft drink categories serves as a significant restraint on the global root beer market. Consumers have access to a wide range of beverage alternatives that enjoy stronger mainstream recognition and greater marketing support. Root beer directly competes with cola drinks, lemon-lime sodas, fruit-flavored carbonates, sparkling water, iced tea, sports drinks, energy drinks, kombucha, and functional beverages. Many of these alternatives benefit from higher shelf presence and more frequent promotional activities. This intense competition can hinder root beer’s ability to attract new consumers, particularly in markets where the category remains niche or less familiar. Additionally, broader soft drink categories often capitalize on faster flavor innovation cycles, wellness-focused positioning, and stronger alignment with evolving consumer preferences, such as hydration, energy, immunity, and low-sugar lifestyles.

Health regulations and sugar content scrutiny

Health regulations and increased scrutiny over sugar content serve as significant restraints for the global root beer market. Many traditional root beer products fall within the carbonated soft drink category, which is often associated with high sugar and calorie content. Governments, public health organizations, and consumer advocacy groups are intensifying efforts to reduce sugar consumption through measures such as labeling requirements, sugar taxes, advertising restrictions, and reformulation targets. These initiatives pose compliance challenges for manufacturers and exert pressure on conventional root beer formulations that depend on sweet taste profiles. Additionally, rising consumer awareness of obesity, diabetes, and other lifestyle-related health concerns is prompting buyers to closely examine nutritional labels and limit purchases of sugary beverages. This trend may reduce demand for regular root beer variants and drive a shift toward zero-sugar, diet, or alternative beverage options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Root Beer Market Segment Analysis

By Product Type:

Hard Root Beer Gains as Adult Substitution AcceleratesNon-Alcoholic Root Beer accounted for 89.06% of the global root beer market share in 2025, primarily due to its broad mass-market appeal, widespread consumer accessibility, and steady demand within the carbonated soft drinks category. This segment drives growth by catering to all age groups and various consumption occasions, making it more versatile and widely accepted compared to alcoholic variants. Its caffeine-free and alcohol-free attributes encourage frequent consumption, as it can be enjoyed as a daily refreshment without the restrictions associated with alcoholic beverages. The familiar sweet, creamy, and herbal flavor profile fosters repeat purchases among loyal consumers while attracting new buyers seeking alternatives to traditional cola drinks.

Alcoholic Hard Root Beer is projected to grow at a 5.56% CAGR through 2031, driven by increasing consumer interest in flavored alcoholic beverages that provide a distinct alternative to traditional beer, cider, and ready-to-drink products. This segment is gaining traction by combining the familiar sweet, creamy, and spiced flavor of classic root beer with alcoholic content, appealing to consumers seeking unique and indulgent drinking experiences. Younger adult consumers, in particular, are drawn to beverages with smoother taste profiles and lower bitterness compared to conventional beers, supporting the adoption of hard root beer. The segment also benefits from the premiumization trend, as consumers show a growing willingness to explore craft-inspired and specialty alcoholic beverages with distinctive flavor profiles.

By Flavor:

Dessert Variants Drive Trial and Limited-Time VelocityOriginal or Traditional Root Beer accounted for 72.12% of the global root beer market share in 2025, driven by strong consumer familiarity, authentic taste appeal, and its association with the classic identity of the category. This segment continues to lead as many consumers favor its signature flavor profile, characterized by creamy sweetness, vanilla notes, herbal undertones, and mild spice complexity, which define the traditional root beer experience. Long-term brand loyalty and repeat purchasing behavior remain robust, as consumers often associate original root beer with nostalgia, comfort, and trusted quality. Additionally, its broad appeal across multiple age groups makes it the most universally accepted flavor compared to experimental or niche variants.

Flavored Root Beer is projected to grow at a 6.32% CAGR through 2031, fueled by increasing consumer demand for product variety, taste innovation, and personalized beverage experiences. This segment is gaining momentum as consumers seek alternatives to traditional soft drink flavors and show a growing interest in experimenting with new taste combinations. Flavor-infused root beer varieties, including vanilla-enhanced, cherry, caramel, berry, spicy, and seasonal editions, are attracting younger consumers and trend-driven buyers seeking novelty. The segment also benefits from the premiumization trend, where unique and limited-edition flavors generate excitement, encourage trial purchases, and support higher-value sales.

By Packaging:

Light weighting and Sustainability Propel PET GrowthAluminium cans accounted for 51.09% of the global root beer packaging market share in 2025, driven by their convenience, sustainability, and efficiency in beverage supply chains. These cans are lightweight, durable, portable, and easy to chill, making them a preferred choice for single-serve consumption, outdoor events, travel, and on-the-go lifestyles. Their stackable shape and compact design enhance transportation, warehousing, and retail shelf efficiency, enabling brands to optimize logistics and merchandising. A key factor supporting the segment's growth is the increasing consumer and brand preference for environmentally responsible packaging solutions. According to the International Aluminium Institute, aluminium achieved the highest global recycling rate at 75% in 2025, solidifying its position as a circular packaging material [2]Source: International Aluminium Institute, "Global Aluminium Can Recycling Reaches 75%, Marking Major Step Toward Circular Economy", international-aluminium.org.

PET bottles are projected to grow at a 6.81% CAGR through 2031, fueled by rising demand for convenient, resealable, and multi-serve beverage packaging formats. These bottles are practical for consumers who value portability and the flexibility to consume beverages across multiple occasions rather than in a single sitting. Their lightweight design facilitates easy carrying, storage, and transportation, aligning with the growing trend of on-the-go consumption. PET bottles are also popular for family-size and value-pack formats, appealing to households seeking bulk purchases and pantry stocking convenience. Additionally, their transparent packaging allows consumers to visually assess product quality, carbonation levels, and fill volume, positively influencing purchasing decisions.

By Distribution Channel:

Off-Trade Dominance ContinuesOff-trade distribution accounted for 77.98% of global root beer sales in 2025, driven by consumer preference for convenient retail purchasing, broader product accessibility, and increasing at-home beverage consumption. This segment dominates as consumers frequently purchase root beer through supermarkets, hypermarkets, specialty stores, convenience outlets, and online retail platforms, where they can compare brands, flavors, pack sizes, and pricing in one location. Additionally, the segment benefits from the rapid growth of e-commerce and digital grocery channels, which offer doorstep delivery, subscription services, and access to niche or premium root beer varieties. For example, according to Eurostat, 11.74% of individuals made an online purchase of food or beverages in 2024, underscoring the growing importance of digital retail in beverage sales [3]Source: Eurostat, "Share of people that bought food or beverages online in Germany", ec.europa.eu.

On-trade channels are projected to grow at a 5.85% CAGR through 2031, fueled by increasing out-of-home beverage consumption and rising demand for experiential dining and social drinking occasions. This segment is gaining traction as consumers increasingly visit restaurants, cafés, diners, bars, entertainment venues, and quick-service outlets for beverages consumed on-site. Root beer is benefiting from this trend as foodservice operators expand beverage menus to include differentiated soft drinks and specialty options, providing alternatives to mainstream cola products. The segment is further supported by the growing popularity of premium fountain beverages, craft-style soft drinks, and nostalgic beverage offerings that enhance the overall customer experience.

Geography Analysis

North America Root Beer Market

North America is projected to retain 62.32% of the global root beer market share in 2025, maintaining its leadership position due to strong consumer familiarity, a rich heritage appeal, and an established consumption culture for root beer products. The region benefits from high product availability across retail and foodservice channels, diverse flavor portfolios, and robust demand for both mainstream and premium offerings. Frequent household purchases, strong brand loyalty, and widespread availability in restaurants, diners, and convenience outlets continue to reinforce its market dominance. Additionally, innovation in zero-sugar, craft-style, and hard root beer variants is contributing to market maturity and value growth in the region.

APAC Root Beer Market

The Asia-Pacific region is forecast to grow at a 6.96% CAGR through 2031, emerging as the fastest-growing regional market. This growth is driven by rising urbanization, increasing exposure to international beverage trends, and growing demand for novel carbonated drinks. Younger consumers are showing heightened interest in imported and premium beverages with unique flavor experiences, creating favorable conditions for root beer expansion. The rapid development of modern retail, convenience stores, digital commerce, and food delivery ecosystems is improving product accessibility across the region. Furthermore, increasing experimentation with Western-style beverages, coupled with expanding middle-class lifestyle preferences and demand for ready-to-drink refreshments, is expected to accelerate market growth.

EMEA and South America Root Beer Market

Europe is experiencing moderate growth, driven by rising demand for craft, artisanal, and sustainable beverage products. Consumers are increasingly attracted to premium soft drinks made with natural ingredients and distinctive flavor profiles. Interest in niche American-style beverages and clean-label formulations is also supporting regional demand. South America and the Middle East and Africa remain comparatively smaller markets due to lower category awareness and limited mainstream penetration. However, gradual expansion through modern retail channels, tourism, and premium beverage imports is creating selective long-term opportunities in these regions.

Competitive Landscape

The global root beer market is moderately fragmented, featuring a mix of multinational beverage corporations, heritage root beer brands, craft soda producers, and regional specialty manufacturers. These players compete across both mainstream and premium price tiers. Large-scale companies leverage extensive production capabilities, strong retail partnerships, and broad distribution networks, while smaller brands focus on authenticity, niche flavor profiles, and premium ingredient positioning. Key competitive factors include flavor consistency, packaging innovation, shelf visibility, pricing strategies, and fostering brand loyalty in a category heavily influenced by repeat purchasing behavior.

Major companies in the market include PepsiCo, Inc., The Coca-Cola Company, The Dad’s Root Beer Company, Reed’s Inc., and Sprecher Brewing Company. These players offer diversified product portfolios, including regular, diet, zero-sugar, craft-style, and flavored root beer variants. To enhance consumer reach, brand owners are increasingly investing in packaging modernization, digital marketing campaigns, nostalgic branding themes, and expanding availability through supermarkets, convenience stores, foodservice outlets, and online retail platforms.

Significant opportunities exist in functional positioning, adult non-alcoholic social occasions, and geographic expansion. Manufacturers can tap into the growing demand for beverages with reduced sugar, natural botanicals, probiotics, or added wellness attributes to attract health-conscious consumers. Additionally, there is potential in premium non-alcoholic social beverages designed for gatherings, nightlife, and moderation-focused lifestyles, catering to consumers seeking sophisticated alcohol-free alternatives. Emerging markets with low penetration offer long-term growth potential through localized flavor adaptations, improved retail distribution, and targeted awareness-building initiatives to introduce root beer to new consumer segments.

Root Beer Industry Leaders

-

PepsiCo, Inc.

-

The Coca-Cola Company

-

The Dad’s Root Beer Company

-

Reed’s Inc.

-

Sprecher Brewing Company

- *Disclaimer: Major Players sorted in no particular order

Root Beer Market Companies Covered in this Report

- PepsiCo, Inc.

- The Coca-Cola Company

- Keurig Dr Pepper (IBC, Hires)

- The Dad's Root Beer Company

- Reed's Inc. (Virgil's)

- Sprecher Brewing Company

- Frostie Enterprises

- White Rock Beverages (Sioux City)

- Hank's Gourmet Beverages

- Boylan Bottling Co.

- Bundaberg Brewed Drinks

- Maine Root Handcrafted Beverages

- Olipop Inc.

- Enjoy Beer LLC (Abita Brewing)

- Appalachian Brewing Co.

- Orca Beverages (Thomas Kemper)

- National Beverage Corp. (Faygo)

- Nickel Brook Brewing Co.

- Dog n Suds LLC

- Cariboo Brewing

Recent Industry Developments in Root Beer Market

- February 2026: A&W unveiled its latest offerings, including the Root Beer Float and the Zero Sugar Root Beer Float, both of which are available in Original Cola and Cherry Vanilla flavors.

- February 2026: Sprecher Brewing Company has partnered with Ubisoft to launch a limited-edition 16-ounce root beer can in celebration of Assassin’s Creed Shadows. This collaboration features unique artwork and includes an exclusive in-game reward, appealing to fans of the franchise.

- August 2025: Mitra9, a company in the functional beverage market, launched soda-inspired beverages, including root beer. The product is described as smooth, rich, and subtly herbal, offering a classic flavor with a refreshing twist.

Global Root Beer Market Report Scope

Root beer is a sweet, non-alcoholic carbonated soft drink made from herbs, bark, and plant roots, most notably safrole-free sassafras. The root beer market is segmented by product type, flavor, packaging, distribution channel, and geography. Based on product type, the market is segmented into alcoholic (hard) root beer and non-alcoholic root beer. Based on flavor, the market is segmented into original/traditional root beer and flavored root beer. Based on packaging, the market is segmented into aluminium cans, glass bottles, PET bottles, and others. Based on distribution channel, the market is segmented into on-trade and off-trade. The off-trade segment is further categorized into supermarkets and hypermarkets, specialty stores, online retail stores, and others. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (liters) for all the mentioned segments.

Segmentation Overview

| Alcoholic (Hard) Root Beer |

| Non-Alcoholic Root Beer |

| Original/Traditional Root Beer |

| Flavored Root Beer |

| Aluminium Cans |

| Glass Bottles |

| PET Bottles |

| Others |

| On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Type | Alcoholic (Hard) Root Beer | |

| Non-Alcoholic Root Beer | ||

| By Flavor | Original/Traditional Root Beer | |

| Flavored Root Beer | ||

| By Packaging | Aluminium Cans | |

| Glass Bottles | ||

| PET Bottles | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How large will the root beer market be by 2031?

The root beer market size is forecast to reach USD 1.13 billion by 2031, growing at a 5.13% CAGR from 2026 to 2031.

Which product segment is expanding fastest?

Alcoholic hard root beer is projected to post a 5.56% CAGR through 2031 as adults trade mainstream beer for nostalgic flavored options.

What share do non-alcoholic SKUs hold today?

Non-alcoholic offerings controlled 89.06% of 2025 revenue, underlining their dominance within the root beer market.

Which region will add the most incremental sales?

Asia-Pacific is expected to deliver the highest regional CAGR at 6.96%, aided by e-commerce expansion and premium craft imports.

Page last updated on: