Flavor Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 24.96 Billion |

| Market Size (2031) | USD 34.65 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flavor Market Analysis by Mordor Intelligence

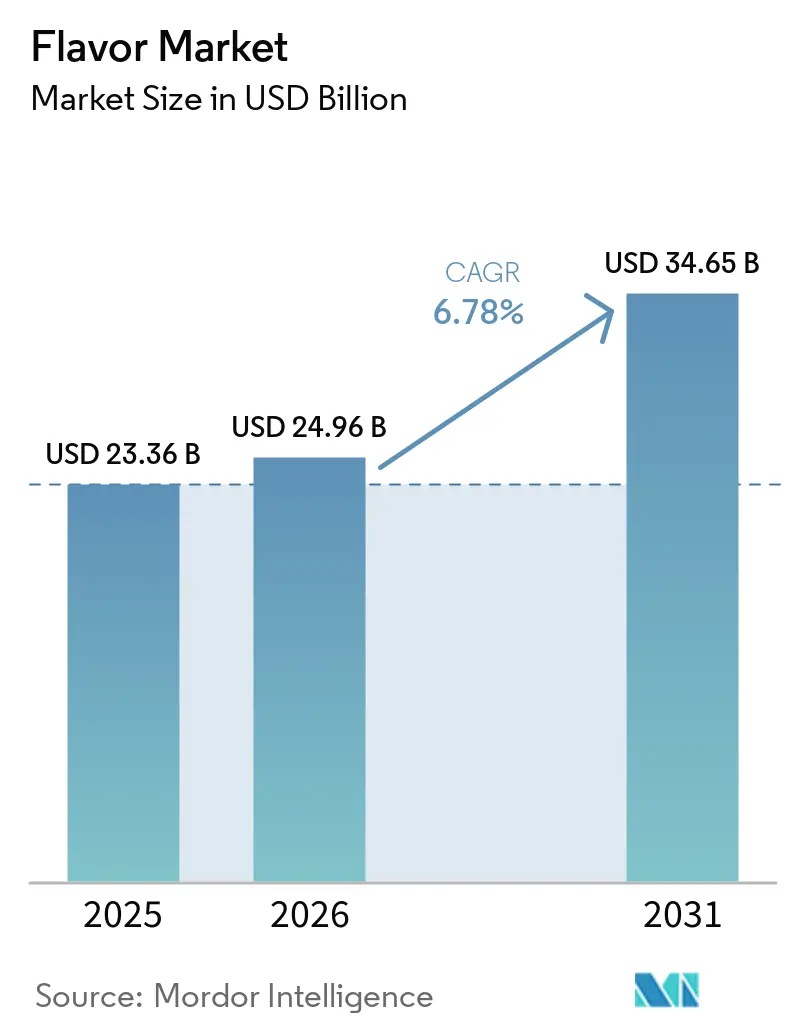

The flavors market size was valued at USD 23.36 billion in 2025 and estimated to grow from USD 24.96 billion in 2026 to reach USD 34.65 billion by 2031, at a CAGR of 6.78% during the forecast period (2026-2031). The flavors market is supported by continued packaged food growth in emerging economies, where modern retail, convenience food demand, and urban consumption patterns are expanding simultaneously. The flavors market is also benefiting from reformulation work focused on lower-sugar and lower-sodium products, as taste restoration now requires more specialized flavor systems than earlier product cycles. Precision fermentation is widening the supply base for selected flavor molecules, which matters in a business that has long depended on volatile crop-linked inputs and long sourcing chains. Plant-based foods, supplements, and oral care products are also expanding the flavors market beyond its traditional food role into applications where taste performance, masking, and stability carry greater value. At the same time, the flavors market remains shaped by raw material volatility and uneven regulatory rules across regions, which gives larger suppliers an advantage in sourcing, compliance, and contract execution.

Key Report Takeaways

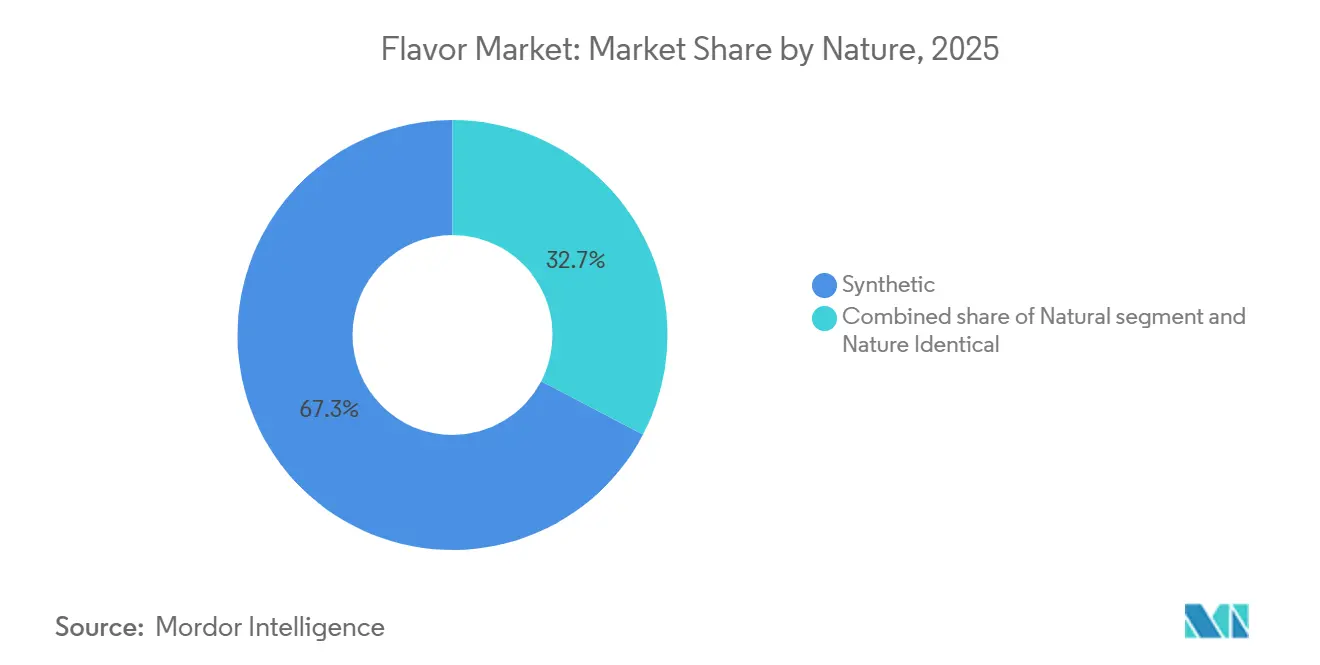

- By nature, synthetic flavors held 67.34% of the flavors market share in 2025, while natural flavors are anticipated to register the fastest CAGR of 7.67% during 2026-2031.

- By form, powder formats accounted for 65.36% of the flavors market size in 2025, while liquid formats are projected to grow at 6.75% CAGR through 2031.

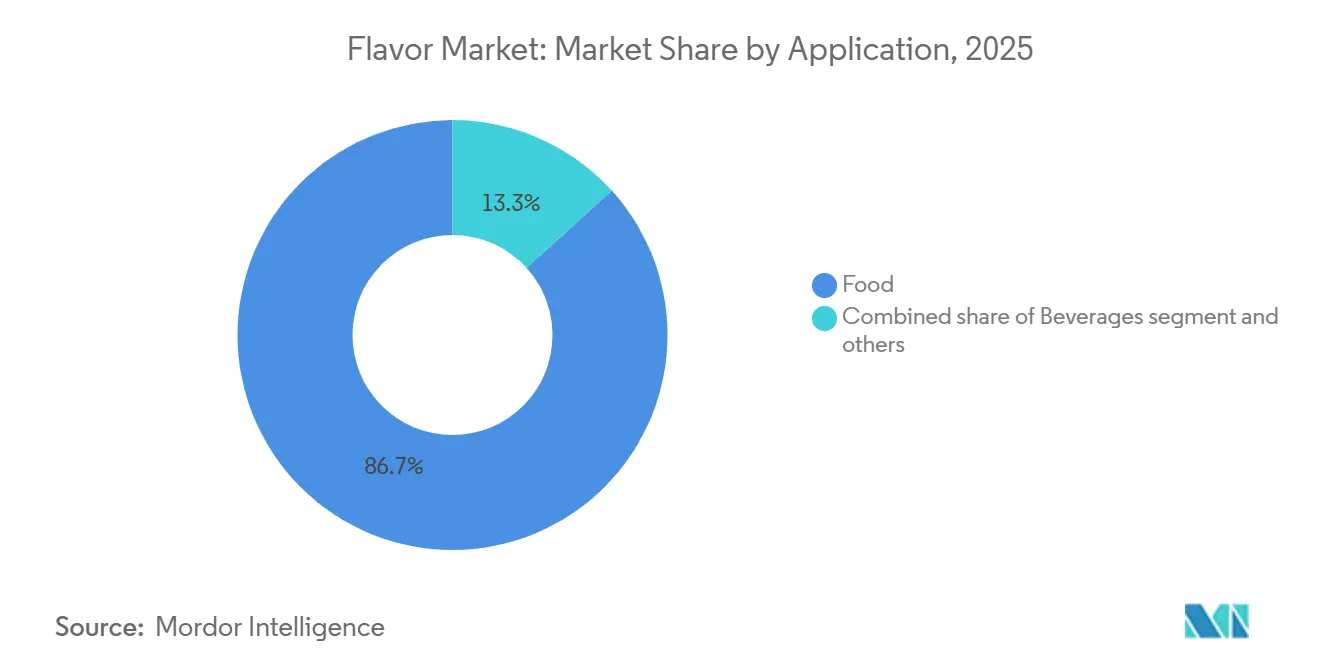

- By application, food accounted for 86.72% of 2025 revenue, but beverages are expected to grow the fastest at 9.19% through 2031.

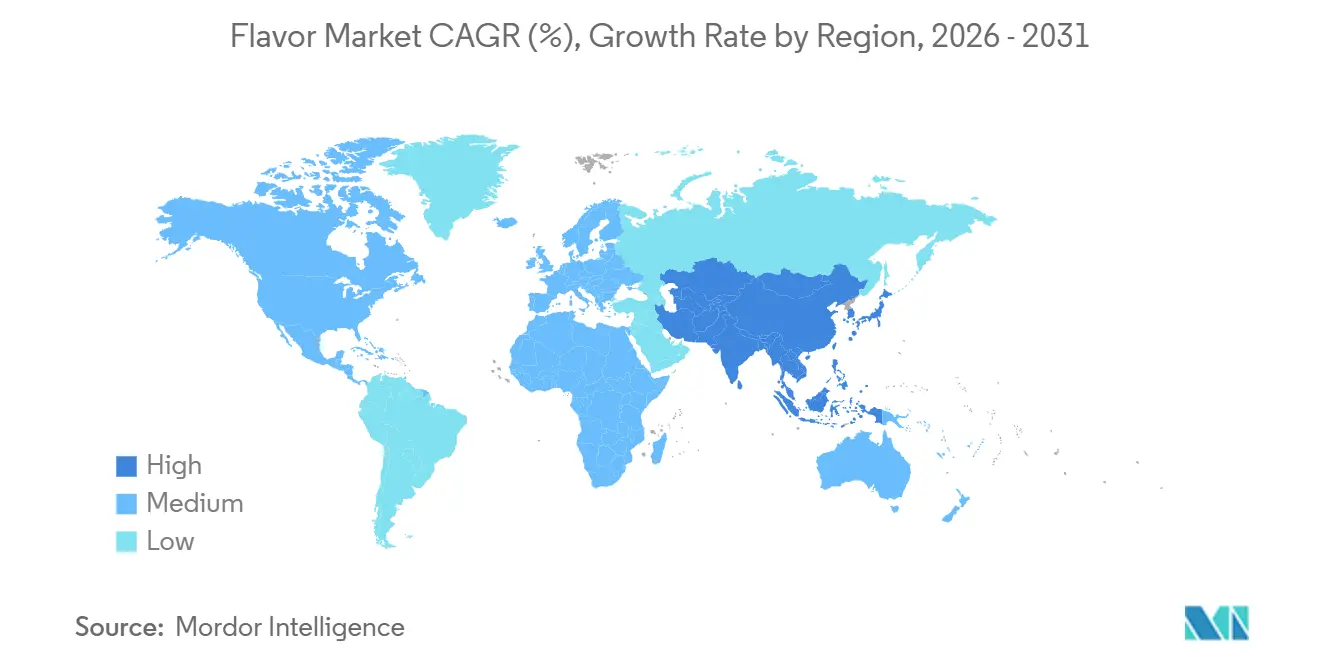

- By geography, the Asia Pacific captured 36.64% of the flavors market share in 2025 and is projected to grow at 7.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Flavor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Clean-Label, Natural Flavor Systems | +1.4% | Global, particularly North America, Europe, and Australia | Medium term (2-4 years) |

| Functional Reformulation Need in Low-Sugar and Low-Sodium Foods | +1.2% | North America and Europe, with spillover to Asia Pacific | Medium term (2-4 years) |

| Expansion of Palate-Masking Demand in Pharma and Supplements | +0.9% | Global, with early gains in North America, Western Europe, and Japan | Long term (≥ 4 years) |

| Growth of Plant-Based and Alternative Protein Formulations | +1.1% | Asia Pacific, North America, and Europe | Medium term (2-4 years) |

| Precision Fermentation and Biotech Flavor Scale-Up | +0.8% | Global, with early commercial gains in North America, the European Union, and Asia Pacific | Long term (≥ 4 years) |

| Cross-Category Adoption in Oral Care and Personal Care Formulations | +0.5% | North America, Europe, and Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label, natural flavor systems

Consumer resistance to long ingredient lists has made natural flavor reformulation a standard requirement in many retail channels rather than a premium positioning choice. More than 65% of new food launches in Europe during 2025 and 2026 carried a natural flavor or no artificial flavors claim, which kept clean-label work active across the flavors market, according to the European Food Safety Authority[1]Source: European Food Safety Authority, “Open Call for Food Additives/Food Flavourings Analytical, Use Level and Presence Data During the First Pilot Under the Monitoring Programme,” EFSA, efsa.europa.eu. Natural systems usually carry ingredient costs that are 30% to 60% higher than nature-identical options, so brand owners are being pushed to rethink pricing, product mix, and supplier selection. That cost pressure is helping vertically integrated suppliers win contracts because food manufacturers want tighter control over extraction, traceability, and audit readiness. Organic rules and natural flavor definitions add another layer of review, raising compliance costs and making scale more important in this part of the flavors market.

Functional reformulation need in low-sugar and low-sodium foods

Sodium-reduction mandates from public health authorities are driving sustained demand for flavor modulators that enhance saltiness perception without adding sodium. Kerry's TasteSense Salt platform has demonstrated sodium reductions of up to 40% in applications including processed meats and snacks, and in 2025, the company reported that its Americas division posted 3.7% volume growth, driven largely by customer-led sodium and sugar reformulation programs. Ajinomoto Health & Nutrition North America launched its Salt Answer platform in June 2025, offering up to 30% sodium reduction without taste compromise, an indicator that B2B demand for these solutions is reaching scale rather than remaining a specialty purchase[2]Source: Ajinomoto Health & Nutrition North America, “Ajinomoto Health & Nutrition North America, Inc. Launches New Product Platforms Tackling Top Food Formulation Challenges,” Ajinomoto Health & Nutrition North America, ajihealthandnutrition.com . What often goes unacknowledged is the flavor complexity penalty: removing sodium or sugar simultaneously degrades mouthfeel, sweetness linger, and umami perception, requiring 3-5 complementary flavor inputs to restore the original sensory architecture. This multiplier effect means that each reformulation cycle results in a larger flavor ingredient spend than a simple substitution would suggest.

Expansion of palate-masking demand in pharma and supplements

The dietary supplements market's transition toward gummies, chewable tablets, and ready-to-drink powders has created a structurally new demand stream for palate masking. Gummy supplements, which require effective masking of bitterness from vitamins, minerals, and botanicals, are among the fastest-growing delivery formats globally. The technical challenge is significant: masking agents must be stable across variable pH, temperature, and moisture conditions within a single product, without introducing off-notes of their own or compromising the bioavailability of active ingredients, according to the Royal Society of Chemistry. Flavor houses entering the pharmaceutical-grade masking segment face a distinct compliance regime: FDA guidance on pediatric formulation development requires palatability validation data, while EFSA applies its own safety assessment framework for flavoring substances in medicinal products. This regulatory bifurcation means that flavor systems cleared for food use are not automatically transferable to supplement or pharmaceutical matrices, creating a sustained investment requirement in product development that smaller, specialist flavoring companies are well positioned to serve.

Growth of plant-based and alternative protein formulations

Plant proteins, including soy, pea, canola, and faba bean, carry beany, earthy, and bitter off-notes arising from lipid oxidation, phenolic compounds, and Maillard reaction byproducts during processing. These off-notes remain the primary barrier to mainstream consumer adoption, outranking price and texture in repeat-purchase intent studies. dsm-firmenich's 2025 launch of ModulaSense, a receptor-based molecular masking system that targets specific off-notes in canola protein at the biological receptor level, represents a generational shift from broad-spectrum flavor masking to precision sensory engineering. The strategic implication is that flavor suppliers who achieve proprietary receptor-blocking formulations for a given protein substrate can lock in long-term supply contracts with alternative protein manufacturers, creating a switching-cost moat that commodity flavor systems cannot replicate. Advanced oxidation technologies, including ultrasound treatment and cold plasma processing, are being explored in the peer-reviewed literature as complementary deodorization techniques, but their industrial scalability remains constrained compared with chemical masking solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Fragmentation Across Food, Pharma, and Personal Care Claims | -0.8% | Global, concentrated in the European Union and North America | Long term (≥ 4 years) |

| Supply Volatility in Botanical, Citrus, and Vanilla Inputs | -0.7% | Global, most acute in Asia Pacific and North America | Short term (≤ 2 years) |

| High Reformulation Cost for Stable Flavor Performance Across Matrices | -0.6% | North America, Europe, and Asia Pacific | Medium term (2-4 years) |

| Label Sensitivity Around Artificial, Allergens, and Country-Specific Additives | -0.5% | Europe, North America, and Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory fragmentation across food, pharma, and personal care claims

The EU Flavoring Regulation (EC) No 1334/2008 has undergone three substantive amendments since January 2024, delisting specific flavoring substances, introducing usage restrictions, and adding new approved compounds, creating a rolling compliance burden for manufacturers operating across EU member states, according to the EU Commission[3]Source: European Commission, “Commission Regulation (EU) 2025/140 of 29 January 2025 Amending Annex I to Regulation (EC) No 1334/2008,” Eurlexa, eurlexa.com. In parallel, the FDA's GRAS self-affirmation pathway, state-level food safety legislation in California, and the EFSA's ongoing monitoring of flavor compound safety data create a multi-jurisdictional compliance matrix that no single product formulation can simultaneously satisfy without significant reformulation costs. The least-discussed dimension of this restraint is its effect on innovation timelines: a novel natural extract that clears EFSA assessment in the EU can take an additional 12-24 months and incur a high cost to receive FDA GRAS status in the US, effectively forcing flavor houses to sequence geographic launches and delay global scale-up for new flavor molecules. This asymmetry disadvantages smaller innovation-driven firms disproportionately relative to large incumbents with established regulatory affairs infrastructure.

Supply volatility in botanical, citrus, and vanilla inputs

The flavors market remains exposed to supply volatility in key natural raw materials such as citrus oils, botanicals, and vanilla. Citrus greening disease, an incurable bacterial infection spread by the Asian citrus psyllid, has affected orange production in major producing regions such as Brazil, Florida, and Mexico. Since Brazil accounts for nearly 70% of the global supply of concentrated orange juice, reduced orange yields have pushed citrus essential oil prices to multi-decade highs, increasing cost pressure on flavor houses and food manufacturers. Similarly, natural vanilla supply remains highly concentrated in Madagascar, which accounts for around 80% of global production, according to Livelihoods. This creates a significant single-origin supply risk, as cyclones, crop failures, or logistics disruptions can sharply reduce annual availability and trigger price spikes. While alternatives such as citrus extenders, precision-fermented vanillin, and nature-identical synthetic molecules are gaining commercial relevance, adoption in premium formulations remains gradual due to consumer expectations, regulatory considerations, and clean-label positioning. As a result, mid-sized food and beverage manufacturers face higher margin pressure during raw material price surges, as they often lack the pricing power to absorb costs or the flexibility to reformulate quickly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nature: Reformulation Pressure Reshapes a Synthetic-Dominated Market

Synthetic flavors accounted for 67.34% of the total value in 2025 and remained the largest segment because they offered lower cost variability, consistent batch-to-batch performance, and broad suitability across processed food applications. Their strength was most evident in packaged snacks, confectionery, and other high-volume categories, where manufacturers closely guard margins and prioritize repeatable sensory consistency. Nature-identical systems continued to serve as a middle ground in applications such as dairy, meat, and seafood, offering a familiar balance between functionality and labeling flexibility. This left the flavors market with a structure in which synthetic products still held the scale advantage, even as customer preferences continued to shift toward cleaner ingredient declarations.

Natural flavors are projected to grow at a 7.67% CAGR through 2031, making them the fastest-growing segment within this group. Retail standards in Europe and similar clean-label pressure in other developed markets are pushing more suppliers to accelerate natural reformulation before regulation forces them to do so. This shift is not happening evenly because natural systems still carry higher input costs and more demanding sourcing requirements. Even so, the direction is clear, and the flavors industry is moving toward a lower dependence on purely synthetic systems where brand positioning and label transparency matter most.

By Form: Powder Dominance Holds, While Liquid Formats Gain Speed

Powder flavors accounted for 65.36% of market value in 2025, which kept them firmly in the lead across the flavors market. Their position rested on long shelf life, lower transport and handling complexity, and a strong fit with dry mixes, seasoning blends, bakery applications, and confectionery. Powder also remained important in ambient products where moisture management and stability are critical for finished product quality. This gave the segment a practical advantage that was tied as much to manufacturing needs as to flavor design itself.

Liquid flavors are projected to grow at a 6.75% CAGR through 2031, supported by ready-to-drink beverages, liquid supplements, and dairy-alternative drinks that require fast-release, water-soluble systems. The faster pace reflects where new product activity is strongest rather than a broad erosion of powder demand. Other formats, such as encapsulated and emulsified systems, are also gaining relevance where controlled release, heat stability, or targeted masking are required. In the flavors industry, form selection is becoming increasingly tied to application performance and process conditions rather than simple cost comparisons.

By Application: Food Leads Value, While Beverage Demand Expands Faster

Food remained the largest application in 2025, with an 86.72% share, and continued to anchor the flavors market across bakery, confectionery, dairy, savory foods, and meat-related uses. These categories consume large volumes and create a steady base load for suppliers, especially where repeat formulations run across mass retail channels. Premiumization in food has also increased flavor spend in selected areas, particularly where heritage profiles are being updated for modern formulations. As a result, food continued to provide the value foundation even as new demand pockets emerged outside its traditional core.

Beverages are projected to grow at 9.19% CAGR through 2031, which makes them the fastest-growing application group in the flavors market. Functional drinks, botanical alcohol variants, and reformulated soft drinks are driving greater demand for proprietary flavor systems than for standard commodity aromatics. Pharmaceuticals and dietary supplements remain smaller in absolute value, but they command higher value per kilogram because stability, masking, and compliance requirements are stricter. Oral care adds another useful growth layer, widening the application mix even as food remains central.

Geography Analysis

North America and Europe were the second- and third-largest regional markets in 2025, respectively, with both regions playing a stronger role in high-value flavor innovation than in volume-led growth. In North America, demand remains supported by reformulation activity focused on sodium and sugar reduction, which continues to drive demand for taste restoration, flavor modulators, and masking systems. McCormick reported USD 2.89 billion in 2025 net sales from its Flavor Solutions business, while the segment’s operating profit increased by 9% year over year, reflecting resilient B2B demand from food and beverage manufacturers. Canada and Mexico are also becoming more important within the regional supply chain due to their production capabilities and strategic access to broader North American and Latin American markets. McCormick’s January 2026 decision to increase its stake in McCormick de Mexico to 75% for USD 750 million further highlights Mexico’s role as a long-term platform for expanding flavor solutions.

Europe remains one of the most regulated regions in the global flavors market, pushing suppliers to focus on compliance-led innovation, portfolio optimization, and continuous reformulation. EFSA’s active monitoring framework and the continued importance of Regulation (EC) No. 1334/2008 keep regulatory compliance central to the development and commercialization of both established and new flavoring substances. Germany, the United Kingdom, France, and the Netherlands remain key demand centers, supported by large food manufacturing bases, strong private-label activity, and continuous branded product innovation. As a result, Europe’s opportunity is less about volume expansion and more focused on premium, compliant, clean-label, and retailer-aligned flavor solutions. This keeps the region strategically important despite growth rates remaining below those of the Asia-Pacific.

Asia-Pacific held 36.64% of global market value in 2025 and is projected to grow at a 7.83% CAGR through 2031, making it the leading region in both scale and growth momentum. India is emerging as a major growth engine, as the expansion of its food processing sector is widening demand for flavors across packaged snacks, beverages, dairy, bakery, and convenience foods. According to the USDA, India’s food processing sector is projected to grow from USD 355 billion in 2024 to USD 535 billion by fiscal year 2026, supporting continued local capacity expansion by flavor and ingredient suppliers[4]Source: United States Department of Agriculture Foreign Agricultural Service, “India, Food Processing Ingredients Annual,” USDA FAS, fas.usda.gov. China also remains highly important, with its foodservice sector reaching USD 812 billion in 2025, reflecting a large downstream ecosystem that supports packaged food, beverage, and foodservice innovation. Meanwhile, Japan and South Korea are relatively mature markets, but they remain attractive due to premium flavor positioning, localized taste profiles, and strong demand for technically advanced solutions. South America, the Middle East, and Africa remain smaller in absolute market size, but they represent important white-space opportunities for flavor suppliers. Brazil and Mexico form the core demand base in Latin America, with Brazil serving as both a major consumption market and a key production hub. In the Middle East and Africa, Gulf countries, Nigeria, and South Africa are gaining importance as packaged food consumption, modern retail penetration, cold-chain infrastructure, and local food manufacturing continue to expand.

Competitive Landscape

The flavors market is moderately consolidated, and the leading group still consists of Givaudan SA, dsm-firmenich AG, International Flavors & Fragrances Inc., Symrise AG, and Kerry Group plc. Givaudan remained the largest participant in the source draft, with 2025 sales of CHF 7.47 billion, approximately USD 9.74 billion, and its Taste and Wellbeing division grew 2.4% on a like-for-like basis. Givaudan also entered its next planning cycle with medium-term annual organic sales growth targets of 4% to 6% for 2026 to 2030 and a global production footprint of 167 sites. That scale matters because large flavor houses can support customers across sourcing, regulatory review, application testing, and local production in a way smaller peers often cannot.

Recent portfolio actions show that large players are sharpening focus on higher-value flavor, nutrition, and formulation positions. In February 2026, dsm-firmenich announced the divestiture of its Animal Nutrition and Health business to CVC Capital Partners for an enterprise value of EUR 2.2 billion, which the source draft stated as approximately USD 2.34 billion, while retaining a 20% equity stake. In January 2026, McCormick completed a USD 750 million acquisition of an additional 25% stake in McCormick de Mexico, increasing its controlling interest to 75% and reinforcing its regional flavor solutions platform. In September 2025, BASF completed the sale of its Food and Health Performance Ingredients business to Louis Dreyfus Company, confirming that this activity no longer fit its core priorities. Moves like these show that competition in the flavors market is no longer only about size, because portfolio discipline and category focus are now shaping capital allocation as well.

There is still room for smaller players such as Robertet Group, Mane SA, and Bell Flavors & Fragrances to gain share through faster decision making and stronger category specialization. The most attractive openings remain in pharma-grade masking, fermentation-linked clean-label systems, South and Southeast Asian customer programs, and faster formulation turnaround for complex briefs. These areas favor suppliers that can move quickly while still meeting customer expectations on stability, labeling, and regulatory fit. As a result, the flavors market is likely to remain moderately consolidated rather than tightly concentrated, with the largest groups leading on scale while smaller firms continue to defend focused niches.

Flavor Industry Leaders

Givaudan SA

dsm-firmenich AG

International Flavors and Fragrances Inc.

Symrise AG

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: McCormick completed its USD 750 million acquisition of an additional 25% stake in McCormick de Mexico, raising its controlling interest to 75%. The transaction is intended to support McCormick's growth in flavor solutions in Mexico and Latin America, a region where the company generated approximately 39% of its 2025 net sales of USD 6.84 billion from non-US operations.

- December 2025: EvodiaBio raised EUR 6 million (approximately DKK 45 million) in a new funding round to accelerate growth in existing markets and expand into Asian markets. The Copenhagen-based industrial biotech company produces natural aromas through fermentation with significantly lower CO₂ emissions than traditional methods, and its technology is already in commercial use in the beverage industry.

- July 2025: dsm-firmenich launched ModulaSense, a receptor-based molecular masking range for plant-based protein off-notes, at IFT First 2025. The system targets bitterness, licorice notes, and astringency in canola protein (Vertis CanolaPro) at the receptor level and, in consumer testing, showed significantly higher flavor perception and purchase intent scores versus unmasked formulations.

- June 2025: Ajinomoto Health and Nutrition North America launched two flavor platform solutions: Salt Answer, delivering up to 30% sodium reduction without taste compromise, and Palate Perfect, designed to mask off-notes and reduce reliance on high-cost flavor ingredients in cost-sensitive reformulations.

Global Flavor Market Report Scope

Flavors are ingredients used to enhance, modify, or impart taste and aroma to food, beverages, pharmaceuticals, and other consumer products. The flavor market is segmented by nature, form, application, and geography. By nature, the market includes natural, synthetic, and nature-identical flavors. Based on form, the market is categorized into powder, liquid, and other forms. By application, the market covers food, beverages, pharmaceuticals, dietary supplements, oral care, and other applications. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market sizes and forecasts for each region. For each segment, market sizing and forecasts have been conducted on a value (USD) and volume (Tons) basis.

| Natural |

| Synthetic |

| Nature Identical |

| Powder |

| Liquid |

| Others |

| Food | Bakery and Confectionery |

| Dairy Products | |

| Meat and Seafood Products | |

| Snacks | |

| Sauces, Dressings, and Condiments | |

| Other Food Applications | |

| Beverages | Juices and Juice Concentrates |

| Functional Beverages | |

| Alcoholic Beverages | |

| Carbonated Soft Drinks | |

| Other Beverage Applications | |

| Pharmaceuticals | |

| Dietary Supplements | |

| Oral Care | |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| By Nature | Natural | |

| Synthetic | ||

| Nature Identical | ||

| By Form | Powder | |

| Liquid | ||

| Others | ||

| By Application | Food | Bakery and Confectionery |

| Dairy Products | ||

| Meat and Seafood Products | ||

| Snacks | ||

| Sauces, Dressings, and Condiments | ||

| Other Food Applications | ||

| Beverages | Juices and Juice Concentrates | |

| Functional Beverages | ||

| Alcoholic Beverages | ||

| Carbonated Soft Drinks | ||

| Other Beverage Applications | ||

| Pharmaceuticals | ||

| Dietary Supplements | ||

| Oral Care | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected size of the global flavors market by 2031?

The flavors market is forecast to reach USD 34.65 billion by 2031, rising from USD 24.96 billion in 2026 at a 6.78% CAGR over 2026-2031.

Which region leads global demand for flavors?

Asia Pacific led in 2025 with 36.64% of global value and is also projected to post the fastest regional growth at 7.83% CAGR through 2031.

Which type of flavor remains the largest today?

Synthetic flavors remained the largest type in 2025 with 67.34% share because they offer lower cost volatility and strong batch consistency.

Which application is growing the fastest?

Beverages are projected to expand at 9.19% CAGR through 2031, supported by functional drinks, reformulated soft drinks, and more specialized flavor demand.

Page last updated on: